Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.62; (P) 147.60; (R1) 148.37; More...

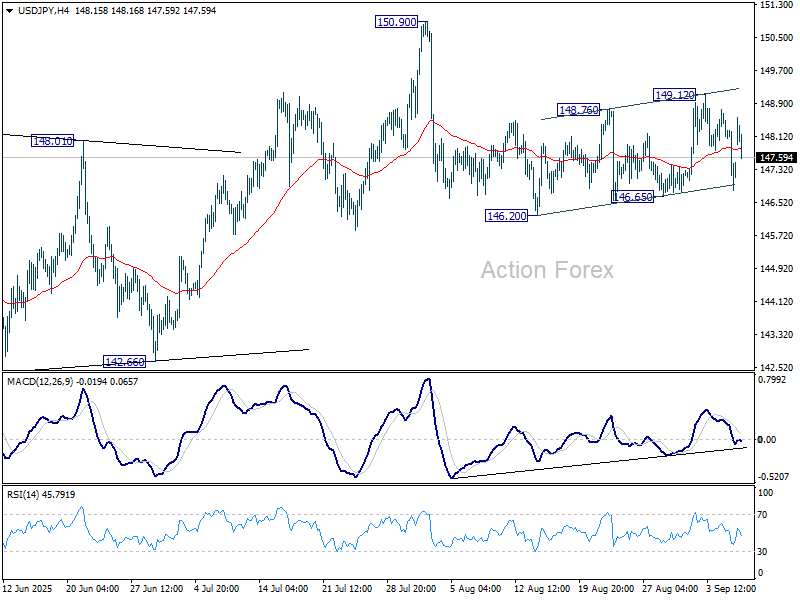

USD/JPY rebounded today as range trading continues and intraday bias stays neutral. On the downside, break of 146.65 will suggest that fall from 150.90 is resuming. More importantly, sustained trading below 55 D EMA (now at 147.15) will argue that whole rebound from 139.87 has completed with three waves up to 150.90. Deeper decline should then be seen to 142.66 support next. However, break of 149.12 will turn bias back to the upside for retesting 150.90.

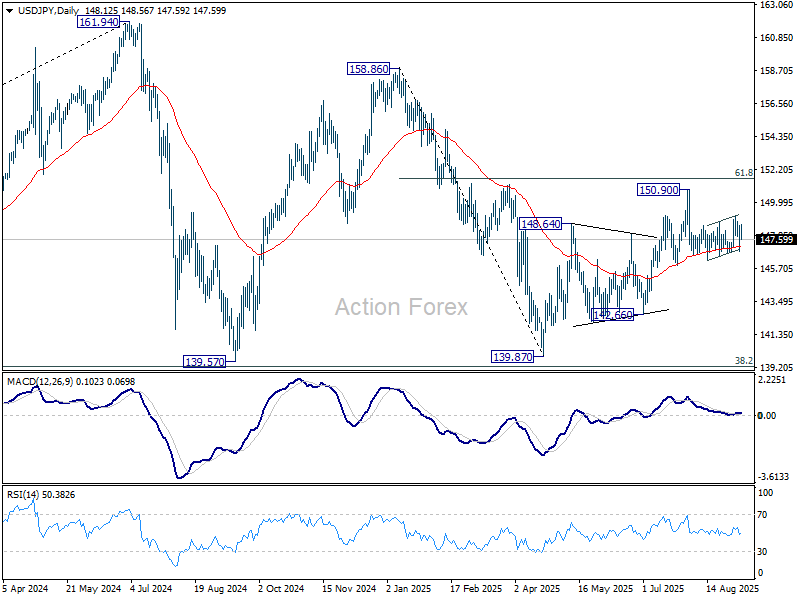

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3436; (P) 1.3495; (R1) 1.3568; More...

