Sample Category Title

RBA minutes: Case for easing intact, but timing still debated

Minutes from the RBA’s July 7–8 meeting reveal a Board broadly aligned on the view that there will be "some additional reduction in interest rates over time". Yet, the board is divided on the "appropriate timing and extent of further easing". The majority ultimately judged it prudent to keep the cash rate steady at 3.85%.

The decision to hold reflected stronger-than-expected recent data, including "a little stronger than expected" private demand in Q1 and resilient labor market that " has not eased as anticipated". Monthly inflation readings had also been "marginally higher" than staff projections. Additionally, Members noted that reduced global risks allowed greater confidence in the RBA’s baseline forecasts, rather than the worst-case scenario.

Still, the minutes make clear that the RBA remains on an easing path. Some members argued there was already enough evidence to justify a cut now, but the Board as a whole leaned toward keeping a cautious, gradual approach, which is inconsistent with a third rate cut within the space of four meetings at that time.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 7 and 8 July 2025

Members present

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor and Deputy Chair), Marnie Baker AM, Renée Fry-McKibbin, Ian Harper AO, Carolyn Hewson AO, Iain Ross AO, Alison Watkins AM, Jenny Wilkinson PSM

Others present

Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Head, Monetary Policy Strategy), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department)

Financial conditions

Members commenced their discussion of financial conditions by observing that financial market pricing continued to imply a relatively benign outlook for global growth and inflation. Corporate bond spreads had fallen back to levels close to those prevailing immediately prior to the US Administration’s tariff announcements in early April. Equity prices were at or near record highs and measures of equity risk premia were low. The improvement in market conditions in preceding weeks appeared to reflect an expectation that the most extreme outcomes for US tariffs were likely to be avoided. However, the final scope of tariffs and policy responses in other countries remained unknown; there were persistent geopolitical tensions, including conflict in the Middle East and Ukraine; and increasing concerns about long-run fiscal sustainability in a number of major advanced economies. Members discussed whether current financial market pricing reflected a degree of complacency on the part of market participants about the impact of these factors on the outlook for the global economy or suggested that earlier pessimism might have been overstated.

Central bank policy rate expectations had generally been little changed since the previous meeting. In the United States, financial market participants expected the US policy rate to be reduced only slightly over the remainder of 2025, consistent with relatively high near-term market-implied measures of inflation expectations, and then by more in 2026. Likewise, policy interest rates in most other major advanced economies were expected to be reduced by only a small amount over coming months, following significant reductions over the prior year. The Bank of Japan was expected to continue raising its policy rate gradually.

Longer term sovereign bond yields had declined a little across most advanced economies since the previous meeting but remained higher than around a year earlier. There had been minimal immediate reaction in yields to the passage in the US Congress of the Administration’s One Big Beautiful Bill Act of 2025. Nonetheless, the prospect of the passage of the legislation had contributed to growing concerns over sizeable fiscal deficits in future. Members noted that yields in Australia had declined by more than in the United States, including in response to the market’s interpretation of how incoming domestic data might influence monetary policy.

The Australian dollar had been little changed on a trade-weighted basis since the start of 2025, despite significant global developments. The decline in yield differentials between Australia and the rest of the world since the turn of the year had placed downward pressure on the Australian dollar, but this had been offset by the broad-based depreciation of the US dollar from the historical highs reached in 2024. The RBA index of commodity prices had been little changed since the previous meeting. Members noted that a combination of the higher supply of iron ore and the recent decline in Chinese steel production had weighed somewhat on iron ore prices. But this had been offset by rises in the prices of gold, rural and other commodities. Model estimates of the Australian dollar exchange rate suggested that the trade-weighted exchange rate was close to its long-run equilibrium level.

Members discussed how best to assess the ‘neutral’ cash rate in Australia. The forecasts in the May Statement on Monetary Policy – which provided the staff’s most recent comprehensive assessment of the outlook – suggested that underlying inflation would stay around the midpoint of the 2–3 per cent range and the labour market would remain close to full employment, assuming that the cash rate followed the then-prevailing market path, which was for a gradual decline to a little over 3 per cent by mid-2026. Those forecasts therefore suggested that the current setting of monetary policy was modestly restrictive.

The average of a range of alternative model estimates of the neutral cash rate pointed to a broadly similar conclusion. However, members observed that estimates from these models are subject to considerable dispersion and uncertainty and the average is sensitive to the choice of models included in the range. Against that backdrop, public discussion of the stance of monetary policy had possibly overemphasised the inferences that could be drawn from these alternative models, especially for the near term.

Another indication of the current restrictiveness of monetary policy could be obtained from trends in household credit growth. Members noted that household credit had continued to decline gradually relative to household incomes, providing further corroboration of the judgement that monetary policy had been modestly restrictive. The recent easing in policy had not yet resulted in a pick-up in demand for housing credit, and neither loan applications nor loan commitments had increased materially.

Scheduled household debt repayments had declined as expected following the reductions in the cash rate in both February and May. Households’ extra payments into their offset and redraw accounts (relative to household incomes) remained above average. This was consistent with the further rise in the aggregate household savings ratio in the March quarter and with the current level of interest rates providing an incentive to save.

