Sample Category Title

US Job Growth Stalled in August

In focus today

In the euro area, focus turns to the no-confidence vote on French prime minister Bayrou. Bayrou and his government are expected to fall with both the far right and the left-wing parties vowing to vote against his minority administration. President Macron can then choose a new premier or call for a snap election. Macron has expressed a preference to avoid snap elections, with hints of forming a centrist government potentially led by a Socialist prime minister. However, the outlook for a new government remains highly uncertain. We expect political uncertainty in France to persist and view significant near-term improvements in public finances as unlikely.

We also receive the Sentix investor confidence indicator for September.

For the remainder of the week, the key focus is the US CPI release on Thursday, alongside the ECB meeting. Ahead of this, markets will watch the BLS preliminary annual benchmark NFP revision on Tuesday, followed by inflation data from China and Norway as well as US PPI on Wednesday. The week wraps up with the US Michigan survey on Friday.

Economic and market news

What happened overnight

In China, export growth slowed to 4.4% y/y in August (prior: 7.2%), the weakest pace since February and below expectations. While exports have outperformed in recent months, supported by stronger exports to Asia offsetting weaker shipments to the US, the latest data highlights emerging pressures. Import growth, though slightly improved in recent months, remains subdued, reflecting weak domestic demand. Imports rose 1.3% y/y (prior:4.1%), also missing forecasts. Read more in Research China - Domestic economy struggles while exports power ahead, 8 September.

What happened since Friday

In the US, the August jobs report came in very weak, with employment rising by 22k (cons: 75k). Revisions of previous months reveals 21k fewer jobs created. Manufacturing jobs declined further, with 38k fewer than prior to Trump's presidency. Unemployment increased to 4.3% from 4.2%, partly driven by a growing labour force. The data confirms the signs of a cooling labour market, though broader economic indicators remain stable. Read more in Research US - Tariff impact set to intensify towards winter, 5 September. The weak report strengthens the case for a rate cut in September, with inflation data and payroll revisions this week unlikely to change the outlook. Markets reacted by sending yields lower and weakening the dollar.

In the euro area, wage growth, measured as compensation per employee by the ECB, declined to 3.9% y/y in the second quarter of 2025 from 4.0% y/y in Q1. The data follows the higher-than-expected negotiated wage data and is markedly above the ECB's latest staff projection of 3.4% wage growth in Q2. Persistently elevated wage growth means services price pressures are likely to decline less slowly, which on the margin is hawkish.

In China, tensions with the EU escalated further as China on Friday announced anti-dumping tariffs on EU pork imports ranging from 15.6-62.4%. Although labelled as preliminary, the tariffs are likely to remain if the EU maintains higher tariffs on Chinese EVs. Although the overall economic impact on the EU is limited, the move will hurt EU pork exporters, as China accounts for half of their export market.

In Japan, after less than a year in the seat, PM Ishiba decided to step down yesterday ahead of a vote among party parliamentarians which would have likely forced him out. Ishiba's term has seen headwinds from the start, after a bold move to call a snap election after his election as Liberal Democratic Party (LDP) president backfired. Among candidates for the LDP-leadership are the fiercest competition from last year's elections. Sanae Takaichi, last year's runner-up and an Abenomics-loyalist, has previously been critical of BoJ hiking rates and will likely stand for a looser fiscal policy stance, but many other candidates will likely appear ahead of the election likely taking place in early October. The LDP is currently running an unusual minority government, and thus the new president will not necessarily become the new PM and might call for another snap election. Markets reacted by trading USD/JPY back above 148 levels and investors have increasingly retraced their bets on an October hike from the BoJ amid the political uncertainty.

In the commodity space, OPEC+ announced on Sunday a further oil production increase of 137,000 barrels per day from October. The move is driven by Saudi Arabia's push to regain market share. Although the increase is smaller than recent monthly hikes, it signals a shift towards prioritising market share over prices, amid expectations of weakening global demand in the months ahead.

Equities: Equities were mostly lower on Friday, but not as much as one might think after such a weak US job report. It was a tug of war between growth fears on one side, but lower bond yields on the other, leaving most main indexes only modestly lower but after rallying shortly upon the release. Stoxx 600 closed down -0.1%, S&P 500 -0.3% but Nasdaq was unchanged and interest rate sensitive small cap Russell 2000 even closed 0.5% higher. Sector performance painted a similar picture; yield sensitive real estate and high multiple stocks outperformed while growth sensitive value cyclicals like banks and industrials sold off. Similarly, falling yields and weakening growth tend to favour US equities over Europe. This was the case last week as well, marking another week of underperformance for Europe (-0.5pp). US and European futures are modestly higher this morning.

FI and FX: Friday's session was naturally dominated by the US NFP market reaction with the USD FX selling off and US FI rallying. EUR/USD initially traded as high as 1.1760 before erasing part of the gains now trading at around 1.1710 this morning. Overnight oil prices have traded higher, Brent crude hitting 66 USD/bbl, despite OPEC+ announcements on higher supplies. EUR/NOK trades around 11.75 while EUR/SEK is testing the 11.00 threshold which technically will be important for the near-term direction.

