Sample Category Title

Cautious Trade Ahead of Fed Powell; Dollar Retains Upper Hand

Dollar is holding broadly firm as markets head into the US session, though intraday momentum has slowed. Traders are reluctant to commit to new positions ahead of Fed Chair Jerome Powell’s highly anticipated Jackson Hole speech.

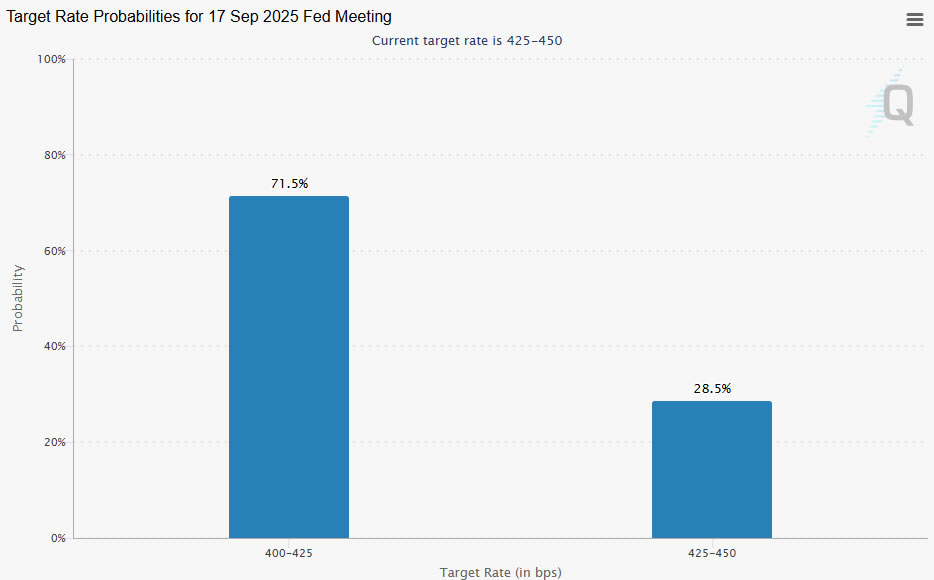

Expectations for a September rate cut have already been pared back sharply, with Fed fund futures now pricing around a 71% chance, down from over 90% just a week ago. Powell’s remarks will be closely scrutinized for any hint on whether he sees scope for a near-term move, or whether inflation risks still outweigh concerns about labor market cooling.

Market participants are also mindful that Powell’s tone will not be the only driver today. Comments from other Fed officials are expected to hit the wires, helping investors gauge the balance of views across the committee. By the end of the day, markets should have a clearer sense of the prevailing hawkish or dovish leanings inside the Fed.

Still, it must be stressed that today’s speeches are not the final word. Both the August nonfarm payrolls and CPI reports will be released before the next FOMC meeting, and those could easily shift expectations again. Market pricing will therefore remain highly data-dependent over the coming weeks.

For now, the Dollar sits as the strongest performer of the week, trailed by Swiss Franc and Loonie. Kiwi remains the weakest, followed by Aussie and Sterling, while Euro and Yen are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.08%. DAX is down -0.03%. CAC is up 0.11%. UK 10-year yield is up 0.007 at 4.74. Germany 10-year yield is down -0.013 at 2.746. Earlier in Asia, Nikkei rose 0.05%. Hong Kong HSI rose 0.93%. China Shanghai SSE rose 1.45%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield rose 0.008 to 1.619.

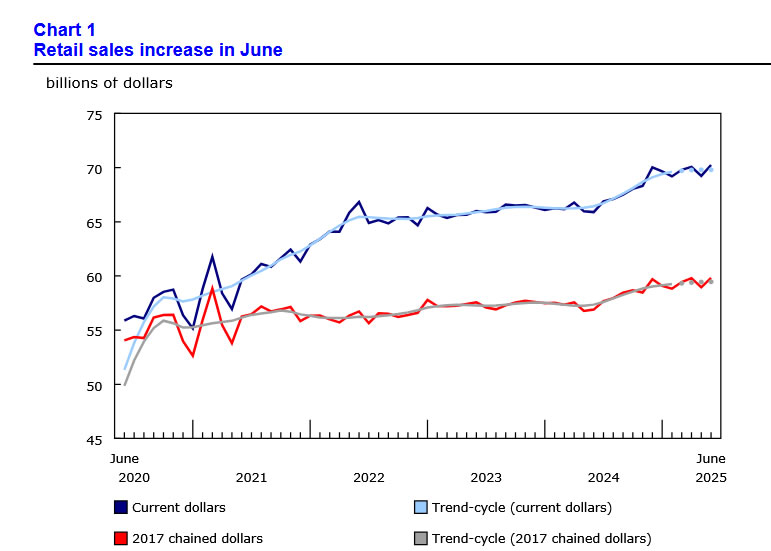

Canadian retail sales jump in 1.5% mom June, but July seen weakening

Canada’s retail sales climbed 1.5% mom to CAD 70.2B in June, though the gain fell just short of expectations of 1.6% mom. The increase was broad-based, with all nine subsectors contributing, led by food and beverage retailers.

