Sample Category Title

Bitcoin Price Climbs Back Above $120k

Over the weekend, the value of the leading cryptocurrency rose significantly. While the BTC/USD rate closed around $116.6k on Friday, today Bitcoin is trading above $120k and is nearing a potential new all-time high.

Since its August low, the price has increased by approximately 9%.

Why Bitcoin is Rising Today

From a fundamental perspective, this growth may be driven by:

→ Expectations ahead of tomorrow’s key US inflation data release (CPI report due at 15:30 GMT+3);

→ Donald Trump’s decision to allow pension and other funds to include cryptocurrencies and other alternative assets in their portfolios. Analysts believe the presidential decree could trigger a fresh wave of capital inflows into Bitcoin.

BTC/USD Technical Analysis

Last week, when analysing Bitcoin’s price, we extended the long-term blue ascending channel and:

→ Marked an intermediate descending channel with red lines;

→ Highlighted the importance of the $116k level.

The latest data shows that:

→ The $116k level has shifted from resistance to support (as indicated by the arrow);

→ The descending channel acted as a Bull Flag pattern — a temporary correction within the prevailing upward trend.

What’s Next for BTC/USD?

It is possible that the bullish momentum will be sufficient for the price to attempt surpassing its previous all-time high this week. However, such a move could push the market into an even more overbought state (the RSI indicator is already above 70).

So, BTC/USD could aim for the upper boundary of the blue channel, while forming short-term corrections along the way — for example, retesting the psychological $120k mark (recently breached by a strong bullish candle and potentially serving as important support going forward).

It is worth noting that analysts at the on-chain options research platform Dervie expect Bitcoin to reach $150,000 by year-end.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

