Sample Category Title

Singapore Stocks Hit Record High, Gold (Chart of the Day) Bullish Momentum Building Up

Asia Pacific stock markets opened the week on a mixed note. Singapore’s Straits Times Index (STI) led the pack, surging 0.5% intraday to a new all-time high of 4,225, breaking above the psychological 4,200 mark and continuing its bullish run.

Singapore leads Asia as STI hits record high, Hang Seng extends gains, ASX 200 lags

Hong Kong’s Hang Seng Index added 0.3%, building on last Friday’s breakout above the 19 March 2025 high. In contrast, Australia’s ASX 200 underperformed with a sharp 1.2% decline, reflecting divergent regional market sentiment.

Japan markets react calmly to the election outcome

Sunday’s Upper House election in Japan resulted in the ruling LDP-Komeito coalition losing its majority. However, the market response was relatively muted as the outcome had already been priced in. The Japanese yen recovered 0.4% intraday after falling to a three-month low last week. Nikkei 225 futures gained 0.3% on Globex trading, although the Tokyo market remained shut for a public holiday.

Dovish Fed comments weigh on US Dollar

The US dollar stayed soft in Asia following dovish remarks from Fed Governor Waller on Friday. Waller signalled openness to a rate cut, diverging from his colleagues’ cautious stance. This shifted market expectations: while the July FOMC is still seen as a hold (95% odds), the probability of a 25-bps cut in September rose to 61%, up from 55% a week ago, per CME FedWatch data.

Yen, Aussie, Sterling gain; Gold extends rebound

In the FX space, the Japanese yen led gains (0.4%) during the Asian session, followed by the Australian dollar and British pound (both up 0.2%). The softer US dollar supported Gold (XAU/USD), which posted a 0.6% intraday gain, marking its second consecutive daily advance, as it eyes the US$3,374 resistance level set on 14 July.

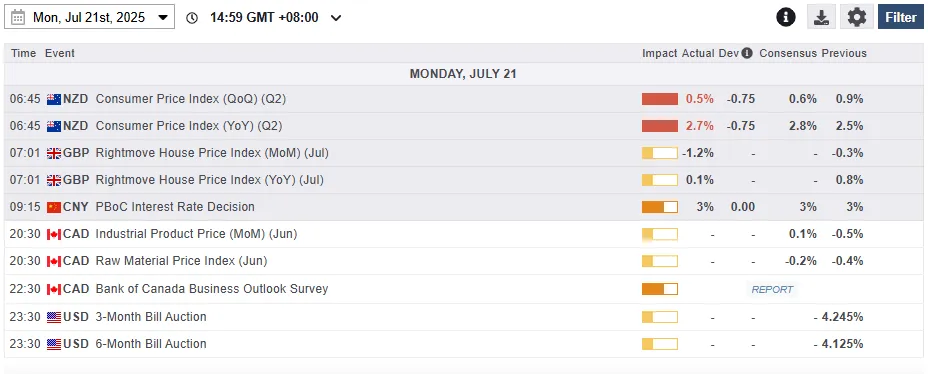

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – Gold (XAU/USD) looks poised for a potential minor bullish breakout

Fig 2: Gold (XAU/USD) minor trend as of 21 July 2025 (Source: TradingView)

The recent minor sideways range compression of Gold (XAU/USD) in place since 3 July has reached a potential tipping point for at least a minor breakout scenario.

Two key elements have increased the odds of a bullish breakout scenario. Firstly, Gold (XAU/USD) has retested the medium-term ascending trendline support in place since 31 December 2024 low for the third time on last Thursday, 21 July.

Secondly, in conjunction with the third retest on the medium-term ascending trendline support of Gold (XAU/USD), the hourly MACD trend indicator has traced a bullish divergence condition on 17 July, inched higher, and staged a MACD-Signal line bullish crossover in today’s Asia session at this time of writing.

Watch the US$3,328 short-term pivotal support, and a clearance above US$3,374 upside trigger level may see a minor bullish breakout unfolding for the next intermediate resistances to come in at US$3,400 and US$3,450 in the first step.

