Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3508; (P) 1.3534; (R1) 1.3556; More...

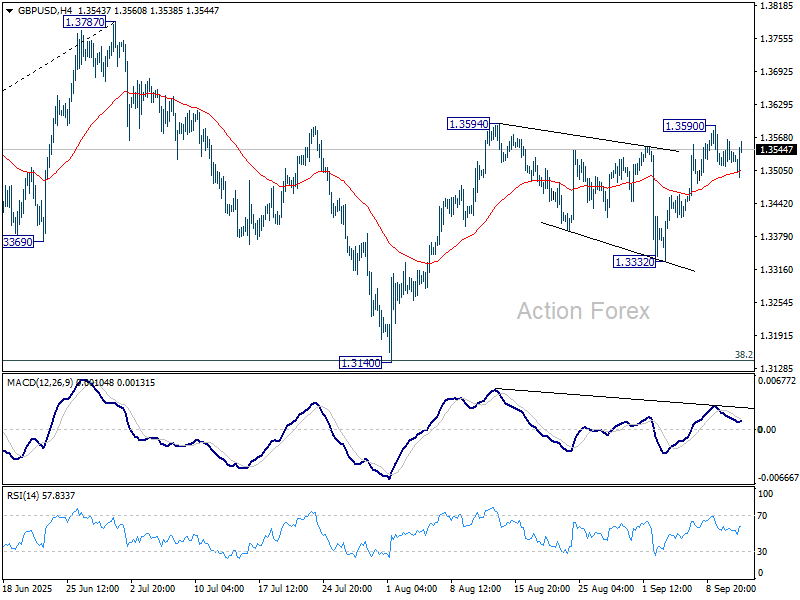

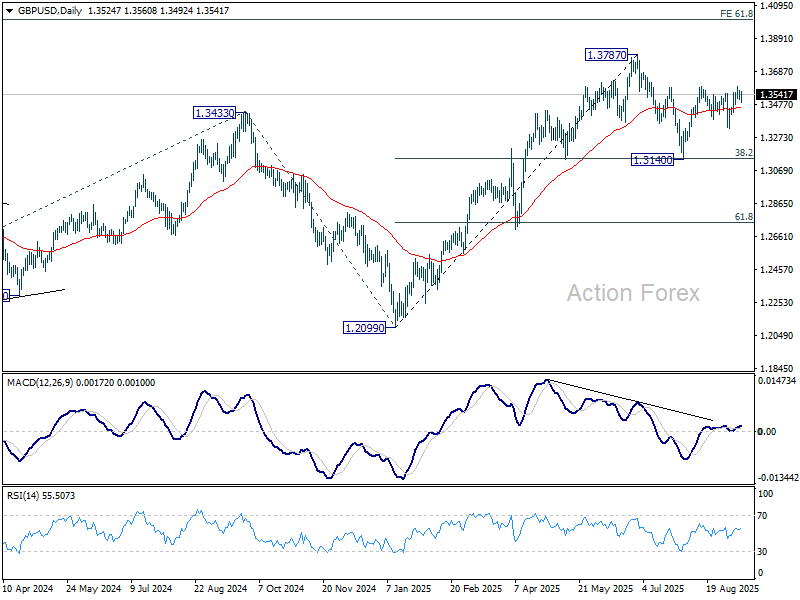

GBP/USD is staying in consolidations below 1.3590 temporary top and intraday bias stays neutral. Further rise is expected with 1.3332 support intact. Firm break of 1.3594 will resume the rally from 1.3140 and target a retest on 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

