Sample Category Title

Sunset Market Commentary

Markets

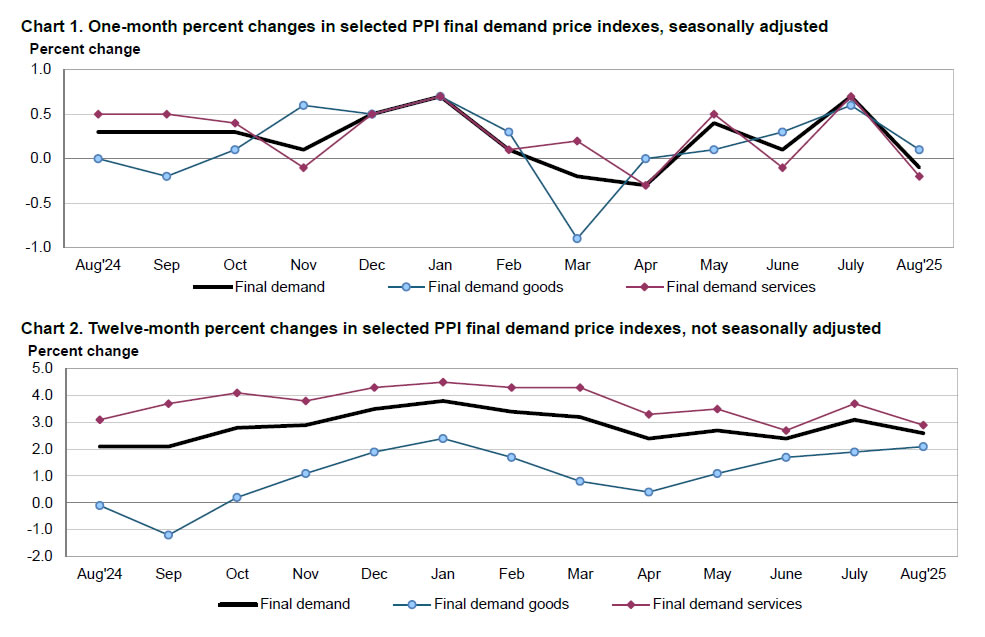

The BLS’s employment revision yesterday offered the final input from the labour market perspective for next week’s Fed policy meeting. The 911k downward adjustment for April 2024 through March 2025 was a historically high one but didn’t lure markets into adding to their Fed easing bets for 2025 - the opposite actually happened. It’s perhaps not that farfetched given that inflation has been reaccelerating since April to still be above the central bank’s 2% target. PPI numbers for August today addressed those concerns a bit. They unexpectedly printed a negative 0.1% m/m in the headline and core (ex. energy and food) gauge, missing the 0.3% estimate. The annualized figures slowed to 2.6% and 2.8% respectively, well below the 3.3% and 3.5% expected. A downward revision to July’s (though sizeable) PPI increase adds to the magnitude of the sub-consensus outcome. The supercore series (ex. food, trade and energy) matched the 0.3% m/m forecast (2.8% y/y). Crude food acted as a major drag, tumbling a whopping 13.2% on a monthly basis. Energy (-0.4% m/m) and services (trade in particular: -1.7%) weighed as well. The numbers raise the stakes for tomorrow’s consumer equivalent, for which a rise to 2.9% from 2.7% is expected, and offered markets a welcome distraction from an otherwise dull trading session today. US yields fell in a bull flattening move with net daily changes varying between -3.3 bps (2-yr) to -0.8 bps (30-yr). Money markets attach a slightly higher albeit still very low probability to an outsized cut (50 bps, 7%) by the Fed next week. US President Trump once again called for a “big” move minutes after the release. European rates left the intraday highs in sympathy and are now flat for the day. European stocks trade in the green but are underperforming US peers in the wake of the lower-than-expected PPIs. The US dollar loses some marginal ground. EUR/USD trades around 1.172, up from a 1.171 open. DXY is going nowhere close to but below 98. Oil prices are in a three-day winning streak (Brent 67$/b). Today’s move is possibly geopolitically inspired. Russian drones crossed Polish territory early this morning and were later downed by Nato-member warplanes. The military alliance discussed the incident after Poland invoked Article 4 of the treaty. Together with lower (US) bond yields, its keeping gold near record highs.

