Sample Category Title

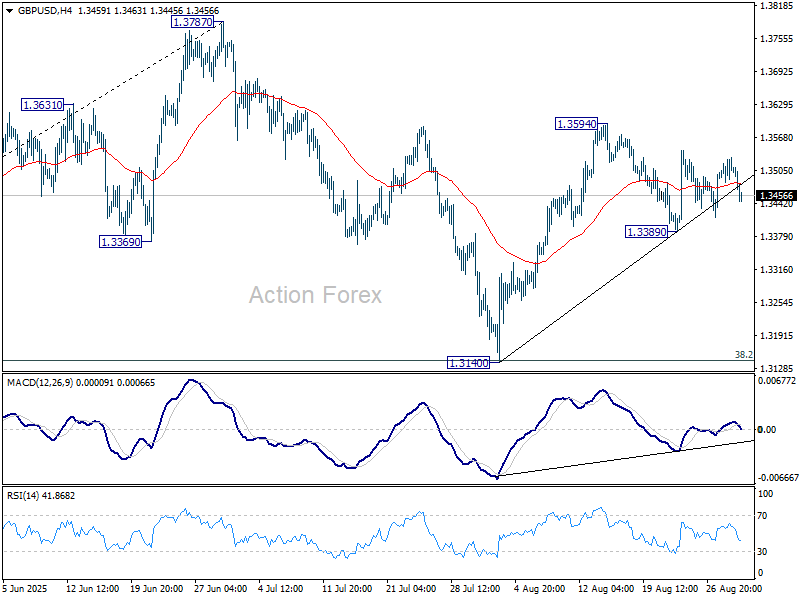

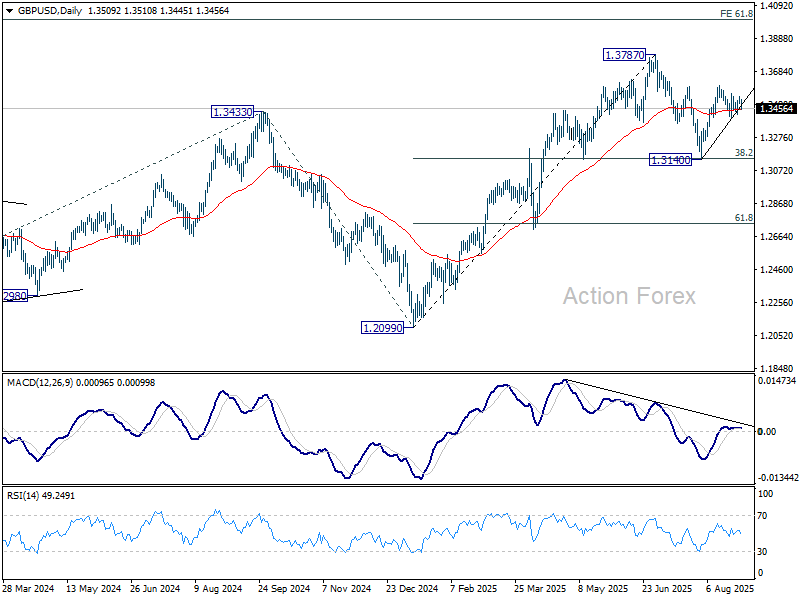

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3486; (P) 1.3509; (R1) 1.3534; More...

GBP/USD is still bounded in established range and intraday bias remains neutral. Further rally is mildly in favor as long as 1.3389 support holds. Above 1.3594 will resume the rebound from 1.3140 to retest 1.3787 high. On the downside, however, break of 1.3389 support will extend the corrective pattern from 1.3787 with another fall, and target 1.3140 support.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3073) holds, even in case of deep pullback.