US: Inflationary Pressures Show Further Signs of Heating Up in August

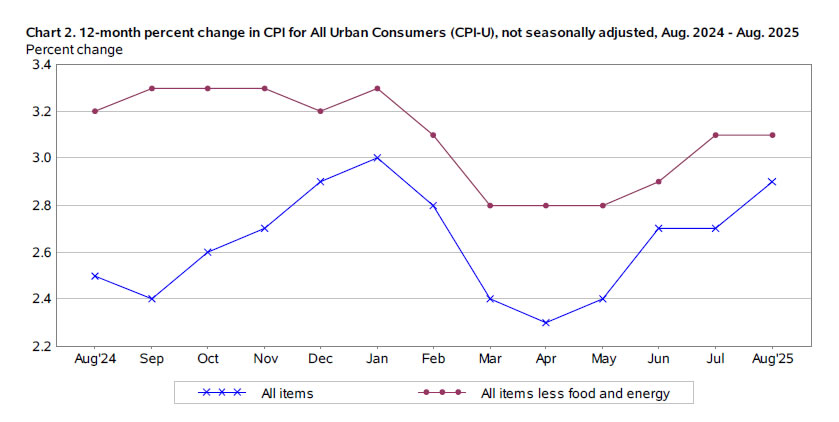

The Consumer Price Index (CPI) rose 0.4% month-on-month (m/m) in August, a tick ahead of the consensus forecast in Bloomberg and up from the 0.2% m/m gain in July. On a twelve-month basis, CPI was up 2.9% (from 2.7% the month prior).

- Energy costs (+0.7% m/m) turned higher last month, while food prices (+0.5% m/m) also firmed due to higher grocery costs (+0.6% m/m). Price growth for 'food away from home' was up 0.3%m/m - unchanged from July.

Excluding food and energy, core inflation rose 0.3% m/m (0.35% m/m unrounded), largely matching last month's gain and meeting the consensus forecast. The twelve-month change held steady at 3.1%.

Price growth of services continued to come in on the hotter side, rising 0.35% m/m, following a similar gain of 0.36% m/m in July. Primary shelter costs rose at its fastest monthly clip in several months, while price growth of non-housing services (+0.4% m/m) remained firm for a second consecutive month.

- Higher travel costs (+3.0% m/m) were a big driver of price growth in non-housing services, thanks to a sharp uptick in airfares (+5.9% m/m) and hotels (+2.3% m/m).

Tariff passthrough continued to materialize in core goods prices, which were up 0.3% m/m or its fastest monthly gain since January. Price gains were most notable in apparel (+0.5% m/m), appliances (+0.5% m/m), household furniture and bedding (+0.4% m/m) and new vehicle prices (+0.3% m/m). Used vehicle prices also rose 1.0% m/m, which could in part be driven by consumer switching to used models in an effort avoid paying tariff costs.

Key Implications

Inflationary pressures continued to heat up in August, with broad strength in goods and services inflation. Goods prices are likely to continue to drift higher over the coming months as businesses increasingly pass-on more of the tariff costs. However, further upward pressure on services inflation looks limited against the backdrop of a cooling labor market which is likely to limit upward pressure on wage growth and keep a lid on discretionary services spending.

But nothing is a guarantee, and policymakers will need to balance the risks of reducing the policy rate by enough to breathe some life back into the labor market, but not by so much that they risk unnecessarily stoking inflation. We see the Fed delivering on three quarter-point cuts by year-end, with the first coming at next week's meeting. We've long held this view, and following this morning's release, Fed futures are pricing in a similar rate-cut path by year-end.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1703; (R1) 1.1722; More...

