Sample Category Title

Sunset Market Commentary

Markets

Most markets were mired in technical trading today. Core bonds, at least up until now, are taking a breather after soft US labour market data that last week supported bets for accelerated Fed easing and a further easing of (global) financial conditions. Markets usually take a forward looking approach, mostly ignoring statistical data revisions. For once, this might be different with the BLS benchmark payrolls revision spanning the period April 2024-March 2025 to be published later today. With markets expecting in a downward revision of potentially 700k or more, the report in some way might profoundly ‘rewrite recent US economic history’, with equally important consequences for the Fed’s assessment. After the recent bond market rally and with money markets already discounting a sub 3% Fed policy rate, US yield markets today are shifting to a wait-and-see modus ahead of the BLS revision. US yields add between 1.5 bp (2-y) and 2.5 bps (30-y). US price data tomorrow (PPI) and on Thursday (CPI) maybe also cause some caution. Questions remains how much weight inflation still gets in both markets’ and the Fed’s assessment. With the Fed policy rate still in restrictive territory, we continue to see the risk for faster Fed easing in case of weak (labour) data. Later today, the US Treasury will sell $58 of 3-y notes. Interesting to see investor appetite after the recent rally and given higher yield levels for short-term US T-bills. Also little news on this side of the Atlantic. The German curve corrects sightly on recent flattening move with yields rising between 1.2 bps (2-y) and 3.0 bps (30-y). The (unsurprising) fall of the Bayrou government in France and President Macron restarting its exercise to find a new Prime Minister, is holding the French-German 10-y spread at a fragile ‘equilibrium’ near 80 bps. Both US equities (S&P 500 unchanged, EuroStoxx 50 -0.2%) are going nowhere. Oil jumps on the headlines of an Israeli strike against senior Hamas leadership in Doha (Brent $ 67 p/b).

On FX markets, the dollar took a weak start in Europe this morning, but reversed initial losses later in the session. DXY trades marginally higher at 97.55. EUR/USD came within reach of the 1.1789 level (24 July top and finally hurdle ahead of the 1.1829 YTD top). However, a real test/break didn’t occur yet. A combination of USD-rebound and euro-softness currently brings EUR/USD back to the 1.174 area. The yen slightly outperforms both the dollar and the euro on headlines of a BOJ still considering a rate hike this year (USD/JPY 146.8; EUR/JPY 172.35).

News & Views

Hungarian inflation figures printed exactly in line with consensus for the month of August. There was no price growth on average on a monthly basis with the annual figure stabilizing at 4.3%, above the central bank’s 3% inflation target. A separate analysis by the MNB shows core inflation excluding processed food dipping below 4% (3.9% Y/Y) for the first time since August 2021. Its sticky price inflation gauge was unchanged at 4.8% Y/Y Monthly data showed food and energy prices unchanged. The highest price rise of 0.6% was measured for alcoholic beverages and tobacco. Service prices rose by 0.5% on average and those of durable consumer goods by 0.4% M/M. In annual terms, Hungarian food prices rose by 5.9% with energy prices increasing by 11%. Services became 5.4% more expensive while consumer durable prices were up by 2.4%. Today’s data suggest that the MNB will stick with its stead, hawkish, monetary course for the foreseeable future. The Hungarian forint didn’t respond to the data and holds its ground near strongest HUF-levels since the summer of last year (EUR/HUF 393).

People familiar with the matter told Bloomberg that the Bank of Japan is of the view that it may be possible to raise the benchmark interest rate again this year regardless of domestic political instability, as economic conditions have developed in line with expectations. The US-Japan trade deal has also removed a key source of uncertainty. While an unchanged decision will be the outcome at the September central meeting, odds for a 25 bps rate hike to 0.75% in October (meeting with new quarterly forecasts) surged from 44% to 64%. Earlier today, Reuters reported that the BoJ is highly likely to trim purchases of 10- to 25-yr Japanese government bonds in its Q4 plan. The Japanese yen initially gained ground on the rate hike rumours with USD/JPY slipping from 147.30 to 146.30 before returning towards 146.80.

US: Small Business Optimism Improves Modestly in August

The NFIB's Small Business Optimism Index rose 0.5 points to 100.8 in August, coming in right in line with market expectations. As confidence improved, uncertainty pulled back, falling 4 points to a still elevated reading of 93.

Four out of ten subcomponents improved on the month, four decreased, and two remained unchanged. The largest gains were in expectations about higher real sales (up 6 points to 12%), earnings trends (up 3 points to -19%), and current inventory being too low (up 3 points to 0%). The declines among key subcomponents were more muted in comparison.