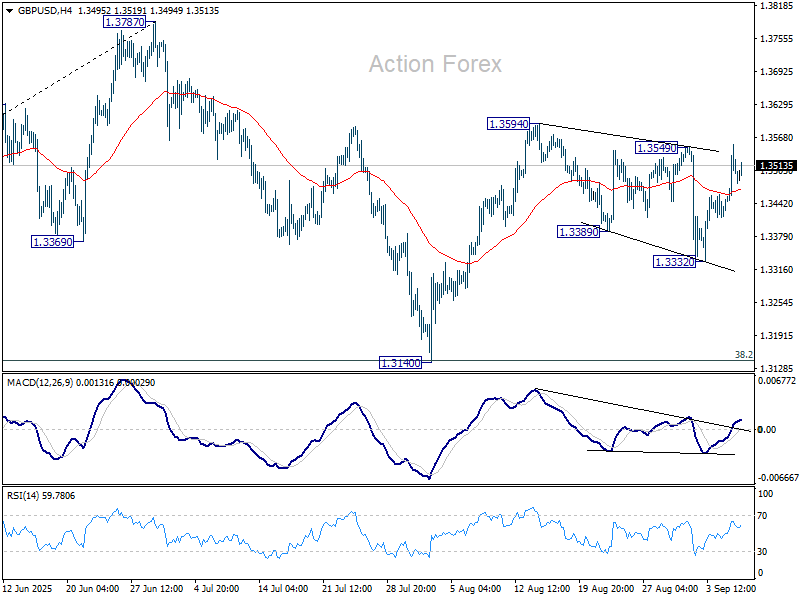

Intraday bias in GBP/USD stays on the upside for the moment. Rise from 1.3140 should be ready to resume. Firm break of 1.3594 resistance will confirm and target a retest on 1.3787 high. For now, risk will stay on the upside as long as 1.3332 support holds, in case of retreat.

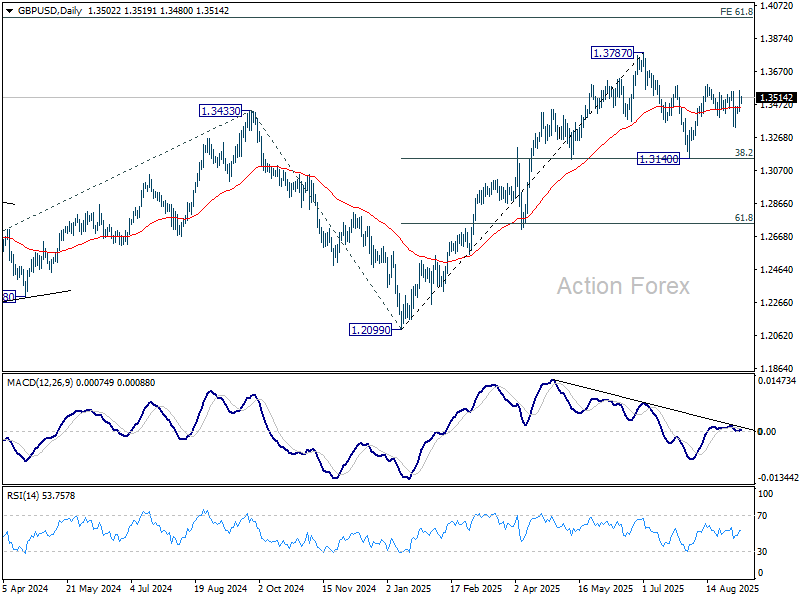

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7936; (P) 0.8000; (R1) 0.8043; More….

Intraday bias in USD/CHF remains on the downside for the moment. Corrective rebound from 0.7871 should have completed with three waves up to 0.8170. Deeper fall should be seen to 0.7910 support first, and then 0.7871 low. For now, risk will stay on the downside as long as 0.8071 resistance holds, in case of recovery.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

