Sample Category Title

Australian Dollar Hits Two-Week High, Confidence Data Next

The Australian dollar has extended its gains on Monday. In the North American session, AUD/USD is trading at 0.6588, up 0.49% on the day. Earlier, the Australian dollar climbed to a daily high of 0.6598, its highest level since July 25.

The US dollar ended the week broadly lower, as investors dumped the greenback after the soft US employment report. August nonfarm payrolls fell to 22 thousand, well below the revised market estimate of 79 thousand and lower than the July gain of 75 thousand. The Australian dollar rose as much as 1.1% on Friday before giving up about half its gains.

Australian confidence levels are expected to show an improvement on Tuesday. Westpac Consumer Confidence is projected to rise 1.0% in September after a strong 5.7% gain in August. The NAB Business Confidence has been moving higher and is expected to rise in August to 8 points from 7 a month earlier, which was the highest reading since August 2022.

Chinese exports slip

US tariffs are taking their toll on China's economy. In August, China's exports to the US fell by 33%. The US and China extended a trade truce in August, but that has still left US tariffs of 55% on Chinese goods and 35% Chinese tariffs on US goods.

China is in a deflationary phase and growth has been subdued. This does not bode well for the Australian economy or the Aussie, as China is Australia's largest trading partner. Australia hasn't been hit as hard as other countries by US trade policy, with tariffs of 10% on Australian products, but the US-China trade war could pose a serious headache for Australia's export sector.

AUD/USD Technical

- The Australian dollar tested resistance at 0.6594 earlier. Above, there is resistance at 0.6633

- 0.6551 and 0.6512 are providing support

AUDUSD 1-Day Chart, September 8, 2025

Sunset Market Commentary

Markets

Markets took a calm start to what could become an interesting trading week. Things kick off tonight with French PM Bayrou’s self-imposed confidence vote on his plans to tackle derailing public finances. While a defeat is market’s base scenario, a lot uncertainty remains on the way forward with all eyes directed at French president Macron afterwards. Will he put efforts in finding yet again a new “neutral” candidate to help overcome major ideological viewpoints in the hung parliament, ending in less fiscal discipline than proposed by PM Bayrou, or immediately throw the towel by calling early elections? Both scenarios suggest French assets will face continued pressure in the short term especially with the country’s credit rating at risk on Friday (AA- with negative outlook) of falling into single A category for a first time (Moody’s Aa3 stable, S&P AA- negative). Tomorrow’s key talking point will be the US Bureau of Labour Statistics’ preliminary benchmark revision to the establishment survey data for the 12 months through March 2025. Using more comprehensive data from the Quarterly Census of Employment and Wages, the BLS revises job data with final revisions due in March of next year. Markets anticipate significant downward revisions in line with last year when the job numbers in the 12 months to March 2024 were downwardly revised by 818k mainly because of issues with the birth-death model of companies and undocumented immigration. A significant revision might push US money markets into attaching a larger probability to a 50 bps Fed rate cut next week as it confirms fears of deeper labour market weakness. The BLS revisions need to be balanced with August US producer price (Wednesday), consumer price inflation (Thursday) and inflation expectations in the University of Michigan consumer survey for September (Friday) which are expected to reveal more signs of tariff-related inflation and argue in favour of a more gentle 25 bps rate cut next week. On Thursday, ECB President Lagarde probably faces one of the more easy-going press conferences since taking the helm at the central bank. An unchanged policy decision will be backed by nearly unchanged GDP and CPI forecasts in a world of reduced geopolitical uncertainty. It helps Lagarde spreading the message that monetary policy is in a comfortable position to face the future. We see a next evaluation point as early as March of next year. EMU money markets currently err slightly on the dovish side, pricing a 37% probability of a rate cut before year-end. Finally, we keep a close eye at the US Treasury’s mid-month refinancing operation. Tuesday’s $58bn 3-yr Note sale is followed by a $39bn 10-yr Note deal on Wednesday and a $22bn 30-yr Bond auction on Thursday. The recent bull steepening of the US yield curve also helped the very long end of the curve (30-yr) away from make-or-break levels (5%). Question remains whether there will be a lot of interest at current levels given the still dire shape of US finances and political & reputational risk still present (eg Fed independence debate).

News & Views

Two weeks ahead of the Swiss National Bank’s September policy meeting, the central bank’s governor took a critical view of reintroducing negative interest rates. The current level stands at 0% and recent inflation numbers (0.2% y/y) at first glance suggest further monetary easing is perhaps needed. Martin Schlegel in an interview with Migros Magazin, however, said the hurdle to revert back to an era of negative rates is high. He added that it can have undesirable side effects, for example for savers and pension funds. Schlegel pushed back when asked whether the central bank shot its monetary powder too early, saying that making forward-looking decisions is key in order to avoid having to take stronger countermeasures later. Schlegel’s views were in line with those the vice-governor aired end of August. Market implied odds for another 25 bps cut remain around 25% for end 2025 though. The Swiss franc strengthens today to EUR/CHF 0.932. Schlegel in the interview wasn’t so concerned about the strong CHF, since its real appreciation was not as great.

