Sample Category Title

FOMC minutes show Waller, Bowman the dove outliers amid tariff uncertainty

FOMC minutes from July 29–30 meeting showed that while two members, Governor Christopher Waller and Michelle Bowman, dissented in favor of a rate cut, they remained isolated within the Committee. “Almost all participants” judged it appropriate to keep the federal funds rate at 4.25%–4.50%, highlighting the broad consensus to hold steady amid uncertainty.

The discussion revealed a split in emphasis: most officials still see upside inflation risks as "the greater of these two risks", particularly given tariffs and the risk of unanchored expectations. But a couple of members warned that weakening employment should not be underestimated, reflecting the growing tension between Fed’s dual mandate.

The minutes flagged “considerable uncertainty” over the timing and scale of tariff effects, leaving policymakers braced for potential tradeoffs if inflation proves sticky while labor market softens. Rate decisions, thus, would depend on “each variable’s distance from the Committee’s goal and the potentially different time horizons over which those respective gaps would be anticipated to close.”

(FED) Minutes of the Federal Open Market Committee

July 29–30, 2025

A joint meeting of the Federal Open Market Committee and the Board of Governors of the Federal Reserve System was held in the offices of the Board of Governors on Tuesday, July 29, 2025, at 9:00 a.m. and continued on Wednesday, July 30, 2025, at 9:00 a.m.1

Review of Monetary Policy Strategy, Tools, and Communications

Participants continued their discussion related to the ongoing review of the Federal Reserve's monetary policy strategy, tools, and communication practices (framework review). They observed that they had made important progress toward revising the Committee's Statement on Longer-Run Goals and Monetary Policy Strategy (consensus statement). Participants discussed potential revisions to theconsensus statement that would incorporate lessons learned from economic developments since the 2020 framework review and would be designed to be robust across a wide range of economic conditions. Participants noted that the Committee was close to finalizing changes to the consensus statement and would do so in the near future.

Developments in Financial Markets and Open Market Operations

The manager turned first to a review of financial market developments. Over the intermeeting period, the expected path of the policy rate and longer-term Treasury yields were little changed, equity prices increased, credit spreads narrowed, and the dollar depreciated slightly. The manager noted that markets continued to be attentive to news related to trade policy, though markets' reaction to incoming information on this topic was more restrained than in April and May. Against this backdrop, the manager reported that the Open Market Desk's Survey of Market Expectations (Desk survey) indicated that the median respondent's expectations regarding both real gross domestic product (GDP) growth and inflation were roughly unchanged.

The manager turned next to policy rate expectations, which held steady over the intermeeting period, consistent with a relatively stable macroeconomic outlook. The median modal path of the federal funds rate, as given in the Desk survey, was unchanged from the corresponding path in the June survey and continued to indicate expectations of two 25 basis point rate cuts in the second half of this year. Market-based measures of policy rate expectations were also little changed and indicated expectations of one to two 25 basis point rate cuts by the end of the year.

The manager then discussed developments in Treasury securities markets and market-based measures of inflation compensation. Nominal Treasury yields were little changed, on net, over the intermeeting period, consistent with the lack of appreciable changes in the macroeconomic outlook and in policy rate expectations. Perceived risks associated with trade policy developments contributed to an increase in near-term market measures of inflation compensation, while longer-horizon measures of inflation compensation rose more modestly.

The manager then turned to market pricing of risky assets. The increases in equity prices and narrowing of credit spreads suggested that markets assessed that the overall U.S. economy was remaining resilient; still, financial markets appeared to be making distinctions between individual corporations on the basis of the size and quality of their earnings. Valuations of the S&P 500 index continued to move above long-run average levels, mostly driven by optimism about the largest technology firms' scope to benefit from the further adoption of artificial intelligence (AI). However, valuations of an index of smaller-capitalization firms, although higher over the intermeeting period, remained below their historical averages.

Regarding foreign exchange developments, the manager noted that the broad trade-weighted dollar index had continued to depreciate since the previous FOMC meeting but at a slower pace than in recent intermeeting periods. At the same time, the manager noted that correlations between the dollar and its fundamental drivers had normalized recently. The available data continued to suggest relative stability in foreign holdings of U.S. assets.

The manager turned next to money markets. Unsecured overnight rates remained stable over the intermeeting period. Rates on Treasury repurchase agreements (repo) were somewhat higher than the low levels seen in the previous intermeeting period. The manager observed that two factors contributed to this slight increase: the normal upward pressure on money market rates associated with the June quarter-end; and the rise in net Treasury bill issuance amid the rebuilding of the Treasury General Account (TGA) balance following the increase in the debt limit in early July. On June 30, as market rates climbed modestly above the standing repo facility's (SRF) minimum bid rate at quarter-end, there was material usage of the facility, with counterparties borrowing a bit more than $11 billion, the highest utilization to date.

The manager also discussed the projected trajectory of various Federal Reserve liabilities. With increased Treasury bill issuance associated with the rebuilding of the TGA balance likely to result in a rise in money market rates, take-up at the overnight reverse repurchase agreement (ON RRP) facility was expected to decline to low levels relatively soon. Market indicators continued to suggest that reserves remained abundant; however, ongoing System Open Market Account (SOMA) portfolio runoff, a substantial expected increase in the TGA balance, and the depletion of the ON RRP facility were together likely to bring about a sustained decline in reserves for the first time since portfolio runoff started in June 2022. Against this backdrop, the staff would continue to monitor indicators of reserve conditions closely. The manager also noted that there would be times—such as quarter-ends, tax dates, and days associated with large settlements of Treasury securities—when reserves were likely to dip temporarily to even lower levels. At those times, utilization of the SRF would likely support the smooth functioning of money markets and the implementation of monetary policy.

By unanimous vote, the Committee ratified the Desk's domestic transactions over the intermeeting period. There were no intervention operations in foreign currencies for the System's account during the intermeeting period.

Staff Review of the Economic Situation

The information available at the time of the meeting indicated that real GDP expanded at a tepid pace in the first half of the year. The unemployment rate continued to be low, and consumer price inflation remained somewhat elevated.

Disinflation appeared to have stalled, with tariffs putting upward pressure on goods price inflation. Total consumer price inflation—as measured by the 12-month change in the price index for personal consumption expenditures (PCE)—was estimated to have been 2.5 percent in June, based on the consumer and producer price indexes. Core PCE price inflation, which excludes changes in consumer energy prices and many consumer food prices, was estimated to have been 2.7 percent in June. Both inflation rates were similar to their year-earlier levels.

Recent data indicated that labor market conditions remained solid. The unemployment rate was 4.1 percent in June, down 0.1 percentage point from May. The participation rate edged down 0.1 percentage point in June, and the employment-to-population ratio was unchanged. Total nonfarm payroll gains were solid in June, though the pace of private payroll gains stepped down noticeably. The ratio of job vacancies to unemployed workers was 1.1 in June and remained within the narrow range seen over the past year. Average hourly earnings for all employees rose 3.7 percent over the 12 months ending in June, slightly lower than the year-earlier pace.

According to the advance estimate, real GDP rose in the second quarter after declining in the first quarter. Growth of real private domestic final purchases—which comprises PCE and private fixed investment and which often provides a better signal than GDP of underlying economic momentum—slowed in the second quarter, as a step-down in investment growth offset faster PCE growth.

After exerting a substantial negative drag on GDP growth in the first quarter, net exports made a large positive contribution in the second quarter. Real imports of goods and services declined sharply, likely reflecting the aftereffects of the substantial front-loading of imports recorded in the first quarter ahead of anticipated tariff hikes. By contrast, exports of goods declined at a more moderate pace, and exports of services rose further.

Abroad, activity indicators pointed to a slowdown of foreign economic growth in the second quarter, as the transitory boost due to the front-loading of U.S. imports earlier in the year faded. Of note, monthly GDP data through May indicated that economic activity contracted in Canada. China's GDP, however, continued to expand at a moderate pace in the second quarter, supported by solid domestic spending.

