Sample Category Title

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.16; (P) 172.59; (R1) 172.94; More...

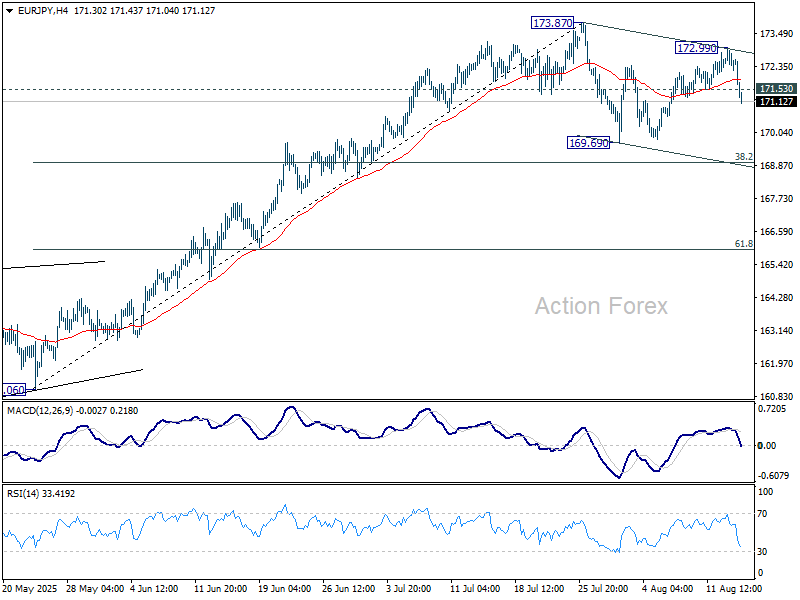

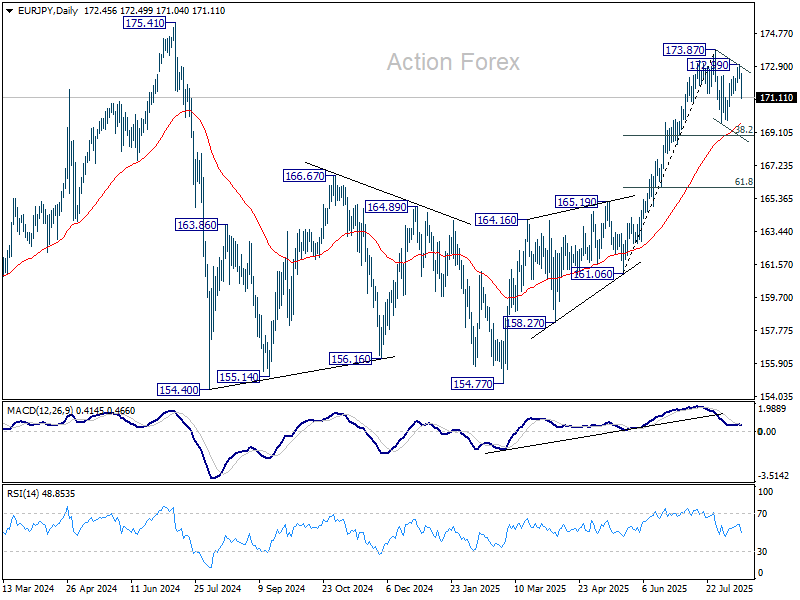

EUR/JPY's steep decline and strong break of 171.53 support suggests that rebound from 169.69 has completed. Corrective pattern from 173.87 is extending with fall from 172.99 as the third leg. Intraday bias is back on the downside for 169.69. Strong support is expected from 38.2% retracement of 161.06 to 173.87 at 168.97 to complete the pattern. On the upside, above 172.99 will bring retest of 173.87.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.64) will delay this bullish case.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7855; (P) 1.7887; (R1) 1.7912; More...