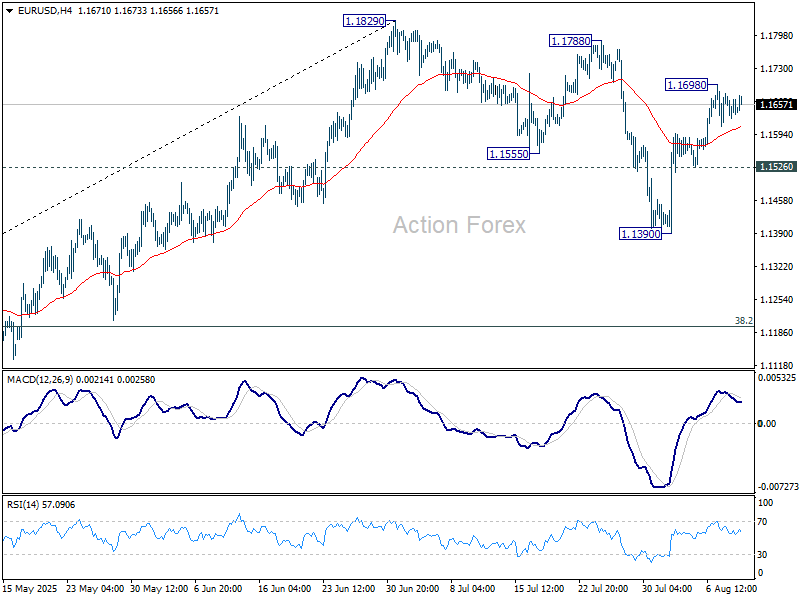

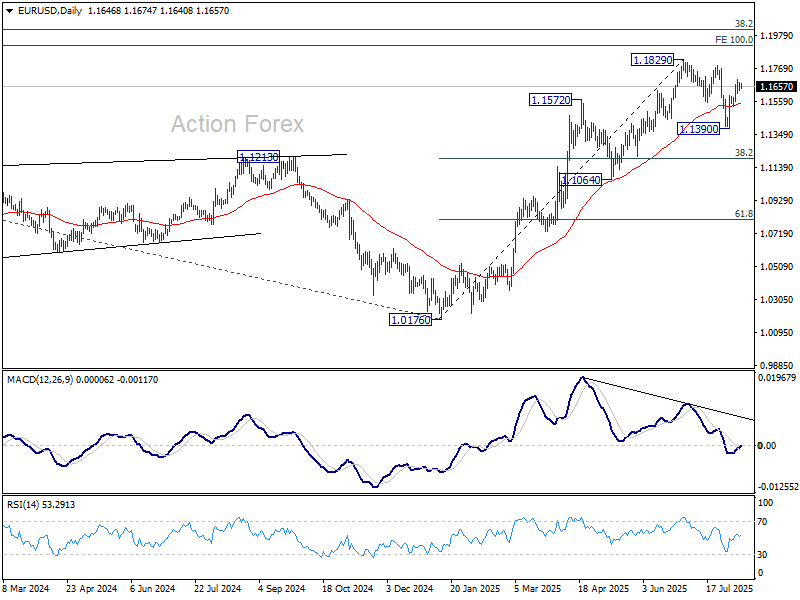

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1621; (P) 1.1650; (R1) 1.1671; More...

Intraday bias in EUR/USD remains neutral first. Outlook is unchanged that correction from 1.1829 should have completed with three waves down to 1.1390. Above 1.1698 will bring retest of 1.1829. However, break of 1.1526 support will dampen this bullish view and bring deeper fall back to 1.1390 instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