The EU is considering a 19th sanction package against Russia over its war with Ukraine. The sanctions would target about half a dozen Russian banks and energy companies as well as Russia’s payment and credit card systems, crypto exchanges and additional restrictions on its oil trade. Oil prices rebound today after losing ground over the three previous trading sessions, when it anticipated OPEC’s decision last week to further restore oil output. Brent currently trades around $66.8 per barrel and remains firmly established within a $65-$75 sideways trading range.

Japan’s GDP Sparkles, Yen Pushes Higher

The Japanese yen is in positive territory on Monday. In the European sesssion, USD/JPY is trading at 147.87, down 0.35% on the day.

Japan's economy expands 2.2% in Q2

The week has started on a positive note in Japan, as GDP for the second quarter was revised sharply higher to 2.2% y/y, up from the initial reading of 1.0% and above the Q1 gain of 0.3%.

This was the fastest pace of growth since Q3 2024, as private consumption was higher, in part due to government subsidies for rice and energy. Exports were higher as firms rushed to ship to the US before the blanket 15% tariffs kicked in. On a quarterly basis, GDP expanded 0.5%, up from the initial reading of 0.3%.

The increase in exports could be short-lived, as the US tariffs are making Japanese exports more expensive. Tariffs concerns could delay the Bank of Japan from raising interest rates, and third-quarter GDP will help gauge the effect of the tariffs on Japan's economy.

The political uncertainty in Japan is another factor which supports the BoJ staying on the sidelines. Prime Minister Shigeru Ishiba has resigned after a disastrous election in which Ishiba's coalition lost its majority in the lower house of parliament. It remains unclear who will replace Ishiba, with leadership vote expected in October.

US nonfarm payrolls fall to 22 thousand

US nonfarm payrolls disappointed with a marginal gain of 22 thousand, well below the upwardly revised gain of 79 thousand in July and the market estimate of 75 thousand. The unemployment rate edged up to 4.3% from 4.2%, the highest level since December 2021.

The money markets responded to the weak nonfarm payrolls report by fully pricing in a rate cut at next week's meeting, with a 90% probability of a quarter-point cut and a 10% chance of a half-point cut, according to CME's FedWatch. Prior to the jobs release, there was a 0% chance of a half-point cut.

