Sample Category Title

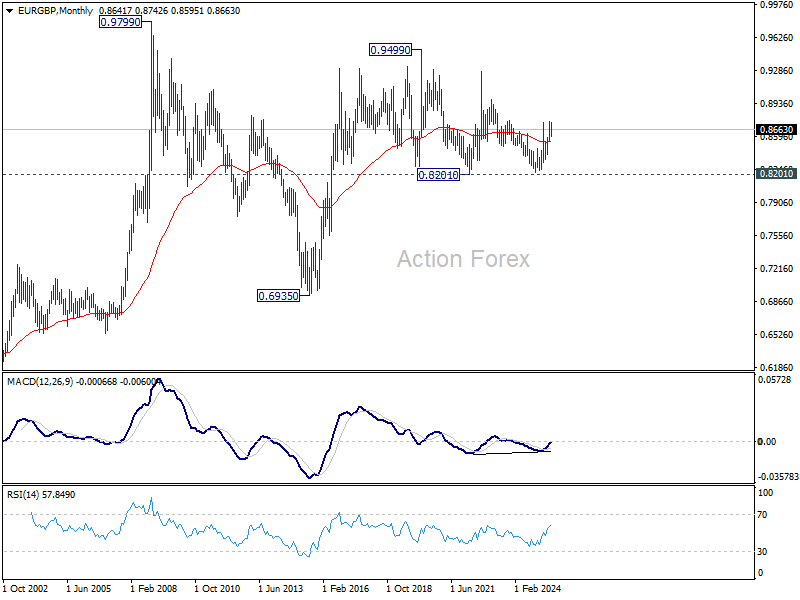

EUR/GBP Weekly Outlook

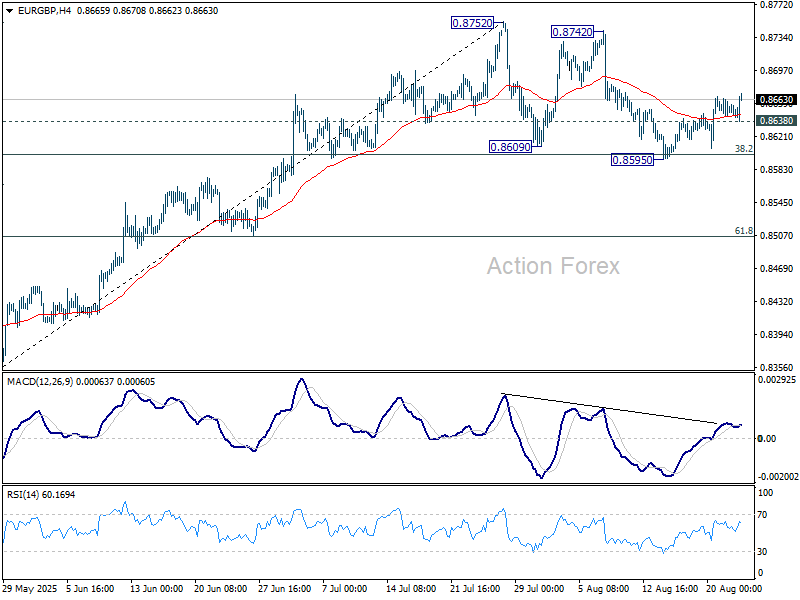

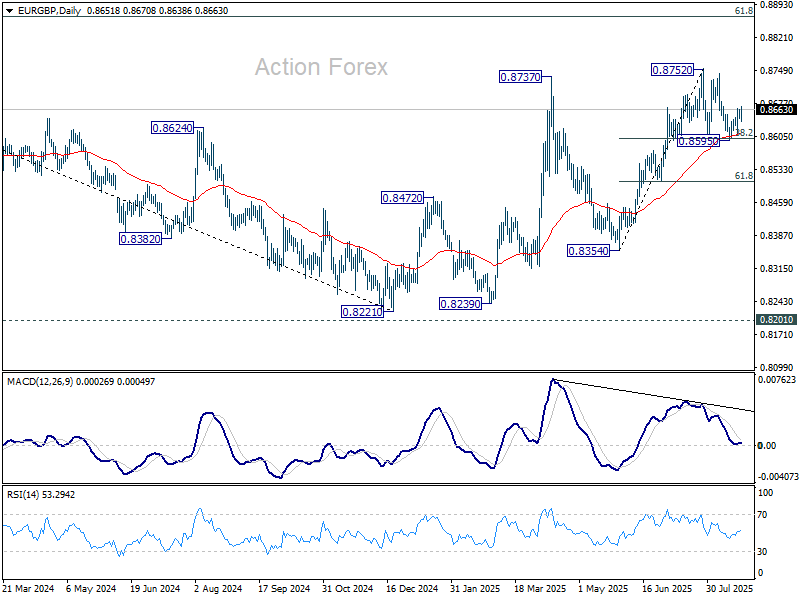

EUR/GBP's extended rebound last week argues that corrective pattern from 0.8752 has completed with three waves down to 0.8595. Initial bias stays mildly on the upside for retesting 0.8752 high. On the downside, below 0.8638 minor support will turn intraday bias neutral again first. Sustained trading below 38.2% retracement of 0.8354 to 0.8752 at 0.8600 will indicate near term bearish reversal and target 61.8% retracement at 0.8506.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8502) holds.

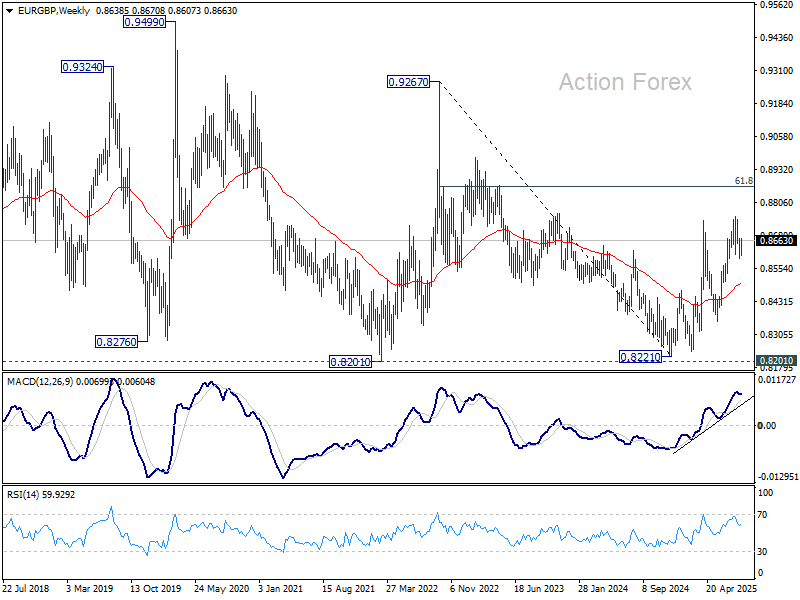

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

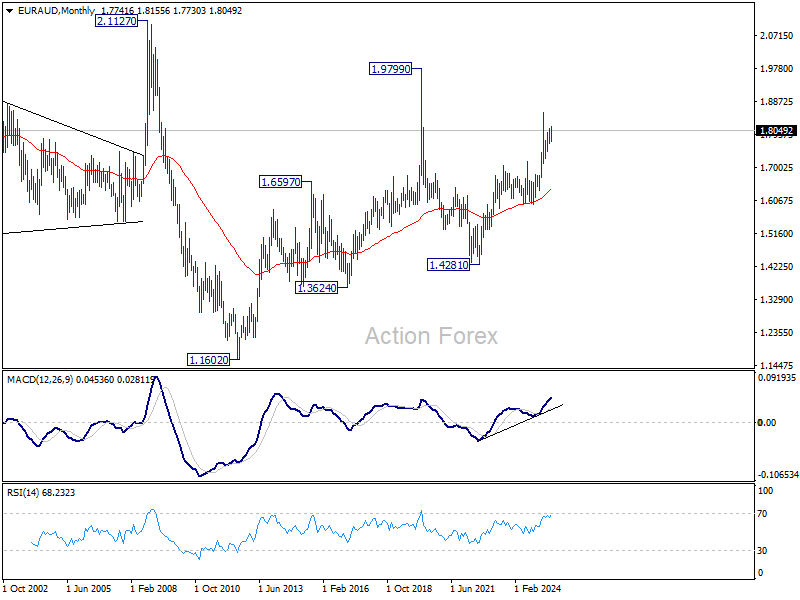

EUR/AUD Weekly Outlook

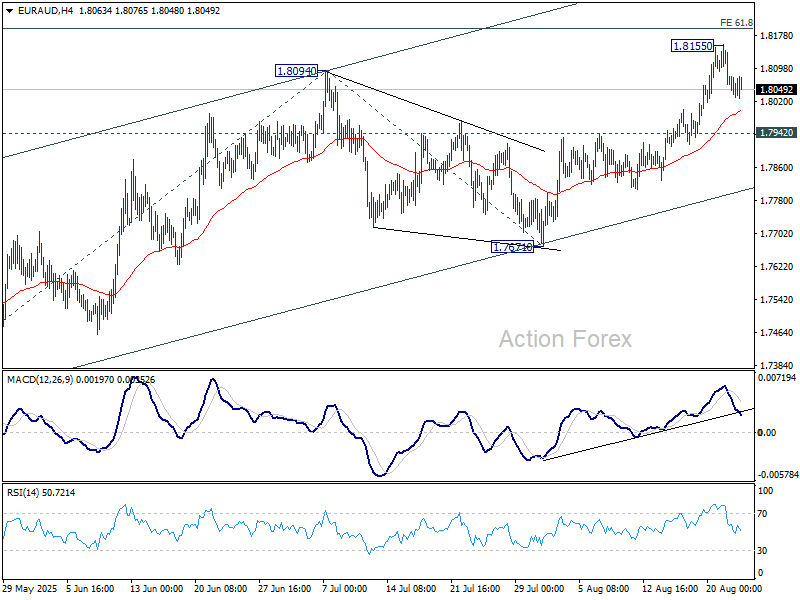

EUR/AUD surged through 1.8094 to resume the rally from 1.7245 last week. As a temporary top was formed at 1.8155, initial bias is neutral this week first. Further rally is expected as long as 1.7942 support holds. Above 1.8155 will target 61.8% projection of 1.7245 to 1.8094 from 1.7671 at 1.8196. Sustained break there will target 100% projection at 1.8520, which is close to 1.8554 high. However, break of 1.7942 will bring deeper fall back to 1.7671 support instead.

