Sample Category Title

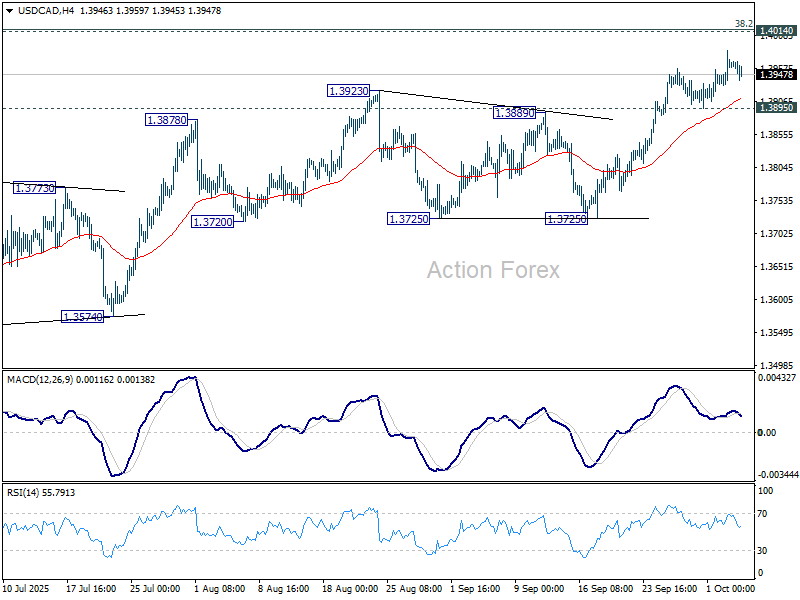

USD/CAD Weekly Outlook

USD/CAD's corrective rise from 1.3538 continued week. Initial bias stays mildly on the upside this week for 1.4014 cluster. But strong resistance should be seen there to complete the corrective rally. On the downside, below 1.3895 support will turn bias back to the downside for 1.3725. However, sustained break of 1.4014 will carry larger bullish implications.

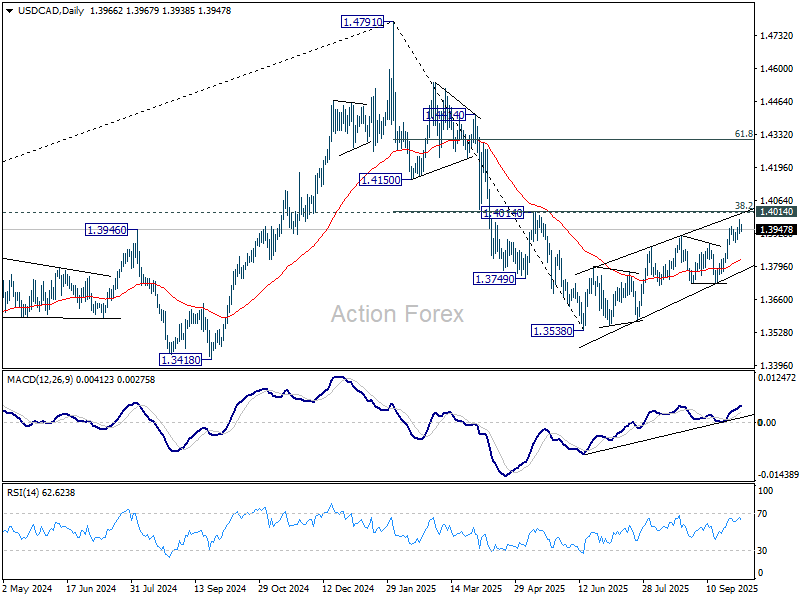

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

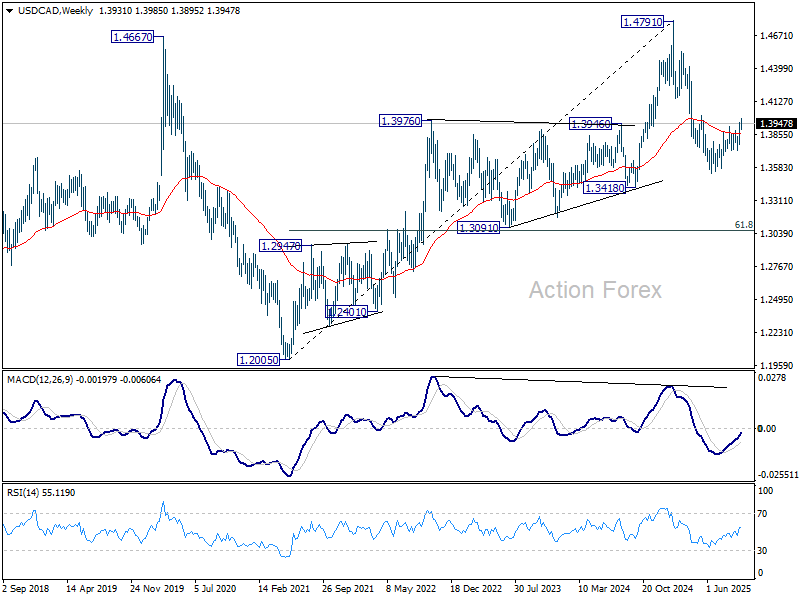

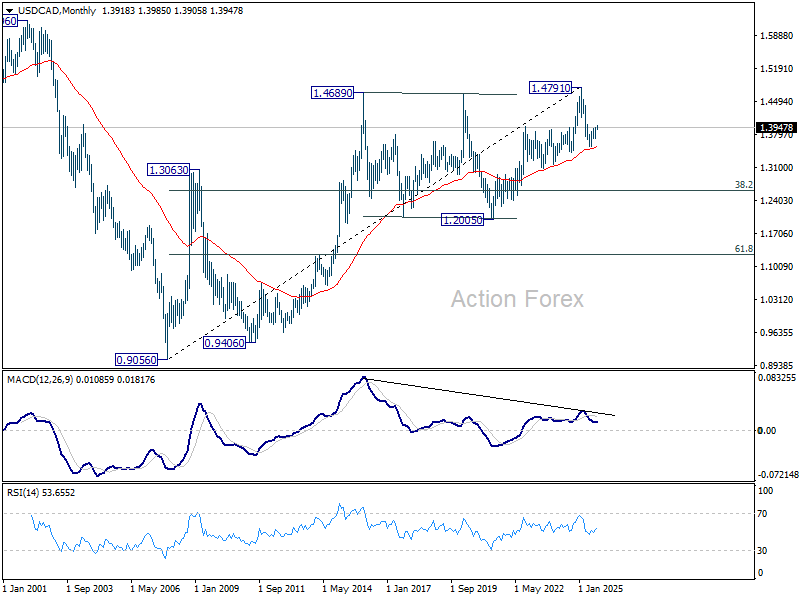

In the long term picture, considering bearish divergence condition in M MACD, up trend from 0.9506 (2027 low) might have completed with five waves up to 1.4791. Sustained trading below 55 M EMA (now at 1.3525) will solidify this case and bring deeper medium term fall to 38.2% retracement of 0.9056 to 1.4791 at 1.2600, even as a correction. Nevertheless, strong rebound from the 55 E MEA will retain bullishness for up trend resumption through 1.4791 later.

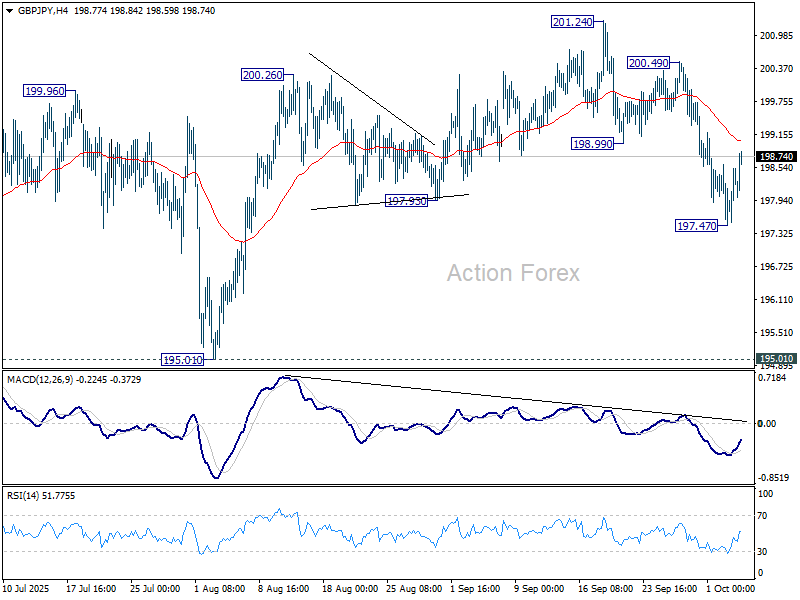

GBP/JPY Weekly Outlook

GBP/JPY's fall from 201.24 extended lower last week but recovered after hitting 197.47. Initial bias remains neutral this week first, but risk will stay on the downside as long as 200.49 resistance holds. Below 197.47 will target 195.01 structural support. Firm break there will indicate that rise fro 184.35 has completed, and possibly the pattern from 180.00 too. Near term outlook will then turn bearish.

