Sample Category Title

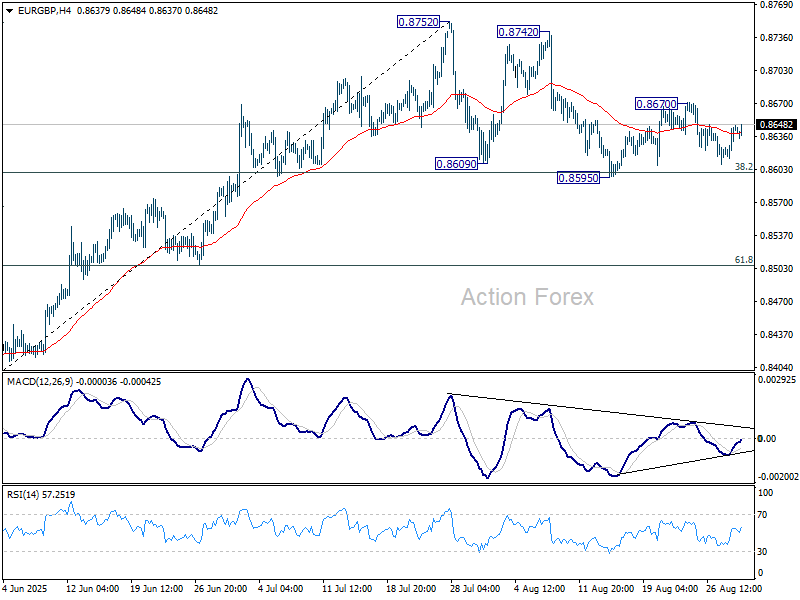

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8624; (P) 0.8637; (R1) 0.8658; More...

Range trading continues in EUR/GBP and intraday bias stays neutral. On the downside, sustained trading below 38.2% retracement of 0.8354 to 0.8752 at 0.8600 will indicate near term bearish reversal and target 61.8% retracement at 0.8506. On the upside, above 0.8670 will retain near term bullishness, and turn bias to the upside for retesting 0.8752 high.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8508) holds.

Dovish Pivot by Fed Chair Powell Takes the Edge of Today’s July PCE Deflators

Markets

Markets turn somewhat more complacent over US political developments. They take a wait-and-see approach with Fed governor Cook yesterday suing US President Trump calling his move to fire her a power grab with potentially irreparable harm to the US economy. She also asked to preserve her current role at the Fed during the lawsuit to protect public interests. A first emergency hearing is set for today with rulings in the case coming in the next days and weeks and remaining a potential source of market stress/volatility. Fed governor Cook also suggested that an unintentional “clerical error” might have been behind the mortgage fraud allegations resulting in President Trump’s decision to fire her for cause. In absence of other strong drivers, US Treasuries corrected on the recent bull steepening with daily changes ranging between +2 bps (2-yr) and -4.5 bps (30-yr). Fed governor Waller, who dissented in July, argued again in favour of lower interest rates: “With underlying inflation close to 2%, market-based measures of longer-term inflation expectations firmly anchored, and the chances of an undesirable weakening in the labor market increased, proper risk management means the FOMC should be cutting the policy rate now.” His base scenario remains a 25 bps rate cut but he wouldn’t mind opting for a jumbo move (50 bps) if next week’s August payrolls report point to a substantially weakening of the economy. Waller expects additional cuts over the next three to six months with the pace being driven by the incoming data. Last week’s dovish pivot by Fed Chair Powell put the onus on labour market data and takes the edge of today’s July PCE deflators. A significant increase in PPI data released earlier this month points to upward risks around the consensus view even as CPI inflation barely showed any signs of (tariff-related) inflation in July. The headline number is forecast to rise by 0.2% M/M and 2.6% Y/Y while the underlying measure is pencilled at 0.3% M/M and 2.9% Y/Y. Even in case of a beat, we don’t think that US money markets will be eager to take on bets on a policy rate status quo in September. So the overall market impact might be low with the approaching long weekend (US closed on Monday for Labour Day) also arguing in favour of subdued trading. European focus turns to national inflation numbers setting the tone for the EMU reading on Monday. The ECB also releases its monthly consumer inflation expectations survey (1y & 3y). With the central bank clearly signalling the monetary policy is in a happy place, we see asymmetric risks with especially sensitivity to upward surprise (weakness at long end of the curve).

