Sample Category Title

China Headlines – A-Shares on Fire, CNY Strengthening, PMIs Confirm Softness

Markets

Chinese stocks on fire: China A-shares (onshore market) have rallied strongly over the past month being up more than 10%. Foreign focus has suddenly shifted from whether China was investable to concerns over a new bubble on the mainland. H-share stocks on the other hand have traded more or less sideways during August. Why the sudden rise in onshore market when data has been quite disappointing lately?

It is hard to point to one trigger but we have seen a confluence of factors coming together. First, on-shore stocks were lagging behind H-shares this year (chart 1) but suddenly in July and especially August played catch-up. Second, there is a lot of herd behaviour in the onshore market dominated by retail investors, which sometimes accelerates moves once the ketchup comes out of the bottle. Household deposits are massive after years of high savings (chart 3) and some of that money increasingly comes into the market when households start fearing to miss out. Third, positive headlines from tech company earnings and tech in general have added to the positive sentiment. Fourth, we saw a big jump in shares of chip producers following signals that Chinese authorities are warning against using Nvidia's H20 chips and it got more fuel when Nvidia was reported to have told suppliers to halt production of components of the H20 chips. Chinese chip company Cambricon more than doubled in value in August leading them to send out a warning of trading risk in the stock.

Bubble or not? The onshore market is now at a 10-year high but with a forward P/E level around 15 it is hard to talk about a bubble at this point. With lots of more potential liquidity coming from more deposits, though, it is not impossible it will turn into the next equity bubble in China around the 10-year anniversary of the previous bubble. FOMO is a strong force andcan drive more investors into the market. The offshore index is more dominated by foreign investors and is still below its' long-term average despite the sharp rally this year of more than 25%. Hence, it is hard to talk about a bubble in this market. For now, the trend seems to be your friend as the macro environment is overall benign and still lots of money that can potentially enter the market.

CNY appreciation: USD/CNY has moved lower lately (chart 4) driven by a couple of factors: a) lower US yields that have narrowed the US-China yield spread, and b) PBOC guiding the cross down with a gradual lowering of the fixingfor some time. I look for some stabilisation as the decline in US yields looks stretched to us. However, there is some downside risk now to our 12M target of 7.12 as PBOC may be aiming for a further appreciation of the CNY as it would support the rebalancing of the Chinese economy towards consumption and accommodate outside pressure due to China's ballooning trade surplus.

Sunset Market Commentary

Markets

European investors profited from the empty eco calendar and the absence of their US counterparts celebrating Labor Day holiday to start the week/month still in vacay mode. Stock markets eke out small gains (EuroStoxx 50: +0.25%) follow last week’s choppy/corrective action. German Bunds cede some ground with the yield curve bear steepening. Daily changes range between +1.6 bps (2-yr) and +3.3 bps (3.2 bps). The French-OAT swapspread is stable at a high 84 bps with French PM Bayrou acknowledging that the odds are against him at next week’s confidence vote: “compromise is a beautiful thing, but I’m not sure it’s possible”. In that case, little options remain apart from snap elections given that previous attempts to find a compromise PM in charge of a minority government over French hung parliament actually failed with Bayrou the latest victim. The French political crisis overlaps with an institutional one trying to find a way out of the debt spiral the country’s trapped in. Doing so calls for brave and unpopular fiscal austerity measures, but those don’t win you elections. Rising French risk premia are the obvious outcome down the road.

EUR/USD is going nowhere, changing hands just above 1.17. Focus turns to the US side of the equation later this week. While the French political crisis is holding the single currency back, we still see a good chance for the pair to test the YtD top at 1.1829 on an even weaker US dollar. For that to happen, we eye any available update on the health of the US labour market, be it employment components in manufacturing and services ISM’s, the ADP employment report, JOLTS job openings or official payrolls. The amount of potential pitfalls is large with Powell’s dovish pivot at Jackson Hole putting a big target on the labour market’s back. The Fed no longer solely focuses on upside inflation risks, but warns for a potentially rapid deterioration of the job market. The current low unemployment rate is a visage, hiding weakness both in demand and in supply. If companies reaction function switches from labour hoarding to lay-offs, the outcome could be a rapid increase in unemployment (rate). In such scenario, the Fed might be forced to implement more rate cuts and on a faster timeline than currently discounted by US money markets. Loss of interest rate support risks hurting the dollar.