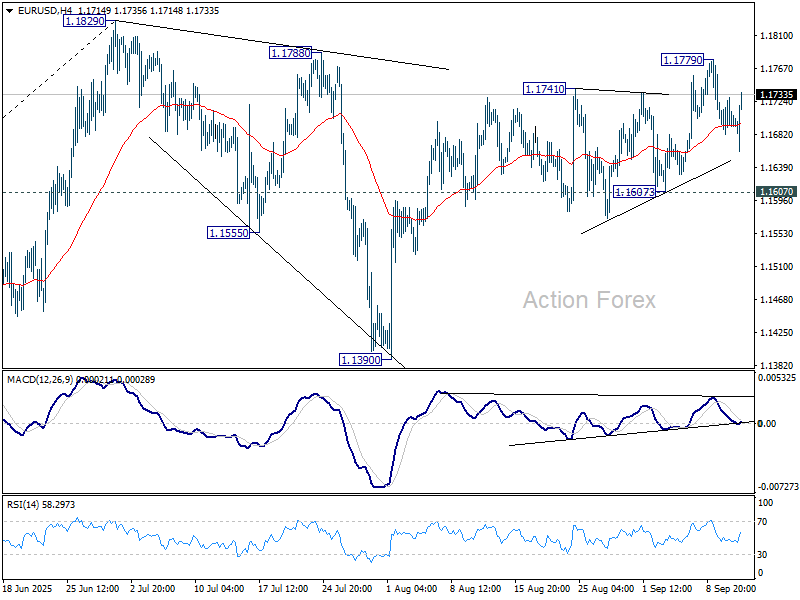

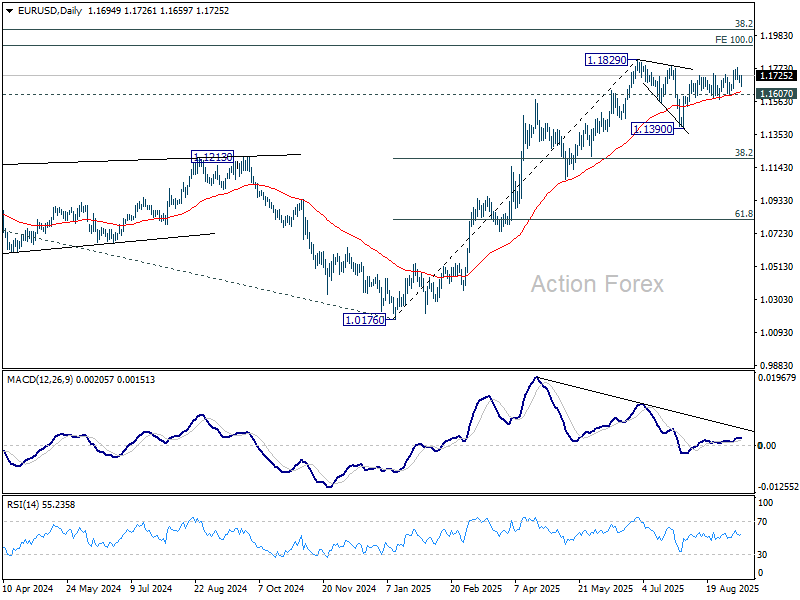

EUR/USD is staying in range below 1.1779 temporary top despite today's volatility. Intraday bias remains neutral for the moment. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

ECB and US CPI Underwhelm, Jobless Claims Take Spotlight

Today’s high-profile events turned out to be something of a letdown for traders. Euro dipped after the ECB held its deposit rate steady at 2.00% and published new staff projections, but the move was shallow and short-lived. Markets took note that both headline and core inflation are now projected slightly below the 2% target by 2026 and 2027, hinting at a possible need for further easing down the road.

For now, however, there is no urgency for additional cuts. ECB reiterated the Governing Council’s commitment to a data-dependent stance, and unless incoming figures deteriorate notably, traders see little chance of a near-term move. That kept the euro relatively stable after its initial dip.

In the U.S., CPI data were broadly in line with expectations. Headline inflation’s 0.4% monthly rise was a touch stronger than forecast, but the annual rate of 2.9% and steady core at 3.1% highlights that inflation is not worsening much under tariff pressures.

The bigger surprise came from the weekly jobless claims report. Initial claims jumped to 263k, the highest since 2021, showing a clear softening in the U.S. labor market. With employment one half of the Fed’s dual mandate, the data reinforced expectations that policymakers will have to expedite easing to cushion the economy.

Market pricing for next week’s FOMC remains anchored to a 25bps cut, with odds for a larger 50bps move still low at about 10%. But expectations for a consecutive cut in October have surged to around 95%, showing traders are becoming more convinced of back-to-back easing.

Despite the data, currency markets remain locked in yesterday's ranges. Swiss Franc, Euro, and Sterling are modestly firmer, while Yen and Loonie are weaker alongside Kiwi. Dollar and Aussie sit in the middle of the pack. For now, the highly anticipated breakout in FX markets has yet to materialize.

In Europe, at the time of writing, FTSE is up 0.37%. DAX is up 0.08%. CAC is up 0.67%. UK 10-year yield is down -0.008 at 4.625. Germany 10-year yield is down -0.006 at 2.650. Earlier in Asia, Nikkei rose 1.22%. Hong Kong HSI fell -0.43%. China Shanghai SSE rose 1.65%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.01 to 1.578.