News & Views

Japanese data painted a complex economic context this morning as the BOJ is still in the process of assessing the timing of further policy normalization. Tokyo inflation (ex fresh food) as expected eased from 2.9% to 2.5%. The decline was mainly due to government subsidies easing consumer utility bills. The core measure excluding both fresh food and energy only slowed marginally from 3.1% to 3%, holding well above the BOJ’s 2% target. National July activity data mostly disappointed. Industrial production declined 1.6% M/M while only a more modest -1.1% was expected, amongst others due to a drop in car production. July retail sales also printed well below expectations at -1.6% M/M and 0.3% Y/Y. The unemployment rate unexpectedly decline from 2.5% to 2.3%. Persistently high inflation eroding real wage growth and consumer spending, still supports a scenario of the BoJ resuming policy tightening later this year. The market sees a 50% probability of a 25 bps rate hike at the end October policy meeting. According to people familiar with the matter, the Japan Finance Ministry also asked primary dealers on their assessment with respect to the issuance of long term bonds. The Fin Min is said to consider cutting back auctions in this sector after the recent rise in long term yields.

The Polish government yesterday unveiled its 2026 budget. The budget still sees a 2026 budget deficit of 6.5% coming from an upwardly revised 6.9% deficit expected for this year. The budget assumes GDP growth of 3.5% compared to 3.4% expected for this year. The government expects a debt to GDP level of 53.8% (according to national standards) up from 48.9% this year. As such it remains below the 55% prudential standard, that could trigger important budget constraints. General debt-to-GDP as defined by the EU is expected to rise to 66.8% next year from 60.8% this year.

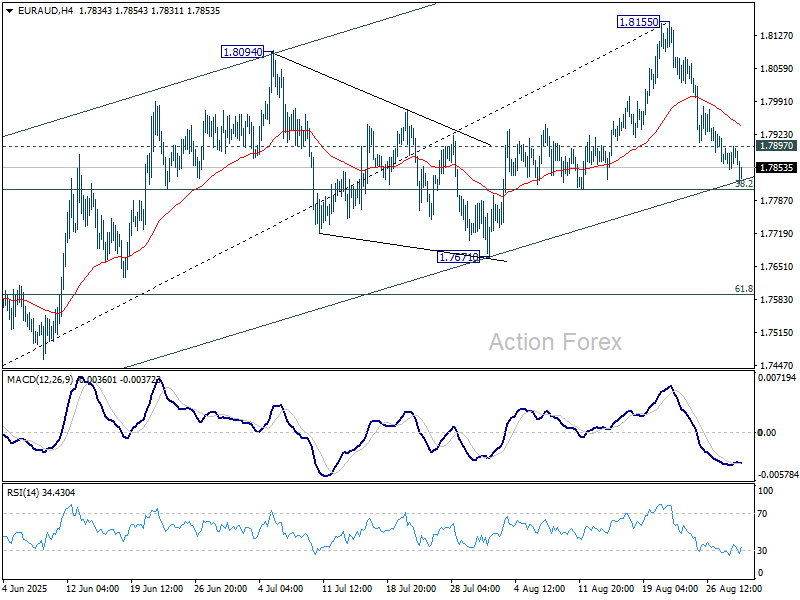

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7859; (P) 1.7879; (R1) 1.7906; More...

EUR/AUD's decline from 1.8155 short term top continues today and intraday bias stays on the downside. Decisive break of 38.2% retracement of 1.7245 to 1.8155 at 1.7807 should confirm that whole rise from 1.7245 has completed. Corrective pattern from 1.8554 should then be in its third leg. Further decline should be seen to 61.8% retracement at 1.7593. On the upside, above 1.7897 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

Aussie Tops FX as China Rally Lifts Mood, Dollar Awaits PCE Data

Aussie and Kiwi are the top performers in FX trading on today so far, supported by the continued surge in Chinese equities. With the local market on course for its biggest monthly rise in nearly a year, risk sentiment spilled into regional currencies, giving both Australian and New Zealand Dollars some fresh momentum.