News & Views

The Turkish economy expanded at a way faster clip in Q2 than expected. GDP rose by 1.6% quarter on quarter, more than double the 0.7% seen in Q1 and the 0.6% analyst estimate. Annual growth stood at 4.4% (seasonally and working day adjusted), quickening from 2.6% in Q1. The growth boost came on the account of strong domestic demand, with both household consumption and especially business investment showing strong increases. It suggests the fall-out of the emergency rate hike by the national bank (CBRT) in March which interrupted an ongoing easing cycle had no significant impact. The CBRT meanwhile has returned to lowering the policy rate, with the level currently standing at 43%. Inflation numbers are due on Wednesday and will help shape expectations for the rate decision September 11. The Turkish lira is exploring new (closing) lows against the euro (EUR/TRY 48.2) and sticks to the recent lows seen against the USD (41.11).

S&P Global’s Czech manufacturing PMI surprised to the downside, easing from 49.7 to 49.4 compared to the 50.1 expected. A faster rise in new orders was offset by firms cutting workforce numbers again and prioritizing stock depletion over input buying as a way of lowering costs. Production levels were more or less unchanged after two successive expansions. Logistic issues, delayed deliveries of materials and the impact of US tariff policy weighed on output. Relatively soft input price pressures, thanks to the recent CZK appreciation, boosted business morale though, with confidence at the second-highest level since February 2022. EUR/CZK tested the 24.4 mark for a second time in as many months before returning to opening levels around 24.44.

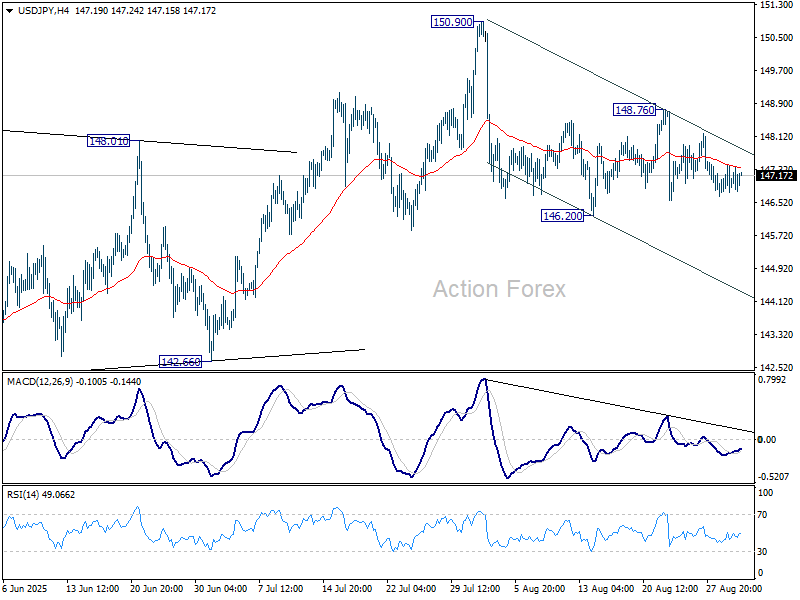

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.74; (P) 147.08; (R1) 147.38; More...

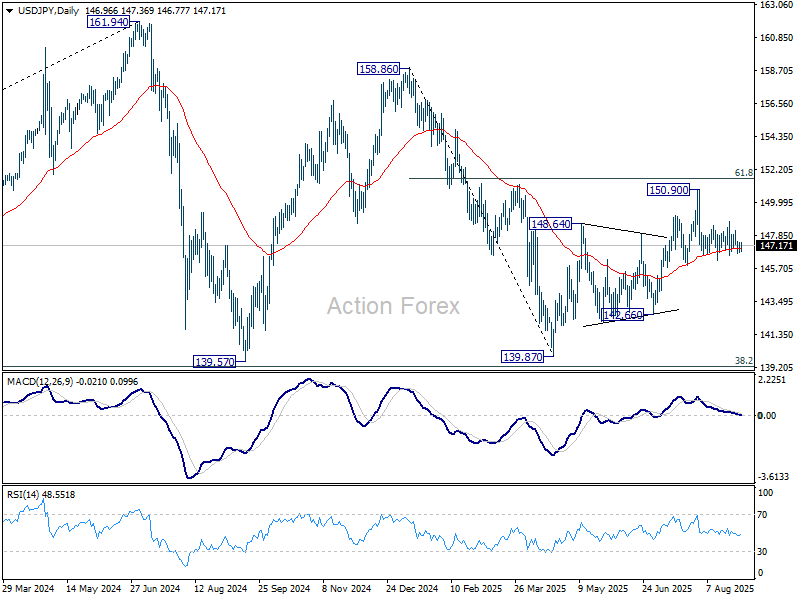

No change in USD/JPY's outlook and intraday bias stays neutral. On the downside, firm break of 146.20 will resume the decline from 150.90. More importantly, that would also argue that rebound from 139.87 has completed as a corrective move to 150.90. Deeper fall should be seen to 142.66 support for confirmation. On the upside, above 148.76 will bring another rise to retest 150.90 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