News & Views

Norwegian inflation fell by 0.6% M/M in August with the headline number accelerating as expected from 3.3% to 3.5% on an annual basis. Underlying core inflation fell less than hoped (-0.7% M/M vs -0.9% M/M) to stabilize at 3.1% Y/Y (vs 2.9% consensus). Details showed food and non-alcoholic beverages prices dropping by 1.8% M/M with furniture, household equipment and routine maintenance (-2.3% M/M) and transport (-1.5%) prices also dragging monthly prices down. Higher prices for housing, water, electricity, gas and other fuels (1.2% M/M), restaurant and hotels (+0.3% M/M) and clothing and footwear (0.3%) couldn’t make up for that. Today’s numbers create some doubt on the outcome of next week’s Norges Bank policy meeting. They lowered the key rate a first time in June (4.5% to 4.25%) with a cautious easing bias for the remainder of the year (4% policy rate by year-end). The market implied probability of a 25 bps rate cut next week fell from 82% to 68%. The NOK swap rate curve bear steepens with yields up to 6.8 bps higher at the front end (2-yr). The NOK profits with EUR/NOK (11.61) touching its lowest level since mid-June.

The Czech National Bank commented on August inflation numbers which were confirmed today at 0.1% M/M and 2.5% Y/Y which was slightly below the central bank’s own forecast (2.7%). Core inflation edged up to 2.8% Y/Y, driven by goods prices. Inflation in market services remained unchanged but elevated (4.4% Y/Y). Core inflation was affected by rising housing costs this year. In August, year-on-year growth in imputed rent remained at 4.9% for the third time in a row. The CNB expects inflation to remain close to recent values for the rest of the year. Given the still elevated inflation and its unfavourable structure, there are still reasons for a cautious monetary policy approach. CNB board member Seidler today argued in favour of keeping Czech rates unchanged for now. Vice-governor Zamrazilova did the same earlier this week. The Czech koruna today nevertheless falls prey to some profit taking with EUR/CZK bouncing off its weakest level since the end of 2023 (24.30) to 24.39.