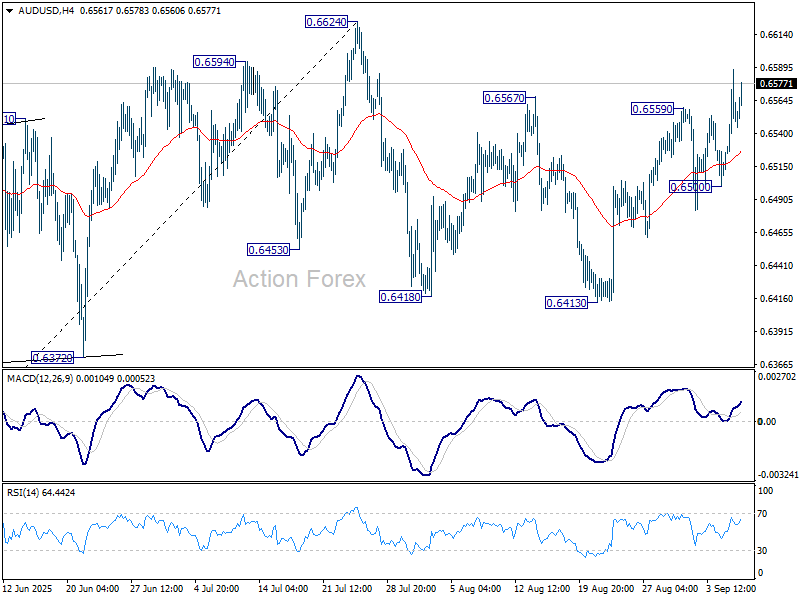

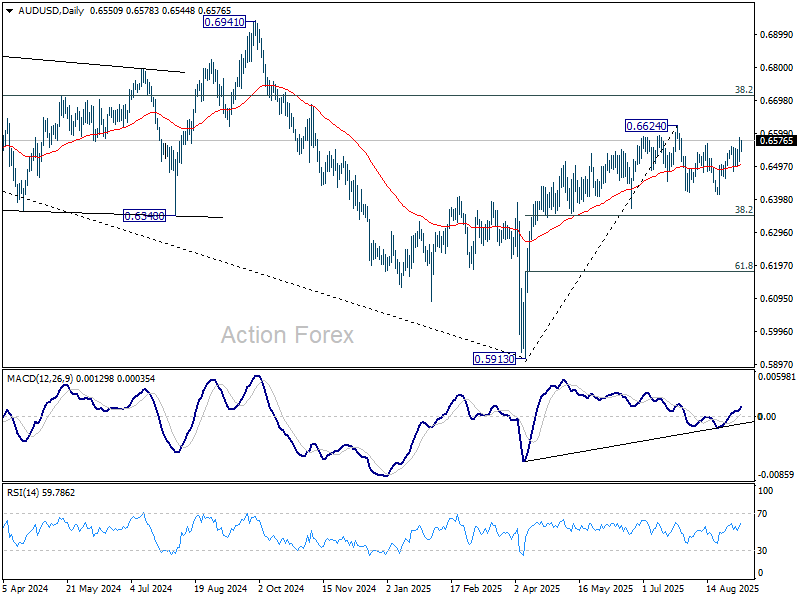

AUD/USD Daily Report

Daily Pivots: (S1) 0.6512; (P) 0.6551; (R1) 0.6594; More...

Intraday bias in AUD/USD stays on the upside and further rise should be seen to retest 0.6624 high. Firm break there will resume larger rally from 0.5913 to 0.6713 fibonacci level. For now, risk will stay on the upside as long as 0.6500 support holds, in case of retreat.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