Expectations for the cash rate had moved a bit lower since the previous meeting; around half of that move had followed the communication of the Board’s decision in May and the remainder largely reflected market interpretations of the subsequent flow of economic data. Members noted that a 25 basis point reduction in the cash rate at the current meeting was almost fully priced in by market participants and was also expected by most market economists. Market pricing implied that a further two reductions in the cash rate over the remainder of the year were expected, one more than had been anticipated prior to the May meeting. Members acknowledged that there had been previous occasions when market participants had been very confident about the outcome of a monetary policy decision but the (Reserve Bank) Board had decided on an alternative course.

International economic conditions

Turning to the global economy, members noted that developments in trade policy settings overall had been broadly consistent with the assumptions in the staff’s baseline forecasts published in May. These assumptions were for tariffs to settle at lower rates than had been announced in early April, but significantly higher than prior to the escalation of trade tensions. Measures of global economic uncertainty had fallen somewhat, as reflected in a narrower range of expectations among professional forecasters for US GDP growth in late 2025, but the outlook remained highly unpredictable. In part, that reflected continued uncertainty over future trade policy. The US President had begun to send letters to trading partners setting out new tariff rates to be applied from 1 August and suggesting that these rates could be adjusted subject to progress on trade negotiations. The global outlook had also been clouded by the 12-day Iran–Israel war. While the conflict in the Middle East had de-escalated significantly and the overall effects on the global economy had been limited, members noted that more persistent shocks to energy prices, should they occur, would affect the prospects for global growth and inflation.

Members noted that trade policy developments thus far had had a limited effect on momentum in the global economy. Household consumption and business conditions in the United States had been fairly resilient amid muted pass-through of higher tariffs to prices. However, the central case remained for US inflation to increase and output growth to slow in the second half of 2025 as inventories are run down and firms’ capacity to absorb higher tariffs diminishes. Members noted that it was possible that the effects could in fact be slower to emerge but more persistently adverse, as had occurred following some other changes to global trading arrangements in prior years. The Act was expected to support US economic activity in the short term but lead to structurally wider fiscal deficits and higher government debt in the long term.

Members considered the outlook for activity in China. They noted that conditions in the property sector remained weak, with only tentative signs that the downturn in activity had reached its trough. Growth in household credit and business financing consequently remained slow. This was being offset somewhat by government spending and programs supporting household consumption and investment. Fiscal policy remained the key potential channel for further stimulus, and there had been a significant pick-up in government bond issuance. Members discussed the commitment of Chinese authorities to their GDP growth target and the ability to achieve the target in the face of potential headwinds. Members also noted that China’s exports had changed remarkably, both in speed and scale, in response to the introduction of tariffs. It was difficult to assess the extent to which these developments reflected changes in the final destination of goods towards alternative markets in Europe and Asia, or changes in the routing of goods to existing markets.

Domestic economic conditions

Turning to the Australian economy, members noted there had been little discernible effect from recent international developments. Forward-looking consumer and business surveys had not fallen sharply in the immediate aftermath of the initial tariff announcements, as they had in other developed economies. And it was too soon to see much effect in the data on domestic economic activity. These developments remained consistent with the assumptions made in the baseline forecasts in May, which anticipated that the overall economic effects would be relatively modest and mostly occur in the second half of 2025 and into 2026. Members debated whether such effects might be larger or smaller than assumed in May.

GDP growth in the March quarter had been a little softer than expected in May because of an unanticipated fall in public demand. By contrast, the recovery in private demand had been slightly stronger than forecast, primarily reflecting the outcomes for household consumption and dwelling investment.

Growth in household consumption had eased in the March quarter, as forecast, but upward revisions to the prior quarter meant that growth over the year had been slightly stronger than expected. Members noted that assessments of underlying momentum in consumption growth were complicated by factors such as the temporary electricity subsidies, increases in promotional sales activity late in 2024 and weather events; that said, there were signs that consumption growth had picked up since mid-2024 as real household incomes had recovered. Even with this recovery, per capita consumption had been little changed over the prior year. Available indicators for the June quarter suggested that growth in household consumption had been slightly below the staff’s expectations.

Dwelling investment had been stronger than expected and now showed a clearer upward trend since early 2024. Activity in the established housing market had also begun to pick up.

Members noted the staff’s assessment that the unexpected decline in public demand in the March quarter at least partly reflected volatility rather than a material slowing. Recent government budgets remained broadly consistent with the staff’s expectations for growth in public demand in the May forecasts.

Employment growth in the non-market sector – which includes health care, education and public administration – had started to ease in early 2025 from a rapid pace, while employment growth in the market sector had picked up a little in year-ended terms. Members noted that a key consideration for the economic outlook was the extent to which any further slowing in growth in non-market sector employment and activity would be offset by stronger growth in the market sector. They observed that the unemployment rate could hold steady even if this transition occurs with somewhat lower overall employment growth, depending on developments in labour force participation.