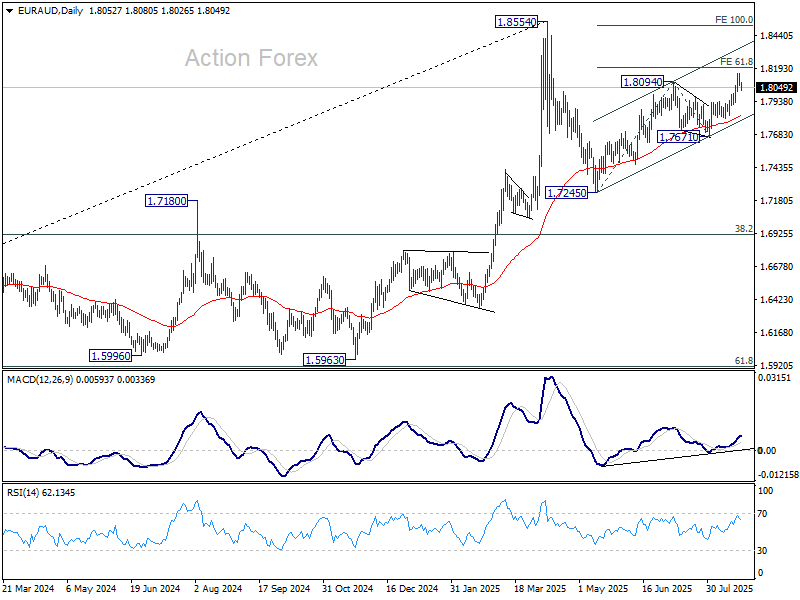

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

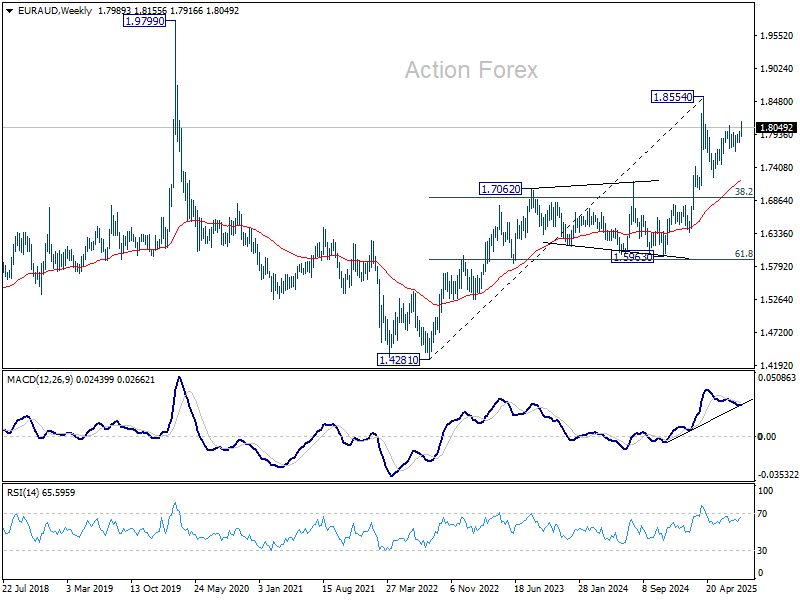

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6419) holds, this second leg could still extend higher.

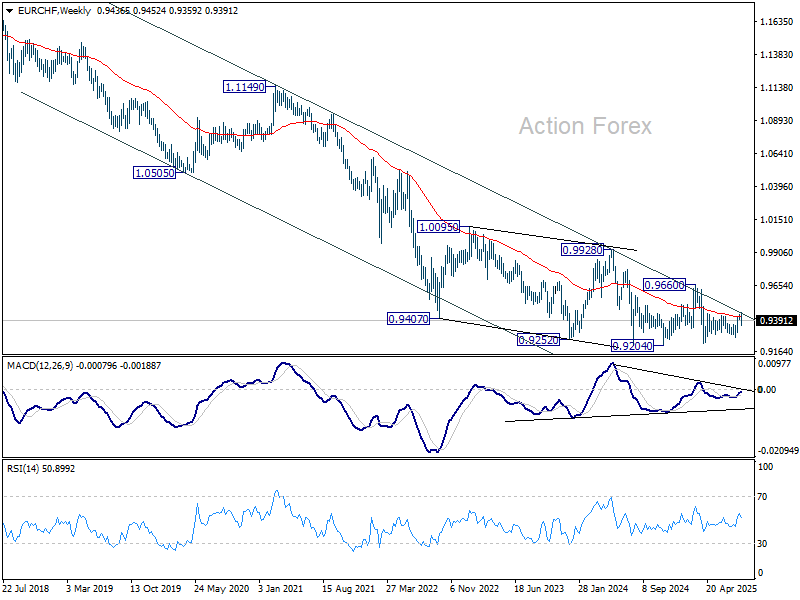

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9452 last week but failed to sustained above 0.9445 resistance and retreated. Nevertheless, with a temporary low formed at 0.9359, initial bias stays neutral this week first. On the upside, above 0.9400 will bring retest of 0.9452. Firm break there will rebound whole rebound from 0.9218. On the downside, however, sustained trading below 55 D EMA (now at 0.9366) will argue that the rebound from 0.9128 has completed as a corrective move. Deeper fall would then be seen to 0.9265 support for confirmation.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

In the long term picture, overall long term down trend is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9860) holds.

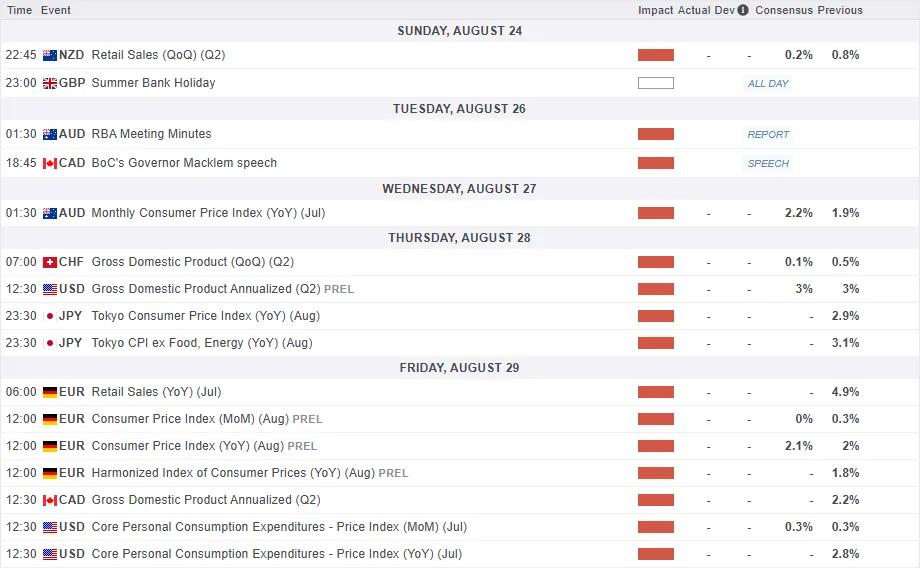

Summary 8/25 – 8/29

Monday, Aug 25, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | 0.20% | 0.80% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | -0.30% | 0.40% |

| 08:00 | EUR | Germany IFO Business Climate Aug | 88.3 | 88.6 |

| 08:00 | EUR | Germany IFO Current Assessment Aug | 86.5 | |

| 08:00 | EUR | Germany IFO Expectations Aug | 90.7 | |

| 14:00 | USD | New Home Sales M/M Jul | 635K | 627K |

| 23:01 | GBP | BRC Shop Price Index Y/Y Aug | 0.70% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 3.20% | 3.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | |

| Forecast: 0.20% | Previous: 0.80% | ||

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | |

| Forecast: -0.30% | Previous: 0.40% | ||

| 08:00 | EUR | Germany IFO Business Climate Aug | |

| Forecast: 88.3 | Previous: 88.6 | ||

| 08:00 | EUR | Germany IFO Current Assessment Aug | |

| Forecast: | Previous: 86.5 | ||

| 08:00 | EUR | Germany IFO Expectations Aug | |

| Forecast: | Previous: 90.7 | ||

| 14:00 | USD | New Home Sales M/M Jul | |

| Forecast: 635K | Previous: 627K | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Aug | |

| Forecast: | Previous: 0.70% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | |

| Forecast: 3.20% | Previous: 3.20% | ||

Tuesday, Aug 26, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||

| 12:30 | USD | Durable Goods Orders Jul | -4.00% | -9.30% |

| 12:30 | USD | Durable Goods Orders ex Transportation Jul | 0.30% | 0.20% |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jun | 2.90% | 2.80% |

| 13:00 | USD | Housing Price Index M/M Jun | 0.00% | -0.20% |

| 14:00 | USD | Consumer Confidence Aug | 96.3 | 97.2 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | |