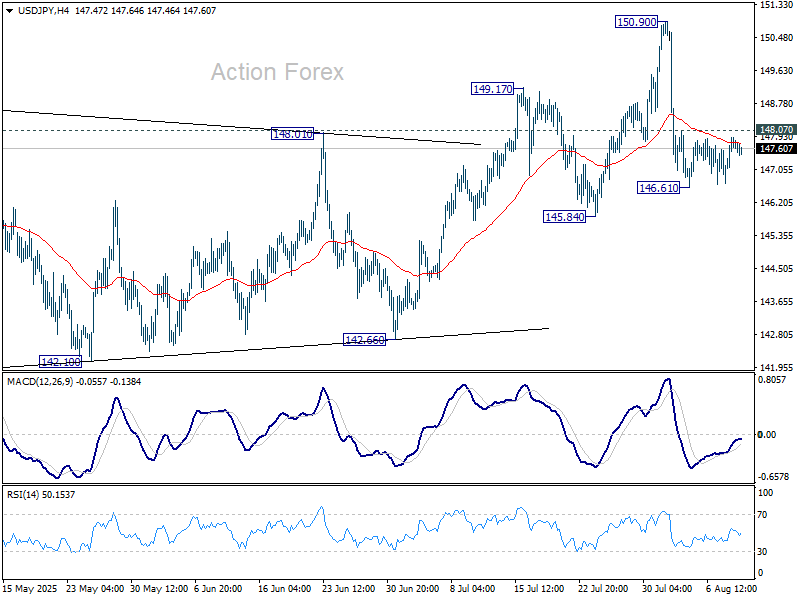

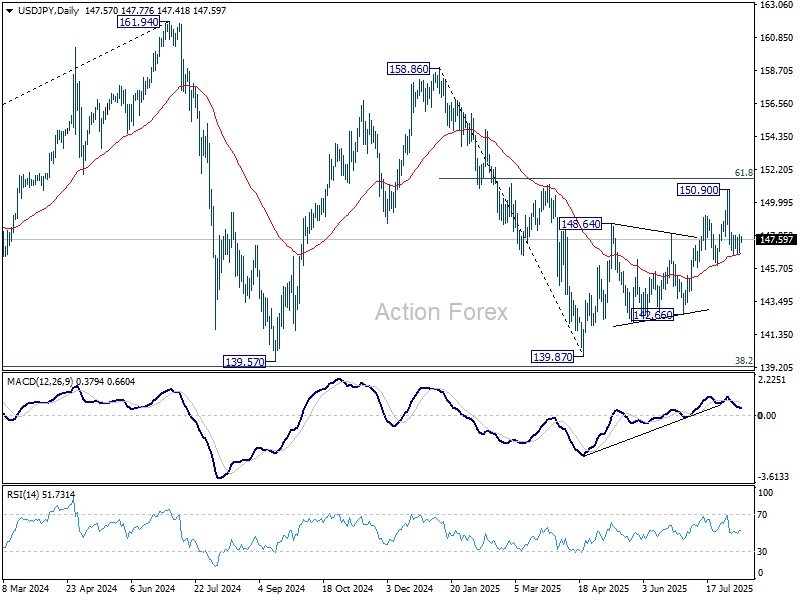

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.00; (P) 147.45; (R1) 148.18; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. As long as 145.84 support holds, larger rebound from 139.87 is still expected to continue. On the upside, above 148.07 minor resistance will bring retest of 150.90 high first. However, decisive break of 145.84 will indicate near term bearish reversal and target 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

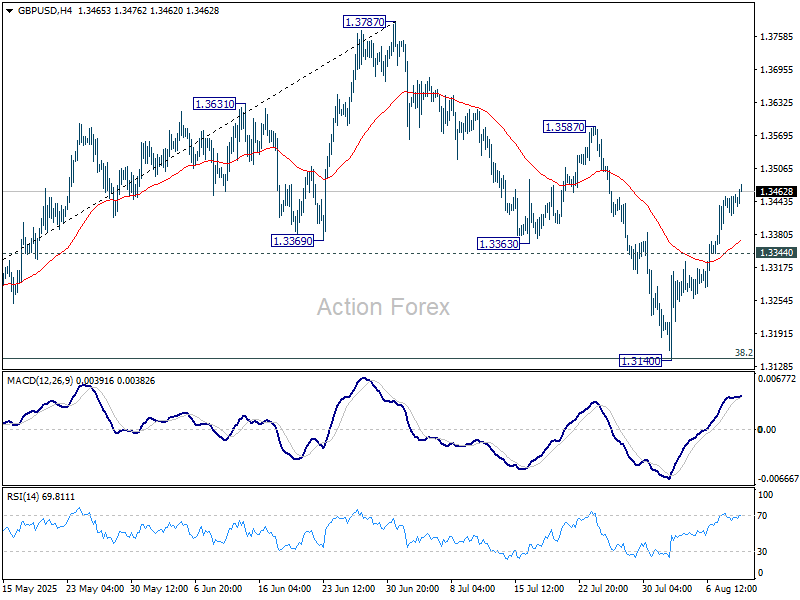

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3426; (P) 1.3442; (R1) 1.3467; More...

Intraday bias in GBP/USD stays on the upside this point. Correction from 1.3787 should have completed with three waves down to 1.3140. Further rally should be seen to 1.3587 resistance first. Firm break there will pave the way to retest 1.3787 high. However, break of 1.3344 minor support will dampen this bullish case and turn bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3055) holds, even in case of deep pullback.