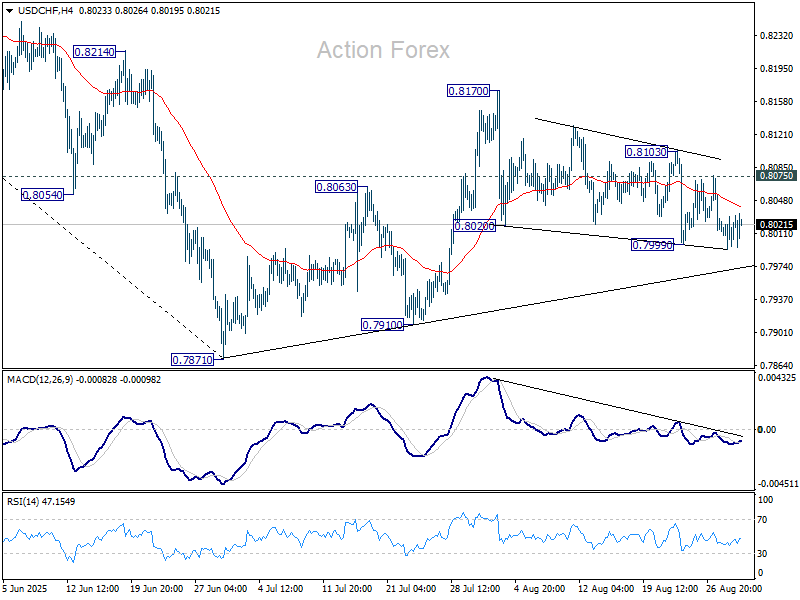

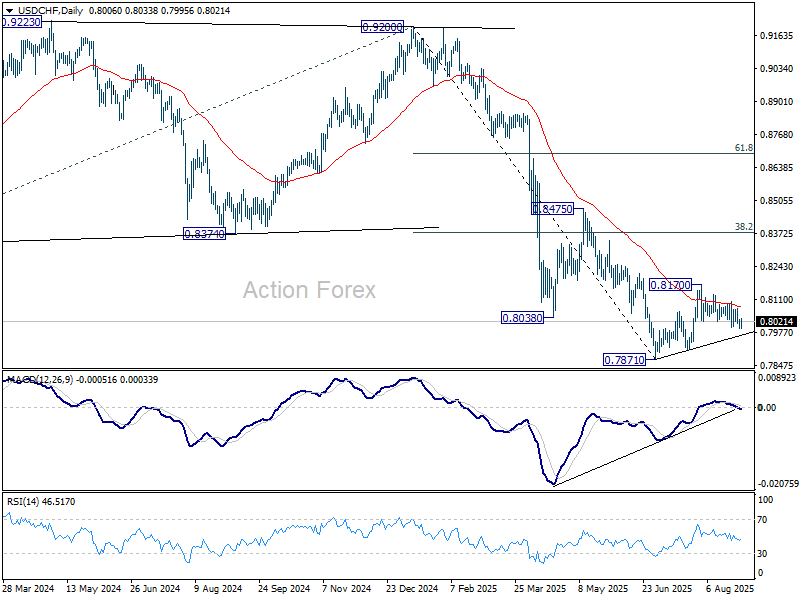

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7991; (P) 0.8017; (R1) 0.8040; More….

Intraday bias in USD/CHF remains mildly on the downside for the moment. Deeper fall would be seen to 0.7910 support first. Break there should confirm that corrective rebound from 0.7871 has completed at 0.8170. On the upside, however, break of 0.8073 will turn bias to the upside for 0.8103. Further break there will resume the rebound from 0.7871 through 0.8170 resistance.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

