Sample Category Title

Gold, Oil Jump on Qatari Attack, US Data in Focus

Those who read these morning notes regularly know how surprising I was to see such strong and much better-than-expected NFP reports month after month at a time when mass layoffs, deportations and tariff-driven uncertainty were supposed to weaken the US jobs market. Well, it appears that I was right to be surprised, and that the numbers were not all that accurate.

The BLS announced yesterday that the payrolls report could be revised down by 911K jobs for the 12 months through March – about 76K fewer jobs per month. That would mark a record-high revision. In simpler words, it means that the US jobs market is in much worse shape than we thought. But it’s not the BLS’s fault. The BLS releases the jobs figures just days after the end of each month by extrapolating from a sample of data. In normal times, this works well and gives investors and economists an early and fairly accurate picture of the underlying jobs market. But in times of heavy disturbance – like we’ve had since the beginning of this year – the extrapolation works much less well, and the numbers now clearly show that the US economy is bearing the brunt of Donald Trump’s policies.

That means the Fed may indeed have fallen behind the curve – at least on the jobs front – while trying to anticipate tariff-led inflation. The latter could mean bigger and faster rate cuts in the coming months, depending on inflation. Today, the US will publish its latest PPI update for August. After last month’s circa one-percentage-point jump, headline PPI is expected to have steadied near 3.3%, and core PPI may have eased from 3.7% to 3.5% YoY. The real question is how much of the rising input costs will flow into the consumer price index – due tomorrow. The stronger the inflation figures, the slower the Federal Reserve (Fed) will lower interest rates – and that could demoralize investors who are currently happy to see the jobs market weaken in exchange for larger rate cuts.

As such, yesterday’s BLS revision didn’t boost appetite in US 2-year bonds, which best capture Fed expectations. The US 2-year yield rebounded to 3.55%, while the US dollar recovered – probably also on some safe-haven flows amid rising geopolitical tensions in the Middle East following Israel’s latest strikes in the region. Fed funds futures now give a 100% probability for at least a 25bp cut at next week’s FOMC meeting, and about an 8% chance for a 50bp cut. Stronger-than-expected inflation numbers this week could cement the case for a 25bp cut – which could lead to an upside correction in US short-term yields and the dollar, and weigh on equities. A softer set of figures would give more weight to the possibility of a 50bp cut, sending US short-term yields and the dollar lower, and equities higher.

The S&P 500 consolidated gains at ATH yesterday, as did the Nasdaq. Tech stocks were in demand, except for Apple – where the unveiling of its thinnest iPhone yet, but with no major AI news, sent the share price down 1.5% after the product reveal. A neocloud company called Nebius, on the other hand, jumped 50% after Microsoft announced a five-year agreement with the company, initially valued at $17.4 billion, with the option to scale up to around $19.4 billion depending on its compute needs. Jackpot! Another Microsoft neocloud provider, the Nvidia-backed CoreWeave, rose 7% as the deal confirmed how strong the demand for AI computing capacity is. Nvidia recovered 1.5%, while Broadcom – which has rallied on news of its cooperation with OpenAI to produce an AI chip to rival Nvidia – gave back 2.6%. Then, Oracle rocketed 28% in after-hours trading – yes, 28% – following its own massive deal with OpenAI and a jump in quarterly bookings. In summary, AI doesn’t know crisis.

Speaking of crisis: if you’re wondering how French markets behaved after another change in prime minister – the fifth in just two years – you’d be surprised to hear that the CAC 40 still eked out a 0.19% gain, despite a rebound in French 10-year yields. The DAX, in contrast, eased 0.37%. Yet, the spread between French and German 10-year yields spiked above 80bp, while the spread against the Italian 10-year collapsed to zero – for the first time since the early 2000s. Fitch is scheduled to deliver its review of France’s sovereign credit rating on Thursday. The current rating is AA- with a negative outlook. A confirmation with a negative outlook would signal caution, reinforcing market concerns, while a downgrade – due to prolonged political uncertainty – would be material, possibly triggering forced selling by institutional investors who must adhere to minimum credit thresholds. For the euro, the French political turmoil implies limited upside potential, and possibly a reversal of gains before reaching the 1.20 level. Also on Thursday, the European Central Bank (ECB) is expected to leave rates unchanged and repeat that its policy remains data-dependent.