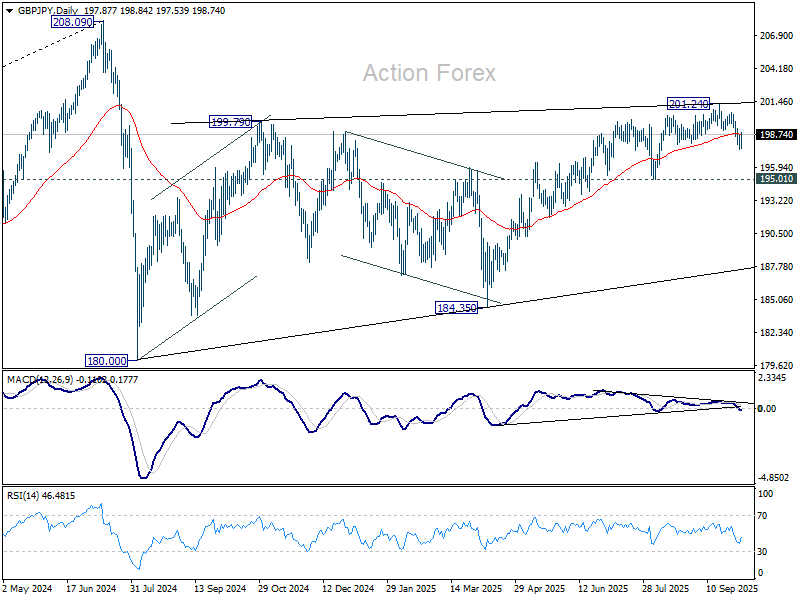

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

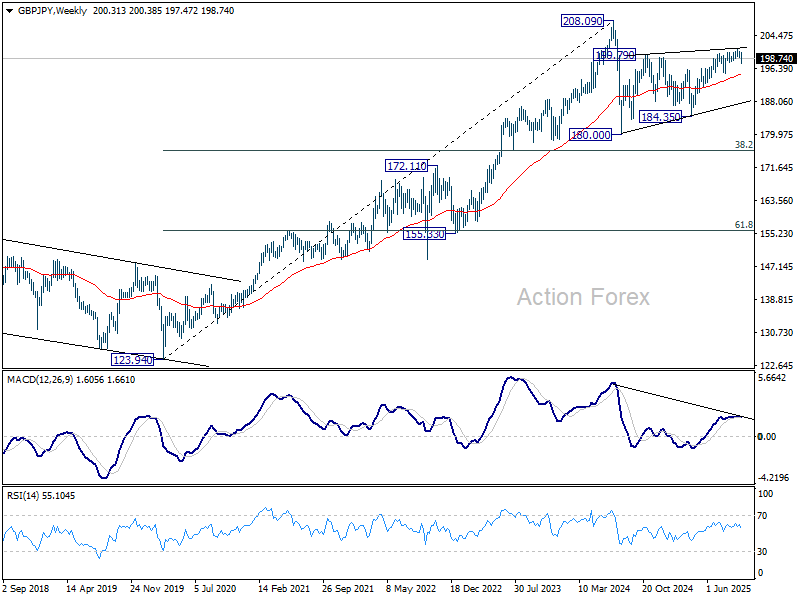

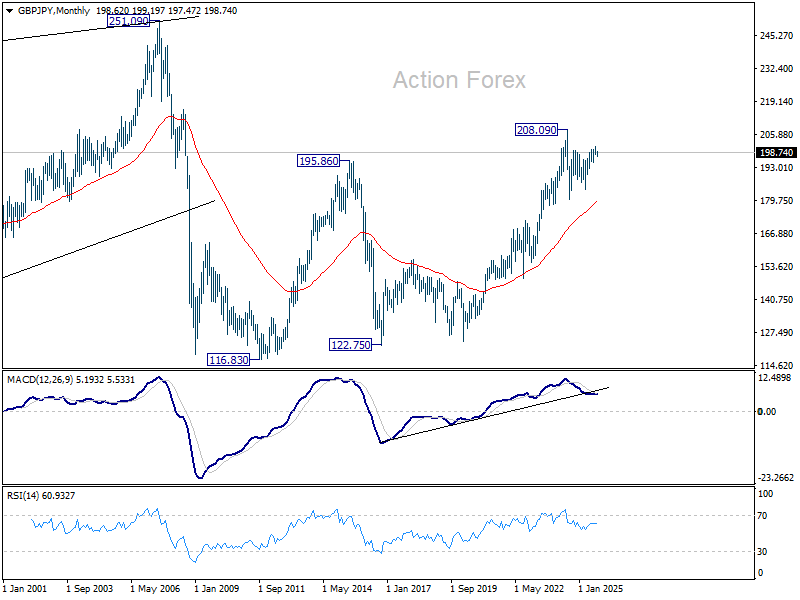

In the long term picture, there is no sign that the long term up trend from 122.75 (2016 low) has concluded. But firm break of 208.09 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

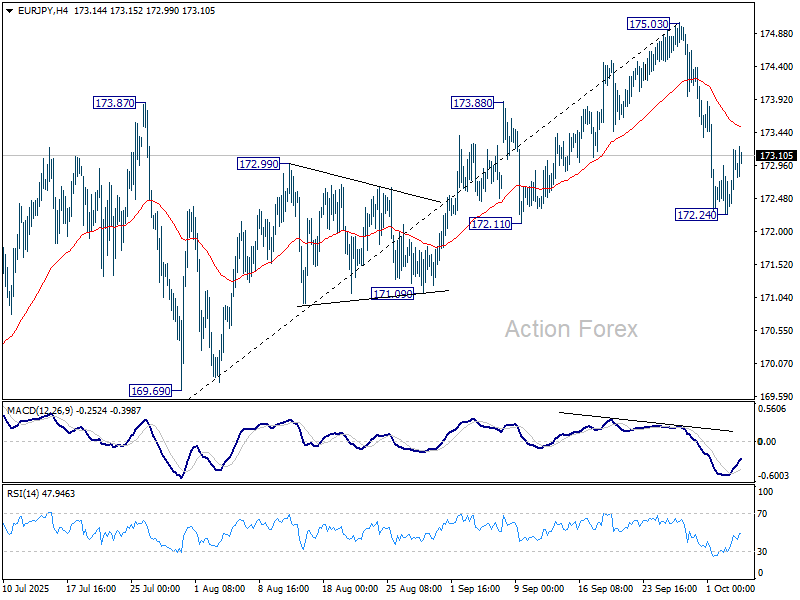

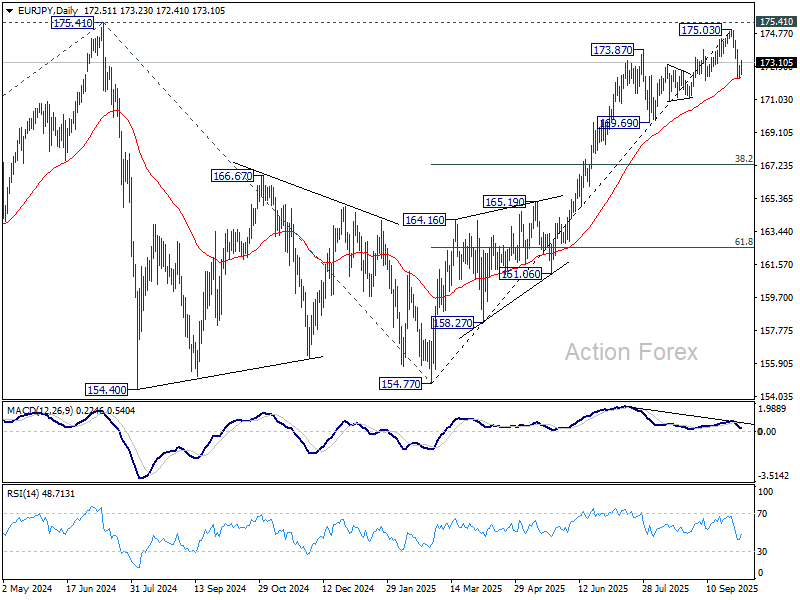

EUR/JPY Weekly Outlook

EUR/JPY's steep pullback last week confirmed short term topping at 175.03, just ahead of 175.41 high. But the cross then recovered after hitting 55 D EMA (now at 172.25). Initial bias remains neutral this week, with risk staying on the downside as long as 175.03 resistance holds. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA will indicate that whole five-wave rise from 154.77 has completed. Deeper decline should then be seen to 169.69 support next, and possibly to 38.2% retracement from 154.77 to 175.03 at 167.29.