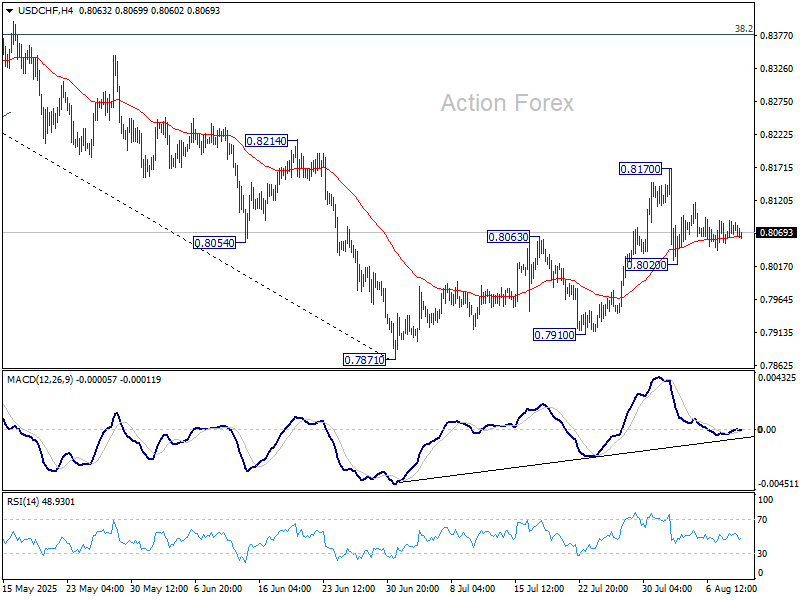

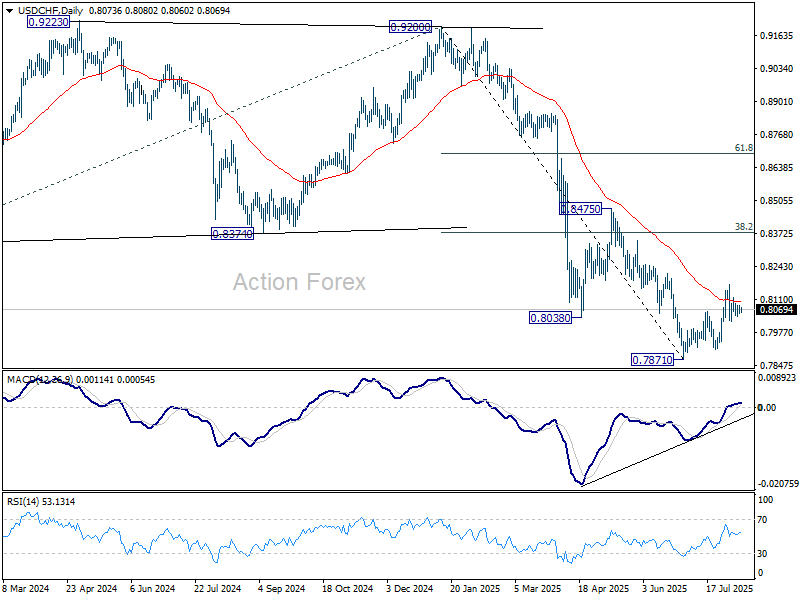

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8061; (P) 0.8075; (R1) 0.8098; More….

Intraday bias in USD/CHF stays neutral for the moment. On the downside, break of 0.8020 will solidify the case that corrective pattern from 0.7871 has completed at 0.8170. Further fall should be seen back to retest 0.7871 low. However, break of 0.8710 will resume the corrective rise towards 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