| Forecast: | Previous: | ||

| 12:30 | USD | Durable Goods Orders Jul | |

| Forecast: -4.00% | Previous: -9.30% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Jul | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jun | |

| Forecast: 2.90% | Previous: 2.80% | ||

| 13:00 | USD | Housing Price Index M/M Jun | |

| Forecast: 0.00% | Previous: -0.20% | ||

| 14:00 | USD | Consumer Confidence Aug | |

| Forecast: 96.3 | Previous: 97.2 | ||

Wednesday, Aug 27, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jul | 0.00% | |

| 01:30 | AUD | Monthly CPI Y/Y Jul | 2.30% | 1.90% |

| 06:00 | EUR | Germany GfK Consumer Confidence Sep | -21.2 | -21.5 |

| 08:00 | CHF | ZEW Expectations Aug | 2.4 | |

| 14:30 | USD | Crude Oil Inventories (Aug 22) | -6.0M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jul | |

| Forecast: | Previous: 0.00% | ||

| 01:30 | AUD | Monthly CPI Y/Y Jul | |

| Forecast: 2.30% | Previous: 1.90% | ||

| 06:00 | EUR | Germany GfK Consumer Confidence Sep | |

| Forecast: -21.2 | Previous: -21.5 | ||

| 08:00 | CHF | ZEW Expectations Aug | |

| Forecast: | Previous: 2.4 | ||

| 14:30 | USD | Crude Oil Inventories (Aug 22) | |

| Forecast: | Previous: -6.0M | ||

Thursday, Aug 28, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Aug | 47.8 | |

| 01:00 | NZD | ANZ Activity Outlook Aug | 40.6 | |

| 01:30 | AUD | Private Capital Expenditure Q2 | 0.50% | -0.10% |

| 07:00 | CHF | GDP Q/Q Q2 | 0.10% | 0.50% |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | 3.50% | 3.30% |

| 09:00 | EUR | Eurozone Economic Sentiment Aug | 95.9 | 95.8 |

| 09:00 | EUR | Industrial Confidence Aug | -11 | -10.4 |

| 09:00 | EUR | Eurozone Services Sentiment Aug | 4.2 | 4.1 |

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | -15.5 | -15.5 |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||

| 12:30 | CAD | Current Account (CAD) Q2 | -18.6B | -2.1B |

| 12:30 | USD | Initial Jobless Claims (Aug 22) | 231K | 235K |

| 12:30 | USD | GDP Annualized Q2 P | 3.00% | 3.00% |

| 12:30 | USD | GDP Price Index Q2 P | 2.00% | 2.00% |

| 14:00 | USD | Pending Home Sales M/M Jul | 0.30% | -0.80% |

| 14:30 | USD | Natural Gas Storage (Aug 22) | 13B | |

| 23:30 | JPY | Tokyo CPI Y/Y Aug | 2.90% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Aug | 2.60% | 2.90% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Aug | 3.10% | |

| 23:30 | JPY | Unemployment Rate Jul | 2.50% | 2.50% |

| 23:50 | JPY | Industrial Production M/M Jul P | -1.00% | 2.10% |

| 23:50 | JPY | Retail Trade Y/Y Jul | 1.80% | 2.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Aug | |

| Forecast: | Previous: 47.8 | ||

| 01:00 | NZD | ANZ Activity Outlook Aug | |

| Forecast: | Previous: 40.6 | ||

| 01:30 | AUD | Private Capital Expenditure Q2 | |

| Forecast: 0.50% | Previous: -0.10% | ||

| 07:00 | CHF | GDP Q/Q Q2 | |

| Forecast: 0.10% | Previous: 0.50% | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | |

| Forecast: 3.50% | Previous: 3.30% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Aug | |

| Forecast: 95.9 | Previous: 95.8 | ||

| 09:00 | EUR | Industrial Confidence Aug | |

| Forecast: -11 | Previous: -10.4 | ||

| 09:00 | EUR | Eurozone Services Sentiment Aug | |

| Forecast: 4.2 | Previous: 4.1 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | |

| Forecast: -15.5 | Previous: -15.5 | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | |

| Forecast: | Previous: | ||

| 12:30 | CAD | Current Account (CAD) Q2 | |

| Forecast: -18.6B | Previous: -2.1B | ||

| 12:30 | USD | Initial Jobless Claims (Aug 22) | |

| Forecast: 231K | Previous: 235K | ||

| 12:30 | USD | GDP Annualized Q2 P | |

| Forecast: 3.00% | Previous: 3.00% | ||

| 12:30 | USD | GDP Price Index Q2 P | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 14:00 | USD | Pending Home Sales M/M Jul | |

| Forecast: 0.30% | Previous: -0.80% | ||

| 14:30 | USD | Natural Gas Storage (Aug 22) | |

| Forecast: | Previous: 13B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Aug | |

| Forecast: | Previous: 2.90% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Aug | |

| Forecast: 2.60% | Previous: 2.90% | ||

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Aug | |

| Forecast: | Previous: 3.10% | ||

| 23:30 | JPY | Unemployment Rate Jul | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 23:50 | JPY | Industrial Production M/M Jul P | |

| Forecast: -1.00% | Previous: 2.10% | ||

| 23:50 | JPY | Retail Trade Y/Y Jul | |

| Forecast: 1.80% | Previous: 2.00% | ||

Friday, Aug 29, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Private Sector Credit M/M Jul | 0.60% | 0.60% |

| 05:00 | JPY | Housing Starts Y/Y Jul | -9.60% | -15.60% |

| 05:00 | JPY | Consumer Confidence Aug | 34.2 | 33.7 |

| 06:00 | EUR | Germany Import Price Index M/M Jul | -0.30% | 0.00% |

| 06:00 | EUR | Germany Retail Sales M/M Jul | -0.20% | 1.00% |

| 06:45 | EUR | France GDP Q/Q Q2 | 0.30% | 0.30% |

| 07:00 | CHF | KOF Economic Barometer Aug | 97.9 | 101.1 |

| 07:55 | EUR | Germany Unemployment Change Jul | 10K | 2K |

| 07:55 | EUR | Germany Unemployment Rate Jul | 6.30% | 6.30% |

| 12:00 | EUR | Germany CPI M/M Aug P | 0.00% | 0.30% |

| 12:00 | EUR | Germany CPI Y/Y Aug P | 2.10% | 2.00% |

| 12:30 | CAD | GDP M/M Jun | 0.20% | -0.10% |

| 12:30 | USD | Personal Income M/M Jul | 0.40% | 0.30% |

| 12:30 | USD | Personal Spending M/M Jul | 0.50% | 0.30% |

| 12:30 | USD | PCE Price Index M/M Jul | 0.30% | 0.30% |

| 12:30 | USD | PCE Price Index Y/Y Jul | 2.60% | 2.60% |

| 12:30 | USD | Core PCE Price Index M/M Jul | 0.30% | 0.30% |

| 12:30 | USD | Core PCE Price Index Y/Y Jul | 2.90% | 2.80% |

| 12:30 | USD | Goods Trade Balance (USD) Jul P | -90.7B | -84.9B |

| 12:30 | USD | Wholesale Inventories Jul P | 0.20% | 0.10% |

| 13:45 | USD | Chicago PMI Aug | 45.3 | 47.1 |

| 14:00 | USD | UoM Consumer Sentiment Index Aug F | 58.6 | 58.6 |

| 14:00 | USD | UoM 1-year Inflation Expectations Aug F | 4.90% | 4.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Private Sector Credit M/M Jul | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 05:00 | JPY | Housing Starts Y/Y Jul | |

| Forecast: -9.60% | Previous: -15.60% | ||

| 05:00 | JPY | Consumer Confidence Aug | |

| Forecast: 34.2 | Previous: 33.7 | ||

| 06:00 | EUR | Germany Import Price Index M/M Jul | |

| Forecast: -0.30% | Previous: 0.00% | ||

| 06:00 | EUR | Germany Retail Sales M/M Jul | |

| Forecast: -0.20% | Previous: 1.00% | ||

| 06:45 | EUR | France GDP Q/Q Q2 | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 07:00 | CHF | KOF Economic Barometer Aug | |

| Forecast: 97.9 | Previous: 101.1 | ||

| 07:55 | EUR | Germany Unemployment Change Jul | |

| Forecast: 10K | Previous: 2K | ||

| 07:55 | EUR | Germany Unemployment Rate Jul | |

| Forecast: 6.30% | Previous: 6.30% | ||

| 12:00 | EUR | Germany CPI M/M Aug P | |

| Forecast: 0.00% | Previous: 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Aug P | |

| Forecast: 2.10% | Previous: 2.00% | ||

| 12:30 | CAD | GDP M/M Jun | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 12:30 | USD | Personal Income M/M Jul | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 12:30 | USD | Personal Spending M/M Jul | |

| Forecast: 0.50% | Previous: 0.30% | ||

| 12:30 | USD | PCE Price Index M/M Jul | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Jul | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 12:30 | USD | Core PCE Price Index M/M Jul | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Jul | |

| Forecast: 2.90% | Previous: 2.80% | ||

| 12:30 | USD | Goods Trade Balance (USD) Jul P | |

| Forecast: -90.7B | Previous: -84.9B | ||

| 12:30 | USD | Wholesale Inventories Jul P | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 13:45 | USD | Chicago PMI Aug | |

| Forecast: 45.3 | Previous: 47.1 | ||

| 14:00 | USD | UoM Consumer Sentiment Index Aug F | |

| Forecast: 58.6 | Previous: 58.6 | ||

| 14:00 | USD | UoM 1-year Inflation Expectations Aug F | |

| Forecast: 4.90% | Previous: 4.90% | ||

Markets Weekly Outlook – Fed Chair Pivot Ignites Rally Ahead of US PCE and Japanese Inflation Data