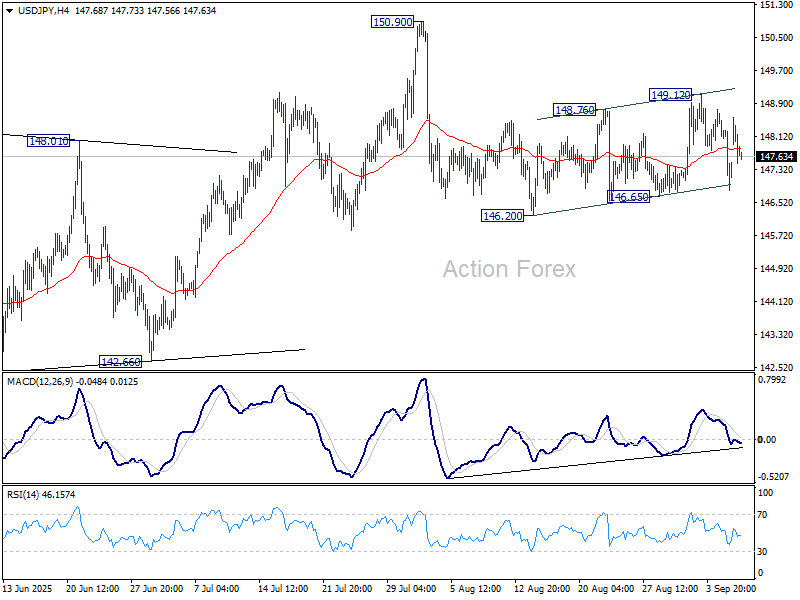

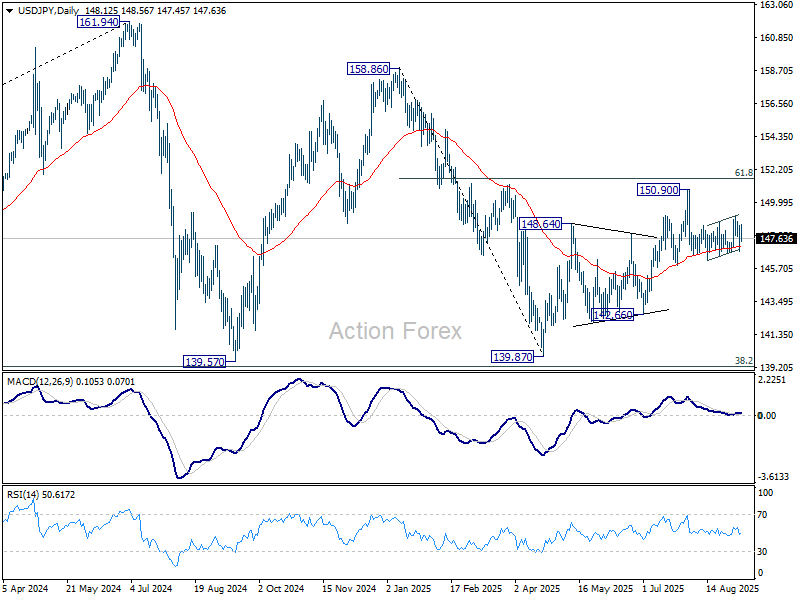

USD/JPY Technical

- USD/JPY is testing support at 147.60. Next, there is support at 146.62

- There is resistance at 148.37 and 149.35

USDJPY 1-Day Chart, September 8, 2025

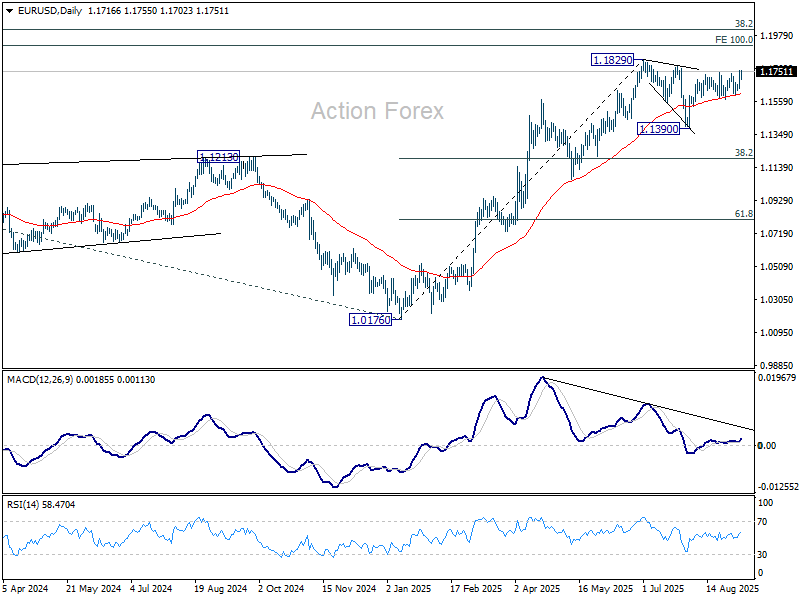

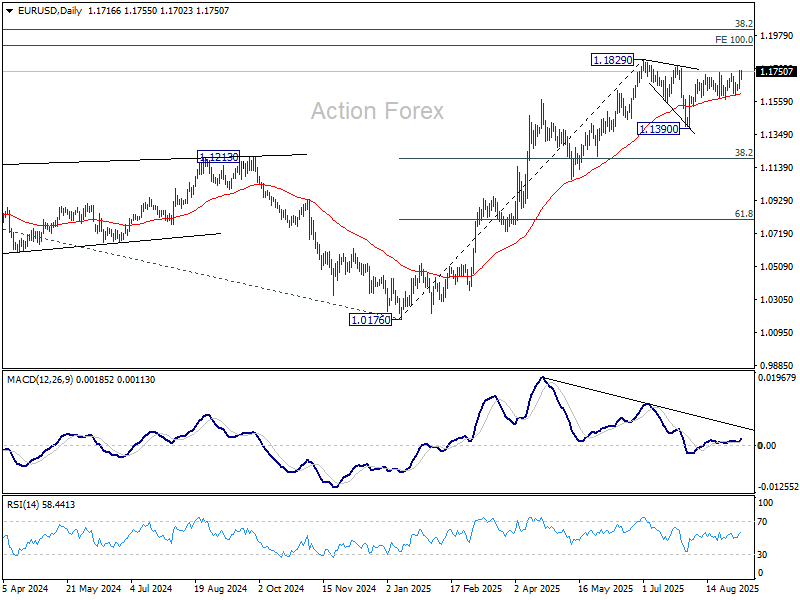

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1656; (P) 1.1708; (R1) 1.1771; More...

Intraday bias in EUR/USD remains on the upside, and rise from 1.1390 should target a retest on 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, below 1.1702 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.1607 support holds, in case of retreat.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