US CPI rises to 2.9% in August, core CPI unchanged at 3.1%

U.S. consumer prices rose more than expected on the month in August, with CPI up 0.4% mom versus forecasts of 0.3% mom. Core CPI rose 0.3% mom, matching expectations. Shelter costs climbed 0.4% mom and were the largest contributor to the monthly increase, while food prices rose 0.5% mom and energy gained 0.7% mom.

On a year-over-year basis, headline CPI accelerated to 2.9% from 2.7% in July, in line with forecasts. Core inflation held steady at 3.1%, also as expected. The data show underlying price pressures remain stable even as headline measures edge higher. Food inflation rose 3.2% over the past year, while energy prices were up a modest 0.2%. Overall, the report points to steady but not accelerating inflation.

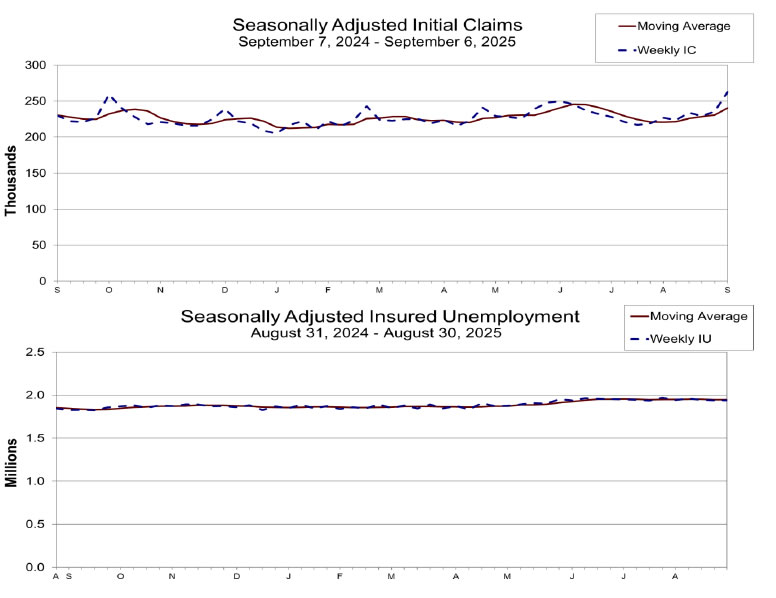

US initial jobless claims spike to 263k, highest since 2021

U.S. initial jobless claims surged by 27k to 263k in the week ending September 6, well above expectations of 240k and marking the highest level since October 2021. The four-week moving average rose 10k to 241k, pointing to a clear softening trend in labor market conditions.

Continuing claims were steady at 1.939 million for the week ending August 30, with the four-week average slipping slightly to 1.936 million. Still, the rise in new claims highlights a labor market that is starting to cool more decisively, adding pressure on the Fed as it weighs the pace of policy easing.

ECB holds at 2.00% Again, upgrades 2025 growth outlook

The ECB left its deposit rate unchanged at 2.00% as widely expected, marking a second consecutive hold. The Governing Council reiterated its commitment to stabilizing inflation at 2% over the medium term and stressed a "data-dependent and meeting-by-meeting" approach. Policymakers emphasized they are "not pre-committing to a particular rate path", leaving flexibility to respond to incoming data.

Fresh staff projections showed little change from June, with headline inflation expected to average 2.1% (prior 2.0%) in 2025, 1.7% (1.6) in 2026, and 1.9% (2.0%) in 2027.

Core inflation, excluding food and energy, is projected at 2.4% in 2025 before easing to 1.9% in 2026 and 1.8% in 2027. The figures reinforce the view that price pressures are gradually converging toward target.

On growth, the ECB revised up its 2025 forecast to 1.2% from 0.9%, but cut its 2026 estimate slightly to 1.0% (prior 1.1%). The 2027 projection was left unchanged at 1.3%.