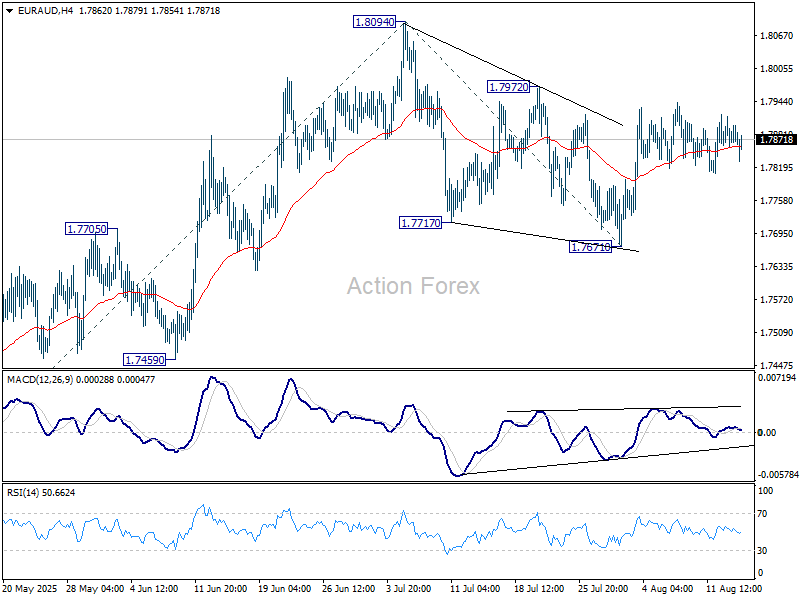

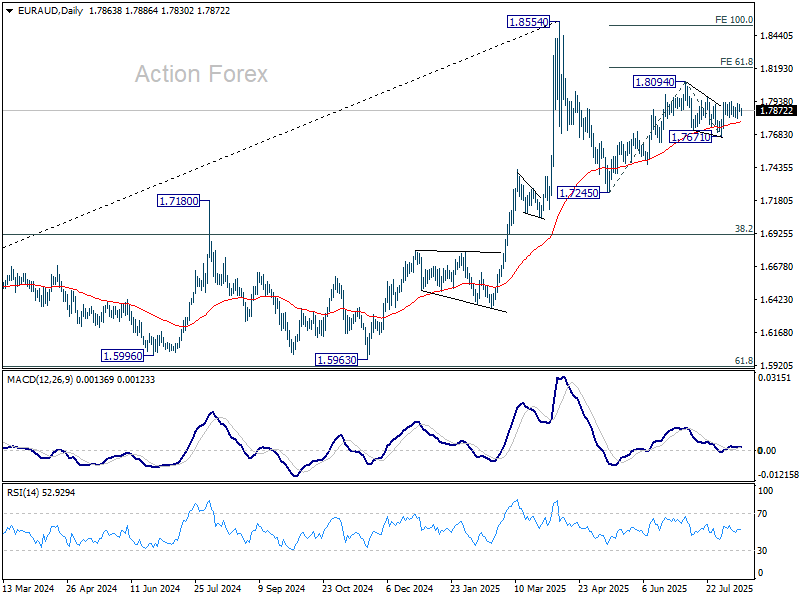

Intraday bias in EUR/AUD remains neutral as sideway trading continues. On the upside, firm break of 1.7972 resistance should confirm that corrective pattern from 1.8094 has completed at 1.7671. Further rise should then be seen through 1.8094, to resume the rebound from 1.7245. Next target is 61.8% projection of 1.7245 to 1.8094 from 1.7671 at 1.8196. On the downside, below 1.7671 will bring deeper fall back to 1.7459 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

