Sample Category Title

UK Services PMI Improves, Pound Continues Losing Streak

The British pound is down for a fourth straight day and has dropped 0.9% this week. In the North American session, GBP/USD is trading at 1.3432, down 0.16% on the day.

The UK was scheduled to release July retail sales on Friday, with a market estimate of 0.4%, but that has been delayed until September 5.

UK PMIs: services accelerates, manufacturing weakens

UK PMIs were a mixed bag in August. The Services PMI improved to 53.6, up from 51.8 in July and above the market estimate of 51.8. Business activity rose for a fourth straight month and hit its fastest pace in a year. There was an increase in new orders and business confidence rose on expectations that consumer demand will improve.

The manufacturing sector continues to struggle and the contraction worsened in August. The PMI fell to 47.3 in August from 48.0 in July. New orders decreased and employment losses deepened as the uncertainty over US tariffs has resulted in subdued global demand. The silver lining was that manufacturers' optimism improved.

Fed minutes points to split

The Federal Reserve released the minutes of the July meeting on Wednesday. The Fed didn't surprise anyone by maintaining rates but the meeting made headlines when two FOMC members voted against the majority in favor of a rate cut. This was the first time in over 30 years that more than one member has voted against a rate decision.

The minutes noted the differing views on the Fed's dual mandate of inflation and employment. The economy faces an upside risk to inflation and a downside risk to employment, complicating rate decisions. At the meeting, the majority judged higher inflation as the greater risk while the minority believed that the deterioration in the labour market was the greater risk.

The Fed is expected to lower rates in September for the first time since December 2024, with an 80% probability of a quarter-point cut according to CME's FedWatch.

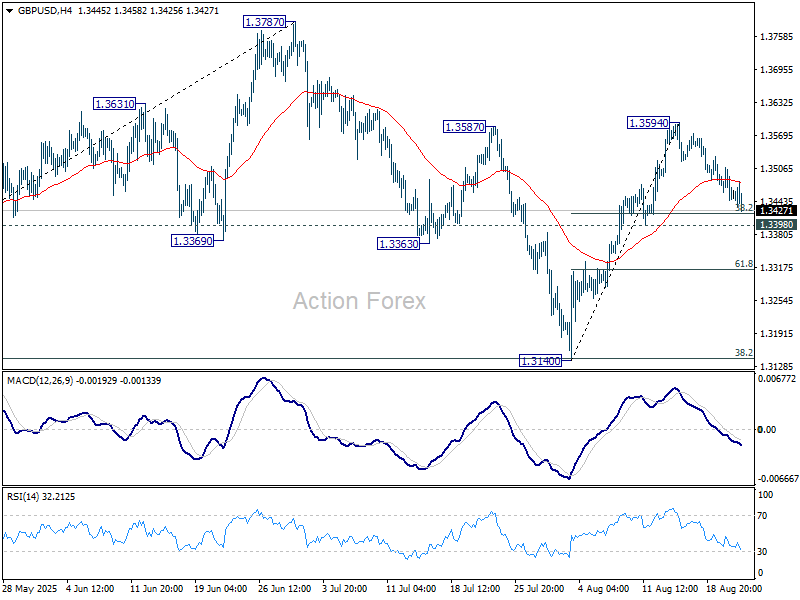

GBP/USD Technical

- GBPUSD is testing support at 1.3431. Below, there is support at 1.3416

- There is resistance at 1.3457 and 1.3472

GBPUSD 4-Hour Chart, Aug. 21, 2025

Japan’s Inflation Rate Expected to Ease, Yen Dips

The Japanese yen is slightly lower on Thursday. In the European session, USD/JPY is trading at 147.87, up 0.39% on the day.

Japan's inflation expected to continue slowing

Japan releases the July inflation report on Friday. The markets will be especially interested in the core rate, which is expected to ease to 3.0% y/y, from 3.3% in June. Core CPI includes energy but excludes fresh food

Core CPI has remained above the Bank of Japan's 2% target for over three years but the central bank has been slow to raise interest rates. BoJ Governor Ueda has said that the Bank will not raise rates until underlying inflation, which is generated by domestic demand and wages, is sustainably at 2%.

The BoJ raised rates to 0.5% in January but took its foot off the rate-hike pedal when Donald Trump became President and imposed a hard-hitting tariff policy which shook up the financial markets. Now that the US and Japan have reached a trade agreement and greatly reduced the uncertainty over tariffs, a major obstacle to raising rates has been removed.