Japan CGPI accelerates to 2.7% yoy, import price declines ease

Japan’s producer prices rose modestly in August, with CGPI climbing 2.7% yoy from 2.5% yoy in July, matching market forecasts. The pickup was driven mainly by food and beverage costs, which rose 5.0% yoy versus 4.7% yoy previously. In contrast, utility bills fell -2.9% yoy due to government subsidies, softening the overall inflation impact.

Import price declines eased significantly in the past two months, with yen-based import prices down -3.9% yoy compared with a revised -10.3% fall in July. The data suggest external cost pressures are stabilizing, even as domestic food inflation remains sticky.

RBNZ’s Hawkesby: OCR seen at 2.5% by year-end, data dependent

RBNZ Governor Christian Hawkesby said today the central bank still projects the Official Cash Rate to fall to around 2.50% by year-end, down from current 3.00%. Though, the pace could be "faster or slower" depending on incoming data. He emphasized that the path of policy easing will hinge on the "speed of New Zealand’s economic recovery".

Hawkesby noted the August Monetary Policy Statement highlighted the sharp blow to household and business confidence, with the economy stalling mid-year and creating more slack. He attributed much of the “confidence shock” to uncertainty over U.S. tariff policies, compounded by cost-of-living pressures and a weak housing market.

Still, leading indicators for July were “better” and aligned with the RBNZ’s outlook for a rebound in the second half of the year. Hawkesby said policymakers will keep monitoring spillovers from U.S. tariffs on both global growth and New Zealand firms. The RBNZ resumed rate cuts last month after a July pause.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1703; (R1) 1.1722; More...

EUR/USD is staying in range below 1.1779 temporary top despite today's volatility. Intraday bias remains neutral for the moment. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

US initial jobless claims spike to 263k, highest since 2021

U.S. initial jobless claims surged by 27k to 263k in the week ending September 6, well above expectations of 240k and marking the highest level since October 2021. The four-week moving average rose 10k to 241k, pointing to a clear softening trend in labor market conditions.

Continuing claims were steady at 1.939 million for the week ending August 30, with the four-week average slipping slightly to 1.936 million. Still, the rise in new claims highlights a labor market that is starting to cool more decisively, adding pressure on the Fed as it weighs the pace of policy easing.

US CPI rises to 2.9% in August, core CPI unchanged at 3.1%

U.S. consumer prices rose more than expected on the month in August, with CPI up 0.4% mom versus forecasts of 0.3% mom. Core CPI rose 0.3% mom, matching expectations. Shelter costs climbed 0.4% mom and were the largest contributor to the monthly increase, while food prices rose 0.5% mom and energy gained 0.7% mom.

On a year-over-year basis, headline CPI accelerated to 2.9% from 2.7% in July, in line with forecasts. Core inflation held steady at 3.1%, also as expected. The data show underlying price pressures remain stable even as headline measures edge higher. Food inflation rose 3.2% over the past year, while energy prices were up a modest 0.2%. Overall, the report points to steady but not accelerating inflation.

ECB holds at 2.00% Again, upgrades 2025 growth outlook

The ECB left its deposit rate unchanged at 2.00% as widely expected, marking a second consecutive hold. The Governing Council reiterated its commitment to stabilizing inflation at 2% over the medium term and stressed a "data-dependent and meeting-by-meeting" approach. Policymakers emphasized they are "not pre-committing to a particular rate path", leaving flexibility to respond to incoming data.

Fresh staff projections showed little change from June, with headline inflation expected to average 2.1% (prior 2.0%) in 2025, 1.7% (1.6) in 2026, and 1.9% (2.0%) in 2027.

Core inflation, excluding food and energy, is projected at 2.4% in 2025 before easing to 1.9% in 2026 and 1.8% in 2027. The figures reinforce the view that price pressures are gradually converging toward target.

On growth, the ECB revised up its 2025 forecast to 1.2% from 0.9%, but cut its 2026 estimate slightly to 1.0% (prior 1.1%). The 2027 projection was left unchanged at 1.3%.

(ECB) Monetary policy decisions

11 September 2025

The Governing Council today decided to keep the three key ECB interest rates unchanged. Inflation is currently at around the 2% medium-term target and the Governing Council’s assessment of the inflation outlook is broadly unchanged.

