Sample Category Title

Weekly Focus – European Industry Grows for the First Time in Three Years

This week's main data highlights were the PMI reports for August. In the euro area, the report showed the manufacturing sector recording growth for the first time since June 2022. The manufacturing PMI crossed the 50-mark in a larger-than-expected rise to 50.5 from 49.8, defying expectations of a decline to 49.5. The rise was due to both France and Germany. At the same time, services PMI declined to 50.7 from 51.0, which was as expected. The positive string of growth surprises thus continues in the euro area, which supports our call that the ECB is done cutting interest rates. We also received data on wage growth for the second quarter of 2025. The indicator of negotiated wages rose to 4.0% y/y in Q2 from 2.5% y/y in Q1, which was heavily affected by base effects, but nevertheless a bit high. Overall, wage growth is trending lower compared to last year.

In the US the PMIs also for August exceeded expectations, with manufacturing rising to 53.3 (consensus: 49.7) from 49.8, while services declined slightly to 55.4 (consensus: 54.2) from 55.7. The manufacturing increase was driven by higher new orders, employment, and output indices, with the output index reaching its highest level in over three years - indicating very strong details overall. However, given the volatility in PMIs since April, caution is warranted in interpreting single-month movements. That said, the August PMI report stands out as more positive compared to the recent downward trends in ISM and weak payroll data.

The UK PMI data came in stronger than expected like in the US and euro area, with the composite index rising to 53.0 from 51.5, driven by a much stronger-than-anticipated performance in the service sector. The August PMIs add to a series of hawkish data, adding to the case for the Bank of England (BoE) to hold rates unchanged in November, though there is plenty of significant incoming data before the November meeting and we continue to expect a cut. July inflation was also to the hawkish side, which surprised to the topside across the board, but the details suggests that it was driven by the volatile air fares component alleviating some concern for the BoE. Headline CPI came in at 3.8% (cons: 3.7%), core at 3.8% (cons: 3.7%) and services at 5.0% (cons: 4.8).

In China, a batch of data for July showed weakness in the economy across the board, which adds to the loss of momentum seen in recent months. Both consumption and housing moved another notch lower, and investments weakened as well. The only bright spot currently is strong exports, but it is paramount for the economy that domestic demand gets on a stronger footing. It is also a high priority for China's leaders, and we expect to see new stimulus soon targeting consumption and housing. See more in China Flash - Further weakening of economy calls for new stimulus, 15 August.

Next week will be light in terms of economic data. The main highlight is the flash August inflation data from Germany, France, Italy, and Spain, which is released ahead of the euro area aggregate. We expect euro area HICP inflation to increase to 2.1% y/y in August from 2.0% y/y in July driven by an increase in energy inflation while core inflation is expected to remain unchanged at 2.3% y/y. In Japan, we receive a batch of data on Friday covering retail sales, unemployment, and Tokyo CPI inflation. US PCE inflation is also due Friday.

Sunset Market Commentary

Markets

Fed chair Powell’s long-awaited speech in Jackson Hole highlights that the balance of risks between the Fed’s price stability and maximum employment goals appears to be shifting. With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting the Fed’s policy stance. The Fed is puzzled by the current balance on the labour market which results from a marked slowing in both the supply and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.That’s a strong hint that the Fed is ready to pivot towards to a 25 bps rate cut at the September FOMC meeting. Markets have to repositioning again as latest PPI and PMI numbers argued in favour of a longer hold. The US yield curve bull steepens with yields dropping 8.5 bps (2-yr) to 3.7 bps (30-yr) in a first reaction. Loss of USD interest rate support propels EUR/USD from 1.16 to 1.1670. US equity markets rally up to 1.5%.