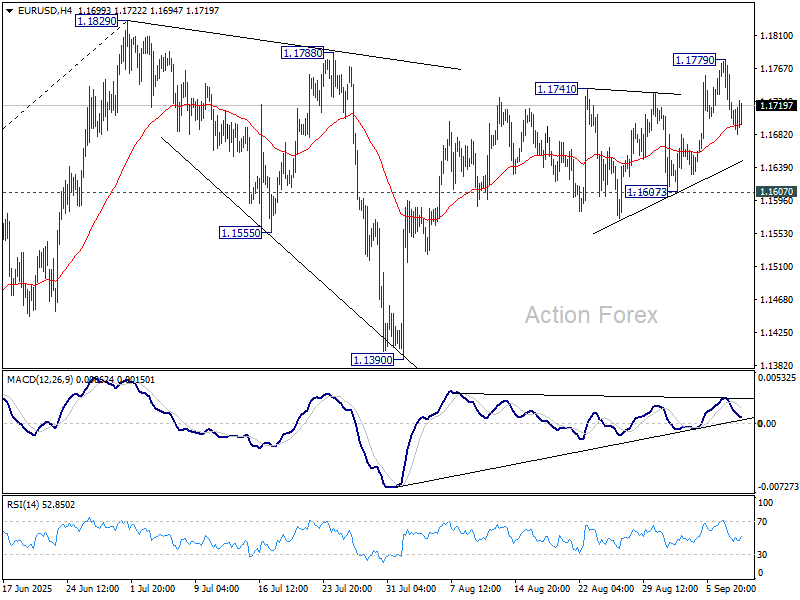

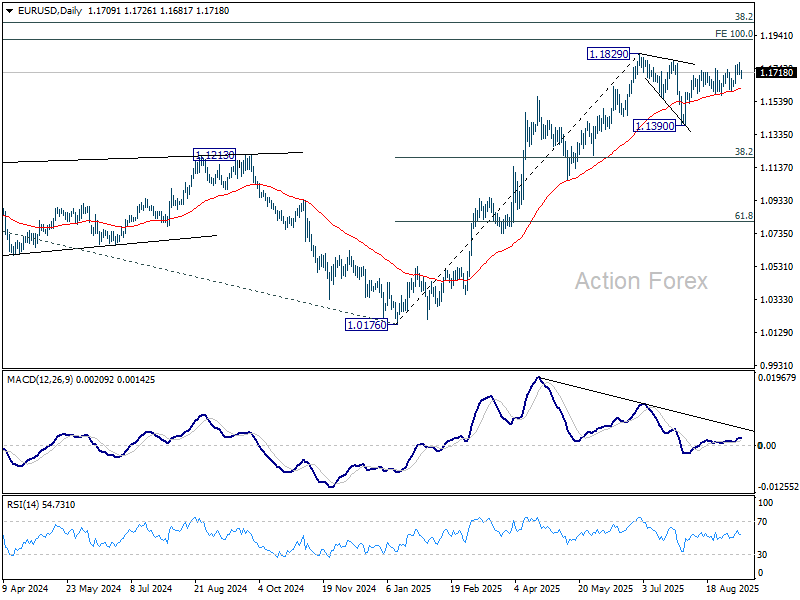

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1681; (P) 1.1731; (R1) 1.1757; More...

Intraday bias in EUR/USD remains neutral for consolidations below 1.1779 temporary top. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

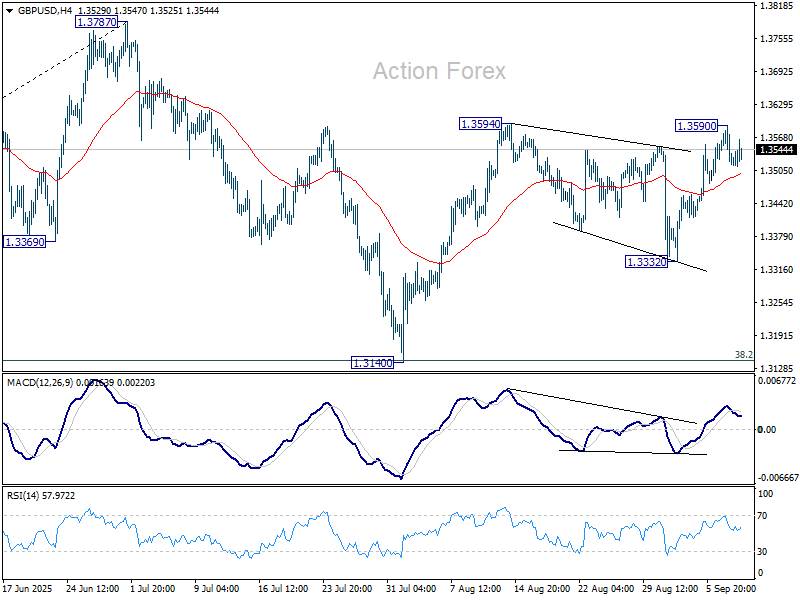

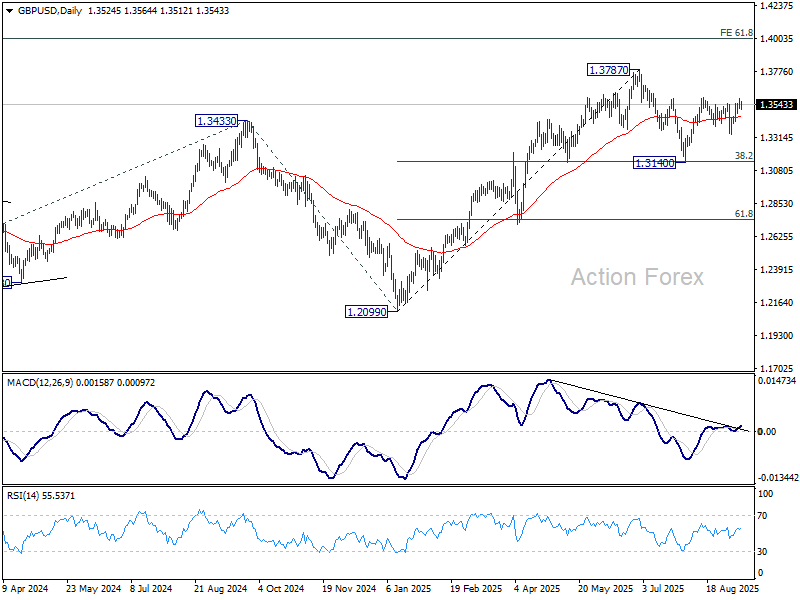

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3500; (P) 1.3545; (R1) 1.3573; More...