The new ECB staff projections present a picture of inflation similar to that projected in June. They see headline inflation averaging 2.1% in 2025, 1.7% in 2026 and 1.9% in 2027. For inflation excluding energy and food, they expect an average of 2.4% in 2025, 1.9% in 2026 and 1.8% in 2027. The economy is projected to grow by 1.2% in 2025, revised up from the 0.9% expected in June. The growth projection for 2026 is now slightly lower, at 1.0%, while the projection for 2027 is unchanged at 1.3%.

The Governing Council is determined to ensure that inflation stabilises at its 2% target in the medium term. It will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance. In particular, the Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook and the risks surrounding it, in light of the incoming economic and financial data, as well as the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Key ECB interest rates

The interest rates on the deposit facility, the main refinancing operations and the marginal lending facility will remain unchanged at 2.00%, 2.15% and 2.40% respectively.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP and PEPP portfolios are declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises at its 2% target in the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

Euro in Holding Pattern Ahead of ECB Decision, US CPI Next

The euro is virtually unchanged on Thursday, trading at 1.1692 in the European session.

ECB expected to maintain rates

The European Central Bank meets later on Thursday and the money markets have priced in a hold at close to 100%, which would keep the key deposit rate at 2.0%. The ECB has cut rates by more than half since last July but has hinted that there is no rush to continue lowering rates.

Has inflation in the eurozone become too much of a good thing? Inflation is under control, but there is now a risk of inflation undershooting the 2% target, which would put pressure on the ECB to respond by reducing rates.

There are differing opinions within the ECB with regard to the impact of the US tariffs. The hawks,, who are against more rate cuts argue that the economy has weathered the tariffs well. The doves, who favor more cuts, are concerned that the tariffs are yet to be fully felt and could dampen growth. The money markets are in agreement with the hawks and don't anticipate another rate cut this year.

All eyes on US CPI

The US releases the August inflation report later on Thursday. CPI is expected to rise to 2.7% y/y from 2.9% y/y in July. Monthly, the market estimate is 0.3%, compared to 0.2% in July. Core CPI is expected to remain unchanged at 3.1% y/y and 0.3% m/m.

The core rate is well above the Federal Reserve's 2% target but that isn't expected to stop the Fed from lowering rates next week for the first time since December 2024. Although a rate cut has been fully priced in, we could see downward pressure on the US dollar if the Fed cuts, especially if the Fed's tone at the meeting is dovish.

The US economy is showing signs of cooling, especially the labor market. The August nonfarm payrolls fell to 22 thousand and annual revisions for the year prior to March 2025 were revised downwards by a massive 911 thousand, much more than expected. The weak nonfarm payrolls report has raised the odds of a half-point cut to 10%, with a 90% chance of a quarter-point reduction.

EUR/USD Technical

- EURUSD tested resistance at 1.1703 earlier. Above, there is resistance at 1.1722.