Looking forward to next week, European trading will be thin on Monday with UK markets closed for Summer Bank holiday. The Belgian debt agency nevertheless auctions three OLO lines (OLO 97 3% Jun2033, OLO 100 2.85% Oct2034 and OLO 101 3.5% Jun2055). So far, the debt agency raised €35.15bn via syndications and auctions compared to a €47bn OLO funding need. German Ifo Business sentiment will be published as well, but the outcome is normally in line with this week’s PMI release. The German composite PMI improved marginally (50.9 from 50.6) on the back of an improvement in the manufacturing sector (49.9 from 49.1). US eco data are plenty, but second tier, on Tuesday with July durable goods orders, Richmond Fed manufacturing index, consumer confidence and housing prices. Especially the latter two will be watched though could give conflicting signal (for the Fed). One might point in the direction of rising inflation expectations, the other to a further cooling of the US housing market. The US Treasury starts its mid-month refinancing operation the same day with a $69bn 2-yr Note auction. $70bn 5-yr Note and $44bn 7-yr Note sales follow on Wednesday and on Thursday. These shorter tenors draw less market attention than the longer (end-of-month) sales of 10-yr and 30-yr Notes/Bonds. Wednesday risks being uneventful in absence of eco data with Minutes of the July ECB decision the highlight on Thursday. Bloomberg today runs an article that the ECB is increasingly convinced that they can keep interest rates unchanged in September with growth and inflation developing largely in line with June projections. An “insurance” rate cut to cover the downside of the risk balance risks backfiring if associated with speculation about deteriorating prospects and is therefore off the table. Q2 EMU negotiated wage data today also showed an uncomfortable acceleration from 2.5% Y/Y to 4% Y/Y, pointing at sticky services inflation. EMU money markets keep repositioning away from a more dovish ECB scenario, with the probability of another 25 bps before year-end currently only at 36%. Inflation is the focal point on Friday with Germany, France, Spain and Italy reporting August CPI numbers, the ECB publishing its consumer inflation expectations and July US PCE deflators due. The Fed’s preferred inflation measure risks showing stronger inflationary dynamics than the July CPI number given certain components from the July producer prices report (+0.9% M/M; highest since March2022) feeding into PCE (eg 1% M/M increase in Airline passenger services or 5.8% M/M higher portfolio management costs).

News & Views

The German IFO institute today already published its survey on residential construction. Sentiment improved significantly in July (-25.8 to -23.5) as companies turned less skeptical, especially about the future. Their assessment of the current situation also brightened slightly. Head of Ifo Surveys Wohlrabe said that residential construction companies are cautiously hopeful, but that there is still a high level of dissatisfaction in the sector. However, with the share of companies lacking orders at the lowest since August 2022 (still 46.1%) and the cancelation rate easing further, IFO assesses that residential construction is heading in the right direction though it needs more than just political announcements. A sustained improvement is also conditional on how financing costs develop.

Powell’s subtle Jackson Hole signal: Risk balance my warrant Fed shift; Dollar sinks

Dollar fell sharply after Fed Chair Jerome Powell hinted that the case for rate cuts may soon strengthen. Speaking at Jackson Hole, Powell highlighted Fed’s growing policy trade-off: inflation risks remain tilted upward while downside risks to employment are building. He stressed that the Fed’s framework requires carefully balancing these competing pressures.

Powell observed that policy is already significantly closer to neutral compared to a year ago, with unemployment and other labor measures steady enough to permit a cautious approach.

Importantly, Powell said that with monetary policy already in restrictive territory, the evolving balance of risks “may warrant adjusting our policy stance.” Markets took this as a subtle hint that easing could be on the horizon, accelerating Dollar losses across the board.

Full speech of Fed's Powell here.

Fed’s Collins stresses balance between inflation and jobs

Boston Fed President Susan Collins said on Bloomberg TV that while U.S. growth has shown signs of slowing, the "overall economic fundamentals are relatively solid." She argued policymakers cannot wait until all uncertainty clears before acting and must carefully weigh the Fed’s dual mandate.