Members considered the effect of recent developments on the unemployment rate and other measures of spare capacity. The unemployment rate was unchanged in May and had been stable over the preceding year, and other indicators pointed to little change in the unemployment rate in the near term (compared with the staff’s previous expectations for a slight increase). The staff still assessed that labour market conditions were tight, though with a considerable degree of uncertainty. This assessment was informed by a range of indicators, including the relatively low levels of the unemployment and underemployment rates, as well as the share of firms reporting labour as a significant constraint on output and the ratio of job vacancies to unemployed workers, both of which remained well above their pre-pandemic levels. Growth in unit labour costs – a comprehensive, though volatile, measure of labour costs – remained high, mostly because of persistently weak productivity growth. By contrast, members noted that measures of job mobility had continued to decline (suggesting an easing in competition among firms to attract and retain staff), and year-ended growth in the wage price index and services price inflation had continued to moderate over the prior year. Members noted that these factors might imply that supply and demand in the labour market were closer to balance.

Members discussed the broad-based slowdown in productivity growth in Australia and other advanced economies. The slowing over recent decades reflected structural headwinds, though other factors (including a decline in productivity in the mining sector and an expansion in the size of the non-market sector) had also weighed on productivity growth in preceding years. The staff’s forecast for output growth continued to assume that annual productivity growth would pick up, despite no rise in productivity since 2016. Members noted that this assumption materially influences the medium-term outlook for growth in the economy’s supply capacity, incomes and demand.

Members noted that the sharp declines in the monthly indicators for headline and trimmed-mean inflation were likely to have overstated the easing in underlying inflation momentum. They noted that a measure that removes electricity and some other volatile prices from the monthly CPI indicator has had a closer relationship with quarterly trimmed-mean inflation over preceding years than the monthly trimmed-mean indicator. This exclusion-based measure had not eased as much as the monthly trimmed-mean indicator recently. Further, movements in components of the monthly CPI data that contained new information suggested that underlying inflation in the June quarter could be slightly higher than the staff had forecast in May. This reflected upside surprises to new dwelling costs and consumer durables inflation in April.

Underlying inflation over the year to the June quarter was still expected to ease further but remain in the upper half of the 2–3 per cent range. Headline inflation over the year to the June quarter was expected to be broadly in line with the May forecast (given the impact of declining fuel prices throughout May). Looking ahead, headline inflation was expected to pick up temporarily to around the top of the target range in late 2025 and remain there in 2026, reflecting the currently legislated unwinding of government energy subsidies to households.

Considerations for monetary policy

Turning to considerations for the monetary policy decision, members noted that inflation had returned to the target range and was expected to be around the midpoint once the volatility associated with temporary cost of living relief abates. Recent monthly CPI indicator data – which can be volatile and do not cover all items in the CPI – were broadly consistent with this expectation. The labour market was assessed to have remained tight, with measures of labour utilisation little changed over the prior year. Growth in private demand had begun to recover but was still subdued.

Members agreed that the outlook for the global economy was highly uncertain. The probability of the global economy evolving in line with the most severe downside scenarios, such as the one considered in the May Statement on Monetary Policy, looked to have declined since the previous meeting. However, the future state of US trade and other policies was unpredictable and geopolitical tensions remained acute.

Members agreed that the stance of monetary policy was still modestly restrictive. However, financial conditions had eased over prior months, given the decisions to lower the cash rate target in February and May and the subsequent decline in market expectations for the future path of the cash rate.

In light of these developments, and with the May forecasts having been conditioned on further reductions in the cash rate in the period ahead, members considered whether to leave the cash rate target unchanged at this meeting or to reduce it by 25 basis points.

All members agreed that, based on the information currently available, the outlook was for underlying inflation to decline further in year-ended terms, warranting some additional reduction in interest rates over time. The focus at this meeting was on the appropriate timing and extent of further easing, against the backdrop of heightened uncertainty.

The case to leave the cash rate target unchanged at this meeting rested on a number of considerations. One related to what the flow of recent data implied for the economic outlook. Several indicators had been in line with, or even slightly stronger than, staff projections, pointing to the benefit of waiting for a little more information to confirm that inflation remains on track to be at 2.5 per cent on a sustainable basis. Monthly indicators of inflation had been marginally higher than were consistent with the staff’s forecast for underlying inflation in the June quarter, growth in private demand in the March quarter had been a little stronger than expected and conditions in the labour market had so far not eased as anticipated. In addition, the reduced likelihood of the most severe scenarios materialising for the world economy meant that more weight could be placed on the baseline forecasts, and less on the downside scenario, than had been warranted in May when assessing the medium-term outlook. Members noted that the baseline forecasts already incorporated some deterioration in global economic conditions because of higher tariffs and policy uncertainty, which was consistent with the evidence currently available on how the trade tensions and other factors might be resolved. Moreover, the forecasts had been conditioned on a relatively modest and gradual path of further easing of monetary policy over the period ahead. Hence, these developments supported the view that the Board could wait a little longer for further confirmation of the economy’s trajectory before adjusting policy again.