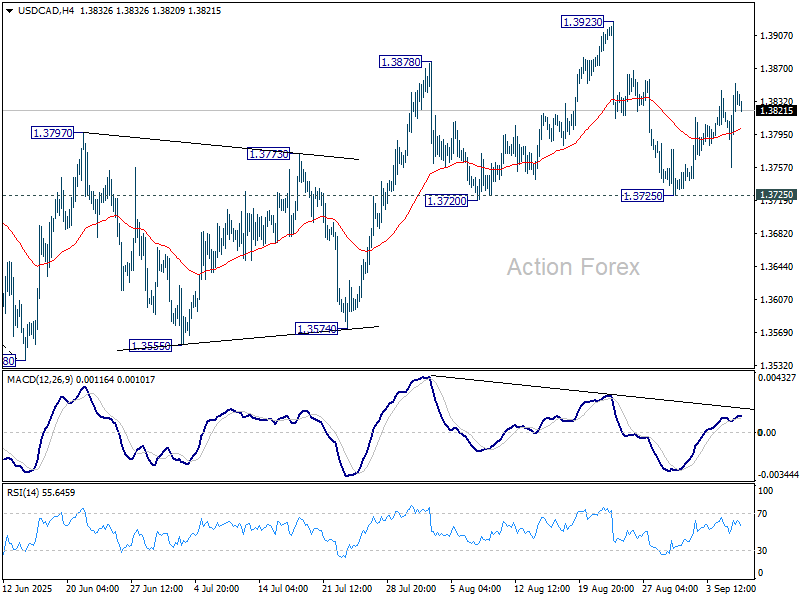

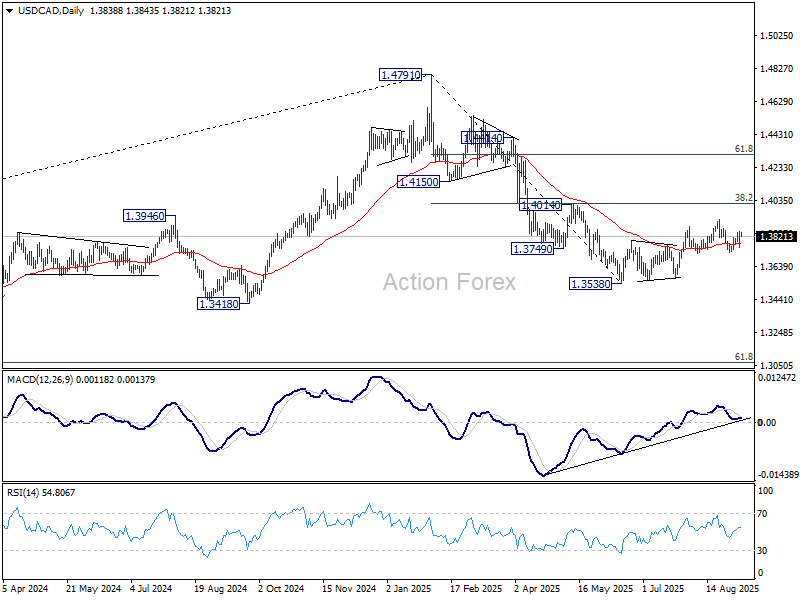

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3774; (P) 1.3814; (R1) 1.3869; More...

Intraday bias in USD/CAD remains on the upside at this point. Pullback from 1.3923 could have completed at 1.3725 already, and corrective rebound from 1.3538 is possibly resuming. Further rise should be seen to retest 1.3923 first. For now, risk will stay on the upside as long as 1.3725 support holds, in case of retreat.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

