Sample Category Title

Sell or Hold?

Yesterday’s FOMC minutes further dampened investor mood and accelerated the equity selloff – again led by a significant drop across Big Tech. The minutes stated that Fed officials were worried about both weakening jobs data and inflation risks, but that “a majority of participants judged the upside risks to inflation as the greater of these two risks.” That means officials remain inclined to prioritize inflation control by keeping monetary policy tight rather than cutting rates.

Yet, one caveat makes the minutes look less hawkish than they first appeared: this meeting was held before the release of the problematic July jobs report – with big downside revisions – that spooked investors and fueled expectations for a September cut. Jerome Powell’s speech tomorrow could therefore strike a middle ground: acknowledging rising concern about the labour market, while underscoring that inflation remains a key risk to be addressed carefully.

As such, the Federal Reserve (Fed) will probably announce a 25bp cut next month but stop short of signaling more. The US 2-year yield was under pressure ahead of the minutes but rebounded on the committee’s broadly hawkish stance. The US 2-30 year spread is widening on fears that today’s rate cuts could fuel tomorrow’s inflation, while the ballooning US debt will be more expensive to finance. One bright spot: Trump’s tariffs are bringing in revenue that S&P Global Ratings says could soften the fiscal burden. But they also warn that the trade war risks ushering in a new world order dominated by China.

The pressure on the long end of the yield curve doesn’t calm investor nerves either, as less risky bonds are now offering higher returns and attracting flows. The Japanese 30-year JGB yield is also testing its highest levels in more than two decades. That raises the risk of Japanese reverse carry trades – investors closing yen-funded positions abroad and returning to higher-yielding domestic assets. If that accelerates, global risk assets could face further pressure on top of Fed and trade worries.

The S&P 500 remained under pressure from Big Tech selling, though a small rebound appeared late in the session, and futures hint at a steadier open this morning. Futures on the Taiwan Stock Exchange are better bid, with TSMC up 1.3%, suggesting US tech selling could cool. Nvidia slipped below $160 before dip buyers stepped in, and the SPDR tech ETF bounced off its 50-DMA. Whether the tech-led selloff – and thus the broader indices – deepens into sector rotation remains to be seen. Earnings have been solid, and Nvidia hasn’t said its last word yet, but AI enthusiasm looks largely priced in, and Fed expectations have run far enough that markets could shift back toward the hawkish side, especially as long-term bond yields look increasingly attractive.

Today, investors will watch global PMI releases to recalibrate policy expectations. Japan’s manufacturing PMI beat forecasts but remained in contraction due to weaker foreign demand from tariffs. That suggests the BoJ won’t rush into further hikes until the recovery looks steadier. In India, manufacturing PMI showed its strongest growth since 2008, with robust domestic demand offsetting flat export orders. The Nifty 50 extended gains above the 50-DMA, bucking global risk aversion. Europe’s numbers will likely show continued contraction in manufacturing, with slight services expansion. European Central Bank (ECB) President Lagarde warned yesterday that euro-area growth could slow this quarter under tariff pressure, noting the announced tariffs were “a little higher” than assumed in June but still below worst-case scenarios. The EURUSD is treading water around the 50-DMA, awaiting Powell’s Jackson Hole speech for direction.

In the UK, sterling extended losses despite a hotter-than-expected CPI print, pointing to sticky services inflation. While the data initially lifted hawkish Bank of England (BoE) expectations and weighed on November cut bets, many concluded it won’t stop a November cut: April’s tax and minimum-wage hikes are seen weighing enough on growth for the BoE to keep easing.

Meanwhile, Ukraine talks continue in the background, with Russia expressing willingness to join security talks with Western allies. Any lack of progress toward durable peace could revive oil bulls. US crude found support near $62pb and is pushing higher this morning. The summer decline leaves room for a medium-term rebound: fading peace hopes could send prices back above $65pb. A space to watch.

EMU Composite PMI Expected to Confirm Scenario of Lackluster Growth

Markets

Markets remained mired in mostly technical, order-driven trading yesterday. On equity markets, Tuesday’s ‘rotation’ out of some US tech-related stocks to some extent continued (Nasdaq -0.63%, Dow +0.04%, Eurostoxx 50 -0.20%), but it still occurred in an orderly fashion. Core bonds again attracted a mild (safe haven?) bid. At the end of the day US yields eased up to 1.5 bps (30-y), off softer levels intraday. This intraday rebound in yields was at least partially supported by the minutes of the July Fed meeting. The report said that ‘participants generally saw risks to both sides of the Fed’s dual mandate (upside for inflation, downside to employment), but that a majority judged the upside risk to inflation to be the greater of the two risks, with the impact of tariffs still containing a substantial degree of uncertainty. At that time, the labour market situation was still assessed to be solid. Of course this picture might have evolved after this month’s (labour and inflation) data. In the risk assessment, several members also note concerns on elevated asset valuations. Bunds slightly outperformed Treasuries (2-y -2.5 bps, 10-y -3.3 bps). ECB’s Lagarde in a speech assessed that “Recent trade deals have alleviated, but certainly not eliminated, global uncertainty”. This might still translate to slower growth this quarter. The ECB staff will factor in the impactions of the EU-US trade deal in its projections that will be available at the September 11 policy meeting. On FX markets, the dollar briefly dipped as US president Trump urged Fed Governor Lisa Cook to resign on allegations of mortgage fraud. The issue again raised concerns on political interference with Fed independence. Cook already indicated that she intends to stay. Initial USD losses were limited and short-lived. DXY closed in well-known territory (98.22) as did EUR/USD (1.165). UK gilt markets showed surprising/remarkable outperformance despite higher than expected July price data (yields lower by 6-7 bps across the curve). Sterling initially tried to gain after the inflation release, but was dragged lower later by the reversal in yields. EUR/GBP closed near 0.866 (from 0.863).