In commodities, gold refreshed records – this time on safe-haven demand following escalating Middle East tensions – while crude oil remains bid on both the geopolitical backdrop and waning hopes in Ukraine. Nat gas futures also rebounded from a key Fibonacci support and could extend gains on fresh geopolitical concerns. The UK’s energy- and miner-heavy FTSE 100 continues to be supported by strong commodity demand. Yesterday’s mega-deal, in which Anglo American agreed to buy Canada’s Teck Resources for its copper mines, added to the momentum. It’s all about real and tangible assets, now that confidence in the most popular sovereign debt papers is crumbling.

Trump Puts Pressure on EU to Enter Trade War

In focus today

In the US, August producer prices (PPI) are due for release in the afternoon. This time, the PPI will attract even more attention than usual both because it is released ahead of the August CPI and because the previous July release surprised significantly to the upside. It will provide markets with the first sense of how tariff-related costs have continued to build.

In Norway, we expect the August inflation figures to show core inflation (CPI-ATE) rising by 2.8% y/y (cons: 3.1%) and declining -1.0% m/m (cons: 0.8%). This aligns with Norges Bank's June MPR estimate of 3.1% when we correct for the government's decision to cut kindergarten prices from 1 August. The price cut is expected to help pull down core inflation by approximately 0.2-0.3 percentage points.

In Sweden, we will receive economic data for July, including the production value index (PVI), industrial production, the consumption indicator, and the GDP indicator. In June, the PVI increased y/y, and industrial production has been strong. While the GDP indicator is volatile and should be interpreted cautiously, the consumption indicator is generally more reliable and has shown signs of improvement.

In Denmark, inflation data for August is also released. We expect inflation will fall to 2.0% y/y from 2.2% y/y in July. It is particularly driven by an August surge in electricity prices last year now exiting the inflation measure, while at the same time prices look to have declined in August this year. It will be interesting to see how big the usual August food price decline will be following three months of surging prices.

Economic and market news

What happened overnight

In China, August CPI inflation dropped back into negative territory at -0.4% y/y (prior: 0.0%), generating fresh deflation headlines. However, core inflation rose to 0.9% y/y (prior: 0.8%) and has been increasing over the past quarters, nearing 1%. PPI eased to -2.9% y/y (prior: -3.6%) but remains in deflation, reflecting ongoing overcapacity issues in certain sectors driven by intense competition and insufficient demand.

In the US, a federal judge ruled that President Trump's attempt to remove Fed Governor Lisa Cook lacks legal ground, temporarily keeping her in office as the case proceeds. This likely means that Cook can attend the Fed meeting on 16-17 September, reinforcing Fed's independence.

Also in the US, President Trump has urged the EU to impose tariffs of up to 100% on China and India to pressure Putin by targeting key buyers of Russian oil. The request came as the EU delegation met in Washington to discuss sanctions coordination. An EU diplomat stated the US signalled readiness to impose similar tariffs if the EU agreed.

What happened yesterday

In the US, the preliminary NFP benchmark revision came in more negative than expected with a significant downward adjustment of -911k jobs. However, note that the revision applies to employment data from April 2024 to March 2025 and, as such, does not reflect recent growth momentum in labour markets. The data shows no sharp rise in layoffs or unemployment, but slowing job growth reflects limited available workers. While the data alone does not strongly justify immediate rate cuts, it may serve as an argument for those already advocating for it. We expect the Fed to resume its rate cutting cycle starting at next week's September meeting.

In France, President Macron appointed defence minister Sebastien Lecornu as prime minister. A close ally of the president and the only minister to have remained in government since Macron's 2017 election. A tough challenge now awaits the new PM of helping the minority government secure opposition support to pass the 2026 budget.