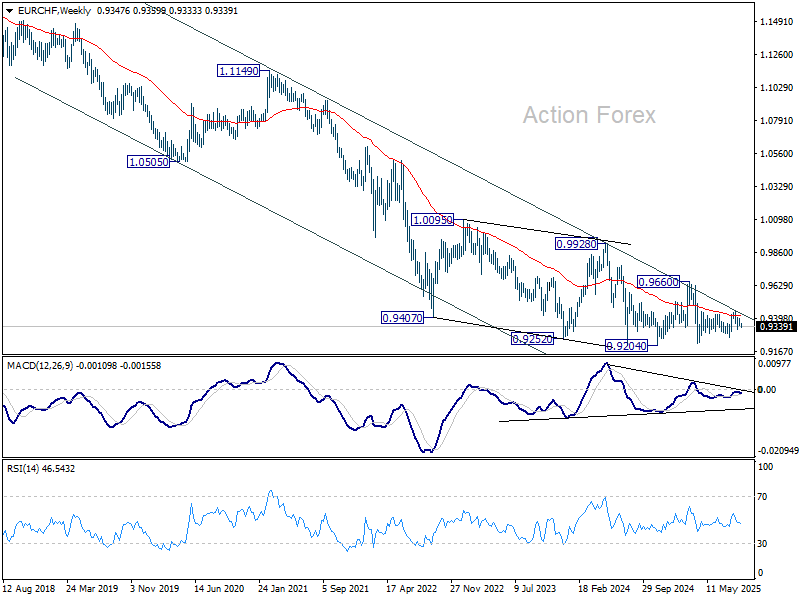

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9334; (P) 0.9366; (R1) 0.9381; More....

Intraday bias in EUR/CHF remains on the downside for 0.9317 support. Overall outlook is unchanged that corrective pattern from 0.9218 might have completed with three waves up to 0.9452 already. Break of 0.9317 will solidify this bearish case and target 0.9265 support, and then 0.9204 low. For now, risk will stay on the downside as long as 0.9394 resistance holds, in case of recovery.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

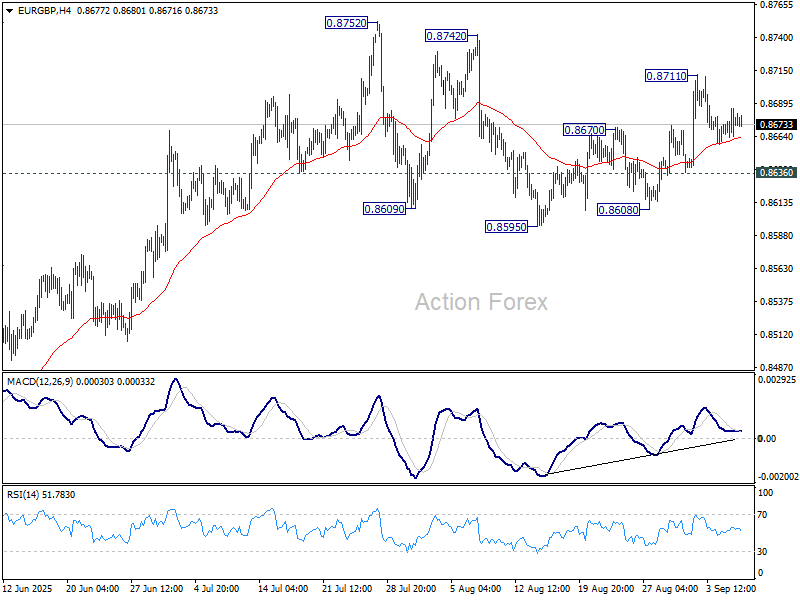

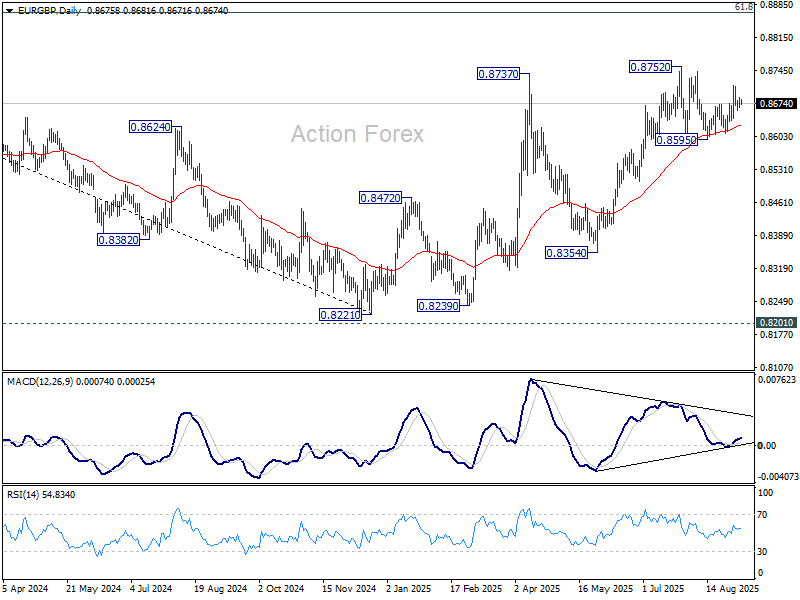

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8664; (P) 0.8675; (R1) 0.8686; More...