EMU but also US PMI’s take center stage today. The Philly Fed business outlook and US weekly jobless claims will also fuel the debate on the Fed reaction function as markets look forward to tomorrow’s Jackson Hole address of Fed Chair Powell. The EMU composite PMI is expected to confirm a scenario of lackluster growth (50.6). Maybe there is room for some improvement as trade-uncertainty eases (to some extent). After recent mixed/divergent US labour and inflation data, US PMI’s this time also have potential to cause some intraday repositioning with (both FI and FX) markets maybe slightly more sensitive to weaker/softer than expected outcome.

News & Views

S&P global this morning already published PMI business surveys for India, Japan and Australia. The Indian survey pointed at record expansion in private sector business activity in August with the composite PMI surging from 61.1 to 65.2. Sub-sector data revealed broad-based strength across India's economy as growth in both manufacturing and services output accelerated. Expectations for next 12 months also improved strongly, underpinned by the demand outlook. As for pricing trends, the latest survey data indicated an intensification of inflationary pressures across India's private sector. Japanese overall business activity expanded at the quickest pace in six months (composite 51.9 from 51.6). Like in India, the upturn was broad-based with a fresh rise in factory production accompanying a further strong increase in services activity. The manufacturing outlook nevertheless remains subdued with new orders still falling. Growth is being largely fueled by domestic demand with companies recording lower foreign demand (eg yesterday’s trade data; US tariffs hurting). Average input costs rose sharply but intense competition and requests from clients for discounts dampened overall pricing power resulting in a stronger squeeze in operating margins. Finally, also the Australian PMI (54.9 from 53.8) beat consensus with private sector output expanding at the fastest pace since April 2022. Domestic factors (RBA rate cuts) supported better conditions domestically, but external conditions also started to pick-up. To cope with demand, Australian firms raised staffing levels in the services sector. It’s the best of both worlds with price pressures also easing according to the survey. Companies broadly cited hopes for better market conditions and business expansion plans to drive growth in the year ahead...

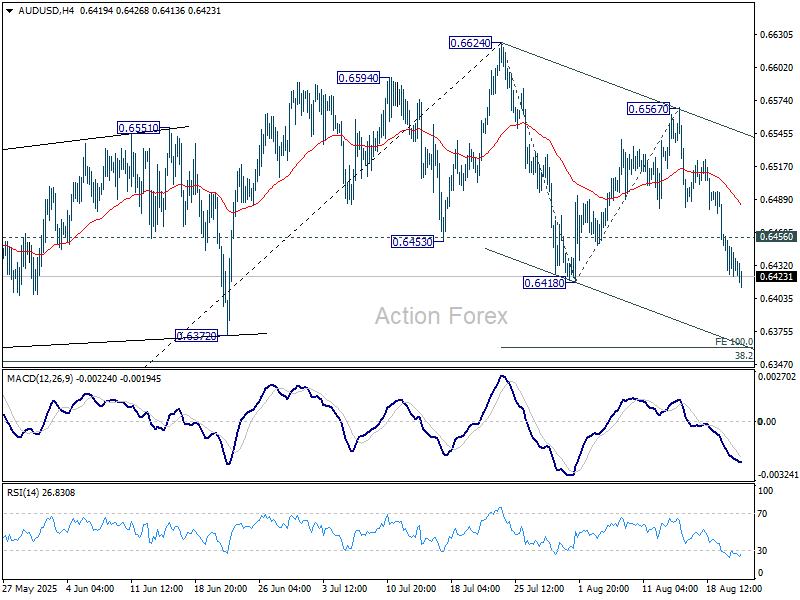

AUD/USD Daily Report

Daily Pivots: (S1) 0.6416; (P) 0.6442; (R1) 0.6461; More...

Intraday bias in AUD/USD stays on the downside for the moment. Firm break of 0.6418 support will resume the whole corrective fall form 0.6624. Next target is 38.2% retracement of 0.5913 to 0.6624 at 0.6352. On the upside, above 0.6456 minor resistance will turn intraday bias neutral again first.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

Caution Dominates FX as Jackson Hole Opens, Risk Mood Fragile

Market activity cooled notably in Asian session today, with major currency pairs and crosses confined to tight ranges. The cautious mood reflects investor focus on the Jackson Hole Symposium, which begins today. The gathering of global central bankers is always a closely watched event, but this year’s comes at a particularly sensitive moment for markets.