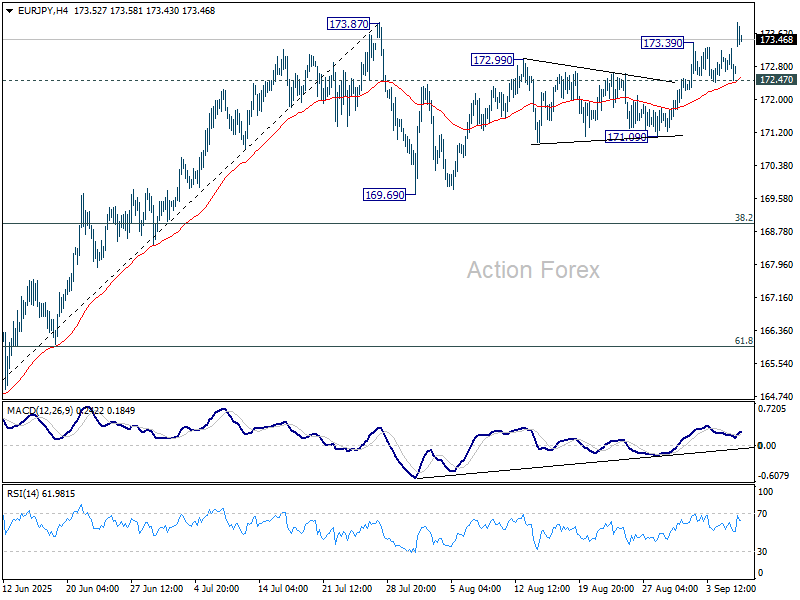

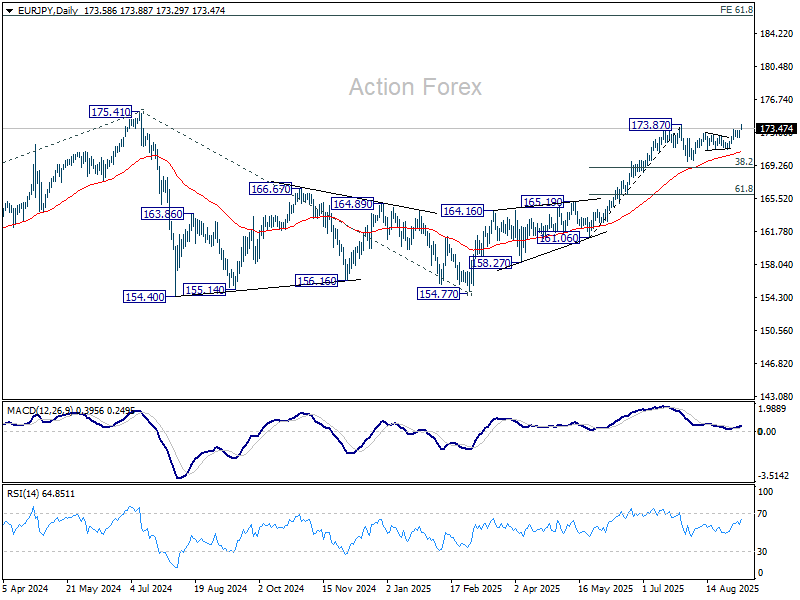

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.39; (P) 172.83; (R1) 173.17; More...

EUR/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Firm break of 173.87 will resume larger rise to retest 175.41 key resistance. On the downside, though, break of 172.47 support will extend the corrective pattern from 173.87 with another falling leg, before rally resumption.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, sustained break of 38.2% retracement of 161.06 to 173.87 at 168.97 will delay this bullish case, and probably extend the correction from 175.41 with another fall.

Yen Under Siege, Dollar Mixed Awaits CPI, Euro Steady Before ECB

A political shock in Tokyo is dominating global markets today, with Prime Minister Shigeru Ishiba announcing to step down over the weekend. The surprise resignation boosted risk appetite, propelling Nikkei. Yen, meanwhile, looks increasingly vulnerable. Last week’s dip in U.S. Treasury yields provided only temporary relief, and the currency has quickly reversed lower today. If optimism surrounding Japan’s leadership transition holds and the Nikkei breaks into record territory, Yen’s selloff could extend further in the days ahead.

For Dollar, the picture is mixed after last week’s sharp post-NFP selloff. Markets are now shifting attention to upcoming U.S. CPI and PPI reports, which will be critical in gauging the impact of August’s tariff escalation. After another weak jobs print, the inflation data will be crucial in determining whether the Fed has the flexibility to accelerate easing to support employment.

Euro trading has turned cautious as investors look toward Thursday’s ECB meeting, where policymakers are widely expected to leave the deposit rate unchanged at 2.00%. With inflation near target and unemployment still low, the ECB is seen maintaining its wait-and-see stance after delivering 200bps of cuts over the past year.

Across broader FX markets, the commodity bloc is outperforming, with Kiwi leading gains, followed by Aussie and Loonie. At the other end of the spectrum, Yen is the weakest, trailed by Sterling and Euro. Dollar and Swiss Franc are sitting in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 1.42%. Hong Kong HSI is up 0.53%. China Shanghai SSE is up 0.21%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is down -0.006 at 1.570.