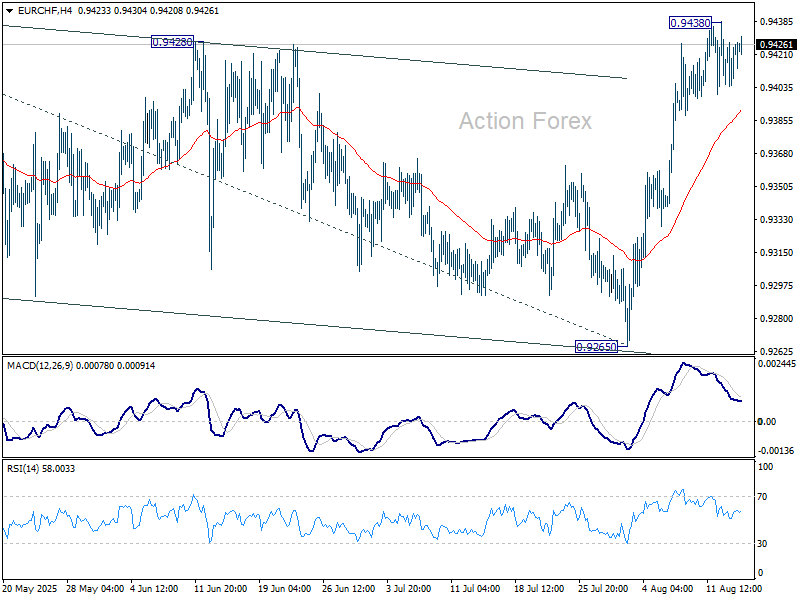

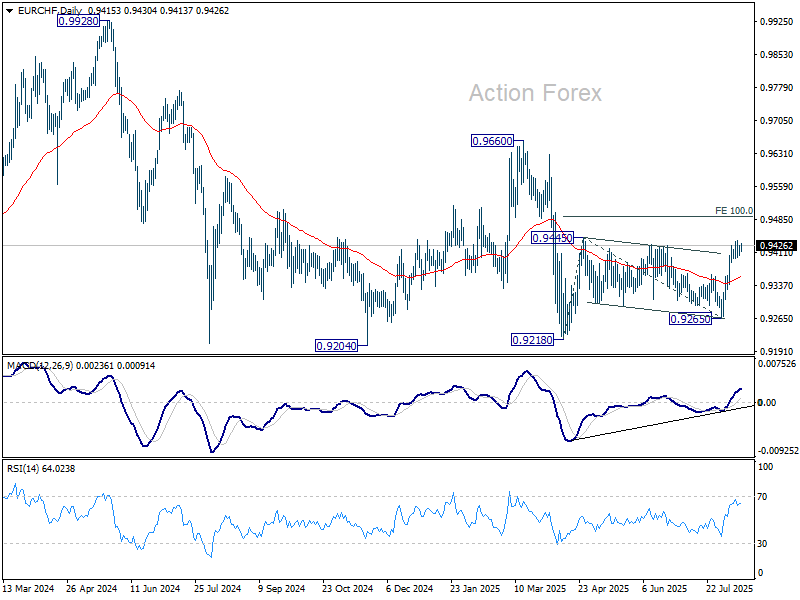

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9413; (P) 0.9421; (R1) 0.9438; More....

Intraday bias in EUR/CHF stays neutral and some more consolidations could be seen below 0.9438 temporary top. On the upside, decisive break of 0.9445 resistance will resume the whole rebound from 0.9218. Next target is 100% projection of 0.9218 to 0.9445 from 0.9265 at 0.9492. However, sustained trading below 55 4H EMA (now at 0.9391) will extend the corrective pattern from 0.9445 with another falling leg.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside position should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