In geopolitics, Israel launched an attack on Hamas in Qatar, drawing condemnation from Qatari officials, Arab leaders, and the UN. The White House stated that the strike did not advance Israeli or American goals but reaffirmed eliminating Hamas as a worthy objective. Israeli authorities have also threatened to expand their assault against the Houthis in Yemen, as the humanitarian situation in Gaza worsens. In our view, yesterday's attack seems more like an act to sabotage ongoing ceasefire talks, even as Israeli leadership is likely to frame it as a coercive measure to force a truce. Oil prices showed little reaction, reflecting a high threshold in markets for disruptions in the Middle East.

Equities: Equities extended their grind higher yesterday in what some would call a pain trade - an uncomfortable lift where investors remain uneasy about valuations and macro risks, yet the market keeps drifting up. Cyclicals outperformed defensives, volatility edged lower, and we saw a classic rally given where we are in the cycle and how positioning is. In the US yesterday, Dow +0.4%, S&P 500 +0.3%, Nasdaq +0.4% and Russell 2000 -0.6% and into the US close, the Dow, Nasdaq and S&P 500 all hit fresh all-time highs, underlining the strength of the move.

The wall of worries remains intact - from sharp downward revisions to US payrolls, to the French government losing a confidence vote, to geopolitical tensions following the Israeli strike in Qatar. Yet the market shrugged it off, as the underlying data flow yesterday was generally solid and the political/geopolitical noise did not fundamentally alter the economic outlook. This morning, Asian markets are higher and the same goes for most futures in the US and Europe.

FI and FX: For the first session in a week, global yields ended yesterday on a higher footing. Overnight this move has extended with 10Y US Treasury yields hitting 4.09%. The USD FX is also stronger with EUR/USD completing an almost full-figure drop down close to the 1.17-figure. In broader FX markets, commodity exporting currencies have enjoyed higher commodity prices with notably NOK and AUD being among the outperformers in Majors' space. On the other hand, commodity importing currencies have suffered with CEEs and the EUR doing poorly.

AUD/USD Breakout Watch – Can Momentum Drive More Gains?

Key Highlights

- AUD/USD started a fresh rally from the 0.6500 region.

- A key bullish trend line is forming with support at 0.6540 on the 4-hour chart.

- Gold surged further to a new all-time high above $3,660.

- EUR/USD could aim for a move toward 1.1850 or even 1.1880.

AUD/USD Technical Analysis

The Aussie Dollar remained supported above 0.6500 and started a fresh increase against the US Dollar. AUD/USD rallied above 0.6550 and 0.6580 to enter a positive zone.

Looking at the 4-hour chart, the pair settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). The pair even spiked above 0.6615 before it faced some resistance.

On the upside, the pair could face resistance near the 0.6620 level. The first major hurdle for the bulls could be 0.6640. A close above 0.6640 could set the pace for another increase. In the stated case, the pair could rise toward 0.6720, above which the bulls could aim for a move toward 0.6850.

Any more upsides could send the pair toward 0.6900. On the downside, immediate support is 0.6575. The next key area of interest might be 0.6550. There is also a major bullish trend line forming with support at 0.6540 on the same chart.

The trend line is close to the 61.8% Fib retracement level of the upward move from the 0.6501 swing low to the 0.6619 high. Any more losses could send the pair toward 0.6510 and the 100 simple moving average (red, 4-hour).

Looking at Gold, the bulls remain in action as they were able to push the price to a new all-time high above $3,660.

Upcoming Key Economic Events:

- US Producer Price Index for August 2025 (MoM) – Forecast +0.3%, versus +0.9% previous.

- US Producer Price Index for August 2025 (YoY) – Forecast +3.3%, versus +3.3% previous.

- US Wholesale Inventories for July 2025 (preliminary) – Forecast +0.2%, versus +0.2% previous.

China CPI falls -0.4% yoy, core inflation hits 2-1/2 year high

China’s consumer prices slipped deeper into deflation in August, with CPI down -0.4% yoy after July’s flat reading, worse than expectations of -0.2% yoy and the weakest in six months. Food prices were the main drag, falling -4.3% yoy versus -1.6% yoy previously. On a monthly basis, CPI was unchanged, undershooting forecasts for a small 0.1% mom rise.

At the same time, core inflation showed signs of life, rising 0.9% yoy in August compared with 0.8% yoyin July — the fastest pace in two and a half years. The pickup suggests underlying demand in services and other non-food sectors is holding up better than headline numbers imply, even as consumers face falling food costs.