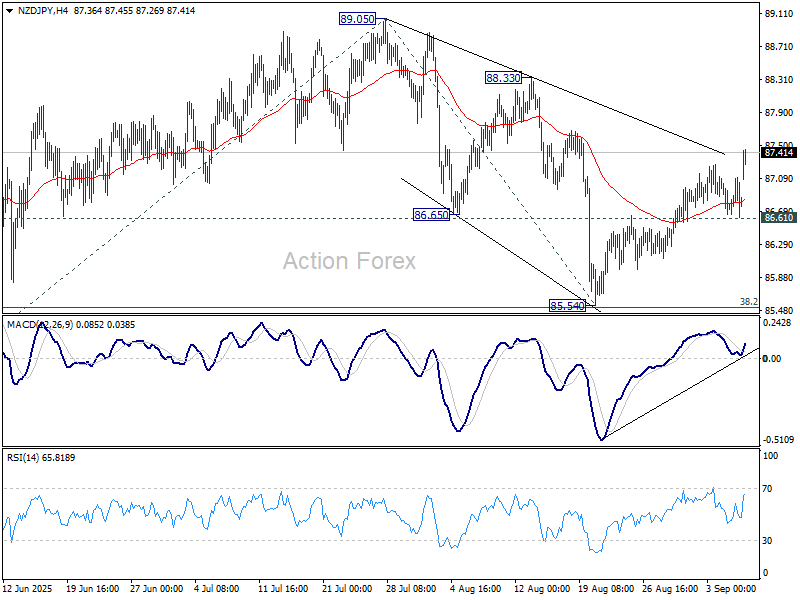

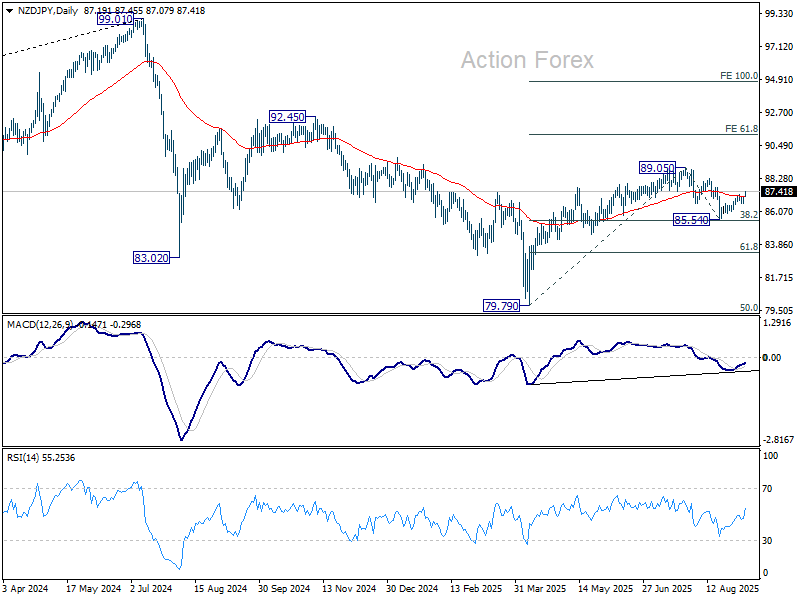

Japanese stocks soar towards record as Ishiba exit sparks optimism, NZD/JPY breaks higher

Japanese equities surged at the start of the week, with the Nikkei jumping more than 800 points in early trade and holding firm through the morning session. The index now sits within striking distance of a fresh record high. Risk-on appetite spilled over into currency markets, sending Yen sharply lower and leaving it vulnerable to further pressure if sentiment holds.

The trigger was the surprise resignation of Prime Minister Shigeru Ishiba over the weekend. Ishiba said the timing was deliberate, coming days after he secured the formal reduction of U.S. auto tariffs from 27.5% to 15%. “Now that negotiations on U.S. tariff measures have reached a conclusion, I believe this is the appropriate moment to resign,” he told reporters. His departure marks a sudden end to a premiership that began less than a year ago but was hampered by his coalition losing control of the lower house.

Nevertheless, Ishiba's exit opens the door to fresh leadership amid hopes that new faces could re-energize both the party and the electorate. Koizumi Shinjiro, agricultural minister and son of former prime minister Junichiro Koizumi, is widely viewed as a frontrunner, with his youth and broad appeal resonating with markets. Takaichi Sanae, closely aligned with the late Abe Shinzo, is also expected to be a serious contender. The leadership race is expected to fuel speculation of policy continuity combined with a push for fresh fiscal initiatives.

Investors are betting that the incoming administration will prioritize expansionary fiscal measures to secure opposition cooperation, given the LDP-led coalition still commands only a minority. Such expectations have buoyed equities further and reinforced the risk-on backdrop weighing on Yen.

Technically, NZD/JPY's rally from 85.54 resumed today. The break of 55 D EMA (now at 87.10) suggests that correction from 89.05 has completed after defending 38.2% retracement of 38.2% retracement of 79.79 to 89.05 at 85.51. Further rise is expected as long as 86.61 support holds. Break of 88.33 resistance will indicate that whole up trend from 79.79 is ready to resume through 89.05 short term top.

China exports growth slows in August, US flows collapse -33% yoy

China’s trade report for August showed growing pressure from U.S. tariffs. Exports rose 4.4% yoy, below expectations of 5.0% yoy and the slowest pace in six months. Shipments to the U.S. plunged -33.1% yoy, while flows to Southeast Asia jumped 22.5% yoy, suggesting exporters may be rerouting goods through regional partners to cushion losses.