The spotlight, of course, is on Fed Chair Jerome Powell’s remarks tomorrow. But in the meantime, headlines will still be populated by interventions from other central bankers, making it a cautious and headline-driven session. This year’s symposium carries extra weight given the backdrop of shifting Fed expectations and recent volatility across asset classes.

The event comes just after the release of the July FOMC minutes overnight, which revealed that most Fed officials maintained caution around tariff risks. That document, however, already looks dated. Since then, the US has reported a much weaker July payrolls report with sharp downward revisions, while early August brought another round of tariff escalations. These developments have significantly shifted the debate inside and outside the Fed.

Still, Fed’s latest dot plot projected two cuts in the second half of the year, suggesting September is the logical window for the first move. Fed funds futures currently price in an 82% chance of a September cut, slightly down from 92% a week ago. The real uncertainty lies in how forcefully the Fed will move after September, with opinions ranging from front-loading cuts to spreading them more cautiously.

This nuance will be critical for market sentiment, particularly with Wall Street already showing cracks. Technology stocks have been under heavy selling pressure this week, with NASDAQ struggling to recover after sharp declines. While the index managed to pare back some losses overnight, it remains vulnerable. Any hawkish surprise at Jackson Hole could amplify risk aversion and extend safe-haven flows into the Yen.

Beyond central bank rhetoric, attention today also turns to flash PMI data. The UK release is especially important after yesterday’s hotter-than-expected CPI print, which raised doubts about another BoE cut in November. For now, markets have pushed back expectations, with a quarter-point cut not fully priced until March 2026, compared with consensus earlier this month for a move by year-end.

A strong PMI reading would add further support to Sterling, though as recent sessions have shown, domestic strength may still be overshadowed by global risk-off sentiment. Sterling’s rebound after CPI data was already capped by souring risk appetite.

On the weekly performance scoreboard, Swiss Franc is currently the strongest currency, followed by Dollar and Yen. At the other end, Kiwi has underperformed badly, followed by Aussie and Sterling, while Euro and Loonie hold middle ground.

In Asia, at the time of writing, Nikkei is down -0.54%. Hong Kong HSI is down -0.25%. China Shanghai SSE is up 0.24%. Singapore Strait Times is up 0.22%. Japan 10-year JGB yield is up 0.005 at 1.613. Overnight, DOW rose 0.04% S&P 500 fell -0.24%. NASDAQ fell -0.67%. 10-year yield fell -0.006 to 4.296.

FOMC minutes show Waller, Bowman the dove outliers amid tariff uncertainty

FOMC minutes from July 29–30 meeting showed that while two members, Governor Christopher Waller and Michelle Bowman, dissented in favor of a rate cut, they remained isolated within the Committee. “Almost all participants” judged it appropriate to keep the federal funds rate at 4.25%–4.50%, highlighting the broad consensus to hold steady amid uncertainty.

The discussion revealed a split in emphasis: most officials still see upside inflation risks as "the greater of these two risks", particularly given tariffs and the risk of unanchored expectations. But a couple of members warned that weakening employment should not be underestimated, reflecting the growing tension between Fed’s dual mandate.

The minutes flagged “considerable uncertainty” over the timing and scale of tariff effects, leaving policymakers braced for potential tradeoffs if inflation proves sticky while labor market softens. Rate decisions, thus, would depend on “each variable’s distance from the Committee’s goal and the potentially different time horizons over which those respective gaps would be anticipated to close.”

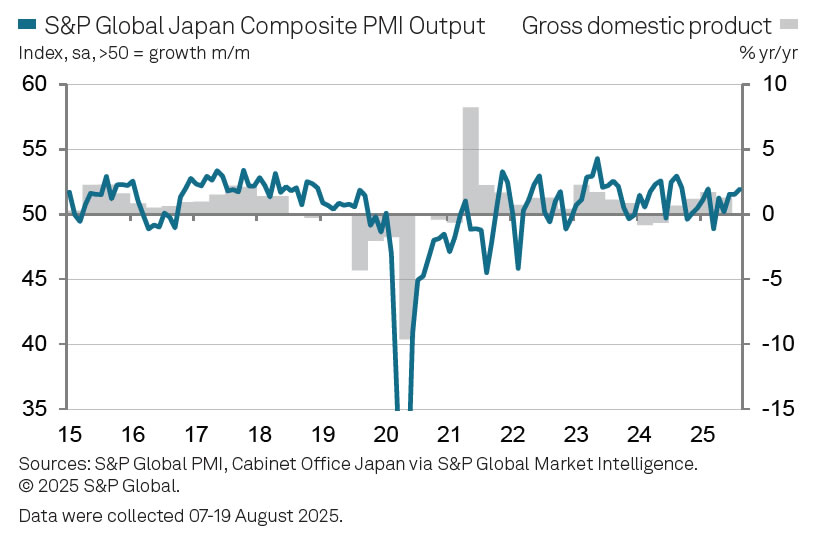

Japan’s PMI manufacturing nears expansion at 49.9, but external demand raises sustainability concerns

Japan’s flash PMI data for August showed momentum improving, with the composite index rising slightly from 51.6 to 51.9. Manufacturing posted a surprise recovery, with output climbing back into expansion at 50.5 from 47.6, while the broader PMI Manufacturing rose to 49.9 from 48.9. However, services growth slowed, with the index easing to 52.7 from 53.6.