In the bigger picture, rise from 154.77 is seen as resuming the larger up trend from 114.42 (2020 low). While initial set back could be seen as it tests 175.41 (2024 high), outlook will stay bullish as long as 55 W EMA (now at 166.48) holds. However, sustained break of the 55 W EMA will dampen this bullish case, and bring deeper fall back to 154.77 to extend the pattern from 175.41.

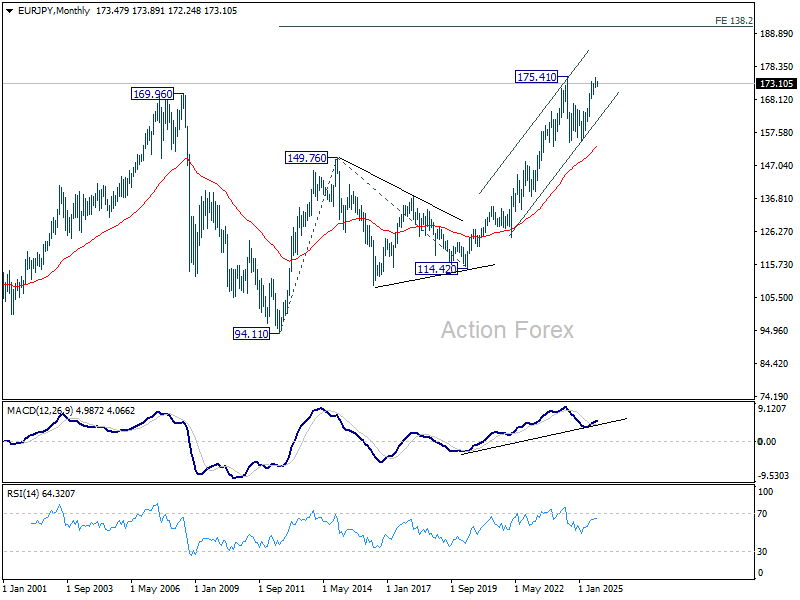

In the long term picture, up trend from 94.11 (2021 low) is still in progress. On resumption, next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

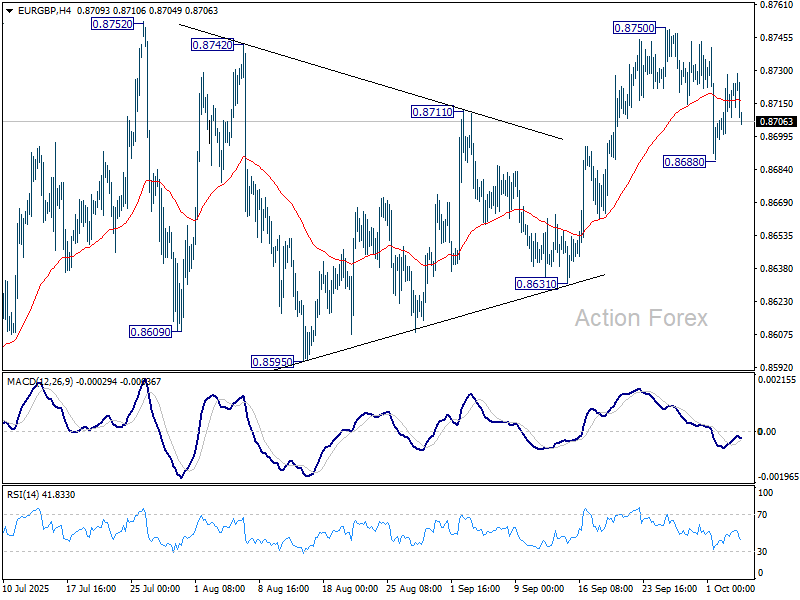

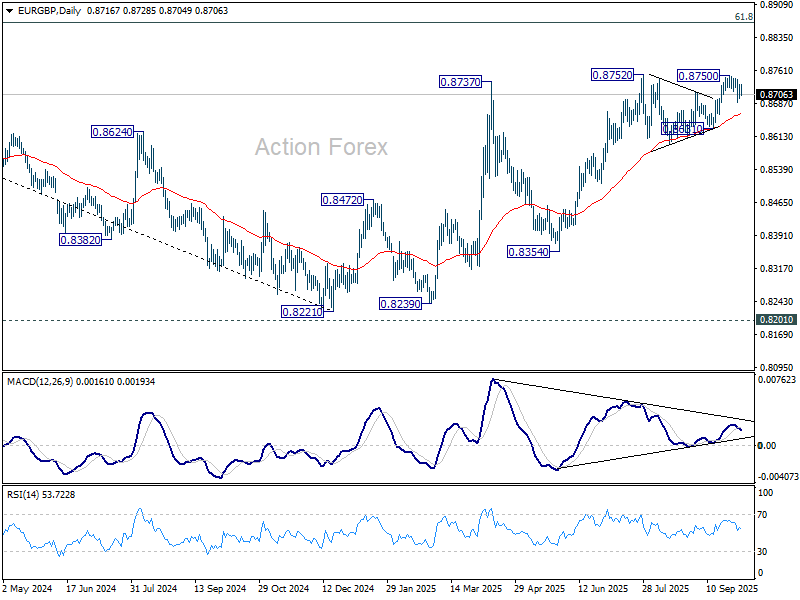

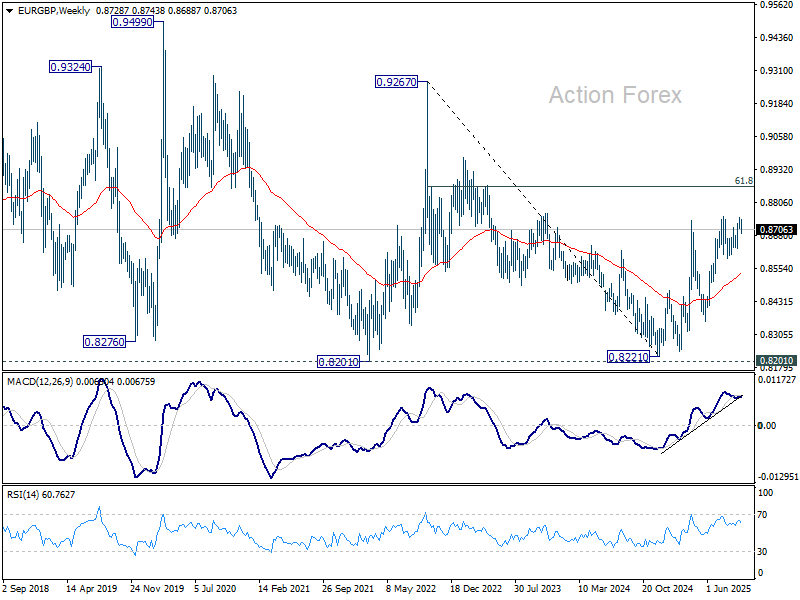

EUR/GBP Weekly Outlook

EUR/GBP stayed in consolidations below 0.8750 last week and outlook is unchanged. Initial bias stays neutral this week first. On the downside, break of 0.8688 will extend the fall to 0.8631 support. Decisive break there will indicate near term bearish reversal. On the upside, though, above 0.8750 will resume the larger rally towards 0.8867 fibonacci level.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8631 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8539) will confirm, and bring retest of 0.8221 low.