Week in review

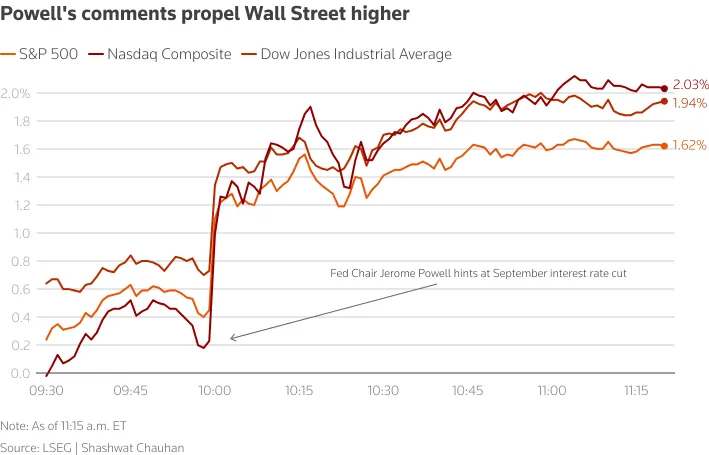

Wall Street's main indexes surged on Friday after Federal Reserve Chair Jerome Powell hinted at a possible interest rate cut during his speech at the Jackson Hole Symposium.

The Dow Jones rose 887.83 points (1.99%) to a record high of 45,680.14. The S&P 500 gained 102.14 points (1.61%) to 6,472.31, and the Nasdaq climbed 421.85 points (2.00%) to 21,520.79.

Ten of the 11 S&P 500 sectors were up, with consumer discretionary stocks jumping nearly 3% and communication services rising 2.3%. The Philadelphia Semiconductor Index soared 3.3%, while major growth stocks also saw gains, led by Tesla, which rose 5.7%.

The Russell 2000 Index, which is sensitive to interest rates, surged 3.9%, reaching its highest level this year.

Source: LSEG

Fed Chair Powell Pivots. September Cut Incoming?

Chair Powell’s Jackson Hole speech represented a marked shift in tone from the Fed’s July minutes earlier this week. The minutes suggested that most FOMC members saw the upside risks to inflation as “more salient” than the downside risks to inflation, but Chair Powell acknowledged today that the balance of risks "appears to be shifting”.

Chair Powell's speech highlighted a tricky situation: inflation risks are rising, while employment risks are falling. He explained that when these goals conflict, the Fed's approach is to balance both. He noted that interest rates are now much closer to a neutral level than they were a year ago, and the steady unemployment rate gives the Fed room to carefully consider any policy changes. However, since rates are already high, the changing economic outlook might require adjustments to policy.

Powell's tone was more cautious (or "dovish") than expected. He didn’t push back against the idea of a rate cut, keeping his options open. A key point was his reduced concern about inflation caused by tariffs, likely due to signs of a weakening job market. Markets reacted strongly to his comment about "shifting risks may warrant adjusting policy," as many had feared he would take a more aggressive (or "hawkish") stance.

As a result:

- Short-term bond yields dropped below 3.7%.

- -The 10-year yield also fell, nearing 4.25%.

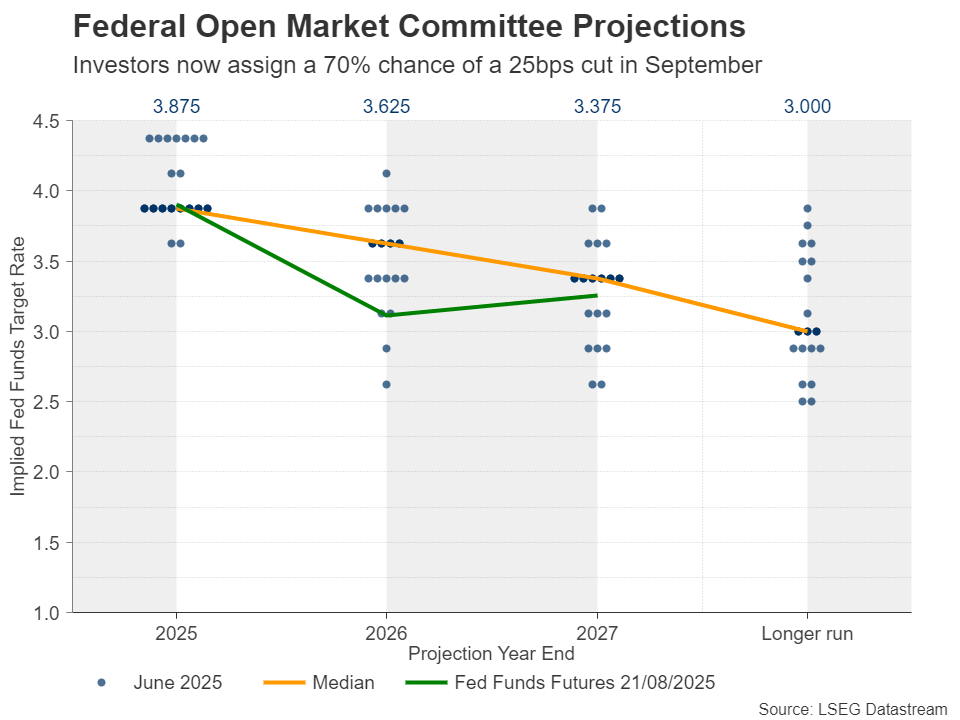

- The chances of a rate cut in September jumped back to 90%, up from less than 70% before his speech.

The dollar index dropped 0.96% to 97.66 after Powell's comments. It had been around 98.7 earlier in the day.

The euro rose 1.06% to $1.1728, hitting $1.1742 at one point, its highest since July 28. The dollar weakened 1.08% against the Japanese yen, falling to 146.77.

The British pound gained 0.86%, reaching $1.3527. The Australian dollar climbed 1.14% to $0.6492.

In cryptocurrencies, Bitcoin jumped 4.10%, reaching $117,035.

Gold received a much needed shot in the arm rising close to the $3380/oz mark after Fed Chair Powell's speech.

The Week Ahead

The week ahead will be all talk around a potential Fed Pivot while high impact data from the US and Japan will be in focus.

Asia Pacific Markets - BoJ in Focus as Ueda Speaks at Jackson Hole, Tokyo Inflation Next Week

From China we will get July's industrial profits data, released on Wednesday, is expected to show ongoing declines. To address issues like deflationary price wars, policies to reduce excessive competition and industrial overcapacity will be important.

However, these measures may have side effects and are likely to be implemented slowly. As a result, profits could stay weak throughout the year.

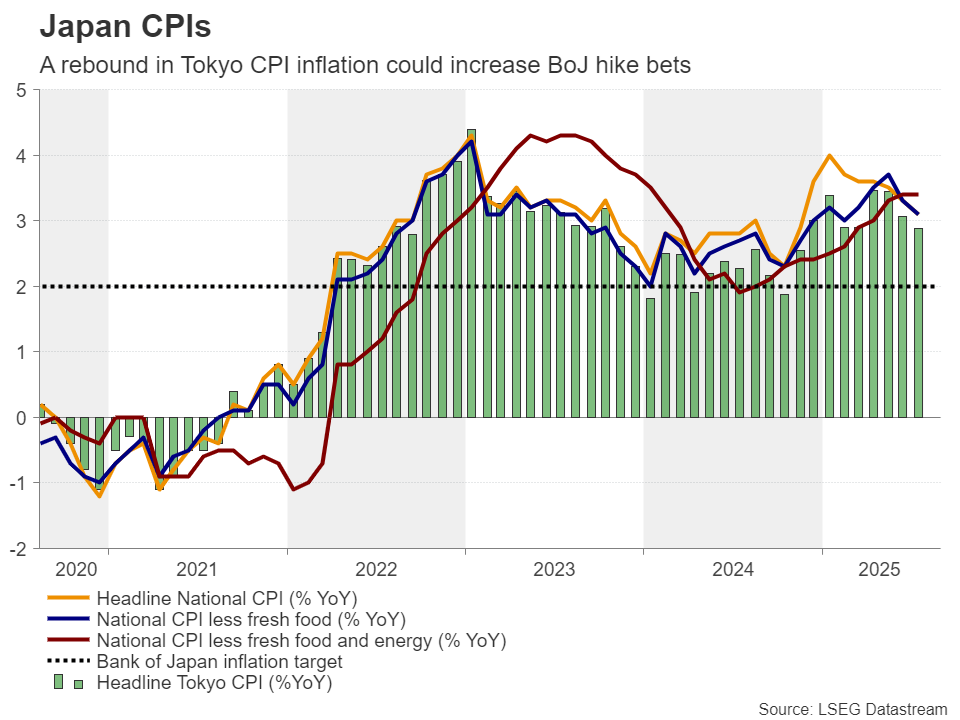

Over the weekend we will hear from BoJ Governor Ueda who will be speaking at the Jackson Hole Symposium. Market participants will be hoping for signs of whether a rate hike will be coming anytime soon especially after headline inflation hit an 8 month low.

Tokyo's inflation data is highly anticipated, with overall prices expected to slow to 2.6% in August from 2.9% in July, mainly due to lower energy costs, though fresh food prices are still rising. Core inflation (excluding fresh food and energy) is likely to stay above 3%, giving the Bank of Japan more confidence that underlying inflation is nearing its 2% target.