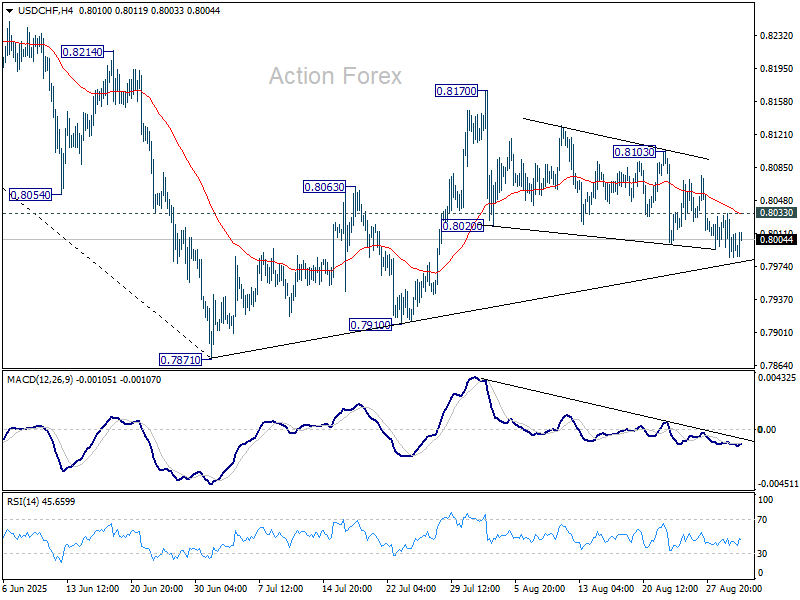

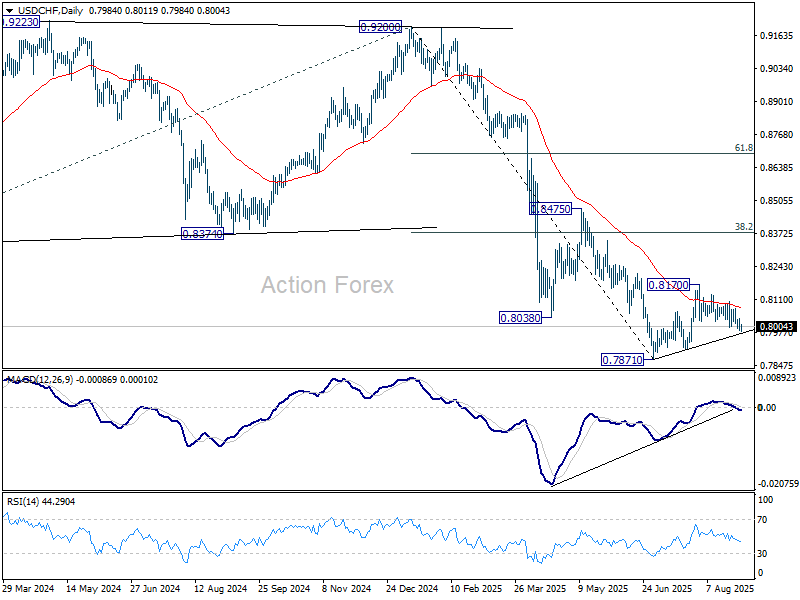

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7983; (P) 0.8010; (R1) 0.8034; More….

Intraday bias in USD/CHF stays mildly on the downside. The current favored case is that corrective rebound from 0.7871 has completed at 0.8170. Deeper fall would be seen to 0.7910 support, and then retest 0.7871. Nevertheless, break of 0.8033 minor resistance will dampen this bearish view and turn intraday bias neutral again first.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