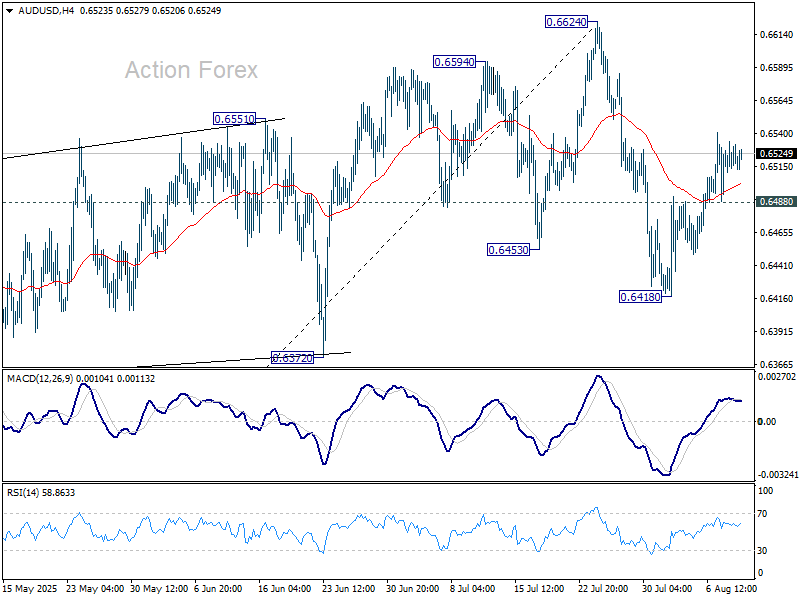

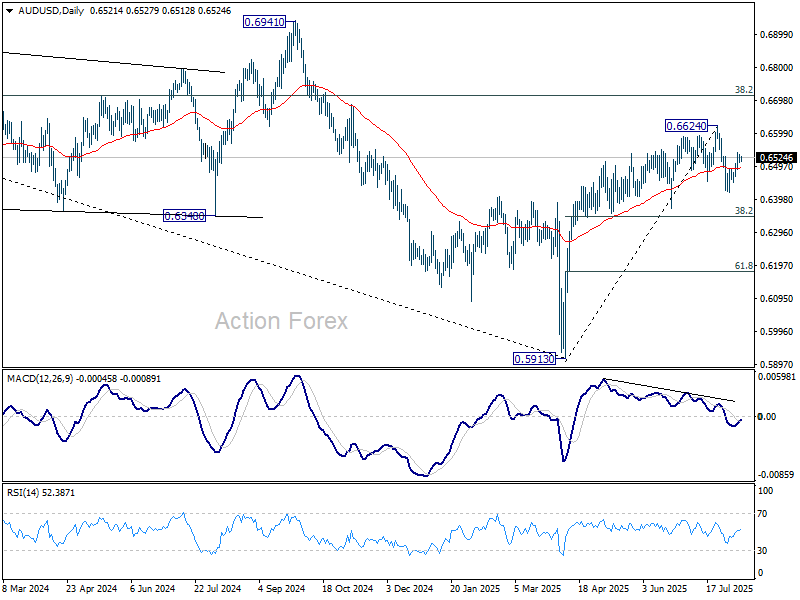

AUD/USD Daily Report

Daily Pivots: (S1) 0.6508; (P) 0.6522; (R1) 0.6536; More...

Intraday bias in AUD/USD remains mildly on the upside at this point. Corrective fall from 0.6624 could have completed at 0.6418 already. Further rise would be seen to retest this high. On the downside, however, firm break of 0.6449 will argue that the pattern from 0.6624 is extending with another falling leg. Break of 0.6418 will target 38.2% retracement of 0.5913 to 0.6624 at 0.6352.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