The net share of businesses planning to increase employment rose 1 point for the third month in a row to 15%, but the share of firms with unfilled job openings continued to trend lower (down 1 point to 32%). Quality of labor concerns remained unchanged at an elevated level, with 21% of business owners identifying this as their top business problem.

The share of firms reporting "few or no qualified workers for job openings" fell 5 points to 43% – aside from the start of the pandemic, this is the lowest level since early 2016.

Inflation metrics were muted. The share of businesses 'raising' average selling prices fell 3 points to 21%, while the share of those 'planning’ to raise average selling prices ahead 2 points to 28% – both measures remain well above their historical averages. Meanwhile, inflation concerns held steady at 11% for the third month in a row – lower than the 20-25% in the 2023-24 period, but still elevated compared to historical norms.

Key Implications

Small business optimism improved modestly in August, extending the turnaround in the confidence measure that began back in April. Among the key developments in today's report is the fact that, alongside some normalization in inflation-related metrics, businesses have been feeling more upbeat about 'real sales' in the months ahead.

Following a period of job cuts at small firms (June to August), the share of businesses planning to increase employment in the months ahead has also trended moderately higher. While 'quality of labor' remains the top concern, small businesses appear to have plenty of applicants for their job openings. The not so good news is that these openings continue to trend lower, which speaks to a more moderate pace of job creation ahead. Overall, with the Fed putting more emphasis on labor market concerns recently, this data leans in favor of a rate cut at next week's FOMC meeting.

Elliott Wave Blue Box Payoff: CADJPY Drops as Predicted

In this technical blog, we are going to take a look at the past performance of CADJPY Daily Elliott wave Charts that we presented to our members. In which, the decline from 7.10.2024 high took place in a double three corrective sequence and showed a lower sequence calling for more downside to happen. Therefore, our members knew that selling the bounces in the direction of the right side tag remained the preferred path. We will explain the Elliott wave structure & selling opportunity our members took below:

CADJPY Daily Elliott Wave Chart From 7.19.2025

CADJPY Daily Elliott Wave Chart from 7.19.2025 Weekend update. In which the pair is showing 5 swings lower low sequence supporting 6th bounce to fail for another leg lower to complete 7 swings corrective sequence from the peak. Whereas the decline to 101.26 low ended wave (A) of ((Y)). Up from there, the pair made a bounce towards the blue box area within wave (B). The internals of that bounce unfolded as zigzag structure where wave A ended at 106.25 high. Wave B pullback ended at 103.01 low. And wave C managed to reach the blue box area. From there, sellers were expected to appear looking for further downside or a minimum 3-wave reaction lower.

CADJPY Latest Daily Elliott Wave Chart From 9.06.2025

This is the latest Daily view from the 9.06.2025 Weekend update. In which the pair is showing a reaction lower taking place from the blue box area. Allowing shorts to get into a risk-free position shortly after taking the position. However, a break below 101.26 low is needed to confirm the next extension lower & avoid double correction lower.