She emphasized policymakers "cannot wait until all of the uncertainty is behind us," and must instead weigh both sides of the Fed’s mandate.

"If we start to see worsening labor market risks relative to inflation, starting to dial back the restrictiveness would become appropriate," she said.

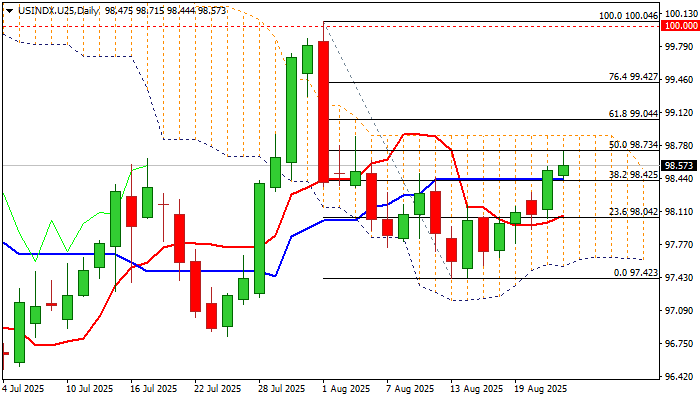

Dollar Index Keeps Firm Tone Ahead of Powell’s Speech

The dollar index stood at the front foot and hit three-week high on Friday morning, as improved sentiment on Fed policy outlook continued to boost dollar in past few days.

Initial signals that the central bank may opt for more aggressive policy easing after disappointing July labor data, along with strong downward revisions of June and May numbers, were overshadowed by the latest inflation data which pointed to increased inflationary risk and tempered expectations for rate cuts, with significant drop in bets for widely expected September rate cut, contributing to more cautious approach.

All eyes are on today’s speech of Fed Chair Powell in Jackson Hole symposium, with expectations to get more information about Fed’s action in coming months.

Powell is very likely to put priority on inflationary risk against threats from weakening labor market, which would result in more hawkish stance, however, he may not come with many details as there will be release of another labor report before Fed’s September meeting, suggesting that Powell will be very cautious with his comments in Jackson Hole.

This may result in repeating his standard mantra that the central bank remains on track for policy easing, but any decision will be dependent on the latest economic data.

The dollar is so far on track for strong weekly gain which has retraced the biggest part of losses in past two weeks and about to complete weekly bullish engulfing pattern that would add to developing bullish signals.

Technical picture on daily chart has improved, but bulls started to face headwinds from cracked resistance at $98.73 (50% retracement of $100.04/$97.42 bear-leg, reinforced by falling 100DMA) and nearby daily cloud top ($98.88).

Bullish scenario requires break of $98.73/88 barriers that will signal continuation and expose targets at $99.42 (Fibo 76.4%) and $100 psychological / Aug 1 peak).

Broken Fibo 38.2% ($98.42) reinforced by daily Kijun-sen, marks solid support which should ideally hold and keep bulls intact.

Break here and dip through daily Tenkan-sen ($98.07) will be bearish.

Res: 98.73; 98.88; 99.04; 99.42

Sup: 98.42; 98.30; 98.07; 97.61

Canada: Retail Sales Rebound in June, But Lose Steam in July

Retail sales rose 1.5% month-on-month (m/m) in June, just a tad lower than Statistics Canada's 1.6% advanced estimate.

After adjusting for inflation, the volume of retail sales increased 1.5% m/m.

Unlike in previous months, auto sales were not a major swing factor, with sales edging up just 0.2% m/m after a 1.8% decline in May.

Receipts at gas stations and fuel vendors rose 1.8%, following three consecutive declines. In volumes terms, sales grew an even stronger 2.7% m/m, as lower fuel prices weighed on the nominal gain.

Core sales – excluding auto sales and receipts at gas stations – were solid, rising 1.9% m/m in June. Food and beverage stores led the way (+1.2% m/m) with broad-based gains across most categories. Notably, sales at clothing and clothing accessories stores surged 5.1% m/m, while sales at general merchandise stores climbed 1.8% m/m.

