Sample Category Title

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3735; (P) 1.3749; (R1) 1.3764; More...

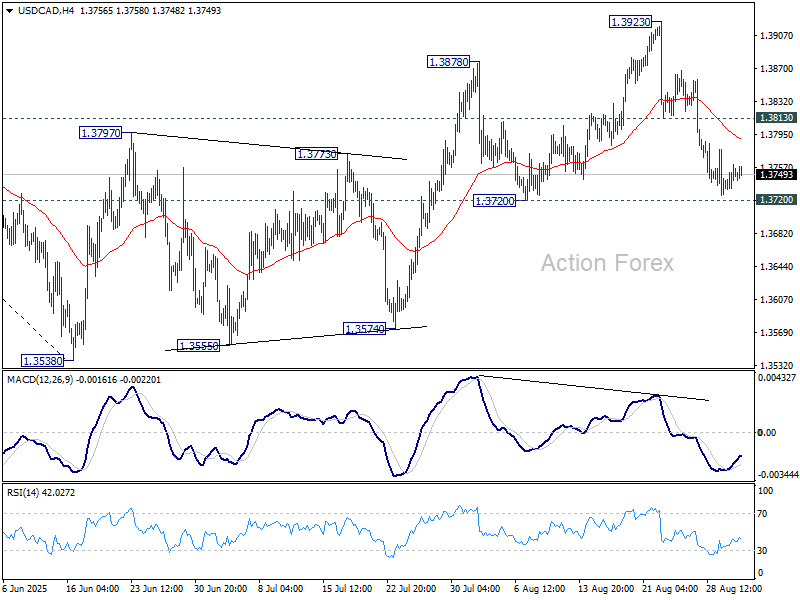

Intraday bias in USD/CAD remains neutral for the moment. On the downside, decisive break of 1.3720 will argue that the corrective pattern from 1.3538 has already completed at 1.3923. Intraday bias will be back on the downside for 1.3574 support first. Break there will bring retest of 1.3538 low. On the upside, though, break of 1.3813 resistance will retail near term bullishness, and bring retest of 1.3923 high instead.