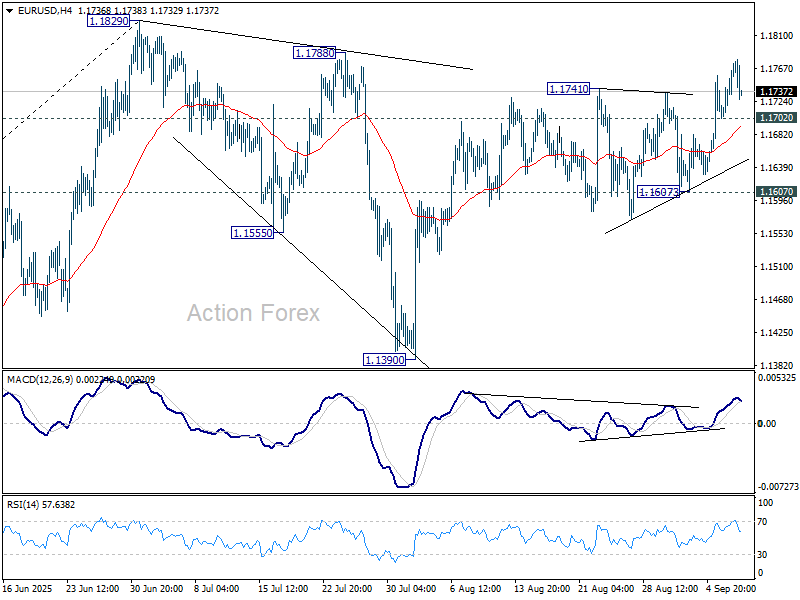

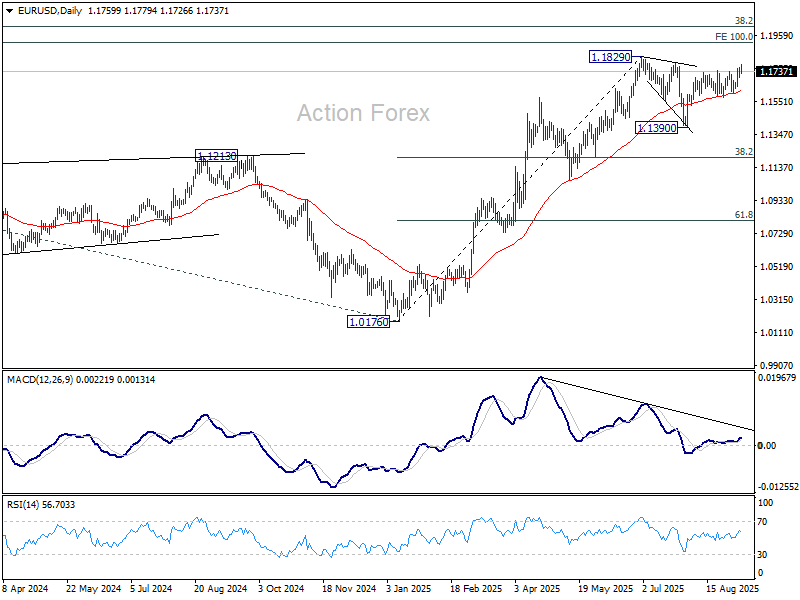

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1656; (P) 1.1708; (R1) 1.1771; More...

Intraday bias in EUR/USD remains on the upside for retesting 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, below 1.1702 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.1607 support holds, in case of retreat.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

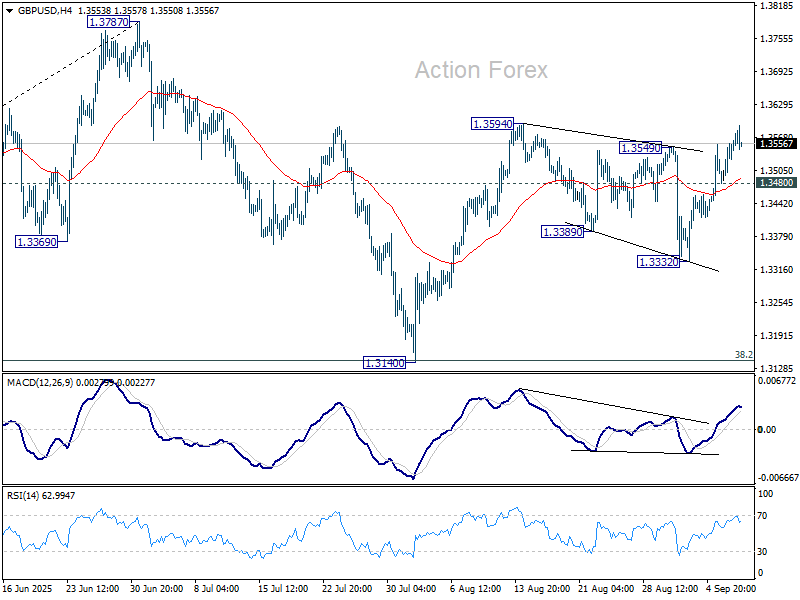

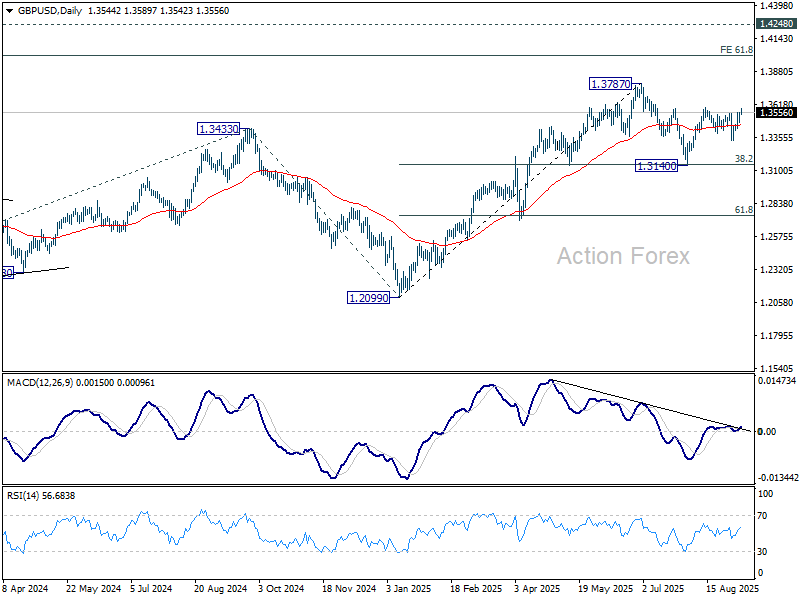

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3499; (P) 1.3528; (R1) 1.3574; More...