On the flip side, failure to hold at US$3,328 invalidates the bullish scenario for another round of minor choppy corrective decline sequence to expose the next intermediate supports at US$3,309, and US$3,293/3,282.

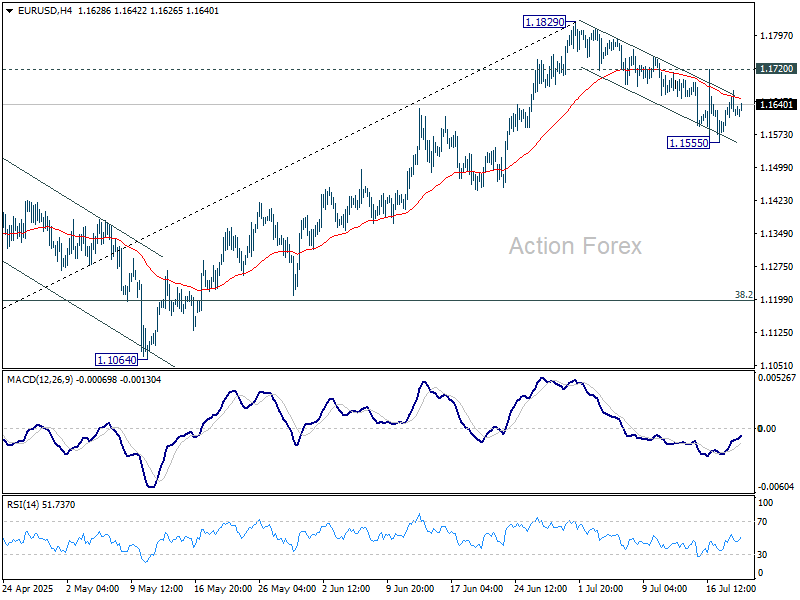

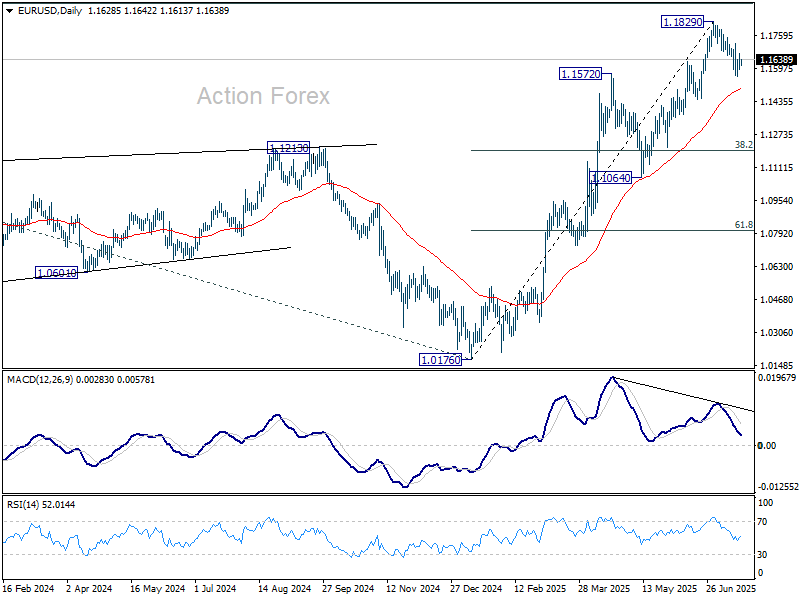

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1587; (P) 1.1630; (R1) 1.1667; More...