S&P Global’s Annabel Fiddes noted that the upturn was broad-based, led by a fresh rise in factory production alongside continued service-sector strength. Still, new orders in manufacturing remained weak, raising questions about how sustainable the rebound in factory output will be without stronger demand.

Foreign demand was a drag across both goods and services, leaving the recovery heavily reliant on domestic activity. At the same time, rising input costs squeezed firms’ margins as competitive pressures limited their ability to pass costs on to clients. Selling price inflation slowed to its weakest pace since October, underlining the profitability challenge for Japanese businesses.

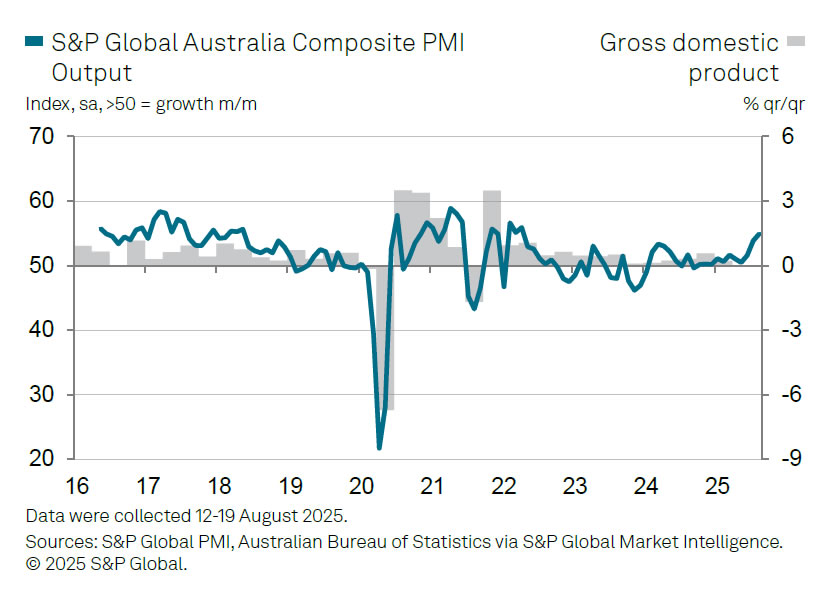

Australia PMI composite rises to 54.9, growth broadening, inflation cooling

Australia’s private sector gained momentum in August, with both manufacturing and services showing stronger growth. Manufacturing PMI climbed to 52.9 from 51.3, while Services PMI improved to 55.1 from 54.1. As a result, Composite PMI rose to 54.9 from 53.8, its highest since April 2022, signaling a broadening recovery.

S&P Global’s Jingyi Pan noted that easier interest rates have supported domestic activity, while external demand is also beginning to revive. Export orders picked up, adding to optimism among Australian businesses, and sentiment strengthened notably through the month.

Price pressures, meanwhile, showed signs of easing. Output price inflation pulled back from July’s recent high, a shift that could help sustain demand in the months ahead. That combination of stronger demand and softer price growth points to a healthier balance in the economy and gives RBA space to assess policy moves more carefully in the coming months.

NZ trade swings back into deficit despite broad export gains

New Zealand’s trade balance flipped back into deficit in July, with imports outpacing exports despite solid overseas demand. Goods exports climbed 10% yoy to NZD 6.7 billion, but imports rose 2.6% yoy to NZD 7.3 billion, leaving a monthly deficit of NZD -578 million compared with expectation of NZD 70 million surplus.

Export performance was broadly positive across major partners. Shipments to the EU jumped 28% yoy, while sales to Japan rose 23%. Exports to the U.S. and China also advanced by 7.7% and 7.1% respectively. Australia remained steady with a 4.7% increase.

On the import side, gains were concentrated in the EU and U.S., up 22% yoy and 24% respectively. Purchases from China increased 6.9%, while imports from Australia ticked up by 2.7%. However, imports from South Korea slumped by a sharp -33%.

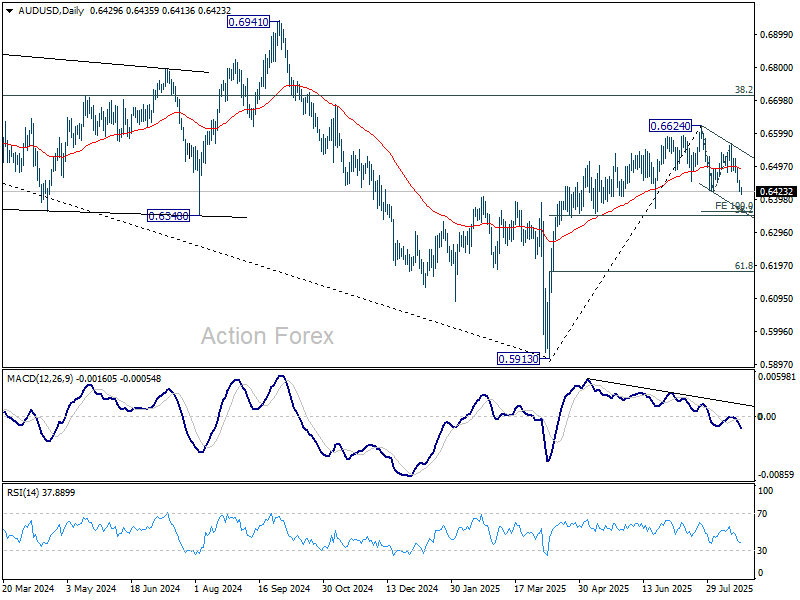

AUD/USD Daily Report

Daily Pivots: (S1) 0.6416; (P) 0.6442; (R1) 0.6461; More...