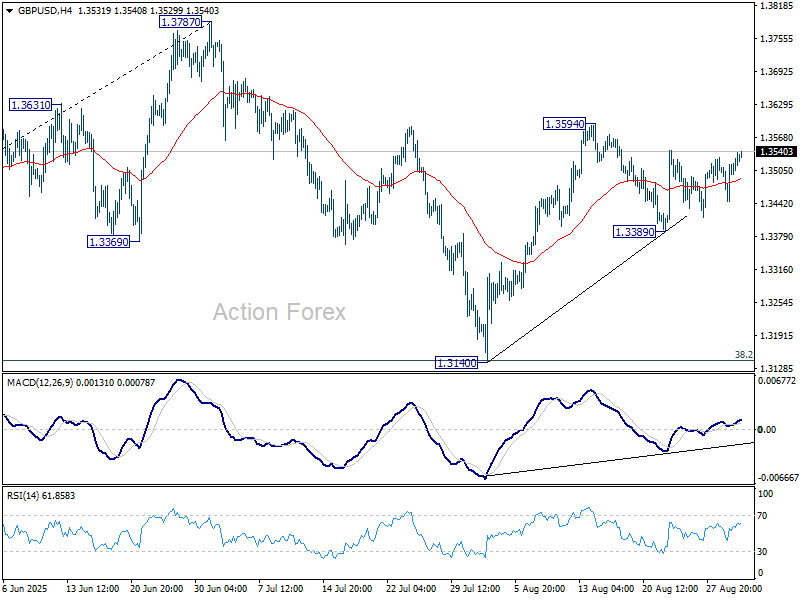

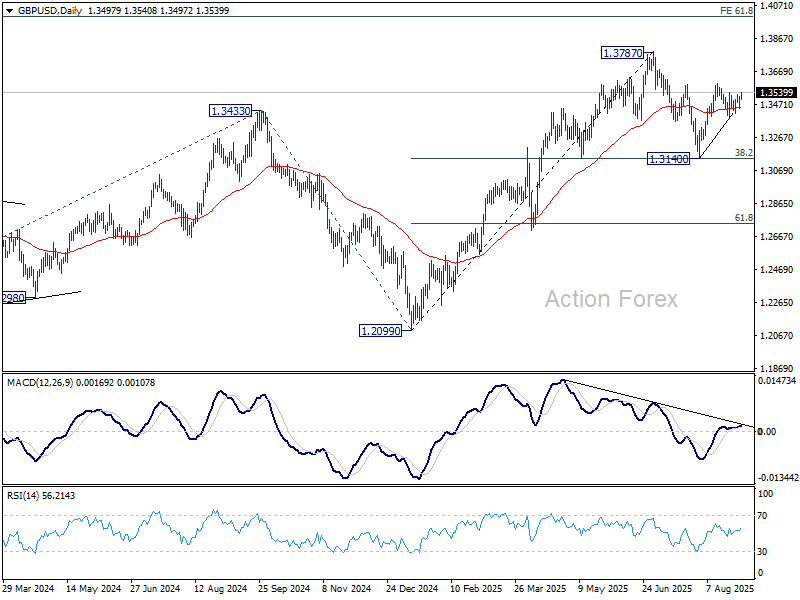

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3459; (P) 1.3490; (R1) 1.3534; More...

Range trading continues in GBP/USD and intraday bias remains neutral. With 1.3389 support intact, further rally is in favor. On the upside, above 1.3594 will resume the rebound from 1.3140 to retest 1.3787 high. On the downside, however, break of 1.3389 support will extend the corrective pattern from 1.3787 with another fall, and target 1.3140 support.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3104) holds, even in case of deep pullback.

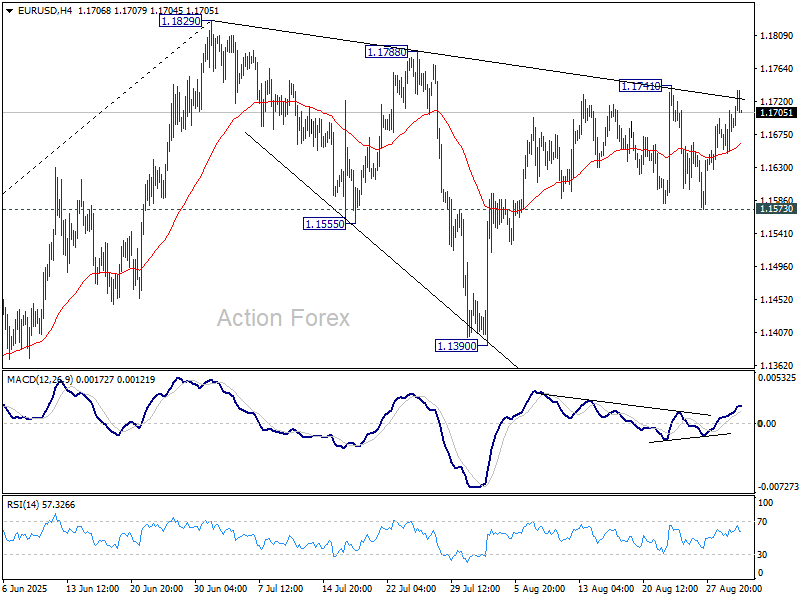

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1655; (P) 1.1682; (R1) 1.1713; More...