Intraday bias in EUR/GBP stays neutral and further rise is in favor with 0.8636 minor support intact. On the upside above 0.8711 will bring retest of 0.8752 high. However, break of 0.8636 will extend the pattern from 0.88752 with another falling leg, and target 0.8959 support.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8519) will argue that the pattern has completed and bring retest of 0.8221 low.

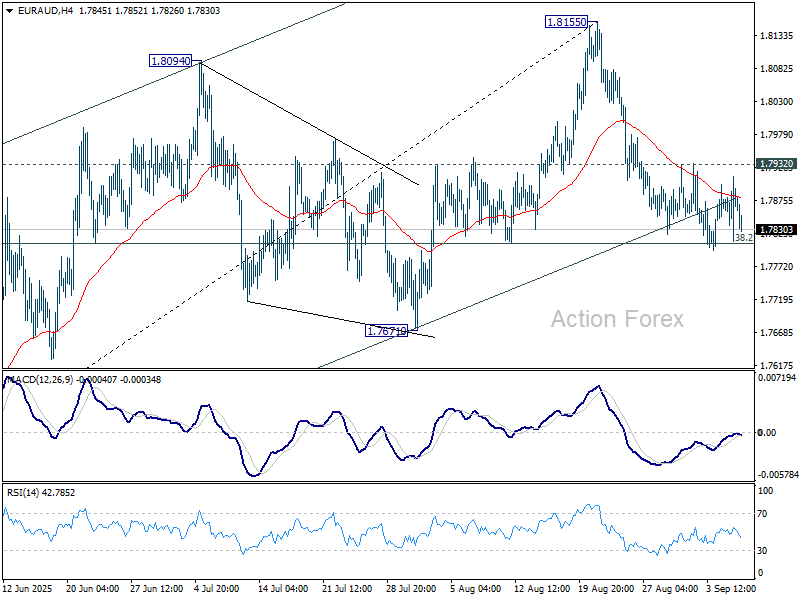

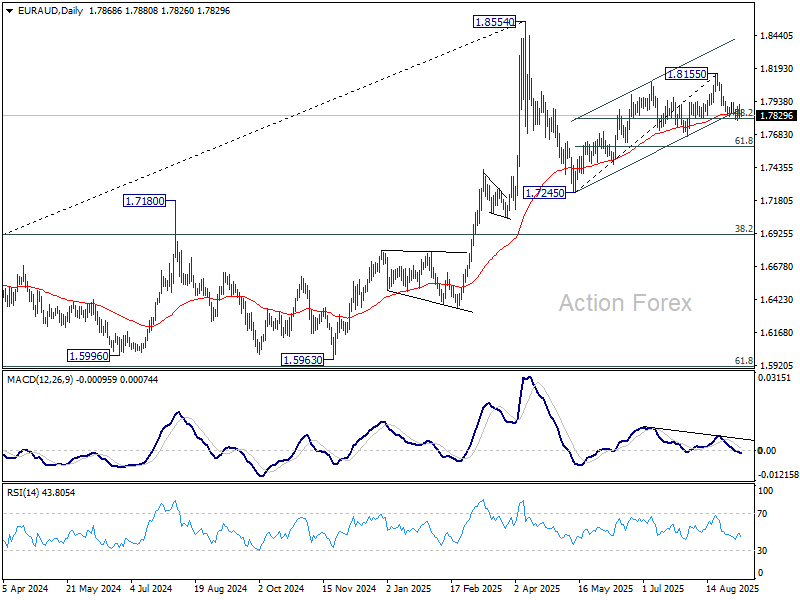

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7819; (P) 1.7866; (R1) 1.7919; More...