Industrial production is predicted to drop by 1.2% in July, partly reversing June's 2.1% increase, as temporary output boosts from tariff-related demand return to normal. However, retail sales are expected to grow, helped by strong wage increases. The unemployment rate is likely to stay at 2.5%, reflecting a tight job market that could lead to more stable wage growth over time.

Euro Area Economic Sentiment and the Feds Preferred Inflation Gauge

Eurozone sentiment will be closely monitored next week to see if it matches the positive results of last Thursday's PMI. The strong manufacturing data gave hope that the trade war's impact has been smaller than expected. If the European Commission's data confirms this, it would strengthen the outlook for a better-performing eurozone economy.

The Fed's preferred inflation measure is expected to match the 0.3% month-on-month increase seen in core CPI. However, there's a chance it could come in slightly lower. While producer price data was strong, the parts that directly impact core PCE were more mixed.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index (DXY)

This week's Chart of the week is the US Dollar Index (DXY).

The DXY rallied earlier this week before running into the long-term descending trendline. This coincided with Fed Chair Powell's speech which sent the Dollar Index tumbling.

The index has broken below the ascending triangle which was in play from the July low at 96.37.

This leaves the index vulnerable to further downside with immediate support now at 96.90.

The period-14 RSI also broke back below the 50 neutral level which hints at a shift to bearish momentum once more.

US Dollar Index (DXY) Daily Chart - August 22, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 96.90

- 96.36

- 95.00

Resistance

- 98.60

- 98.98

- 99.57

The Weekly Bottom Line: Fed Chair Powell Opens Door for Rate Cuts

Canadian Highlights

- Shorter-term core inflation metrics cooled in July, lifting the odds BoC rate cut on September 17th. However, the odds are still low, according to markets.

- Next week’s second quarter GDP report should show a sizeable contraction, indicating increased economic slack.

- However, the Canadian economy has been more resilient than initially feared, with this week’s housing starts and retail sales volumes reports adding to this narrative.

U.S. Highlights

- In his Jackson Hole speech, Fed Chair Powell highlighted that the downside risks to employment have risen. This shifts the balance of risks on employment and inflation, and opens the door for a September rate cut more widely.

- Odds of a September rate cut rose after his speech, boosting stock markets.

- Also this week, July housing data improved but did not change the overall slow market trend.

Canada – Dovish Inflation Reports Helps BoC Rate Cut Odds

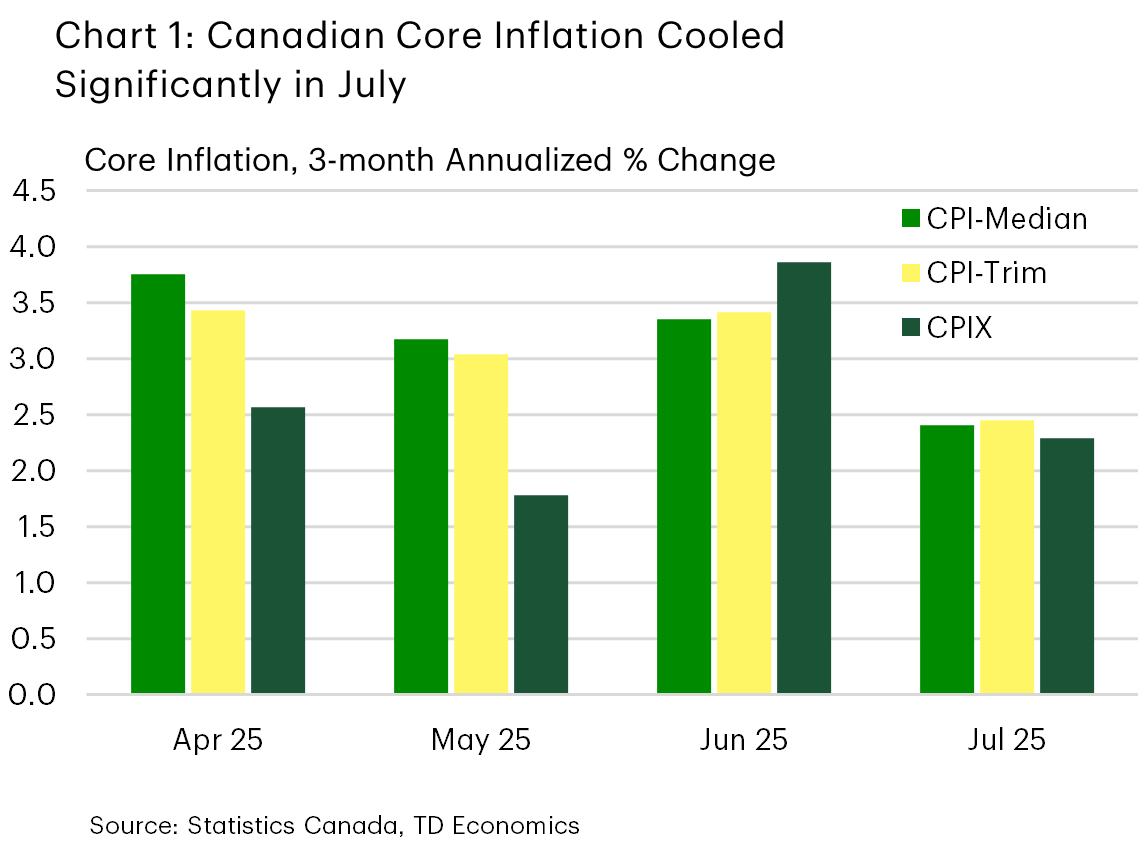

We have long believed that economic slack from a softening Canadian economy would help ease inflationary pressures, counterbalancing the upward push on consumer prices caused by retaliatory tariffs on U.S. goods, efforts to diversify exports away from the U.S., and Canadian firms seeking new suppliers. The July inflation data aligned closely with this narrative. Headline inflation remained mild at 1.7% year-over-year, with the continued effects of the April carbon tax removal and falling gasoline prices weighing on the overall number—though gasoline prices are on track to stabilize in August.

More crucially, core inflation trends have shown encouraging signs of cooling. The Bank of Canada’s (BoC’s) preferred measures of core inflation remained elevated on a year-over-year basis, but shorter-term momentum slowed notably. On a three-month annualized basis, the average of the BoC’s key metrics (CPI-Median and CPI-Trim) eased to 2.4%, the slowest pace seen in nearly a year. Similarly, more traditional core measures—CPI excluding food and energy, and CPIX—both dropped by over one percentage point to about 2.2%. These trends prompted a market reaction, with both bond yields and the Canadian dollar slipping, and modestly raised expectations for a possible BoC rate cut at the September 17th meeting.

Even with the CPI report, markets are still only assigning a 33% chance of a rate cut at the September meeting. And, the BoC has a chance to review another round of jobs and inflation data before its next rate announcement. Next week’s second-quarter GDP report is also highly anticipated; we expect an annualized contraction of about 1.5%, signaling increased slack in the economy and adding further downward pressure on inflation. This economic backdrop could pave the way for two more rate cuts this year (see our updated economic forecast here), given that the current policy rate still sits at the midpoint of what the Bank considers neutral for the economy. Trade was the main drag on second-quarter growth, with exports dropping due to softer U.S. demand (amid tariffs) and an unwinding of earlier gains prompted by anticipation of tariffs.

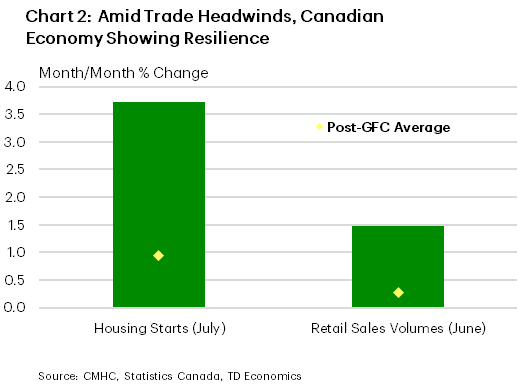

Despite an expected weak GDP report for the second quarter, the Canadian economy has shown more resilience than we expected a few months ago. This week offered more glimpses of this durability (Chart 2), with July housing starts reaching their highest level since 2022, as the rental market is receiving a tailwind from powerful past population growth and government programs targeting this sector. Meanwhile, retail sales volumes advanced 1.5% month-on-month, supported by gains in a broad range of categories. Encouraging as these results may be, significant uncertainty remains. The country also continues to face tariffs and a notable slowdown in population growth. Reports indicate that some progress may come on the tariff front, with the Canadian government to remove some retaliatory tariffs on U.S. goods to restart stalled trade talks. However, in the near-term, these factors remain in play, and the economy will be hard pressed to generate strong momentum in the third quarter.

U.S. – Fed Chair Powell Opens Door for Rate Cuts

Financial markets appeared set to finish slightly lower for the week. However, following Chair Powell’s keynote speech on Friday morning at the Federal Reserve’s annual symposium in Jackson Hole, Wyoming—where he indicated the possibility of rate cuts—equities rallied. The 10-year yield declined from around 4.33% earlier in the day to 4.26%, while the S&P 500 rose by 1.4% at the time of writing, surpassing last week’s close.

With few major data releases during the week (only two main housing reports), attention was focused on developments related to the central bank. The FOMC minutes provided additional context regarding the July decision not to cut rates. Participants highlighted risks associated with both sides of the Committee’s dual mandate, referencing “upside risk to inflation and downside risk to employment.” In July, most participants considered the inflation risk to be more significant, citing uncertain tariff effects and concerns about inflation expectations.