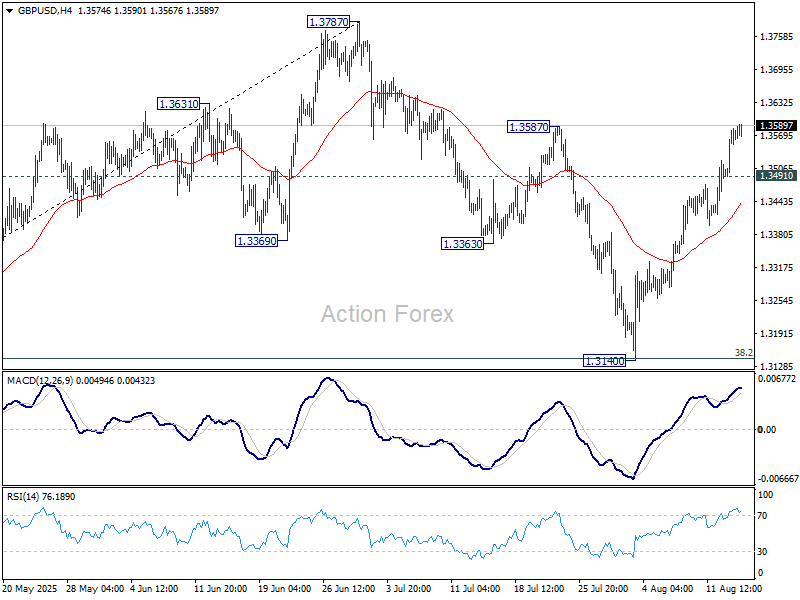

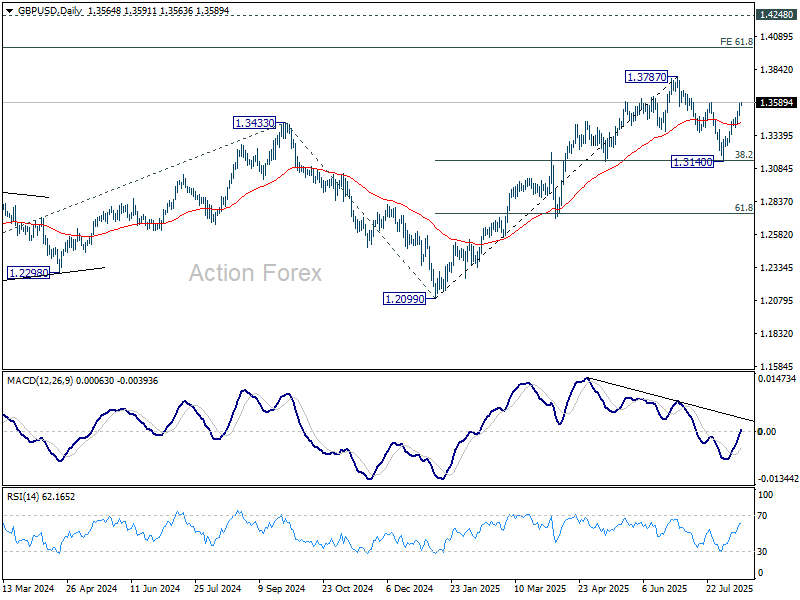

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3518; (P) 1.3551; (R1) 1.3610; More...

Intraday bias in GBP/USD remains on the upside as rise from 1.3150 continues. Firm break of 1.3587 resistance will bring retest of 1.3787 high. On the downside, below 1.3491 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3068) holds, even in case of deep pullback.

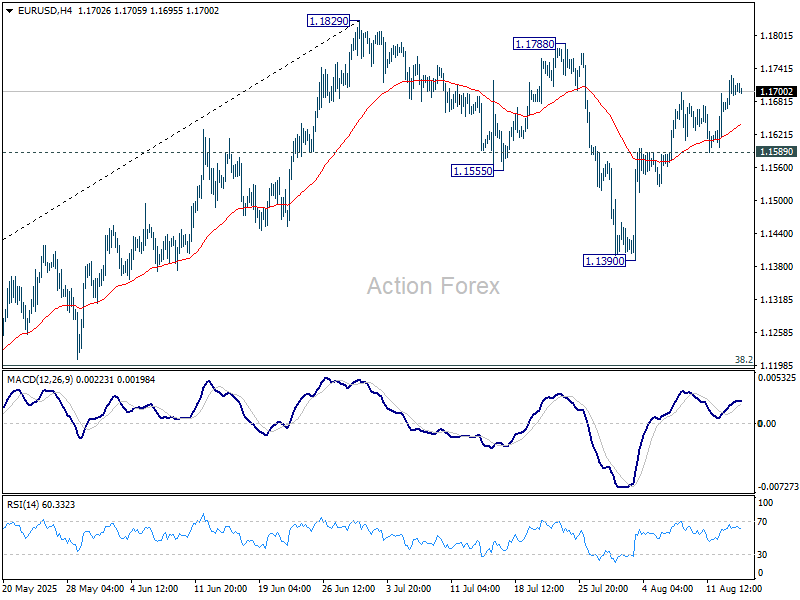

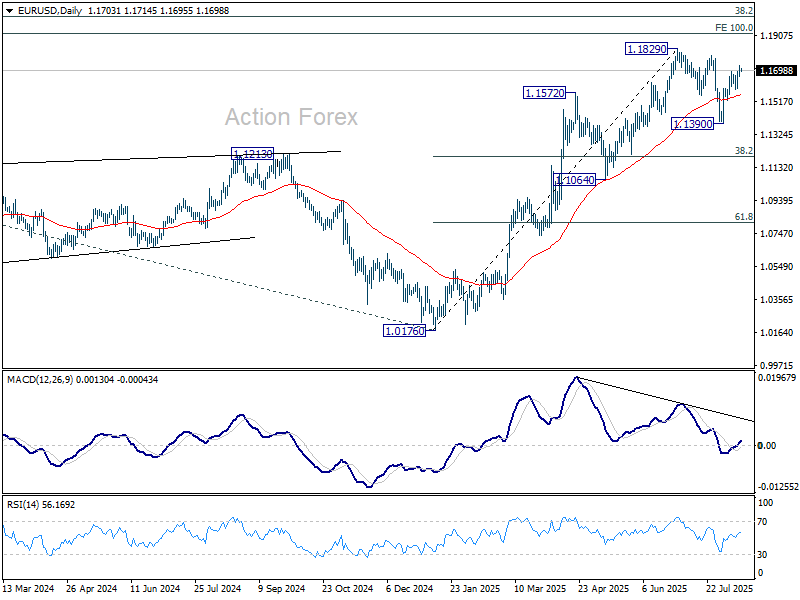

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1673; (P) 1.1701; (R1) 1.1734; More...