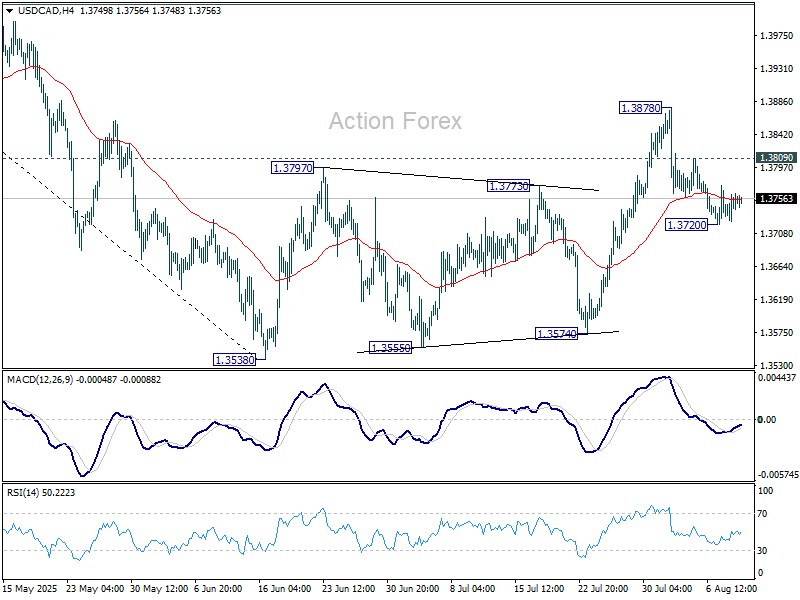

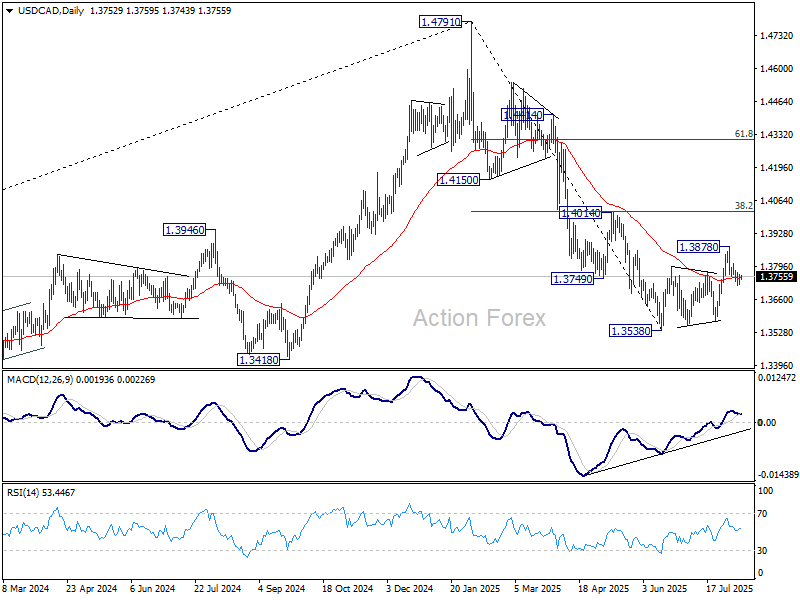

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3733; (P) 1.3748; (R1) 1.3771; More...

Intraday bias in USD/CAD remains neutral at this point. On the downside, break of 1.3720 will reaffirm the case that corrective pattern from 1.3538 has completed at 1.3878. Further decline should then be seen back to retest 1.3538 low. However, break of 1.3809 will bring retest of 1.3878. Further break there will extend the corrective rebound from 1.3538 with another rising leg.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

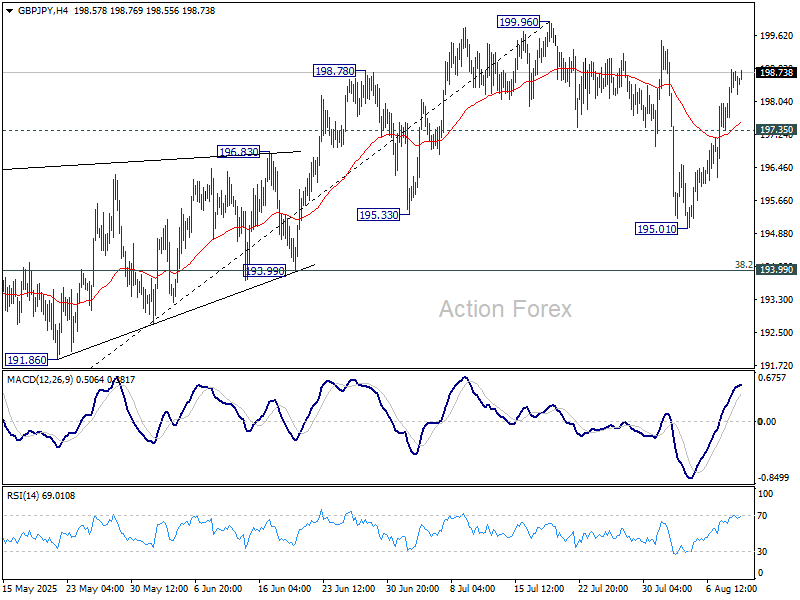

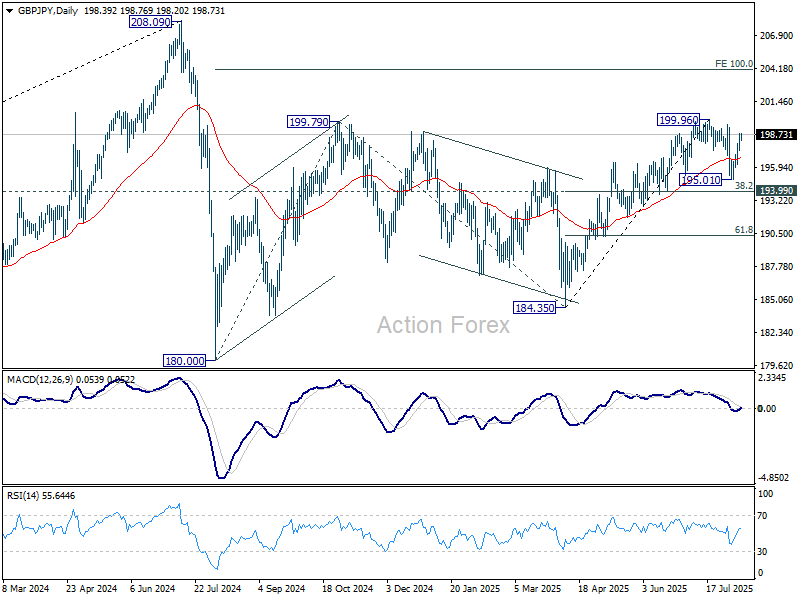

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.75; (P) 198.29; (R1) 199.20; More...