Intraday bias in GBP/USD remains neutral and some more consolidations could be seen below 1.3590 temporary top. Further rise is expected with 1.3332 support intact. Firm break of 1.3594 will resume the rally from 1.3140 and target a retest on 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

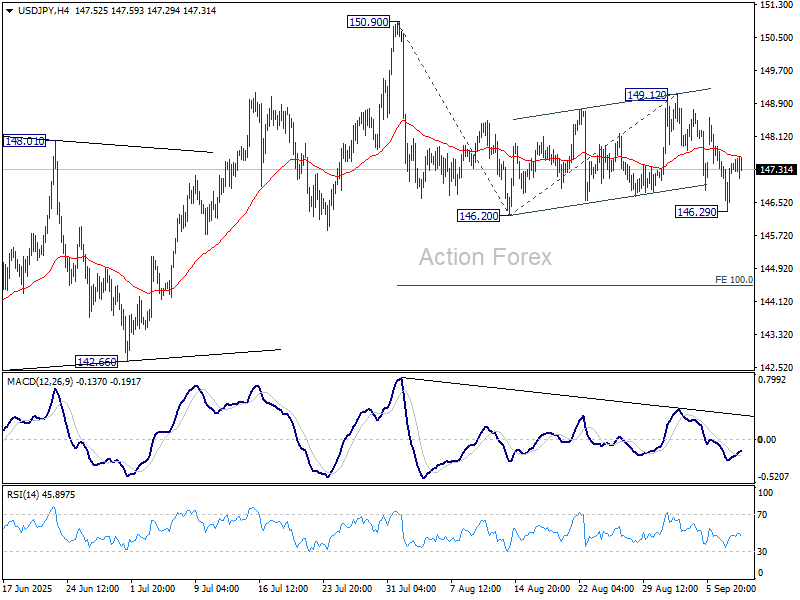

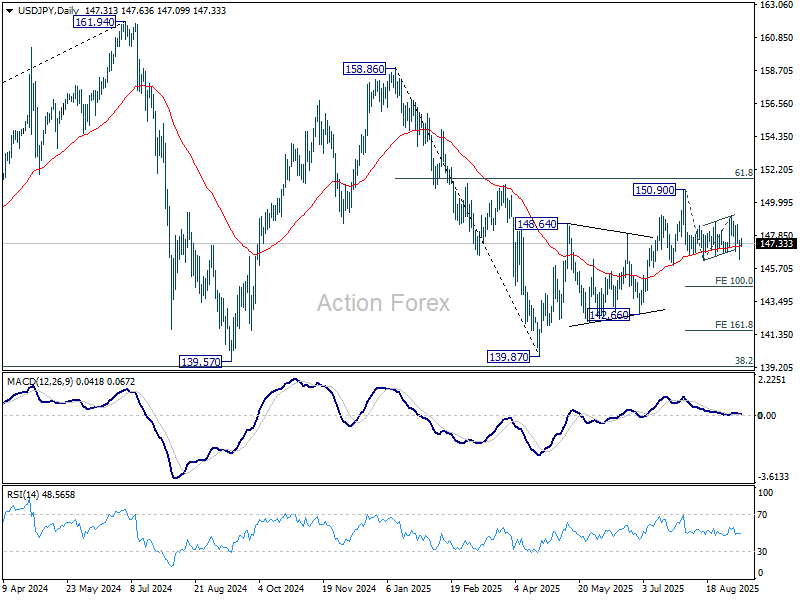

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.62; (P) 147.10; (R1) 147.90; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen above 146.29 temporary low. Risk will stay on the upside as long as 149.12 resistance holds. Firm break of 146.20 will target 100% projection of 150.90 to 146.20 from 149.12 at 144.42. Also, sustained trading below 55 D EMA (now at 147.15) will argue that whole rebound from 139.87 has completed with three waves up to 150.90.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7934; (P) 0.7958; (R1) 0.7999; More….