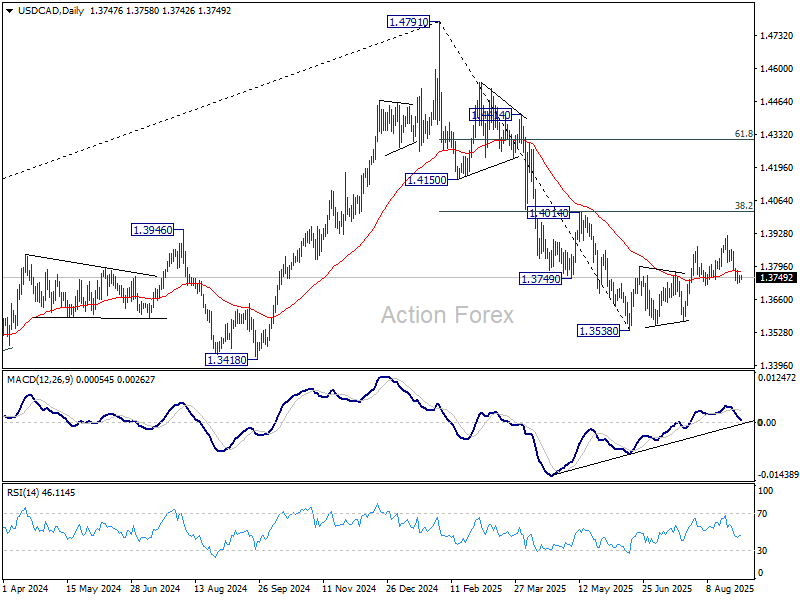

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

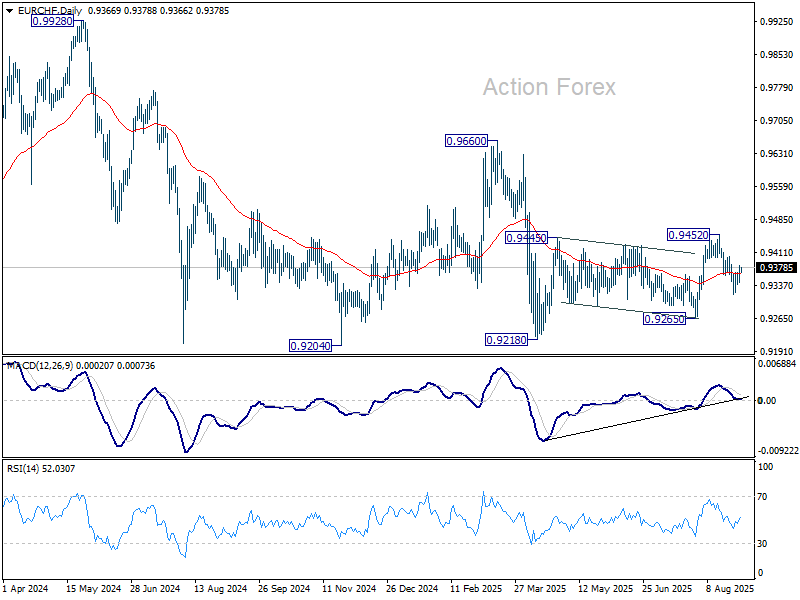

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9353; (P) 0.9368; (R1) 0.9390; More....

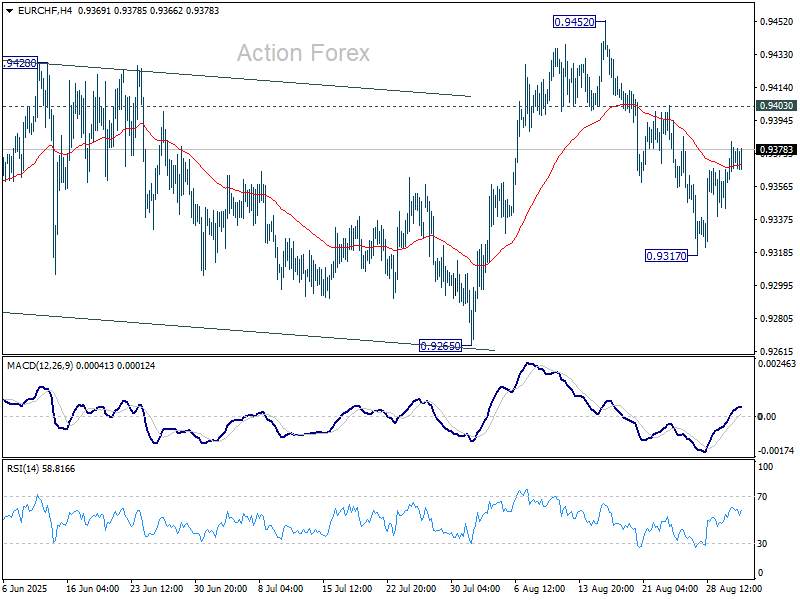

Intraday bias in EUR/CHF remains neutral at this point. More consolidations could be seen above 0.9317. Still, current development suggests that corrective pattern from 0.9218 might have completed with three waves up to 0.9452 already. Further decline is in favor as long as 0.9403 resistance holds. On the downside, below 0.9317 will target 0.9265 support first. Firm break there should resume larger fall to retest 0.9204 low. Nevertheless, break of 0.9403 will dampen this view and bring stronger rise back to 0.9452 resistance instead.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