Fed minutes point to dissension

The Federal Reserve released the minutes of the July meeting on Wednesday. The Fed's decision at the meeting to maintain rates was widely expected but the meeting made headlines when two FOMC members went against the majority and voted for a rate cut. This was the first time in over 30 years that more than one member voted against a rate decision.

The minutes reflected this dissension, noting the differing views on the Fed's dual mandate of inflation and employment. The economy faces an upside risk to inflation and a downside risk to employment, complicating rate decisions. At the meeting, the majority judged higher inflation as the greater risk while the minority believed that the deterioration in the labour market was the greater risk.

The Fed is widely expected to lower rates in September, after holding rates since December 2024.

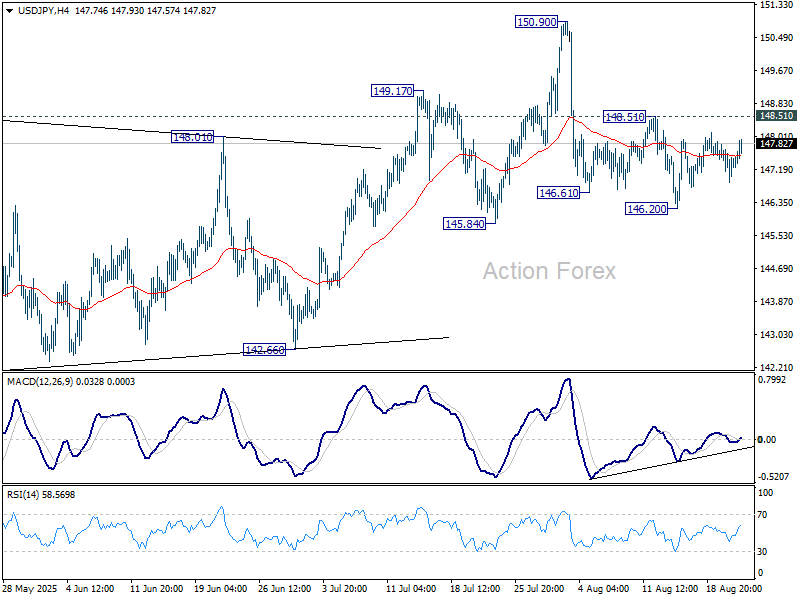

USD/JPY

- USD/JPY has pushed above resistance at 147.33 and is testing 147.79 Above, there is resistance at 148.28

- 146.84 and 146.38 are providing support

USDJPY 1-Day Chart, Aug. 21, 2025

Sunset Market Commentaryt

Markets

The HCOB flash Eurozone PMI’s provided a guarded, but after all constructive picture as the economy navigates a new era post the EU-US trade deal. The output composite index increased to from 50.9 to 51.1, the best in 15 months and marking an eight consecutive month of expansion. According to S&P global, the improvement was driven by a further solid improvement in the manufacturing output (output index 52.3; 41 month high). Services activity also rose, albeit only slightly (50.7) and at a slower pace compared to July. Promising: new orders returned to growth for the first time after 14 months of decline, with new business increasing slightly both in the manufacturing and services sectors even as exports orders continue to decline. Better activity and orders also caused companies to extend the recent sequence of job creation, be it at a modest pace and limited to the services sector. The report also mentions inflationary pressures to have picked up in August, with both input and out prices increasing at a faster pace than last month. Despite the rather positive current assessment, business confidence eased for the second consecutive month, suggesting ongoing uncertainty going forward. Regarding the major countries, activity in Germany expanded further (50.9). France neared stabilization (49.8). The rest of the Eurozone continued to register increasing output, albeit with the pace of growth easing slightly from July. After some ‘hesitation’ this week, German yields are again trending north, rising between 4 bps (2-5-y) and 3 bps (30-y). The PMI report provides a perfect narrative for the ECB to adhere a ‘sine die’ policy pause. Markets further scaled back expectations on a final ECB rate cut to about 60% somewhere next year. The Eurostoxx 50 cedes 0.5%. US indices also continue their recent correction (S&P 500 -0.45%). UK yields rebounded after yesterday’s surprise (higher inflation) setback on a decent UK PMI (cf infra) and better than expected monthly UK government budget data. While positive, the latter are highly volatile. Sterling gains marginally against the single currency (EUR/GBP 0.8653).