Excluding autos, sales rose an even stronger 1.9% mom, more than doubling forecasts of 0.9% mom, suggesting underlying consumer spending remains resilient.

In volume terms, retail sales advanced 1.5% mom in June, reinforcing that the pick-up was not purely price-driven. On a quarterly basis, sales grew 0.4% qoq, with volumes up 0.7% qoq, pointing to a modest but positive contribution from consumption to Q2 GDP.

However, early signals from Statistics Canada suggest the momentum could be fading. The agency’s advance estimate shows sales likely slipped -0.8% in July mom, raising the risk that strong second-quarter consumption may not carry through into the third.

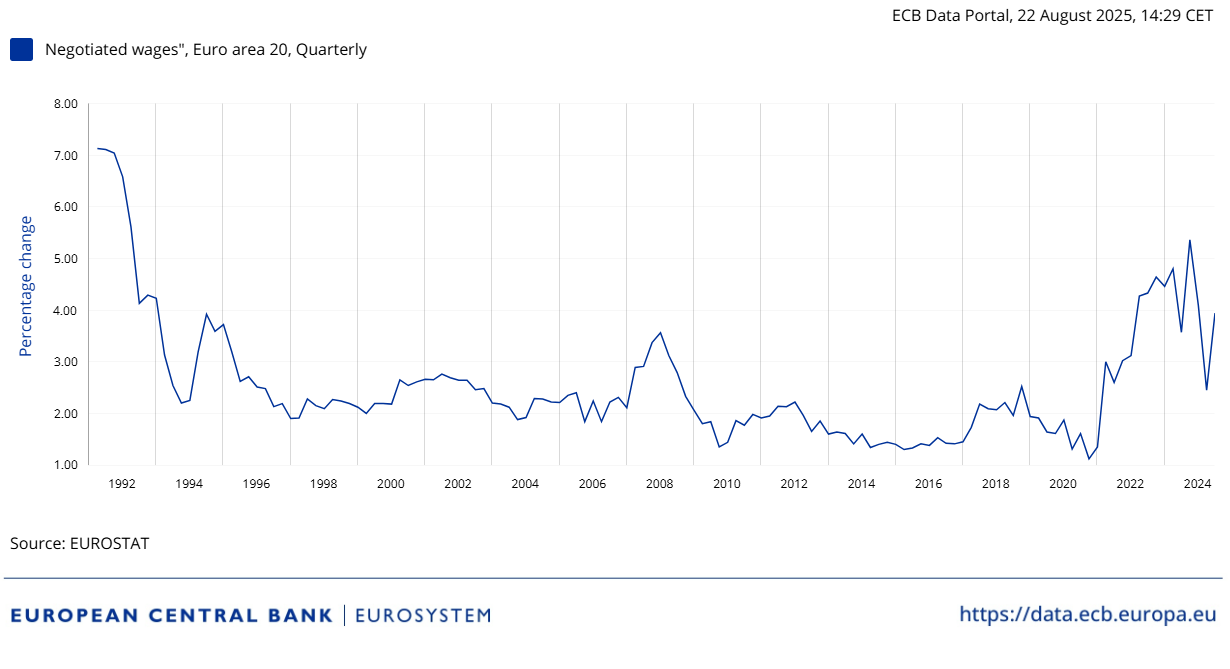

Eurozone wages growth jump to 3.95%, supports ECB pause

Eurozone negotiated wages accelerated to 3.95% in Q2, up sharply from 2.46% in Q1, the ECB reported on Friday. Though well below the 2024 peak of 5.4%, the acceleration suggests cost pressures remain sticky.

Some analysts noted that much of the gain reflected one-off payments, raising the possibility that the rise is short-lived. Still, with services inflation remaining elevated, policymakers have little scope to accelerate easing after already cutting the deposit rate to 2.00%.

Whether wage growth cools in the coming quarters will be central to determining if the ECB can continue on its path toward looser policy.

Japan core CPI slows to 3.1% as rice inflation cools, but underlying pressures persist

Japan’s inflation slowed again in July, with core CPI (ex-fresh food) easing to 3.1% yoy from 3.3% yoy, slightly above expectations of 3.0% yoy. Headline CPI also dipped to 3.1% yoy. The moderation was driven in part by cooling rice prices, which rose 90.7% yoy after surging 100.2% yoy in June, alongside the reintroduction of energy subsidies. Together, these helped bring core inflation down from May’s 3.7% peak.

However, price pressures remain entrenched. Food inflation excluding fresh items actually quickened to 8.3% yoy from 8.2% yoy. Core-core CPI (ex-food and energy) stayed unchanged, elevated at 3.4%. Energy prices provided some relief with a -0.3% yoy annual decline, the first drop since March 2024, but this was not enough to counter stubborn underlying strength.

For policymakers at BoJ, the data paints a mixed picture: rice and energy are finally easing their grip on consumer prices, but persistently high core inflation highlights why interest rate hikes remain on the table. While inflation is clearly off its May peak, the road back toward the 2% target looks slow and uneven.