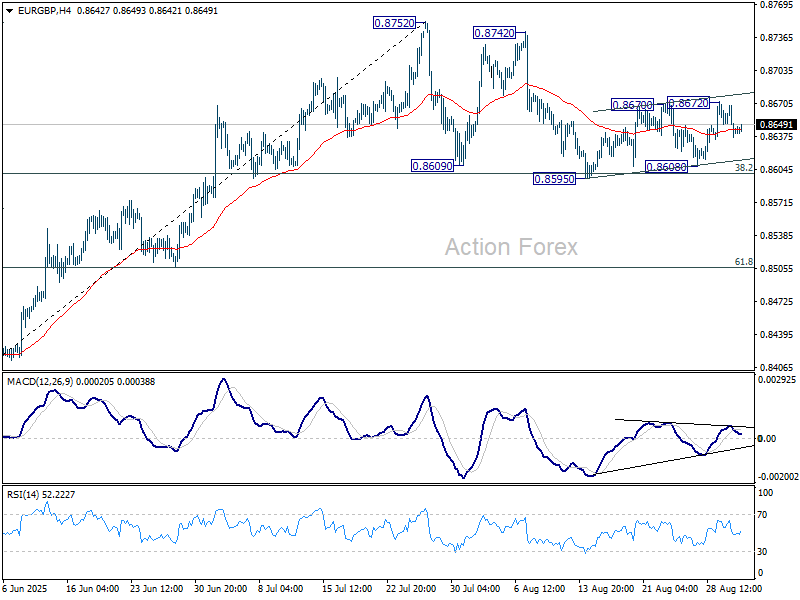

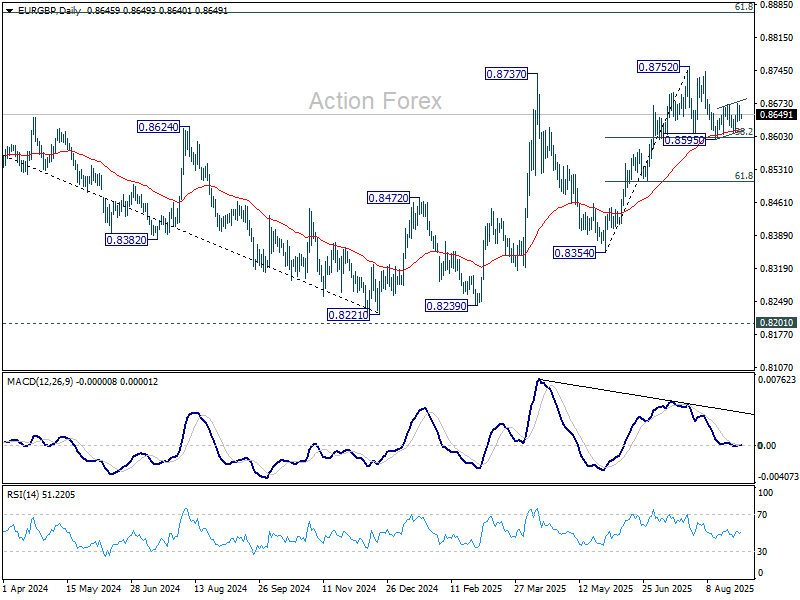

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8632; (P) 0.8652; (R1) 0.8665; More...

EUR/GBP failed to sustain above 0.8670 resistance and retreated, and intraday bias stays neutral. On the upside, firm break of 0.8672 resistance will retain near term bullishness and extend the rebound from 0.8595 to retest 0.8752 high. However, sustained trading below 38.2% retracement of 0.8354 to 0.8752 at 0.8600 will indicate near term bearish reversal and target 61.8% retracement at 0.8506.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8513) will argue that the pattern has completed and bring retest of 0.8221 low.