Intraday bias in AUD/USD stays on the downside for the moment. Firm break of 0.6418 support will resume the whole corrective fall form 0.6624. Next target is 38.2% retracement of 0.5913 to 0.6624 at 0.6352. On the upside, above 0.6456 minor resistance will turn intraday bias neutral again first.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

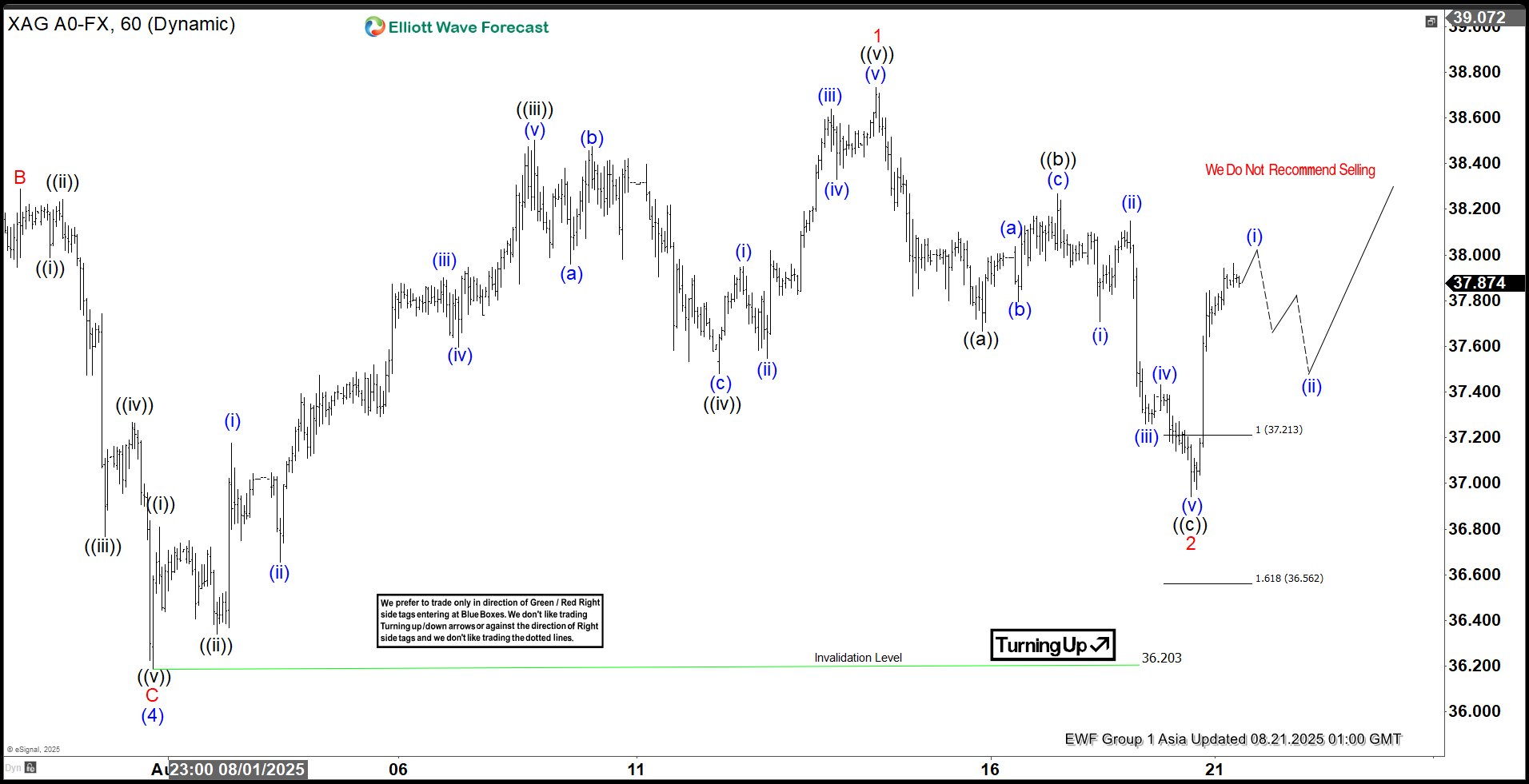

Elliott Wave Analysis: Silver (XAGUSD) Rallies Post Three Wave Pullback, Aiming for New Highs

The bullish cycle in Silver (XAGUSD), initiated from the April 2025 low, continues to unfold as an impulse pattern. Starting from that low, wave (1) peaked at 33.68, followed by a corrective dip in wave (2) that concluded at 31.65. Silver then surged in wave (3) to 39.52, with a subsequent pullback in wave (4) finding support at 36.2, as illustrated on the 1-hour chart. Currently, wave (5) is developing as a lower-degree impulse. For the bullish trend to persist without risk of a double correction, Silver must break above 49.52.