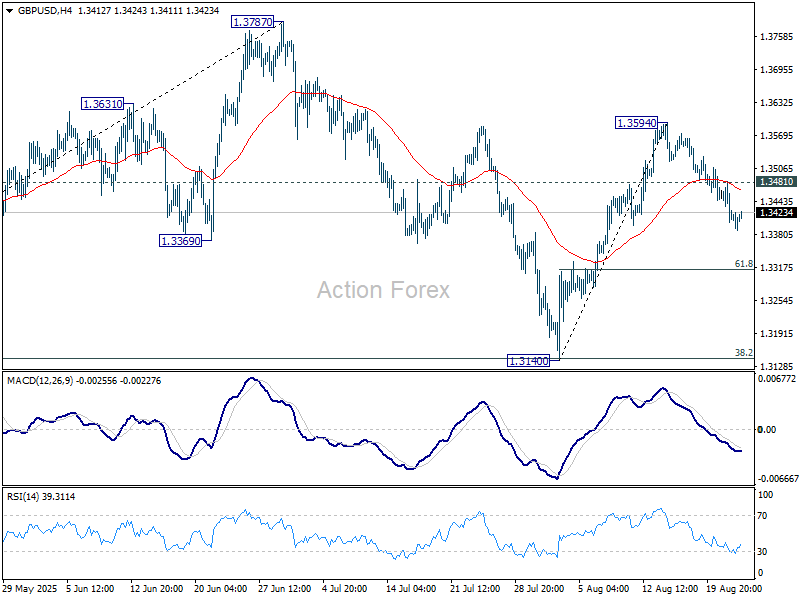

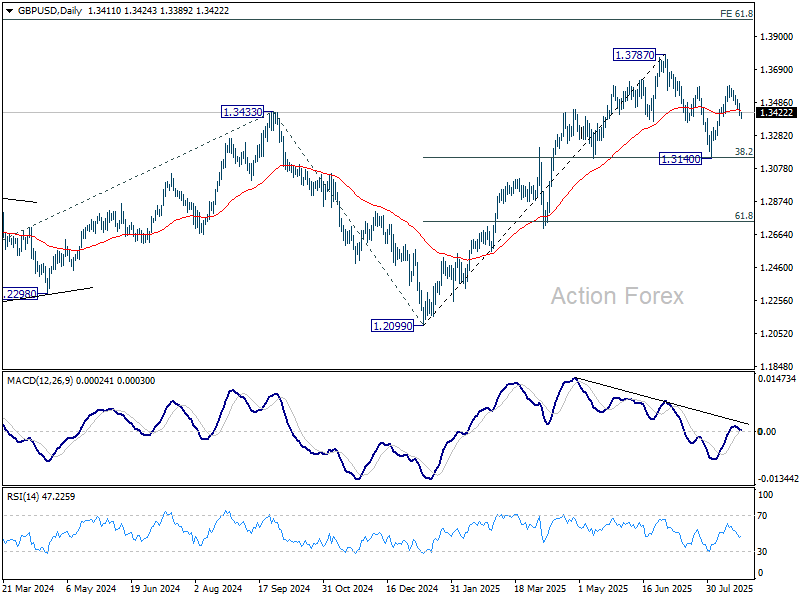

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3384; (P) 1.3434; (R1) 1.3462; More...

Intraday bias in GBP/USD remains mildly on the downside for the moment. Fall from 1.3594 is in progress for 61.8% retracement of 1.3140 to 1.3594 at 1.3313. Firm break there will bring retest of 1.3140 low. On the upside, above 1.3481 minor resistance will bring retest of 1.3594 first. Overall, corrective pattern from 1.3787 is extending.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3090) holds, even in case of deep pullback.

Canadian retail sales jump in 1.5% mom June, but July seen weakening

Canada’s retail sales climbed 1.5% mom to CAD 70.2B in June, though the gain fell just short of expectations of 1.6% mom. The increase was broad-based, with all nine subsectors contributing, led by food and beverage retailers.

Excluding autos, sales rose an even stronger 1.9% mom, more than doubling forecasts of 0.9% mom, suggesting underlying consumer spending remains resilient.

In volume terms, retail sales advanced 1.5% mom in June, reinforcing that the pick-up was not purely price-driven. On a quarterly basis, sales grew 0.4% qoq, with volumes up 0.7% qoq, pointing to a modest but positive contribution from consumption to Q2 GDP.

However, early signals from Statistics Canada suggest the momentum could be fading. The agency’s advance estimate shows sales likely slipped -0.8% in July mom, raising the risk that strong second-quarter consumption may not carry through into the third.

Eurozone wages growth jump to 3.95%, supports ECB pause

Eurozone negotiated wages accelerated to 3.95% in Q2, up sharply from 2.46% in Q1, the ECB reported on Friday. Though well below the 2024 peak of 5.4%, the acceleration suggests cost pressures remain sticky.

Some analysts noted that much of the gain reflected one-off payments, raising the possibility that the rise is short-lived. Still, with services inflation remaining elevated, policymakers have little scope to accelerate easing after already cutting the deposit rate to 2.00%.

Whether wage growth cools in the coming quarters will be central to determining if the ECB can continue on its path toward looser policy.

Canadian Dollar Eyes Retail Sales Report, Markets Await Powell Speech

The Canadian dollar is unchanged on Friday, trading at 1.3912. Earlier, USD/CAD hit 1.3917, its highest level since May.