Intraday bias in EUR/USD remains neutral. Fall from 1.1829 might extend lower, and sustained trading below 55 D EMA (now at 1.1498) will argue that it's already correcting the rally from 1.0176, and target 38.2% retracement of 1.0176 to 1.1829 at 1.1198. On the upside, though, break of 1.1720 will bring retest of 1.1829 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

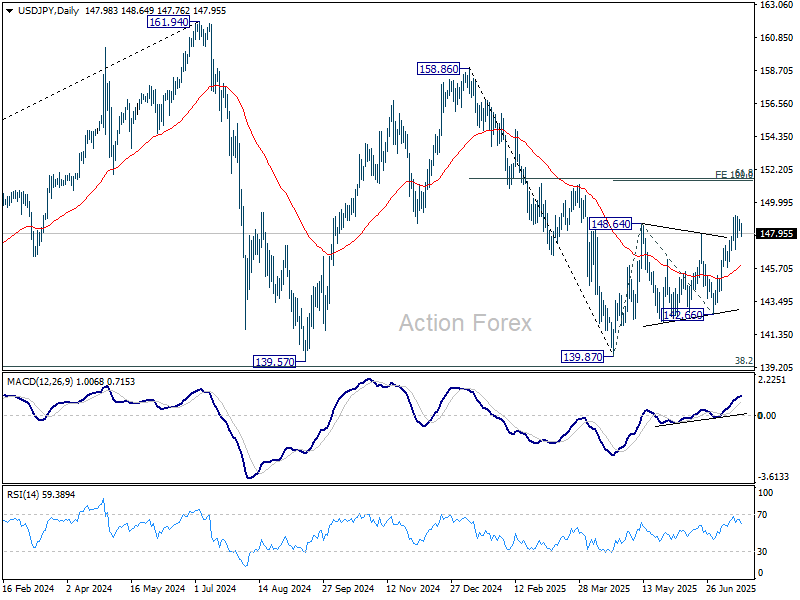

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.39; (P) 148.64; (R1) 149.08; More...

Intraday bias in USD/JPY remains neutral for the moment, and more consolidations could be seen below 149.17. Further rally is expected as long as 55 D EMA (now at 145.86) holds. On the upside, break of 149.17 will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

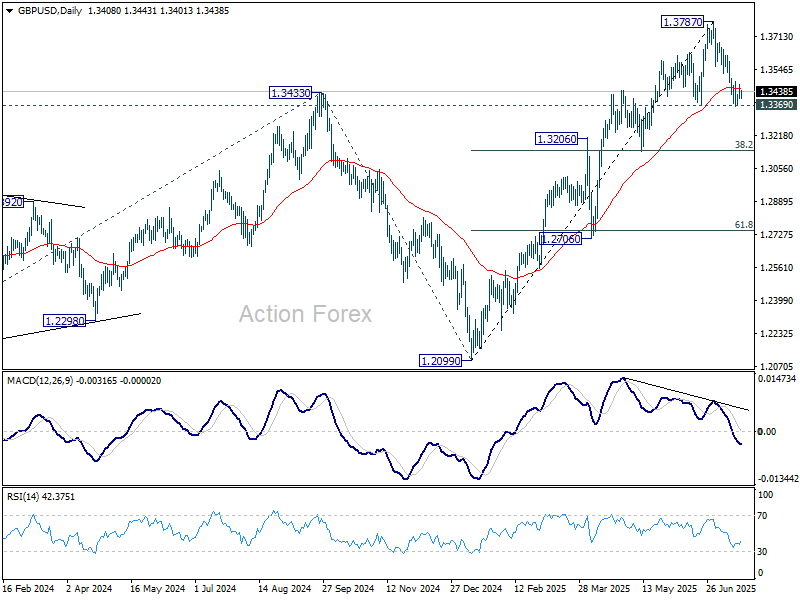

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3383; (P) 1.3429; (R1) 1.3455; More...

Intraday bias in GBP/USD stays neutral at this point. On the downside, firm break of 1.3363/9 will suggest that fall from 1.3787 short term top is already correcting the rise from 1.2099. Deeper decline should then be seen to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142). However, strong rebound from current level will retain near term bullishness. Break of 1.3561 support turned resistance will bring retest of 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3017) holds, even in case of deep pullback.