The lone laggard category was furniture and home furnishings stores, which slipped 0.8% m/m.

E-commerce sales declined by 1.7% m/m in June.

Statistics Canada's advanced estimate points suggests that sales pulled back in July, falling 0.8% m/m.

Responses to the supplementary questions showed that 27% of retailers reported being affected by trade tensions, down from 32% in May.

Key Implications

Retail sales matched expectations at the headline level but surprised to the upside in core categories. This indicates that auto-driven gains seen in the spring now lost momentum. On a quarterly basis, real retail sales posted a respectable 3.1% annualized gain with June's strength leaving core sales as the main driver of the topline tally.

Consumer spending held up better than we previously expected and we now see real spending tracking 1.2% in the second quarter (quarter-on-quarter, annualized). However, as the advance estimate indicates, momentum is likely to cool in Q3. With employment growth slowing and trade tensions clouding the outlook, there is little for the average Canadian household to get excited about.

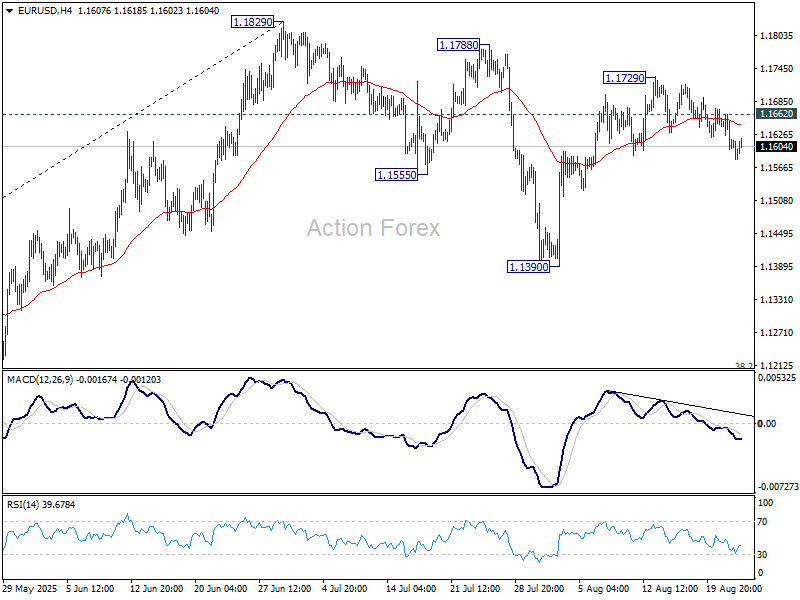

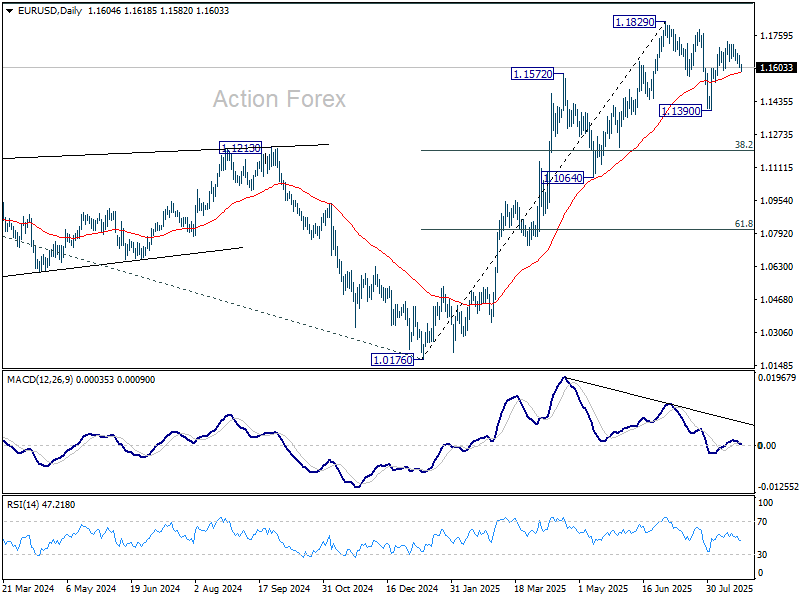

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1584; (P) 1.1623; (R1) 1.1646; More...