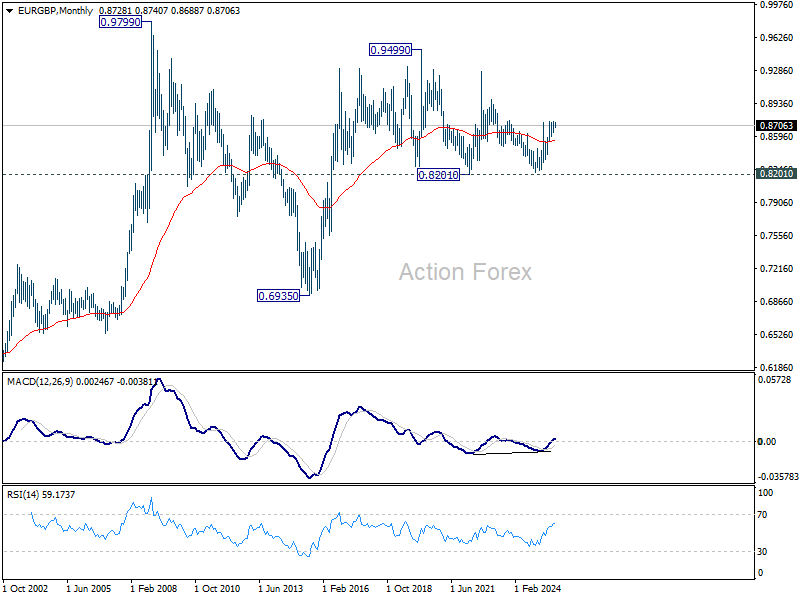

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

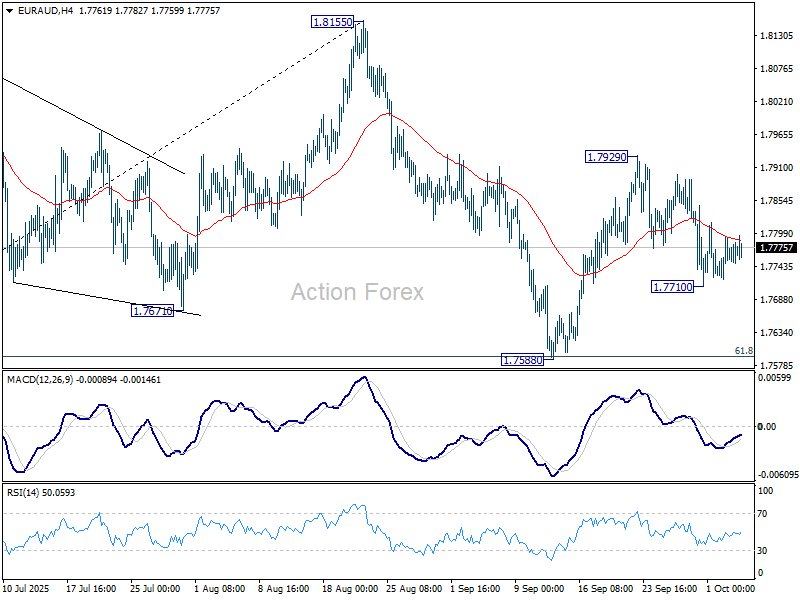

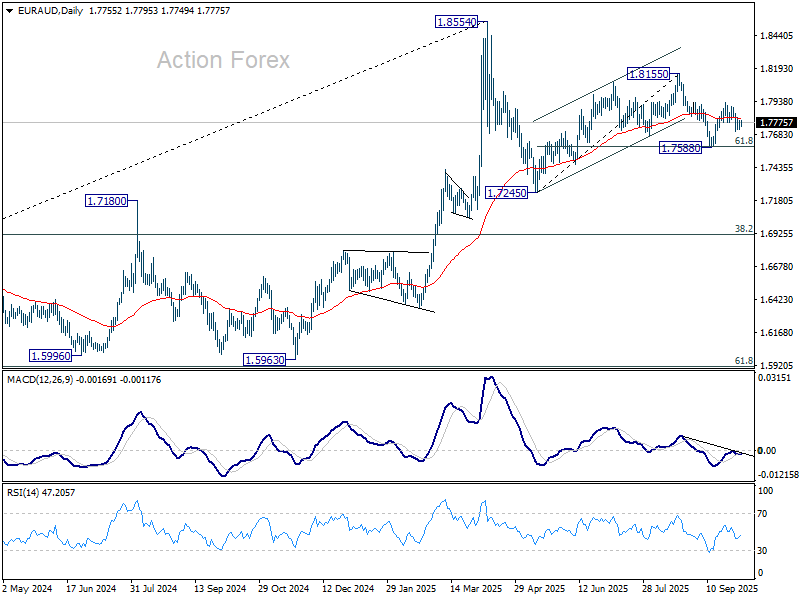

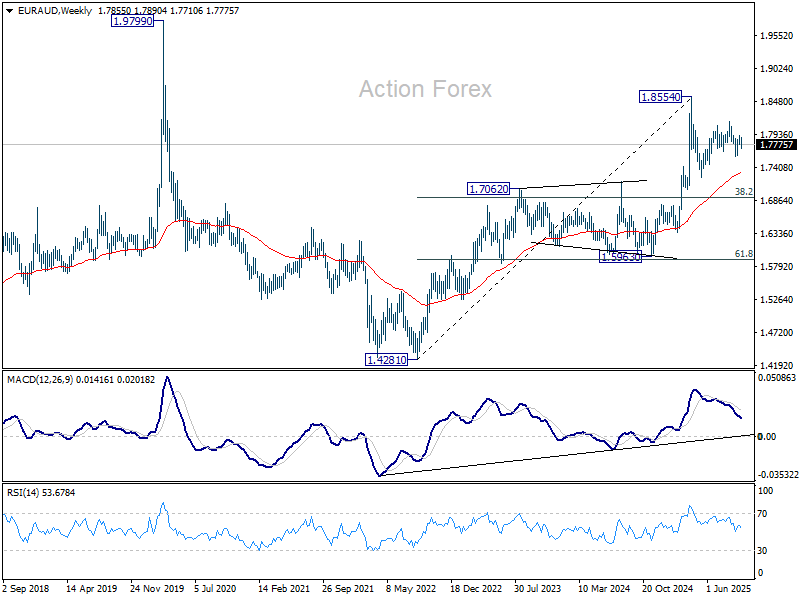

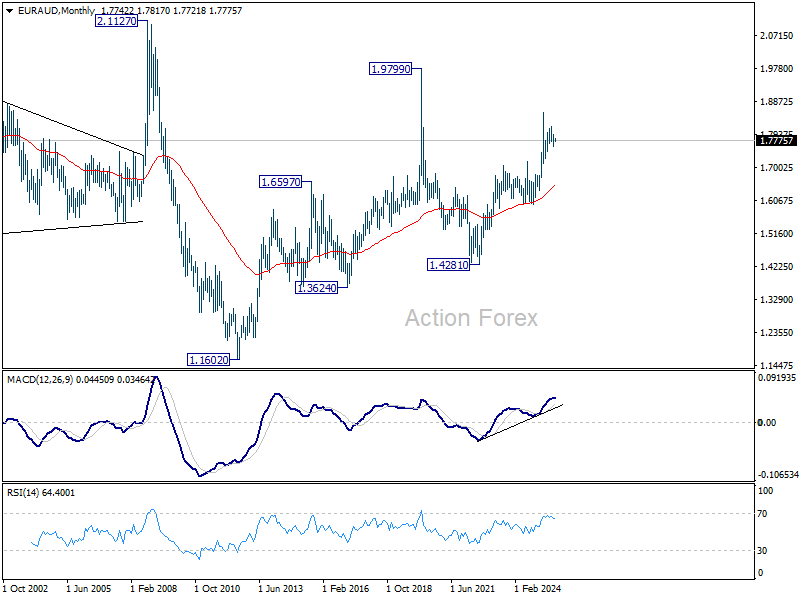

EUR/AUD Weekly Outlook

EUR/AUD gyrated lower last week but downside was contained well above 1.7588 support. Initial bias remains neutral this week first. On the upside, break of 1.7929 will resume the rebound from 1.7588 to retest 1.8155 high. On the downside, however, sustained break of 61.8% retracement of 1.7245 to 1.8155 at 1.7593 will bring deeper fall to 1.7245 resistance, as part of the corrective pattern from 1.8554 high.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6506) holds, this second leg could still extend higher.