Canada's retail sales expected to rebound

Canada wraps up the week with the June retail sales report, which is expected to rebound with a gain of 1.5% y/y. This follows a 1.1% decline in May, as consumers cut back on spending when US tariffs took effect in April.

The trade war between Canada and the US continues but consumers have had time to adjust to the new reality of tariffs and the markets expect a strong rebound in consumer spending.

It is somewhat surprising that the US has concluded trade agreements with the EU and Japan but not Canada, which is one of the largest trading partners of the US. Canada sends about 75% of its exports to its southern neighbor, so it cannot afford a prolonged trade war with the US. President Trump's sharp rhetoric about annexing Canada and turning it into the 51st state has touched a raw nerve with Canadians and had a major impact on the recent Canadian election.

All eyes on Jackson Hole

The heads of the major central banks have converged for a meeting at Jackson Hole, Wyoming. The star of the show will be Federal Reserve Chair Powell, who will deliver a speech later today. The markets have priced in a rate cut at next month's Fed meeting and are hoping for some confirmation from Powell.

The Fed must chart a rate path in challenging economic conditions. Inflation is still high, which would support maintaining rates, but the labor market is deteriorating, which supports the case to lower rates and boost economic activity.

What should be the Fed's priority? There is a split among members, as reflected in the rare split vote at the July meeting. The majority of the FOMC members, which voted to hold rates, judges the upside risk of inflation to be the primary concern, while the two members who voted to lower rates are most concerned by softening employment. The Fed meets next month and is widely expected to deliver its first rate cut since December 2024.

USD/CAD Technical

- USD/CAD is putting pressure on resistance at 1.3926, which has held since May. Above, there is resistance at 1.3941

- There is support at 1.3897 and 1.3882

USD/CAD 1-Day Chart, Aug. 25, 2025

GBP/USD: Friday Correction After Surge

On Friday, the GBP/USD pair declined to 1.3401 after strong gains earlier in the week. The previous rally was triggered by July business activity data, which showed the best performance in a year, mainly supported by the services sector.

The release came alongside fresh UK inflation statistics, which briefly lifted sterling. However, economists noted that the price acceleration was largely driven by airfare increases rather than broad-based inflationary pressure, meaning its effect on the Bank of England policy remains limited.

Money markets are currently pricing in less than a 50% chance of a rate cut before the end of 2025. The probability of a 25-basis-point cut this year stands at only 36%, while investors do not expect the next move in interest rates before spring 2026. Since the start of 2025, the pound has already gained almost 8% against the US dollar.

Technical analysis of GBP/USD

The market built a consolidation range around 1.3472 and broke it to the downside. A decline to 1.3350 is possible, followed by a correction bounce back to 1.3472. The downtrend may later extend to 1.3270. This outlook is supported by the MACD indicator, whose signal line remains below zero and is pointing sharply downwards, confirming bearish momentum.

On the H1 timeframe, the market nearly completed a corrective wave at 1.3594 before starting a new downward movement. A decline to 1.3350 is expected, after which a short-term pullback to 1.3472 is likely. The Stochastic oscillator confirms this view: its signal line is below 50, moving downwards towards 20, indicating further downside pressure.

Summary

After a strong rally, GBP/USD entered a corrective phase. Technical indicators suggest a bearish outlook with 1.3350 and 1.3270 as key downside targets, while 1.3472 may serve as a corrective rebound level.

Dollar Index (DXY) Rises Ahead of Fed Chair’s Speech

On Monday, we:

→ noted that the US Dollar Index (DXY) was consolidating at the start of a week packed with key events;

→ outlined a descending channel (shown in red);

→ highlighted that the price was trading around the channel’s median line, signalling a balanced market;

→ suggested that a test of one of the quarter lines (QL or QH), which divide the channel into four parts, could take place.

As the DXY chart indicates, since then the balance has shifted in favour of buyers, with the price forming an upward trajectory (shown in purple lines) and breaking through short-term resistance R (which has now turned into support, as marked by the blue arrow). Support line S remains relevant.

Today brings the key event that may have the greatest impact on the US Dollar Index (DXY) this week – Jerome Powell’s speech at the annual Jackson Hole Symposium.

This appearance is particularly significant because:

→ it is likely to be Powell’s last speech after seven years as Fed Chair, with his term expiring in May amid ongoing tensions with President Trump;

→ market participants will closely monitor the tone of his remarks, as a rate cut is expected in September, while recent economic data – namely the rise in the Producer Price Index – suggest that the US economy could face renewed inflationary pressures due to Trump’s tariffs.

Technical analysis of the DXY chart

From a bullish perspective, in the short term the US dollar is advancing within the purple channel, supported by:

→ the lower boundary of this channel;

→ the demand imbalance zone in favour of buyers (shown in green), confirmed by yesterday’s sharp bullish candle.

From a bearish perspective:

→ the RSI has entered overbought territory;

→ bullish momentum may fade after a breakout above the QH line;

→ a key resistance at the 99 level lies nearby – a level that reclaimed its role as resistance at the beginning of August (indicated by black arrows).