Intraday bias in EUR/USD remains up the upside for retesting 11829 high. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, however, break of 1.1589 support will delay the bullish case and extend the corrective pattern from 1.1829 with another falling leg.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

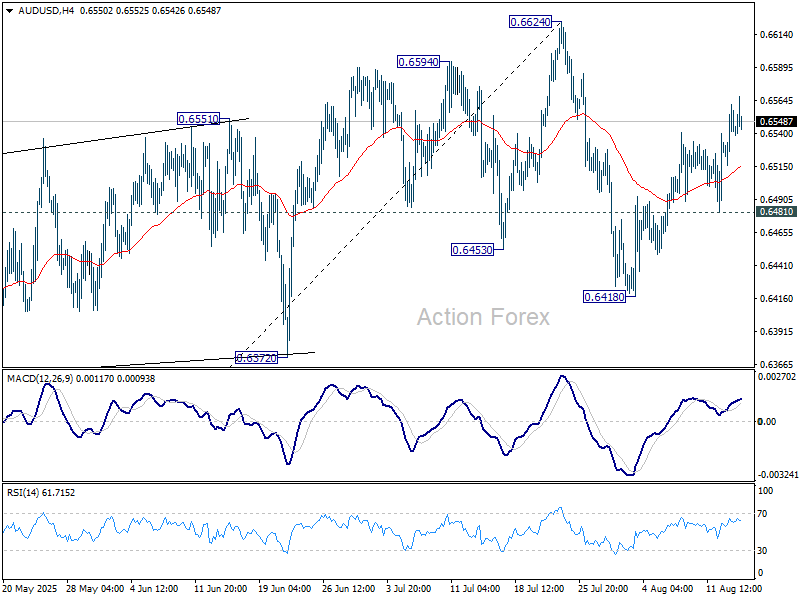

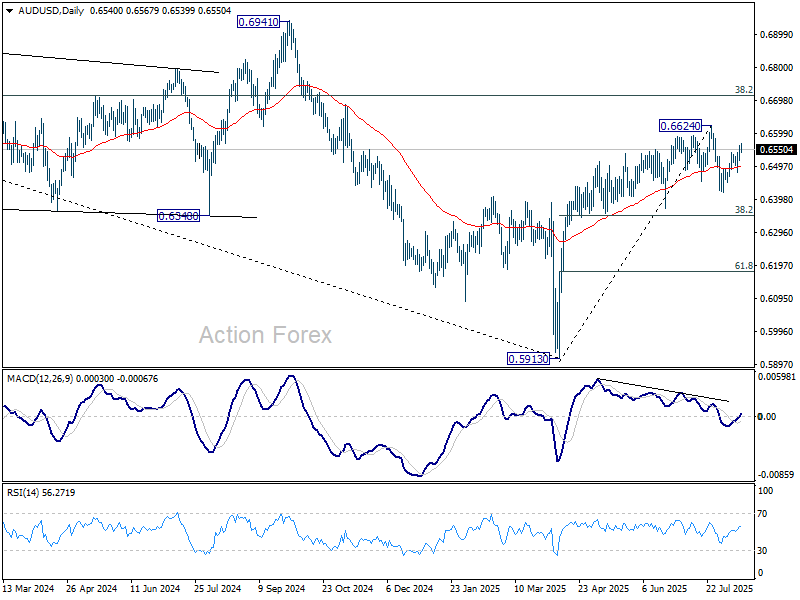

AUD/USD Daily Report

Daily Pivots: (S1) 0.6520; (P) 0.6542; (R1) 0.6567; More...

Intraday bias in AUD/USD stays on the upside as rebound from 0.6418 s in progress. Further rise should be seen back to retest 0.6625 high. Overall, price actions from 0.6624 are seen as a corrective pattern that might still extend. On the downside, break of 0.6481 will suggest that it's in the third leg and bring deeper fall to 0.6418 first.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