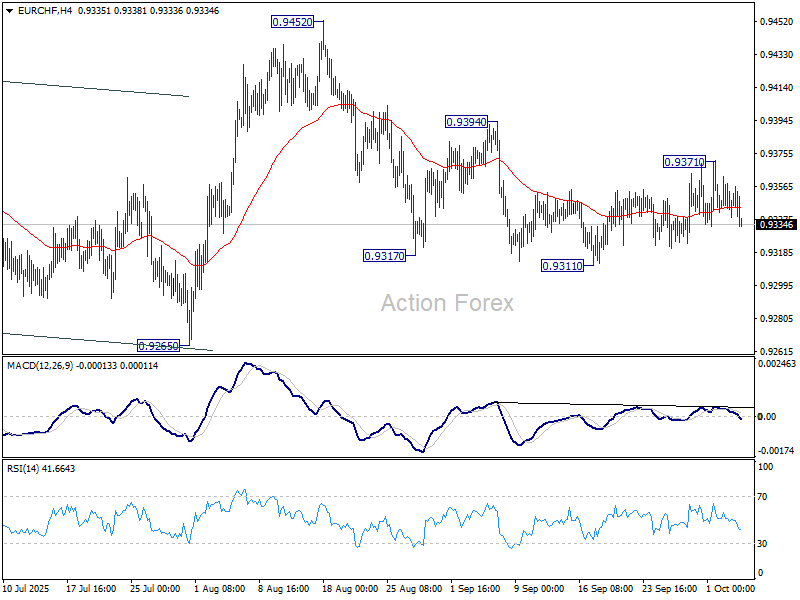

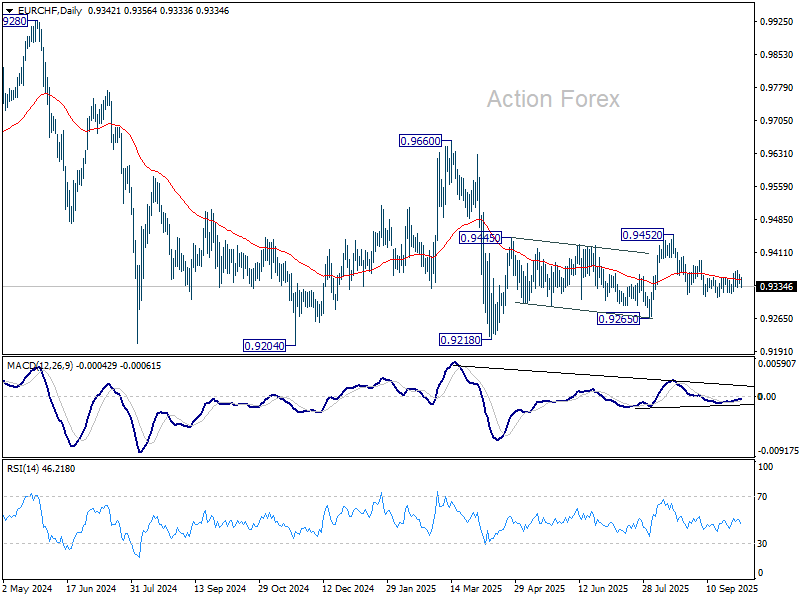

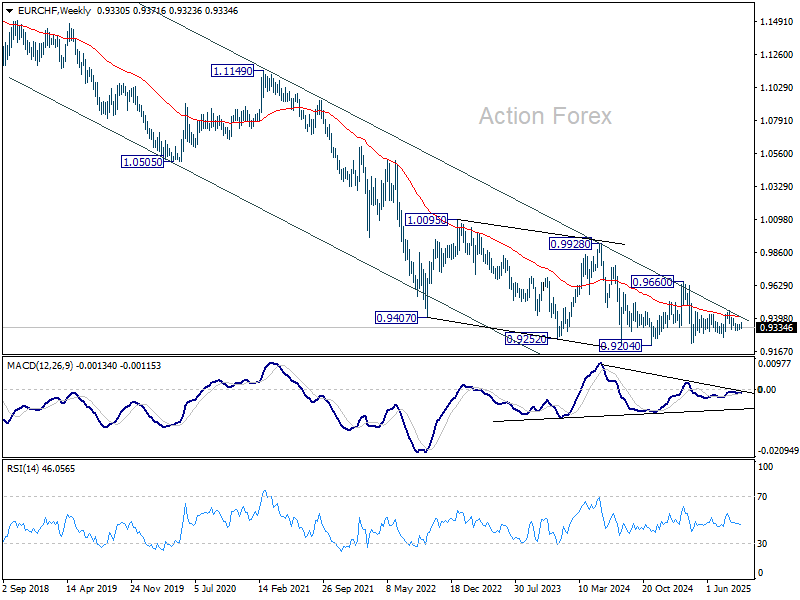

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9371 last week but retreated back into established range. Initial bias remains neutral this week first. As price actions from 0.9311 are corrective looking, fall from 0.9452 is likely still in progress. On the downside, break of 0.9311 will target 0.9265 support next. For now, risk will stay on the downside as long as 0.9394 resistance holds, in case of another recovery.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

In the long term picture, overall long term down trend is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9820) holds.

Markets Weekly Outlook – Navigating the US Shutdown & Global Trends as Equity Markets Continue to Soar

Week in review

A week that seemed like it might be a busy one from a data perspective did not deliver. Markets were braced for US jobs numbers and the NFP report which never arrived after the US congress failed to agree on funding.

This led to a Government shutdown, something which occurred during the first Trump administration as well.

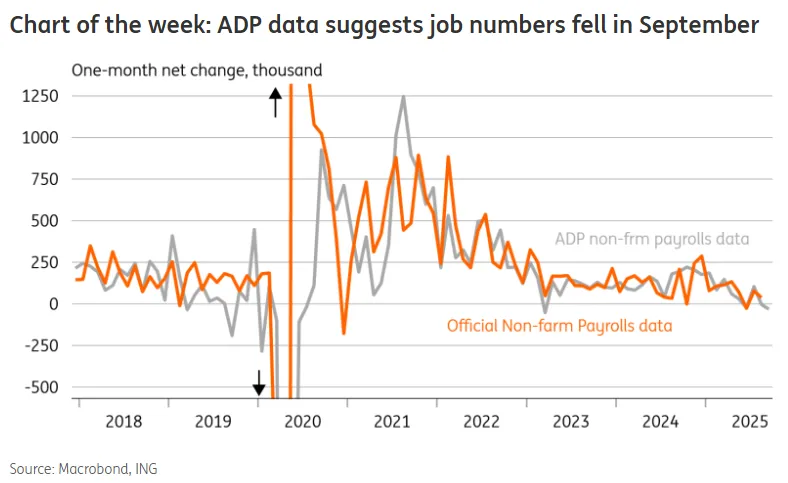

Since the official government jobs report was delayed, some people turned to the ADP employment estimate instead, a report that measures only private-sector jobs.

This report, which is sometimes unreliable compared to the official data, was quite negative this week. It showed that the US private sector lost 32,000 jobs in September.

Source: Macrobond, ING

As things stand markets continue to fully price in a rate cut at the Fed's October meetings with a December rate cut also priced in at around a 90% probability.

The current government shutdown and the resulting lack of new economic data probably won't change this long-term debate. As long as the shutdown doesn't last for an extremely long time, the affected government workers will receive all their missed pay, meaning there should be very little permanent damage to the economy.

The only uncertainty is whether the threats of widespread layoffs will actually happen.

So How did the Markets Perform?

On Friday, the major Wall Street stock indexes hit new record highs during the trading day. This continued strong rally is notable because it's happening even as the federal government shutdown enters its third day, making the economic outlook unclear due to missing data.

The positive mood in the market is being helped by excitement over Artificial Intelligence (AI), and investors seem unconcerned since markets have generally ignored shutdowns in the past.

According to the most recent survey of individual investors (AAII):

- Bullish sentiment (the belief that stocks will rise) increased to 42.9%. This is above its historical average for the third time in nine weeks, showing growing optimism.

- Bearish sentiment (the expectation that stocks will fall) remained unchanged and has been above its historical average for almost all of the past 35 weeks, indicating lingering caution.

- Neutral sentiment (the belief that stocks will stay the same) fell to 17.9%. This number has been well below its long-term average for over a year, meaning very few investors currently believe the market will simply remain flat.

US Indices were all on course for another week of gains. The Nasdaq 100 is on course for gains of around 1.20%, the Dow Jones is up 0.94% and the S&P 500 is eyeing gains of 1.16%.

In Europe and Asia the story was similar as they tracked gains from Wall Street. The STOXX 600 is set for its biggest weekly jump since April.The IBEX was ending the week strong, trading up around 0.98% on Friday.