A corrective pullback in the US Dollar Index (DXY) could happen after its rally to the highest level since 6 August. However, the further trajectory will largely depend on Powell’s words this evening. According to Forex Factory, the speech is scheduled for 17:00 GMT+3.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Nikkei 225 Technical: A Potential Bullish Reversal Looms After 4% Decline as Market Breadth Improves With Earnings Upgrade

The Japan 225 CFD Index (a proxy of the Nikkei 225 futures) rallied as expected and hit the first resistance level of 43,560 as mentioned in our previous report. It printed a fresh intraday record high of 43,943 on Monday, 18 August.

Thereafter, it staged a decline of -4% to record an intraday low of 42,330 on Friday, 22 August, before it recovered to an intraday level of 42,570 at the time of writing.

Several technical elements and a fundamental factor suggest that the ongoing 5-day decline is likely a minor corrective decline within its medium-term uptrend phase rather than the start of a medium-term bearish trend.

Fig. 1: Japan 225 CFD Index minor trend as of 22 Aug 2025 (Source: TradingView)

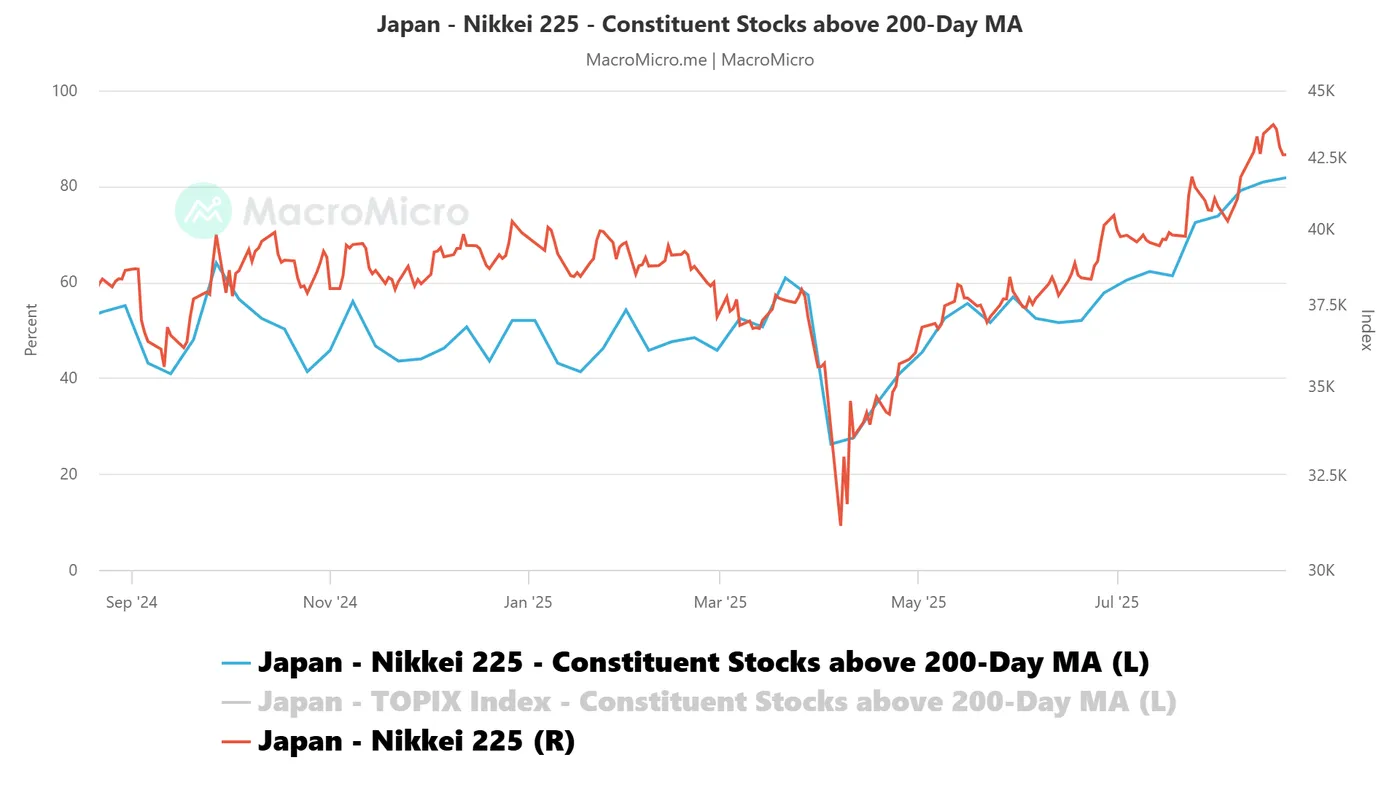

Fig. 2: Nikkei 225 component stocks above 200-day as of 22 Aug 2025 (Source: MacroMicro)