Members also observed that, if productivity growth proves to have been persistently lower than had been the case historically, the recent subdued outcomes for GDP growth may not have been far below the rate of growth in supply capacity. Similarly, it was difficult to determine with precision how far interest rates needed to fall before monetary policy was no longer restrictive, and so members observed that it might be prudent to lower interest rates cautiously as the required degree of policy restrictiveness declines.

The case to lower the cash rate target at this meeting rested on a view that there was already sufficient evidence to be confident that inflation was on track to be sustainably back at the midpoint of the target range, if not lower. This implied less need to wait before easing policy further, which was a relevant consideration given the lags in the effect of monetary policy on economic activity and inflation. Uncertainty in the world economy remained pronounced and the material increase in US tariffs – even if not as extreme as had been announced in early April – would be a drag on future growth abroad, and thereby domestic economic activity and inflation. GDP growth in Australia was already subdued, the saving rate had risen, the underlying momentum in wages growth and services price inflation appeared to be lower and some concerns were expressed that the recent data suggested a loss of momentum in activity. Overall, this might suggest less capacity pressure than embodied in the May baseline projections. Moreover, there was uncertainty around whether market sector employment growth would increase by enough to offset an expected slowing in non-market sector employment growth to maintain momentum in overall employment growth.

Having weighed up the alternative arguments, a majority of members judged that the case to hold the cash rate target unchanged at this meeting was the stronger one. They believed that lowering the cash rate a third time within the space of four meetings would be unlikely to be consistent with the strategy of easing monetary policy in a cautious and gradual manner to achieve the Board’s inflation and full employment objectives. While the flow of recent data had been broadly in line with earlier forecasts, they judged that some data had been slightly stronger than expected. Therefore, these members argued that it would be prudent to wait for confirmation that inflation would sustainably return to target as forecast before easing policy further. They noted that the Board would receive important information before the next meeting, including another quarterly inflation report and additional information on the labour market and how the world economy is evolving, along with a revised set of staff forecasts.

A minority of members judged that there was a case to lower the cash rate target at this meeting. These members placed more weight on downside risks to the economic outlook – stemming from a likely slowing in growth abroad and from the subdued pace of GDP growth in Australia. That in turn posed a risk that underlying inflation would moderate somewhat more rapidly than envisaged in the May projections. Therefore, these members considered that easing policy at this meeting would be consistent with the Board’s strategy and manage the risk that spare capacity might emerge in future.

In finalising the Board’s statement, members agreed that the effectiveness of the Board’s communication would be strengthened by disclosing an unattributed record of votes at this and future meetings. They also emphasised the need to be attentive to the data and to be guided by how the data shape the evolving assessment of risks. Members agreed that the Board should remain focused on its mandate to deliver both price stability and full employment and that it will do what it considers necessary to achieve that outcome.

The decision

The Board decided by majority (six in favour, three against) to leave the cash rate target unchanged at 3.85 per cent.

New Zealand imports jump 19% yoy in June, while exports rise 10% yoy

New Zealand posted a trade surplus of NZD 142m in June, falling well short of market expectations for NZD 1.02B. The softer balance came despite solid annual growth in both exports and imports. Goods exports rose 10% yoy to NZD 6.6B and imports surging 19% to NZD 6.5B.

Regionally, exports to the EU jumped 38% yoy, followed by gains to China (11% yoy) and Australia (16% yoy). However, exports to the US and Japan declined -8.8% yoy and -4.7% yoy respectively.

The strength in exports was not enough to offset the broader pressure from surging imports, particularly as US ( 21% yoy) and South Korean (40% yoy) shipments rose sharply. Imports from EU (0.8% yoy), Australia (6.8% yoy) and China (9.1% yoy) also grew.

WTI Oil Slips as 200-day MA Caps Upside Potential

Oil prices continue to trade in a tight range between the 100 and 200-day MAs. Similar to Gold last week Oil prices appear to be in need of a catalyst that could provide some direction.

EU Sanctions on Russian Oil Exports

On Friday, the European Union approved its 18th round of sanctions against Russia for the war in Ukraine, including measures against India's Nayara Energy, which exports oil products made from Russian crude.

The latest round of European sanctions on Russian oil exports are not expected to have a significant impact on Oil prices. The bigger question which remains is still on the tariff front which continues to keep demand concerns on the minds of market participants and thus hamper upside potential.

Kremlin spokesperson Dmitry Peskov said on Friday that Russia has developed some resistance to Western sanctions.

The EU sanctions came after U.S. President Donald Trump warned last week that he would sanction buyers of Russian exports if Russia doesn’t agree to a peace deal within 50 days.

Iran, which is also under oil sanctions, will hold nuclear talks with Britain, France, and Germany in Istanbul on Friday, according to an Iranian Foreign Ministry spokesperson. This comes after the three European countries warned that if negotiations don’t restart, international sanctions on Iran could be reimposed.

If international sanctions are reimposed on Iran, it could affect oil prices. However, it’s uncertain if these changes would last in the medium term. Similar to Russia, Iran has adapted to sanctions over time and has developed strategies to manage during such periods.