Producer prices continued to contract, though at a slower pace. PPI dropped -2.9% yoy, in line with expectations and an improvement from -3.6% yoy in July. The figures highlight China’s ongoing struggle with persistent factory-gate deflation, which has now lasted nearly three years.

US CPI Preview: Implications for the DXY & Federal Reserve

The CPI outlook looks shaky and this week's print may show a rise of about 0.3% this past month, which could lift the annual rate to roughly 2.9%. Some analysts even think it might hit 3% year‑over‑year.

The boost seems tied to higher food and energy costs. One estimate even points to a 2% jump in gas prices month‑to‑month, therefore pressure stays on and shoppers likely notice higher costs at checkout.

US Core CPI Debate

The real debate, though, centers on core CPI numbers – the ones that leave out the wild food and energy swings. Different analysts see two paths ahead. One camp thinks we’ll see a 0.3 % rise from month to month, which would leave the annual rate stuck around 3.1 %. The other, more cautious group, pictures a 0.4 % jump, the biggest since January and the second biggest in almost two years. That tiny gap between 0.3 and 0.4 isn’t just a math detail; it could change how we read inflation.

A 0.3 increase might still be called “sticky,” yet it could be part of a rough but steady slowdown in price growth. A 0.4 rise, however, seems to signal a clear push back up, shaking the idea that inflation is finally easing.

If that happens, the question is will the Fed change its policy stance? My answer is no but markets would probably react quickly, and investors might demand higher yields on bonds.

Source: TradingEconomics

Underlying Drivers: Where the Inflationary Pressures Originate

The rise in inflation looks like it will be spread across many items, not just a few. A bounce back in core goods prices may add about 0.25 % from month to month, which could push the annual rate up to its biggest point since May 2023. Parts of this push could be new cars, clothing, sports gear, and even phones or tablets.

At the same time, the hoped‑for relief from slower service inflation appears to be fading. Forecasts suggest core services might go up roughly 0.30 % in August, with travel‑related services—especially hotel costs—showing a strong climb of around 1.0 %. This broader strength in both goods and services therefore hints that price pressures are no longer limited to narrow sectors but may be more rooted in the overall economy.

Policymakers will be watching these trends closely even as the labor market dominates the discussion at the moment.

The Fed’s Policy Puzzle: A Rough Road Ahead

The road ahead for the Federal Reserve is expected to be a bumpy one. Concerns about Fed independence, worsening labor market conditions and political drama will keep the Fed the center of attention for the remainder of 2025.

As things stand, the labor market is going to be the center of focus for now. However, if inflation begins to rise again as tariffs begin to start filtering through and companies pass the increases to consumers, inflation could play a much bigger role later in the year.

Potential Implications for the US Dollar and Rate Cut Expectations

Two things mainly push the dollar when a CPI report comes out. First, interest‑rate gaps – the difference between U.S. Treasury yields and the yields you see in other countries. Those gaps decide where money moves.

Second, Fed‑policy guesses – how people see the chances of the Fed raising or lowering rates. Those guesses shift the gaps. When CPI numbers change what folks expect the Fed will do, they also change how attractive U.S. assets look. That can lift the dollar or drop it.

When the CPI looks “hot” – say the core number is 0.4 % or higher – it hints that inflation is still strong. That may mean the Fed will keep tightening or even go harder. Traders then want more dollars, Treasury yields climb, and the DXY (the dollar index) usually goes up. At the same time, stocks can feel pressure because borrowing costs look higher.

But a “cool” CPI – core 0.3 % or lower – suggests price growth is slowing. The market may turn more dovish, thinking the Fed could pause or cut rates sooner. Lower expected yields make the dollar less tasty, so it often slides down. Treasury yields tend to fall, and risk assets like equities might get a boost from cheaper money.

In short, the dollar’s move is a straight line from CPI‑driven belief changes to interest‑rate gaps, then to the dollar’s strength.

What could happen based on those ideas:

- Hot CPI (core 0.4 %+): Dollar likely goes up against other currencies (DXY climbs); Treasury yields rise; stocks may drop.