Intraday bias in GBP/USD stays on the upside for the moment. Firm break of 1.3594 resistance will resume the rally from 1.3140 and target a retest on 1.3787 high. On the downside, below 1.3480 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.3332 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

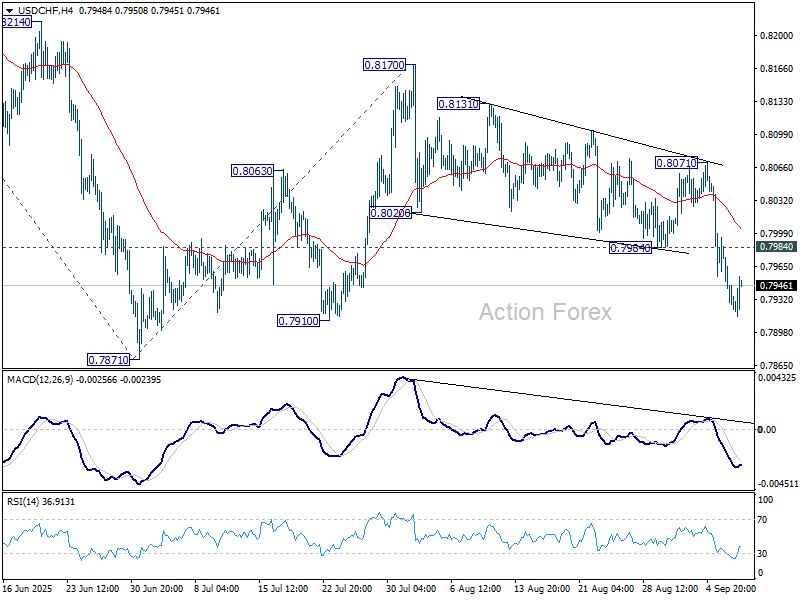

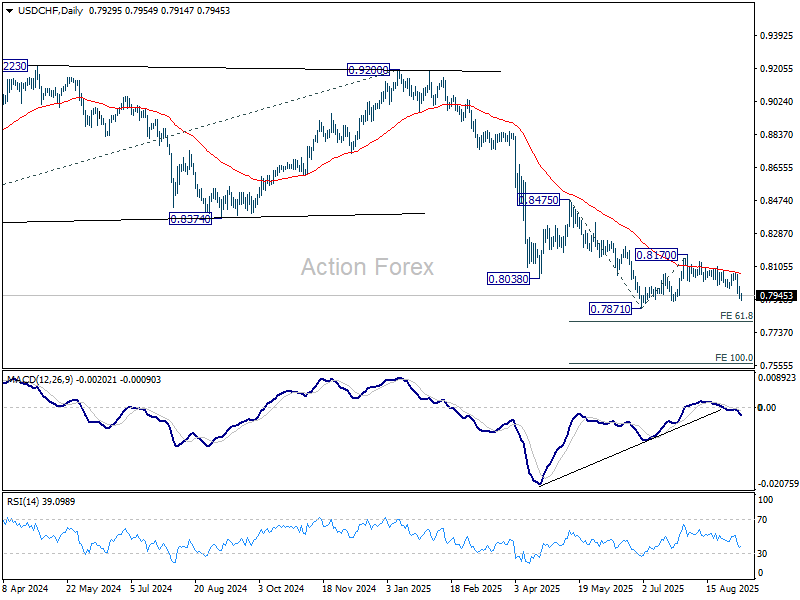

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7908; (P) 0.7952; (R1) 0.7976; More….