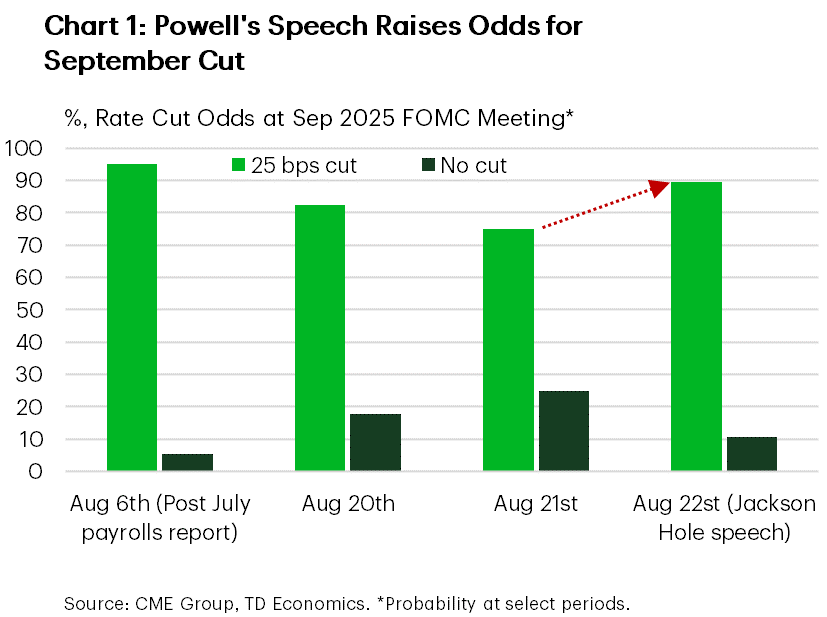

In his Jackson Hole speech this Friday morning, Chair Powell suggested a change in the Fed’s position. He noted that with policy currently restrictive, adjustments may be warranted given the outlook and balance of risks (see commentary). The key shift in Powell’s messaging relative to July reflects the recent jobs data and acknowledges that downside risks to employment are rising. This both tips the balance on the Fed’s dual mandate to greater concern about fostering maximum employment, and reduces the risks that tariff-driven inflation leads to a wage-price spiral. By emphasizing downside risks to employment and reduced risks of persistent inflation, Chair Powell has opened the door for a rate cut in September. There is still an employment and an inflation report for the Fed to parse before deciding whether to walk through the door. This is a key shift from Chair Powell, and not surprisingly market odds of a September rate cut jumped back up following his speech (Chart 1).

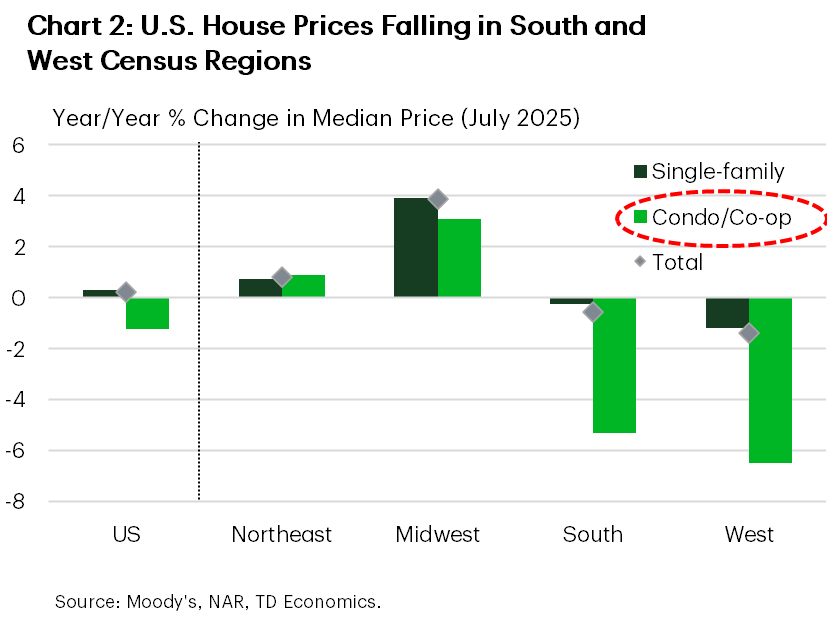

Lower rates can’t come fast enough for the housing market. Existing home sales increased moderately in July (up 2% month-over-month), but overall activity remained subdued, with sales levels near those seen during the Global Financial Crisis. Soft demand and some inventory growth have contributed to slower home price appreciation, particularly in the West and South Census regions (Chart 2). There was a notable rise in multifamily starts in July, primarily in the South, though this series is volatile and permitting data suggest a weaker outlook. Single-family starts showed little change from subdued levels, in tune with looser conditions in the new home market. Should the Federal Reserve lower rates later in the year as expected, mortgage rates should decline further, supporting housing activity in the future.

All told, barring any major surprises in payroll and inflation data, it is widely expected that the Federal Reserve will resume rate cuts in mid-September.

Weekly Economic & Financial Commentary: Powell Keeps Options Open for September Rate Cut

Summary

United States: Is the Housing Drag Intensifying?

- Housing was the focus of attention this week as markets prepared for Chair Powell's speech at Jackson Hole. All told, upside surprises in existing home sales and housing starts during July conceal a weakening trend in residential activity.

- Next week: New Home Sales (Mon.), Durable Goods Orders (Tue.), Personal Income & Spending (Fri.)

International: Easing Bias and Uneven Global Data

- This week saw a mix of monetary policy decisions and economic data across G10 economies. The Reserve Bank of New Zealand delivered a dovish rate cut, while Sweden’s Riksbank held rates steady. In Canada, July CPI came in softer than expected, while UK inflation surprised to the upside. Meanwhile, Eurozone and UK PMIs showed modest improvement and Norway’s Q2 GDP pointed to strengthening momentum.

- Next week: Canada GDP (Fri.), India GDP (Fri.)

Interest Rate Watch: Powell Keeps Options Open for September Rate Cut

- With upside risks to inflation and downside risks to employment keeping the FOMC's dual mandate in tension, Chair Powell was careful not to pre-commit to a policy change at Jackson Hole. However, he kept the prospects for a September rate cut alive and reconfirmed the Committee's existing bias for rate cuts later this year.

Credit Market Insights: Hope Meets Headwinds

- Last month, the NFIB Small Business Optimism Index rose 1.7 points to 100.3, hitting just above the historical average of 98. While the headline suggests improved sentiment, elevated uncertainty weighs on small businesses.

Topic of the Week: The Forces Behind Stronger Productivity Growth

- Productivity growth is firming, driven less by labor shifts and more by technology, innovation and capital investment. Generative AI and R&D could lift it further, though trade policy and immigration constraints pose risks to sustaining long-term economic potential growth.

Chair Powell Signals FOMC Bias to Easing, Leaving the Door Open to September Cut

At the Federal Reserve Bank of Kansas City's Jackson Hole Economic Symposium, Fed Chair Jerome Powell delivered a much-anticipated speech, titled Monetary Policy and Fed's Framework Review.

Powell highlighted the challenges facing the U.S. economy, including significantly higher tariffs and tighter immigration policy, with both affecting supply and demand. Powell noted that, "in this environment, distinguishing cyclical developments from trend or structural developments is difficult. This distinction is difficult because monetary policy can work to stabilize cyclical fluctuations but can do little to alter structural changes".

The Chair's assessment of the labor market was notably more downbeat than his characterization at the July press conferences, noting, "the slowdown is much larger than assessed just a month ago", but balanced that with the unemployment rate remaining "historically low … and broadly stable over the past year".

On tariffs, Powell noted that inflation passthrough has started to materialize on some categories of goods and, "… we expect those effects to accumulate over the coming months". But also noted that both survey and market-based measures of inflation expectations remain well anchored and said it is a reasonable "base case" that tariffs will have a one-time impact on inflation. However, he also acknowledged the risk of a wage-price spiral, though that appears less likely given current labor market conditions.

Lastly on monetary policy, Powell noted "with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance" – highlighting the FOMC's bias towards easing.

Powell's speech also highlighted the Fed's 2025 framework review. The last review was conducted in 2020, where the changes were largely the result of the policy rate being at the effective lower bound for a significant period. The 2025 framework review made three notable changes, including:

- Removing language indicating that the effective lower bound was a defining feature of the economic landscape and instead noted that "monetary policy strategy is designed to promote maximum employment and stable prices across a broad range of economic conditions".

- Returned to the framework of flexible inflation targeting and eliminated the "makeup" strategy. Back in 2020, the motivation for allowing some inflation overshoot was to account for the fact that inflation had run persistently below the Fed's 2% target over the decade following the Global Financial Crisis. However, the persistent overshoot post-pandemic has led to concerns that it could lead to inflation expectations becoming unanchored.

- The Committee also revised its language on maximum employment. The 2025 framework removed the reference to "shortfalls" and instead states that "the Committee recognizes that employment may at times run above real-time assessments of maximum employment without necessarily creating risks to price stability".

Key Implications

Chair Powell struck a more dovish tone in today's speech, sending a clear signal that further policy easing is on the way. While a September cut is looking more likely, it is still not a guarantee and will largely hinge on the August employment and inflation reports. However, markets responded sharply, with the S&P 500 extending earlier gains and is now up 1.5%, while the 2-year Treasury fell 10 basis points to 3.69%. Fed futures have shifted back to pricing in a 90% probability of a September cut – up from yesterday's 70%.

There's a growing divide among policymakers on what's behind the recent slowing in employment. Powell and others acknowledge the role of supply-side factors, including tighter immigration and point to the low and stable unemployment rate as a sign of overall balance. Conversely, Waller and Bowman attribute the cooling to a broader slowing in economic activity. But it's clear that neither camp would disagree that the downside risks have increased since the July FOMC meeting. We would argue that today's market reaction could be a bit overdone. With the Fed's dual mandate coming into tension, Fed officials will remain acutely attuned to risks on both sides, meaning the FOMC's approach to adjusting policy is probably best characterized as a move to a less-restrictive environment as opposed to a return to neutral.