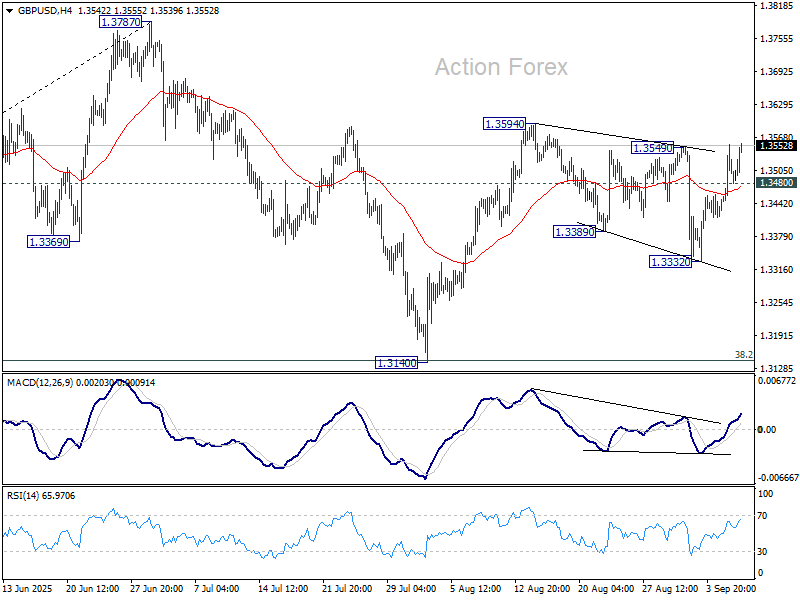

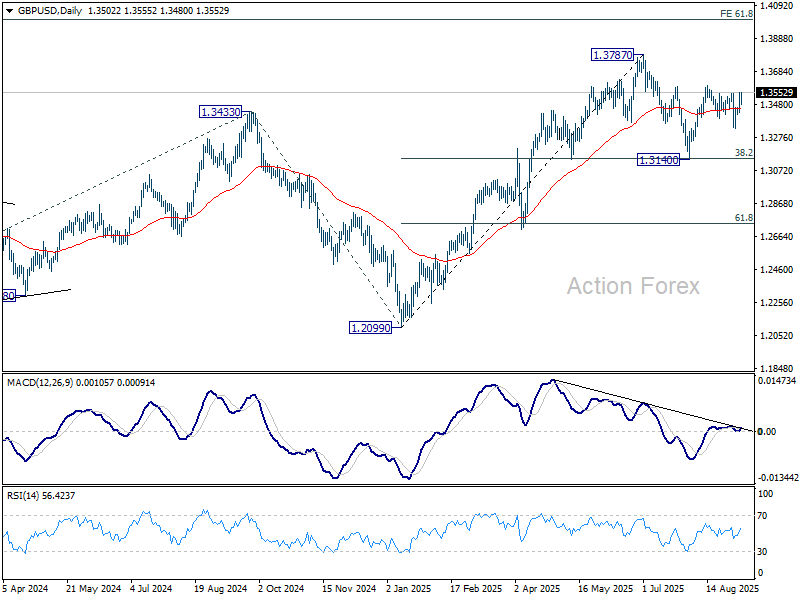

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3436; (P) 1.3495; (R1) 1.3568; More...

Outlook in GBP/USD is unchanged and intraday bias stays on the upside. Firm break of 1.3594 resistance will resume the rally from 1.3140 and target a retest on 1.3787 high. On the downside, below 1.3480 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.3332 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