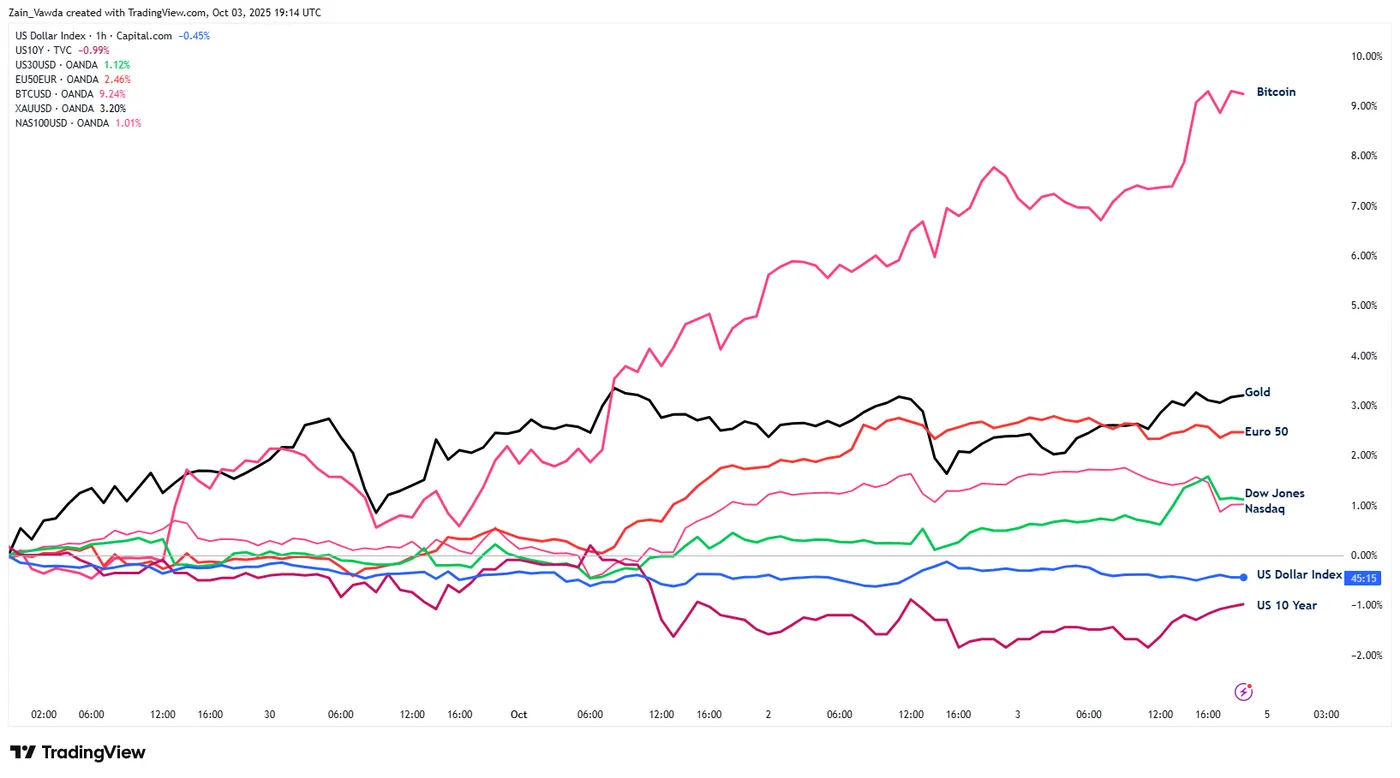

Cross Asset Performance for the Week

Source: TradingView

How has the US Dollar Reacted?

The US dollar pulled back on Friday and is expected to finish the week with losses against several major currencies. Leading this trend, the euro rose 0.2% against the dollar to $1.1739, putting it on track for its best weekly performance in a month.

This strength in the euro caused the overall dollar index (which tracks the dollar's value against key currencies) to drop 0.1% to 97.72, setting it up for its worst weekly result since July.

The dollar also weakened against the Swiss franc, falling 0.3% and heading for its biggest weekly drop since mid-August.

Similarly, the dollar slid against the British pound, which rose 0.3% and is poised for its largest weekly gain since August. The dollar's decline accelerated after new data showed that the US services sector growth stalled in September due to a sharp drop in new business.

Meanwhile, the Japanese yen pulled back from the strong gains it made earlier in the week as traders looked ahead to a major political election this weekend and tried to predict the next move by the Bank of Japan.

In commodity markets, gold prices rose and stayed near their record highs, on track for their seventh straight weekly gain.

Finally, oil prices rose on Friday but are still heading for a large weekly loss of 7% or more, following reports that OPEC+ might increase its supply.

The Week Ahead

Next week is a quiet week from a data perspective and may be welcomed by market participants.

Obviously the US shutdown is not ideal, but after a busy few weeks of data releases and with earnings season around the corner, market participants may welcome some calm before a potential storm in Q4.

Let us take a look at what may move markets from a data perspective next week.

Asia Pacific Markets

Since Chinese markets are currently closed for the long Golden Week holidays (they won't reopen until next Thursday), the usual economic reports on inflation and trade will be delayed by a week.

Therefore, the main focus for now will be on reports detailing how much people traveled and spent money during the holiday period. It is also possible that the data on China's total new loans and credit (aggregate financing) could be released later in the week.

It is a quiet week in Japan with a speech by Governor Ueda the main highlight after the elections this weekend.

Attention will turn to the Reserve Bank of New Zealand rate decision on Wednesday. Markets are expecting the Reserve Bank of New Zealand (RBNZ) will lower its interest rate by 0.25% on October 8th, which is what most experts and market pricing currently expect.

US Government Shut Down, Euro Area & bData

The main issue next week is the government shutdown in the U.S. Depending on how long it lasts, market participants might not receive many official economic reports. Even if an agreement is reached soon, it will take time to get workers back and release schedules back on track. Reports that could be delayed next week include the trade balance, weekly jobless claims, and inventory numbers.

Despite this, the Federal Reserve (Fed) will still release the minutes from its September meeting (on Wednesday), where they cut rates by 25 basis points. We will also get the August consumer credit data and the initial October consumer sentiment index from the University of Michigan.

Consumer spending is currently stable, but confidence has already fallen sharply this year due to a weaker job market and worries about how tariffs are driving up prices. With millions of federal workers facing missed paychecks or permanent layoffs due to the shutdown, it is unlikely that consumer confidence will improve.

A quiet week for the Euro Area and the UK as well from a data perspective. The EU will release retail sales before we get a speech by ECB President Christine Lagarde.

In the UK the main highlight of the week comes from a speech by Bank of England (BoE) Governor Bailey.

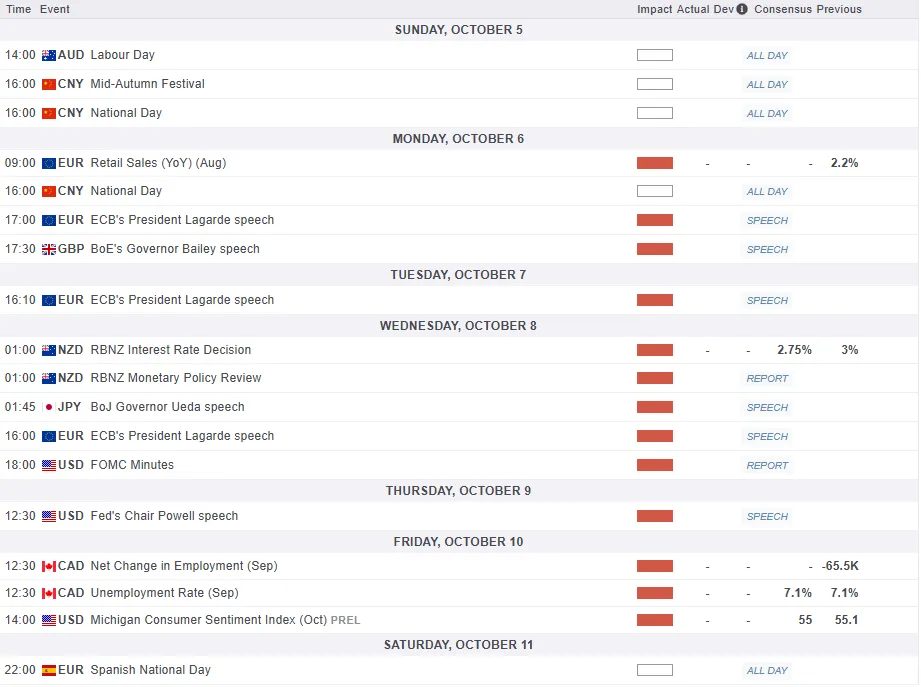

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index (DXY)

This week's Chart of the week is the US Dollar Index (DXY)

From a technical perspective, the DXY continues to hug on to a key area of support around the 97.70 handle.

Any attempt to push higher by DXY bulls is facing a challenge with the 100-day MA resting at the 98.19 handle. A move beyond that handle may find resistance at 99.58 before the psychological pivot level at 100.00 comes back into the discussion.

A move lower may find support at the swing low around the 97.20 handle before the 96.90 and YTD low 96.37 handles come into focus.

US Dollar Index (DXY) Daily Chart - October 3, 2025

Source:TradingView.Com (click to enlarge)

Safe Trades.

The Weekly Bottom Line: Shutdown Throws a Curveball at the Fed

Canadian Highlights

- Canadian equity markets continued their ascent this week, although bond yields and oil prices sent a somewhat weaker signal about economic growth prospects.

- Canadian job markets have softened, which should downwardly pressure consumption moving forward. The Bank of Canada will be no doubt be closely watching the September Labour Force Survey report out next week.

- Markets are assigning a roughly 60% chance of a BoC cut later this month. Given the weak economic backdrop and diminished inflation risks, we think the chance is much higher.

U.S. Highlights

- The U.S. government has shut down all “non-essential” services this week as Congress failed to pass a bill to fund government spending.

- In the absence of payrolls data, the ADP report took the center stage, and showed that private payrolls declined by 32,000 in September. August’s JOLTS report showed that businesses remained in low hire, low fire mode.

- The ISM manufacturing index rose slightly in September but remained in contractionary territory. Its services counterpart dropped sharply, narrowly avoiding slipping into contractionary territory.