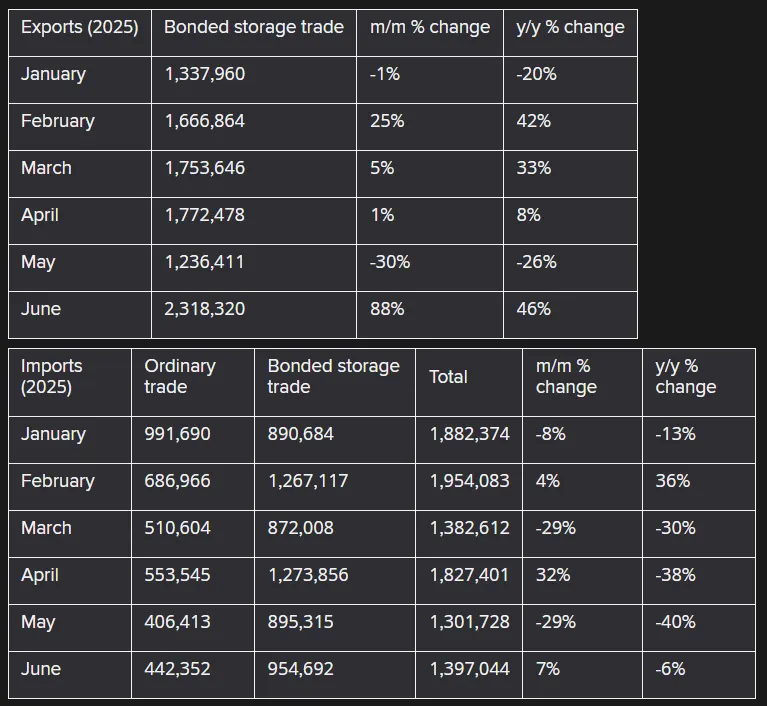

China Fuel Oil Imports Rise in June

China’s fuel oil imports bounced back in June after dropping in May, while exports of bunker fuel oil also increased compared to the previous month, according to customs data released on Sunday.

In June, fuel oil imports reached about 1.4 million metric tons (around 295,708 barrels per day), which is a 7% increase from May but 6% lower than the same time last year.

The rebound came after the Shandong provincial government increased tax rebates on fuel oil imports for some independent refineries. Earlier in the year, demand for refinery feedstock had dropped due to higher import tariffs and reduced tax rebates on fuel oil.

From January to June, total imports fell 19.8% compared to the same period last year, totaling 9.75 million tons.

Source: LSEG

However with trade deal uncertainty lingering, demand concerns are keeping Oil prices in check and this is likely to continue till the August deadline at least.

Saudi Crude Exports Hit 3 Month-Highs

Demand concerns may be on the mind of market participants, however Saudi Arabia crude oil exports rose to a three month high in May. This is according to the latest data by the Joint Organizations Data Initiative (JODI) with the Kingdom leading OPEC + production increases in a move that many analysts view as a pivot strategy to gain more market share.

Oil exports increased by 25,000 barrels per day (bpd) in May, reaching 6.19 million bpd, according to JODI data, which is based on reports from individual countries.

May’s export levels were the highest since February, when shipments surpassed 6.5 million bpd, the data revealed.

At the same time, Saudi crude oil production rose by 179,000 bpd in May, hitting a 23-month high as the Kingdom and its OPEC+ partners began easing production cuts in April.

Technical Analysis - WTI

From a technical analysis standpoint, Oil continues to trade in the tight range between the 100 and 200-day MAs.

Each time it appears that a breakout may materailize in either direction buying or selling pressure has been rearing its head of late.

This is a clear sign of the non-commital nature of market participants at present as they grapple with a host of uncertainties.

For now though, immediate support rests at 66.150 before the 100-day MA at 65.17 comes into focus. A break of this level could lead to further downside.

A move higher needs a clean break and daily candle close above the 200-day MA resting at 68.27, which could open up further upside potential toward the psychological 70.00 handle.

A move beyond this level will find resistance at 71.38 before the psychological 75.00 handle becomes the focus.

WTI USOIL Daily Chart, July 21, 2025

Source: TradingView (click to enlarge)