Headline inflation rates were near targets in most foreign economies, held down by past declines in oil prices and fading wage pressures following a tightening in monetary policy stances over the past few years. However, core inflation remained somewhat elevated in some foreign economies.

Over the intermeeting period, several foreign central banks, such as the Bank of Mexico and the Swiss National Bank, further eased their monetary policy stance, while others, such as the Bank of England and the European Central Bank, held their policy rates steady. In their communications, foreign central banks continued to emphasize that U.S. trade policies and accompanying uncertainty have started to weigh on economic activity in their economies.

Staff Review of the Financial Situation

Over the intermeeting period, both the market-implied expected path of the federal funds rate over the next year and nominal Treasury yields were little changed, on net, while real yields declined. Inflation compensation rose across the maturity spectrum—particularly at shorter horizons—reflecting, at least in part, perceived risks associated with trade policy developments.

Broad equity price indexes increased and credit spreads tightened, consistent with improving risk sentiment attributed in part to easing geopolitical tensions as well as stronger-than-expected economic activity. Credit spreads for all rating categories except the lowest-quality bonds narrowed to exceptionally low levels relative to their historical distribution. The VIX—a forward-looking measure of near-term equity market volatility—declined moderately to just below the median of its historical distribution.

Over the intermeeting period, news about trade policy interpreted as positive by investors together with some easing of geopolitical tensions in the Middle East led to moderate increases in foreign equity prices and longer-term yields. The broad dollar index was little changed on net.

Conditions in U.S. short-term funding markets remained orderly over the intermeeting period while displaying typical quarter-end dynamics. The One Big Beautiful Bill Act, which became law on July 4, ended the previous debt issuance suspension period, after which the TGA balance increased from $313 billion on July 3 to an expected $500 billion by the end of July. Rates in secured markets were, on average, somewhat elevated relative to the average over the previous intermeeting period, owing in part to quarter-end effects. Although upward pressure on repo rates was modest at quarter-end, take-up at the SRF was $11.1 billion on June 30—its highest level since the inception of the facility—as the addition of an early settlement option seemed to encourage participation. Average usage of the ON RRP facility was little changed over the intermeeting period.

In domestic credit markets, borrowing costs facing businesses, households, and municipalities eased moderately but remained elevated relative to post-Global Financial Crisis (GFC) average levels. Yields on both corporate bonds and leveraged loans declined modestly, while interest rates on small business loans were little changed on net. Rates on 30-year fixed-rate conforming residential mortgages were little changed and remained near the top of the post-GFC historical distribution. Interest rates on new auto loans and for new credit card offers have fluctuated in a narrow range in recent months around the upper end of their post-GFC distributions.

Credit remained generally available. Financing through capital markets and nonbank lenders was readily accessible for public corporations as well as large and middle-market private corporations. Issuance of nonfinancial corporate bonds and leveraged loans was solid in June, and private credit continued to be broadly available despite ebbing somewhat in May and June. Loan balances on banks' books increased at a moderate pace in the second quarter, led by growth in commercial and industrial (C&I) loans. Lending to small businesses remained subdued, an outcome attributed to weak borrower demand.

Banks in the July Senior Loan Officer Opinion Survey on Bank Lending Practices reported that, on net, underwriting standards were little changed in the second quarter across most loan categories, although the level of standards remained on the tighter end of their historical range. C&I loan standards, however, were reported to be a little easier than the range seen since 2005, yet still somewhat tighter than in periods not associated with financial stress. Consumer credit continued to be readily available for high-credit-score borrowers, though growth in applications for home purchases, refinances, auto loans, and revolving credit was relatively weak, reflecting heightened borrowing costs and tighter credit standards for lower-credit-score borrowers.

In the second quarter, credit performance was generally stable but somewhat weaker than pre-pandemic levels. Corporate bond and leveraged loan credit performance declined moderately in May and June, though defaults remained below post-GFC medians through June. In the commercial real estate market, delinquency rates on commercial mortgage-backed securities remained elevated through June. The rate of serious delinquencies on Federal Housing Administration mortgages continued to be elevated. By contrast, delinquency rates on most other mortgage loan types continued to stay near historical lows. In May, the credit card delinquency rate was a little below its year-earlier value, while that for auto loans was roughly the same as in May last year; both were elevated relative to their pre-pandemic levels. Student loan delinquencies reported to credit bureaus shot up in the first quarter of the year after the expiration of the on-ramp period for student loan payments.

The staff provided an updated assessment of the stability of the U.S. financial system and, on balance, continued to characterize the system's financial vulnerabilities as notable. The staff judged that asset valuation pressures were elevated. In equity markets, price-to-earnings ratios stood at the upper end of their historical distribution, while spreads on high-yield corporate bonds narrowed notably and were low relative to their historical distribution. Housing valuations edged down but remained elevated.

Vulnerabilities associated with nonfinancial business and household debt were characterized as moderate. Household debt to GDP was at its lowest level in the past 20 years, and household balance sheets remained strong. The ability of publicly traded firms to service their debt remained solid. For private firms, debt grew at a rapid pace, while these firms' interest coverage ratios declined to the lower range of their historical distributions, suggesting that vulnerabilities may be growing in that sector.

Vulnerabilities associated with leverage in the financial sector were characterized as notable. Regulatory capital ratios in the banking sector remained high, while recent annual supervisory stress-test results showed that all participants stayed above minimum capital requirements even under stress conditions. Banks, however, were still seen as more exposed to interest rate risk than had been historically typical, albeit to a lesser degree than was the case earlier in the decade. In the nonbank sector, life insurers' allocation of assets toward private credit and risky assets, funded in part by nontraditional liabilities with short maturities, continued to grow. Leverage and rollover risk at hedge funds remained high and concentrated in the largest firms.

Vulnerabilities associated with funding risks were characterized as moderate. Money market funds (MMFs) continued to be vulnerable to runs, though the aggregate assets of such prime and prime-like investment vehicles remained in the middle of their historical range as a fraction of GDP. Prime-like alternatives—including private liquidity funds, offshore MMFs, and stablecoins—have grown rapidly and were noted as relatively less transparent.

Staff Economic Outlook

The staff's real GDP growth projection for this year through 2027 was similar to the one prepared for the June meeting, reflecting the offsetting effects of several revisions to the outlook. The staff expected that the rise in the cost of imported goods inclusive of tariffs would be smaller and occur later than in their previous forecast; in addition, financial conditions were projected to be slightly more supportive of output growth. However, these positive influences on the outlook were offset by weaker-than-expected spending data and a smaller assumed population boost from net immigration. The staff continued to expect that the labor market would weaken, with the unemployment rate projected to move above the staff's estimate of its natural rate around the end of this year and to remain above the natural rate through 2027.

The staff's inflation projection was slightly lower than the one prepared for the June meeting, reflecting the downward revision to the assumed effects of tariffs on imported goods prices. Tariffs were expected to raise inflation this year and to provide some further upward pressure on inflation in 2026; inflation was then projected to decline to 2 percent by 2027.

The staff continued to view the uncertainty around the projection as elevated, primarily reflecting uncertainty regarding changes to economic policies, including trade policy, and their associated economic effects. Risks to real activity were judged to remain skewed to the downside in light of the weakening in GDP growth seen so far this year and elevated policy uncertainty. The staff continued to view the risks around the inflation forecast as skewed to the upside, as the projected rise in inflation this year could prove to be more persistent than assumed in the baseline projection.

Participants' Views on Current Conditions and the Economic Outlook

In their discussion of inflation, many participants observed that overall inflation remained somewhat above the Committee's 2 percent longer-run goal. Participants noted that tariff effects were becoming more apparent in the data, as indicated by recent increases in goods price inflation, while services price inflation had continued to slow. A couple of participants suggested that tariff effects were masking the underlying trend of inflation and, setting aside the tariff effects, inflation was close to target.