Intraday bias in USD/CHF remains on the downside and deeper fall should be seen to retest 0.7871 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. On the upside, above 0.7984 resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.8071 resistance holds, in case of recovery.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

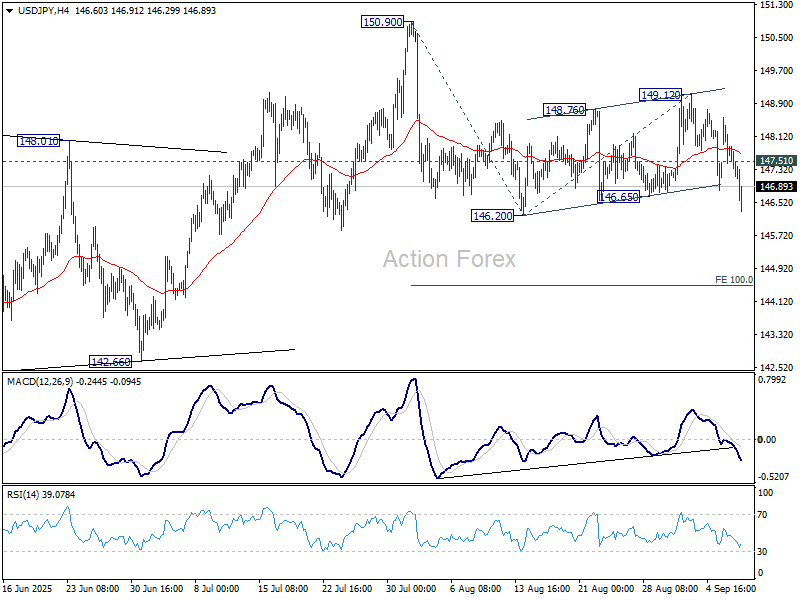

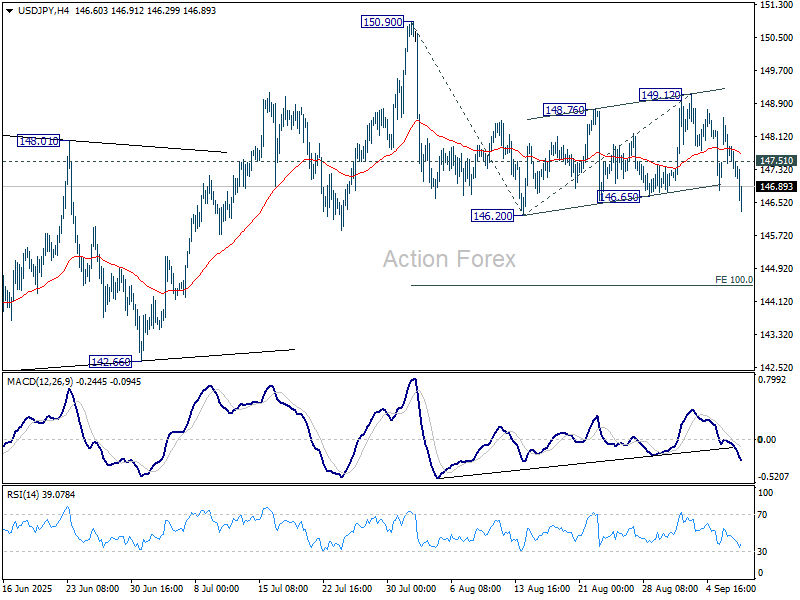

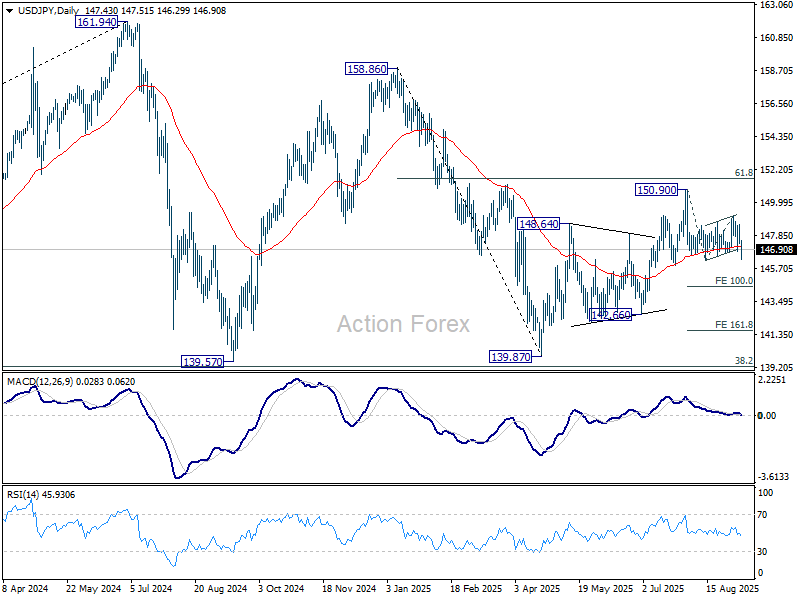

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.05; (P) 147.82; (R1) 148.29; More...