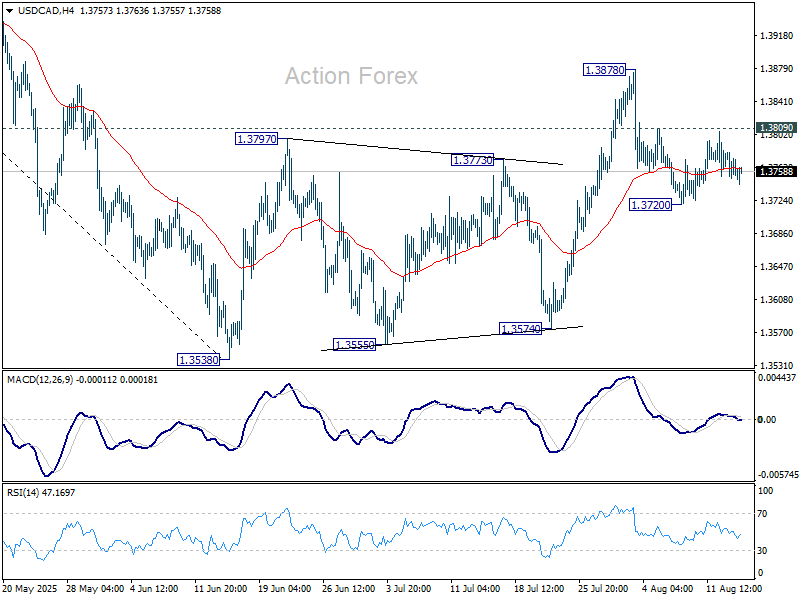

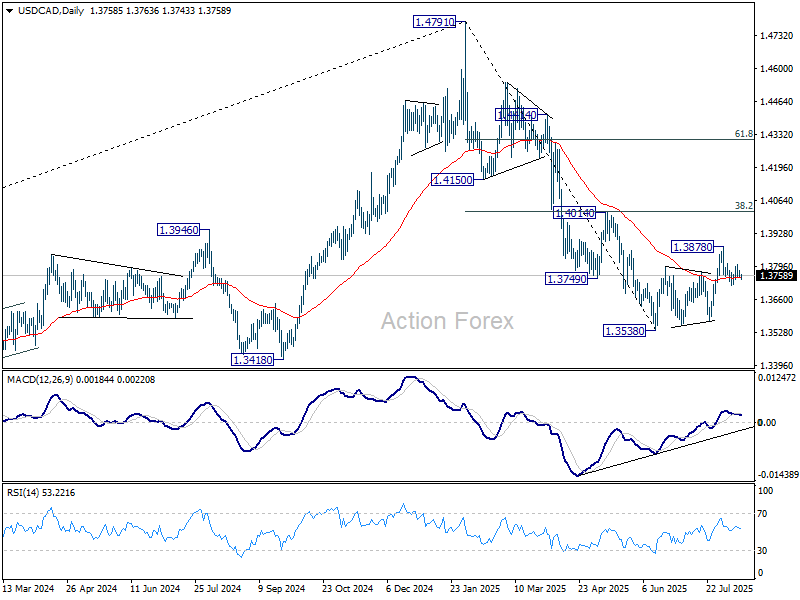

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3747; (P) 1.3765; (R1) 1.3777; More...

Intraday bias in USD/CAD stays neutral for the moment. On the downside, break of 1.3720 will reaffirm the case that corrective pattern from 1.3538 has completed at 1.3878. Further decline should then be seen back to retest 1.3538 low. However, break of 1.3809 will bring retest of 1.3878. Further break there will extend the corrective rebound from 1.3538 with another rising leg.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