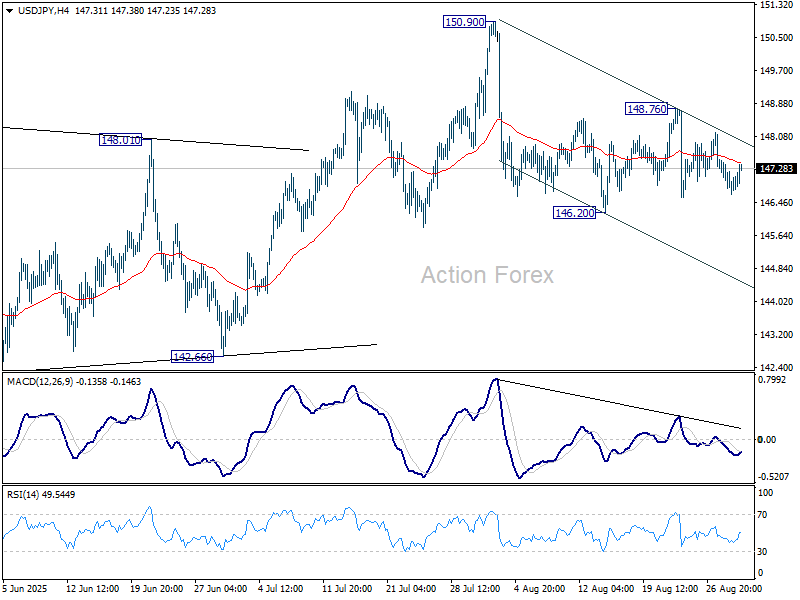

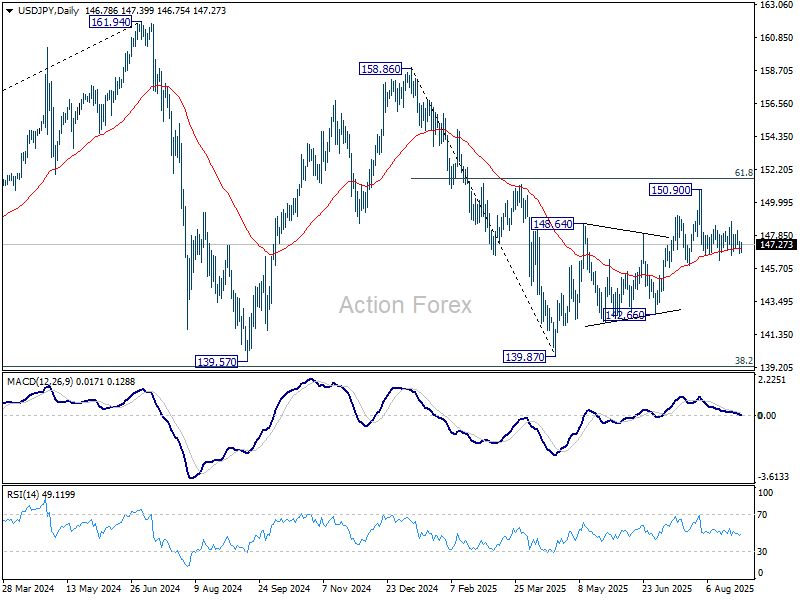

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.56; (P) 147.03; (R1) 147.41; More...

USD/JPY is still bounded in established range and intraday bias stays neutral. On the downside, firm break of 146.20 will resume the fall from 150.90. Also, that would argue that rebound from 139.87 has completed as a corrective move to 150.90. Deeper fall should be seen to 142.667 support for confirmation. On the upside, above 148.76 will bring another rise to retest 150.90 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