Imports also disappointed, rising just 1.3% yoy versus forecasts of 4.1% yoy. Imports from the U.S. dropped -16% yoy, reflecting both weaker domestic demand and the bite of tariffs. Still, the overall trade surplus widened from USD 98.2B to USD 102.3 B, beating expectations of USD 99.4B.

While the surplus provides headline support, the underlying dynamics are fragile. U.S. President Donald Trump has already threatened a 40% penalty tariff on goods deemed to be transshipped from China, raising questions about how long exporters can sustain the ASEAN workaround. Besides, economists warn that once U.S. tariffs rise above 35%, they become prohibitively high for many Chinese manufacturers.

Washington and Beijing extended their tariff truce by 90 days on August 11, locking in 30% U.S. duties on Chinese goods and 10% Chinese tariffs on U.S. exports. But with no path yet beyond the pause, uncertainty lingers over whether China can maintain export growth as tariff pressure intensifies.

SNB Schlegel: Hurdle to reintroducing negative rates remains high

SNB President Martin Schlegel said the bar for reintroducing negative rates remains “high,” acknowledging the policy’s “undesirable side effects” for savers and pension funds. His comments reinforced market expectations that the SNB will hold its policy rate steady well into 2026, with inflation staying positive for a third month in August.

Switzerland faces new headwinds from U.S. tariffs of 39%, which threaten its export-heavy economy and raise risks of further disinflation. Schlegel cautioned that while some firms will be hit hard, the overall economic impact is not yet clear. “Many companies are investing less, which is having a negative impact on the economy,” he told Migros-Magazin.

ECB to Lean Back; Fed Awaits US CPI

The ECB is widely expected to keep its deposit rate unchanged at 2.00% this week, marking its second consecutive hold. After cutting by 200bps between June 2024 and June 2025, markets are increasingly convinced the easing cycle is over. With inflation at target and unemployment still at record lows, policymakers see little urgency to move further.

This backdrop has been described as a soft landing: inflation near 2% and a labor market that remains resilient. In such an environment, the ECB can afford to step back, assess the impact of past cuts, and wait for clearer signs before shifting again. The balance of risks no longer tilts toward urgent easing, and consensus is building that rates could stay at current levels well into 2026.

Survey data backs up this outlook. A Reuters poll showed nearly 60% of economists expect the ECB to hold through 2025, while a narrow majority predict the deposit rate will still be at or above 2% by end-2026. For now, expectations of a long pause are keeping the euro broadly supported.

In contrast, the Fed faces mounting pressure to resume easing after two consecutive weak non-farm payrolls. Markets still lean toward a 25bps cut in September, but the risk of a 50bps move is rising as the Trump administration intensifies political pressure on the FOMC. Even if the Fed opts for caution this month, markets see a strong chance of back-to-back easing with another cut in October.

The week’s major focus in the U.S. will be on August CPI and PPI releases, which should reflect the early impact of tariff escalation. Consensus sees headline CPI rising from 2.7% to 2.9% yoy, while core CPI is expected to hold at 3.1% yoy. Any upside surprise would deepen the Fed’s dilemma: inflation edging higher while growth signals weaken.

For Fed hawks, a downside surprise in core CPI would provide the opening to pivot toward deeper or faster cuts. But expectations remain fluid, and market reaction is set to remain volatile. Dollar moves will likely mirror each CPI headline as traders recalibrate the odds of 25bps versus 50bps in September.

Beyond the Fed and ECB, investors will watch UK GDP for clues on fiscal drag, Eurozone investor confidence for signals on growth resilience, and sentiment data out of Australia, where the RBA has recently leaned less dovish. Together, these releases could set the tone for risk sentiment and FX positioning into mid-September.

Here are some highlights for the week:

- Monday: Japan GDP final; China trade balance; Germany industrial production, trade balance; Eurozone Sentix investor confidence.

- Tuesday: New Zealand manufacturing sales; Australia Westpac consumer sentiment, NAB business confidence; France industrial production.

- Wednesday: China CPI, PPI; US PPI.

- Thursday: Japan BIS manufacturing, PPI; ECB rate decision; US CPI, jobless claims.

- Friday: New Zealand BNZ manufacturing; Germany CPI final; UK GDP, trade balance; US UoM consumer sentiment and inflation expectations.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.39; (P) 172.83; (R1) 173.17; More...

EUR/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Firm break of 173.87 will resume larger rise to retest 175.41 key resistance. On the downside, though, break of 172.47 support will extend the corrective pattern from 173.87 with another falling leg, before rally resumption.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, sustained break of 38.2% retracement of 161.06 to 173.87 at 168.97 will delay this bullish case, and probably extend the correction from 175.41 with another fall.

China exports growth slows in August, US flows collapse -33% yoy

China’s trade report for August showed growing pressure from U.S. tariffs. Exports rose 4.4% yoy, below expectations of 5.0% yoy and the slowest pace in six months. Shipments to the U.S. plunged -33.1% yoy, while flows to Southeast Asia jumped 22.5% yoy, suggesting exporters may be rerouting goods through regional partners to cushion losses.

Imports also disappointed, rising just 1.3% yoy versus forecasts of 4.1% yoy. Imports from the U.S. dropped -16% yoy, reflecting both weaker domestic demand and the bite of tariffs. Still, the overall trade surplus widened from USD 98.2B to USD 102.3 B, beating expectations of USD 99.4B.