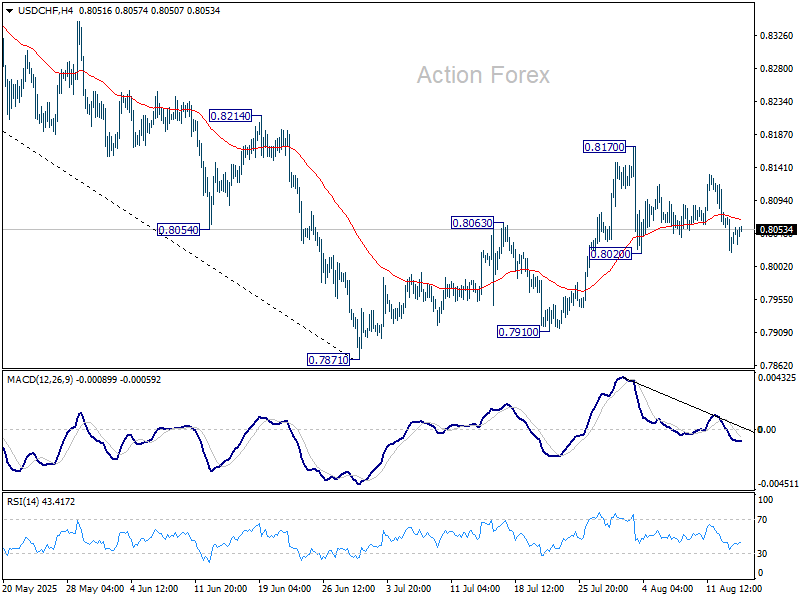

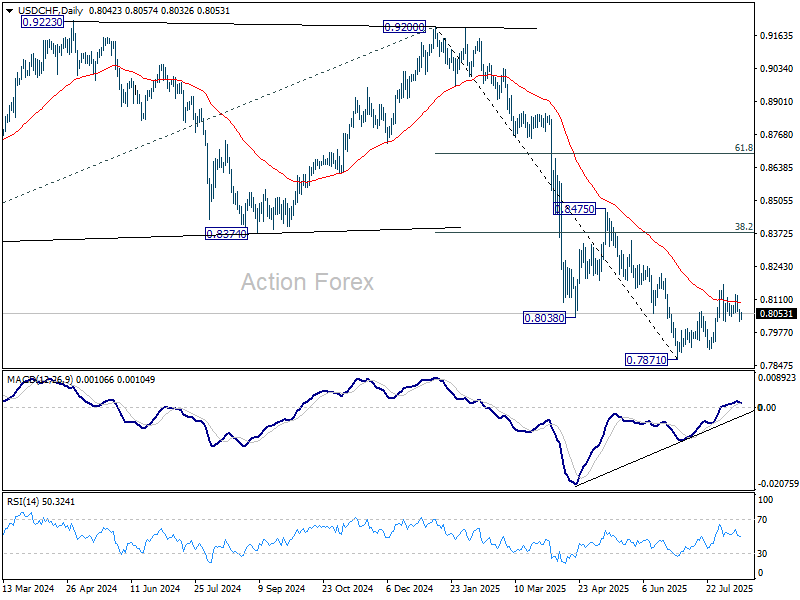

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8028; (P) 0.8051; (R1) 0.8081; More….

Intraday bias in USD/CHF remains neutral as it's still bounded in range of 0.8020/8170. On the downside, break of 0.8020 will revive that case that the corrective pattern from 0.7871 has completed, and target a retest on 0.7871 low. On the upside, firm break of 0.8710 will resume the corrective from 0.7871. Intraday bias will be back on the upside for 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

Once Fed Engages to Additional Rate Cuts, They Should/Could Opt for a Bigger Start

Markets

An interview with US Treasury Secretary Bessent got full coverage thanks to an otherwise empty economic agenda. He suggested that the Fed should cut rates by 50 bps in September given lack of evidence of significant tariff-related inflation and following significant downward revisions to June and May payrolls data. Bessent thinks that the Fed probably already pulled the trigger if data would have been more accurate. He sees scope for the Fed funds target range to fall by 150-175 bps. While we don’t side with the total magnitude of policy easing, we do side with the argument that once the Fed engages to additional rate cuts, they should/could opt for a bigger start. The Powell Fed has a history of waiting until they are absolutely convinced about something and then opting to move quickly. In this respect, it’s telling that US money markets in the wake of the Bessent interview for the first time discounted more than a 25 bps rate cut in September. It even triggered hawkish comments by Chicago Fed Goolsbee (voter) who warned against being lurched into action especially given persisting services inflation. We’d err on the side of the dovish positioning to be extended though if today’s (producer price inflation, weekly jobless claims) or tomorrow’s (retail sales, empire manufacturing survey, University of Michigan consumer confidence) data shows signs of weakness. US Treasuries rallied yesterday with the curve moving lower in a parallel shift (5-6 bps across). We continue to prefer steepening going forward. EUR/USD closed above 1.17 for the first time since end July with the YtD top at 1.1829 being the reference. The approaching Alaska summit between US president Trump and Russian president Putin is a wildcard for trading.

News & Views

Australian labour market data for the month of July came out near consensus this morning. Employment rose by 24.5k (from +2k in June and vs +25k consensus). The full-time/part-time breakdown was opposite to last month. More pronounced gains in full-time occupations (+60.5k) were partly offset by a 35.9k decline in part-time jobs. The unemployment rate ticked lower (4.3% to 4.2%) but the participation rate (67.1% to 67%) did the same thing. The female employment-to-population ratio and participation rate reached 60.9% and 63.5% respectively, both new historical highs. In a separate release, the Australian Bureau of Statistics indicated that average weekly ordinary time earnings for full-time adults has been greater than A$2000 for the first time ever in May (A$2010). Annual wage growth remained high at 4.5%. The solid labour market report strengthens the view that the Reserve Bank of Australia can take a gradual normalization approach going forward after lowering its policy rate by 25 bps to 3.6% earlier this week. Money markets favour a skip at the next, September, meeting followed by a 25 bps rate cut in November. They see room for one more additional move after that early next year. The Aussie dollar briefly profited from the labour numbers, but couldn’t hold on to gains. AUD/USD (0.6550) is locked in a trading range between roughly 0.64 and 0.66.