US data evidently still face a long shadow from tomorrow’s Jackson Hole address from Fed Chair Powell. US yields and the dollar eased slightly/briefly after weaker than expected weekly jobless claims (235k from 224k) and a softer than expected Philly Fed business outlook, but the move was soon reversed going into the US PMI’s release.US PMI’s printed much stronger than expected. The composite measure improved to 55.4 from (55.1) as manufacturing activity rebounded sharply (53.3 from 49.8). Services also continued to grow solidly (55.4). S&P also assess that the ‘rise in selling prices for goods and services suggests that consumer price inflation will rise further above the Fed’s 2% target in the coming months. Indeed, combined with the upturn in business activity and hiring, the rise in prices signaled by the survey puts the PMI data more into rate hiking, rather than cutting, territory’. Even so, the market reaction remains guarded; US yields add about 3 bps across the curve. The dollar gains (DXY 98.4, EUR/USD 1.163.

News & Views

The UK composite PMI joined the global move in August, rising from 51.8 to 53.6 (vs 51.8 expected). It was the strongest rise in private sector business activity since August of last year, led by a solid upturn in the services economy (53.6 from 51.8). New business volumes expanded at the strongest pace since October 2024 while employment was a weak spot, decreasing for the eleventh month running and at a marked pace. Business activity expectations for the year ahead edged up to the highest since October 2024 even as companies report concerns over the impact of recent government policy changes as well as unease emanating from broader geopolitical uncertainty. Input cost inflation meanwhile edged up to its highest since May. Suppliers try to pass on increased National Insurance costs with higher payroll costs also resulting in another robust rise in prices charged.

Belgian consumer confidence rose to its highest level in a year in August (-2 from -4). The increase was mainly driven by reduced fears over a rise in unemployment (1 from 7; lowest since February 2022). Consumer expectations for the general economic situation remain unchanged at -26. On a personal level, households intend to save more (21 from 19) and have slightly raised their expectations regarding their own financial situation (-1 from -2). On Monday, the National Bank of Belgium releases its August business confidence indicator with Belgian inflation numbers out next Thursday.

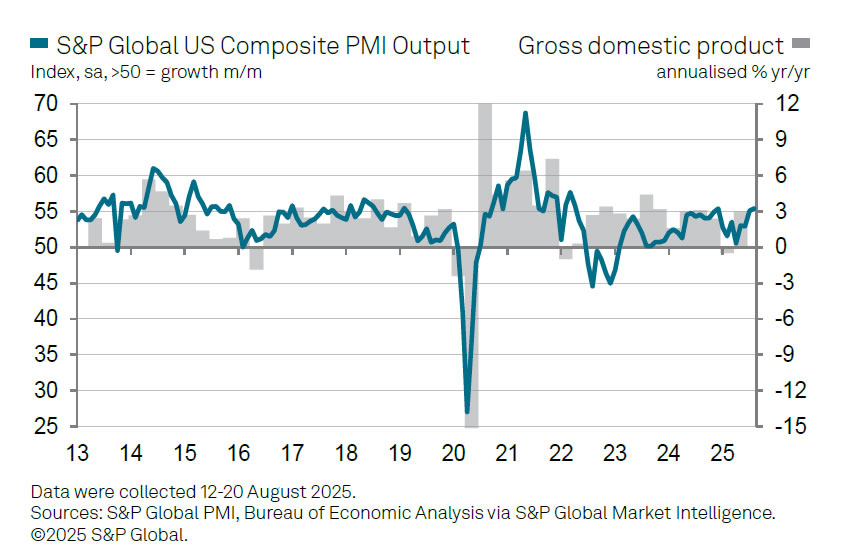

US PMI surge suggests Fed may need to tighten rather than ease

US flash PMI survey showed the sharpest manufacturing rebound in over three years, as the index jumped from 49.8 to 53.3. Services held firm at 55.4, down slightly from 55.7, lifting Composite PMI to an eight-month high of 55.4. The data point to an economy expanding at a 2.5% annualized pace, well above the average 1.3% seen in the first half of 2025.

S&P Global’s Chris Williamson noted that companies across both sectors are seeing stronger demand, with rising backlogs suggesting capacity constraints reminiscent of the early 2022 supply bottlenecks. This surge has also underpinned a pickup in hirin.