While the surplus provides headline support, the underlying dynamics are fragile. U.S. President Donald Trump has already threatened a 40% penalty tariff on goods deemed to be transshipped from China, raising questions about how long exporters can sustain the ASEAN workaround. Besides, economists warn that once U.S. tariffs rise above 35%, they become prohibitively high for many Chinese manufacturers.

Washington and Beijing extended their tariff truce by 90 days on August 11, locking in 30% U.S. duties on Chinese goods and 10% Chinese tariffs on U.S. exports. But with no path yet beyond the pause, uncertainty lingers over whether China can maintain export growth as tariff pressure intensifies.

Japanese stocks soar towards record as Ishiba exit sparks optimism, NZD/JPY breaks higher

Japanese equities surged at the start of the week, with the Nikkei jumping more than 800 points in early trade and holding firm through the morning session. The index now sits within striking distance of a fresh record high. Risk-on appetite spilled over into currency markets, sending Yen sharply lower and leaving it vulnerable to further pressure if sentiment holds.

The trigger was the surprise resignation of Prime Minister Shigeru Ishiba over the weekend. Ishiba said the timing was deliberate, coming days after he secured the formal reduction of U.S. auto tariffs from 27.5% to 15%. “Now that negotiations on U.S. tariff measures have reached a conclusion, I believe this is the appropriate moment to resign,” he told reporters. His departure marks a sudden end to a premiership that began less than a year ago but was hampered by his coalition losing control of the lower house.

Nevertheless, Ishiba's exit opens the door to fresh leadership amid hopes that new faces could re-energize both the party and the electorate. Koizumi Shinjiro, agricultural minister and son of former prime minister Junichiro Koizumi, is widely viewed as a frontrunner, with his youth and broad appeal resonating with markets. Takaichi Sanae, closely aligned with the late Abe Shinzo, is also expected to be a serious contender. The leadership race is expected to fuel speculation of policy continuity combined with a push for fresh fiscal initiatives.

Investors are betting that the incoming administration will prioritize expansionary fiscal measures to secure opposition cooperation, given the LDP-led coalition still commands only a minority. Such expectations have buoyed equities further and reinforced the risk-on backdrop weighing on Yen.

Technically, NZD/JPY's rally from 85.54 resumed today. The break of 55 D EMA (now at 87.10) suggests that correction from 89.05 has completed after defending 38.2% retracement of 38.2% retracement of 79.79 to 89.05 at 85.51.

Further rise is expected as long as 86.61 support holds. Break of 88.33 resistance will indicate that whole up trend from 79.79 is ready to resume through 89.05 short term top.

SNB Schlegel: Hurdle to reintroducing negative rates remains high

SNB President Martin Schlegel said the bar for reintroducing negative rates remains “high,” acknowledging the policy’s "undesirable side effects" for savers and pension funds. His comments reinforced market expectations that the SNB will hold its policy rate steady well into 2026, with inflation staying positive for a third month in August.

Switzerland faces new headwinds from U.S. tariffs of 39%, which threaten its export-heavy economy and raise risks of further disinflation. Schlegel cautioned that while some firms will be hit hard, the overall economic impact is not yet clear. “Many companies are investing less, which is having a negative impact on the economy," he told Migros-Magazin.

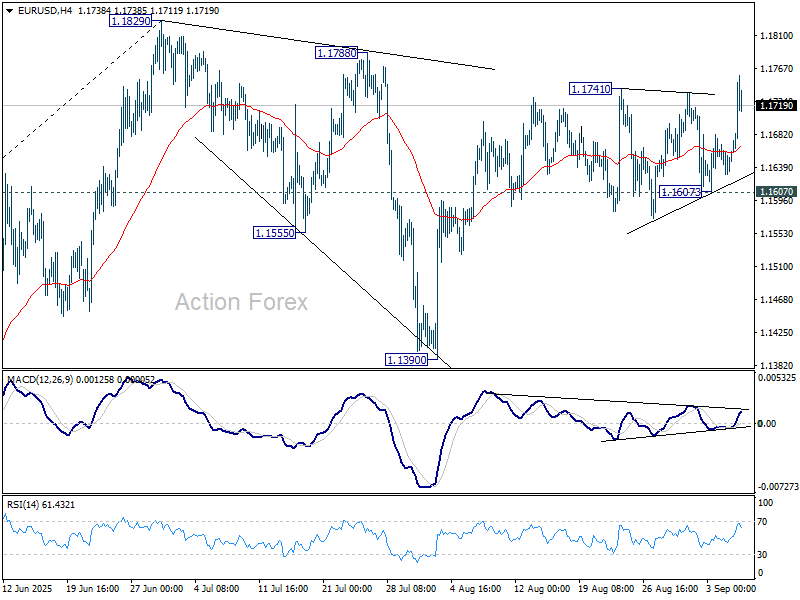

EUR/USD Bulls Press Higher – Can Resistance Give Way This Time?

Key Highlights

- EUR/USD started a fresh rally from the 1.1600 region.

- A major bullish trend line is forming with support at 1.1680 on the 4-hour chart.

- Gold surged further above $3,580 and $3,590.

WTI Crude Oil prices declined sharply and traded below $63.50.