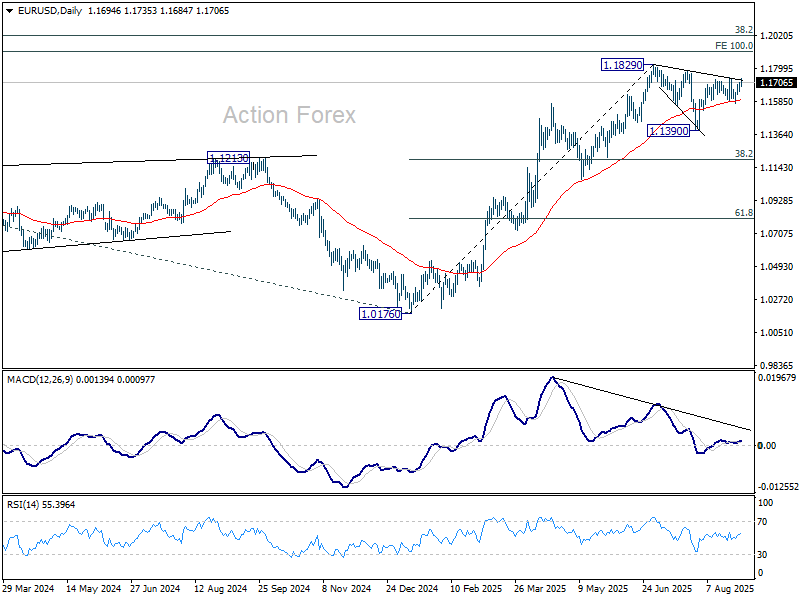

EUR/USD continues to struggle to break through 1.1741 resistance and intraday bias stays neutral Overall outlook is unchanged that corrective fall from 1.1829 should have completed with three waves down to 1.1390. On the upside, above 1.1741 will bring retest of 1.1829 high first. Firm break there will resume larger up trend. However, sustained break of 1.1573 will dampen this view, and indicate that corrective pattern from 1.1829 is extending with another falling leg towards 1.1390 again.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

Euro Leads But French Politics Cap Gains, Dollar Mixed

Euro is leading the foreign exchange market today, staging a solid recovery from last week’s weakness. Investors are clearly positioning back into the single currency, but the rally has yet to find a convincing fundamental driver, leaving momentum somewhat constrained.

Political uncertainty in France is also serving as a cap on Euro gains. The minority government of Prime Minister Francois Bayrou faces a high-stakes confidence vote on September 8 over its budget plans for 2026. With opposition parties aligned against the austerity package, defeat is seen as highly likely.

Still, markets are not turning bearish on the Euro purely on political grounds. Historically, domestic instability within one Eurozone member weighs heavily on the currency only when there are signs of contagion spreading across the bloc. At this stage, broader Eurozone fundamentals remain stable, and no such contagion is evident.

Dollar, meanwhile, is trading on the softer side but also lacks decisive momentum. Traders are cautious ahead of a heavy week of U.S. releases, with Friday’s nonfarm payrolls at the center of attention. The risk is skewed toward further Dollar weakness if data fall short, forcing the Fed to act more forcefully than the current market pricing suggests. For now, however, markets are waiting rather than moving aggressively.

In today’s performance table, Euro tops the leaderboard so far, followed by Sterling and Aussie. Yen is the weakest, trailed by Swiss Franc and Loonie, while the greenback and Kiwi are mixed in the middle.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.41%. CAC is up 0.02%. UK 10-year yield is up 0.029 at 4.752. Germany 10-year yield is up 0.029 at 2.756. Earlier in Asia, Nikkei fell -1.24%. Hong Kong HSI rose 2.15%. China Shanghai SSE rose 0.46%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield rose 0.02 to 1.625.

ECB's Lagarde warns on Fed independence, tariff uncertainty

ECB President Christine Lagarde issued a stark warning today, saying it would be “very worrying” if U.S. President Donald Trump succeeded in his efforts to exert control over the Fed.