Yet, the survey also showed mounting inflation pressures. Businesses are increasingly passing tariff-related costs through to consumers, and the PMI price indices are now running at their highest levels in three years. Selling prices for goods and services have moved higher, suggesting that consumer inflation will "rise further above the Fed’s 2% target in the coming months."

For the Fed, the PMI results raise more questions than answers. Far from reinforcing the case for imminent rate cuts, the data place the economy closer to historical conditions that align with policy tightening.

"Combined with the upturn in business activity and hiring, the rise in prices signaled by the survey puts the PMI data more into rate hiking, rather than cutting," Williamson noted.

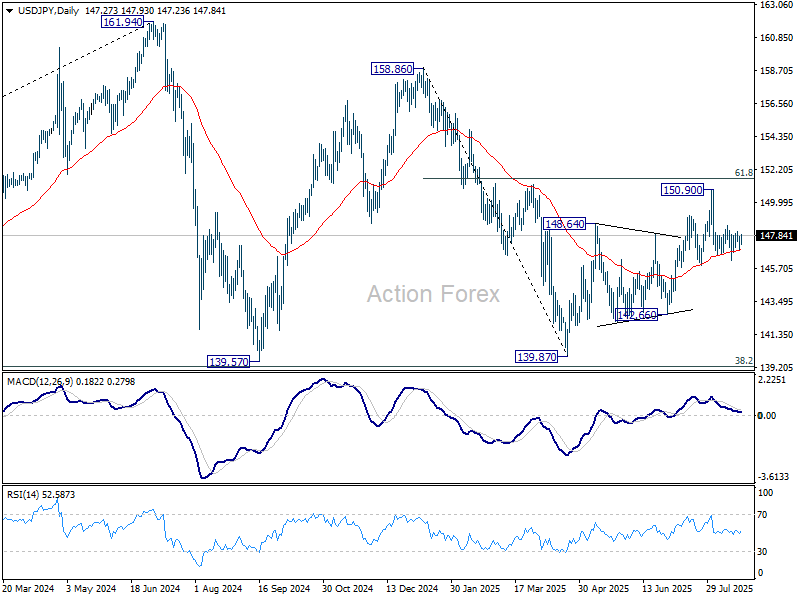

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.84; (P) 147.33; (R1) 147.79; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the upside, break of 148.51 will indicate that the pullback from 150.90 has completed, and bring retest of this high. This will also keep the whole rise from 139.87 alive. However, firm break of 145.84 support will argue that the rebound from 139.87 has completed, and turn near term outlook bearish.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