Intraday bias in EUR/AUD stays neutral and further decline is expected with 1.7932 resistance intact. On the downside, sustained trading below 38.2% retracement of 1.7245 to 1.8155 at 1.7807 should confirm that whole rise from 1.7245 has completed at 1.8155. Corrective pattern from 1.8554 should then be in its third leg. Further decline should be seen to 61.8% retracement at 1.7593. On the upside, break of 1.7932 resistance will retain near term bullishness and bring retest of 1.8155 resistance instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

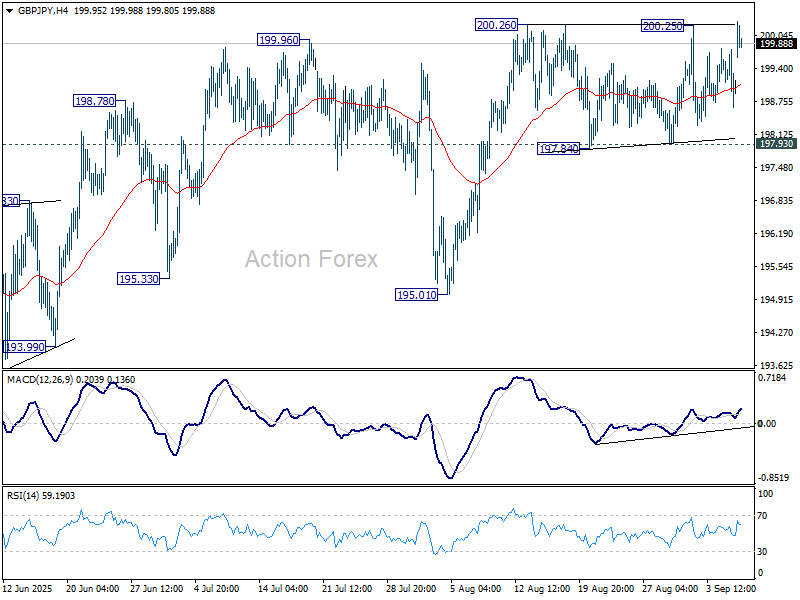

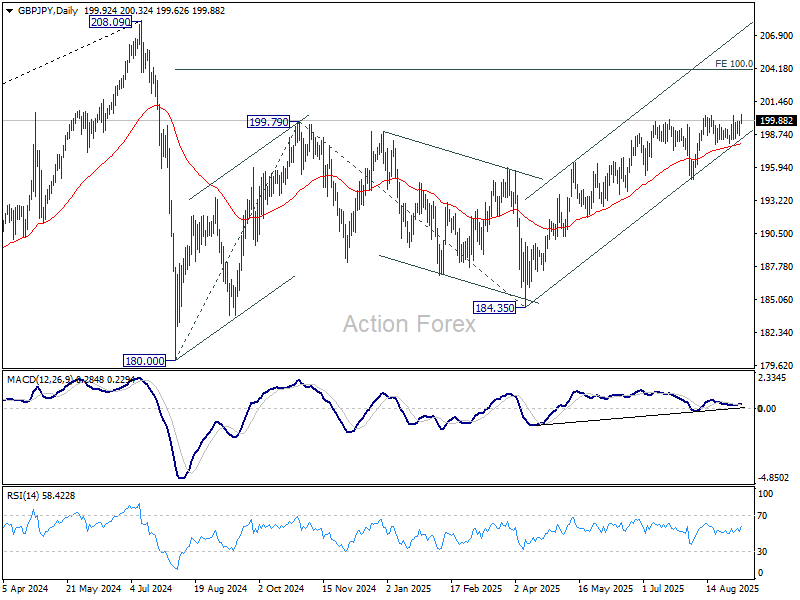

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.60; (P) 199.20; (R1) 199.73; More...