However, skepticism remains about the durability of the equity boom. The bulk of Chinese household wealth is tied up in property, which remains weak, suggesting that rising stock prices may not deliver much of a consumption boost. Still, for now, markets are embracing the positive sentiment, with the Aussie and Kiwi riding the tide.

Dollar has been more subdued, trading without a clear direction. Investors are holding back ahead of the July PCE release, the Fed’s preferred inflation gauge. Core PCE is expected to edge up to 2.9% yoy, while personal spending is forecast to grow 0.5% mom.

Spending may prove the bigger market mover. Any downside surprise in spending could point to early signs of consumer fatigue, even before August’s tariff escalations hit household budgets. That would bolster the case for the Fed to begin cutting rates in September, a path already widely anticipated.

Fed Governor Christopher Waller, one of the more dovish voices on the Board, urged that rates should eventually move back toward a neutral 3%. Still, he emphasized that the pace of cuts will depend on how data evolve.

In terms of weekly performance, Aussie tops the leaderboard this week, followed by Loonie and Kiwi. Euro is the weakest, trailed by Sterling and Swiss Franc, while Dollar and Yen sit in the middle of the field. That leaves the FX market neatly divided: commodity currencies strong, European currencies weak, and Dollar and Yen mixed.

In Asia, Nikkei fell -0.19%. Hong Kong HSI is up 0.94%. China Shanghai SSE is up 0.43%. Singapore Strait Times is up 0.39%. Japan 10-year JGB yield fell -0.007 to 1.612. Overnight, DOW rose 0.16%. S&P 500 rose 0.32%. NASDAQ rose 0.53% 10-year yield fell -0.031 to 4.207.

Fed’s Waller: Time to start cutting in September, target neutral around 3%

Fed Governor Christopher Waller said he would support a 25bps cut at the September 16–17 FOMC meeting, warning that waiting for further labor market deterioration would risk the Fed “falling behind the curve.” He said conditions warrant a move now to put policy on a path toward neutral.

He placed the neutral rate near 3%, around 125–150bps below current levels. While not convinced the Fed is behind the curve yet, he emphasized that signaling a path toward neutral is a way to reassure markets that the Fed won’t let policy remain too tight for too long.

Waller said he expects more easing over the next three to six months, "and the pace of rate cuts will be driven by the incoming data". He left open whether that would mean "a sequence of cuts" or a more gradual adjustment with pauses. Either way, he made clear that policy should head steadily toward neutral. "It's just a question how fast we get there," he added.

The stance reflects his dissent at the July 30 meeting alongside Governor Michelle Bowman. Both argued then that signs of a softening labor market were enough reason to begin easing earlier.

Tokyo CPI core eases on to 2.5% yoy, but food inflation remains stubborn

Japan’s Tokyo CPI slowed in August as government fuel subsidies pushed down utility bills, but stubborn food inflation kept underlying price pressures elevated. Core CPI excluding fresh food eased to 2.5% yoy from 2.9% yoy, below expectations of 2.6% yoy. Headline CPI also cooled to 2.6% yoy, while the narrower core measure excluding both food and energy edged down to 3.0% yoy from 3.1% yoy.

Food inflation, however, remained sticky. Prices of rice, coffee beans and other groceries kept food CPI ex-fresh food at 7.4% yoy, unchanged from the previous month, highlighting persistent pressure on household budgets.

On the activity side, July industrial production dropped -1.6% mom, worse than forecasts of -1.0% mom, dragged down by a -6.7% mom slump in auto output. Manufacturers expect a rebound of 2.8% mom in August before a modest -0.3% mom dip in September.

Retail sales disappointed, rising only 0.3% yoy against expectations of 1.8% yoy. The labor market was a bright spot, with unemployment falling to from 2.5% to 2.3%, the lowest since December 2019.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7859; (P) 1.7879; (R1) 1.7906; More...