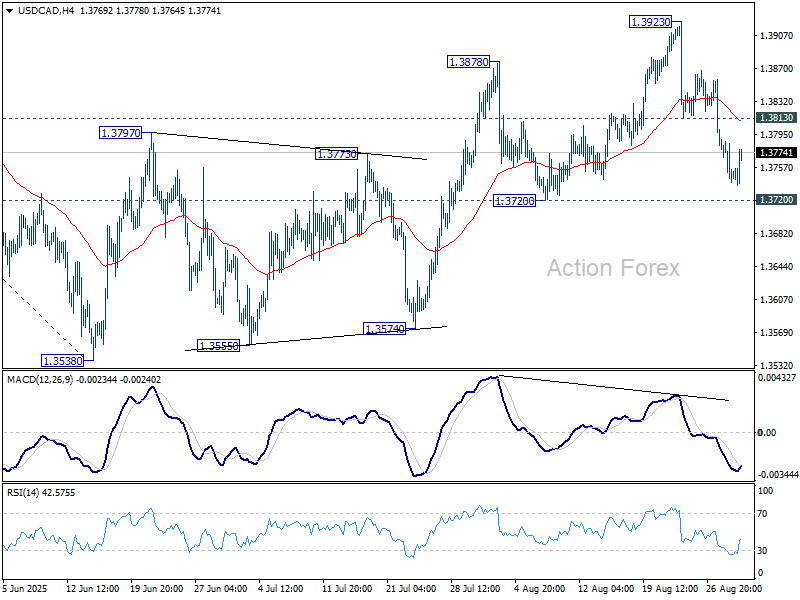

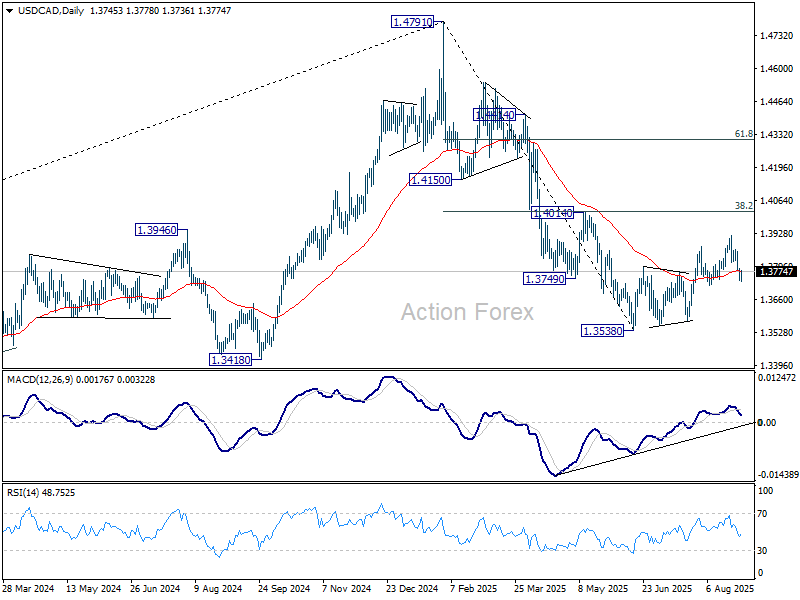

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3729; (P) 1.3761; (R1) 1.3782; More...

Intraday bias in USD/CAD stays neutral first despite current recovery. On the upside, firm break of 1.3813 will indicate that the pullback from 1.3923 has completed, and corrective rise from 1.3538 is still in progress. Retest of 1.3923 should be seen next. But upside should be limited by 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017). Meanwhile, firm break of 1.3720 will argue that the corrective bounce has already completed, and bring retest of 1.3538 low.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Canada GDP Miss Sends Loonie Lower, BoC Rate Cut Bets Rise

Canadian Dollar came under pressure in early U.S. session after GDP data revealed a deeper slowdown than markets had anticipated. Canada’s economy contracted -0.4% qoq in Q2, marking its first quarterly decline in seven quarters. More concerning was June’s monthly contraction, which signaled that the weakness might carry on into Q3.

The drag came primarily from exports, which tumbled under the weight of U.S. tariffs. With auto exports collapsing and machinery shipments down sharply, external headwinds are likely to remain a persistent strain on Canada’s economy in the months ahead.

The disappointing GDP print has shifted attention back to the BoC, where markets now see increased odds of a September rate cut. After holding for three straight meetings, the weak growth outlook could prompt policymakers to restart easing in an effort to cushion the economy.

In contrast, U.S. data releases offered few surprises. Core PCE inflation rose in line with forecasts while personal spending remained solid. The resilience in household demand suggests the U.S. economy retains some momentum, and it did little to alter expectations for Fed easing.

Markets still anticipate September as the starting point of the Fed’s new easing cycle, with two cuts expected in total this year. However, the next two weeks—featuring the August nonfarm payrolls and CPI reports—will be pivotal in determining how aggressive the Fed can be.