- Cool or Neutral CPI (core ≤0.3 %): Dollar may sell off; Treasury yields fall; equities could rally.

If the CPI lands right at the expected 0.3 % core, markets sometimes do a “buy the rumor, sell the fact” trick. If people already priced in a hawkish Fed, the on‑target number can cause a quick, technical dip in the dollar. That shows why the headline number and how it differs from consensus both matter.

So, in the current climate markets are expecting a slight uptick in inflation. Meaning if we do get a softer print, the immediate reaction could see the probability of a 50 bps rate cut on September 17 rise. This will lead to a selloff in the US Dollar but is unlikely to last as markets will likely cool off once the data has been fully digested.

US Equities may attract a lot of interest as they have continued to rise in recent trading sessions. I expect that the volatility we see with US equities will outweigh volatility elsewhere irrespective of whether the data is positive or negative.

US Dollar Index (DXY) Daily Chart, September 9, 2025

Source: TradingView.com (click to enlarge)

Dollar Index (DXY) Faces Key Test from Upcoming PPI and CPI – Potential Reactions

Some contradicting headlines are influencing the US Dollar in a battle of wits right ahead of quintessential inflation data.

Markets have been unable to provide a clear answer on how the upcoming FOMC (September 17th) and its rate cut expectations will affect the future outlook for the Dollar.

The thesis had been that despite negative news (Jerome Powell's change in tone at Jackson Hole or the recent Non-Farm Payrolls), traders have failed to sell the US Dollar convincingly, with the DXY doomed in sideways action.

The freshly released downward revisioned BLS report (bearish for the USD) and the rising tensions in the Middle East with Israel-Hamas war taking another turn (bullish for the USD) are once again prevented a clear path ahead for the Greenback.

However, some interesting technical patterns might be getting into play as we approach the surely decisive pair of inflation reports in the US PPI (8:30 E.T. tomorrow) and Thursday's CPI report.

Let's take a look at the Dollar Index.

How could the data influence the US Dollar? Potential reactions

The upcoming PPI report should bring back memories of the previous humoungous beat in the past month (0.9% vs 0.2% exp) pushing inflation expectations higher for the consecutive University of Michigan surveys (the FED hates that).

This comes as Participants started to be less and less cocnerned by tariffs and their impact.

Despite hurting producers before consumers, fears are that Producer Prices increases will repercutate in upcoming CPI releases, highlighting Thursday's number even more.

A relatively weak PPI could help to support current sentiment quite largely, indicating that the past month increase was just a one off – This should support a 50 bps cut further (Dollar down).

However an upward beat should do just the reverse and add to the anxiety (Dollar up)

CPI will really be in focus however as Participants look to see if the higher producing costs have started to bite in consumers pockets.

Reactions should be similar to the PPI, but their extent could be much larger: A higher inflation for Consumers should prevent a 50 bps entirely, towards more gradual cut and spark stagflation fears.

US Dollar could hence maintain its sideways movement.

Dollar Index intraday outlook

Dollar Index 4H Chart

US Dollar Index (DXY) 4H Chart, September 9, 2025 – Source: TradingView

Last week's data has brought some renewed selling momentum as bears have managed to form a downward tight bear channel (bear candles overlapping each other).

The weekly open hence formed a small gap to test the July support/pivot zone, and this morning of action actually saw a decent rebound, undoing some of the bear advantage.

Arriving at a key technical standpoint, bears entering here could take the hand by rejecting the 97.60 to 97.80 range lows (break-retest style).

Keep in mind that action will be swift tomorrow (expect spikes) and prices may just dawdle around until then.

Key levels of interest for the Dollar Index:

Support Levels:

- 97.40 to 97.80 Range Support (currently getting tested)

- Last Pivot before run-higher 97.15 Zone acting as Key Support

- 2025 Lows Major support 96.50 to 97.00

Resistance Levels:

- 98.00 Mid-Range pivot

- 98.50 to 98.80 Resistance Zone

- Mid-line of the ascending channel and psychological level 99.50

- 100.00 Main resistance zone

Dollar Index 30m Chart

Dollar Index (DXY) 30M Chart, September 9, 2025 – Source: TradingView

Looking closer to the short-timeframe, the support zone that is currently trading will be a major test for bulls.