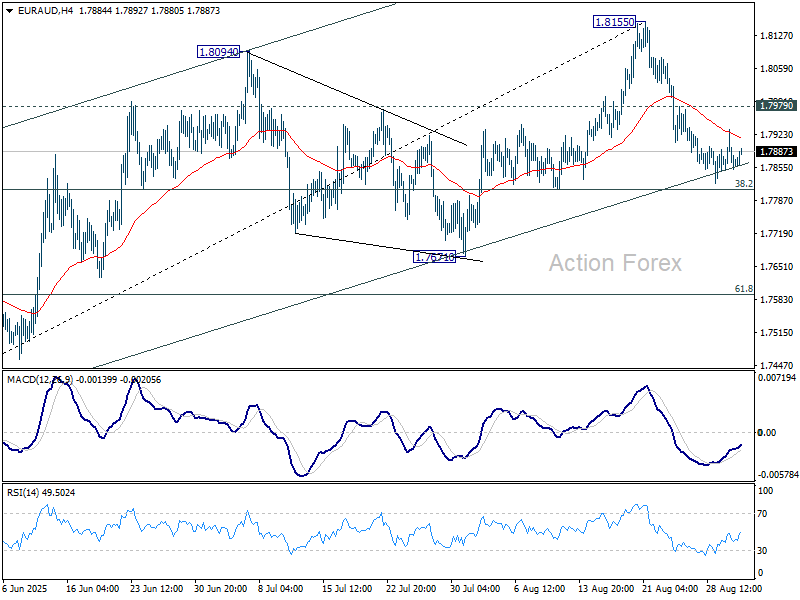

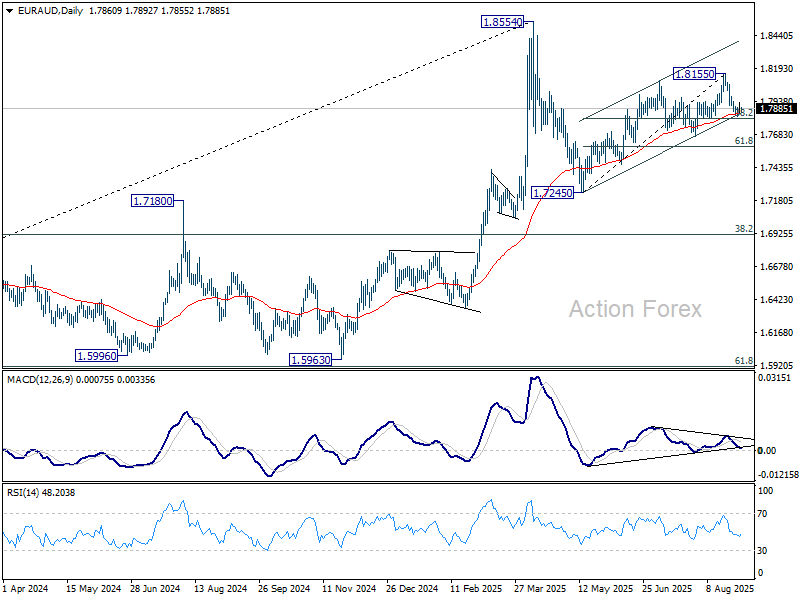

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7834; (P) 1.7884; (R1) 1.7915; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the downside, sustained break of 38.2% retracement of 1.7245 to 1.8155 at 1.7807 should confirm that whole rise from 1.7245 has completed. Corrective pattern from 1.8554 should then be in its third leg. Further decline should be seen to 61.8% retracement at 1.7593. On the upside, break of 1.7979 resistance will retain near term bullishness and bring retest of 1.8155 resistance instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

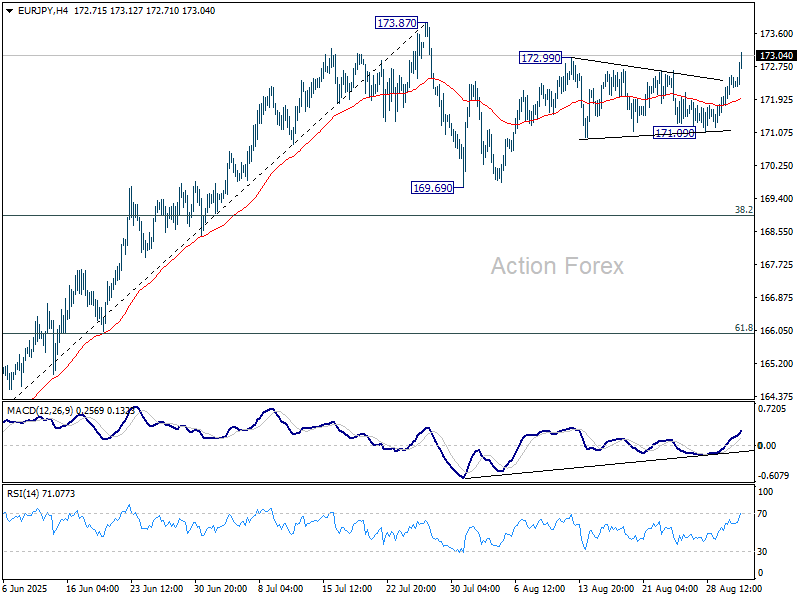

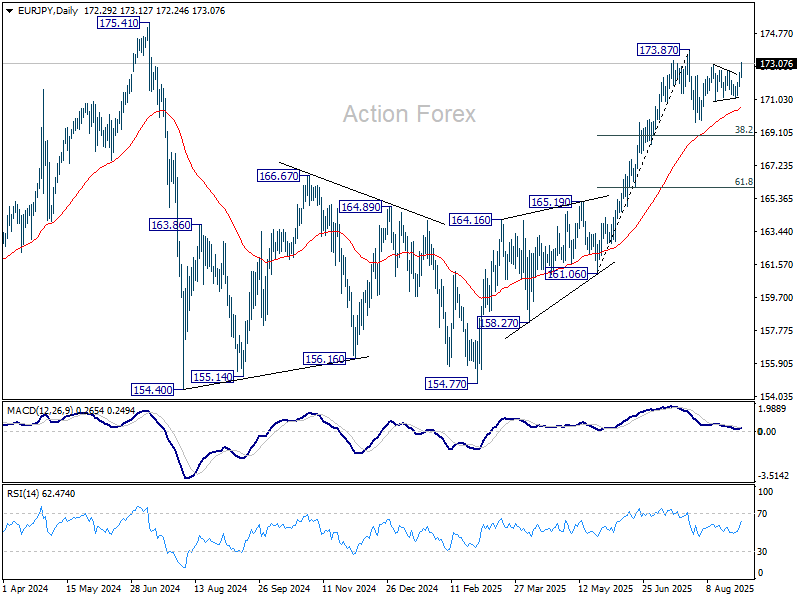

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.94; (P) 172.24; (R1) 172.68; More...

Intraday bias in EUR/JPY is back on the upside with break of 172.99. Further rise should be seen to retest 173.87 high. Decisive break there will resume larger rally from 154.77, and target a retest on 175.41 key resistance. On the downside, however, break of 171.09 will turn bias to the downside for 169.69 support, and possibly below.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, sustained break of 38.2% retracement of 161.06 to 173.87 at 168.97 will delay this bullish case, and probably extend the correction from 175.41 with another fall.