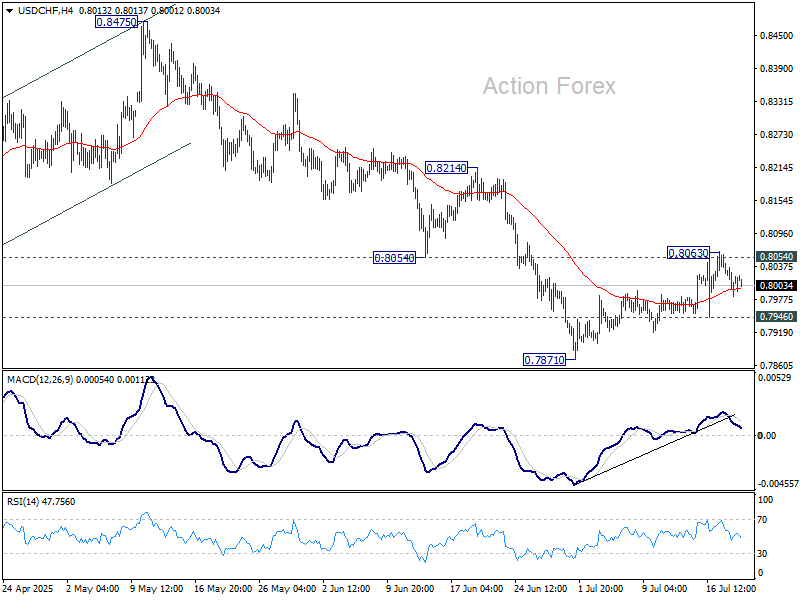

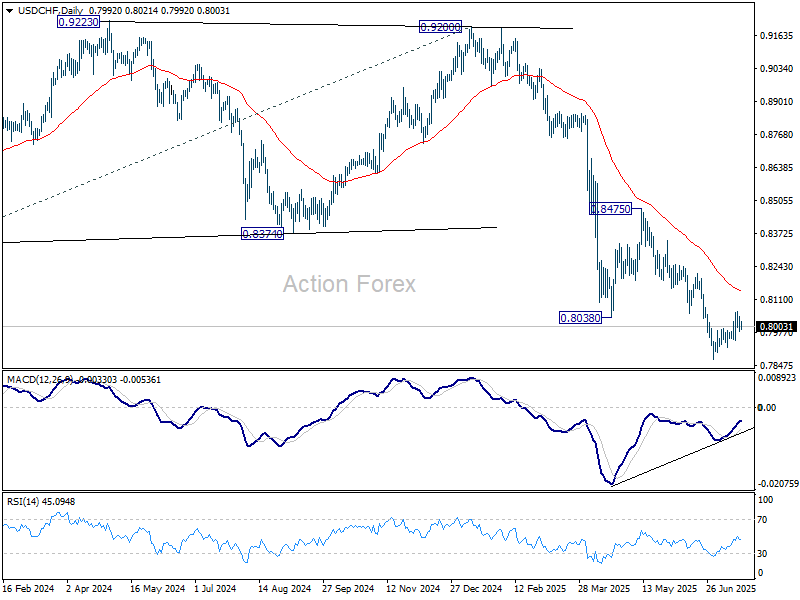

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7982; (P) 0.8020; (R1) 0.8054; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, break of 0.7946 support will argue that correction from 0.7871 has completed, and bring retest of this low. Nevertheless, firm break of 0.8054/63 will bring stronger rebound to 55 D EMA (now at 0.8140).