Managing to hold the lows of the current support (97.40, immediate short-term support) would indicate balanced action, which would be more in the bulls favor after failing to hold lower.

On the other hand, sellers appearing at the immediate short-term resistance (97.70) could trigger break-retest selling reactions.

A breakout in any direction should see continuation.

Safe Trades!

Dow Jones 30 (DJIA): Dow Renews Highs at the Close, Breaks Above Consolidation

Closing at $45,711, up +0.43%, the Dow Jones 30 has renewed recent highs in today’s session, breaking above previously held consolidation at around $45,642.

Dow Jones 30 (DJIA): Key takeaways from today’s session

- Up around 7.00% year-to-date, recent developments suggesting the Fed will cut in their upcoming decision are benefiting US equity pricing

- While interest rate cuts stand to benefit Dow Jones pricing, weak jobs data and a potential for infamous ‘stagflation’ could limit upside in the medium term

Dow Jones 30 (DJIA): Interest rate cut predictions boost Dow Jones pricing

Although playing second fiddle to the tech-dominant Nasdaq-100 for much of 2025, the Dow Jones remains around ~7.83% year-to-date, even with zero interest rate cuts, which, on paper, would be negative for index pricing.

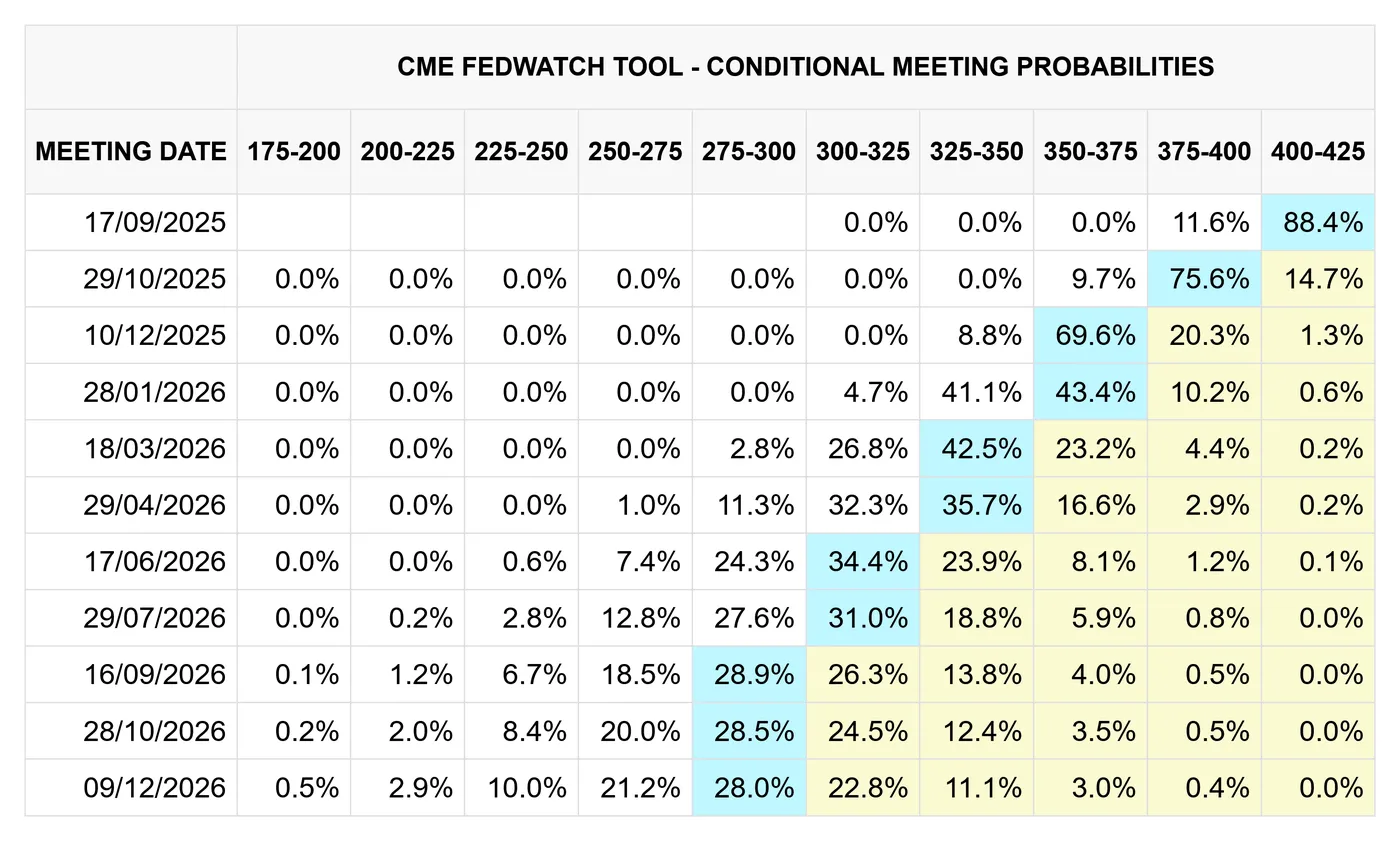

As we all know by now, this could be about to change; most predict that the Fed will cut rates by 25 bps in their upcoming decision, while others are even expecting a cut of 50 bps in response to poor US labour data.

CME FedWatch, 08/09/2025

While the latter remains unlikely compared to a more tame approach, what is more certain is that a Fed rate cut is undeniably positive for the Dow Jones, with the benefit of holding dollars instead of investing set to be lowered for the first time in 2025.

It should be noted that despite the Fed's choice of tight monetary policy, the Dow Jones has performed fairly well this year, all things considered. While we can expect some short-term upside from expectations of rate cuts, the proof in the metaphorical pudding will be how data reacts to a change in interest rates, especially regarding inflation and labour data