From the wave (4) low, wave ((i)) reached 36.8, and a brief pullback in wave ((ii)) stabilized at 36.34. The metal then climbed in wave ((iii)) to 38.5, followed by a correction in wave ((iv)) to 37.48. The final leg, wave ((v)), concluded at 38.73, completing wave 1 in a higher degree. A corrective wave 2 then unfolded as a zigzag Elliott Wave structure. From the wave 1 peak, wave ((a)) declined to 37.7, wave ((b)) rallied to 38.26, and wave ((c)) fell to 36.94, finalizing wave 2. Silver has now resumed its ascent in wave 3. As long as the 36.2 pivot holds, expect Silver to continue rallying.

Silver (XAGUSD) – 60 Minute Elliott Wave Technical Chart:

XAGUSD – Elliott Wave Technical Video:

https://www.youtube.com/watch?v=slkMV79bebg

FOMC Minutes to Set the Tone Ahead of Jackson Hole Symposium

In focus today

The spotlight is on the Kansas City Fed's annual Jackson Hole economic policy symposium which begins today. This year's theme will be "Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy".

On the data front, the PMIs are released for the euro area, US and UK for August. For the euro area, we expect growth to be weaker in the second half of the year due to the unwind of front-loading effects that made growth surprise positively in the first half.

In the Nordics, we receive Danish consumer sentiment which we anticipate will continue to decline slightly. This is driven by the continued rise in food prices, which typically have a significant effect on sentiment, despite solid personal finances. In Norway, Q2 mainland GDP growth is expected to come in at 0.3%.

Overnight nationwide Japanese CPI inflation will be released. Tokyo data indicates that core price pressures were very muted in July, however, that food prices, which are the real headache in Japan, continued higher.

Economic and market news

What happened overnight

In Japan, the preliminary PMI data for August improved as manufacturing PMI rose closer to the 50-mark. The services PMI was slightly softer, dropping from 53.6 to 52.7. Subindices for input prices rose, while the corresponding increase in output prices was more muted. This suggests some margin compression and that the pricing power among Japanese companies is rather modest these days.

In the US, Federal Reserve governor Lisa Cook announced she would not step down following accusations of mortgage fraud from Bill Pulte, whom Trump nominated as the head of the Federal Housing Finance Agency last March. The continuing series of attacks on the Fed by the Trump administration is a concern markets are watching closely.

What happened yesterday

In the US, yesterday's FOMC minutes from the July meeting revealed that most FOMC members remain more concerned about inflation than labour market conditions, with many expecting the full impact of tariffs on goods and services prices to take time to materialise. However, the market reaction was muted, as incoming data - and mainly employment growth - has shifted considerably since the July meeting.

In the euro area, the final HICP print confirmed the flash release of 2.0% y/y in headline and 2.3% y/y in core inflation. Core inflation was revised marginally up to 2.31% y/y from 2.28% y/y, but there were overall no significant surprises in the details of the final print. The 'LIMI' measure of domestic inflation declined from 3.8% y/y to 3.6% y/y, which shows that domestic price pressures are slowly abating as expected given lower wage growth.

In Denmark, the Danish government is planning to cut the electricity fee to the EU minimum in 2026 and 2027. It is not ruling out that it will be permanent, which would be expensive though, with an annual cost of DKK 7bn. Officially the proposal will likely be presented in the budget proposal for 2026, likely next week. This will roughly shave off 0.7% from the CPI index, which comes on top of the 0.1% from the already planned small cut for 2026. Given that the government has a majority, it will likely pass.

In Sweden, the Riksbank kept the policy rate unchanged at 2.0% as widely expected and kept the downside bias from the June meeting, saying in the report that it 'still sees some probability of a further interest rate cut this year'. This formulation is very similar to the one used in the June MPR of 'some probability of another cut this year'(See our review here: Riksbank review - August 2025 Unchanged at 2.0% as expected, keeping downside bias, 20 August).

In the UK, the CPI for July surprised to the topside across the board and above Bank of England (BoE) expectations from the August meeting. Headline came in at 3.8% (cons: 3.7%), core at 3.8% (cons: 3.7%) and services at 5.0% (cons: 4.8). Service inflation remained surprisingly sticky and with goods inflation rising this should make the BoE take a more cautious approach. With recent labour market weakening and weak underlying growth this leaves a very tricky backdrop for the BoE with pronounced signs of stagflation. Note we still have two more CPI prints and labour market reports before the next meeting in November.

In China, the one- and five-year Loan Prime Rate (LPR) remained unchanged at 3.0% and 3.5% as widely expected. The LPRs are based on the banks' lending rates and typically adjusted on the back of prior changes in the reverse repo rate by The People's Bank of China (PBOC). Since there has been no change in the repo rate it is no surprise the LPRs are unchanged. However, we do expect the PBOC to ease their monetary policy over the next month or two, based on the recent soft data and stimulus signals coming from Beijing.