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

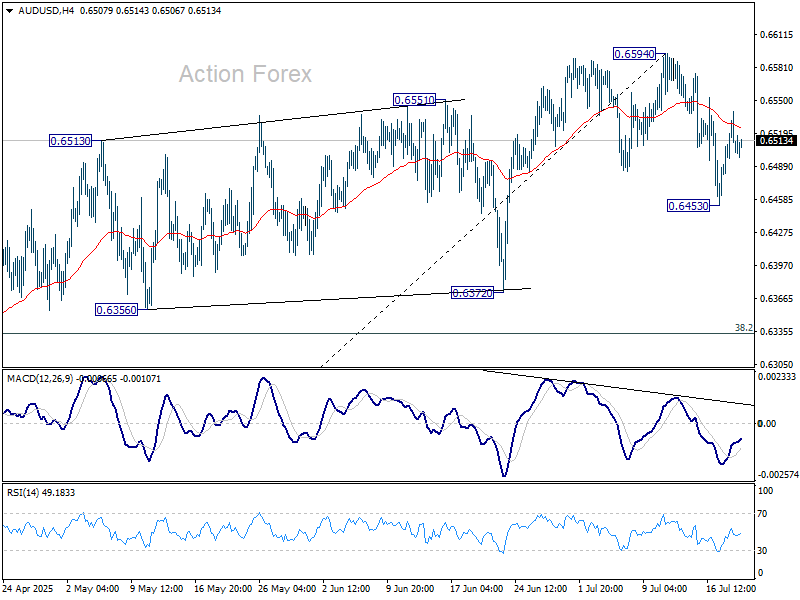

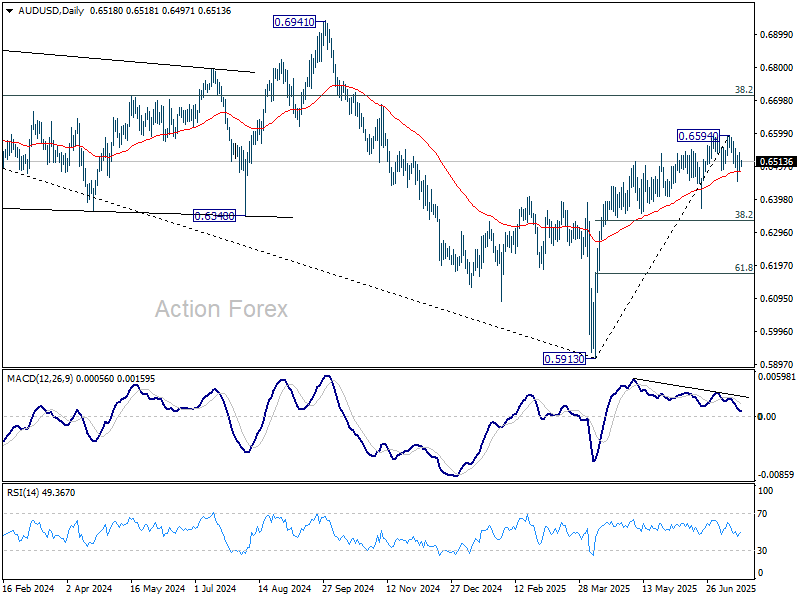

AUD/USD Daily Report

Daily Pivots: (S1) 0.6478; (P) 0.6509; (R1) 0.6539; More...

Intraday bias in AUD/USD remains neutral for the moment. Decline from 0.6594 could extends lower. Break of 0.6453 will target 38.2% retracement of 0.5913 to 0.6594 at 0.6334, as a correction to the whole rally from 0.5913. Risk will stay mildly on the downside for now as long as 0.6594 resistance holds, in case of stronger recovery.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