Dow Jones 30 (DJIA): Stagflation fears and poor labour data cast doubt over upside

With poor labour data having virtually cemented the chances of an interest rate cut next week, markets are keenly watching upcoming US inflation data releases to understand whether fears of ‘stagflation’ are justified:

- Core Producer Price Index (MoM) (Aug), Wednesday, September 10th, 08:30 ET

- Core Producer Price Index (YoY) (Aug), Wednesday, September 10th, 08:30 ET

- Producer Price Index (MoM) (Aug), Wednesday, September 10th, 08:30 ET

- Producer Price Index (YoY) (Aug), Wednesday, September 10th, 08:30 ET

- Core Consumer Price Index (MoM) (Aug), Thursday, September 11th, 08:30 ET

- Core Consumer Price Index (YoY) (Aug), Thursday, September 11th, 08:30 ET

- Consumer Price Index (MoM) (Aug), Thursday, September 11th, 08:30 ET

- Consumer Price Index (YoY) (Aug), Thursday, September 11th, 08:30 ET

It’s important to remember that, even if interest rates are to be cut, sentiment and general confidence in the US economy will be the most significant determining factor in equity performance in the near future.

As such, labour and inflation data remain as crucial as ever. When considering the Fed’s dual mandate, here are a couple possible outcomes in the next few months:

- Lower rates boost jobs growth while inflation starts to fall

If a decision to cut rates is made, and the labour market responds well, while inflation starts to fall, we can consider this the best possible outcome. Naturally, this would substantially boost belief in the US economy, which would be US equity positive

2. Lower rates fail to promote jobs growth, while inflation remains stubborn

If the Federal Reserve decides to cut rates and the labour market responds poorly while inflation proves stubborn, this would be a very difficult position to maintain. While further rate cuts would potentially help the labour market, maintaining or even hiking rates would better control inflation, making monetary policy decisions difficult. In this scenario, we can expect higher levels of market uncertainty, which would be generally US equity negative