Intraday bias in EUR/USD remains mildly on the downside as fall from 1.1729 is in progress. Deeper decline would be seen towards 1.1390 support as corrective pattern from 1.1829 extends. On the upside, above 1.1662 minor resistance will turn intraday bias neutral again.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

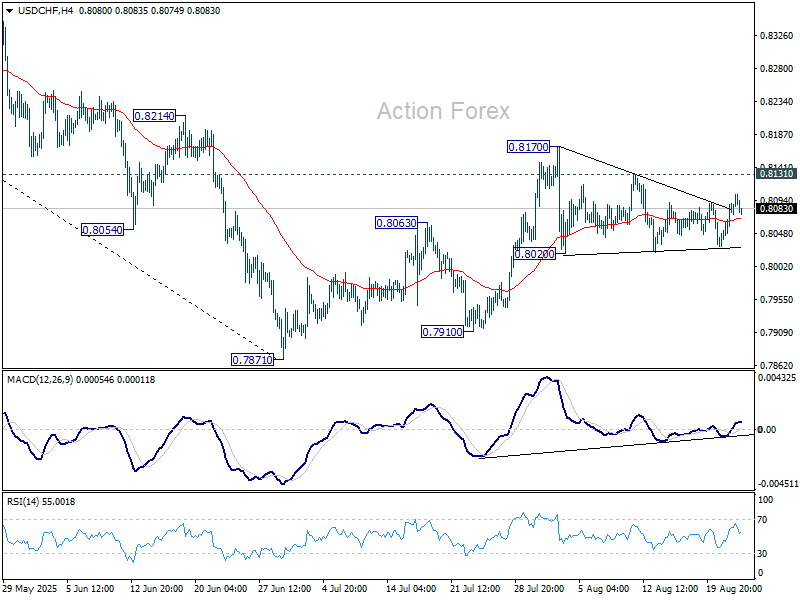

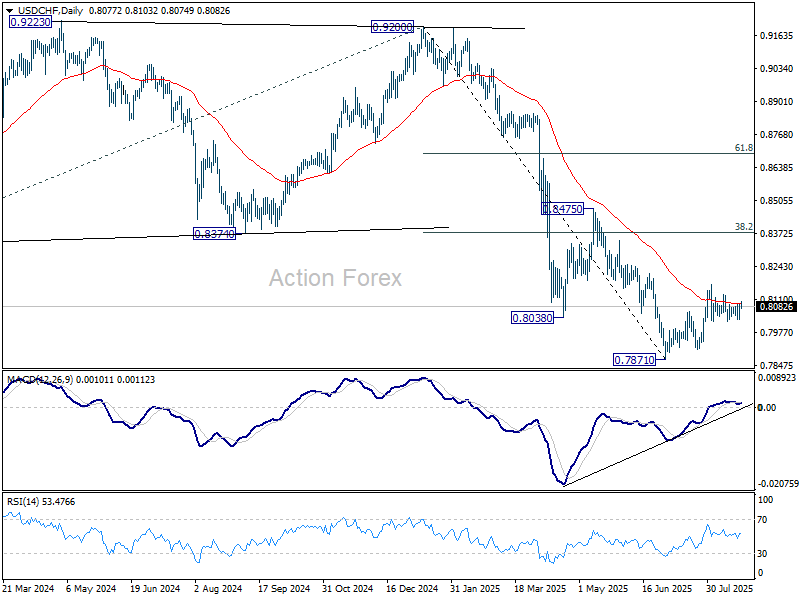

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8050; (P) 0.8071; (R1) 0.8109; More….