Equities: Equities sold off again yesterday in a session that could almost have been a replay of Tuesday's dynamics. Tech led the decline, while defensive value and low-volatility names outperformed alongside increasing implied volatility. As is typically the case when tech underperforms, US indices lagged Europe, with the Dow again outperforming both the S&P 500 and the Nasdaq. Seven of eleven US sectors still finished higher, echoing Tuesday's pattern. For details on why we see headwinds for tech persisting, we refer to yesterday's Espresso. In the US yesterday, Dow +0.04%, S&P 500 -0.2%, Nasdaq -0.7% and Russell 2000 -0.3%. In Asia, parts of the market are stabilizing this morning, most notably Taiwan and Korea, where tech is driving gains, while the rest of the region trades mixed. Futures point to a modestly firmer tone in US tech. European equity futures are higher as well.

FI and FX: Rates extended the move lower across regions as risky assets and namely tech stocks continue to struggle, and markets disregarded the somewhat outdated hawkish signals in the FOMC minutes. EUR/USD continues to hover in the mid-1.16 to 1.17 range in what has been a very quiet week so far, with the USD modestly firmer across the G10. Despite a topside surprise to UK CPI for July, GBP FX came under pressure during yesterday's session with GILTS outperforming the broader FI market. Brent moved up by 1.75% to USD67/bbl. as US inventories declined according to the weekly EIA report. Asian equities are mixed this morning.

Japan’s PMI manufacturing nears expansion at 49.9, but external demand raises sustainability concerns

Japan’s flash PMI data for August showed momentum improving, with the composite index rising slightly from 51.6 to 51.9. Manufacturing posted a surprise recovery, with output climbing back into expansion at 50.5 from 47.6, while the broader PMI Manufacturing rose to 49.9 from 48.9. However, services growth slowed, with the index easing to 52.7 from 53.6.

S&P Global’s Annabel Fiddes noted that the upturn was broad-based, led by a fresh rise in factory production alongside continued service-sector strength. Still, new orders in manufacturing remained weak, raising questions about how sustainable the rebound in factory output will be without stronger demand.

Foreign demand was a drag across both goods and services, leaving the recovery heavily reliant on domestic activity. At the same time, rising input costs squeezed firms’ margins as competitive pressures limited their ability to pass costs on to clients. Selling price inflation slowed to its weakest pace since October, underlining the profitability challenge for Japanese businesses.

Australia PMI composite rises to 54.9, growth broadening, inflation cooling

Australia’s private sector gained momentum in August, with both manufacturing and services showing stronger growth. Manufacturing PMI climbed to 52.9 from 51.3, while Services PMI improved to 55.1 from 54.1. As a result, Composite PMI rose to 54.9 from 53.8, its highest since April 2022, signaling a broadening recovery.

S&P Global’s Jingyi Pan noted that easier interest rates have supported domestic activity, while external demand is also beginning to revive. Export orders picked up, adding to optimism among Australian businesses, and sentiment strengthened notably through the month.

Price pressures, meanwhile, showed signs of easing. Output price inflation pulled back from July’s recent high, a shift that could help sustain demand in the months ahead. That combination of stronger demand and softer price growth points to a healthier balance in the economy and gives RBA space to assess policy moves more carefully in the coming months.

NZ trade swings back into deficit despite broad export gains

New Zealand’s trade balance flipped back into deficit in July, with imports outpacing exports despite solid overseas demand. Goods exports climbed 10% yoy to NZD 6.7 billion, but imports rose 2.6% yoy to NZD 7.3 billion, leaving a monthly deficit of NZD -578 million compared with expectation of NZD 70 million surplus.

Export performance was broadly positive across major partners. Shipments to the EU jumped 28% yoy, while sales to Japan rose 23%. Exports to the U.S. and China also advanced by 7.7% and 7.1% respectively. Australia remained steady with a 4.7% increase.

On the import side, gains were concentrated in the EU and U.S., up 22% yoy and 24% respectively. Purchases from China increased 6.9%, while imports from Australia ticked up by 2.7%. However, imports from South Korea slumped by a sharp -33%.