USD/JPY's break of 146.65 support suggest that fall from 150.90 is resuming. Intraday bias is back on the downside, and break of 146.20 will target 100% projection of 150.90 to 146.20 from 149.12 at 144.42. Also, sustained trading below 55 D EMA (now at 147.15) will argue that whole rebound from 139.87 has completed with three waves up to 150.90. On the upside, however, break of 147.51 minor resistance will mix up the outlook again and turn intraday bias neutral.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Yen Rebounds Despite Confusion Over BoJ’s Next Move

Yen rebounded broadly today, climbing to the top of the performance leaderboard as traders latched onto speculation that the BoJ may still raise rates as soon as October. A Bloomberg report citing unnamed officials suggested some policymakers favor an earlier move, with reduced concern about growth risks following the U.S.–Japan trade deal. The report noted that the key variable for policymakers is whether the drag from U.S. tariffs on Japan’s economy remains within expectations. If so, the bank could argue there is room to resume normalizing rates despite political turbulence in Tokyo.

However, the report relied on anonymous sources and came alongside conflicting headlines. Many analysts argue the resignation of Prime Minister Shigeru Ishiba and the ensuing LDP leadership contest are reasons for caution. The BoJ, they contend, is unlikely to risk tightening policy amid such political uncertainty. The central bank also has time on its side. Policymakers can afford to wait until early next year for the next hike, ensuring stability while avoiding the impression of acting in haste. For markets, this means rate expectations are likely to remain volatile as headlines shift.

Elsewhere, Euro weakened broadly, with investors still digesting the ouster of French Prime Minister François Bayrou on Monday. His government’s collapse has heightened perceptions of instability in Paris, though the turmoil alone is unlikely to drive sustained Euro weakness without broader contagion. Still, the picture of France cycling through four prime ministers in two years have weighed on confidence. With President Emmanuel Macron scrambling to find another candidate capable of surviving parliament, Euro has remained defensive.

In the wider FX market, Yen is the day’s strongest performer so far, followed by Aussie and Kiwi. Euro is the weakest, trailed by the Swiss Franc and Loonie. Dollar and Sterling sit mid-pack.

In Europe, at the time of writing, FTSE is up 0.26%. DAX is down -0.48%. CAC is up 0.31%. UK 10-year yield is up 0.012 at 4.62. Germany 10-year yield is up 0.029 at 2.674. Earlier in Asia, Nikkei fell -0.42%. Hong Kong HSI rose 1.19%. China Shanghai SSE fell -0.51%. Singapore Strait Times fell -0.25%. Japan 10-year JGB yield fell -0.03 to 1.565.

Westpac: Australia consumer optimism elusive, RBA to pause in September

Australia’s Westpac Consumer Sentiment Index dropped -3.1% mom to 95.4 in September, reversing part of last month’s boost from the RBA’s third rate cut. While sentiment remains modestly above July levels and well above the April tariff-driven low, the index has slipped back into “cautiously pessimistic” territory. Westpac said outright optimism remains "elusive", with households still uneasy about the path ahead despite relief from the cost-of-living crisis.

The RBA is expected to keep its cash rate steady at 3.6% when it meets later this month. Westpac noted recent data on inflation and demand came in "somewhat firmer than expected", reinforcing the case for caution. Policymakers are seen waiting for further confirmation that underlying trends remain benign before resuming cuts.

For now, consumer recovery looks sluggish, and Westpac expects "further easing will likely be needed" to sustain momentum. It forecasts another 25bp cut in November and two additional moves in 2026, underscoring the gradual path ahead for both sentiment and policy.

Australia NAB business survey: Confidence falls, costs ease, capacity still tight

Australia’s NAB Business Confidence index slipped from 8 to 4 in August, but conditions showed improvement, rising from 5 to 7. Trading remained steady at 12, while profitability rose from 2 to 4 and employment from 2 to 5. NAB Chief Economist Sally Auld said the results support the view that “the outlook for businesses continues to improve,” with both confidence and conditions now near long-run averages.

Capacity utilisation rose to 83.1% from 82.5%, staying two percentage points above its long-run norm. Capital expenditure intentions also improved, climbing from 8 to 10. Together, these suggest firms are still operating at high levels of resource use despite broader uncertainties.

At the same time, cost pressures eased further. Purchase cost growth slowed from 1.3% to 1.1%, its lowest since 2021, while labour costs moderated to from 1.9% 1.5% and product price growth dipped to from 0.8% 0.6%. The survey points to an environment of resilient business activity and capacity tightness, but with inflation pressures continuing to recede.