With regard to the outlook for inflation, participants generally expected inflation to increase in the near term. Participants judged that considerable uncertainty remained about the timing, magnitude, and persistence of the effects of this year's increase in tariffs. In terms of timing, many participants noted that it could take some time for the full effects of higher tariffs to be felt in consumer goods and services prices. Participants cited several contributors to this likely lag. These included the stockpiling of inventories in anticipation of higher tariffs; slow pass-through of input cost increases into final goods and services prices; gradual updating of contract prices; maintenance of firm–customer relationships; issues related to tariff collection; and still-ongoing trade negotiations. As for the magnitude of tariff effects on prices, a few participants observed that evidence so far suggested that foreign exporters were paying at most a modest part of the increased tariffs, implying that domestic businesses and consumers were predominantly bearing the tariff costs. Several participants, drawing on information provided by business contacts or business surveys, expected that many companies would increasingly have to pass through tariff costs to end-customers over time. However, a few participants reported that business contacts and survey respondents described a mix of strategies as being undertaken to avoid fully passing on tariff costs to customers. Such strategies included negotiating with or switching suppliers, changing production processes, lowering profit margins, exerting more wage discipline, or exploiting cost-saving efficiency measures such as automation and new technologies. A few participants stressed that current demand conditions were limiting firms' ability to pass tariff costs into prices. Regarding inflation persistence, a few participants emphasized that they expected higher tariffs to lead only to a one-time increase in the price level that would be realized over a reasonably contained period. A few participants remarked that tariff-related factors, including supply chain disruptions, could lead to stubbornly elevated inflation and that it may be difficult to disentangle tariff-related price increases from changes in underlying trend inflation.

Participants noted that longer-term inflation expectations continued to be well anchored and that it was important that they remain so. Several participants emphasized that inflation had exceeded 2 percent for an extended period and that this experience increased the risk of longer-term inflation expectations becoming unanchored in the event of drawn-out effects of higher tariffs on inflation. A couple of participants noted that inflation expectations would likely be influenced by the behavior of the overall inflation rate, inclusive of the effects of tariffs. Various participants emphasized the central role of monetary policy in ensuring that tariff effects did not lead to persistently higher expected and realized inflation.

In their discussion of the labor market, participants observed that the unemployment rate remained low and that employment was at or near estimates of maximum employment. Several participants noted that the low and stable unemployment rate reflected a combination of low hiring and low layoffs. Some participants observed that their contacts and business survey respondents had reported being reluctant to hire or fire amid elevated uncertainty. Regarding the outlook for the labor market, some participants mentioned indicators that could suggest a softening in labor demand. These included slower and more concentrated job growth, an increase in cyclically sensitive Black and youth unemployment rates, and lower wage increases of job switchers than job stayers. Some of these participants also noted anecdotes in the Beige Book or in their discussions with contacts that pointed to slower demand. Furthermore, a number of participants noted that softness in aggregate demand and economic activity may translate into weaker labor market conditions, as could a potential inability of some importers to withstand higher tariffs. Some participants remarked, however, that slower output or employment growth was not necessarily indicative of emerging economic slack because a decline in immigration was lowering both actual and potential output growth as well as reducing both actual payroll growth and the number of new jobs needed to keep the unemployment rate stable. A few participants relayed reports received from contacts that immigration policies were affecting labor supply in some sectors, including construction and agriculture.

Participants observed that growth of economic activity slowed in the first half of the year, driven in large part by slower consumption growth and a decline in residential investment. Several participants stated that they expected growth in economic activity to remain low in the second half of this year. Some participants noted that economic activity would nevertheless be supported by financial conditions, including elevated household net worth, and a couple of participants highlighted stable or low credit card delinquencies. A couple of participants remarked that economic activity would be supported by the resolution of policy uncertainty over time. Regarding the household sector, several participants observed that slower real income growth may be weighing on growth in consumer spending. A few participants noted a weakening in housing demand, with increased availability of homes for sale and falling house prices. As for businesses, several participants remarked that ongoing policy uncertainty had continued to slow business investment, but several observed that business sentiment had improved in recent months. A few participants commented that the agricultural sector faced headwinds due to low crop prices.

In their evaluation of the risks and uncertainties associated with the economic outlook, participants judged that uncertainty about the economic outlook remained elevated, though several participants remarked that there had been some reduction in uncertainty regarding fiscal policy, immigration policy, or tariff policy. Participants generally pointed to risks to both sides of the Committee's dual mandate, emphasizing upside risk to inflation and downside risk to employment. A majority of participants judged the upside risk to inflation as the greater of these two risks, while several participants viewed the two risks as roughly balanced, and a couple of participants considered downside risk to employment the more salient risk. Regarding upside risks to inflation, participants pointed to the uncertain effects of tariffs and the possibility of inflation expectations becoming unanchored. In addition to tariff-induced risks, potential downside risks to employment mentioned by participants included a possible tightening of financial conditions due to a rise in risk premiums, a more substantial deterioration in the housing market, and the risk that the increased use of AI in the workplace may lower employment.

In their discussion of financial stability, participants who commented noted vulnerabilities to the financial system that they assessed warranted monitoring. Several participants noted concerns about elevated asset valuation pressures. Regarding banks, a couple of participants commented that, though regulatory capital levels remained strong, some banks continued to be vulnerable to a rise in longer-term yields and the associated unrealized losses on bank assets. A few participants commented on vulnerabilities in the market for Treasury securities, raising concerns about dealer intermediation capacity, the increasing presence of hedge funds in the market, and the fragility associated with low market depth. A couple of participants discussed foreign exchange swaps, noting that these served as key sources of dollar funding for foreign financial institutions that lend dollars to their customers in the U.S. and abroad, but also that they entailed vulnerabilities due to maturity mismatch and rollover risk. Many participants discussed recent and prospective developments related to payment stablecoins and possible implications for the financial system. These participants noted that use of payment stablecoins might grow following the recent passage of the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act). They remarked that payment stablecoins could help improve the efficiency of the payment system. They also observed that such stablecoins could increase the demand for the assets needed to back them, including Treasury securities. In addition, participants who commented raised concerns that stablecoins could have broader implications for the banking and financial systems as well as monetary policy implementation, and thus warranted close attention, including monitoring of the various assets used to back stablecoins.

In their consideration of monetary policy at this meeting, participants noted that inflation remained somewhat elevated. Participants also observed that recent indicators suggested that the growth of economic activity had moderated in the first half of the year, although swings in net exports and inventories had affected the measurement and interpretation of the data. Participants further noted that the unemployment rate remained at a low level and that the labor market was at or near maximum employment. Participants judged that uncertainty about the economic outlook remained elevated. Almost all participants viewed it as appropriate to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent at this meeting. All participants judged it appropriate to continue the process of reducing the Federal Reserve's securities holdings.

In considering the outlook for monetary policy, almost all participants agreed that, with the labor market still solid and current monetary policy moderately or modestly restrictive, the Committee was well positioned to respond in a timely way to potential economic developments. Participants agreed that monetary policy would be informed by a wide range of incoming data, the economic outlook, and the balance of risks. Participants assessed that the effects of higher tariffs had become more apparent in the prices of some goods but that their overall effects on economic activity and inflation remained to be seen. They also noted that it would take time to have more clarity on the magnitude and persistence of higher tariffs' effects on inflation. Even so, some participants emphasized that a great deal could be learned in coming months from incoming data, helping to inform their assessment of the balance of risks and the appropriate setting of the federal funds rate; at the same time, some noted that it would not be feasible or appropriate to wait for complete clarity on the tariffs' effects on inflation before adjusting the stance of monetary policy. Some participants stressed that the issue of the persistence of tariff effects on inflation would depend importantly on the stance of monetary policy. Several participants commented that the current target range for the federal funds rate may not be far above its neutral level; among the considerations cited in support of this assessment was the likelihood that broader financial conditions were either neutral or supportive of stronger economic activity.