In weekly currency performance, Aussie remains the strongest, followed by Loonie and Kiwi. On the weaker side, Euro leads losses, trailed by Sterling and Yen, while Swiss Franc and Dollar sit in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.16%. DAX is down -0.14%. CAC is down -0.34%. UK 10-year yield is up 0.019 at 4.721. Germany 10-year yield is up 0.016 at 2.714. Earlier in Asia, Nikkei fell -0.26%. Hong Kong HSI rose 0.32%. China Shanghai SSE rose 0.37%. Singapore Strait Times rose 0.37%. Japan 10-year JGB yield fell -0.013 to 1.605.

US Core PCE ticks higher to 2.9%, spending stays firm in July

U.S. headline inflation held steady in July, with the PCE price index unchanged at 2.6% yoy. Core measure ticked up to 2.9% from 2.8%, in line with forecasts. On a monthly basis, PCE rose 0.2% mom, and core prices increased 0.3% mom, pointing to modest but persistent price pressures.

Personal income rose 0.4% mom and spending climbed 0.5% mom, both as expected. The data suggest households remain resilient despite elevated borrowing costs, giving the Fed little urgency to accelerate easing.

Canada GDP contracts -04% qoq in Q2, tariffs hit exports hard

Canada’s economy shrank -0.4% qoq in Q2, as exports and business investment fell sharply. The downturn was led by a steep -7.5% drop qoq in exports, with machinery, travel services, and particularly autos hit hard by U.S.-imposed tariffs. Passenger car and light truck exports plunged -24.7% qoq.

Meanwhile, imports fell -1.3% in the quarter, reflecting Ottawa’s counter-tariff measures against the U.S. That helped cushion the trade balance slightly, though it also underscored the disruption in cross-border commerce.

Monthly GDP data painted an equally weak picture, with output slipping -0.1% mom in June versus expectations for modest growth of 0.1% mom.

ECB consumer survey shows long-term inflation anchored, growth views weaken

The ECB’s July Consumer Expectations Survey showed households continue to see inflation remaining above target in the near term, with 12-month expectations steady at 2.6% and three-year expectations edging higher to 2.5% from 2.4%. Five-year inflation expectations were unchanged at 2.1% for an eighth consecutive month, underscoring anchored long-term views.

Notably, uncertainty around one-year inflation stayed at its lowest since January 2022, with the median at 1.6%. This suggests households feel more confident about the inflation outlook, even as near-term expectations remain somewhat elevated.

Growth and labor market expectations turned more downbeat. Economic growth was expected to contract by -1.2% over the next 12 months, compared with -1.0% in June. Unemployment expectations rose to 10.6% from 10.3%. The results highlight continued pessimism about the Eurozone’s economic prospects despite inflation stability.

Tokyo CPI core eases on to 2.5% yoy, but food inflation remains stubborn

Japan’s Tokyo CPI slowed in August as government fuel subsidies pushed down utility bills, but stubborn food inflation kept underlying price pressures elevated. Core CPI excluding fresh food eased to 2.5% yoy from 2.9% yoy, below expectations of 2.6% yoy. Headline CPI also cooled to 2.6% yoy, while the narrower core measure excluding both food and energy edged down to 3.0% yoy from 3.1% yoy.

Food inflation, however, remained sticky. Prices of rice, coffee beans and other groceries kept food CPI ex-fresh food at 7.4% yoy, unchanged from the previous month, highlighting persistent pressure on household budgets.

On the activity side, July industrial production dropped -1.6% mom, worse than forecasts of -1.0% mom, dragged down by a -6.7% mom slump in auto output. Manufacturers expect a rebound of 2.8% mom in August before a modest -0.3% mom dip in September.

Retail sales disappointed, rising only 0.3% yoy against expectations of 1.8% yoy. The labor market was a bright spot, with unemployment falling to from 2.5% to 2.3%, the lowest since December 2019.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3729; (P) 1.3761; (R1) 1.3782; More...