Canada – Tough Times

The mood in Canadian financial markets was somewhat sour this week, except that the unrelenting bull run in equities continued. This is despite the U.S. government shutdown, and a fresh set of U.S. tariffs placed on lumber (10%) and kitchen cabinets, bathroom vanities, and upholstered furniture (25% each). Tariffs on the latter categories are unlikely to massively dent the Canadian economy, although if stacked on to existing duties, the lumber tariffs would yield a 45% import tax on Canadian lumber. President Trump has also pledged tariffs on branded pharmaceuticals and heavy trucks at a later time. Notably, PM Carney will meet with President Trump next week to discuss trade and other important issues.

Developments in other financial markets signaled some more concern about the economic outlook. The Canadian 10-year yield was down a few bps this week (as of writing), following its U.S. counterpart lower amid the government shutdown. Meanwhile, oil prices traded near multi-month lows, weighed down by both demand and supply worries.

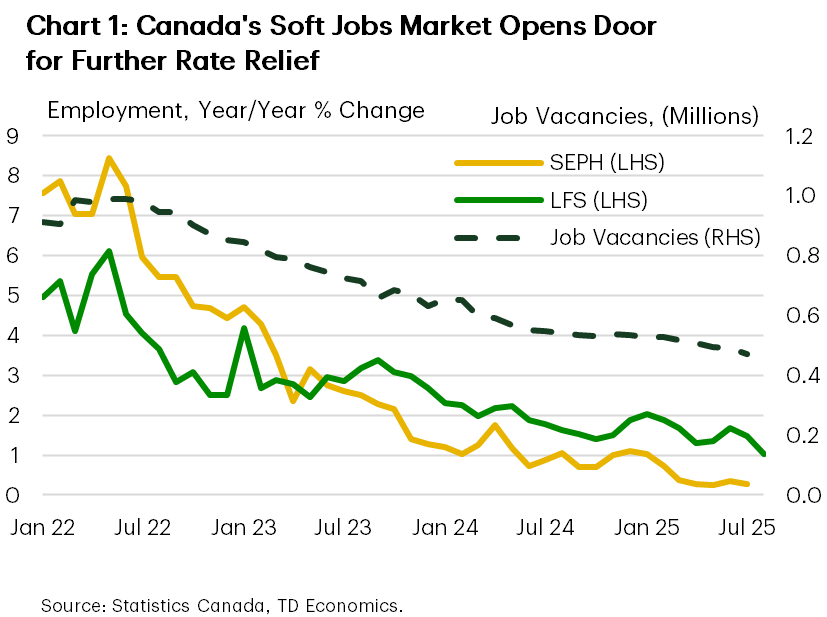

There is reason to be apprehensive about Canada’s economic backdrop, with troubling signs aplenty in the jobs market (Chart 1). There were no major data releases this week (although preliminary housing data signalled cooling sales growth in key markets last month). However, September’s Labour Force Survey (LFS) data is on tap for next week. So far, the LFS has painted an ugly picture of the current jobs market, with a cumulative 100k jobs lost in July and August. Part of this story is tied to demographics and labour supply, with rapidly slowing population growth reducing the labour force so far in the third quarter. And there’s a good chance this dynamic shows itself again next week. However, labour demand is also soft - evidenced by falling job vacancies - while wage growth is slowing and the unemployment rate is on the rise.

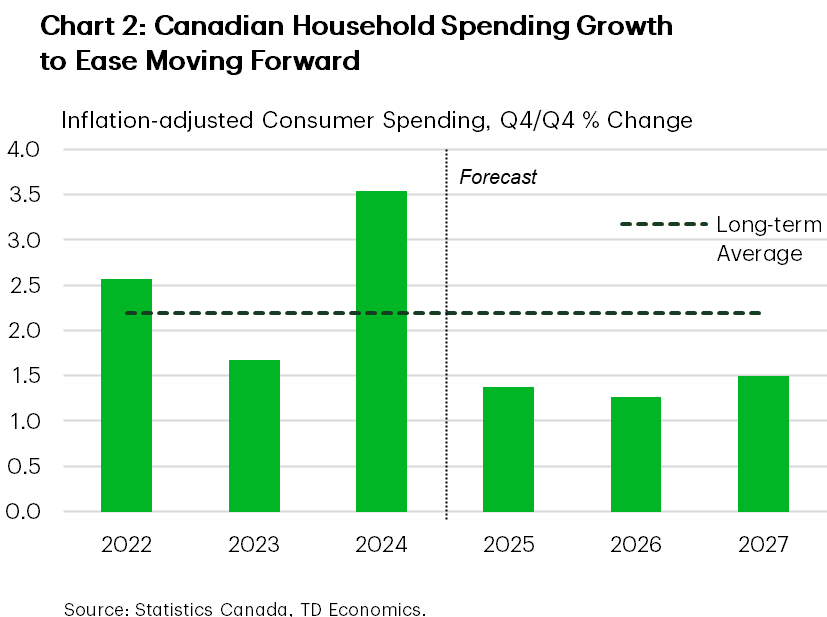

One way a slowing jobs market will impact the economy is through household spending (Chart 2). Consumer spending was surprisingly resilient in the first half of 2025, which we chalk up to past rate cuts, a rise in housing market activity, and travelers choosing to stay (and spend) in Canada instead of heading south of the border. However, we question the durability of this spending strength, given Canada’s slowing population growth and, crucially, it’s weakening jobs market. As such, we think Canadian consumption is likely to post sub-trend growth performances moving forward.

Policymakers are certainly aware of the downside risks to Canada’s economic growth. Minutes from the Bank of Canada’s deliberations ahead of their September rate cut were released this week. And, they were dotted with dovish statements, including the observation that upward momentum in core inflation had diminished, the labour market had softened, and most counter-tariffs on U.S. products had been removed (reducing Canadian inflation risk). As of now, markets see a 60% chance of a follow-up rate cut by the BoC this month. However, we think the BoC will pull the trigger given the weak economic backdrop.

U.S. – Shutdown Throws a Curveball at the Fed

On October 1st, the U.S. government shut down all “non-essential” services, as Congress failed to pass a bill necessary to fund government in the current fiscal year. Financial markets have shrugged off the shutdown so far, with equities ending the week higher, bond yields declining, and the U.S. dollar weakening only slightly. In past shutdowns in 2013 and 2018, equities and the USD declined modestly and recovered quickly, so the reaction this time is even more muted.

If this shutdown is brief, the markets may be right to discount it. Most lost output in previous shutdowns was eventually recovered. Studies show shutdowns reduce annualized quarterly real GDP growth by up to 0.1 percentage points for each week. However, negative effects increase non-linearly the longer the shutdown lasts as disruptions accumulate.

The lack of updated official economic data is another casualty of the shutdown. September’s payrolls release has been postponed. A prolonged shutdown may delay other key indicators like the Consumer Price Index (CPI). A lack of official data complicates decision-making for the Fed. For now, the Fed will have to rely on private and internal data sources. Earlier this week, Chicago Fed President Goolsbee (who is a voting member of the FOMC) echoed that, but also acknowledged that it worries him “that we wouldn’t be getting official statistics at exactly a moment when we’re trying to figure out is the economy in transition.”

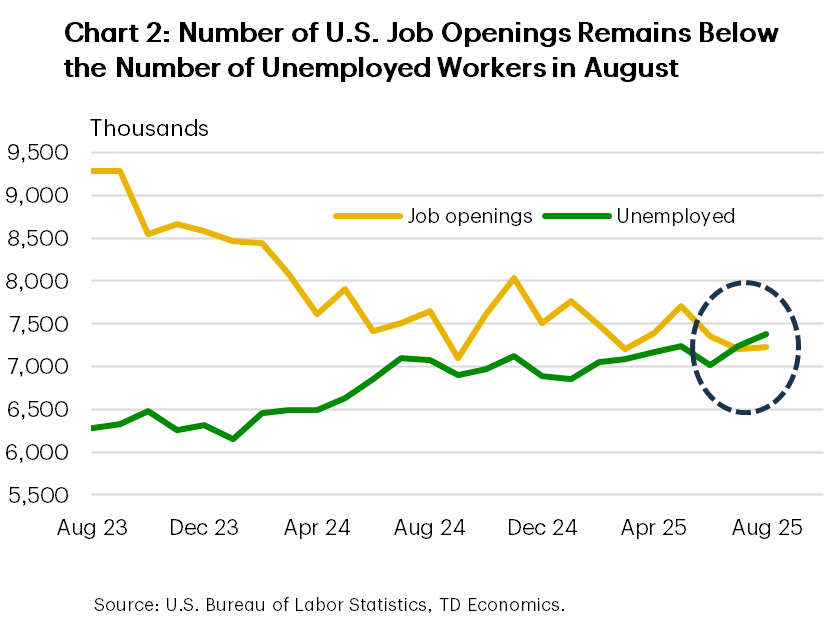

Without official payrolls data, employment surveys—such as ADP and JOLTS—filled the gap. The ADP report showed continued weakness in job growth in September, with private payrolls declining by 32,000. Though ADP data can be volatile, recent trends show greater alignment with payroll figures through 2025, especially on a three-month moving average (Chart 1). The August JOLTS report, released before the shutdown, also showed a hiring drought, with job openings below the number of unemployed for a second consecutive month (Chart 2). Although job opportunities were scarce, layoffs have remained subdued. Employers seem to be in “low hire, low fire” mode, supporting stability in the unemployment rate and helping to cushion consumer spending for now.