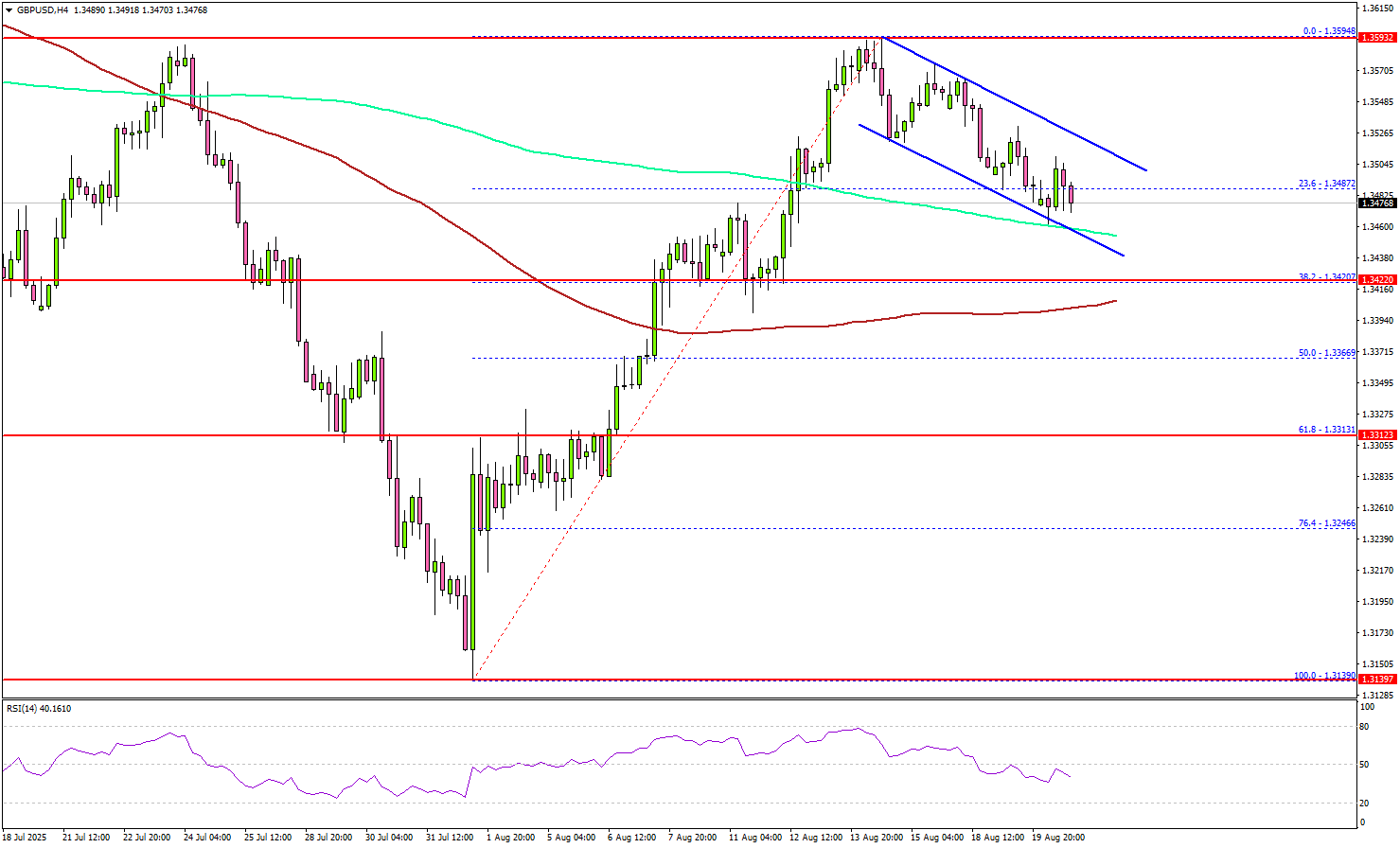

GBP/USD Charts Signal Trouble, Will Bears Dominate the Market?

Key Highlights

- GBP/USD seems to be forming a double top pattern at 1.3590.

- A declining channel is forming with resistance at 1.3510 on the 4-hour chart.

- Bitcoin declined below the $118,500 and $115,500 support levels.

- Ethereum started a downside correction and traded below $4,250.

GBP/USD Technical Analysis

The British Pound failed to continue higher above 1.3590 against the US Dollar. GBP/USD seems to be forming a double top pattern at 1.3590 and is at risk of a bearish reaction.

Looking at the 4-hour chart, the pair corrected some gains and traded below the 1.3525 support level. There was a move below the 23.6% Fib retracement level of the upward move from the 1.3139 swing low to the 1.3594 high.

However, the pair is still above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the downside, immediate support is 1.3450.

The next key support sits at 1.3420 and the 100 simple moving average (red, 4-hour). Any more losses could send the pair toward the 61.8% Fib retracement level of the upward move from the 1.3139 swing low to the 1.3594 high at 1.3310.

On the upside, the pair now faces resistance near the 1.3510 level and a declining channel. The next key resistance sits near 1.3540. A close above 1.3540 could set the pace for another increase. In the stated case, the pair could rise toward 1.3590, above which the bulls could aim for a move toward 1.3680.

Looking at EUR/USD, the pair started a downside correction, but the bulls were able to protect the 1.1600 support.

Upcoming Key Economic Events:

- Euro Zone Manufacturing PMI for August 2025 (Preliminary) – Forecast 49.5, versus 49.8 previous.

- Euro Zone Services PMI for August 2025 (Preliminary) – Forecast 50.6, versus 51.0 previous.

- UK Manufacturing PMI for August 2025 (Preliminary) – Forecast 48.3, versus 48.0 previous.

- UK Services PMI for August 2025 (Preliminary) – Forecast 52.0, versus 51.8 previous.

- US Manufacturing PMI for August 2025 (Preliminary) – Forecast 49.5, versus 49.8 previous.

- US Services PMI for August 2025 (Preliminary) – Forecast 54.2, versus 55.7 previous.

- US Initial Jobless Claims - Forecast 225K, versus 224K previous.