In discussing risk-management considerations that could bear on the outlook for monetary policy, participants generally agreed that the upside risk to inflation and the downside risk to employment remained elevated. Participants noted that, if this year's higher tariffs were to generate a larger-than-expected or a more-persistent-than-anticipated increase in inflation, or if medium- or longer-term inflation expectations were to increase notably, then it would be appropriate to maintain a more restrictive stance of monetary policy than would otherwise be the case, especially if labor market conditions remained solid. By contrast, if labor market conditions were to weaken materially or if inflation were to come down further and inflation expectations remained well anchored, then it would be appropriate to establish a less restrictive stance of monetary policy than would otherwise be the case. Participants noted that the Committee might face difficult tradeoffs if elevated inflation proved to be more persistent while the outlook for the labor market weakened. Participants agreed that, if that situation were to occur, they would consider each variable's distance from the Committee's goal and the potentially different time horizons over which those respective gaps would be anticipated to close. Participants noted that, in this context, it was especially important to ensure that longer-term inflation expectations remained well anchored.

Several participants remarked on issues related to the Federal Reserve's balance sheet. Of those who commented, participants observed that balance sheet reduction had been proceeding smoothly thus far and that various indicators pointed to reserves being abundant. They agreed that, with reserves projected to decline amid the rebuilding of the TGA balance following the resolution of the debt limit situation, it was important to monitor money market conditions closely and to continue to evaluate how close reserves were to their ample level. A few participants also assessed that, in this environment, abrupt further declines in reserves could occur on key reporting and payment flow days. They noted that, if such events created pressures in money markets, the Federal Reserve's existing tools would help supply additional reserves and keep the effective federal funds rate within the target range. A couple of participants highlighted the role of the SRF in monetary policy implementation—as reflected in increased usage at the June quarter-end—and expressed support for further study of the possibility of central clearing of the SRF to enhance its effectiveness.

Committee Policy Actions

In their discussions of monetary policy for this meeting, members agreed that although swings in net exports had affected the data, recent indicators suggested that the growth of economic activity had moderated in the first half of the year. Members agreed that the unemployment rate had remained at a low level and that labor market conditions had remained solid. Members concurred that inflation remained somewhat elevated. Members agreed that uncertainty about the economic outlook remained elevated and that the Committee was attentive to the risks to both sides of its dual mandate.

In support of the Committee's goals, almost all members agreed to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. A couple of members preferred to lower the target range for the federal funds rate by 25 basis points at this meeting. These members judged that, excluding tariff effects, inflation was running close to the Committee's 2 percent objective and that higher tariffs were unlikely to have persistent effects on inflation. Furthermore, they assessed that downside risk to employment had meaningfully increased with the slowing of the growth of economic activity and consumer spending, and that some incoming data pointed to a weakening of labor market conditions, including low levels of private payroll gains and the concentration of payroll gains in a narrow set of industries that were less affected by the business cycle. Members agreed that in considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee would carefully assess incoming data, the evolving outlook, and the balance of risks. All members agreed that the postmeeting statement should affirm their strong commitment both to supporting maximum employment and to returning inflation to the Committee's 2 percent objective.

Members agreed that, in assessing the appropriate stance of monetary policy, the Committee would continue to monitor the implications of incoming information for the economic outlook. They would be prepared to adjust the stance of monetary policy as appropriate if risks emerged that could impede the attainment of the Committee's goals. Members also agreed that their assessments would take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

At the conclusion of the discussion, the Committee voted to direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the SOMA in accordance with the following domestic policy directive, for release at 2:00 p.m.:

"Effective July 31, 2025, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 4-1/4 to 4-1/2 percent.

- Conduct standing overnight repurchase agreement operations with a minimum bid rate of 4.5 percent and with an aggregate operation limit of $500 billion.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 4.25 percent and with a per-counterparty limit of $160 billion per day.

- Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $5 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.

- Reinvest the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities (MBS) received in each calendar month that exceeds a cap of $35 billion per month into Treasury securities to roughly match the maturity composition of Treasury securities outstanding.

- Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons."

The vote also encompassed approval of the statement below for release at 2:00 p.m.:

"Although swings in net exports continue to affect the data, recent indicators suggest that growth of economic activity moderated in the first half of the year. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments."

Voting for this action:Jerome H. Powell, John C. Williams, Michael S. Barr, Susan M. Collins, Lisa D. Cook, Austan D. Goolsbee, Philip N. Jefferson, Alberto G. Musalem, and Jeffrey R. Schmid.

Voting against this action: Michelle W. Bowman and Christopher J. Waller.

Absent and not voting: Adriana D. Kugler

Governors Bowman and Waller preferred to lower the target range for the federal funds rate by 1/4 percentage point at this meeting. Governor Bowman preferred at this meeting to lower the target range for the federal funds rate by 25 basis points to 4 to 4-1/4 percent in light of inflation moving considerably closer to the Committee's objective, after excluding temporary effects of tariffs, a labor market near full employment but with signs of less dynamism, and slowing economic growth this year. She also expressed her view that taking action to begin moving the policy rate at a gradual pace toward its neutral level would have proactively hedged against a further weakening in the economy and the risk of damage to the labor market.

Consistent with the Committee's decision to leave the target range for the federal funds rate unchanged, the Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 4.4 percent, effective July 31, 2025. The Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 4.5 percent.

It was agreed that the next meeting of the Committee would be held on Tuesday–Wednesday, September 16–17, 2025. The meeting adjourned at 10:15 a.m. on July 30, 2025.

Notation Vote

By notation vote completed on July 8, 2025, the Committee unanimously approved the minutes of the Committee meeting held on June 17–18, 2025.

Attendance

Jerome H. Powell, Chair

John C. Williams, Vice Chair

Michael S. Barr

Michelle W. Bowman

Susan M. Collins

Lisa D. Cook

Austan D. Goolsbee

Philip N. Jefferson

Alberto G. Musalem

Jeffrey R. Schmid

Christopher J. Waller

Beth M. Hammack, Neel Kashkari, Lorie K. Logan, Anna Paulson, and Sushmita Shukla, Alternate Members of the Committee

Thomas I. Barkin, Raphael W. Bostic, and Mary C. Daly, Presidents of the Federal Reserve Banks of Richmond, Atlanta, and San Francisco, respectively

Joshua Gallin, Secretary

Matthew M. Luecke, Deputy Secretary

Brian J. Bonis, Assistant Secretary

Michelle A. Smith, Assistant Secretary

Mark E. Van Der Weide, General Counsel

Richard Ostrander, Deputy General Counsel

Trevor A. Reeve, Economist

Stacey Tevlin, Economist

Beth Anne Wilson,2 Economist

Shaghil Ahmed, Kartik B. Athreya, Brian M. Doyle, Eric M. Engen, Carlos Garriga, Joseph W. Gruber, and Egon Zakrajšek, Associate Economists

Roberto Perli, Manager, System Open Market Account

Julie Ann Remache, Deputy Manager, System Open Market Account

Jose Acosta, Senior System Engineer II, Division of Information Technology, Board

Isaiah C. Ahn, Information Management Analyst, Division of Monetary Affairs, Board

Mary L. Aiken, Senior Associate Director, Division of Supervision and Regulation, Board

Gianni Amisano, Assistant Director, Division of Research and Statistics, Board

Roc Armenter, Executive Vice President, Federal Reserve Bank of Philadelphia

David M. Arseneau, Deputy Associate Director, Division of Financial Stability, Board

Alyssa Arute,3 Assistant Director, Division of Reserve Bank Operations and Payment Systems, Board

William F. Bassett, Senior Associate Director, Division of Financial Stability, Board