Intraday bias in USD/CHF remains neutral for the moment and some more consolidations could be seen above 0.7914 temporary low. But risk will stay on the downside as long as 0.8071 resistance holds. Below 0.7914 will bring retest of 0.7871 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

Dollar Dips Slightly on Softer PPI, Bigger Bets Deferred Until CPI

Dollar dipped briefly in early American session while U.S. futures rebounded after producer price data showed cost pressures easing modestly. The report emboldened bets on further Fed easing, with odds of a 50bps cut next week edging up to 10% and expectations for a back-to-back October move climbing back toward 80%.

Still, traders appeared reluctant to commit heavily ahead of Thursday’s CPI release. The inflation print will be decisive for the September FOMC outcome and the broader policy path. For now, the market is content to price in a dovish tilt without taking on larger risk positions.

Judging from today’s price action, however, Dollar looks vulnerable. Any signs of softer-than-expected inflation could accelerate selling, leaving the greenback under renewed pressure across major pairs. The CPI report could therefore act as a tipping point for markets already primed for easing.

Overall in the currency markets today, Aussie led gains, boosted by optimism that Fed easing will give China’s PBoC room to cut rates and stimulate its sluggish economy. Kiwi followed closely, with Sterling also firmer, reflecting a broader risk-on tone.

On the weaker side, Loonie was the worst performer, trailed by Euro and Swiss Franc. The common currency’s attention is fixed on Thursday’s ECB decision, where policymakers are expected to stand pat. Any signal of a prolonged pause could give Euro some breathing space. Dollar and Yen traded mixed in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.17%. CAC is up 0.74%. UK 10-year yield is up 0.016 at 4.64. Germany 10-year yield is up 0.01 at 2.67. Earlier in Asia, Nikkei rose 0.87%. Hong Kong HSI rose 1.01%. China Shanghai SSE rose 0.13%. Singapore Strait Times rose 1.14%. Japan 10-year JGB yield rose 0.003 to 1.568.

U.S. PPI falls -0.1% mom in August, annual rate cools to 2.6% yoy

U.S. producer prices unexpectedly fell in August, with PPI slipping -0.1% mom versus expectations of a 0.3% mom gain. The decline was driven by a -0.2% mom drop in final demand services, while goods prices edged higher by 0.1% mom.

On a year-over-year basis, PPI slowed sharply to 2.6% yoy from yoy 3.3% in July, undershooting forecasts of 3.3% yoy and signaling easing price pressures at the factory gate. The slowdown will be welcomed by markets seeking evidence that inflationary pressures are moderating.

However, underlying measures stayed firmer. Core PPI, excluding food, energy, and trade services, rose 0.3% mom, a fourth straight month of increase, leaving the annual rate at 2.8% yoy — the fastest since March.

China CPI falls -0.4% yoy, core inflation hits 2-1/2 year high

China’s consumer prices slipped deeper into deflation in August, with CPI down -0.4% yoy after July’s flat reading, worse than expectations of -0.2% yoy and the weakest in six months. Food prices were the main drag, falling -4.3% yoy versus -1.6% yoy previously. On a monthly basis, CPI was unchanged, undershooting forecasts for a small 0.1% mom rise.

At the same time, core inflation showed signs of life, rising 0.9% yoy in August compared with 0.8% yoy in July — the fastest pace in two and a half years. The pickup suggests underlying demand in services and other non-food sectors is holding up better than headline numbers imply, even as consumers face falling food costs.

Producer prices continued to contract, though at a slower pace. PPI dropped -2.9% yoy, in line with expectations and an improvement from -3.6% yoy in July. The figures highlight China’s ongoing struggle with persistent factory-gate deflation, which has now lasted nearly three years.