- 1.1674 and 1.1655 are providing support

EURUSD 1-Day Chart, September 11, 2025

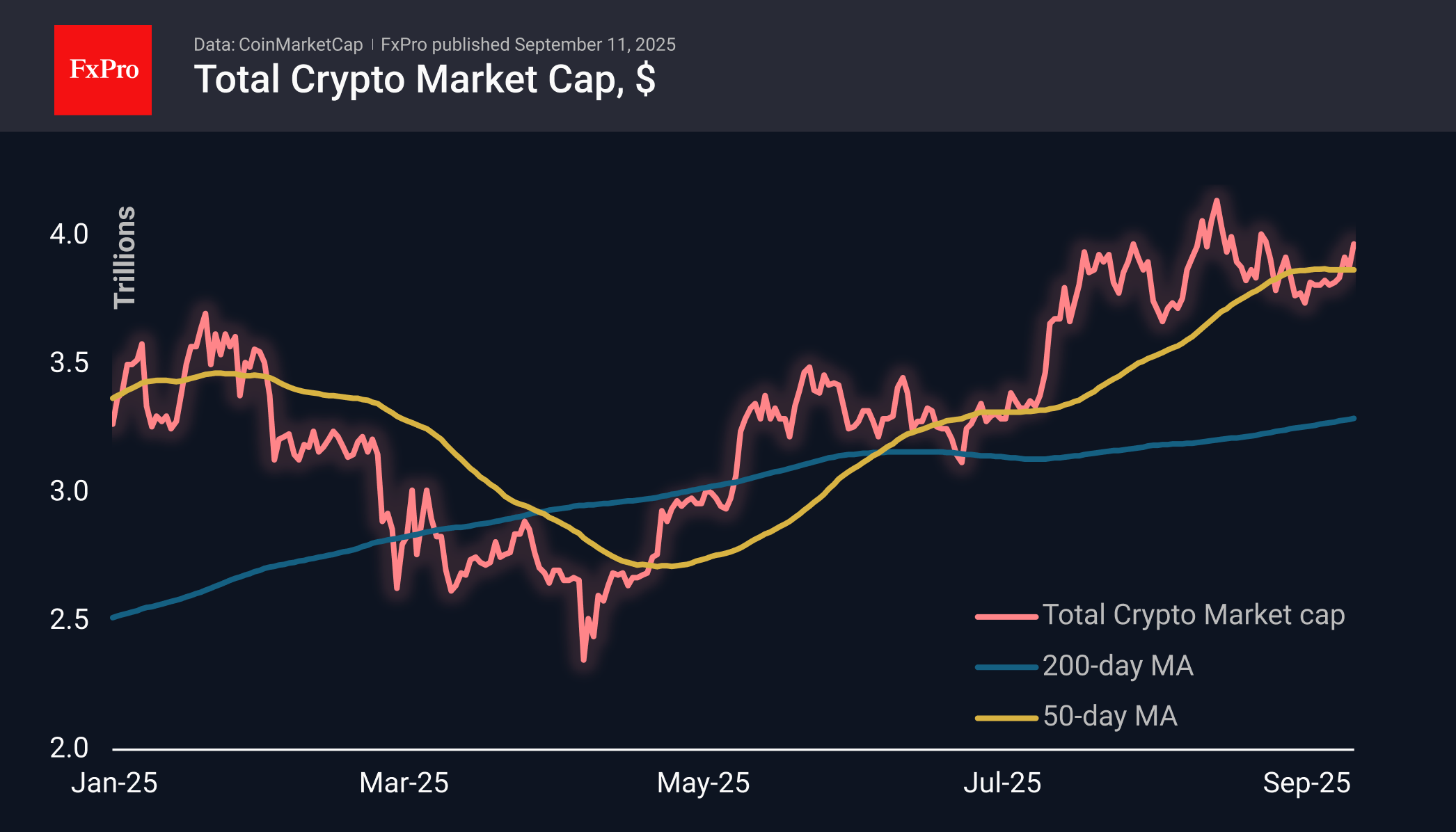

Crypto Market Has Returned to $4 Trillion Mark

Market Overview

Once again, the crypto market capitalisation has approached $4 trillion, rising by more than 2% over the past 24 hours. The whole market is managing to gain above the 50-day moving average, which the first cryptocurrency is unable to do. There are no super rallies or confetti like before, but these are still signs of an altcoin season with heavy altcoins leading the way.