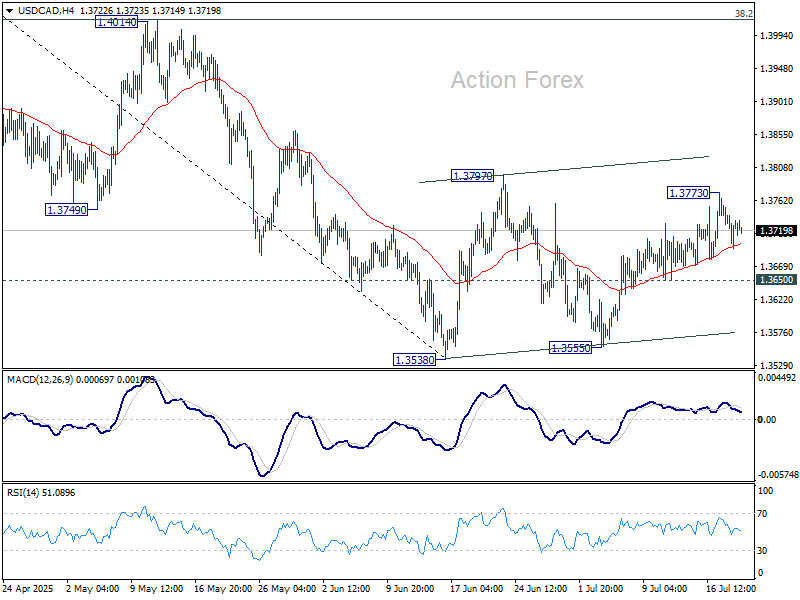

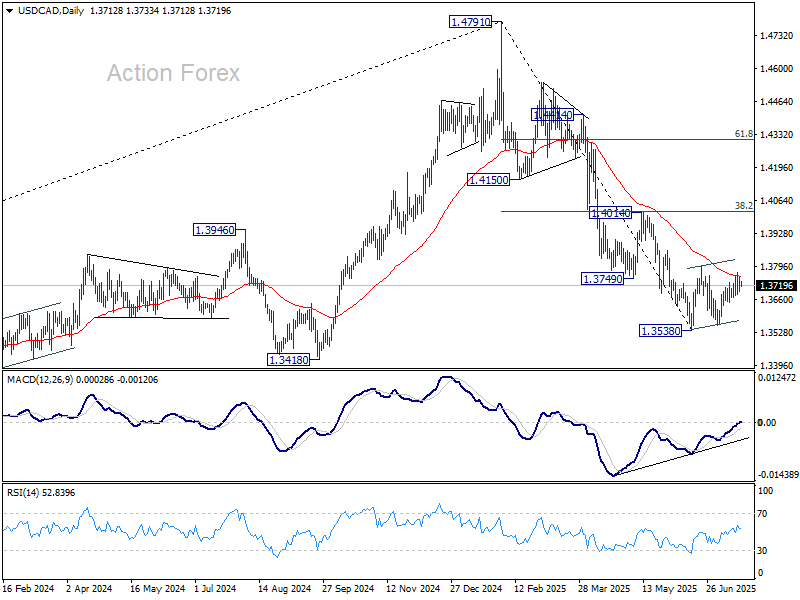

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3693; (P) 1.3726; (R1) 1.3755; More...

Intraday bias in USD/CAD stays neutral for the moment. Corrective pattern from 1.3538 could extend further. On the upside, above 1.3773 will target 1.3797 and possibly above. On the downside, break of 1.3650 support will bring retest of 1.3538/55 support zone.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