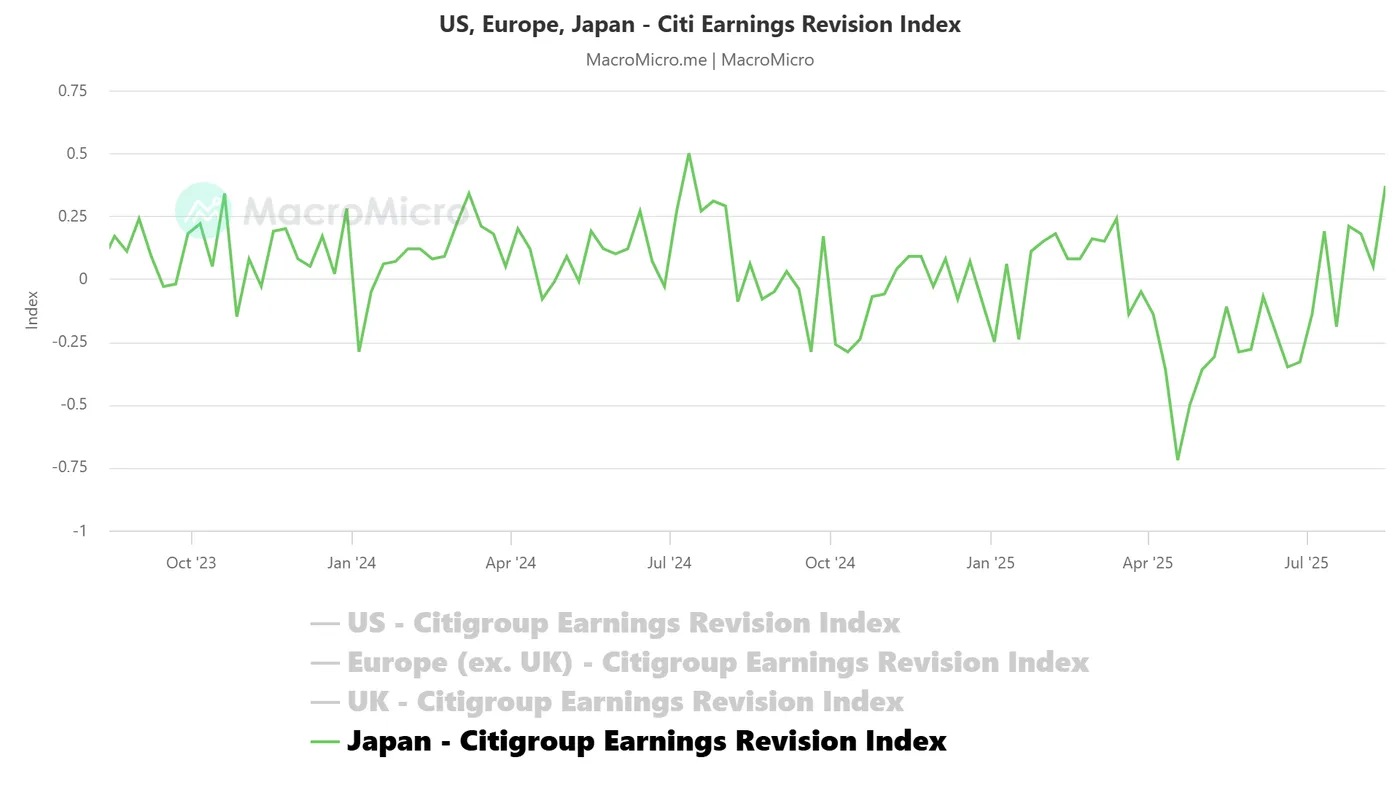

Fig. 3: Japan Citigroup Earnings Revision Index as of 15 Aug 2025 (Source: MacroMicro)

Preferred trend bias (1-3 days)

Maintain a bullish bias with short-term pivotal support at 42,000/41,760 for the Japan 225 CFD Index, and a clearance above 43,060 sees the next intermediate resistances coming at 43,470 and 44,050/44,110 (Fibonacci extension cluster levels) (see Fig. 1).

Key elements

- The 42,000/41,760 key support zone is likely an inflection point, a potential bullish reversal as it confluences with the 20-day moving average and 50% Fibonacci retracement of the prior minor up move from 1 August 2025 low to 18 August 2025 high.

- The hourly RSI momentum indicator has traced out a bullish divergence condition after it dropped towards its oversold region on Wednesday, 20 August. These observations suggest bearish momentum of the ongoing 5-day decline has started to ease.

- Market breadth has continued to improve; the percentage of the Nikkei 225 component stocks trading above their respective key 200-day moving averages has increased steadily since 1 August’s print of 74% to 82% as of Friday, August (see Fig. 2).

- Analysts, on average, have continued to upgrade their earnings outlook on Japanese corporations. The Citigroup Earnings Revision Index has been on a path of a steady uptrend since 18 April 2025’s 5-year low of -0.72; it has jumped to 0.37 as of 15 August 2025 from -0.19 printed on 18 July 2025 (see Fig. 3).

Alternative trend bias (1 to 3 days)

A break below the 41,760 key support invalidates the bullish recovery to see an extension of the corrective decline to expose the 41,275/41,070 medium-term support zone.