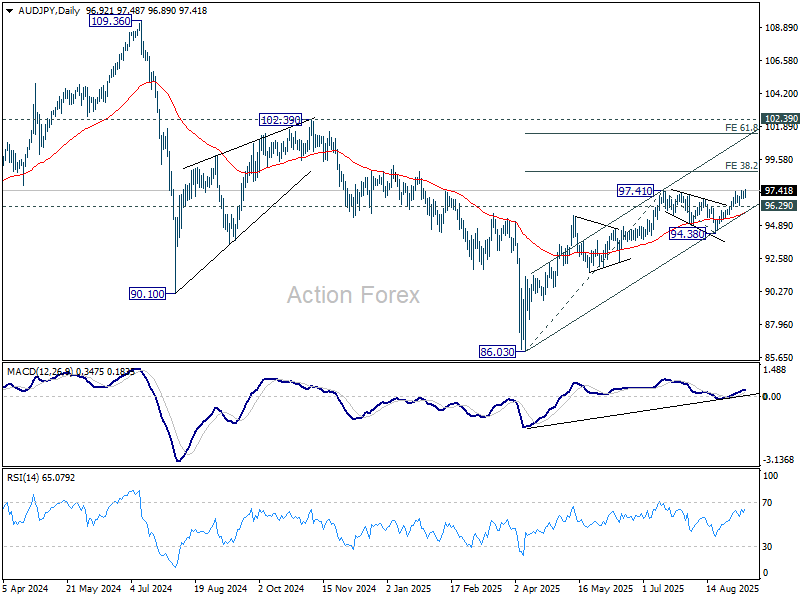

Aussie Strength Builds in Crosses as China CPI Opens Door to Stimulus

Australian Dollar jumped further today, particularly in cross rates, as risk appetite in China improved. The move was fueled by gains in Chinese equities after inflation data suggested room for further stimulus, with Hong Kong’s Hang Seng Index climbing to a four-year high.

The -0.4% yoy decline in China's highlighted weak domestic demand and strengthened the case for the PBoC to cut borrowing costs. Producer prices also stayed in deflation, highlighting the pressures on manufacturers. More importantly, the Fed’s shift toward easing to reduce pressure on Yuan exchange rate, giving the PBoC greater latitude to stimulate without sparking destabilizing outflows.

Technically, Hong Kong’s HSI remains in a steady uptrend, with D MACD showing signs of momentum returning. For now, outlook will stay bullish as long as 25013.26 support holds. Current up trend should be on track to 161.8% projection of 14597.31 to 22770.85 from 14794.16 at 27905.69, which is close to 28000 psychological level.

AUD/JPY is now pressing 97.41 key resistance. Further rise is expected as long as 96.29 support holds. Sustained trading above 97.41 will pave the way to 38.2% projection of 86.03 to 97.41 from 94.38 at 98.72, and then 61.8% projection at 101.41.

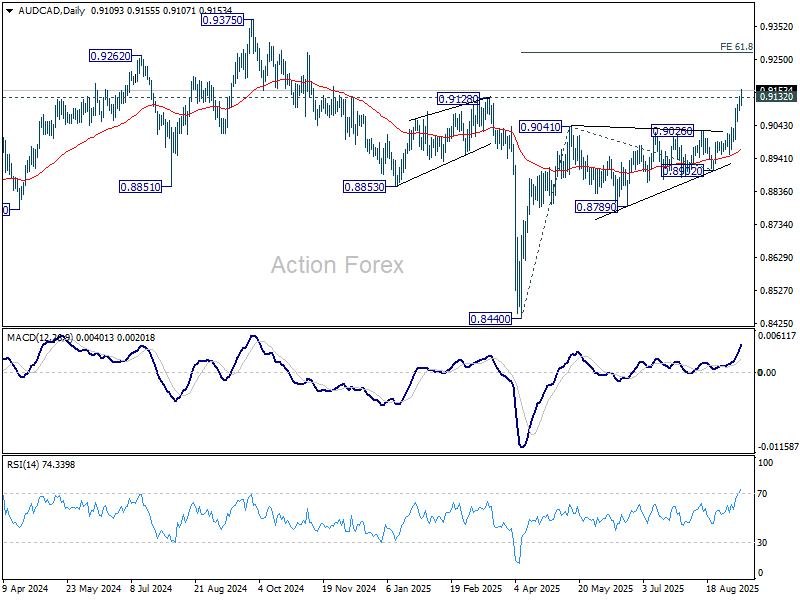

AUD/CAD's rally continues today and broke through 0.9218 structural resistance. Current up trend should target 61.8% projection of 0.8440 to 0.9041 from 0.8902 at 0.9273.