Dow Jones 30 (US30USD), OANDA, TradingView, 09/09/2025

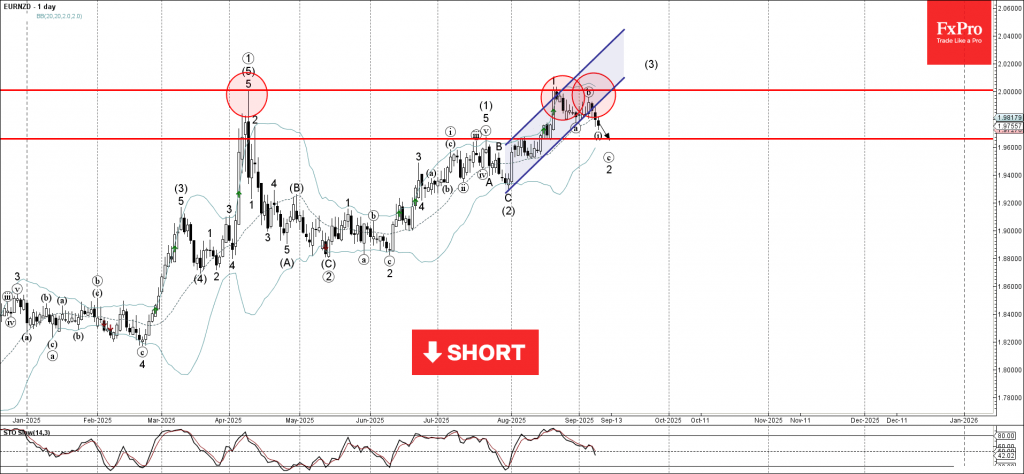

EURNZD Wave Analysis

EURNZD: ⬇️ Sell

- EURNZD broke daily up channel

- Likely to fall to support level 1.9660

EURNZD currency pair recently reversed down from the resistance area between the round resistance level 2.0000 (former powerful resistance from April) and the upper daily Bollinger Band.

The downward reversal from this resistance area started active short-term impulse wave c, which then broke the daily up channel from July.

EURNZD currency pair can be expected to fall toward the next support level 1.9660 (former resistance from July and the start of August).

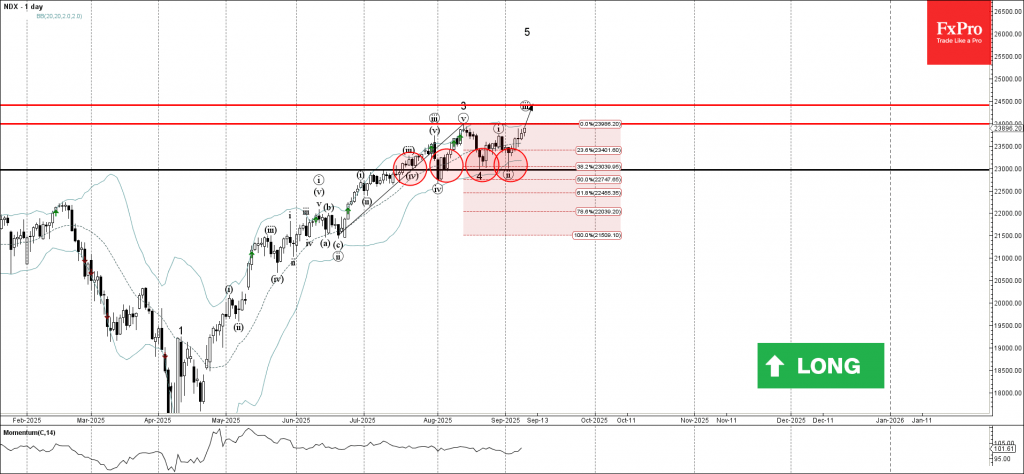

Nasdaq-100 Wave Analysis – 9 September 2025

Nasdaq-100: ⬆️ Buy

- Nasdaq-100 reversed from the support area

- Likely to rise to resistance level 24500.00

Nasdaq-100 index recently reversed up from the support area between the pivotal support level 23000.00 (which has been reversing the price from July), lower daily Bollinger Band and the 38.2% Fibonacci correction of the upward impulse from June.

The upward reversal from this support zone created the daily Japanese candlesticks reversal pattern Hammer – which started the active impulse wave iii.

Given the clear daily uptrend, Nasdaq-100 index can be expected to rise toward the next resistance level 24000.00 (top of wave 3), the breakout of which can lead to further gains toward 24500.00.