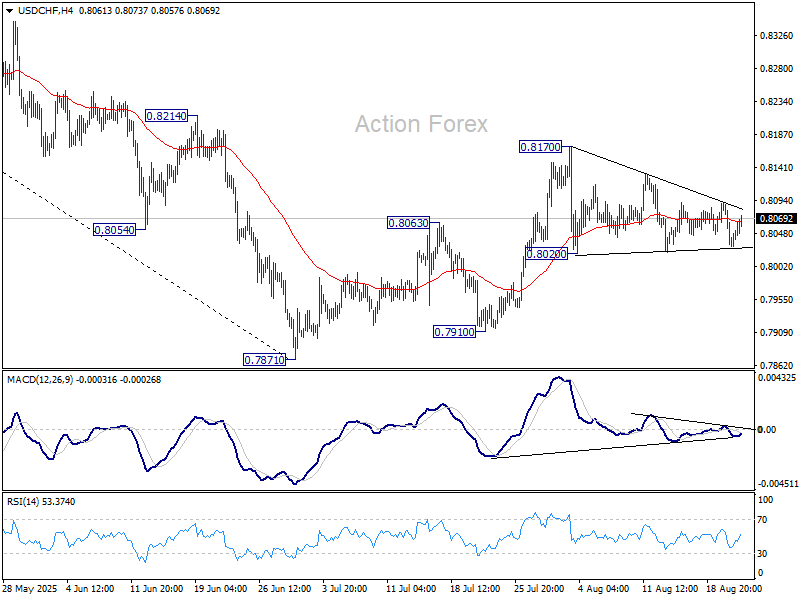

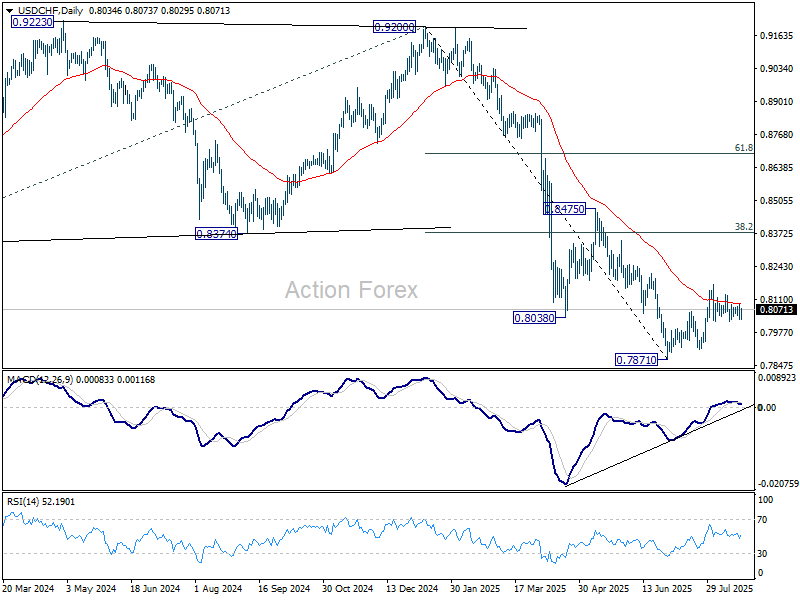

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8018; (P) 0.8055; (R1) 0.8080; More….

Range trading continues in USD/CHF and intraday bias stays neutral. On the downside, break of 0.8020 will revive that case that the corrective pattern from 0.7871 has completed, and target a retest on 0.7871 low. On the upside, firm break of 0.8710 will resume the corrective from 0.7871. Intraday bias will be back on the upside for 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

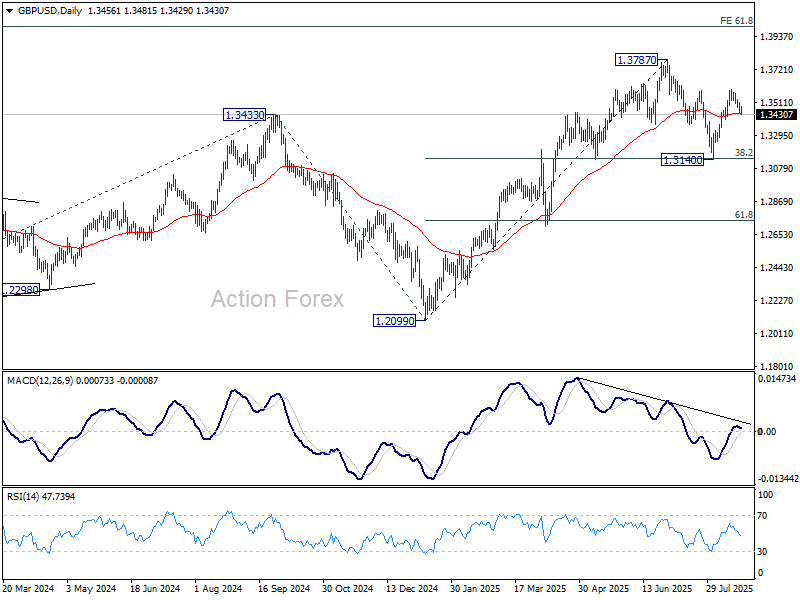

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3432; (P) 1.3471; (R1) 1.3494; More...

No change in GBP/USD's outlook and intraday bias remains neutral. While correction from 1.3594 might extend lower, down side should be contained by 1.3399 support. On the upside, break of 1.3594 will resume the rise from 1.3140 to retest 1.3787 high. However, firm break of 1.3398 will argue that the corrective pattern from 1.3787 is extending with another falling leg. Deeper decline should the be seen back towards 1.3140.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3090) holds, even in case of deep pullback.