Gold Hits Fresh Record

The week started slowly in the US and Canada as markets were closed for the Labour Day holiday.

In Asia, Chinese equities retreated after Monday’s rally backed by hopes of improved China–India ties. A nearly 20% jump in Alibaba shares, after the company reported a triple-digit surge in AI revenues, lifted the Hang Seng Index by 2% on Monday before some profit-taking this morning. Alibaba briefly reached its highest level since April before pulling back. The Chinese AI rally still appears to have room to run.

In energy, US crude opened the week on a firmer footing as a softer dollar and fading hopes for Ukraine peace talks outweighed concerns over India’s reluctance to buy US crude. Those factors helped oil bulls retest the $65pb resistance, with scope to extend toward $66–67.70pb range that aligns with the 50- and 200-DMAs.

In metals, gold hit a fresh all-time high above $3’500 per ounce in Asia, surpassing its April peak. The rally reflects a softer dollar but also strong central-bank and institutional demand as investors rotate out of US Treasuries. The share of US Treasuries held by foreign central banks has been declining for over a decade, but that shift into gold accelerated this year amid US debt concerns, ratings downgrades, trade tensions and geopolitical risks. Central banks’ gold allocations even surpassed their US Treasury holdings this year. Meanwhile, Indian pension funds are seeking approval to invest in gold ETFs, hinting at strong demand despite record price. Silver also surged to its highest level since 2011. Both metals have further room to run. Yet, with the gold–silver ratio still above its long-term range of 60–80, silver may have greater upside potential.

In Europe, equities posted modest gains on Monday after PMI data suggested a faster expansion in euro area manufacturing. Germany’s figure slipped just below 50, but Italy and France moved back into expansion territory after prolonged contractions. The release helped the euro rise to 1.1736 against a broadly weaker dollar, though sellers quickly re-emerged as the widening French–German 10-year yield spread revived concerns over French political risk. Separately, Paris accused Rome of fiscal dampening, adding another layer to French tensions. That said, France’s budget strains are not viewed as contagious so far, which should limit broader euro-area fallout. The CAC 40 remains vulnerable — both to fiscal worries and weakening demand in the luxury sector — while the broader Stoxx 600 has been supported by strength in defense, utilities, and banks. Any French-related selloff could be interesting buying opportunity.

On the data front, attention now shifts to the euro-area CPI flash estimate for August. Headline inflation is expected at 2.0%, with core easing to 2.2% — both near the European Central Bank’s (ECB) target. A print in line with expectations should reinforce the view that the ECB will hold rates steady in September. The next move is still likely a cut; softer growth could justify one more 25bp reduction by year-end. Yet markets now assign less than a 40% chance of another cut in 2025, down from ~50% in July.

This relative hawkishness versus the Federal Reserve (Fed) has supported the euro’s rebound since late August. However, if eurozone growth disappoints, ECB doves could regain the upper hand. CFTC data show net speculative euro longs have risen sharply this year, largely on hopes of stronger military/security spending and diversification away from US assets. Central banks have also increased their euro holdings: official buyers accounted for 20% of eurozone bond issuance so far in 2025 (vs. 16% in 2024), while an OMFIF survey pointed at a net 16% of central banks plan to increase euro reserves over the next 12–24 months (vs. 7% last year).

In the short term, the euro’s appreciation already reflects much of this, meaning crowded long positioning could leave it vulnerable to a pullback. A flare-up in French politics would be a natural trigger. But in the medium run, the euro’s outlook remains constructive thanks to diversification away from US assets.

Eyes on Euro Area Inflation

In focus today

In the euro area, flash inflation figures for August will be released. Following lower-than-expected inflation in France, Spain, Italy, we project euro area HICP inflation to come in at 2.0% y/y, below the expected 2.1% y/y, despite an upside surprise in Germany. For the ECB, we anticipate that the August inflation print will not alter their assessment of inflation, and we continue to expect the deposit rate to remain unchanged at 2% through the rest of the year and in 2026.

From the US, ISM Manufacturing index will be released for August in the afternoon. The preliminary PMI released earlier surprised clearly to the upside, and the regional Fed manufacturing indices are also pointing towards an uptick despite the ongoing political.