Intraday bias in USD/CHF remains neutral for the moment. On the upside, firm break of 0.8131 resistance will argue that consolidation from 0.8170 has already completed. Bias will be back on the upside. Further break of 0.8170 will resume the rise from 0.7871 towards 38.2% retracement of 0.9200 to 0.7871 at 0.8379. On the downside, break of 0.8020 support will bring retest of 0.7871 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

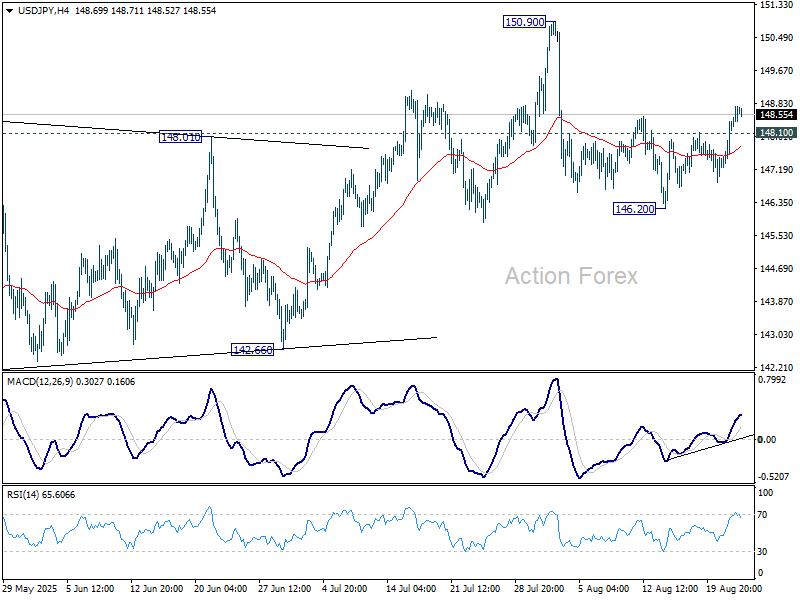

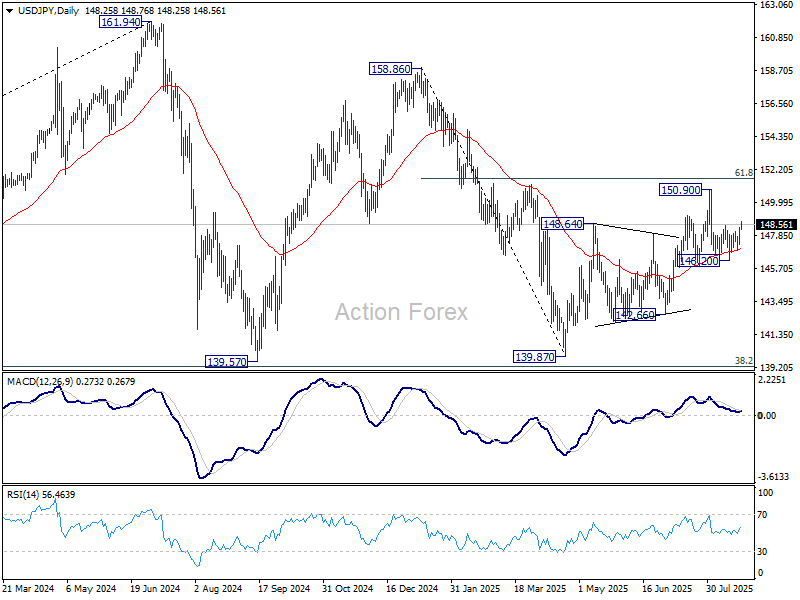

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.62; (P) 148.01; (R1) 148.78; More...