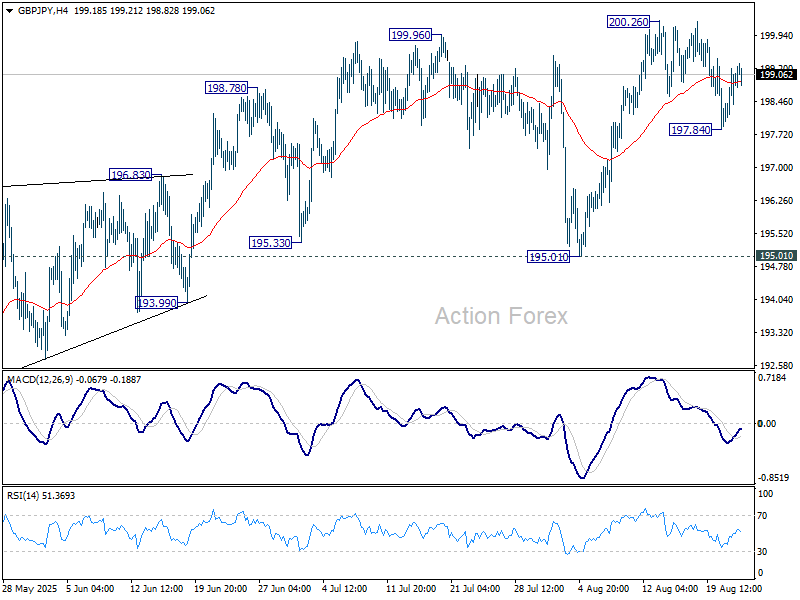

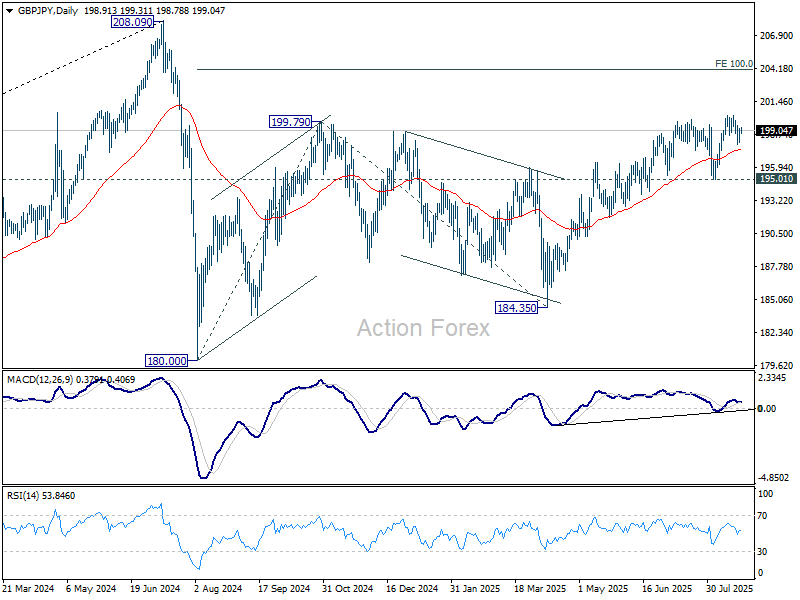

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.31; (P) 198.77; (R1) 199.45; More...

GBP/JPY recovered after brief dip to 197.84 and intraday bias is turned neutral first. More consolidations could be seen and below 197.84 will bring deeper pullback. But overall, near term outlook will stay bullish as long as 195.01 support holds. On the upside, firm break of 200.26 will resume the whole rise from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