EUR/AUD's decline from 1.8155 short term top continues today and intraday bias stays on the downside. Decisive break of 38.2% retracement of 1.7245 to 1.8155 at 1.7807 should confirm that whole rise from 1.7245 has completed. Corrective pattern from 1.8554 should then be in its third leg. Further decline should be seen to 61.8% retracement at 1.7593. On the upside, above 1.7897 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

Move On

Investors on Thursday quickly shrugged off the initial disappointment from Nvidia’s quarterly report, which hinted at a slower growth rate for AI demand. The company still posted 56% year-over-year growth, though data center revenue came in flat to slightly lower. Some analysts pointed to Meta’s decision to slow AI spending, raising concerns that other big players could follow if returns don’t materialize as expected. On the brighter side, Nvidia’s results and guidance excluded any contribution from China, meaning any potential access would provide further upside. Sentiment was also buoyed by 10 firms raising their 12-month price targets after the report, lifting the average by 3% to $202.60 per share. After a volatile session that saw the stock test its all-time high, shares closed just 0.79% lower. In short, Nvidia’s latest report didn’t trigger a meaningful negative reaction — the fairy tale continues.

Broadly, S&P 500 companies delivered a far stronger Q2 than expected, with earnings growth near 12% versus 4–5% anticipated at the start of the season. Federal Reserve (Fed) expectations have softened markedly since the beginning of August, clearing the way for further equity gains. The index set yet another record yesterday — its 20th since the end of June when intraday highs are included — despite mounting worries over a weakening jobs market.

Thursday’s Q2 GDP revision added to the optimism: the US economy rebounded 3.3%, real final sales rose 6.8%, and core PCE inflation steadied near 2% annualized. Big-cap earnings remain robust, while smaller firms — currently pressured by tariffs — are likely to benefit from rate cuts as tariff-related inflation hasn’t yet filtered into the Fed’s preferred metrics. Markets expect the Fed’s core PCE index for July (due today) to tick up to 2.9% YoY. That would keep inflation sticky above the 2% target, but with attention shifting toward softening labour data, anything short of a major upside surprise is unlikely to derail expectations for a September cut, followed by another by year-end. That outlook remains supportive for equities.

In FX, the US Dollar has been pressured this year by trade tensions and now by dovish Fed bets. Still, if inflation stays contained while growth remains firm, the dollar could rebound. While a stronger dollar might weigh on equity valuations, the prospect of Fed easing should dominate.

However, there is no guarantee that inflation will remain contained. From today, the US will end the “de minimis” exemption that allowed packages under $800 to enter tariff-free. Nearly 1.4 billion such parcels entered in fiscal 2024 — about 3.7 million a day — fueling e-commerce growth at firms like Amazon, Shein and Temu. Temu has already reported a sharp drop in demand. The policy shift could lift prices for low-value goods and add upside pressure to August CPI, just as the Fed begins cutting rates — potentially complicating the easing cycle. For now, though, the outlook remains cautiously positive.

In Europe, preliminary August inflation data from major economies are due today and are expected to show some upside pressure. That, together with reduced trade uncertainties, could prompt the European Central Bank (ECB) to pause cuts in September. A potential US-EU deal could also reduce tariffs on European carmakers from 27.5% to 15%, offering relief to the sector. Still, euro bulls face headwinds from French political instability and a widening French-German yield spread, with EURUSD hovering near its 50-day moving average and offers into the 1.08 level.

Elsewhere, USDJPY is testing its 50-DMA to the upside after data showed slower inflation alongside weaker-than-expected sales and production data. The pair’s downside potential remains uncertain as slower inflation could give the Bank of Japan (BoJ) more time before hiking rates.

In energy, US crude again failed to clear the $65/barrel level this week. A 2.3-million barrel draw in US inventories and stalled Ukraine peace talks keep downside limited, while geopolitical risks raise the odds of a temporary spike toward the 200-DMA near $68. Meanwhile, the SPDR Energy Fund climbed to its highest level since April on the back of strong GDP data. Looking ahead, persistent inflationary pressures could channel more capital into dividend-paying energy names.

All Eyes on US PCE

In focus today

In the US, today's main data focus will be on the July PCE. Consensus expects headline to decline to 0.2% m/m and core PCE inflation to remain steady at 0.3% m/m. In the afternoon, University of Michigan's revised August consumer sentiment survey will be released. While inflation expectations declined from May to July, the preliminary data showed that new tariffs appear to have caused renewed concerns in early August.