Economic and market news

What happened yesterday

In the euro area, the unemployment rate fell to 6.2% in July from 6.3% in June, as widely expected, driven by a reduction in unemployed persons. The decline was primarily led by Greece and Italy, while France and Germany recorded slight increases in unemployment. We expect modest employment growth in the coming years, aligning with workforce expansion, and project an average unemployment rate of 6.2% in 2025 and 6.1% in 2026. The unemployment rate is likely to remain a hawkish argument for the ECB.

Additionally, euro area final manufacturing PMI was revised up to 50.7 in August, making a larger upside than initially reported. The revision was largely driven by France, where the manufacturing sector continues to benefit from lower interest rates and energy prices, a trend we expect to persist for the remainder of 2025.

In Sweden, manufacturing PMI rose to 55.3 in August from 54.4 in July, reaching a new high for 2025. While PMI shows stronger momentum, it contrasts with the less optimistic NIER survey on manufacturing confidence. As PMI often leads, it could signal a potential recovery in the NIER survey. Growth was primarily driven by business volume, new orders and delivery times, with reduced global trade policy uncertainty also contributing.

In Norway, manufacturing PMI fell to 49.6 in August (prior: 51.1), indicating a slowdown in manufacturing activity. However, it is important to note that hard data has been significantly stronger than PMI signals throughout Q2 and into Q3, so we currently place limited emphasis on PMI readings. Employment dropped to 42.8, the lowest since May 2020, aligning with Friday's NAV figures and reflecting weakening labour demand.

Equities: European equities edged slightly higher yesterday, rising 0.3% (Eurostoxx 50), while US markets were closed. Industrials outperformed, likely buoyed by the slight positive revision in the European manufacturing PMI and the record-low unemployment rate in the euro area. Additionally, Swedish PMIs delivered very strong results. Sweden often leads the European manufacturing cycle by approximately nine months, making this noteworthy. The headline PMI printed at 55, with orders accelerating to an index level of 57. This indicates a sharp sequential improvement in August and represents the best momentum in the sector since 2021/2022.

FI and FX: NOK and SEK were on the rise yesterday - the latter supported by stronger PMIs, while the former shrugged off disappointing PMIs. EUR/SEK slipped below 11.00 for the first since June. EUR/USD hovered in the 1.16-1.17 range despite heightened French political uncertainty. Bond yields in Europe rose a couple of basis points yesterday, with UK slightly underperforming European peers. Tightening pressure on the 10Y German swap spread prevailed yesterday.