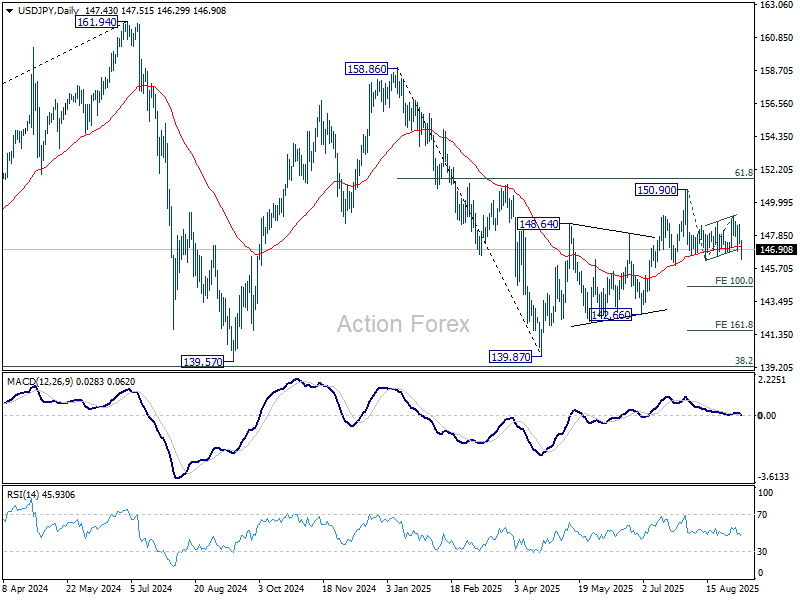

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.05; (P) 147.82; (R1) 148.29; More...

EUR/JPY's break of 146.65 support suggest that fall from 150.90 is resuming. Intraday bias is back on the downside, and break of 146.20 will target 100% projection of 150.90 to 146.20 from 149.12 at 144.42. Also, sustained trading below 55 D EMA (now at 147.15) will argue that whole rebound from 139.87 has completed with three waves up to 150.90. On the upside, however, break of 147.51 minor resistance will mix up the outlook again and turn intraday bias neutral.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