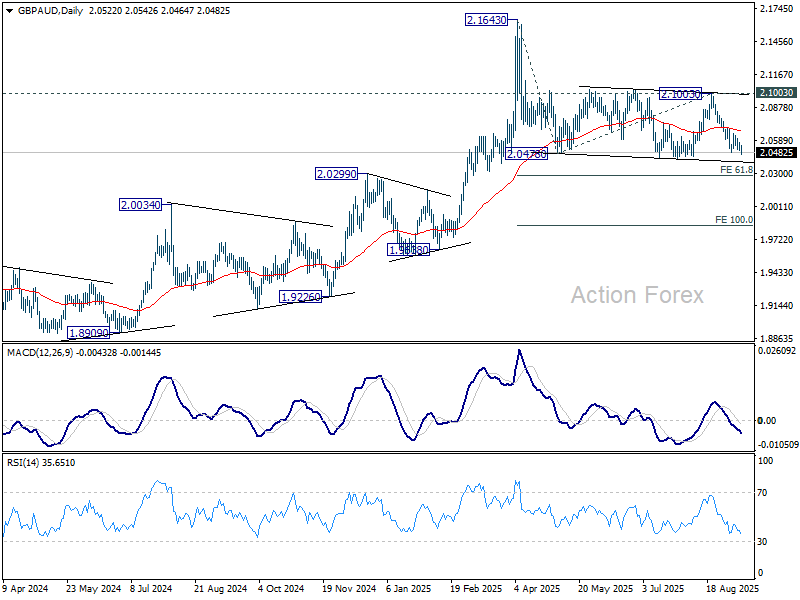

GBP/AUD also edges lower today and near term outlook remains bearish for 61.8% projection of 2.1643 to 2.0478 from 2.1003 at 2.0283 next.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7934; (P) 0.7958; (R1) 0.7999; More….

Intraday bias in USD/CHF remains neutral for the moment and some more consolidations could be seen above 0.7914 temporary low. But risk will stay on the downside as long as 0.8071 resistance holds. Below 0.7914 will bring retest of 0.7871 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

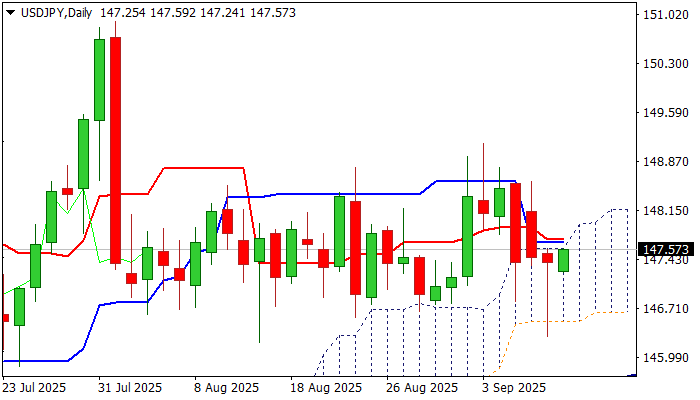

USD/JPY: Recovery Attacks Key Barriers, Bear-Trap Underpins the Action

USDJPY regained traction on Wednesday, after spiking to the lowest in nearly one month on Tuesday.

Strong downside rejection formed a bear trap pattern (under daily cloud base), as well as Hammer candle (Tuesday), adding to developing positive signals.

Strong resistances at 147.60 zone (daily cloud top / converged 10/20 DMA’s) are under pressure, with sustained break here to strengthen near-term structure for fresh recovery towards targets at 148.05/46 (Fibo) and key barrier at 148.70 (200DMA).

Bullish near-term bias expected while the price holds above 55DMA (147.18), but caution is required as daily studies are bearishly aligned (daily RSI below 50 / 14-d momentum in negative territory).

Thursday’s release of US August inflation report will be in focus for the final signals ahead of FOMC policy meeting next week.

Res: 147.72; 148.05 148.46; 148.70.

Sup: 147.39; 147.18;146.70; 146.30.