Intraday bias in GBP/JPY remains neutral at this point. Further rise is expected as long as 197.93 support holds. Firm break of 200.26 resistance will resume the rally from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14. On the downside, however, break of 197.93 support will turn bias to the downside for 195.01 support next.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

More Rate Cuts, More OPEC Barrels, More Political Uncertainty

22,000. That’s how many jobs the US economy added last month. A meagre 22K new nonfarm jobs – far weaker than analysts expected. Prior months’ revisions even showed the US economy lost jobs in June. The unemployment rate climbed to 4.3% as anticipated, while the participation rate ticked slightly higher – but not enough to improve the outlook. On the contrary, the US labour market is expected to deteriorate further amid mass deportations, restrained immigration and tariff-related uncertainty. Manufacturing shed another 12K jobs in July, suggesting the bleeding may continue before production and employment eventually shift back to the US – though many of those factory-floor jobs will likely be replaced by robots.

For now, the weakening jobs picture fuels expectations that the Federal Reserve (Fed) will not only cut rates in September but may have to cut more aggressively to shore up the labour market and compensate for what many see as a delayed response. To me – and many others – the Fed’s wait-and-see stance on inflation amid tariff disruptions made sense, as it was hard to paint a rosy picture for the US economy in such conditions. But if inflation doesn’t pick up – which is highly surprising – then yes, they’ll have to lower rates to avoid political and public backlash.

The US 2-year yield briefly slipped below 3.50% and is consolidating just above that level. The probability of rate cut in September surged to 100%, while Fed funds futures now price about a 10% chance of a 50bp move. Many now think the Fed could cut at all three remaining meetings this year and might even pause balance sheet tightening, depending on how quickly the labour market deteriorates and whether inflation ticks up – or doesn’t.

This week, we’ll shed some light on inflation dynamics. Last month, US CPI showed little consumer price pressure, while producer prices jumped – suggesting tariff costs were mostly absorbed by companies. We’ll see if some of those input costs are now passed on to consumers. On Wednesday, PPI is expected to show easing pressure in August. But on Thursday, CPI could warn that tariffs are starting to show up in headline inflation. A softer-than-expected print could temper Fed dovishness – but rate cuts are coming and risk assets will continue to enjoy the scent of cheaper money.

The S&P 500 hit a fresh record high after the payrolls data. The index closed Friday slightly lower, though more S&P 500 constituents ended the day in positive territory. The limited appetite could be blamed on Nvidia, which fell 2.7% after news that OpenAI will start mass producing AI chips with Broadcom. Capital rotated into Broadcom, which surged as much as 15% before paring gains to close up more than 9%.

In Asia, dovish Fed expectations boosted sentiment. The Nikkei jumped at the open, and European and US futures point to a positive start to the week. Chinese investors, however, were cautious on weakening exports and a smaller-than-expected August trade surplus.

Inside Japan: Prime Minister Shigeru Ishiba resigned over the weekend under mounting LDP pressure to step down. The news pushed the USDJPY lower at the open, on expectations that his successor will pursue looser fiscal policy and that political instability could delay a Bank of Japan (BoJ) hike. But the dark side is rising fiscal concerns: 20- and 30-year JGB yields reversed their recent decline and climbed higher on prospects of looser fiscal discipline.

Rising long-term yields are a quietly building risk for global risk appetite. In the US, the 30-year Treasury yield dropped below 4.80% after the weak jobs data, though risks remain.

Speaking of risks, French PM François Bayrou faces a make-or-break no-confidence vote today. His government is likely to collapse under opposition pressure, which could weigh on French stocks and bonds and cap euro gains into 1.18. Still, the dollar’s trajectory will ultimately decide whether the EURUSD deserves to reach 1.20. Net speculative positioning in the euro is strongly positive, meaning any adverse news could trigger a sharp correction.

In energy, US crude opened the week with a rebound after testing $62 per barrel support on Friday, just ahead of the OPEC meeting. OPEC announced supply increases of 137K barrels/day from October – which was below the previous moves, below expectations and flexible. That prompted some oil bears to take profit after last week’s 3.5% slide. Prices could correct further into the $65–66 range, which includes a key Fibonacci level as well as the 50- and 200-day moving averages. A breakout above would likely require fresh geopolitical tension.