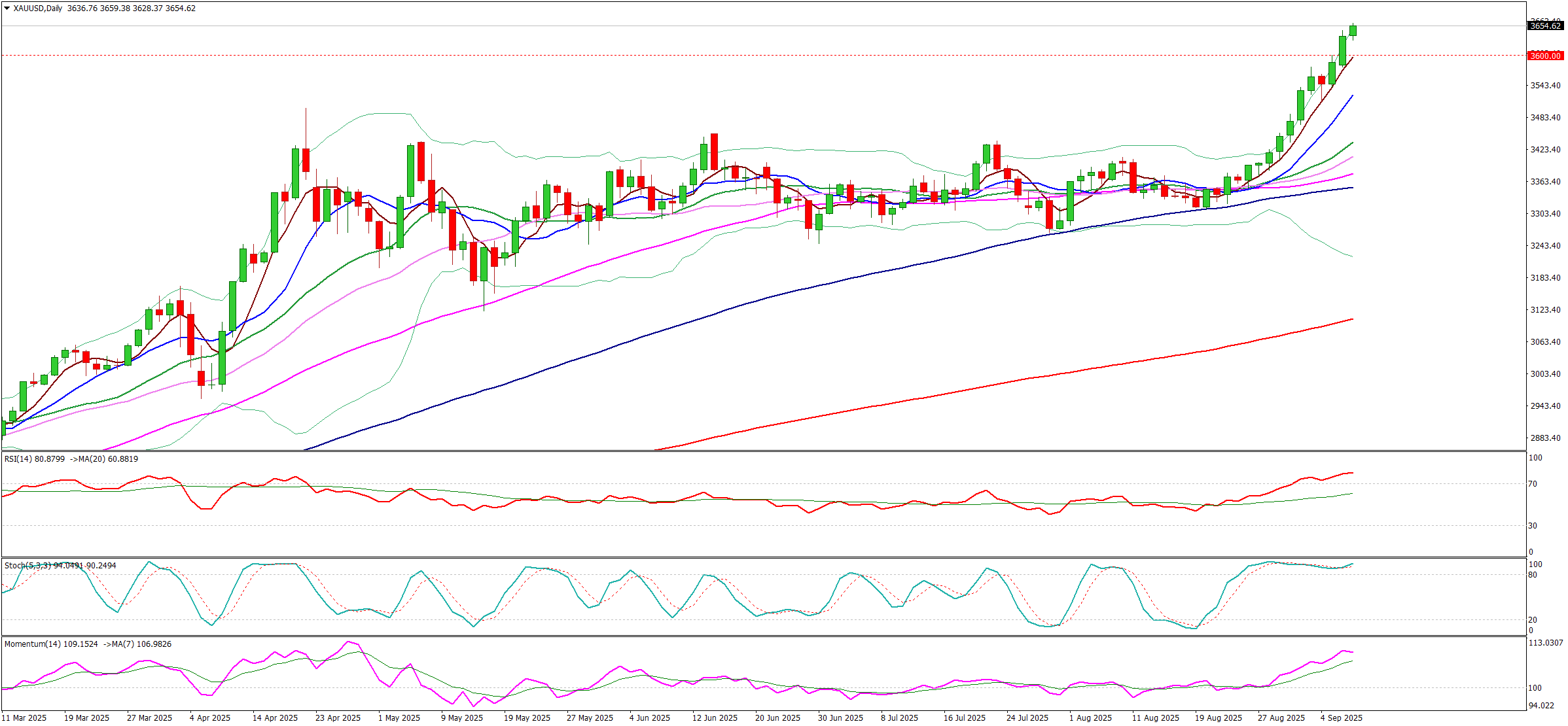

XAU/USD: Gold Extends Rally into Uncharted Zone

Gold rose to new record high ($3659) in early Tuesday’s trading, after strong acceleration on Monday (up 1.5%) which resulted in break and close above psychological $3600 barrier.

The latest economic data from the US showed that labor market continues to weaken (weakness further accelerated in August) that adds to strong expectations for Fed rate cut in the policy meeting next week.

Growing uncertainty over political crisis in the US and the latest negative developments in France after the government collapsed, as well as fragile political situation in the UK were the main political factors.

Worsening geopolitical situation on intensifying clashed in Ukraine and the Middle East and the latest crisis in Caribbean region (Venezuela) as well as darkening economic outlook, particularly in Europe, were also behind the latest rally into safety.

Technical pictures remain firmly bullish but overbought conditions on daily chart (although RSI and Stochastic continue to head north) warn that bulls may start losing traction.

Consolidation and shallow dips would be likely scenario, as bullish sentiment remains strong in current environment.

Broken $3600 level reverted to solid support which should ideally contain dips and confirm positioning for fresh push towards targets at $3690/$3700) Fibo projection / round-figure).

Res: 3668; 3690; 3700; 3434.

Sup: 3628; 3600; 3577; 3540.

Gold (XAU/USD) Technical: Overbought But Bullish Trend Remains Intact

The precious yellow metal has staged the expected bullish breakout above its former all-time high of US$3,500 printed on 22 April 2025. Gold (XAU/USD) rallied by 5.3% to hit a current fresh intraday record high of US$3,655 at the time of writing.

Lower opportunity costs reinforced the current bullish acceleration phase of Gold

10-year US Treasury real yield is extending its decline

Fig. 1: 10-YR US Treasury real yield major trend with Gold (XAU/USD) as of 9 Sep 2025 (Source: TradingView).

Gold (XAU/USD), as a non-interest-bearing asset, tends to benefit in lower-rate environments. A decline in interest rates reduces the opportunity cost of holding gold, thereby supporting stronger demand.

This dynamic can reinforce bullish momentum, potentially creating a positive feedback loop that drives further price appreciation.

Since Fed Chair Powell’s dovish speech at Jackson Hole on 22 August, the 10-year US Treasury real yield (stripping out 10-year inflation expectations derived from the 10-year US Treasury inflation-protected bond) has declined by 19 basis points (bps) to a current level of 1.66% from 1.85% (see Fig. 1).

Let’s now examine Gold (XAU/USD)’s latest short-term (1 to 3 days) trajectory and key technical levels to watch.

Fig. 2: Gold (XAU/USD) minor trend as of 9 Sep 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

Maintain bullish bias with a key short-term pivotal support at US$3,600 for Gold (XAU/USD). Minor bullish impulsive up move sequence is likely in progress, and a clearance above US$3,670 sees the next intermediate resistances coming in at US$3,697 and US$3,725 (Fibonacci extension cluster) (see Fig. 2).

Key elements

- The current price actions of Gold (XAU/USD) in place since the 29 August 2025 low of US$3,404, are classified as a bullish acceleration movement depicted by a steeper minor ascending channel.

- The lower boundary of the steeper minor ascending channel confluences closely with the US$3,500 key short-term pivotal support.

- The hourly RSI momentum indicator has managed to find support at its parallel ascending support after it exited from its overbought zone in today’s Asia session (9 September).

Alternative trend bias (1 to 3 days)

A break below the US$3,600 key short-term support on Gold (XAU/USD) invalidates the bullish tone to trigger a deeper minor corrective decline towards the next intermediate supports at US$3,561 and US$3,536.