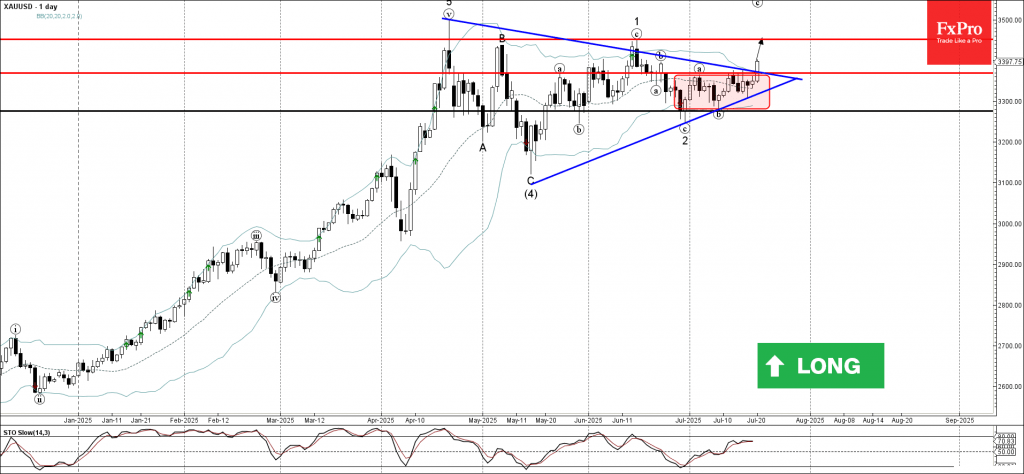

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold broke resistance daily Triangle

- Likely to rise to resistance level 3450.00

Gold recently broke the resistance zone between the resistance level 3370.00 (upper border of the narrow sideways price range inside which Gold has been trading from the end of June) and the resistance trendline of the daily Triangle from April.

The breakout of this resistance zone accelerated the active impulse wave 3, which is a part of the intermediate impulse wave (5) from May.

Given the clear daily uptrend, Gold can be expected to rise further to the next resistance level 3450.00 (top of the minor impulse wave 1 from the middle of June).

US Dollar Falls Off to Start the Week

The US Dollar has started to show some signs of relative weakness after an almost flawless beginning to July.

Between a rebirth in Tariff talks, extended until the 1st of August and some general volatility in global Geopolitics, there has been some sell-side covering for the Greenback.

The rally has (at least for now) concluded through last week's bout of Middle East tensions (with intense Syrian local conflicts), encouraging PPI Data and FED's Waller starting the Blackout Period from the US Central Bank with some repeating of his dovish comments.

For those who haven't seen the headlines, Japan's Prime Minister and his electorate have lost the majority which has created some movement in JGBs (Japanese Governement Bonds) and led to a strengthening of the Yen (with Japan markets off today) – Another contributor of a weaker dollar to start the week – USDJPY is down close to 1% on the session.

Markets were also concerned by talks around Jerome Powell, whose term finishes in May 2026, getting fired from his FED Chair role – US Treasury's Scott Bessent has denied such outcomes, however markets had still sold off some treasuries which trickled to the Dollar on the last weekly close – Any possibility has to get priced in!

Let's take a look at what technicals indicate to spot potential trends for this starting week.

Dollar Index Technical update

Dollar Index 1H Chart

Dollar Index 1H Chart, July 21, 2025 – Source: TradingView

The Dollar came shy of the 99.00 psychological handle – A failure to breach that landmark has been seen as a sign of weakness despite a solid July tenure and some testing of higher levels through risk-off spikes.

Failed patterns and breaks are the best signs for reversals, and the last spike on Thursday to form a double-top was a good example for this.

Since, the Index is down close to 1 full handle, with prices consolidating in the 98.00 Pivot Zone (+20 pips) and currently breaking the psychological level.

Sellers are taking the momentum, as they are currently pushing through the 97.98 overnight lows pursuing the break-retest of the July Channel.

Watch for other currency pairs and assets how this dynamic trickles – Gold is also up 1.10% on the session and close to $3,400.

Stepping back to the 4H Chart

Dollar Index 4H Chart, July 21, 2025 – Source: TradingView

There is a move down ongoing, which gets also reflected in the 4H RSI trading below its neutral zone (neutral is typically close to the middle line).

There has been a golden cross between the 50 and 200 MAs on Friday which led to some bull candles, however such technical patterns can come late and have done just that.

Buyers will look at the 97.60 Support Zone (+/-10 pips) to show some presence – Selling outflows from the US are still potentially massive with the short-term positioning having became more neutral in the past two weeks – Still, the week is young and markets will have to slow down a bit towards next week as they will prepare for the July 31st FED Meeting.

Levels to place on your charts:

Support Levels:

- 97.60 Support Zone (+/-10 pips)

- 97.30 last pivot before run-higher

- 96.50 2025 Lows

Resistance Levels:

- 98.00 Major Pivot Zone (50 and 200 MA Confluence)

- 98.50 Gap/Resistance Zone

- 98.95 to 99.00 Last week highs

Safe Trades and successful week!