In terms of economic growth, ISM indexes pointed to slowing momentum in September, with businesses increasingly citing the growing impact of tariffs on their bottom lines. The ISM manufacturing index edged higher, but remained in contractionary territory, with only 5 out of 18 industries reporting growth. Activity moderated in the services sector, with the ISM non-manufacturing index declining to 50.0 from 52.0, narrowly avoiding slipping into contraction. Details were disappointing: new orders and business activity moderated, prices rose and the employment subcomponent remained in contractionary territory. While limited, this week’s data continues to support the case for additional monetary stimulus from the Fed, with another rate cut in October being nearly priced in by markets.

Weekly Economic & Financial Commentary: Shutdown Showdown

Summary

United States: Employment Friday That Wasn't

- The first Friday of the month has come, but since the U.S. federal government is shut down, it didn't bring with it the latest read on the jobs market. The manufacturing and services sector purchasing manager surveys suggest activity held up at the end of the third quarter, but underlying conditions remain uneasy.

- Next week: Trade Balance (Tue.), Consumer Credit (Tue.)

International: Mix of Economic Data from Advanced and Emerging Economies

- This week saw a range of international economic data releases. On the policy front, the Reserve Bank of Australia held its Cash Rate steady at 3.60%. In the Eurozone, inflation ticked higher but remained broadly in line with expectations. Across Asia, Japan’s Q3 Tankan survey reflected broadly favorable trends, while China’s PMI readings were more mixed but still suggested modest overall improvement.

- Next week: Japan Labor Cash Earnings (Wed.), RBNZ Policy Rate (Wed.), Norway CPI (Fri.)

Topic of the Week: Shutdown Showdown

- Fiscal year 2026 began on Wednesday, Oct. 1 with a government shutdown. The economic and financial market impact of a 1-2 week government shutdown should be modest, but a longer shutdown would be more painful, and the indefinite delay of key economic data clouds the near-term outlook for U.S. monetary policy.

Summary 10/6 – 10/10

Monday, Oct 6, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | TD-MI Inflation Gauge M/M Sep | -0.30% | |

| 05:45 | CHF | Unemployment Rate M/M Sep | 2.90% | 2.90% |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Oct | -7.7 | -9.2 |

| 08:30 | GBP | Construction PMI Sep | 46.3 | 45.5 |

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | 0.10% | -0.50% |

| 23:30 | AUD | Westpac Consumer Confidence Oct | -3.10% | |

| 23:30 | JPY | Overall Household Spending Y/Y Aug | 1.20% | 1.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | TD-MI Inflation Gauge M/M Sep | |

| Forecast: | Previous: -0.30% | ||

| 05:45 | CHF | Unemployment Rate M/M Sep | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Oct | |

| Forecast: -7.7 | Previous: -9.2 | ||

| 08:30 | GBP | Construction PMI Sep | |

| Forecast: 46.3 | Previous: 45.5 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | |

| Forecast: 0.10% | Previous: -0.50% | ||

| 23:30 | AUD | Westpac Consumer Confidence Oct | |

| Forecast: | Previous: -3.10% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Aug | |

| Forecast: 1.20% | Previous: 1.40% | ||

Tuesday, Oct 7, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Aug P | 107.2 | 106.1 |

| 06:00 | EUR | Germany Factory Orders M/M Aug | 1.20% | -2.90% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | 715B | |

| 12:30 | CAD | Trade Balance (CAD) Aug | -5.7B | -4.9B |

| 12:30 | USD | Trade Balance (USD) Aug | -61.0B | -78.3B |

| 14:00 | CAD | Ivey PMI Sep | 51.2 | 50.1 |

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | 2.80% | 4.10% |

| 23:50 | JPY | Current Account (JPY) Aug | 2.24T | 1.88T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Aug P | |

| Forecast: 107.2 | Previous: 106.1 | ||

| 06:00 | EUR | Germany Factory Orders M/M Aug | |

| Forecast: 1.20% | Previous: -2.90% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | |

| Forecast: | Previous: 715B | ||

| 12:30 | CAD | Trade Balance (CAD) Aug | |

| Forecast: -5.7B | Previous: -4.9B | ||

| 12:30 | USD | Trade Balance (USD) Aug | |

| Forecast: -61.0B | Previous: -78.3B | ||

| 14:00 | CAD | Ivey PMI Sep | |

| Forecast: 51.2 | Previous: 50.1 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | |

| Forecast: 2.80% | Previous: 4.10% | ||

| 23:50 | JPY | Current Account (JPY) Aug | |

| Forecast: 2.24T | Previous: 1.88T | ||

Wednesday, Oct 8, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | RBNZ Interest Rate Decision | 2.75% | 3.00% |

| 05:00 | JPY | Eco Watchers Survey: Current Sep | 47.1 | 46.7 |

| 06:00 | EUR | Germany Industrial Production M/M Aug | -1.00% | 1.30% |

| 14:30 | USD | Crude Oil Inventories (Oct 3) | 1.8M | |

| 18:00 | USD | FOMC Minutes | ||

| 23:01 | GBP | RICS Housing Price Balance Sep | -17% | -19% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | RBNZ Interest Rate Decision | |

| Forecast: 2.75% | Previous: 3.00% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Sep | |

| Forecast: 47.1 | Previous: 46.7 | ||

| 06:00 | EUR | Germany Industrial Production M/M Aug | |

| Forecast: -1.00% | Previous: 1.30% | ||

| 14:30 | USD | Crude Oil Inventories (Oct 3) | |

| Forecast: | Previous: 1.8M | ||

| 18:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

| 23:01 | GBP | RICS Housing Price Balance Sep | |

| Forecast: -17% | Previous: -19% | ||

Thursday, Oct 9, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Oct | 4.70% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Sep P | 8.10% | |

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | 15.3B | 14.7B |

| 11:30 | EUR | ECB Meeting Accounts | ||

| 12:30 | USD | Initial Jobless Claims (Oct 3) | 223K | 218K |

| 14:00 | USD | Wholele Inventories Aug F | -0.20% | -0.20% |

| 14:30 | USD | Natural Gas Storage (Oct 3) | 53B | |

| 21:30 | NZD | Business NZ PMI Sep | 49.9 | |

| 23:50 | JPY | Bank Lending Y/Y Sep | 3.70% | 3.60% |

| 23:50 | JPY | PPI Y/Y Sep | 2.50% | 2.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Oct | |

| Forecast: | Previous: 4.70% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Sep P | |

| Forecast: | Previous: 8.10% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | |

| Forecast: 15.3B | Previous: 14.7B | ||

| 11:30 | EUR | ECB Meeting Accounts | |

| Forecast: | Previous: | ||

| 12:30 | USD | Initial Jobless Claims (Oct 3) | |

| Forecast: 223K | Previous: 218K | ||

| 14:00 | USD | Wholele Inventories Aug F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 14:30 | USD | Natural Gas Storage (Oct 3) | |

| Forecast: | Previous: 53B | ||

| 21:30 | NZD | Business NZ PMI Sep | |

| Forecast: | Previous: 49.9 | ||

| 23:50 | JPY | Bank Lending Y/Y Sep | |

| Forecast: 3.70% | Previous: 3.60% | ||

| 23:50 | JPY | PPI Y/Y Sep | |

| Forecast: 2.50% | Previous: 2.70% | ||

Friday, Oct 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 12:30 | CAD | Net Change in Employment Sep | 5.0K | -65.5K |

| 12:30 | CAD | Unemployment Rate Sep | 7.10% | 7.10% |

| 14:00 | USD | UoM Consumer Sentiment Oct P | 55 | 55.1 |

| 14:00 | USD | UoM 1-Yr Inflation Expectations Oct P | 4.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 12:30 | CAD | Net Change in Employment Sep | |

| Forecast: 5.0K | Previous: -65.5K | ||

| 12:30 | CAD | Unemployment Rate Sep | |

| Forecast: 7.10% | Previous: 7.10% | ||

| 14:00 | USD | UoM Consumer Sentiment Oct P | |

| Forecast: 55 | Previous: 55.1 | ||

| 14:00 | USD | UoM 1-Yr Inflation Expectations Oct P | |

| Forecast: | Previous: 4.70% | ||