Today, we receive the main data highlights of the week with the flash August inflation data from Germany, France, Italy, and Spain, which is released ahead of the euro area aggregate. We expect euro area HICP inflation to increase to 2.1% y/y in August from 2.0% y/y in July driven by an increase in energy inflation while core inflation is expected to remain unchanged at 2.3% y/y.

In Sweden, a whole battery of interesting and important macro data is released today at 08.00 am CET. At the top of the macro food chain is the GDP figures for Q2, which will serve as a key input (together with next week's inflation data) for the Riksbank's September meeting. We see GDP growth of 0.3%/1.2% q/q/ y/y, with a slight downside risk posited by some of our leading indicators. Additional data releases consist of retail sales for July and wage data for June, both of which are interesting in their own right.

In Norway, we expect the NAV unemployment rate to have fallen to 2.1% (cons: 2.2 %) in August, though we see downside risks as labour supply has increased significantly. Also keep an eye on the development in new vacancies, which appears to be falling somewhat, thus indicating somewhat lower demand for labour.

After moving sideways for two months, retail trade in Norway appears to have picked up again in July, and we expect +1% m/m.

Economic and market news

What happened overnight

In China, the rally in Chinese benchmark equity indices has extended amid new turnover highs. Retail investors have over the last month sent onshore benchmarks close to 10% higher as economic easing and AI optimism have outweighed concerns regarding the Chinese property market and US trade relations. Going forward markets will closely monitor Chinese authorities' communication on the soundness of the rally and to what extend regulators stand ready to cool down the bull run. So far investors have taken it as a positive sign that the People's Bank of China has lifted the CNY reference rate despite little change in the trade weighted USD.

In the US, following the recent batch of US figures markets still price around 20bp worth of Fed rate cuts for the upcoming FOMC meeting on 17 September. Overnight, Fed's Waller repeated his stance that a 25bp rate cut is the most likely for this meeting but that he would back a larger size cut should the August nonfarm payrolls report (released on 5 September) show "substantial weakening". Our base case still entails quarterly 25bp reduction in the Federal Funds target range until September next year.

What happened yesterday

In the US, Q2 GDP growth was revised up to 3.3% (prior: 3.0%), driven by strong consumer spending and increased investment in AI.

In Sweden, the NIER Economic Tendency Survey (ETI) headline claimed improved sentiment across all sectors. However, consumer sentiment showed only a very minor improvement and remains substantially below normal levels. Retail firms' expectations for sales prices over the next three months declined and are now below the historical average. A further decline in selling price expectations supports the board's view that the recent inflation uptick ought to prove temporary, which is seen as dovish. On the other hand, the broad, albeit minor, uptick in the ETI supports the recovery narrative, and makes it marginally hawkish. In our view, the relief regarding selling price expectations likely outweigh the cyclical factors at play, lowering the bar ever so slightly for another cut. That said, next week's inflation data remain the key input for the September meeting.

In the euro area, the growth in bank lending came to a two-year high in July on the back of lower interest rates and a gradual economic recovery. Loans to households grew by 2.4% (prior: 2.2%), while credit to companies increased by 2.8% (prior: 2.7%).

In geopolitics, Britain, France, and Germany triggered the snapback mechanism, launching a 30-day process to reinstate U.N. sanctions on Iran over alleged violations of the 2015 nuclear deal. The E3 cited insufficient progress in talks with Iran and declining cooperation with U.N. nuclear inspectors. Iran criticised the move as harmful to diplomacy but left the door open for engagement, while the U.N. Security Council is set to discuss the issue further behind closed doors today.

Equities: Equities were mixed again on Thursday, with US outperforming for a fifth session (S&P 500 0.3%) while Europe drifted lower (Stoxx 600 -0.2%). This takes US outperformance to a staggering 2.5p.p. in only a week! What we are seeing is the aftermath of Powell's dovish Fed guidance. This is visible in the sector performance where yield sensitive growth sectors like consumer discretionary, tech and communications are up 3-4% in a week. It is this renewed growth preference that have sparked the divergence between US and European markets. Speaking of tech, Nvidia managed the delicate balance to guide down consensus on 34x 12m fwd earnings yesterday, without a panic reaction in markets. The share closed a modest -1% lower. The defensive rotation in European markets stalled yesterday, but defensives have still outperformed cyclicals by 2-3p.p. since the peak in August.