U.S. PPI falls -0.1% mom in August, annual rate cools to 2.6% yoy

U.S. producer prices unexpectedly fell in August, with PPI slipping -0.1% mom versus expectations of a 0.3% mom gain. The decline was driven by a -0.2% mom drop in final demand services, while goods prices edged higher by 0.1% mom.

On a year-over-year basis, PPI slowed sharply to 2.6% yoy from yoy 3.3% in July, undershooting forecasts of 3.3% yoy and signaling easing price pressures at the factory gate. The slowdown will be welcomed by markets seeking evidence that inflationary pressures are moderating.

However, underlying measures stayed firmer. Core PPI, excluding food, energy, and trade services, rose 0.3% mom, a fourth straight month of increase, leaving the annual rate at 2.8% yoy — the fastest since March.

Aussie Strength Builds in Crosses as China CPI Opens Door to Stimulus

Australian Dollar jumped further today, particularly in cross rates, as risk appetite in China improved. The move was fueled by gains in Chinese equities after inflation data suggested room for further stimulus, with Hong Kong’s Hang Seng Index climbing to a four-year high.

The -0.4% yoy decline in China's highlighted weak domestic demand and strengthened the case for the PBoC to cut borrowing costs. Producer prices also stayed in deflation, highlighting the pressures on manufacturers. More importantly, the Fed’s shift toward easing to reduce pressure on Yuan exchange rate, giving the PBoC greater latitude to stimulate without sparking destabilizing outflows.

Technically, Hong Kong’s HSI remains in a steady uptrend, with D MACD showing signs of momentum returning. For now, outlook will stay bullish as long as 25013.26 support holds. Current up trend should be on track to 161.8% projection of 14597.31 to 22770.85 from 14794.16 at 27905.69, which is close to 28000 psychological level.

AUD/JPY is now pressing 97.41 key resistance. Further rise is expected as long as 96.29 support holds. Sustained trading above 97.41 will pave the way to 38.2% projection of 86.03 to 97.41 from 94.38 at 98.72, and then 61.8% projection at 101.41.

AUD/CAD's rally continues today and broke through 0.9218 structural resistance. Current up trend should target 61.8% projection of 0.8440 to 0.9041 from 0.8902 at 0.9273.

GBP/AUD also edges lower today and near term outlook remains bearish for 61.8% projection of 2.1643 to 2.0478 from 2.1003 at 2.0283 next.

Aussie Eyes Australian Inflation Expectations, Aussie Higher

The Australian dollar continues to hover around the 0.66 level and close to three-week highs. In the European session, AUD/USD is trading at 0.6604, up 0.30% on the day.

Inflation expectations expected to remain at 3.9%

The Reserve Bank of Australia will be keeping a close eye on Thursday's consumer inflation expectations, which is expected to remain unchanged in September at 3.9%. Inflation expectations fell in August to 3.9% from 4.7%, the lowest level since March.

With inflation largely under control, the Reserve Bank has continued its easing cycle, lowering rates in August to 3.6%, the lowest level since April 2023. At the meeting, the RBA signaled that it would continue to cut rates as the inflation was easing and the labor market had cooled.

China's inflation points lower

China continues to grapple with deflation. Consumer inflation in August declined 0.4% y/y, down from 0% in July and lower than the market estimate of -0.2%. Monthly, CPI was flat, down from 0.4% in July and below the market estimate of 0.1%. The Producer Price Index fell 2.9% y/y, following a 3.6% decline and in line with the market estimate.

Deflation in China reflects decreased demand, which could spell trouble for Australia, as China is its largest trading partner.

The Federal Reserve is widely expected to lower rates at next week's meeting, even though inflation is around 3%, above the Fed's target of 2%. The US releases August consumer inflation on Thursday, with headline CPI expected to rise to 2.9% from 2.7% and the core rate projected to remain unchanged at 3.1%. The inflation report is unlikely to change any minds at the Fed about a September cut, but could change market expectations about one further rate cut before the end of the year.

AUD/USD Technical

- AUD/USD has pushed above resistance at 0.6590 and is testing 0.6610. Next, there is resistance at 0.6635

- 0.6570 and 0.6555 are the next support levels

AUDUSD 1-Day Chart, September 9, 2025