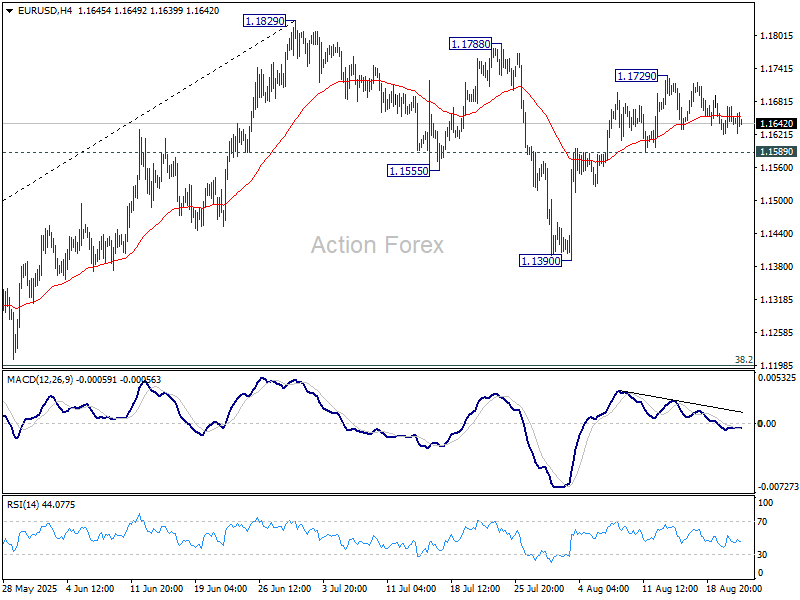

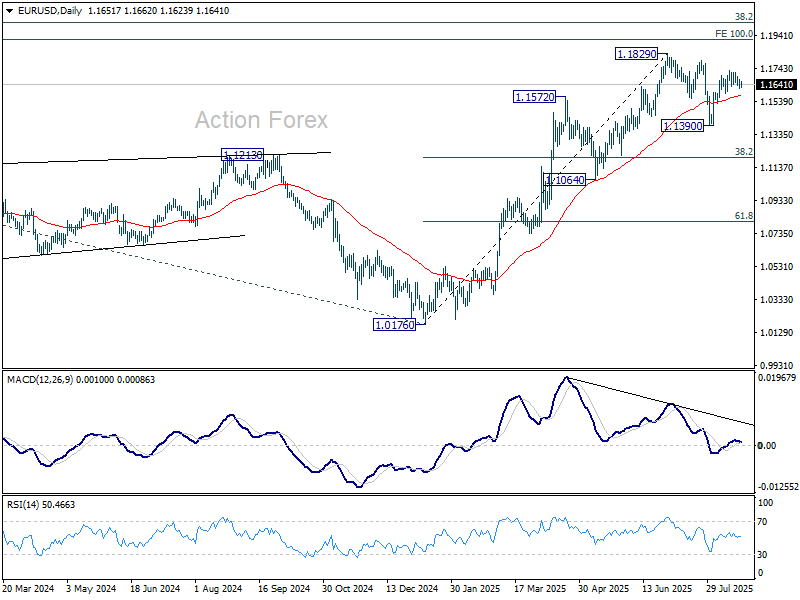

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1623; (P) 1.1649; (R1) 1.1675; More...

EUR/USD is still bounded in consolidations in tight range below 1.1729 and intraday bias stays neutral. Further rally is expected as long as 1.1589 support holds. Above 1.1729 will bring retest of 1.1829 high. On the downside, however, firm break of 1.1589 will turn bias to the downside, and extend the corrective pattern from 1.1829 with another fall.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

Dollar, Euro Slightly Firmer as US–EU Trade Deal Details Emerge, Overall Mood Still Cautious

Currency markets remained reluctant to take on clear direction today, though a mild risk-off undertone was evident in equities and broader risk sentiment. Euro and Dollar emerged as the mildly firmer currencies of the day, underpinned by strong Eurozone PMI data and steady remarks from Federal Reserve officials. Yet the overall tone stayed cautious, with most pairs confined to tight intraday ranges.

Euro’s support stemmed partly from solid PMI figures, which showed manufacturing and services combining to deliver the fastest growth in 15 months. Germany led the expansion in factory output, while France showed tentative stabilization after months of contraction. Even as foreign orders remain weak under tariff pressure, the resilience of intra-EU demand has reinforced the perception that the bloc is coping better than feared.

At the same time, incremental details on the U.S.–EU trade deal offered another modest tailwind. Washington confirmed it will impose 15% tariffs on most EU imports including autos, pharmaceuticals, and chips — a sharp reduction from earlier threats of 30%. Crucially, the administration pledged to roll back duties on cars and auto parts once Brussels enacts reciprocal tariff cuts. EU Trade Chief Maros Sefcovic said proposals will be tabled by the end of the month.