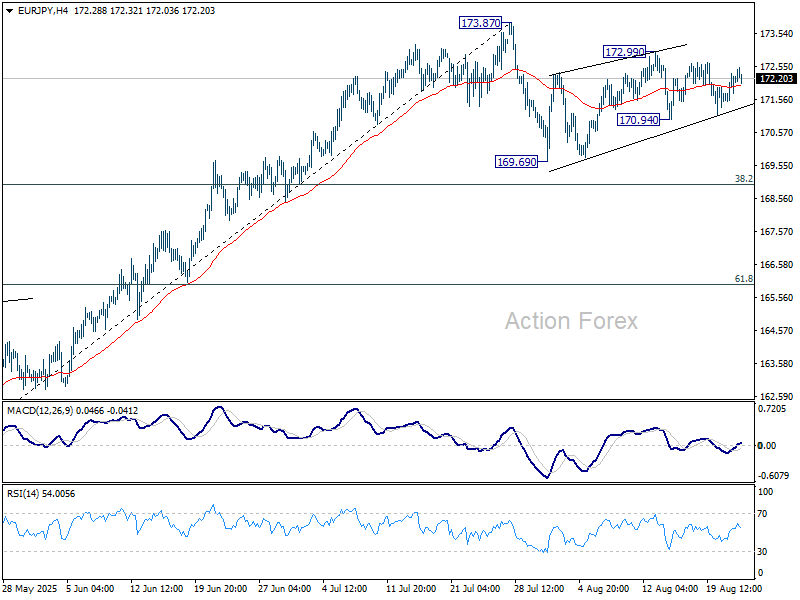

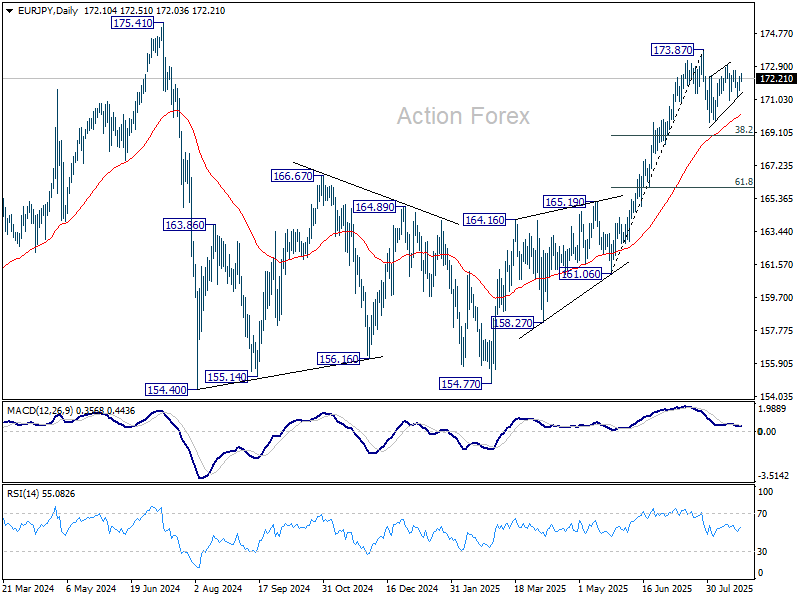

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.70; (P) 172.03; (R1) 172.54; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the upside, above 172.99 will resume the rebound from 169.69 to retest 173.87 high. On the downside, however, firm break of 170.94 will suggest that the corrective pattern from 173.87 has started the third leg. Intraday bias will be turned back to the downside for 169.69 support, and possibly below. But downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to bring rebound.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.95) will delay this bullish case.

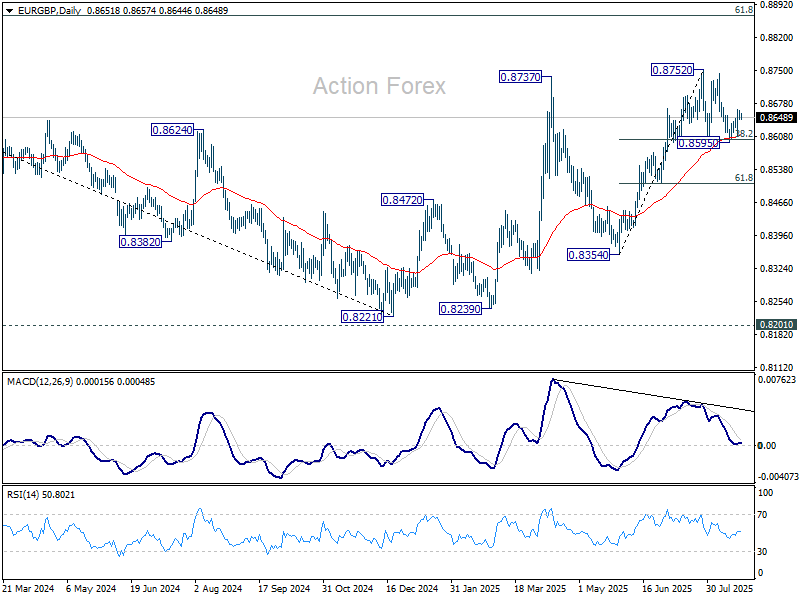

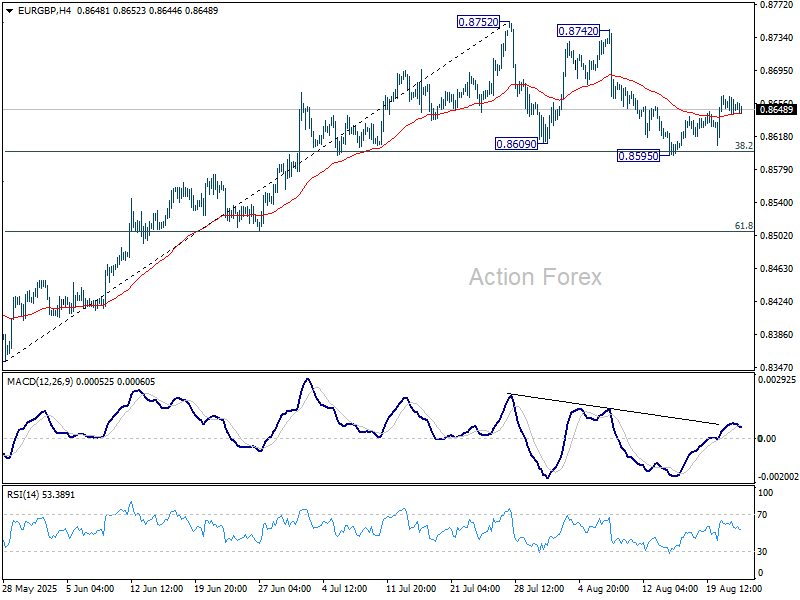

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8644; (P) 0.8656; (R1) 0.8665; More...

Intraday bias in EUR/GBP remains mildly on the upside for the moment. Corrective pattern from 0.8752 should have completed at 0.8595 after hitting 38.2% retracement of 0.8354 to 0.8752 at 0.8600. Further rise should be seen to retest 0.8752. Firm break there will resume larger rebound from 0.8221. For now, risk will stay on the upside as long as 0.8595 support holds, in case of retreat.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8501) holds.