Michele Cavallo, Special Adviser to the Board, Division of Board Members, Board

Andrew Cohen,4 Special Adviser to the Board, Division of Board Members, Board

Daniel M. Covitz, Deputy Director, Division of Research and Statistics, Board

Marnie Gillis DeBoer,3 Senior Associate Director, Division of Monetary Affairs, Board

Wendy E. Dunn, Adviser, Division of Research and Statistics, Board

Eric C. Engstrom, Associate Director, Division of Monetary Affairs, Board

Laura J. Feiveson,5 Special Adviser to the Board, Division of Board Members, Board

Andrew Figura, Associate Director, Division of Research and Statistics, Board

Glenn Follette, Associate Director, Division of Research and Statistics, Board

Etienne Gagnon, Senior Associate Director, Division of International Finance, Board

Jonathan Glicoes, Senior Financial Institution Policy Analyst II, Division of Monetary Affairs, Board

Valerie S. Hinojosa, Section Chief, Division of Monetary Affairs, Board

Jane E. Ihrig, Special Adviser to the Board, Division of Board Members, Board

Margaret M. Jacobson, Senior Economist, Division of Monetary Affairs, Board

Michael T. Kiley, Deputy Director, Division of Monetary Affairs, Board

Don H. Kim, Senior Adviser, Division of Monetary Affairs, Board

Elizabeth Klee, Deputy Director, Division of Monetary Affairs, Board

Anna R. Kovner, Executive Vice President, Federal Reserve Bank of Richmond

Spencer D. Krane, Senior Vice President, Federal Reserve Bank of Chicago

Sylvain Leduc, Executive Vice President and Director of Economic Research, Federal Reserve Bank of San Francisco

Andreas Lehnert, Director, Division of Financial Stability, Board

Kurt F. Lewis, Special Adviser to the Chair, Division of Board Members, Board

Logan T. Lewis, Section Chief, Division of International Finance, Board

Geng Li, Assistant Director, Division of Research and Statistics, Board

Laura Lipscomb, Special Adviser to the Board, Division of Board Members, Board

Benjamin W. McDonough, Deputy Secretary and Ombudsman, Office of the Secretary, Board

Neil Mehrotra, Assistant Vice President, Federal Reserve Bank of Minneapolis

Ann E. Misback,6 Secretary, Office of the Secretary, Board

David Na, Lead Financial Institution Policy Analyst, Division of Monetary Affairs, Board

Edward Nelson, Senior Adviser, Division of Monetary Affairs, Board

Anna Nordstrom, Head of Markets, Federal Reserve Bank of New York

Alyssa T. O'Connor, Special Adviser to the Board, Division of Board Members, Board

Ekaterina Peneva, Assistant Director and Chief, Division of Research and Statistics, Board

Caterina Petrucco-Littleton, Special Adviser to the Board, Division of Board Members, Board

Damjan Pfajfar, Vice President, Federal Reserve Bank of Cleveland

Eugenio P. Pinto, Special Adviser to the Board, Division of Board Members, Board

Jordan Pollinger,3 Associate Director, Federal Reserve Bank of New York

Fabiola Ravazzolo,3 Capital Markets Trading and Policy Advisor, Federal Reserve Bank of New York

Kirk Schwarzbach,7 Special Assistant to the Board, Division of Board Members, Board

Zeynep Senyuz, Special Adviser to the Board, Division of Board Members, Board

Thiago Teixeira Ferreira, Special Adviser to the Board, Division of Board Members, Board

Mary H. Tian, Group Manager, Division of Monetary Affairs, Board

Annette Vissing-Jørgensen, Senior Adviser, Division of Monetary Affairs, Board

Jeffrey D. Walker,3 Senior Associate Director, Division of Reserve Bank Operations and Payment Systems, Board

Jonathan Willis, Vice President, Federal Reserve Bank of Atlanta

Rebecca Zarutskie, Senior Vice President, Federal Reserve Bank of Dallas

_______________________

Joshua Gallin

Secretary

1. The Federal Open Market Committee is referenced as the "FOMC" and the "Committee" in these minutes; the Board of Governors of the Federal Reserve System is referenced as the "Board" in these minutes. Return to text

2. Attended Tuesday's session only. Return to text

3. Attended through the discussion of developments in financial markets and open market operations. Return to text

4. Attended the discussion of economic developments and the outlook. Return to text

5. Attended through the discussion of developments in financial markets and open market operations, and from the discussion of current monetary policy through the end of the meeting. Return to text

6. Attended the discussion of the review of the monetary policy framework. Return to text

7. Attended through the discussion of developments in financial markets and open market operations through the end of the meeting. Return to text

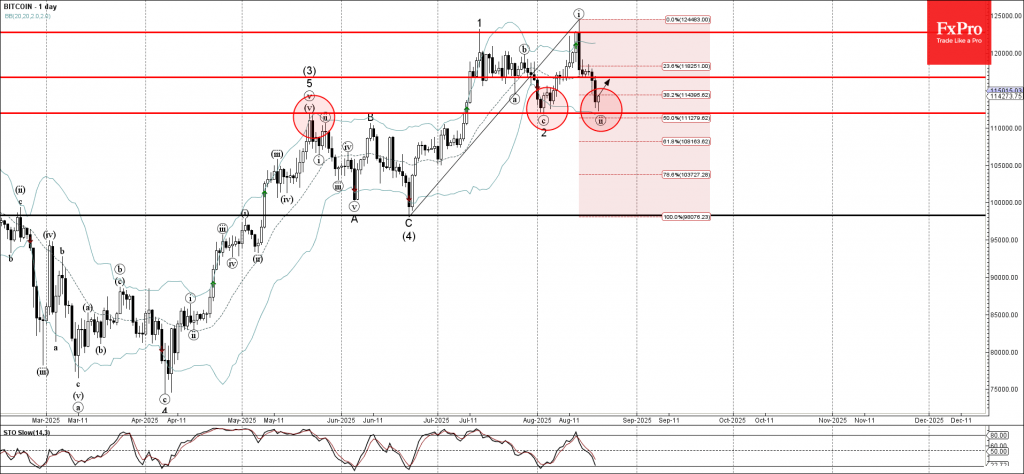

Bitcoin Wave Analysis

Bitcoin: ⬆️ Buy

- Bitcoin reversed from support zone

- Likely to rise to resistance level 116754.00

Bitcoin cryptocurrency recently reversed from the support area between the pivotal support level 111950.00 (former monthly high from May, which stopped earlier wave 2) and the lower daily Bollinger Band.

This support zone was further strengthened by the 50% Fibonacci correction of the previous upward impulse from June.

Given the clear daily uptrend, Bitcoin cryptocurrency can be expected to rise to the next resistance level 116754.00.

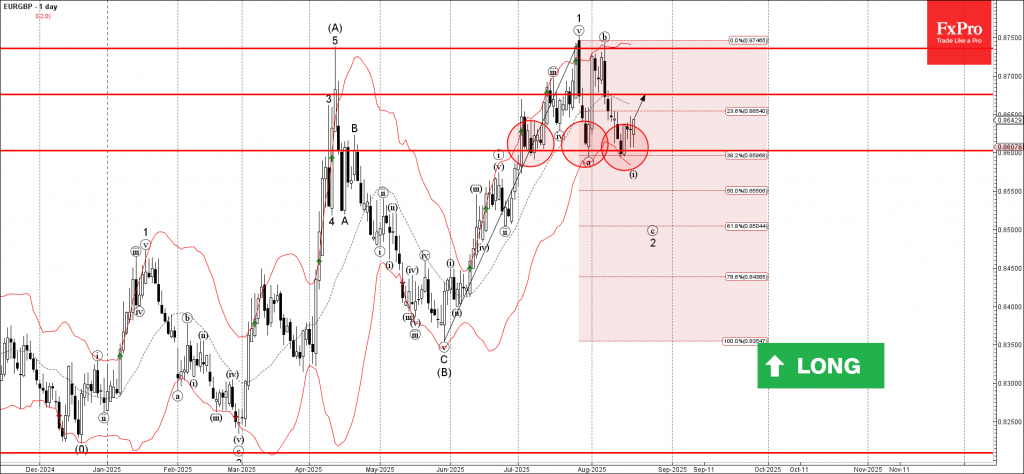

EURGBP Wave Analysis

EURGBP: ⬆️ Buy

- EURGBP reversed from support zone

- Likely to rise to resistance level 0.8675

EURGBP currency pair recently reversed up from the support zone between the pivotal support level 0.8600 (which has been reversing the price from the start of July) and the lower daily Bollinger Band.