Intraday bias in USD/CAD stays neutral first despite current recovery. On the upside, firm break of 1.3813 will indicate that the pullback from 1.3923 has completed, and corrective rise from 1.3538 is still in progress. Retest of 1.3923 should be seen next. But upside should be limited by 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017). Meanwhile, firm break of 1.3720 will argue that the corrective bounce has already completed, and bring retest of 1.3538 low.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Canada GDP contracts -04% qoq in Q2, tariffs hit exports hard

Canada’s economy shrank -0.4% qoq in Q2, as exports and business investment fell sharply. The downturn was led by a steep -7.5% drop qoq in exports, with machinery, travel services, and particularly autos hit hard by U.S.-imposed tariffs. Passenger car and light truck exports plunged -24.7% qoq.

Meanwhile, imports fell -1.3% in the quarter, reflecting Ottawa’s counter-tariff measures against the U.S. That helped cushion the trade balance slightly, though it also underscored the disruption in cross-border commerce.

Monthly GDP data painted an equally weak picture, with output slipping -0.1% mom in June versus expectations for modest growth of 0.1% mom.

US Core PCE ticks higher to 2.9%, spending stays firm in July

U.S. headline inflation held steady in July, with the PCE price index unchanged at 2.6% yoy. Core measure ticked up to 2.9% from 2.8%, in line with forecasts. On a monthly basis, PCE rose 0.2% mom, and core prices increased 0.3% mom, pointing to modest but persistent price pressures.

Personal income rose 0.4% mom and spending climbed 0.5% mom, both as expected. The data suggest households remain resilient despite elevated borrowing costs, giving the Fed little urgency to accelerate easing.

USD/JPY Technical: Eyeing the Ascending Range Support of 145.50

USD/JPY has extended its gradual decline from the 28 July 2025 high of 150.92, losing -2.6% to reach an intraday low of 147.00 at the time of writing.

Today’s Tokyo inflation data and August consumer confidence figures reinforce expectations of a potential 25-basis-point rate hike by the Bank of Japan in October, as it continues along its path of monetary policy normalization.