Intraday bias in USD/JPY remains on the upside for the moment. Rebound from 146.20 would target a retest of 150.90 first. Firm break there will resume the rise from 139.87 and target 151.22 fibonacci level next. On the downside, below 148.10 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

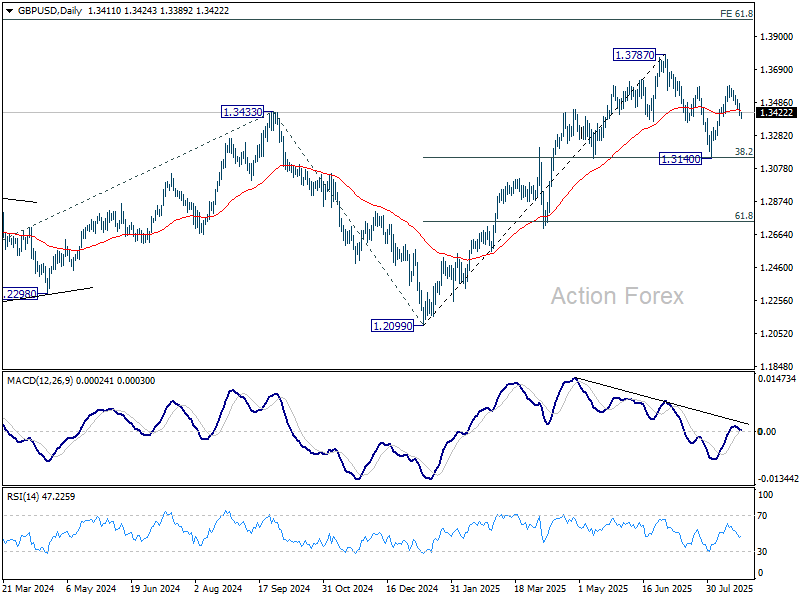

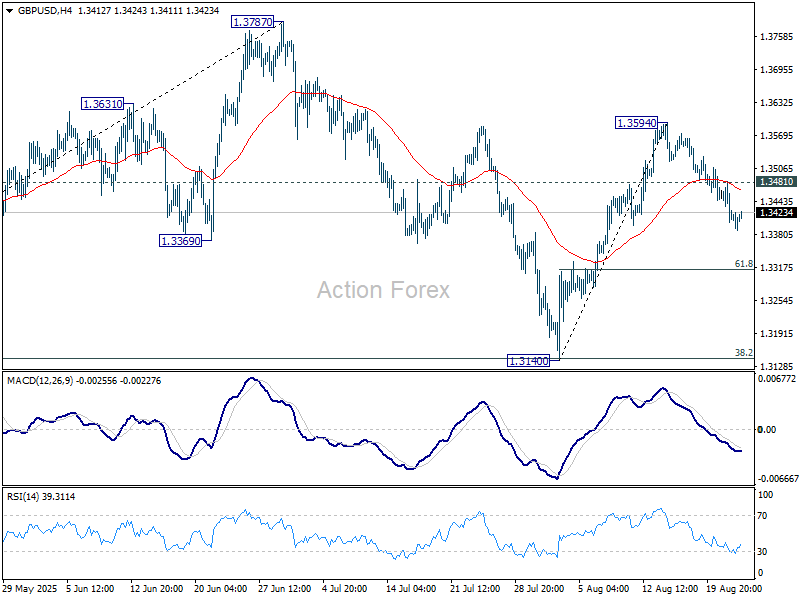

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3384; (P) 1.3434; (R1) 1.3462; More...

Intraday bias in GBP/USD remains mildly on the downside for the moment. Fall from 1.3594 is in progress for 61.8% retracement of 1.3140 to 1.3594 at 1.3313. Firm break there will bring retest of 1.3140 low. On the upside, above 1.3481 minor resistance will bring retest of 1.3594 first. Overall, corrective pattern from 1.3787 is extending.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3090) holds, even in case of deep pullback.