The tariff reprieve is significant: U.S. duties on European autos, previously as high as 27.5%, will be nearly halved. In parallel, Brussels committed to eliminate tariffs on all U.S. industrial goods and expand access for seafood and agricultural exports. More importantly, it reaffirmed plans for US 750 billion in U.S. energy purchases and US 600 billion of additional EU investment in American strategic sectors through 2028. Together, these commitments injected a degree of stability into transatlantic trade relations.

Still, Dollar’s support came less from trade optimism than from Fed commentary. Despite weaker July jobs data and large downward revisions to May and June payrolls, Atlanta Fed President Raphael Bostic and Kansas City Fed President Jeffrey Schmid maintained cautious stances. Both signaled little urgency to cut rates, stressing that inflation near 3% remains too high. Investors await further remarks from other officials at Jackson Hole, which could clarify whether September’s widely expected cut will be accompanied by signals for more aggressive easing.

In the overall currency markets, Swiss Franc continues to lead the weekly performance board, followed by Dollar and Yen. Notably, Yen has given back much of its early-week gains as risk hedging flows moderated. On the other end, commodity currencies are still under heavy pressure, with Kiwi and Aussie at the bottom. Sterling also struggled despite stronger services PMI data, leaving it the third weakest major of the week.

In Europe at the time of writing, FTSE is down -0.14%. DAX is down -0.31%. CAC is down -0.70%. UK 10-year yield is up 0.047 at 4.720. Germany 10-year yield is up 0.031 at 2.75. Earlier in Asia, Nikkei fell -0.65%. Hong Kong HSI fell -0.24%. China Shanghai SSE rose 0.13%. Singapore Strait Times rose 0.27%. Japan 10-year JGB yield rose 0.003 to 1.611.

Fed's Schmid Cautions: No rush to ease without very definitive data

Kansas City Fed President Jeffrey Schmid, in a CNBC interview, stressed there was no urgency to cut rates. With inflation still hovering closer to 3% than 2% and the labor market in solid shape, Schmid said policymakers would need “very definitive data” before adjusting policy.

He argued that the “last mile” of returning inflation to target remains the hardest part and warned that lowering rates too soon could undermine public expectations, reigniting price pressures. “We got to be careful about what lowering short-term rates would do to the inflation mentality,” he noted.

Despite weaker jobs data in recent months, Schmid emphasized optimism among business contacts and questioned whether the current 4.25%–4.50% policy rate was significantly restricting growth. “I don’t know exactly what we are restricting,” he said.

Fed’s Bostic sticks to view of one cut this year

Atlanta Fed President Raphael Bostic reiterated that his outlook for monetary policy remains centered on just one rate cut this year, consistent with guidance he has offered since early 2025. While Bostic emphasized he is not “stuck on anything,” he noted that forecasts carry wide confidence bands in the current environment of heightened uncertainty.

He pointed out that inflation has been moving “sideways” in the 2.5–2.8% range for much of the past nine months, persistently above the Fed’s 2% goal. This suggests progress on disinflation has stalled, keeping policymakers wary of easing too early. At the same time, the unemployment rate remains historically low, though cracks in the labor market are beginning to appear.

Bostic acknowledged the downward revisions to May and June payrolls as a sign of “lot less robust job creation,” though he cautioned against reading too much into one data point.

US initial jobless claims rise to 235k vs exp 227k

US initial jobless claims rose 11k to 235k in the week ending August 16, above expectation of 227k. Four-week moving average of initial claims rose 4.5k to 226k.

Continuing claims rose 30k to 1972k in the week ending August 9, highest since November 6, 2021. Four-week moving average of continuing claims rose 7k to 1955k.

UK PMI composite climbs to 12-month high, fragile demand and job cuts temper optimism

The UK economy showed firmer momentum in August, with Composite PMI climbing from 51.5 to 53.0, its highest in a year. Services provided the bulk of the support, rising from 51.8 to 53.6, also a 12-month high, while manufacturing slipped further into contraction at 47.3, down from 48.0.

S&P Global’s Chris Williamson noted that the UK economy is enjoying its best pace of expansion since last summer, with the services sector driving activity. Manufacturing, though still weak, showed tentative signs of stabilization. However, demand environment remains both "uneven and fragile", and businesses continue to shed staff at an "aggressive rate" amid pressure from rising costs.