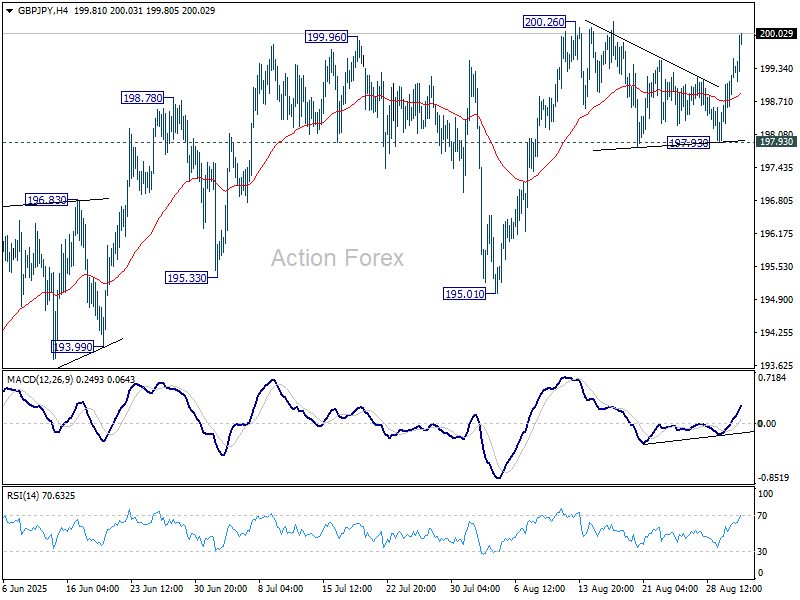

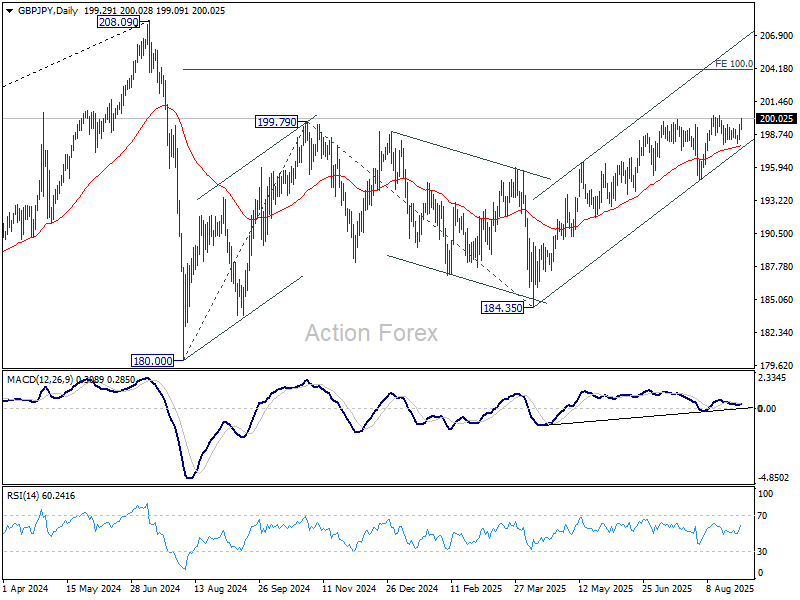

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.65; (P) 199.10; (R1) 199.83; More...

Immediate focus is now on 200.26 resistance in GBP/JPY with today's strong rally. Firm break there will confirm resumption of whole rise from 184.35, and that from 180.00. Further rally should then be seen to 100% projection of 180.00 to 199.79 from 184.35 at 204.14. On the downside, however, break of 197.93 support should confirm short term topping, and turn bias to the downside for 195.01 support next.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Yen Weakens on Trade Stalemate, Doubts on BoJ’s Next Move

Yen dominated currency moves in an otherwise subdued Asian session, with broad-based selling gathering pace. After weeks of range-bound trading, the Japanese currency may finally be breaking lower, particularly in the crosses where momentum is building.

Trade uncertainty is a central factor. Japan is still waiting for a formal executive order from U.S. President Donald Trump to reduce auto tariffs, a key sticking point in bilateral negotiations. Talks hit another setback last week when Tokyo’s top negotiator abruptly canceled a visit to Washington, leaving no new date on the calendar. Ryosei Akazawa confirmed today that no rescheduling has been arranged. The lack of progress casts doubt on Japan’s hopes for near-term relief, adding pressure to a currency that has already been undermined by shifting policy expectations.

At the same time, a senior BoJ official warned that the risk of a “larger-than-expected impact” from tariffs now deserves greater attention than the prospect of a mild slowdown. With a confirmed trade deal, the BoJ might be able to raise rates again later this year. But without clarity on the tariff front, comments from Deputy Governor Ryozo Himino suggest patience will be required. The central bank looks more likely to wait for stronger confirmation that trade risks are subsiding before adjusting policy again.

As a result, Yen is underperforming across the board, currently the weakest currency of the week. It is followed by Kiwi and Swiss Franc. Sterling leads the pack, followed by Euro and Dollar. Aussie and Loonie are trading mid-range.

Looking ahead, attention will turn to Eurozone CPI flash data and the U.S. ISM manufacturing survey later in the day. Eurozone headline CPI is expected to tick up to 2.1% with core slipping slightly to 2.2%. With inflation hovering near target, the ECB faces little pressure to cut further unless economic activity worsens in response to August’s tariff escalations.

In the U.S., ISM manufacturing is expected to remain in contraction at 48.6, with employment and prices subcomponents drawing close scrutiny. Still, the main event of the week will be Friday’s nonfarm payrolls report, which is poised to shape expectations for the Fed’s September policy move.

In Asia, at the time of writing, Nikkei is down -0.18%. Hong Kong HSI is down -0.67%. China Shanghai SSE is down -1.05%. Singapore Strait Times is up 0.47%. Japan 10-year JGB yield is down -0.018 at 1.607.

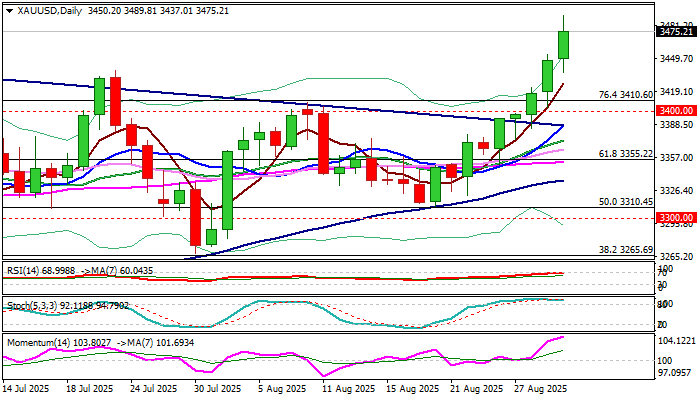

Gold breaks above 3,500, Fed pressure adds fuel

Gold’s rally accelerated this week, surging past 3,500 level for the first time in history. The move reflects growing conviction that the Fed’s rate-cut cycle will extend deep into 2026, eventually bringing policy back to neutral at around 3.00%. With global uncertainty mounting and political interference in Washington intensifying, the precious metal continues to draw strong demand as a hedge.