Week Ahead – US GDP and PCE Data to Mark a Relatively Light Week

- Accelerating US PCE could weigh on Fed rate cut bets.

- Euro traders eye CPI data from Italy, France and Germany.

- Tokyo CPIs could impact chances of a BoJ hike by year-end.

- Wounded loonie seeks salvation in GDP numbers.

Dollar gains as investors scale back Fed cut bets

The US dollar gained ground this week, benefiting from investors scaling back their Fed rate cut bets.

Following the weak NFP report for July, the disappointing ISM non-manufacturing PMI for the same month, and Trump’s reciprocal tariffs, speculation about faster rate cuts by the Fed heightened, perhaps as the aforementioned blend of developments sparked some recession fears. Investors were fully pricing in a September 25bps rate cut, another one thereafter, and went as far as assigning a 30% chance of a third one before the end of the year.

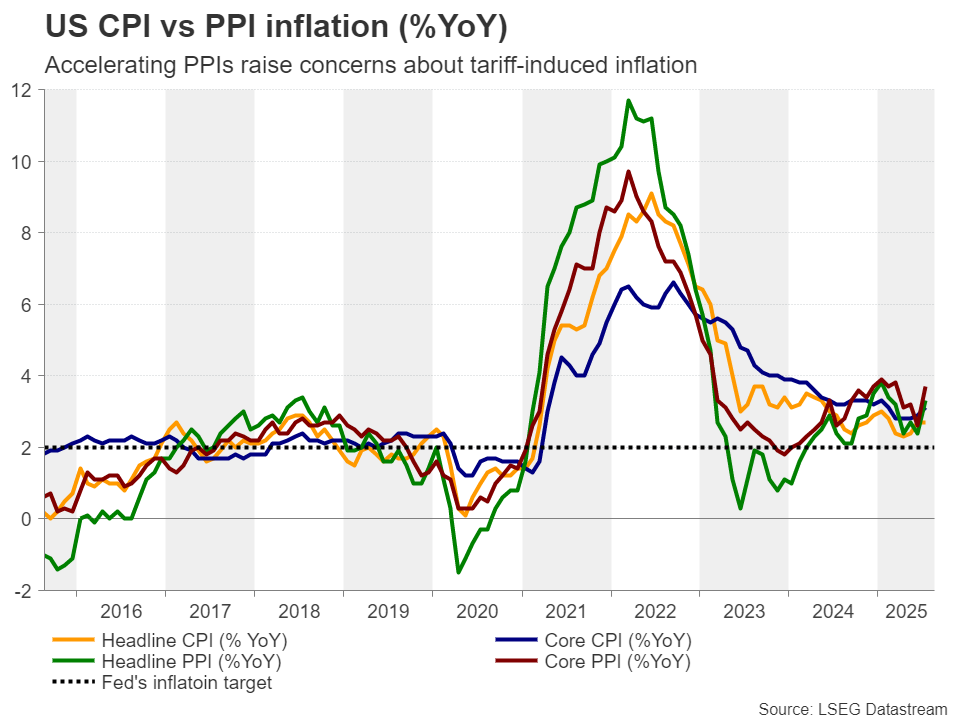

The CPI data for July corroborated that view, showing little evidence of tariff-induced inflation. However, producer prices accelerated sharply, painting a totally different picture and confirming Fed Chair Powell’s view that the impact of Trump’s tariffs on inflation will start appearing during the summer months. Combined with the strong preliminary S&P Global PMIs for August, this prompted investors to price out several basis points worth of rate cuts. They are now assigning a 70% chance of a September reduction.

After Powell’s speech, focus to turn on GDP and PCE data

The Fed Chief is scheduled to speak today at the Jackson Hole economic symposium, and it seems that the market is bracing for a hawkish outcome. Indeed, not only is the dollar gaining, but Wall Street is in pullback mode.

However, even if he sounds hawkish and does not pre-commit to any action beyond September, market participants may seek further validation from next week’s US data, which includes the second estimate of GDP for Q2 and the PCE inflation data for July, due out on Thursday and Friday, respectively.

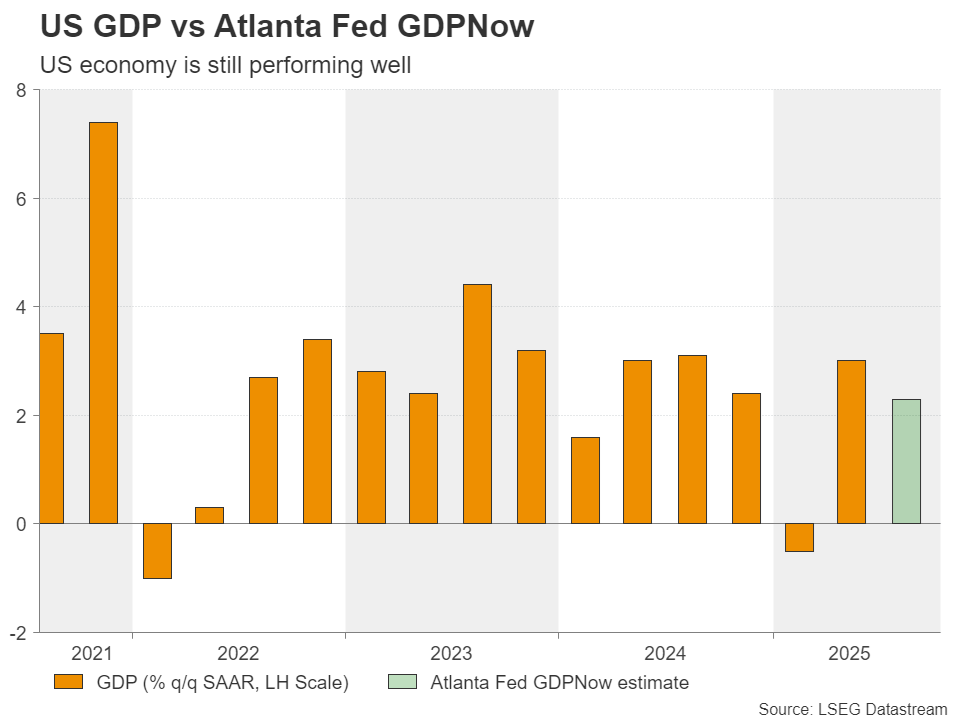

The first estimate of GDP came in at 3.0% q/q SAAR and expectations are for confirmation of that. Combined with the 2.3% forecast of the Atlanta Fed GDPNow model, it adds extra credence to the idea that the Fed should not rush into lowering interest rates, despite US President Trump’s pressure and repeated attacks on Chair Powell. That said, it is worth mentioning that the Atalanta Fed GDPNow estimate will be revised on Tuesday, before the GDP data are out.

As for the PCE numbers, the Fed’s favorite inflation metric is the core PCE index, whose correlation coefficient with the core CPI – taking into account the last 10 years – stands at 0.75. Therefore, given that the core CPI accelerated to 3.1% y/y from 2.9%, the risks for the core PCE index may be tilted to the upside. Therefore, more data suggesting sticky inflation could encourage more market participants to price out a second rate cut beyond September for this year.

This is likely to help the US dollar extend its recovery, while equities could drift lower as a slower pace of rate reductions could translate into lower present values for high-growth firms that are valued by discounting projected free cash flows.

Is the ECB done or are more rate cuts needed?

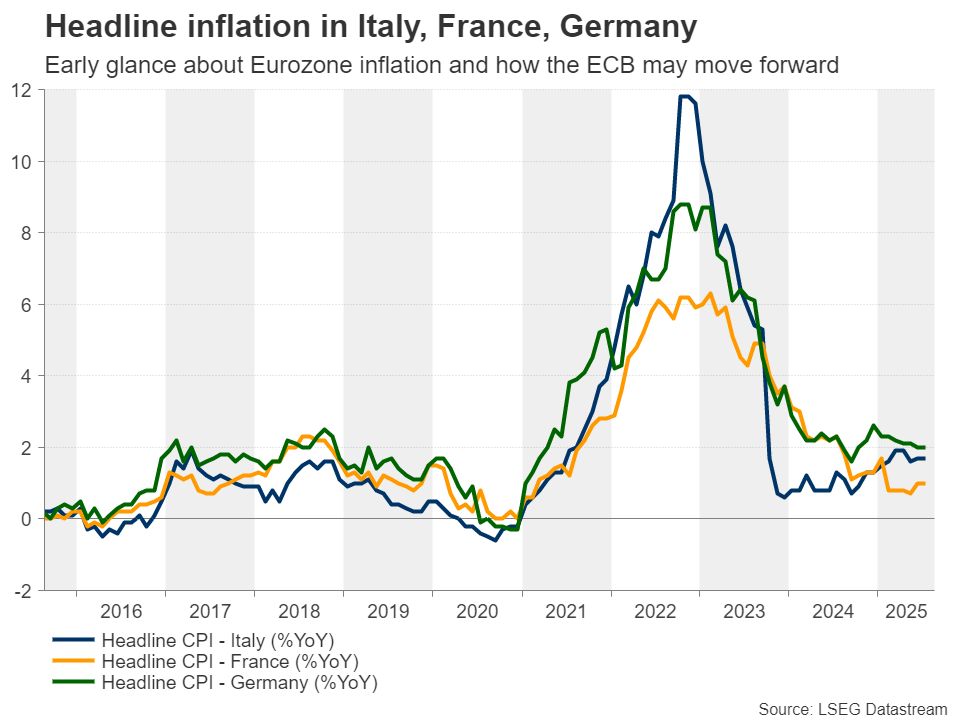

Turning to the Eurozone, the calendar includes the preliminary CPI numbers for August from Italy, France and Germany, set to be released on Friday. At its latest meeting, the ECB kept interest rates unchanged, while President Lagarde appeared more hawkish than expected at the press conference, which combined with the EU-US trade deal, raised speculation of a prolonged pause on interest rates.