EUR/USD Technical Analysis

The Euro remained supported above 1.1600 and started a fresh increase against the US Dollar. EUR/USD cleared 1.1650 and 1.1680.

Looking at the 4-hour chart, the pair settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). The pair even spiked above 1.1740 before the bears appeared.

The 1.1740 and 1.1750 levels present a major hurdle for the bulls. A close above 1.1750 could set the pace for another increase. In the stated case, the pair could rise toward 1.1800, above which the bulls could aim for a move toward 1.1850.

Any more upsides could send the pair toward 1.1920. On the downside, immediate support is 1.1700. The next key area of interest might be 1.1680. There is also a major bullish trend line forming with support at 1.1680 on the same chart.

Any more losses could send the pair toward the 61.8% Fib retracement level of the upward move from the 1.1608 swing low to the 1.1759 high at 1.1665 and the 100 simple moving average (red, 4-hour).

Looking at Gold, the bulls remain in action as they were able to push the price above the $3,580 resistance zone.

Upcoming Key Economic Events:

- Germany’s Trade Balance for July 2025 - Forecast €15.4B, versus €14.9B previous.

- Euro Zone Sentix Investor Confidence for Sep 2025 - Forecast -3.8, versus -3.7 previous.

Weak U.S. Employment Weighs on USD, Markets Eye Inflation, Gold Hits Records

Markets started last week quietly as the U.S. Labor Day holiday marked the end of summer trading. The main focus was U.S. jobs data, which came in much weaker than expected. Only 22,000 jobs were added in August compared with forecasts for 76,500, and the unemployment rate rose to 4.3%, the highest in four years. The weak numbers increased worries about the economy and raised expectations that the Federal Reserve will cut rates later this month. The U.S. dollar, which had been stronger earlier in the week, gave back its gains.

Other data gave a mixed picture. U.S. PMI readings were weaker than expected, showing slower business activity, while U.K. retail sales were stronger than forecasts, pointing to solid consumer spending.

U.S. equities finished the week close to unchanged. Early gains were held back by profit-taking and growing concerns about the weakening economy. Gold, on the other hand, kept climbing to new record highs, helped by safe-haven demand and expectations of lower interest rates.

Markets This Week

U.S. Stocks

The Dow slipped last week as profit-taking set in on worries about the U.S. economic outlook, with investors now expecting a 0.25% rate cut from the Federal Reserve later this month following weak employment data. The quiet conditions were unsurprising as the U.S. summer came to an end, but sideways-to-lower price action still looks most likely. This week’s key U.S. inflation data could bring volatility, while technical indicators such as the 10-day moving average are starting to trend lower, pointing to further profit-taking unless unexpected news provides support. Resistance levels remain at 45,750, 46,000, and 47,000, with support seen at 45,000, 44,000, and 43,000.

Japanese Stocks

The Nikkei resumed its uptrend after U.S. President Donald Trump signed an executive order cutting Japanese auto import tariffs to 15% from 27.5%. The move boosted sentiment, with foreign investors continuing to buy Japanese equities. The index is expected to stay well supported on the tariff news, though with U.S. equities facing resistance, range trading looks like the best approach this week. Resistance is at 43,000円, 44,000円, and 45,000円, while support is at 42,000円, 41,500円, and 41,000円.

USD/JPY

The USD/JPY continued to trade sideways last week, climbing early toward resistance after confirmation of lower U.S. auto import tariffs boosted sentiment. However, much weaker-than-expected U.S. employment data raised the likelihood of further Fed rate cuts, sending the pair back toward its starting levels. Range trading between 146 and 149 remains the best approach until a clear breakout occurs, with upcoming U.S. inflation data likely to provide short-term trading opportunities. Resistance levels are set at 148, 149, and 150, while support lies at 146 and 145.

Gold

Gold had another strong week, surging to record highs as both speculators and investors increased safe-haven buying. Expectations of lower U.S. interest rates following weak employment data further boosted demand. The market remains strong but overbought, so the best approach is to wait for buying opportunities on weakness near the 10-day moving average. In the short term, aggressive traders may also find selling opportunities if momentum eases. Resistance levels are at $3,600, $3,700, and $3,800, while support at $3,500, $3,450, and $3,400.

Crude Oil

WTI came under pressure last week, dropping to three-month lows on expectations that OPEC+ may raise output targets. Additional selling appeared at the end of the week after weak U.S. employment data raised fears of reduced demand from a slowing economy. WTI remains range-bound but looks more likely to test support at $60 in the short term, making selling opportunities the preferred strategy this week. Resistance levels are set at $65, $70, and $75, while support lies at $60 and $55.

Bitcoin

Bitcoin stabilized last week as speculators returned as buyers, though previous support at $112,000 was tested and held as resistance. ETF demand remains weaker than in earlier months, leaving prices likely to stay under pressure and trade sideways to lower in the near term. Resistance levels are set at $112,000, $120,000, $125,000, and $150,000, while support lies at $105,000 and $100,000.