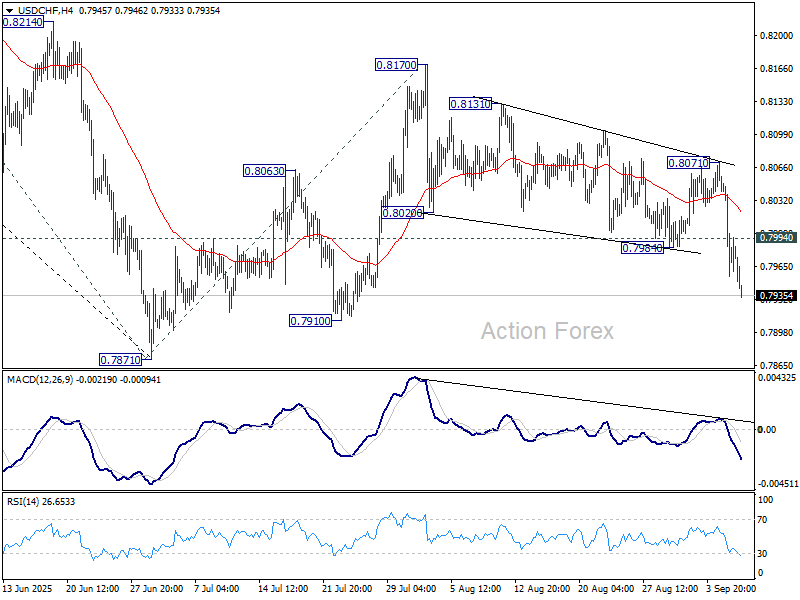

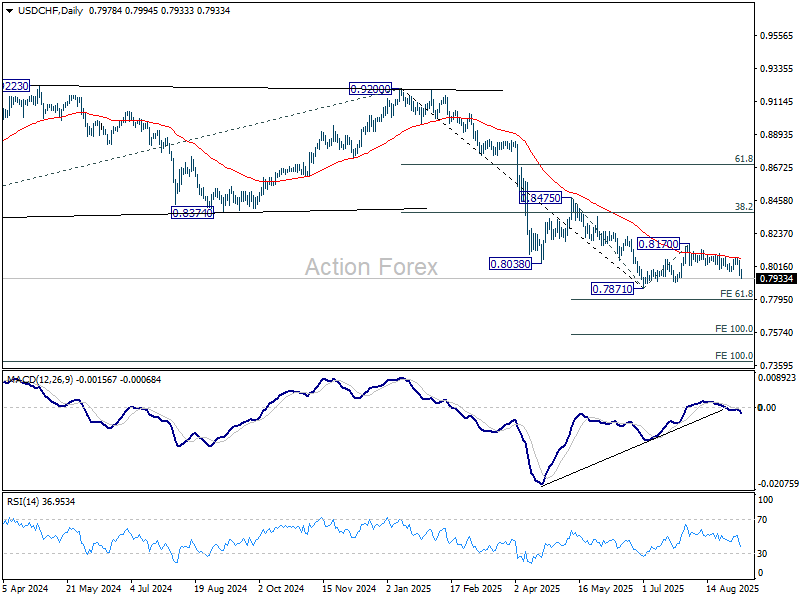

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7936; (P) 0.8000; (R1) 0.8043; More….

Intraday bias in USD/CHF stays on the downside for retesting 0.7871 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. On the upside, above 0.7994 minor resistance will turn intraday bias neutral first. But rise will stay on the downside as long as 0.8071 resistance holds, in case of recovery.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.62; (P) 147.60; (R1) 148.37; More...

Intraday bias in USD/JPY stays neutral for the moment. On the downside, break of 146.65 will suggest that fall from 150.90 is resuming. More importantly, sustained trading below 55 D EMA (now at 147.15) will argue that whole rebound from 139.87 has completed with three waves up to 150.90. Deeper decline should then be seen to 142.66 support next. However, break of 149.12 will turn bias back to the upside for retesting 150.90.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

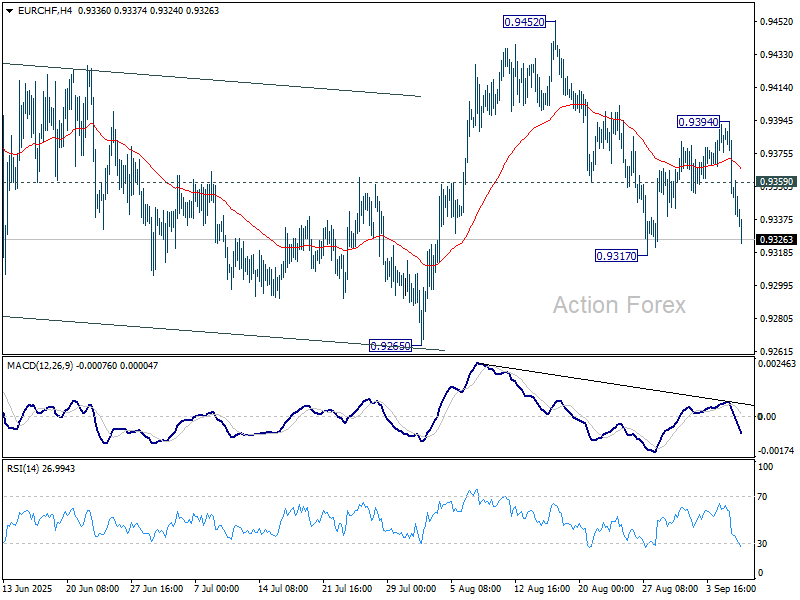

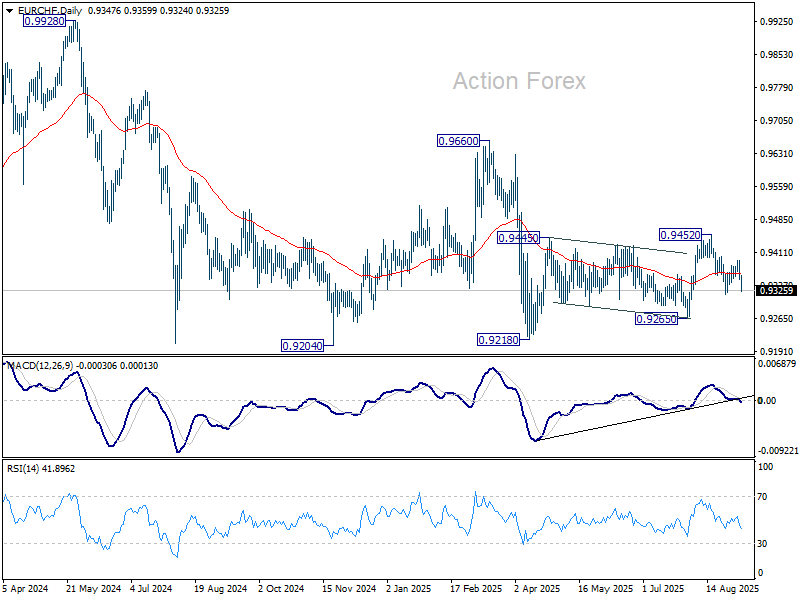

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9334; (P) 0.9366; (R1) 0.9381; More....