In an interview with Radio Classique, Lagarde stressed "if US monetary policy were no longer independent and instead dependent on the dictates of this or that person, then I believe that the effect on the balance of the American economy could, as a result of the effects this would have around the world, be very worrying, because it is the largest economy in the world,"

Lagarde added that Friday’s U.S. appeals court ruling, which declared most of Trump’s tariffs illegal, created a “further layer of uncertainty” for the global economic outlook. The combination of policy unpredictability in Washington and structural risks elsewhere leaves investors wary at a time when global growth is already under strain from weak trade flows and tariff disputes.

Turning to domestic matters, Lagarde addressed mounting political risk in France ahead of the September 8 confidence vote. Opposition parties have pledged to bring down Prime Minister Francois Bayrou’s minority government over unpopular budget squeeze plans for 2026. The political drama has hit French bonds and equities, raising questions about the stability of the Eurozone’s second-largest economy.

Lagarde stressed, however, that France’s banking system is not at the root of the problem. She noted that banks are far better capitalised and structured than during the 2008 financial crisis, and remain responsibly managed. Still, she acknowledged that markets are sensitive to political shocks, and that uncertainty around government stability continues to weigh on risk sentiment.

Eurozone unemployment rate eases to 6.2% in July, matches expectations

Eurozone unemployment edged down to 6.2% in July from 6.3% in June, in line with expectations. The broader EU rate slipped from 6.0% to 5.9%, according to Eurostat.

Eurostat estimated 13.025 million unemployed across the EU in July, including 10.805 million in the Eurozone. Compared with June, jobless figures fell by -165k in the EU and -170k in the Eurozone.

China RatingDog PMI manufacturing rises to 50.5, relief rally rather than turning point

China’s manufacturing sector showed a modest improvement in August, with the RatingDog Manufacturing PMI rising from 49.5 to 50.5, beating expectations of 49.9 and returning to expansion. However, RatingDog described the uptick as a “breath of relief rather than a sustained rally,” reflecting cautious optimism. By contrast, the official NBS survey offered a more subdued view, with manufacturing inching up from 49.3 to 49.4 and non-manufacturing steady at 50.3.

The RatingDog report highlighted firmer new orders, which pushed inventories of raw materials and finished goods higher. Export demand remains weak but showed slower contraction. Yao cautioned that external demand may have been pulled forward while domestic demand stays soft, limiting the scope for sustained output gains without stronger local consumption.

Meanwhile, input costs continued to climb under the “Anti-involution” policy backdrop, and those upstream pressures are now filtering into output prices, ending an eight-month streak of falling charges. With profit recovery still slow, the durability of the latest rebound depends on whether exports can stabilize further and domestic demand begins to catch up.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1655; (P) 1.1682; (R1) 1.1713; More...

EUR/USD continues to struggle to break through 1.1741 resistance and intraday bias stays neutral Overall outlook is unchanged that corrective fall from 1.1829 should have completed with three waves down to 1.1390. On the upside, above 1.1741 will bring retest of 1.1829 high first. Firm break there will resume larger up trend. However, sustained break of 1.1573 will dampen this view, and indicate that corrective pattern from 1.1829 is extending with another falling leg towards 1.1390 again.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

EUR/USD Technical: Euro on the Brink of a Medium-Term Bullish Breakout

Since our last publication, the EUR/USD has indeed shaped the expected minor bullish breakout above the highlighted 1.1520 short-term pivotal support and hit the 1.1680/1.1705 short-term resistance. It rallied by 1.6% to print an intraday high of 1.1730 on 13 August 2025.

Let’s now examine its latest technical elements to determine its next potential trajectory and key levels.

Fig. 1: EUR/USD minor trend as of 1 Sep 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

After shaping a minor corrective range configuration from 13 August 2025 high of 1.1730 to 27 August 2025 low of 1.1574, the EUR/USD is likely to kickstart a potential fresh medium-term bullish impulsive up move sequence.

Bullish bias above 1.1650 key short-term pivotal support. A clearance above 1.1730 intermediate resistance reinforces the bullish tone for the next intermediate resistances to come in at 1.1770/1790 and 1.1830 (also a Fibonacci extension) in the first step.

Key elements

- Price actions of the EUR/USD have started to trade back above its 20-day and 50-day moving averages since last Thursday, 28 August 2025.

- The EUR/USD has oscillated within a minor ascending channel in place since the 1 August 2025 low of 1.1392.