U.S. President Donald Trump has amplified calls for more aggressive easing, declaring in a social media post that “Prices are WAY DOWN in the USA, with virtually no inflation.” Treasury Secretary Scott Bessent added to the pressure, accusing the Fed of “a lot of mistakes” and backing Trump’s effort to remove Governor Lisa Cook. Bessent also urged swift Senate confirmation of White House economic adviser Stephen Miran to temporarily replace Adriana Kugler, who resigned earlier this month, for the upcoming FOMC meeting this month.

Investors increasingly view Gold as a shield against political intrusion into monetary policy, particularly as institutional frictions grow louder in the run-up to key policy meetings. The combination of dovish expectations and political pressure has fueled the current strong rally.

Technically, while there may be some jitters for Gold at the current 3,500 psychological resistance, near term outlook will stay bullish as long as 3,408.21 resistance turned support holds.

Current rally should target 161.8% projection of 3,267.90 to 3,408.21 from 3,311.30 at 3,538.32 in the near term. Firm break there will pave the way to 261.8% projection at 261.8% projection at 3,678.63 next.

BoJ’s Himino: Risk of larger-than-expected tariff impact warrants focus

BoJ Deputy Governor Ryozo Himino warned in a speech today that U.S. trade policies are likely to weigh on Japan’s economy, with overseas slowdowns and weaker corporate profits feeding through domestically. While accommodative financial conditions should cushion the hit, Himino said the baseline scenario is for Japan’s growth to “moderate,” with downside risks from tariffs deserving greater attention.

Looking further ahead, Himino said Japan’s growth should eventually recover as overseas economies return to a more stable expansion path. But in the near term, the tariff shock remains the key uncertainty, with the risk of a “larger-than-expected impact” now seen as more pressing than the chance of a mild outcome.

On inflation, Himino noted that headline prices remain above the BoJ’s 2% target, by a "considerable margin", due in part to surging rice prices and spillovers to other goods. However, he stressed headline inflation is expected to "decline in due course" as food-related effects fade. Underlying inflation, meanwhile, remains below target but is steadily rising, despite some potential "temporary halts", supported by a wage–price feedback loop.

Summing up, Himino said the BoJ’s baseline scenario assumes headline inflation will cool, while core prices continue to edge toward 2%. If that path holds, it would be appropriate for the central bank to keep raising rates gradually, fine-tuning monetary accommodation in line with improving economic activity and stable price gains.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.65; (P) 199.10; (R1) 199.83; More...

Immediate focus is now on 200.26 resistance in GBP/JPY with today's strong rally. Firm break there will confirm resumption of whole rise from 184.35, and that from 180.00. Further rally should then be seen to 100% projection of 180.00 to 199.79 from 184.35 at 204.14. On the downside, however, break of 197.93 support should confirm short term topping, and turn bias to the downside for 195.01 support next.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Gold Holds Near New Record High, US Labor Data May Spark Fresh Rally

Gold continued to trend higher and spiked to the highest levels since late April, just ticks under new record high on Monday.

Weaker dollar on growing bets for Fed’s September rate cut, following more dovish comments from US policymakers and fresh US political turmoil, along with darkened economic and geopolitical outlook, continue to fuel safe haven demand.

Markets await release of US jobs data (due on Friday) for the latest update from the US labor sector, which weakened significantly in past couple of months and is mainly behind Fed’s dovish stance lately.

New record high ($3500) marks very strong resistance which is likely to provide strong headwinds and probably keep the action capped until markets get fresh signals from US labor data.

According to the forecasts, situation in the US labor sector is unlikely to improve, as economists see NFP almost unchanged in August, while hiring in private sector is forecasted to drop and create new jobs too, that contributes to negative outlook.

Overbought daily studies contribute to scenario of consolidation under new all-time high, while development of bullish continuation pattern on monthly chart suggests that bulls may resume after longer consolidation.

Gold may break into uncharted territory after a few month pause if data show persistent weakness in the labor sector that would further weaken the dollar.

Firm break of $3500 to expose projected targets at $3544, $3569 and $3600 (round-figure).

Former tops at $3452 and $3438 reverted to supports, with extended dips to hold above $3410/00 zone to keep larger bulls intact..

Res: 3489; 3500; 3544; 3569

Sup: 3453; 3438; 3410; 3400