This support zone was further strengthened by the 38.2% Fibonacci correction of the previous sharp upward impulse from May.

Given the clear daily uptrend and the bearish Sterling sentiment seen today, EURGBP currency pair can be expected to rise to the next resistance level 0.8675.

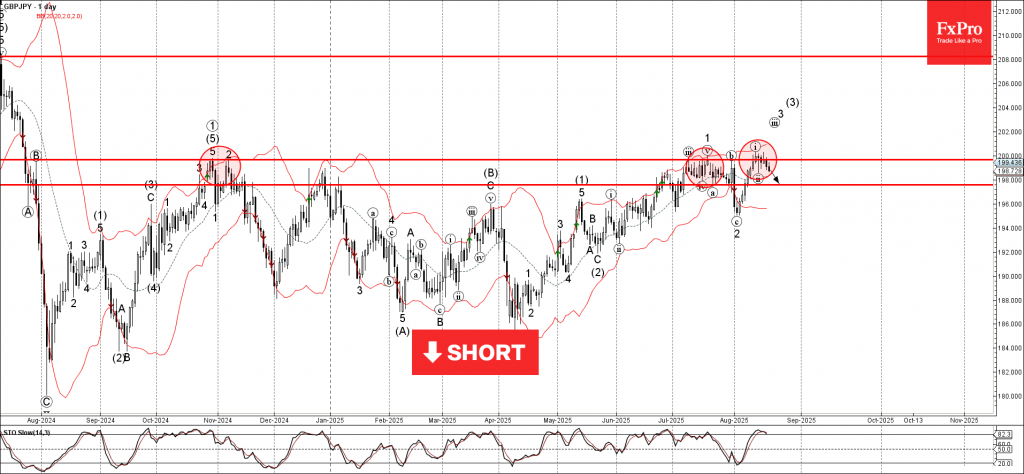

GBPJPY Wave Analysis

GBPJPY: ⬇️ Sell

- GBPJPY reversed from resistance zone

- Likely to fall to support level 198.00

GBPJPY currency pair recently reversed up from the resistance zone located between the long-term resistance level 200.00 (which has been reversing the price from October of 2024) and the upper daily Bollinger Band.

The downward reversal from this resistance zone stopped the earlier impulse wave iii of the intermediate wave (3) from the end of May.

Given the overbought daily Stochastic, GBPJPY currency pair can be expected to fall to the next support level 198.00.