EUR/CHF's fall from 0.9394 accelerates lower today and intraday bias stays on the downside for 0.9371. Firm break there will solidify the bearish case that corrective pattern from 0.9218 has completed with three waves up to 0.9452 already. Deeper fall should then be seen to 0.9265 support, and then 0.9204 low. On the upside, above 0.9359 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.9394 resistance holds, in case of recovery.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

Euro Soft as France Faces Confidence Vote, Yen Weak Despite Recovery

Euro turned softer against both Sterling and Swiss Franc today as investors shifted focus to France ahead of a key confidence vote. While Thursday’s ECB rate decision dominates the week’s agenda, political instability in Paris could add fresh downside risk to the single currency.

Prime Minister François Bayrou’s minority government faces almost certain defeat in a no-confidence vote later in the day. If the government falls, it would mark the second collapse in less than a year following the implosion of Michel Barnier’s administration last December. President Emmanuel Macron would then be forced to appoint his fifth prime minister in under two years, a rapid turnover that has undermined investor confidence and compounded concerns over French fiscal credibility.

Beyond France, attention is also turning back to Japan following Prime Minister Shigeru Ishiba’s resignation over the weekend. The leadership race is shaping up between former economic security minister Sanae Takaichi and agriculture minister Shinjiro Koizumi. A recent Nikkei poll showed Takaichi narrowly ahead, with 23% support against Koizumi’s 22%.

If elected, Takaichi would be Japan’s first female prime minister and is viewed as a staunch supporter of “Abenomics.” Her opposition to BoJ rate hikes and advocacy of larger fiscal stimulus have drawn investor attention, as markets weigh the potential implications for policy continuity. Analysts highlight her strong team of bureaucratic allies as a key advantage.

Overall in the currency markets, Yen managed a partial rebound today but remains the weakest currency on the board, followed by Dollar and Euro. Kiwi leads gains, trailed by the Aussie and Swiss Franc. Sterling and Loonie are holding mid-range.

Elsewhere, oil prices rebounded as traders judged OPEC+’s latest output hike to be modest. The group agreed to raise production by 137,000 barrels per day from October, well below prior monthly increases. Also, many members were already exceeding quotas, suggesting the headline boost may add little new supply. Concerns over additional sanctions on Russian crude added to the upward pressure too.

In Europe, at the time of writing, FTSE is up 0.19%. DAX is up 0.43%. CAC is up 0.52%. UK 10-year yield is down -0.022 at 4.631. Germany 10-year yield is down -0.017 at 2.653. Earlier in Asia, Nikkei rose 1.45%. Hong Kong HSI rose 0.85%. China Shanghai SSE rose 0.38%. Singapore Strait times rose 0.03%. Japan 10-year JGB yield fell -0.008 to 1.568.

Eurozone Sentix confidence sinks to five-month low, summer optimism disintegrating at rapid pace

Eurozone investor sentiment deteriorated sharply in September, with the Sentix Confidence Index falling from -3.7 to -9.2, well below expectations of -1.1 and the weakest since April. Current Situation Index weakened to -18.8 from -13.0, while Expectations tumbled to 0.8 from 6.0.

Germany was the clear weak spot. Its investor confidence plunged from -12.8 to -22.1, while Current Situation gauge collapsed from -29.0 to -39.0. Expectations turned negative again, falling from 5.0 to -3.5, highlighting growing pessimism about Europe’s largest economy emerging from recession.

Sentix attributed the downturn to a mix of political and external headwinds: government instability in France, persistent weakness in German industry, an unfavorable tariffs arrangement with the US, and the ongoing war in Ukraine. These factors, it said, are exerting an “oppressive effect” on Eurozone sentiment.

The institute warned that summer optimism has “disintegrated at a rapid pace” and sees little sign of an autumn rebound. With export-oriented sectors facing more pressure under U.S. tariffs and rising concern over sovereign debt — particularly in France — the outlook for the Eurozone remains fragile heading into year-end.

China exports growth slows in August, US flows collapse -33% yoy

China’s trade report for August showed growing pressure from U.S. tariffs. Exports rose 4.4% yoy, below expectations of 5.0% yoy and the slowest pace in six months. Shipments to the U.S. plunged -33.1% yoy, while flows to Southeast Asia jumped 22.5% yoy, suggesting exporters may be rerouting goods through regional partners to cushion losses.

Imports also disappointed, rising just 1.3% yoy versus forecasts of 4.1% yoy. Imports from the U.S. dropped -16% yoy, reflecting both weaker domestic demand and the bite of tariffs. Still, the overall trade surplus widened from USD 98.2B to USD 102.3 B, beating expectations of USD 99.4B.

While the surplus provides headline support, the underlying dynamics are fragile. U.S. President Donald Trump has already threatened a 40% penalty tariff on goods deemed to be transshipped from China, raising questions about how long exporters can sustain the ASEAN workaround. Besides, economists warn that once U.S. tariffs rise above 35%, they become prohibitively high for many Chinese manufacturers.

Washington and Beijing extended their tariff truce by 90 days on August 11, locking in 30% U.S. duties on Chinese goods and 10% Chinese tariffs on U.S. exports. But with no path yet beyond the pause, uncertainty lingers over whether China can maintain export growth as tariff pressure intensifies.