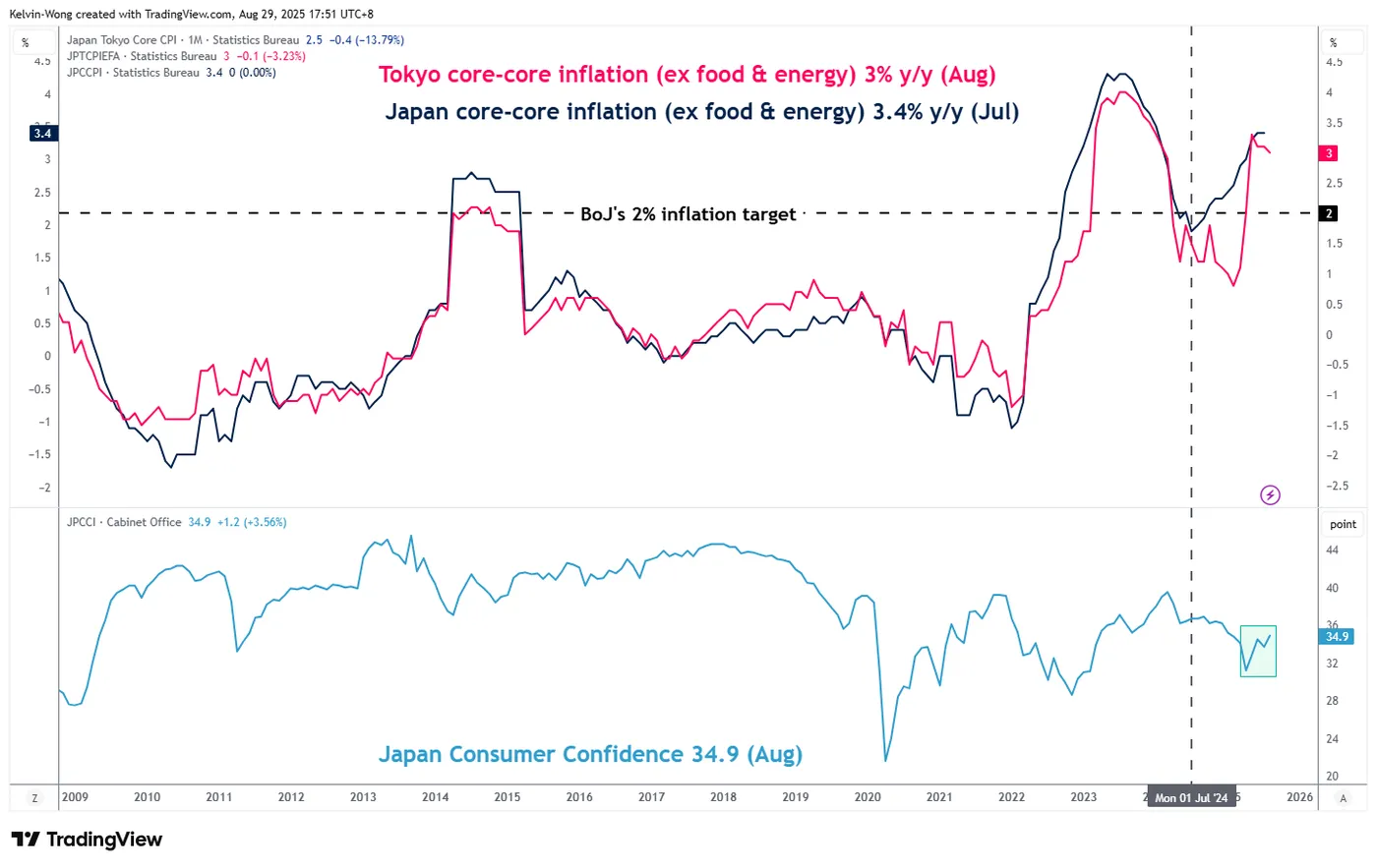

Tokyo inflation and Japan consumer confidence support another BoJ rate hike

Fig. 1: Tokyo core-core inflation & Japan Consumer Confidence as of Aug 2025 (Source: TradingView)

Tokyo core-core inflation (excluding food and energy) rose by 3% y/y in August, a slight slowdown from July’s print of 3.1% but still well above BoJ’s long-term inflation target of 2% (see Fig. 1).

Japan’s consumer confidence index improved further to 34.9 in August from its current year-to-month low of 31.2 printed in April. This marked the highest reading since January seen across all the components; overall livelihood (32.7 vs 31.4 in July), income growth expectations (39.4 vs 38.5), employment outlook (39.3 vs 37.6), and willingness to purchase durable goods (28 vs 27.4).

Fig. 2: USD/JPY minor trend as of 29 Aug 2025 (Source: TradingView)

Preferred trend bias (1-3 days)

Bearish bias below 148.00/148.18 key short-term pivotal resistance.

A break below 146.40 intermediate support (minor swing low area of 14 August 2025) opens the scope for a further potential slide towards the next supports at 145.85 (minor swing lows of 8 July/10 July/24 July 2025) and 145.50 (the lower boundary of the ascending range configuration) (see Fig. 2).

Key elements

- Price actions of the USD/JPY have traded back below its 20-day moving average, and it is now challenging the 50-day moving average.

- The USD/JPY is still oscillating within a medium-term ascending range configuration since the 22 April 2025 low of 139.90.

- The hourly Stochastic oscillator is now attempting to shape a bearish breakdown from its parallel ascending support, which suggests a potential resurgence of bearish momentum conditions at least in the short term.

Alternative trend bias (1 to 3 days)

The key near-term risk event is the upcoming release of July’s US core PCE inflation, along with personal income and spending data later today, which will play a pivotal role in shaping Federal Reserve rate cut expectations ahead of the September FOMC meeting.

A clearance above 148.18 invalidates the bearish scenario and sees a squeeze up towards the upper limit of the medium-term ascending range configuration for the next intermediate resistance to come in at 148.75 (also close to the 200-day moving average).