FI and FX: US stocks closed at all-time highs while 10Y UST fell 2bp to around 4.22% in a flattening move during yesterday's session, with small moves overnight. Today, focus turns to the US PCE data for July and with 22bp of cuts priced for the upcoming September meeting it will likely require a clear overshoot to change the anticipation of a rate cut. After EUR/USD moved higher during much of yesterday, the USD recovered parts of yesterday's move overnight, now at 1.1660. USDJPY is stable around 147-level after Tokyo inflation data came out as expected. EUR/SEK and EUR/NOK have traded sideways since yesterday afternoon. Notably, Swedish yields continued to widen yesterday, and the 10y SGB is some 12bp wider vs Germany since last Friday.

Tokyo CPI core eases on to 2.5% yoy, but food inflation remains stubborn

Japan’s Tokyo CPI slowed in August as government fuel subsidies pushed down utility bills, but stubborn food inflation kept underlying price pressures elevated. Core CPI excluding fresh food eased to 2.5% yoy from 2.9% yoy, below expectations of 2.6% yoy. Headline CPI also cooled to 2.6% yoy, while the narrower core measure excluding both food and energy edged down to 3.0% yoy from 3.1% yoy.

Food inflation, however, remained sticky. Prices of rice, coffee beans and other groceries kept food CPI ex-fresh food at 7.4% yoy, unchanged from the previous month, highlighting persistent pressure on household budgets.

On the activity side, July industrial production dropped -1.6% mom, worse than forecasts of -1.0% mom, dragged down by a -6.7% mom slump in auto output. Manufacturers expect a rebound of 2.8% mom in August before a modest -0.3% mom dip in September.

Retail sales disappointed, rising only 0.3% yoy against expectations of 1.8% yoy. The labor market was a bright spot, with unemployment falling to from 2.5% to 2.3%, the lowest since December 2019.

Fed’s Waller: Time to start cutting in September, target neutral around 3%

Fed Governor Christopher Waller said he would support a 25bps cut at the September 16–17 FOMC meeting, warning that waiting for further labor market deterioration would risk the Fed “falling behind the curve.” He said conditions warrant a move now to put policy on a path toward neutral.

He placed the neutral rate near 3%, around 125–150bps below current levels. While not convinced the Fed is behind the curve yet, he emphasized that signaling a path toward neutral is a way to reassure markets that the Fed won’t let policy remain too tight for too long.

Waller said he expects more easing over the next three to six months, "and the pace of rate cuts will be driven by the incoming data". He left open whether that would mean "a sequence of cuts" or a more gradual adjustment with pauses. Either way, he made clear that policy should head steadily toward neutral. "It's just a question how fast we get there," he added.

The stance reflects his dissent at the July 30 meeting alongside Governor Michelle Bowman. Both argued then that signs of a softening labor market were enough reason to begin easing earlier.

Is Norm-Breaking America ‘Cooked’?

President Trump’s attempt to sack Fed Governor Cook is part of a broader pattern, not only for his administration but an increasingly partisan US. Other high-income countries are not going the same way.

- US President Trump’s attempts to sack Fed Governor Lisa Cook are part of a pattern of norm-breaking behaviour for the administration. While extreme compared with the past, they are also a culmination of decades-long political trends in the US.

- It is unlikely that other countries will follow the US example. More likely is that they will tack in the other direction to distinguish themselves from the Trump administration.

- As with disruptive personalities in volunteer organisations, the norm-breaking behaviour of the Trump administration is working because others are acquiescing to it. A principled rebuttal from Cook, and CDC head Monarez, could even be the beginnings of a cascade of resistance, if it succeeds.

Back in April, many investors were still reeling about the Trump administration’s rapid-fire policy announcements and break from earlier norms. It was not just the tariffs: the DOGE goings-on, attacks on universities and rising deportation rates were among the other concerns I heard on my client trip that month. All of these issues contributed to a general feeling that the US was no longer a nation of laws. One investor even commented to me that ‘America is cooked’.