Intraday bias in GBP/JPY stays on the upside for retesting 199.96 resistance first. Decisive break there resume whole rise from 184.35. Next target is 100% projection of 180.00 to 199.79 from 184.35 at 204.14. On the downside, below 197.35 minor support will delay the bullish case and turn intraday bias neutral again. In this case, corrective pattern from 199.96 would extend with another falling leg.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

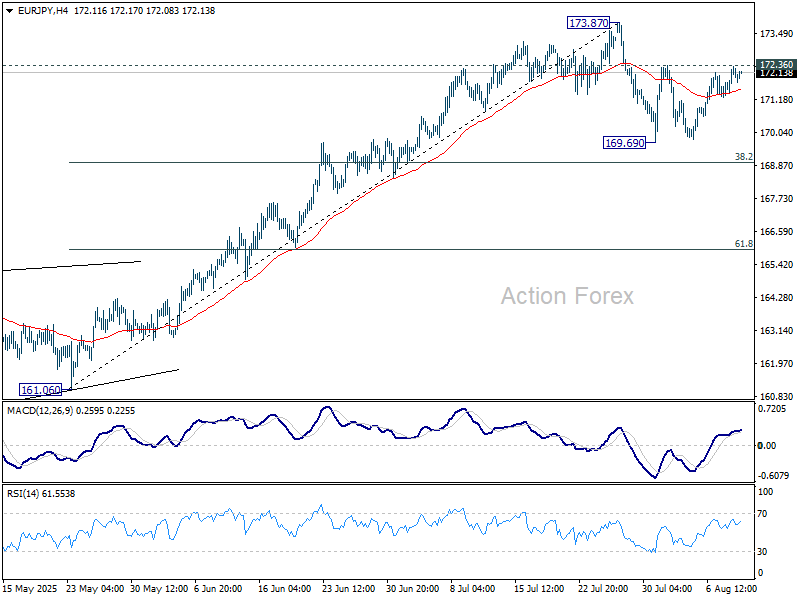

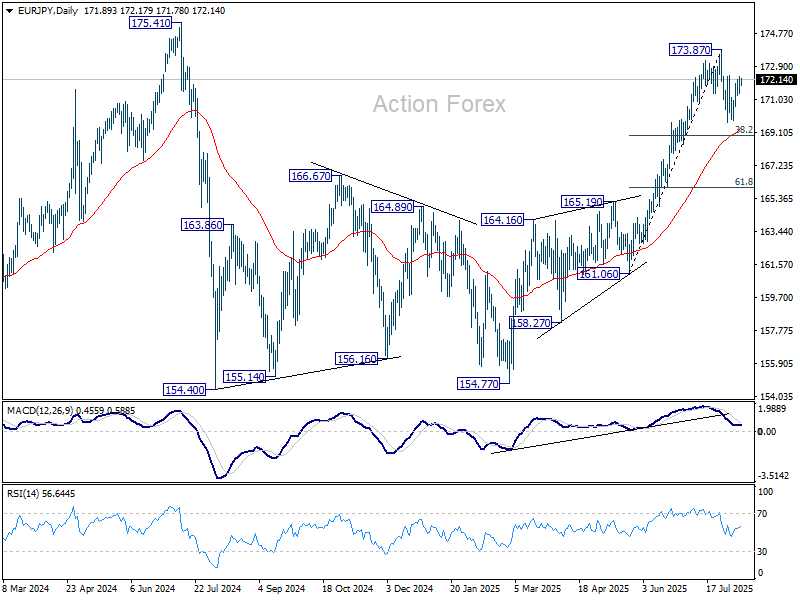

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.46; (P) 171.91; (R1) 172.44; More...