The improved growth backdrop, alongside July’s stronger-than-expected inflation reading, reduces the likelihood of further BoE rate cuts this year. With the MPC split over the policy outlook, upcoming data on growth and inflation will be crucial in determining whether the central bank leans toward patience or resumes its easing path.

Eurozone PMI composite hits 15-month high, but foreign demand falters Under US Tariffs

Eurozone private sector activity gained modest momentum in August, with Composite PMI rising from 50.9 to 51.1, its highest level in 15 months. Manufacturing led the improvement, climbing from 49.8 to 50.5, a 38-month high. Services softened slightly from 51.0 to 50.7. Growth remains fragile, but the data signals that businesses are coping better than expected with the current trade and policy backdrop.

Hamburg Commercial Bank’s Cyrus de la Rubia noted that despite headwinds from U.S. tariffs and lingering uncertainty, the EU’s single market has helped cushion the blow, with domestic demand and tourism acting as stabilizers.

Manufacturing output has now expanded for six straight months, driven by Germany. France, previously a drag, showed signs of stabilization in both manufacturing and services. However, US trade policy continues to bite. Eurozone manufacturing foreign orders fell for the second month in a row, with Germany now also seeing declines after holding up earlier in the year.

While cost pressures in services remain an ECB concern, the steadiness in selling-price inflation provides "a bit of relief".

Japan’s PMI manufacturing nears expansion at 49.9, but external demand raises sustainability concerns

Japan’s flash PMI data for August showed momentum improving, with the composite index rising slightly from 51.6 to 51.9. Manufacturing posted a surprise recovery, with output climbing back into expansion at 50.5 from 47.6, while the broader PMI Manufacturing rose to 49.9 from 48.9. However, services growth slowed, with the index easing to 52.7 from 53.6.

S&P Global’s Annabel Fiddes noted that the upturn was broad-based, led by a fresh rise in factory production alongside continued service-sector strength. Still, new orders in manufacturing remained weak, raising questions about how sustainable the rebound in factory output will be without stronger demand.

Foreign demand was a drag across both goods and services, leaving the recovery heavily reliant on domestic activity. At the same time, rising input costs squeezed firms’ margins as competitive pressures limited their ability to pass costs on to clients. Selling price inflation slowed to its weakest pace since October, underlining the profitability challenge for Japanese businesses.

Australia PMI composite rises to 54.9, growth broadening, inflation cooling

Australia’s private sector gained momentum in August, with both manufacturing and services showing stronger growth. Manufacturing PMI climbed to 52.9 from 51.3, while Services PMI improved to 55.1 from 54.1. As a result, Composite PMI rose to 54.9 from 53.8, its highest since April 2022, signaling a broadening recovery.

S&P Global’s Jingyi Pan noted that easier interest rates have supported domestic activity, while external demand is also beginning to revive. Export orders picked up, adding to optimism among Australian businesses, and sentiment strengthened notably through the month.

Price pressures, meanwhile, showed signs of easing. Output price inflation pulled back from July’s recent high, a shift that could help sustain demand in the months ahead. That combination of stronger demand and softer price growth points to a healthier balance in the economy and gives RBA space to assess policy moves more carefully in the coming months.

NZ trade swings back into deficit despite broad export gains

New Zealand’s trade balance flipped back into deficit in July, with imports outpacing exports despite solid overseas demand. Goods exports climbed 10% yoy to NZD 6.7 billion, but imports rose 2.6% yoy to NZD 7.3 billion, leaving a monthly deficit of NZD -578 million compared with expectation of NZD 70 million surplus.

Export performance was broadly positive across major partners. Shipments to the EU jumped 28% yoy, while sales to Japan rose 23%. Exports to the U.S. and China also advanced by 7.7% and 7.1% respectively. Australia remained steady with a 4.7% increase.

On the import side, gains were concentrated in the EU and U.S., up 22% yoy and 24% respectively. Purchases from China increased 6.9%, while imports from Australia ticked up by 2.7%. However, imports from South Korea slumped by a sharp -33%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1623; (P) 1.1649; (R1) 1.1675; More...

EUR/USD is still bounded in consolidations in tight range below 1.1729 and intraday bias stays neutral. Further rally is expected as long as 1.1589 support holds. Above 1.1729 will bring retest of 1.1829 high. On the downside, however, firm break of 1.1589 will turn bias to the downside, and extend the corrective pattern from 1.1829 with another fall.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.