This Week’s Focus

- Monday: Japan GDP, China Trade Balance

- Tuesday: Australia NAB Business Confidence

- Wednesday: China CPI and PPI, U.S. PPI

- Thursday: E.U. ECB Interest Rate Decision, U.S. Initial Jobless Claims, U.S. CPI

- Friday: Japan Industrial Production, U.K. GDP, U.K. Industrial Production, E.U. German CPI, U.S. Michigan Consumer Sentiment

This week is expected to start quietly, with the U.S. dollar and equities holding in small ranges as traders wait for new drivers. The main focus will be U.S. inflation data, where any surprises could bring short-term trading opportunities. Gold also stays in the spotlight, with investors watching to see if record highs can continue or if profit-taking pushes prices lower. In Japan, GDP data will be closely followed to see if growth is strong enough to support a Bank of Japan rate hike.

Dollar Falters and Yields Dive, Gold Hits New Highs, Stocks Hesitate

The past week in global markets has been anything but routine. What began as cautious positioning around economic data turned into a full-scale rethink of Fed policy and global growth prospects. Currency traders, bond investors, and equity markets were all forced to adjust as the numbers told a weaker story than anyone hoped for.

At the center of it all stood the U.S. jobs report. Instead of offering reassurance that the economy was holding up, the data marked another blow to confidence. For the Federal Reserve, the message was unmistakable: easing is no longer optional but necessary. Futures markets responded instantly, pushing expectations for multiple rate cuts further into the year.

Currency markets captured the story vividly. The dollar’s slide reshuffled the performance table, sending Swiss Franc and Euro to the top while leaving Loonie and Yen at the bottom. Domestic themes added another layer — from Canada’s disappointing jobs to Britain’s fiscal woes — but the common thread was that Dollar weakness magnified all other moves.

In equities, the tug of war between policy relief and growth concerns grew more intense. Optimism over easier Fed conditions helped push benchmarks to new records intraday, but those gains quickly faded. Investors seem less willing to buy the promise of liquidity when the economic foundation looks increasingly fragile.

Gold, however, thrived in the uncertainty. With Dollar under pressure and real yields tumbling, the metal surged to record levels, positioning itself as the standout performer of the week. The move toward the 4000 psychological mark no longer looks distant, and safe-haven demand is clearly back in play.

Labor Cracks Widen; Market Leans Toward Back-to-Back Fed Cuts

The US August jobs report delivered another shockingly weak print, setting Fed-easing expectations firmer than at any point this year. Non-farm payrolls rose just 22k, well below the modest 78k consensus, while the jobless rate ticked up to 4.3%, a near four-year high.

Beneath the headline, the revision story was arguably more damaging for sentiment. June was marked down to -13k, the first monthly job loss since the pandemic, while July was nudged up to 79k—hardly a meaningful rebound when paired with August’s soft gain.

Taken together, the data argue that the labor market is cooling faster than Fed officials anticipated. The narrative has shifted from “soft landing” toward “insurance required,” with growing pressure on policymakers to provide timely support.

Rates markets moved quickly. Fed funds futures now fully price a 25bp cut at this month’s FOMC, with about 11% odds attached to a 50bp move. If next week’s core CPI slows unexpectedly, the probability of a jumbo cut would likely rise further.

Importantly, the market isn’t stopping at September. Odds of a back-to-back 25bp reduction in October have climbed to around 80%, reflecting the view that the Fed is behind the curve and must catch up if labor slack widens.

That makes the September SEP and dot plot pivotal. The question is whether the median still implies two cuts for 2025—or shifts toward three—and how far officials mark down growth and the longer-run policy rate.

Politics adds another wrinkle. The White House has reportedly shortlisted Kevin Hassett, Kevin Warsh, and Christopher Waller to succeed Chair Powell; all three align with the administration’s pro-easing agenda, reinforcing the market’s conviction that policy will turn looser.

With the policy debate reframed, attention now turns to market transmission—Treasury yields and Dollar will tell us how quickly easier policy gets priced.

10-Year Yield Slides Below 4.1%, Dollar at Risk of Deeper Fall

The reaction in Treasuries was swift and decisive after the weak payrolls. 10-year yield plunged through the 4.1 threshold to close at 4.086, marking its lowest levels in months. Traders rushed into bonds on bets that the Fed will move faster and harder to counter cooling labor demand.

Technically, 10-year yield is hovering near the bottom of its near term falling channel, with 4.000 handle also acting as psychological support. Stabilization may occur around current levels, but the near term outlook will stay bearish as long as 4.205 support-turned-resistance holds.

Sustained break below 4.000—particularly if accompanied by dovish Fed projections at the September meeting—could accelerate the slide. Next target is 161.8% projection of 4.629 to 4.205 from 4.493 at 3.807, which is slightly below 3.886 structural support.

The medium-term backdrop also leans negative with rejection by 55 W EMA (now at 4.300). Fall from 4.809 could be seen as the third leg of the corrective pattern from 4.997 (2023 high). This implies scope for further losses through 3.603 to 38.2% retracement of 0.398 (2020 low) to 4.997 at 3.240 in the medium term, before finding a bottom.

Meanwhile, Dollar's selloff wasn’t catastrophic, as Dollar Index closed the week at 97.76, well above the July low at 96.37. But the index is clearly under pressure after multiple rejections at 55 D EMA (now at 98.40). Deeper fall is mildly in favor to retest on 96.37 in the near term. Whether that level holds may depend heavily on the Fed’s updated projections.

Upside recovery, meanwhile, looks limited. A break above 98.83 would extend the corrective structure off 96.37, but gains would likely stall beneath 100.25 resistance.