NZD/USD Rises by ~1.4% in 2 Days

As the NZD/USD chart shows, the New Zealand dollar was trading around 0.5820 against the US dollar on Wednesday, but today it has climbed above 0.5895 – an impressive gain of approximately 1.4% in just two days.

The rise in NZD/USD is being driven both by the general weakening of the US dollar ahead of the Federal Reserve’s expected September rate cut, and by strengthening demand for the “kiwi”. As Reuters notes:

→ the New Zealand dollar is often used as a substitute for the yuan because of close trade relations with China;

→ meanwhile, the yuan is strengthening, with Chinese policymakers recommending support for the currency given its low valuation and the need to facilitate trade negotiations with the US.

Technical Analysis of the NZD/USD Chart

It’s worth paying attention to the unusual trading activity (marked by the arrow) and its context:

→ it was the lowest level in more than four months;

→ after a sharp decline, the price stabilised near the lower boundary of the channel;

→ trading was fairly active, and although the price was drifting lower, it failed to generate strong bearish momentum.

It is possible that so-called Smart Money was attracted by the undervalued asset, preventing further declines through buy orders and accumulating long positions. If so, from this perspective it is notable that:

→ the 0.5820 level acted as support on Wednesday – the price rebounded sharply;

→ yesterday NZD/USD moved into the upper half of the channel, breaking through the 0.5875 resistance.

This week’s price rise has formed a trajectory marked by purple lines. NZD/USD might be heading towards the upper boundary of the ascending channel, with the following resistance levels standing out along the way:

→ the former support at 0.5910;

→ the 50% Fibonacci retracement level from the A→B move.

An attempt to break through this resistance zone could result in a pullback towards the lower boundary of the purple channel.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

August the Best Month for Gold Since April

Gold (XAUUSD) is holding steady near USD 3,410 per ounce on Friday, just shy of its monthly high, and is set to close its second straight week with gains. The metal is supported by a weaker dollar and consistent safe-haven demand as uncertainty over the Federal Reserve’s policy path lingers.

Dollar weakness and Fed uncertainty support gold

Investors are moving into gold amid concerns that political pressure on the Fed could accelerate the pace of rate cuts. Markets are already pricing in a 25 basis point cut in September. Further support came from Fed Board member Christopher Waller, who said he expects rates to begin falling as early as next month, aligning with other policymakers’ dovish stance.

Attention now turns to the upcoming US household spending report, which is forecast to show stronger growth. This follows revised Q2 GDP data, which revealed slightly higher-than-expected economic expansion. However, concerns about rising inflation are also mounting, keeping gold attractive as a hedge.

Overall, August is shaping up to be gold’s strongest month since April, with prices consolidating at the upper end of the range, underpinned by a mix of dollar weakness and growing economic uncertainty.

Technical analysis of XAUUSD

On the H4 timeframe, gold completed a growth wave to 3,423, marking a local target. A decline towards 3,371 is now in play, with the market continuing to develop a wide consolidation range around this level. A downward breakout would open the way to 3,290, while an upward breakout could extend the range to 3,431 before the downtrend resumes towards 3,290. The MACD indicator supports this view: its signal line is above zero at the highs but has left the histogram zone, a sign of potential weakness and the beginning of a move towards new lows.

On the H1 chart, XAUUSD formed a consolidation range around 3,368 and broke upwards, completing the third growth wave at 3,420. The market has now started a downward correction towards 3,368. After reaching this level, a compact consolidation range is expected. A downward breakout would confirm continuation of the decline to 3,290, while an upward breakout could produce another growth structure towards at least 3,425. The Stochastic oscillator confirms the bearish correction, with its signal line below 50 and heading strictly towards 20.

Summary

Gold is consolidating near highs after its best monthly performance since April. While short-term corrections towards 3,371 and 3,290 remain likely, broader support from a weak dollar, Fed policy uncertainty, and inflation concerns continues to underpin the bullish outlook. Resistance levels are at 3,423–3,431, while support lies at 3,371 and 3,290.