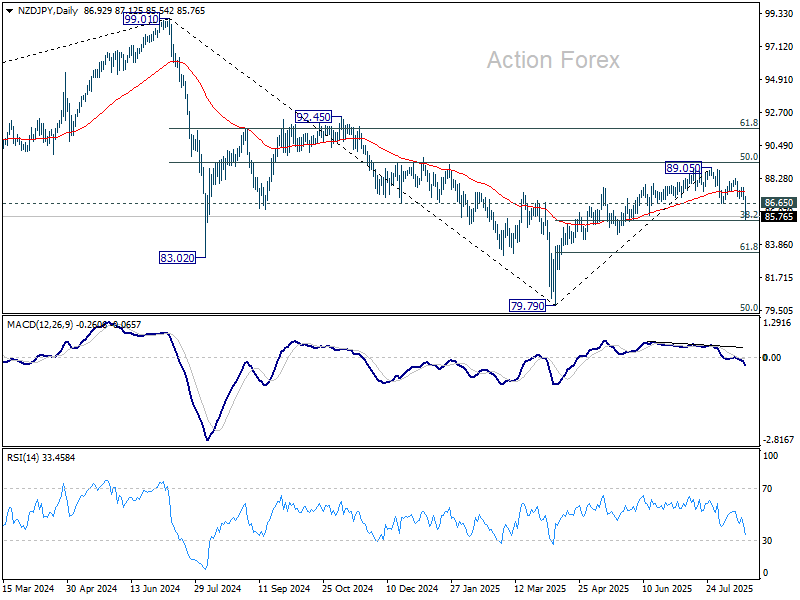

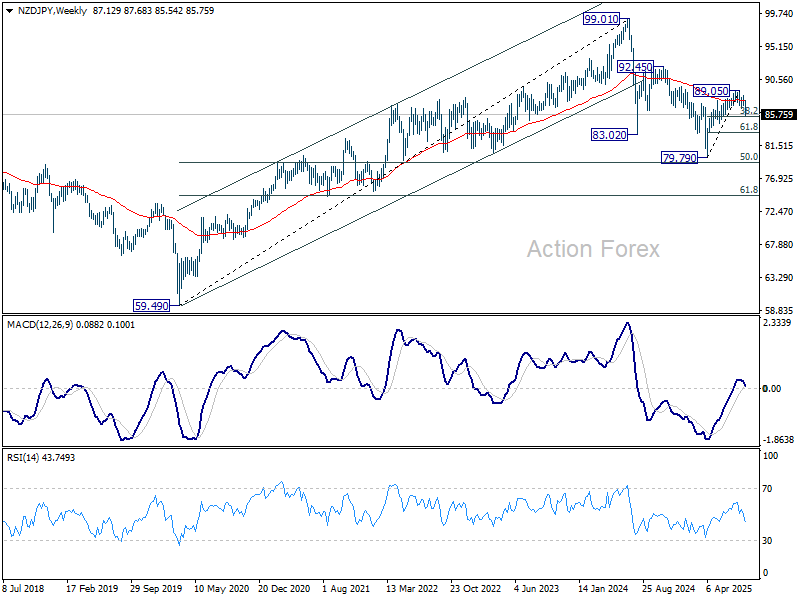

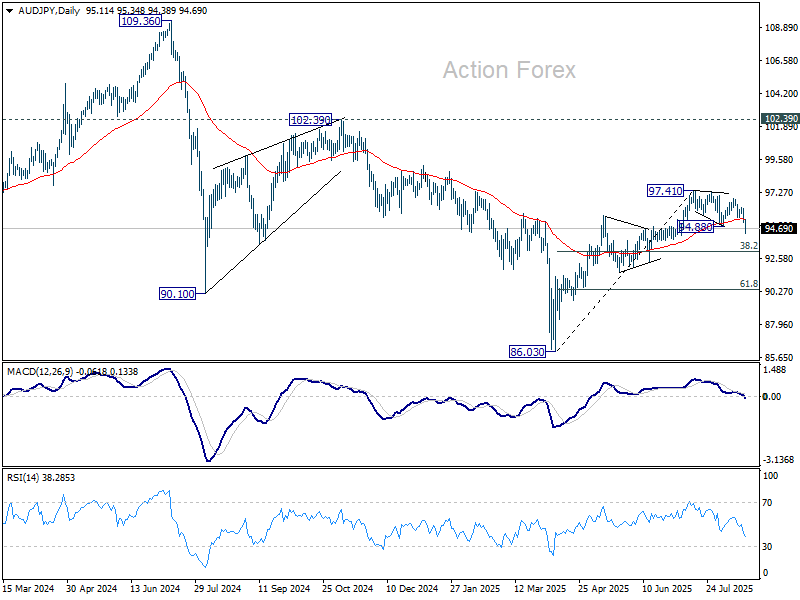

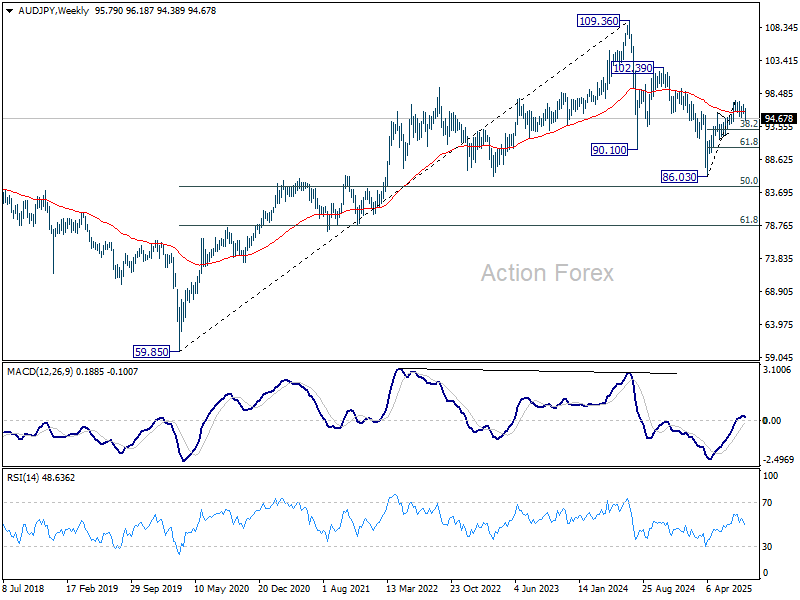

Yen surges as NASDAQ selloff deepens, NZD/JPY and AUD/JPY dive

Yen accelerated higher in US session as the selloff in NASDAQ intensified. Profit-taking in heavyweight technology and semiconductor names deepened concerns that valuations in the AI space may have run too far, too fast. The move fueled risk aversion and sparked a flight to traditional safe havens, leaving commodity currencies under heavy pressure.

Kiwi and Aussie bore the brunt of the market shift. For the New Zealand Dollar, the weakness was compounded by RBNZ’s dovish 25bps cut earlier in the day. Fresh projections showed policymakers still see scope for one more cut this year and another early in 2026, signaling a deeper easing cycle than markets had been positioned for.

Technically, NZD/JPY is now pressing an important support at 38.2% retracement of 79.79 to 89.05 at 85.51. Firm break there will pave the way to 61.8% retracement at 83.32. In case of recovery, outlook will stay bearish as long as 86.65 support turned resistance holds.

More importantly, rejection by 55 W EMA keeps the down trend from 99.01 (2024 high) intact. Further downside acceleration should at least bring another test on 79.79 low.

AUD/JPY's decline from 97.41 also resumed by breaking through 94.88 support. Further decline is now in favor back to 38.2% retracement of 86.03 to 97.41 at 93.06. Sustained break there will target 61.8% retracement at 90.37 next.

Just as in NZD/JPY, AUD/JPY's rejection by 55 W EMA keeps the down trend from 109.36 (2024 high) intact. Any downside acceleration would at least bring a retest on 86.03 low.

Kiwi (NZD) Drops from Dovish RBNZ Meeting, NZDUSD Technical Levels

Yesterday evening's Royal Bank of New Zealand Meeting delivered a much expected 25 bps cut.

Usually, a rate decision that is released as expected will then point participants towards the communication.

As explained in our pre-Rate decision analysis, there are different scenarios: a dovish or hawkish approach to again different possibilities of rate decisions (cut, pause, hike, 25 bps or more).

Yesterday's dovish 25 bps cut from the RBNZ caught markets by surprise: a lower longer-run inflation outlook and subsequent lower projected OCR (New Zealand's main interest rate) combined with some lower revised growth and employment outlooks sent the Kiwi dropping against all majors.

You can access another NZD strategy analysis published earlier on our website for NZDJPY.

Let's now look at the major Kiwi pair: NZDUSD.

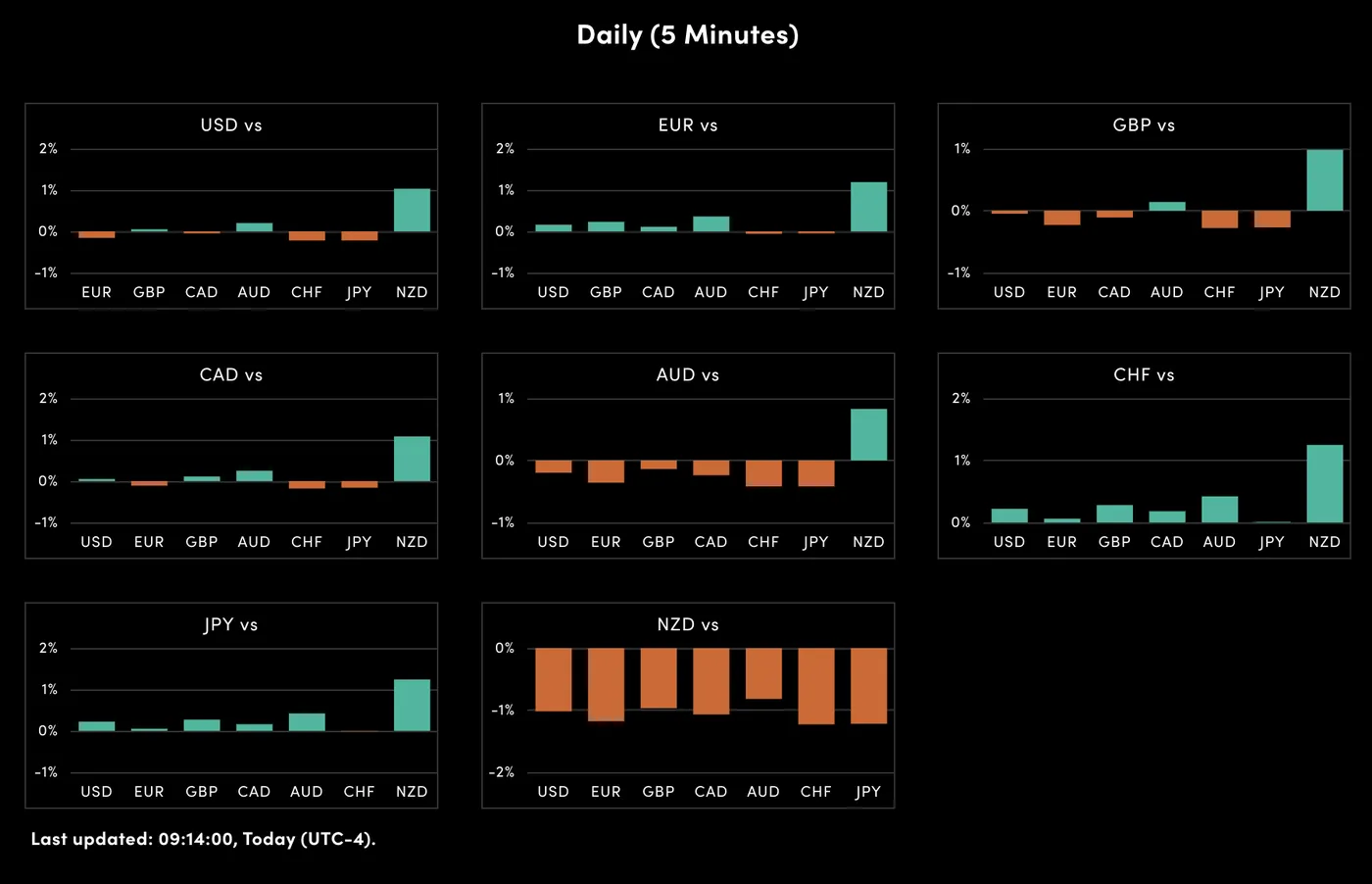

OANDA's Currency Strength tool, August 20, 2025 – Source: OANDA Labs (look at the NZD)

NZDUSD Multi-timeframe technical analysis

NZDUSD Daily Chart

NZDUSD Daily Chart, August 20, 2025 – Source: TradingView

The Kiwi was evolving in a consistent upward trend since the April Liberation Day troughs, but has since broken and retested the channel supporting it.