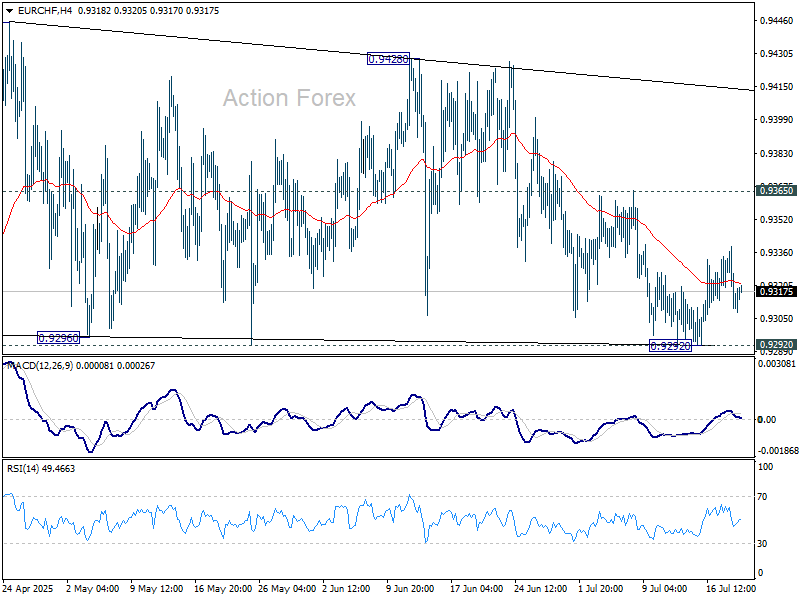

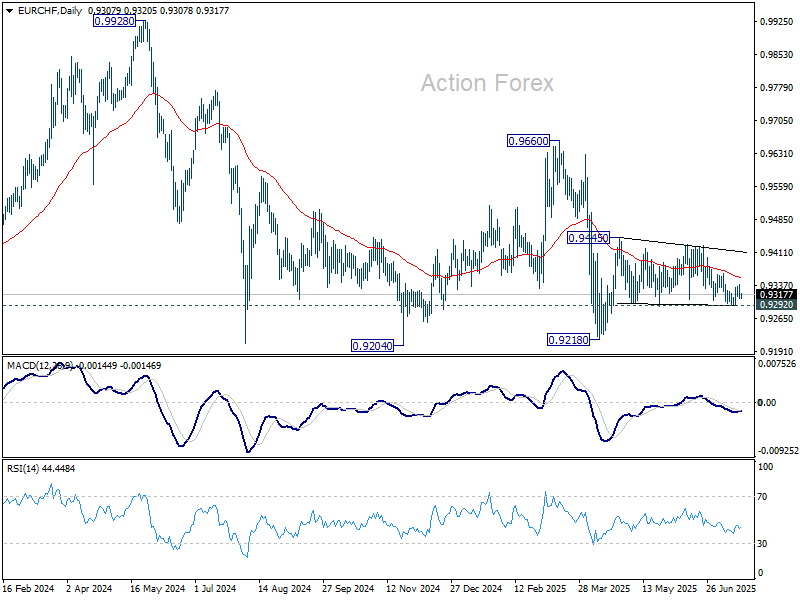

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9307; (P) 0.9324; (R1) 0.9338; More....

Intraday bias in EUR/CHF remains neutral for the moment. On the upside, firm break of 0.9365 resistance will be the first sign that corrective pattern from 0.9445 has already completed. Further rise should then be seen to 0.9428/45 resistance zone. Firm break there will resume the rebound from 0.9218 low. However, firm break of 0.9292 will bring retest of 0.9218 instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA (now at 0.9424) and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