- The hourly RSI momentum indicator has continued to oscillate above a parallel ascending trendline above the 50 level, which short-term bullish momentum is likely intact.

- The yield spread between the 2-year German Bund and the US Treasury note broke higher on Thursday, 28 August, narrowing the differential to –1.68% from –1.82% on 22 August. This development indicates a relative decline in the yield attractiveness of the 2-year US Treasury versus its German counterpart, which in turn exerts downside pressure on the US dollar against the euro.

Alternative trend bias (1 to 3 days)

A break below 1.1650 support negates the bullish tone on the EUR/USD to see another round of minor corrective decline for a retest on the next intermediate support at 1.1590/1.1570 (also the 27 August 2025 swing low area).

EUR/USD Gains Ground Amid Fresh Doubts Over the Fed

The EUR/USD pair rose to 1.1704 on Monday. The US dollar is trading near one-month lows as the market awaits a series of US labour market reports. These figures could influence the Federal Reserve's upcoming policy decisions.

The key event will be Friday's August employment report, alongside data on the unemployment rate, job openings, and private sector employment.

Investors continue to assess Friday's release of the Personal Consumption Expenditures (PCE) index. It confirmed rising prices and heightened uncertainty regarding the pace of future interest rate cuts. Nevertheless, the market is pricing in an approximately 88% probability of a 25-basis-point Fed rate cut this month.

On the trade front, a federal appeals court ruled that the majority of former President Donald Trump's retaliatory tariffs were unlawful, giving the administration until 14 October to appeal to the US Supreme Court.

Trading activity at the start of the week is expected to be subdued due to the US market closure for the Labor Day holiday.

Technical Analysis: EUR/USD

H4 Chart:

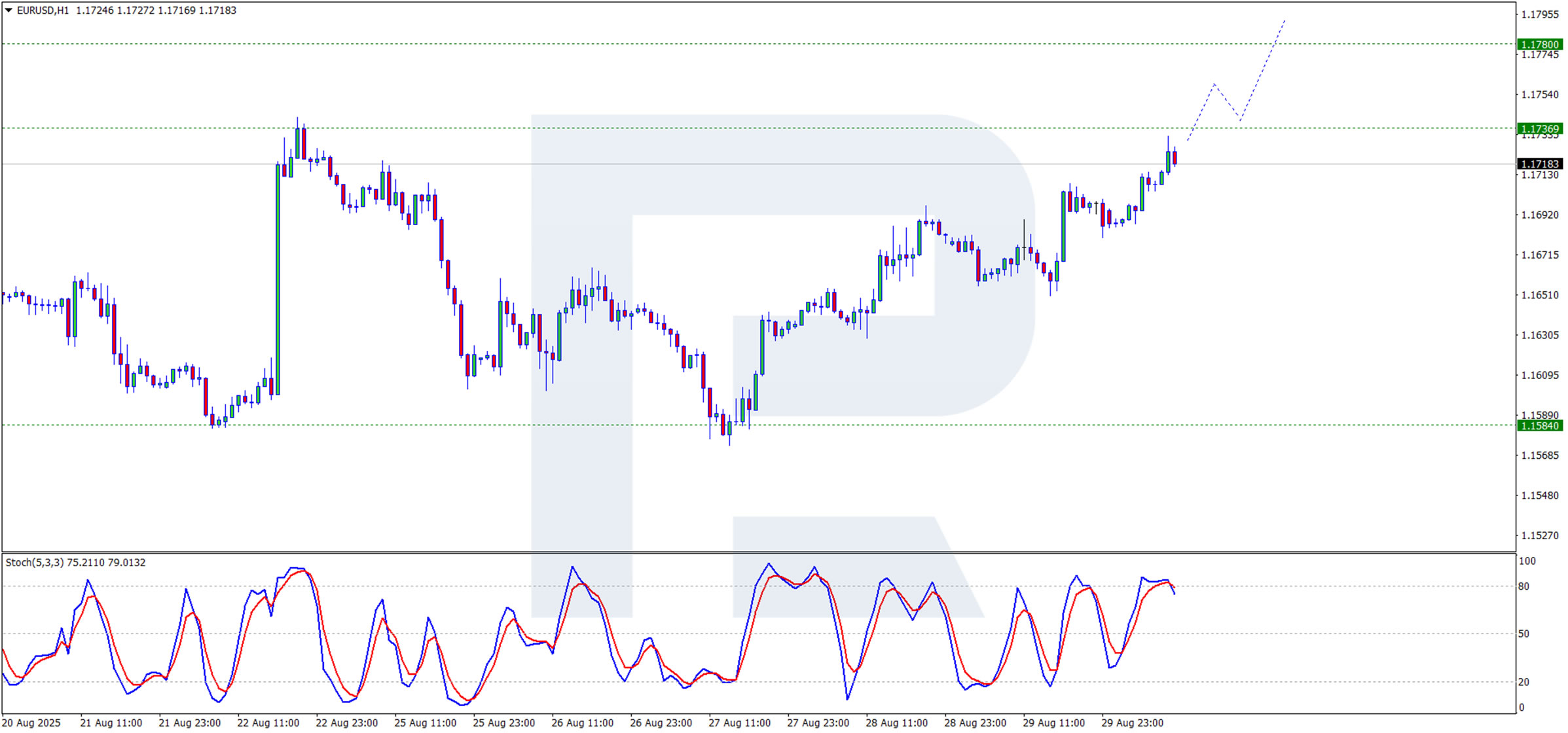

On the H4 chart, EUR/USD has formed an upward wave towards the upper boundary of the sideways channel at 1.1736. A breakout above this resistance level could signal the start of a new upward trend. However, a pullback within a corrective wave is possible, which would see the breached resistance level retested as new support. This scenario is supported by the MACD indicator, whose histogram and signal line are above zero and continue to rise. This momentum suggests the upward trend is likely to persist towards the 1.1780 level, with potential corrections along the way.

H1 Chart:

On the H1 chart, the pair is forming a correction as it tests the resistance level. A breakout above this resistance would indicate a resumption of the upward wave. The signal line of the Stochastic oscillator is crossing above the 80 level, signalling a potential short-term correction before the upward trend potentially continues.

Conclusion

The pair is benefiting from a weaker dollar as market participants reassess the Fed's policy trajectory. All attention is now on the upcoming US labour market data, which will be crucial for determining the pair's short-term direction. Technically, the outlook remains bullish, with a break above key resistance needed to confirm further gains.

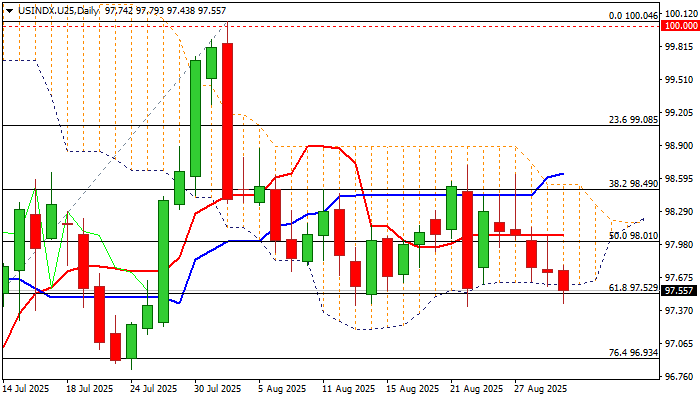

Dollar Index: Dollar Remains Weak on Fed Rate Cut Expectations

The dollar index remains in red for the fifth straight day and probes again through key supports at $97.61/52 (daily cloud base / Fibo 61.8% of 95.97/100.04) which have so far contained a number of attacks and marks solid supports.

The dollar keeps negative tone on rising bets for Fed rate cut in September (the latest dovish comments from two Fed policymakers added to the outlook), as well as the most recent political turmoil in the US after President Trump’s attempt to fire Fed Governor Cook and court ruling that most of Trump’s tariffs are illegal.

However, markets are likely to be more cautious ahead of releases of key economic (US August labor data) that will be in focus this week for the final signal ahead of Fed’s September policy meeting.

US labor sector showed significant signs of slowing in past couple of months that is now Fed’s biggest worry, after Chair Powell said that elevated inflation is likely to be a temporary phenomenon.

Economists expect significant drop in job openings and private sector hiring (JOLTS / ADP) but predict that non-farm payrolls will remain almost unchanged and unemployment tick higher.

Disappointing NFP would be the last signal confirming September rate cut and open prospects for potential further easing towards the end of the year.

In such scenario, pressure on greenback will increase, with firm break of cloud base / Fibo triggers to expose next targets at $96.93/82 (Fibo 76.4% / July 24 higher low).

Conversely, upbeat August NFP (unlikely scenario) would provide temporary relief, but not expected to result in major dollar’s direction changes.

Res: 97.61; 98.01; 98.15; 98.49.

Sup: 97.41; 97.15; 96.93; 96.48.