Intraday bias in EUR/JPY stays neutral as range trading continues. Corrective pattern from 173.87 could extend lower. But downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to bring rebound. On the upside, above 172.36 will bring retest of 173.87 first. Firm break there will resume larger rally from 154.77 to retest 175.41 high.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.27) will delay this bullish case.

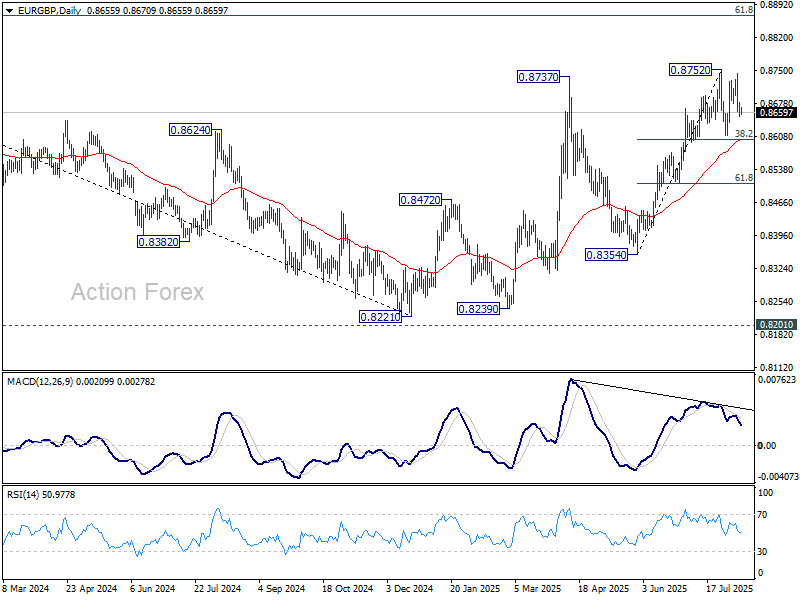

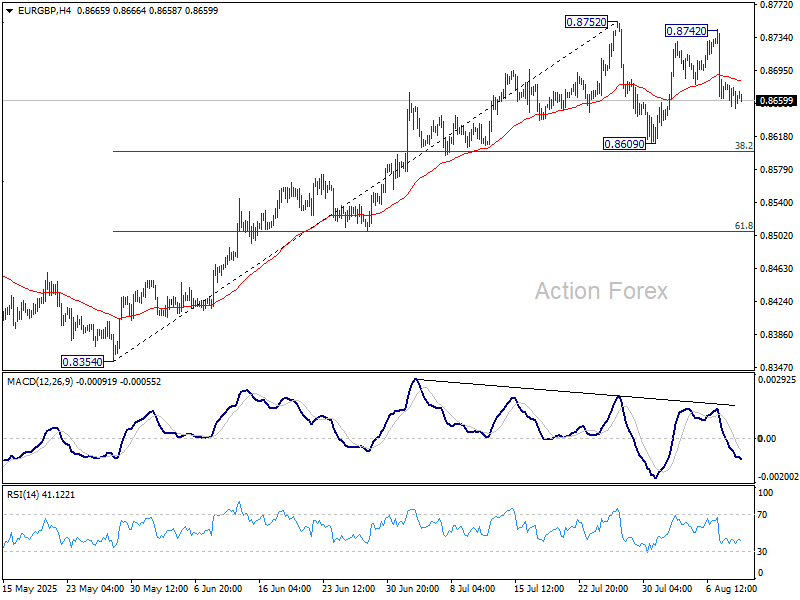

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8645; (P) 0.8664; (R1) 0.8675; More...

Consolidation from 0.8752 short term top is still extending and intraday bias in EUR/GBP remains neutral. Downside should be contained by 38.2% retracement of 0.8354 to 0.8752 at 0.8600. On the upside, firm break of 0.8752 will resume the rise from 0.8354 towards 0.8867 fibonacci level.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8497) holds.