Events of recent weeks have continued in this vein. Trump’s attempt to fire Federal Reserve Governor Lisa Cook is part of a pattern of summary firings designed to give the executive more control over institutions and policy, including the heads of the Bureau of Labor Statistics (BLS) and Center for Disease Control (CDC). Financial market participants have been especially focused on the Cook firing, given the importance of the Fed in the global financial system and the weight traditionally placed on central bank independence. Where the enabling legislation stated that officials served at the pleasure of the President, exits have been confirmed. The Federal Reserve is in a different position legislatively, meaning that Governor Cook has so far resisted dismissal by Truth Social post. (Like Cook, CDC head Susan Monarez has refused to resign.)

The Trump administration’s actions, while much more extreme than the past, represent the culmination of a longer-term pattern in US politics. For the past 30 or so years, we have seen increased partisanship and refusal in some quarters to fully accept the results of Presidential elections – from the constant investigation of Bill Clinton, to ‘hanging chads’, to ‘born in Kenya’, to ‘Russian disinformation’, to ‘stop the steal’. We have also seen – as previously noted – a decades-long decline in state capacity in the US. Its political system now struggles to take collective action and make difficult choices in the pursuit of the common good. And the Trump administration has not been the first group to attempt to ruin people’s careers based on mere accusations without due process – that is what some of the more egregious so-called ‘cancellations’ were about.

The acquiescence of other US institutions to the Trump administration’s norm-breaking is also an essential part of the current situation. Recall that Congress could take away Trump’s powers to enact tariffs, if it wanted to. This acquiescence, too, has its antecedents in broader social trends. Plenty of volunteer organisations can attest that when one norm-breaking disruptive personality joins, the organisation is so discombobulated by that person’s outrageous behaviour that it fails to set the necessary boundaries against the behaviour. Standing up to the norm-breaker and asserting the need for due process and rule of law is hard. Not all organisations have managed to find the necessary resolve when faced with a disruptive individual or a staff revolt, petition campaign or online pile-on against a person facing allegations without due process.

Markets seem, again, to be shrugging off the latest headline outrages. In any case, it pays not to take social media posts at face value, and to remember that Trump Ambit Claims Often. Surface appearances might be just that, though. Although the spread between very long US bond yields (30-year) and the usual 10-year benchmarks remains within the range of recent history, it has widened noticeably, especially in recent days. Growing concerns about US fiscal sustainability are finding expression in this way.

We see little prospect that these moves will spill over to other countries to be replicated at their central banks. If anything, other countries will increase the emphasis on the importance of central bank independence, to distinguish themselves from what is going on in the US.

For similar reasons, we see little prospect of other major advanced economies going down the route of the Trump administration. We are in fact seeing increased determination to stand as a democratic bloc apart from the US. The ‘Coalition of the Willing’ European leaders supporting Ukrainian President Zelenskyy at last week’s Washington meeting is a case in point, as is Canada’s increasing engagement with Nordic nations.

The longer-term question is whether these norm-breaking acts by the Trump Administration will do lasting damage to the US’s economic performance and place in the world. This is a question of whether the checks and balances built into US institutions will ensure that they heal themselves in future years. Some of the pivots by the US’s western and Asian allies to be more self-reliant on defence will be hard to reverse. (And it’s giving President Trump what he wants.) If the experience of Brazil and the Philippines is any guide, though, norm-breaking governments do get voted out, and their legacies tend to fade as successor governments take a more moderate approach.

We also cannot rule out that resistance by Fed Governor Cook and CDC head Monarez could be the beginnings of a preference falsification cascade. First theorised by the economist Timur Kuran, the idea is that people might believe one thing, but do not express it publicly because it does not feel safe to do so. So they think everyone else believes the socially acceptable views publicly expressed even though that is not actually true. Once a few people start stating their true beliefs and ‘survive’, others join in and reveal their own true beliefs. The previous presumed consensus can crumble quickly under these circumstances.

The independence of Fed policymaking is key to the good functioning of global financial markets. But it may be that there is more at stake in a successful resistance of Trump’s attempts to fire Cook and Monarez than the position of the central bank.

Cliff Notes: Inflation Receives a Jolt

Key insights from the week that was.