The current downtrend is forming a downward channel and the 1% down-move from yesterday's meeting is now stalling at the 0.58 support zone.

Look at the reactions as mean-reversion buyers are now stepping at the 200-Day Moving average (0.5830) and lower bound of the same downward channel, from oversold RSI levels – let's have a closer look to see if the current support will be enough to hold the downtrend.

Note that a failure to do so should trigger a prolonged selling trend.

NZDUSD 4H Chart

NZDUSD 4H Chart, August 20, 2025 – Source: TradingView

Multiple scenarios are possible here.

Effectively, despite momentum being in sellers' hands, multiple selling targets have been attained: The 4H RSI is also oversold, with a 4H Head and Shoulders pattern attaining its measured move target at a confluence with the lower bound of the downward channel.

In such bear channels with new fundamentals, mean-reversion isn't always a given: prices may consolidate sideways before attaining the other side, upper bound of the channel.

If buyers do step in around here, look at the mid-point of the channel located right at the 0.59 Pivot Zone.

Levels to look for NZDUSD trading:

Resistance Zones:

- 0.59 (+/- 150 pips) Main Pivot acting as Resistance

- 0.5950 Resistance Zone

- 0.60 Psychological level.

Support Zones:

- 0.58150 Daily lows

- 0.58 immediate Support Zone

- Next Main Support 0.57 to 0.5750

Safe Trades!

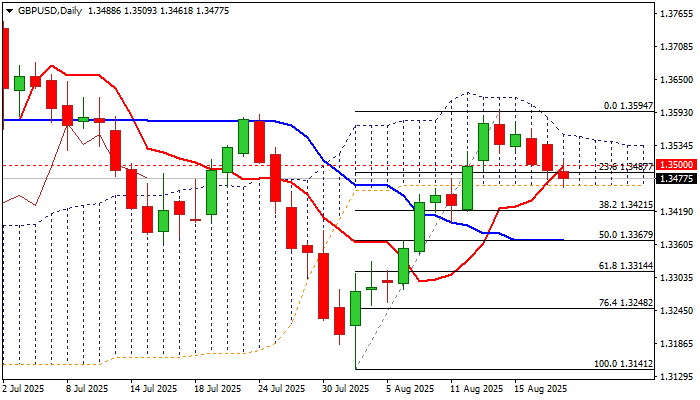

GBP/USD: Continues to Pressure Daily Cloud Base Following Limited Positive Impact

Cable edged higher on Wednesday after testing next key support provided by daily cloud base (1.3464), following break below psychological 1.3500 level (reinforced by daily Tenkan-sen) previous day.

Pound was lifted by disappointing UK July inflation data which further darkened outlook as Britain’s inflation is the highest and fastest growing among G7 economies.

In addition, economic growth remains weak that makes the position of UK policymakers more difficult, with bets about rate cut by the end of the year, fading after today’s data.

However, stronger than expected rise in consumer prices and weaker dollar, were unable to significantly lift pound, as traders remain very cautious about growing threats of stagflation (elevated inflation, weak economy, although the labor sector is still resilient) that may sour sentiment and limit gains.

Daily technical studies are still in predominantly positive configuration, with slight bullish bias expected to stay alive while the price holds above daily cloud base, though sustained break above 1.3500 level will be needed to boost initial positive signal and expose pivotal barrier at 1.3554 (daily cloud top).

Strong positive momentum and multiple MA bull-crosses continue to underpin the price, but risk of further weakness remains in play, due to weakening sentiment.

In the negative scenario on firm break of cloud base, the price would target 1.3421 (Fibo 38.2% of 1.3141/1.3594) and 1.3400 (100DMA) with 1.3367 (50% retracement) expected to come in focus on stronger acceleration.

Res: 1.3500; 1.3554; 1.3564; 1.3594.

Sup: 1.3464; 1.3421; 1.3400; 1.3367.

Sunset Market Commentary

Markets

The waiting game continues today in anticipation of PMI business surveys tomorrow and especially Fed Chair Powell’s speech in Jackson Hole on Friday. Core bonds are marginally better bid with daily changes on the US and EMU yield curve limited to -2 bps. Yesterday’s equity market rotation (out of US tech into European (laggards)) seems to continue with European names able to undo a red start to currently trade mixed. US stock markets start the day on the backfoot (up to -0.5% for Nasdaq). EUR/USD is going nowhere at 1.1660. Bridging the gap to next events/eco data, ECB president Lagarde gave some panel remarks at the International Business Council of the World Economic Forum in Geneva. She didn’t really touch on monetary policy though suggested that the implications of the EU-US trade deal will be factored into the ECB’s September macroeconomic projections which will help guide future decisions. Lagarde’s comments centered around the resilience of the global economy despite trade tensions and uncertainty. Frontloading (stockpiling goods ahead of anticipated tariffs) was name of the game in Q1, especially in export-heavy sectors like pharmaceuticals. Domestic factors such as strong private consumption, investment, and a stable labour markets supported EMU growth as well. However, the frontloading effect began reversing in Q2 as tariffs were implemented and is expected to weigh on growth in Q3 as well. The EU-US trade deal imposes average tariffs of 12%-16% on EU goods, below worst-case scenarios. Lagarde did warn for lingering uncertainty about sector-specific tariffs, particularly on pharmaceuticals and semiconductors. She lauded the EU’s strong position as top trading partner for 72 countries around the world and the extensive network of trade agreements, while emphasizing the importance of further diversification beyond the US.

UK July inflation rose by 0.1% M/M and 3.8% Y/Y (from 3.6% vs 3.7% expected) with core inflation (3.8% from 3.7%) and services inflation (5% from 4.7%) picking up faster as well. The move strengthens the hawkish rate cut signal by the BoE earlier this month, putting in doubt the likelihood of another rate cut this year. Sterling initially tried to gain on the prospect of longer interest rate support, but ran into a countermove. Failing to really test EUR/GBP support, the pair made a U-turn towards 0.8650. UK Gilts equally showed some kind of sell-the-rumour, buy-the-fact reaction. They outperform Bund and Treasuries with UK yields currently up to 5 bps lower across the curve.

News & Views

The Swedish Riksbank (RB) left its policy rate unchanged as expected at 2% today. In its monetary policy update the RB admits that inflation has been higher than expected during summer, with CPIF inflation in July at 3% and CPIF excluding energy printing 3.2% Y/Y. The higher outcome was mainly due to volatile factors such as foreign travel and car rentals. Other services and goods overall basically increased in line with the June RB forecast. The RB sees the summer inflation uptick as temporary as other indicators are not pointing to any lasting elevated inflationary pressures. At the same time, growth has been lower than expected. Amongst others, households are still cautious regarding spending in Q2. That said, the RB sees good conditions for a rebound in the Swedish economy later this year, but it will take time before the labour market improves from the currently elevated unemployment rate. Looking forward, the RB concludes that there is still some probability of a further interest rate cut this year, in line with the June forecast. The market reaction to the RB decision was limited. Money markets still see about a 50% chance of a rate cut next month. The krone briefly oscillated at the time of the RB decision but currently trades little changed near EUR/SEK 11.18.

Bloomberg reports that Karel Havlick, the Deputy Chairman of the Czech ANO opposition party led by former Prime Minster Andrej Bebis, indicated that the party intends to change the current policy of fiscal austerity if it returns to power after parliamentary elections scheduled to take place on October 3-4. According the Havlicek, the Czech Republic needs to move away from excessive focus on fiscal restraint to kickstart economic growth. He assesses that spending on infrastructure and welfare may lead to a “slightly” bigger deficit, but benefit the country and its finances in the longer term. The ANO party currently leads the SPOLU party of reigning prime minister Petr Fiala in the opinion polls.