For the longer term picture, Dollar Index continues to hover slightly above long-term channel bottom that has defined the uptrend since 2008, now sitting around 96.0. Sustained break of the channel would open up deeper down trend to 61.8% retracement of 70.69 (2008 low) to 114.77 (2022 high) at 87.52.

Stocks Struggle Despite Fed Easing Bets

US equities gave back early gains on Friday, with DOW, S&P 500, and NASDAQ all finishing lower despite briefly touching record intraday levels. The pullback highlights investor unease that Fed easing may not fully insulate earnings from a slowing labor market and rising tariff pressures.

For equity bulls, the question is no longer whether the Fed will cut, but whether those cuts will arrive fast enough to cushion corporate profits.

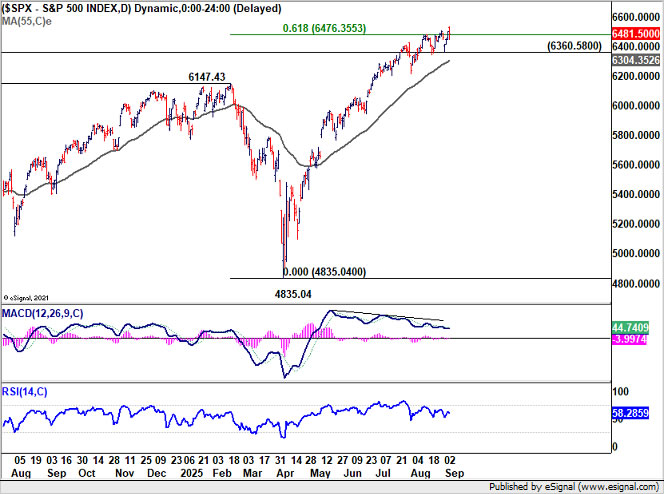

Technical signals continues suggest fatigue after recent record runs. S&P 500 is losing momentum as reflected in D MACD. The index also struggles to break decisively above 61.8% projection of 3491.58 to 6147.43 from 4835.04 at 6476.35.

The market is also running into the ceiling of its long-term rising channel, currently near 6690, further restraining bullish momentum. Even if stocks attempt another leg higher, the path looks constrained.

On the downside, break of 6360.58 support could trigger profit-taking and accelerate a correction. Sustained fall below the 55 D EMA (now at 6304.35) would confirm a medium-term correction, with risks extending toward 55 W EMA (now at 5877.73).

Gold Surges to Record, Eyes 4000 Next

Gold's reaction to NFP was much more clear-cut. While there was brief intraweek retreat, Gold quickly jumps after after the data and closed at new record high. For the near term, outlook will now stay bullish as long as 3511.49 support holds. Next target is 261.8% projection of 3267.90 to 3408.21 from 3311.30 at 3678.63.

More importantly, Gold has now taken out 200% projection of 1160.17 to 2704.87 from 1614.60 at 3443.94 decisively. The current up trend would now be targeting 261.8% projection at 4009.20, which is close 4000 psychological level, in the medium term.

EUR/USD Weekly Outlook

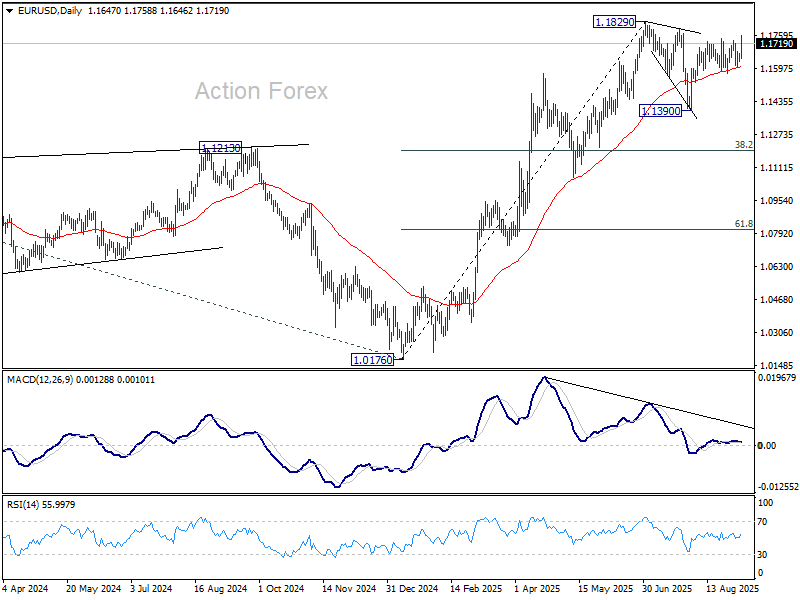

EUR/USD's rise from 1.1390 resumed late last week by breaching 1.1741. The development aligns with the case that correction from 1.1829 has completed with three waves down to 1.1390. Initial bias is now on the upside this week for retesting 1.1829 first. Firm break there will resume larger up trend. For now, risk will stay on the upside as long as 1.1607 support holds, in case of retreat.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

In the long term picture, a long term bottom was in place already at 0.9534, on bullish convergence condition in M MACD. Further rise should be seen to 38.2% retracement of 1.6039 (2008 high) to 0.9534 at 1.2019. Rejection by 1.2019 will keep the price actions from 0.9534 as a corrective pattern. But sustained break of 1.2019 will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.