Following the better-than-expected preliminary GDP data for Q2, the still-above-target core CPI rate, and the improving flash PMIs for August, investors are pricing in only 10bps worth of rate reductions by the end of the year. This translates into a 45% chance of another quarter-point cut by December. However, the market is not fully pricing in a 25bps cut even in 2026. Investors are just assigning a 72% chance that another cut might be delivered by June next year.

Having all that in mind, should preliminary inflation data from the Eurozone’s largest economies suggest that inflation is not further cooling, there may be no need for additional interest rate reductions should growth-related data continue to point to improvement. Euro traders may assign a smaller probability to another rate cut and the common currency may drift higher.

Tokyo CPIs enter the limelight as BoJ hike chances increase

Yen traders will also have to digest a bunch of Japanese data. During the Asian session on Friday, the Tokyo CPI figures for August will be published, alongside the nation’s unemployment rate, industrial production and retail sales for July.

This week, a former foreign minister who is rumoured to be among candidates for becoming a future prime minister, said that Japan must raise interest rates to strengthen the weak yen that has pushed up inflation and brought pain to households. This pushed the probability of another rate hike by the BoJ before year end higher, currently at 70%. Hence, accelerating Tokyo CPIs could take that probability higher and encourage investors to drive the yen higher, especially if the accompanying data also comes on the bright side.

Soft Canadian GDP to increase likelihood of BoC cut

Canada’s GDP for Q2 is also due to be released as the same time with the US core PCE numbers. The loonie was hurt earlier this week as the softness in Canada’s CPI data bolstered the case for further rate cuts by the BoC. Investors are currently assigning a 33% chance of a quarter-point reduction at the Bank’s upcoming gathering on September 17, with that probability rising to 90% in December. A soft GDP print may solidify the case of another reduction before year-end, thereby allowing some further loonie selling.

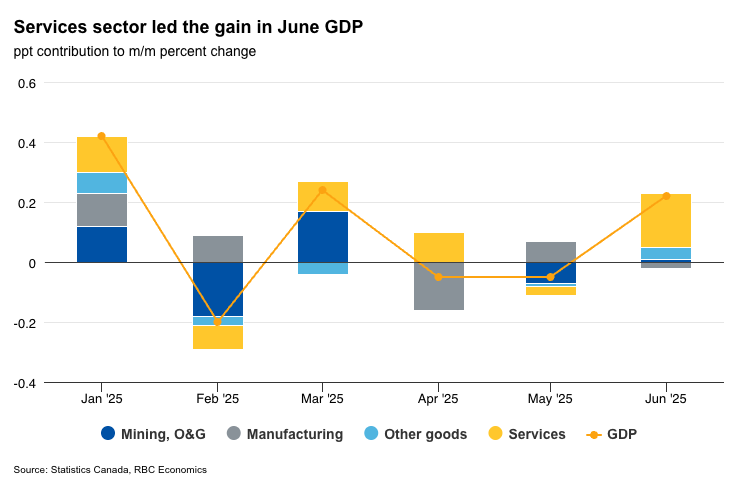

Canada’s Q2 GDP Growth Flat as Household Spending Offsets Trade Weakness

Canada’s gross domestic product report next Friday is expected to show zero growth in Q2─a sharp cooling from the 2.2% gain in Q1 this year.

Still, a flat reading in Q2 consistent with Statistics Canada’s advance estimates of monthly output through June is better than feared, given spring saw a surge in U.S. tariffs (and threats) that rattled business and consumer confidence.

These international trade disruptions have significantly impacted the economy. Canadian merchandise export volumes fell an annualized 31% in Q2 alongside a broader drop in U.S. imports as pre-tariff inventory building unwinds. Business investment likely edged down modestly and would have been substantially weaker without a large ($2 billion) one-time import of machinery for offshore oil production in June.

Household demand stays on course

Household spending, however, held steady with consumer spending tracking a similar pace to Q1’s 1.2% increase. A bounce back in home resales and housing starts also signals an increase in residential investment. Total final domestic demand, which strips out volatile swings in trade and inventories, should post a small gain─suggesting underlying momentum is not as weak as the headline implies.

We expect GDP to post a slightly stronger 0.2% month-over-month increase in June than StatsCan’s 0.1% estimate, marking the first increase in three months following small declines in April and May.

Early indicators also point to a rise in output in service producing industries in June. Retail sales rebounded strongly (+1.5%) following a 1.2% drop in May, consistent with our tracking of RBC consumer card transactions that showed spending held up in Q2 despite the sharp drop in consumer confidence. The real estate sector extended its recovery as housing resales improved through the quarter.

Oil production to boost output

The manufacturing sector continues to be among the industries more significantly impacted by international trade disruptions, and uncertainty. We expect output in the sector to be broadly consistent with flat manufacturing sale volumes reported. But oil production likely bounced back after wildfire-related disruptions in Alberta in May.

Trade uncertainty will continue to affect business investment regardless of future tariff decisions. Nevertheless, CUSMA exemptions for most Canadian exports have prevented worst case scenarios, and we anticipate subdued, but positive growth through the remainder of 2025.

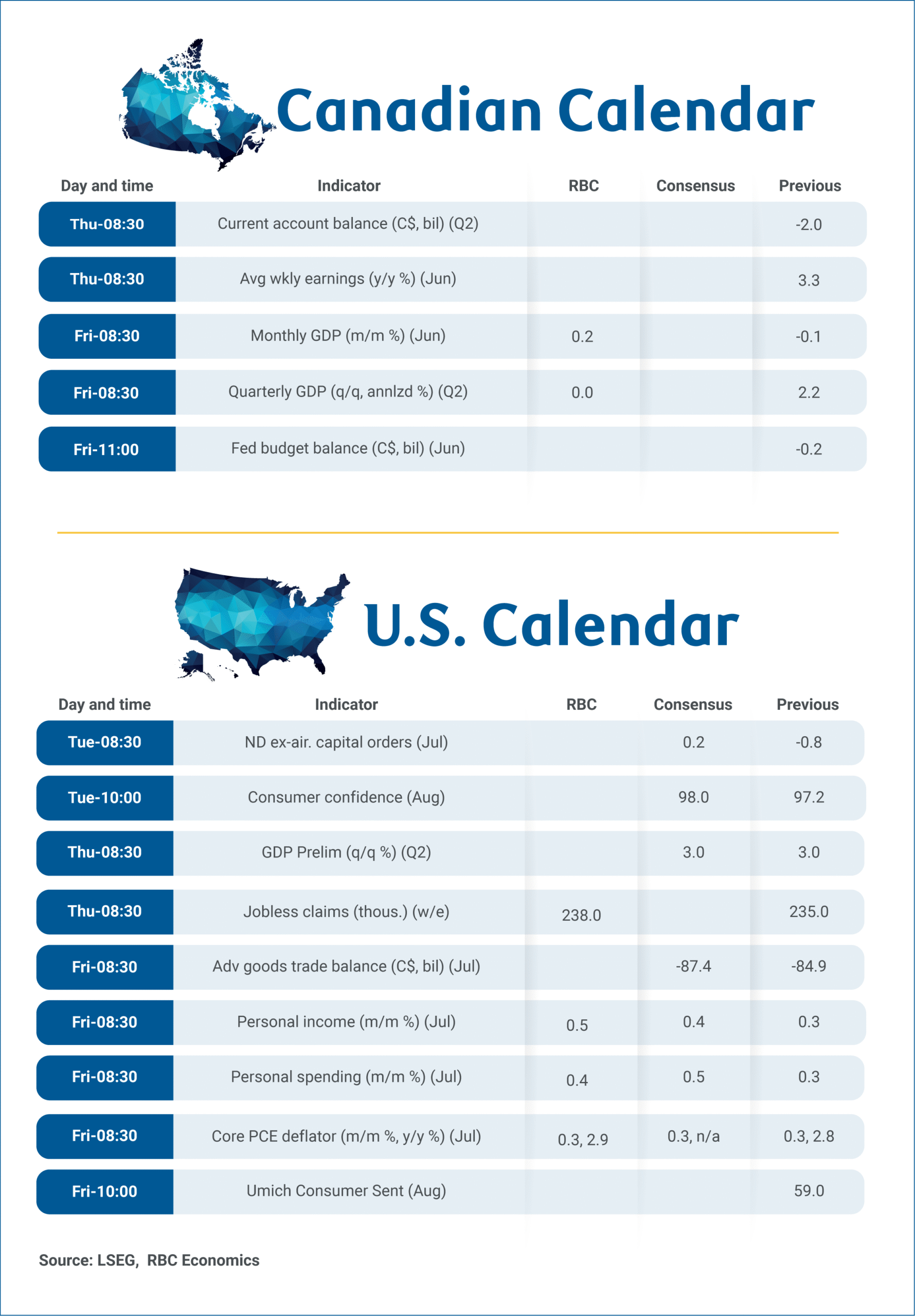

Week ahead data watch:

U.S. personal spending in July likely increased by 0.4%, slightly higher than the previous month. Much of this growth came from stronger auto sales. Additionally, retail sales rose by 0.5% in July, following a larger 0.9% increase in June. We also expect personal income to rise from 0.3% in July to 0.5%, reflecting the higher wage growth reported in the July payroll data.