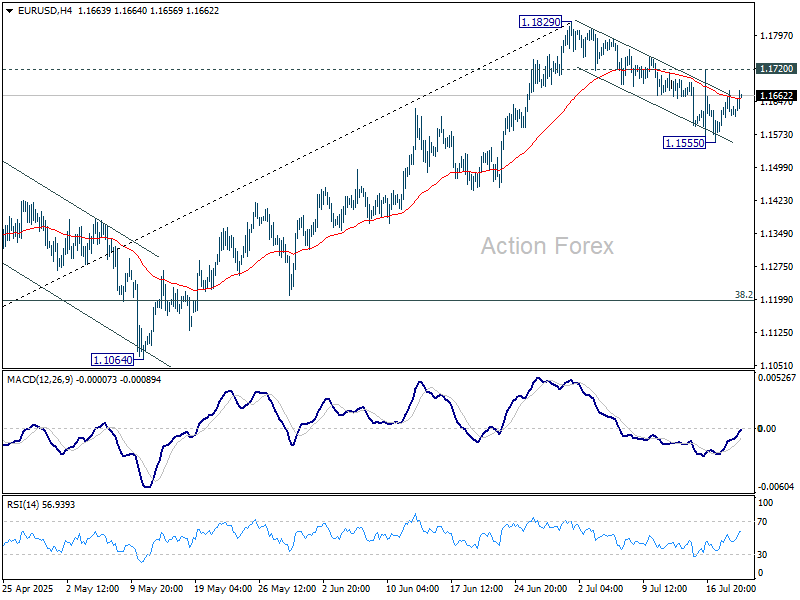

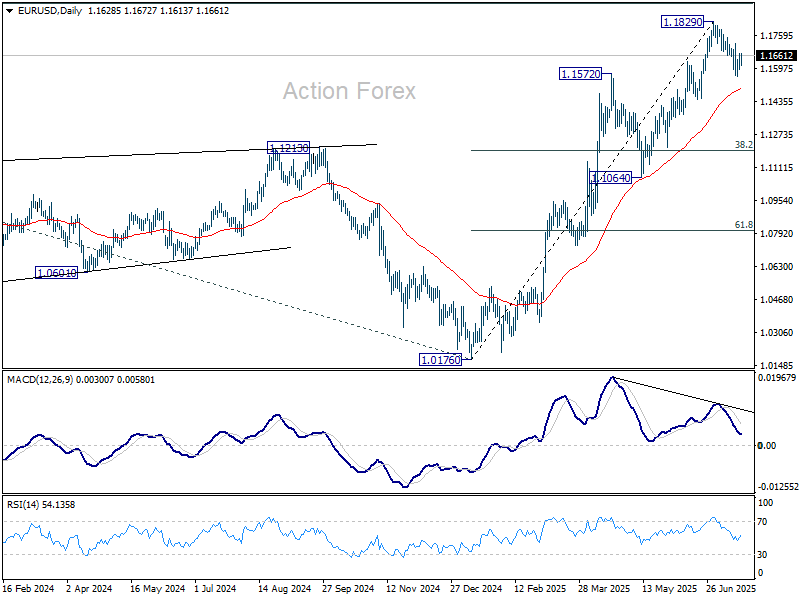

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1587; (P) 1.1630; (R1) 1.1667; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. Fall from 1.1829 might extend lower, and sustained trading below 55 D EMA (now at 1.1498) will argue that it's already correcting the rally from 1.0176, and target 38.2% retracement of 1.0176 to 1.1829 at 1.1198. On the upside, though, break of 1.1720 will bring retest of 1.1829 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