The UK Royal Institution of Chartered Surveyors (RICS) released its July Residential Market Survey. Sales market conditions remain challenging with previous signs of recovery faltering somewhat. Measures of demand (new buyer enquiries – 6 from +4) and agreed sales (-16 from -4) slipping back into negative territory. Meanwhile, forward-looking sentiment now points to a largely flat picture for activity in the near-term (1 from 7). At the 12-month time horizon, sentiment is a little more positive, with a net balance of +8% of contributors anticipating a pick-up in sales activity. Supply indicators point at marginal growth when it comes to new listings on the market and a flatter pipeline for new instructions moving forward. House price indicators signalled a small downward adjustment in average house prices across the country. Over the coming three months, respondents expect prices to remain under a small degree of downward pressure. The 12-month outlook however thus suggest and increase in prices.

US PPI Could Douse Overheated Fed Cut Bets

Investors spent Wednesday betting that the Federal Reserve (Fed) would not only cut rates by 25bp in September but could even deliver a jumbo rate cut, after CPI data released the day before came in softer than analysts expected. Fed doves now see a huge opportunity for the central bank to focus on the slowing jobs market rather than tariff-led inflation risks that have yet to materialise. Fed funds futures currently price around a 95% probability of a 25bp cut and 5% for a 50bp cut. Bets that the Fed would hold off due to inflation risks are now largely off the table. According to Bessent, US rates should be 150–175bp lower.

Diving deeper: Scott Bessent also said that the unique model Trump put in place — forcing a 15% cut from Nvidia and AMD’s Chinese businesses — could serve as a blueprint for other industries. While the approach may make the US government look like a mafia organisation, it would have a major impact in controlling the exploding US debt. In theory, that could mean lower sovereign bond issuance and, over time, reduced long-term borrowing costs. That would be good for companies and valuations — though it would come with a price tag. Bonds reacted positively with the downside pressure on yields coming primarily from dovish Fed expectations. The US 2-year yield is now testing its August lows; the 10-year is steady around 4.23% — well below the 4.50–5.00% range that some have framed as the new normal amid structurally higher long-term inflation bets. The US dollar index has fallen for a third straight session, while Bitcoin hit a fresh record.

Today’s US PPI figures could cool overheated dovish Fed bets, as both headline and core readings are expected to tick higher on tariff costs. If that’s the case, some of the more aggressive bets — especially the 50bp camp — could be reversed by week’s end. Delivering a jumbo cut amid inflation uncertainty could risk a repeat of last September’s market backlash. A 25bp move would likely deliver a steadier, more predictable reaction. Also, Bessent believes the Bank of Japan (BoJ) is ‘behind the curve’ in addressing inflation and should hike. The USDJPY dropped to test its 50-day moving average and the Nikkei fell 1%.

In US equities, rising rate-cut expectations pushed the S&P 500 and Nasdaq to fresh all-time highs yesterday. The equal-weight S&P 500 narrowed its gap with the original, tech-heavy version. Nvidia slipped after CoreWeave — a ‘neo-cloud’ provider backed by Nvidia and with Microsoft and OpenAI among its biggest customers — posted a larger-than-expected Q2 loss. But the loss was mainly due to higher spending and acquisitions to expand capacity quickly enough to meet demand. Revenue beat expectations by a wide margin at $1.20 billion versus $1.08 billion forecast. While volatile, CoreWeave’s drop may look attractive to investors betting that today’s losses are investments for tomorrow’s bigger gains.

The rally in small- and mid-cap stocks, which began after the August jobs report, is gaining momentum on dovish Fed expectations. Lower borrowing costs are especially important for smaller firms struggling with higher tariff-driven costs. That could pull money out of tech — which acted as a safe haven amid tariff and rate uncertainty — and into more rate-sensitive corners of the market.

The million-dollar question: could a premature, outsized cut reignite inflation and backfire? I have no answer. The new BLS chief will no doubt find ways to make the data look ‘not too bad.’

If the US tech rally fades, diversification may be prudent. The Stoxx 600 could catch up after its summer stall caused by tariff issues, though upside is likely capped given limited further potential in defence stocks that drove H1 gains.

Japanese equities — especially the tech-heavy Topix — remain a hot pick. Despite Bessent’s critics, the BoJ will likely support the economy against US disruptions. Meanwhile, Chinese equities remain strong on a stable flow of trade headlines. Mainland-listed firms are on track for 5% profit growth in Q2, rising to 13% for overseas-listed peers. Tencent beat expectations last quarter thanks to AI-driven segments, while Alibaba’s Cloud Intelligence Group posted triple-digit growth in AI-related product revenue, delivering 18% year-on-year growth. The Nasdaq Golden Dragon China index jumped 2% yesterday and is up nearly 30% since its April low, with room for further gains on supportive policy and growing AI demand.