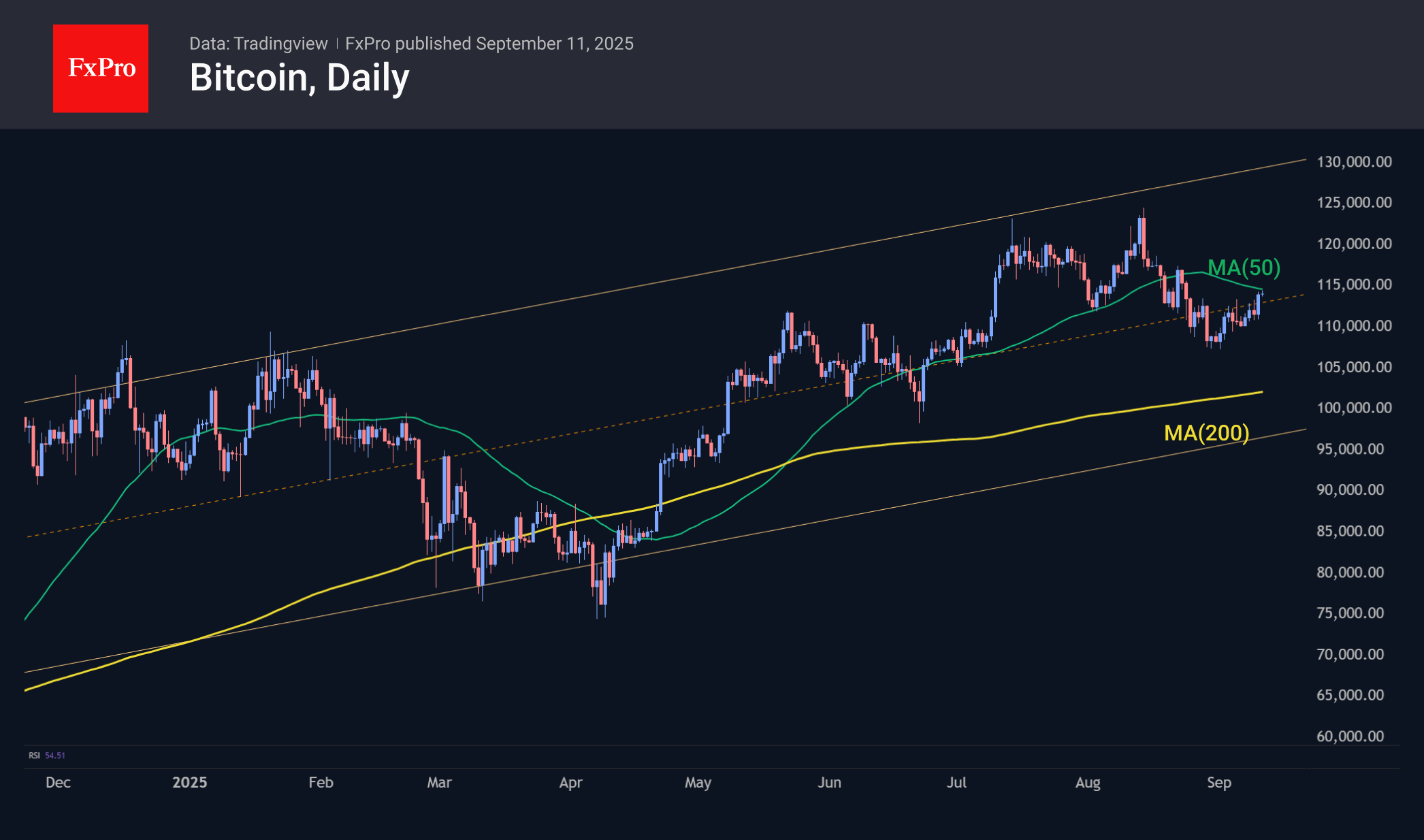

Bitcoin exceeded $114K on Wednesday for the first time in 2.5 weeks after the release of weak US producer price data. On Thursday, US consumer inflation data will be released, which could also influence interest rate decisions in the coming months, thereby affecting the markets. The BTC price has approached the 50-day moving average, and the upcoming data could provide momentum for both a breakout of this resistance and an end to the recent uptrend.

News Background

According to Santiment, traders have turned negative, expecting Bitcoin to fall to $100K, Ethereum to $3,500 and altcoins to pull back. As markets move contrary to crowd expectations, this pullback may not happen.

Japan’s Metaplanet will allocate $1.45 billion to buy Bitcoin this year. The company has completed its share offering, increasing the volume from 185 million to 385 million shares.

According to Bitwise, banks need to raise deposit rates to compete with increasingly popular stablecoins.

The Kyrgyz Parliament has approved a bill on ‘Virtual Assets,’ which provides for the creation of a state cryptocurrency reserve.

The Vietnamese authorities have approved the launch of a legalised cryptocurrency market in the country on a trial basis for the next five years.

Cardano founder Charles Hoskinson said the Ethereum ecosystem is doomed to collapse in the next 10-15 years due to a large number of fundamental flaws. Among the shortcomings of ETH are an inefficient virtual machine, an incorrect accounting model, and a flawed consensus system.