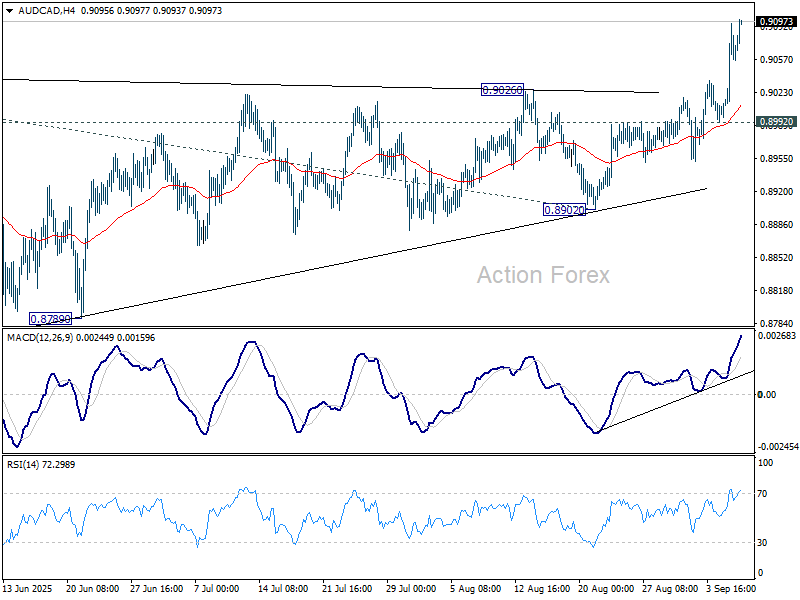

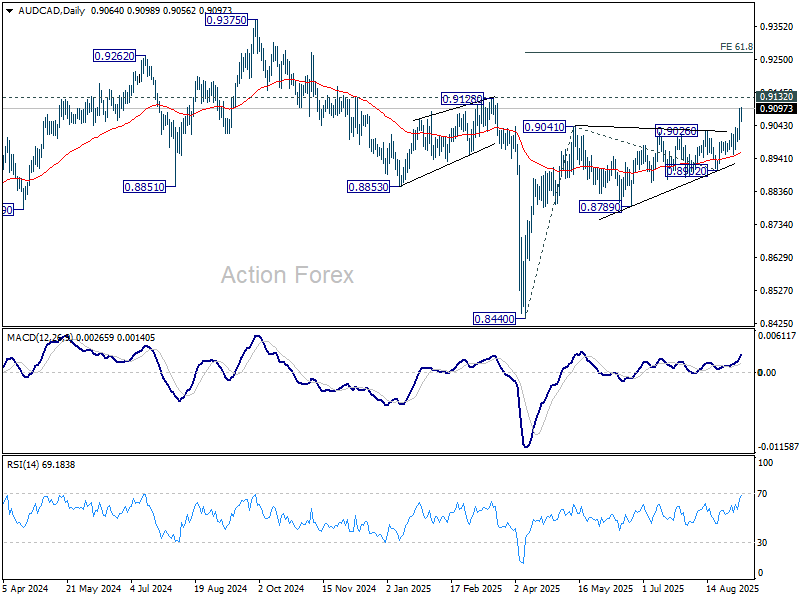

Aussie strength meets Loonie weakness, AUD/CAD targets 0.9128 and above

AUD/CAD resumed its rally from 0.8440 last week, breaking decisively through 0.9041 resistance level. The move reflects diverging fundamentals between Canadian Dollar, which is weighed down by weak domestic data, and Australian Dollar, which is drawing support from stronger consumption and external demand.

For Loonie, the trigger was August’s disappointing jobs report, which reignited expectations that the BoC will resume easing at its September 17 meeting. While markets have not fully priced a rate cut yet, sentiment is shifting toward renewed stimulus. Still, policymakers are likely to wait for the August CPI release on September 16 before making the final call.

Underlying inflation dynamics remain sticky, with CPI common holding at 2.6% yoy for a third consecutive month in July. That has kept some uncertainty in market pricing. But once tariff-driven price pressures ease, the BoC will have scope to bring rates down from the current 2.75% to around 2.00%.

In contrast, the RBA’s easing path looks less certain. Strong consumption data prompted Governor Michele Bullock to caution that fewer cuts may ultimately be delivered. The Australian Dollar has also found support from a sharp rally in Chinese equities, which has helped stabilize sentiment around regional growth prospects.

Technically, AUD/CAD's rise from 0.8440 should be reversing the whole downtrend from 0.8375. Further rise is expected as long as 0.8992 support holds, to 0.9128 structural resistance first. Firm break there will pave the way to 61.8% projection of 0.8440 to 0.9041 from 0.8902 at 0.9273.

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9334; (P) 0.9366; (R1) 0.9381; More....