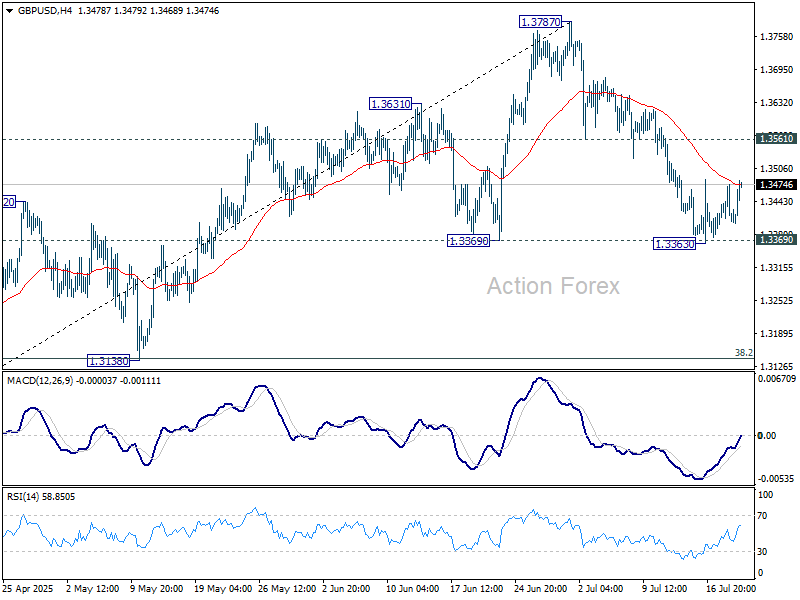

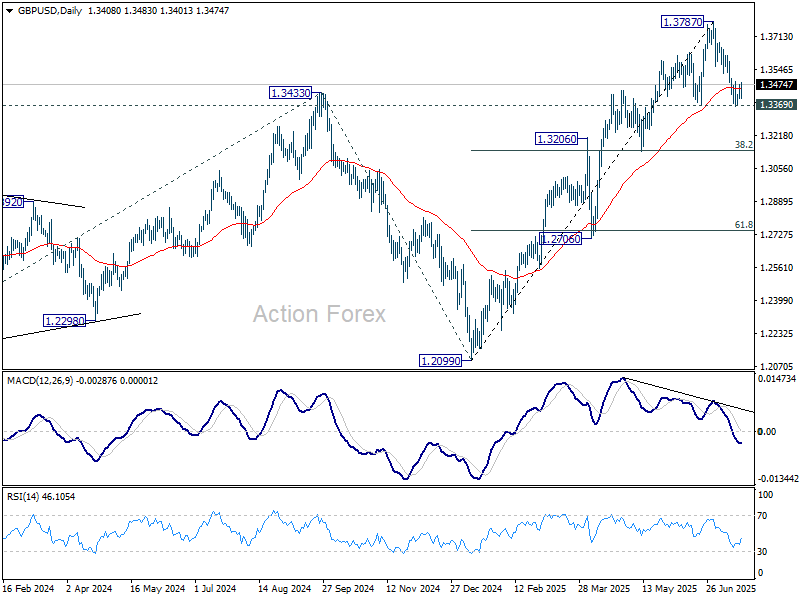

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3383; (P) 1.3429; (R1) 1.3455; More...

Intraday bias in GBP/USD stays neutral for the moment. On the downside, firm break of 1.3363/9 will suggest that fall from 1.3787 short term top is already correcting the rise from 1.2099. Deeper decline should then be seen to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142). However, strong rebound from current level will retain near term bullishness. Break of 1.3561 support turned resistance will bring retest of 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3017) holds, even in case of deep pullback.

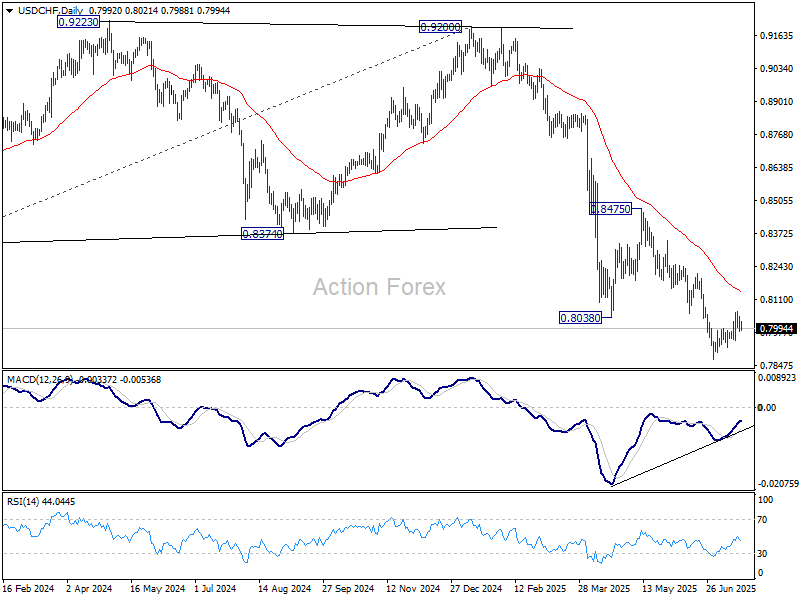

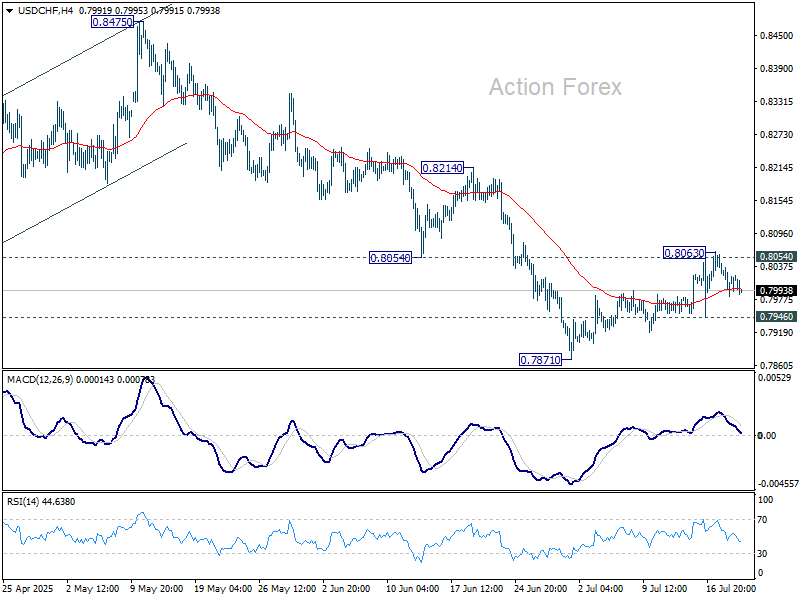

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7982; (P) 0.8020; (R1) 0.8054; More….

No change in USD/CHF's outlook and intraday bias remains neutral. On the downside, break of 0.7946 support will argue that correction from 0.7871 has completed, and bring retest of this low. Nevertheless, firm break of 0.8054/63 will bring stronger rebound to 55 D EMA (now at 0.8140).

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.