The main event for Australia this week was the Monthly CPI Indicator, and it certainly was a striking result. The headline CPI indicator bounced 0.9% in July, driving annual inflation from 2.1%yr to 2.8%yr, near the top of the RBA’s target range. That the trimmed mean measure also shot up to 2.7%yr points to a broad-based pick-up in underlying momentum and consequently upside risk to our Q3 CPI forecast.

One month’s data does not make a trend, especially as electricity prices drove the result. Underlying July’s 13% surge in electricity prices was a combination of state rebate roll-offs, the varied timing of the Commonwealth rebate extension and standard annual price increases. While each dynamic is well understood, their timing is uncertain, hence the relatively subdued reactions to the July report from market participants who continue to expect a 25bp rate cut in November.

In the lead-up to Q2 GDP next week, we also received two partial indicators of investment.

Construction activity was firmer than expected, bouncing 3.0% in Q2 to be up 4.8% over the year. This was mostly driven by a surge in lumpy mining infrastructure installations, accentuated by the release’s accounting treatment that sees projects recorded on completion versus the National Accounts’ accrual method (which incorporates activity completed each quarter). Conditions outside of the mining sector remain delicately poised: public work is retreating from peak levels almost as quickly as it attained them; however, a healthy pipeline of electricity generation and distribution projects should provide offsetting support into the medium-term.

Private CAPEX subsequently disappointed in Q2, a 0.2% gain a long way below the 0.8% consensus expectation. Growth over the past year of 1.7%yr is the result of the building out of essential infrastructure in the non-mining economy – predominately electricity, energy and data assets – while mining investment is 1.0% lower than a year ago. The outlook remains uninspiring, the latest estimate for 2025-26 CAPEX plans pointing to growth in real investment of just 1.2%yr, a touch above FY25’s 0.9%yr gain. To combat low productivity and capacity constraints, strong investment is necessary.

Our full Q2 GDP preview will be released today on Westpac IQ, and the ABS’ Q2 National Accounts release is due next Wednesday.

Offshore markets spent much of the week digesting insights from last weekend’s Jackson Hole Economic Symposium, especially FOMC Chair Powell’s remarks on the near-term outlook for policy.

Powell’s remarks were balanced and constructive overall, highlighting the full spectrum of risks the US economy faces and that the Committee is well placed to adjust policy gradually to match incoming data. That said, Chair Powell's remarks could be interpreted as putting a greater emphasis on the “rising” downside risks for employment which, to date, have been masked by reduced migration and participation.

Referencing the recently completed five-year review of the Federal Reserve’s Monetary Policy Framework, Chair Powell went on to discuss why a tight labour market does not, by itself, signal accelerating inflation and instead needs to be considered in the broader context of the economy and policy. Of course, other potential drivers of inflation also must be taken into consideration. While downside risks to current full employment warrant two cuts from the FOMC by year end, as we and the market forecast, in our view persistent inflationary pressure stemming from capacity constraints are likely to preclude additional easing to a neutral or expansionary setting in 2026, unless labour market slack grows materially.

Turning then to the academic discourse of the Symposium, the evolving state of global labour markets in response to demographic and structural change was the focus. Bank of Japan Governor Kazuo Ueda highlighted the impact of Japan’s ageing population, which has tightened the labour market and spurred increased participation from women as well as older men. Tight conditions have also led to greater job mobility among younger workers and consolidation among smaller firms who are struggling to keep up with wage growth. Ueda also noted that investment in labour-saving technology, particularly in services, is expected to enhance productivity going forward.

Similar dynamics were echoed by ECB President Christine Lagarde who observed that, despite fiscal constraint and the legacy of tight monetary policy, labour markets in the Euro Area have continued to tighten. This strength has been partly driven by delayed wage growth which has contained unit labour costs, thereby making labour a more attractive input. Firms have also increased headcount in response to declining average hours worked, with additional labour demand largely being met by rising participation amongst women, older workers, and foreign labour.

A subsequent paper from Nobel laureate Claudia Goldin investigated the drivers of declining fertility rates – a factor with profound implications for labour supply and policy over coming decades in both the developed world and some large developing markets, most notably China.