EUR/CHF's fall from 0.9394 accelerates lower today and intraday bias stays on the downside for 0.9371. Firm break there will solidify the bearish case that corrective pattern from 0.9218 has completed with three waves up to 0.9452 already. Deeper fall should then be seen to 0.9265 support, and then 0.9204 low. On the upside, above 0.9359 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.9394 resistance holds, in case of recovery.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

WTI Oil Rallies 1.8% as Russian Supply Concerns Outweigh Modest OPEC + Output Hike

Oil prices have risen as much as 1.8% at the start of the week as Oil pares last week's losses. The rally this morning has come as a surprise to some quarters after eight OPEC + members agreed to lift output by 137,000 bpd from October.

However, the move by OPEC + was seen as more modest than expected and thus saw market participants shrug off the potential consequences. On top of that, markets are focused on the possibility of more sanctions on Russian crude.after Russia hit Ukraine with its biggest air attack since the start of the war.

For now, concerns around Russian supply are keeping Oil prices supported.

Russia-Ukraine Developments

Frederic Lasserre, an expert from the energy trading company Gunvor, stated on Monday that new sanctions against countries that buy Russian oil could disrupt the global oil supply.

This comes after Russia carried out its largest air attack of the Ukraine war over the weekend, which set fire to a government building in Kyiv and killed at least four people, according to Ukrainian officials.

On Sunday, Donald Trump said that several European leaders would visit the U.S. to talk about how to solve the conflict.

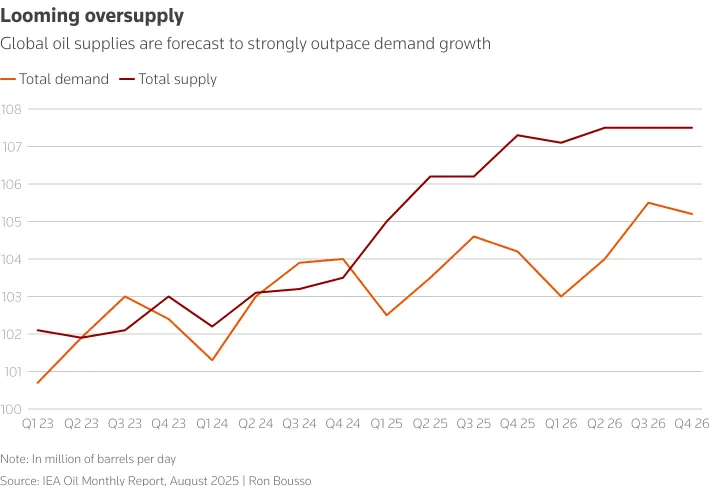

Over the weekend, the investment bank Goldman Sachs released a note saying it expects a slightly larger surplus of oil in 2026. They believe that increased oil production in the Americas will be greater than the decrease in supply from Russia and the stronger demand worldwide. Goldman Sachs kept its oil price forecast for 2025 the same, and for 2026, it predicts the average price for Brent crude to be $56 a barrel and for West Texas Intermediate crude to be $52 a barrel.

OPEC + Production Increases as Saudi Arabia Strategy Pivot Continues

OPEC+, a group of major oil producers led by Saudi Arabia, announced a surprise plan to increase oil production. Although this might seem like a risk to a market that already has too much oil, the actual effect on prices will likely be small.

The decision is more about politics. Saudi Arabia is using this to show its leadership, gain a bigger share of the market, and strengthen its relationship with the U.S.

The group agreed to gradually undo 1.65 million barrels per day of production cuts that were supposed to last until the end of 2026. They will increase their output by 137,000 barrels per day in October. At this rate, it will take them a year to fully reverse those cuts.

Source: LSEG

While the market is expected to have a surplus of oil due to increased production from countries like the U.S. and Argentina, the actual amount of new oil added by OPEC+ will probably be less than announced. This is because most members are already producing as much as they can.

However, Saudi Arabia is a major exception. It has a lot of extra production capacity, unlike Russia, which is limited by sanctions. This puts Saudi Arabia in a strong position to increase its market share, especially from U.S. oil companies that may slow down production as prices fall.

This pivot by Saudi Arabia has been something which has been building over the past few months. The strategy does seem to be a sound one and time will tell whether the Saudis will reap the benefits.

For now though, this move may keep further Oil price gains in check as oversupply concerns also remain a concern.

WTI Oil Daily Chart, September 8, 2025

From a technical analysis standpoint, Oil is eyeing a recovery after last week's selloff.

However, the fundm=amentals might continue to keep a prolonged rally in check as uncertainties continue to dominate the agenda.

Immediate resistance rests at the 100-day MA which rests at 64.65 before the 66.15 and 67.30 handles come into focus.

A move lower from current prices, could bring last week's swing low around 61.50 before the 60.70 and the YTD low at 55.10 come into focus.

WTI Oil Daily Chart, September 8, 2025

Source: TradingView (click to enlarge)

Client Sentiment Data

Looking at OANDA client sentiment data and market participants are long on WTI with 89% of traders net-long. I prefer to take a contrarian view toward crowd sentiment and thus the fact that so many traders are long means WTI prices could decline in the near-term.