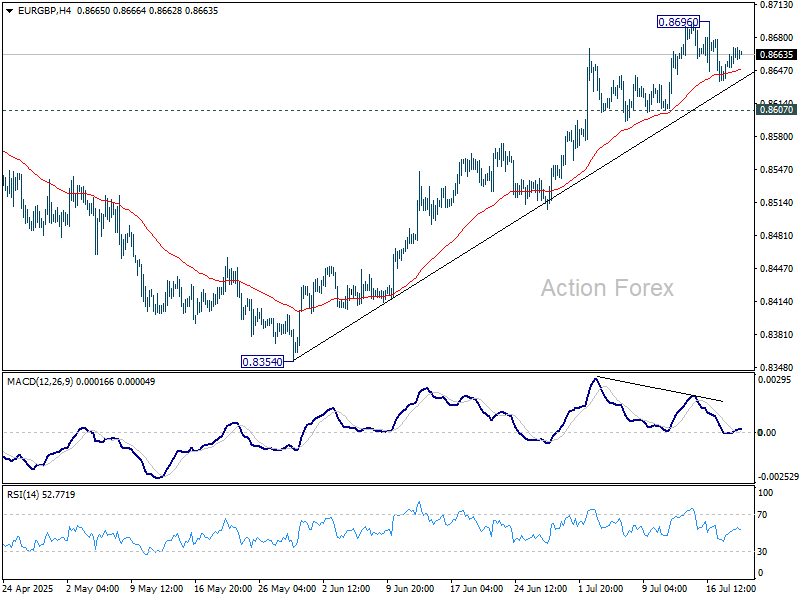

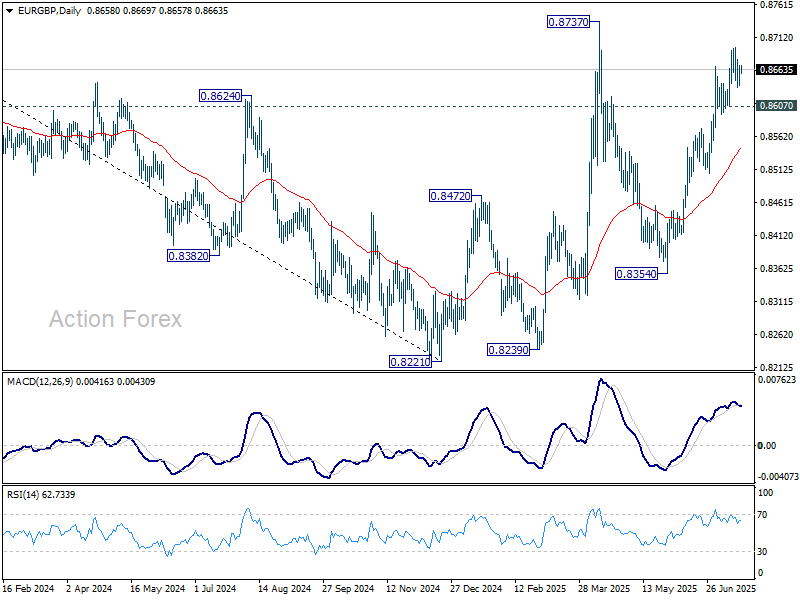

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8649; (P) 0.8661; (R1) 0.8680; More...

Intraday bias in EUR/GBP stays neutral and more consolidations could be seen below 0.8696. As long as 0.8607 support holds, further rally is expected. On the upside, above 0.8696 will bring retest of 0.8737 high. However, firm break of 0.8607 will confirm short term topping, on bearish divergence condition in 4H MACD. Deeper fall should be seen back to 55 D EMA (now at 0.8546).

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, firm break of 0.8737 will still pave the way to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. For now, further rise will remain in favor as long as 55 W EMA (now at 0.8474) holds.

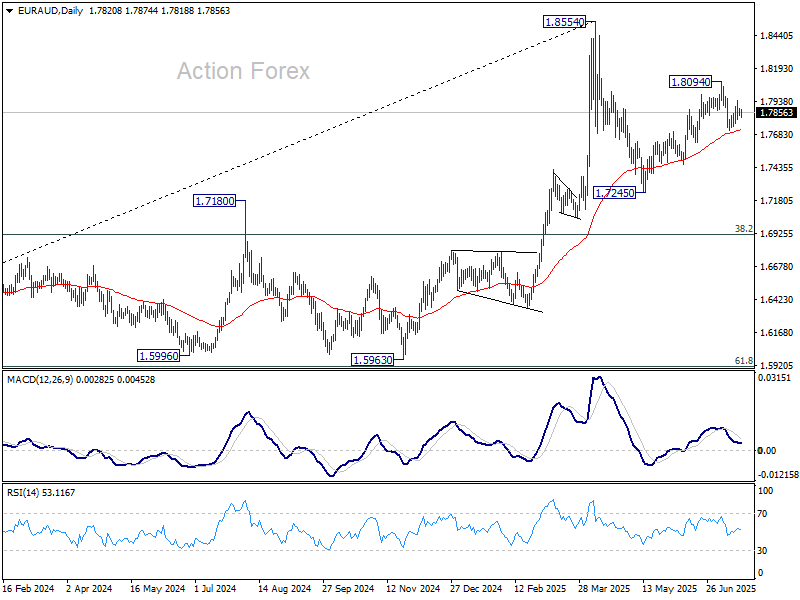

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7836; (P) 1.7862; (R1) 1.7892; More...

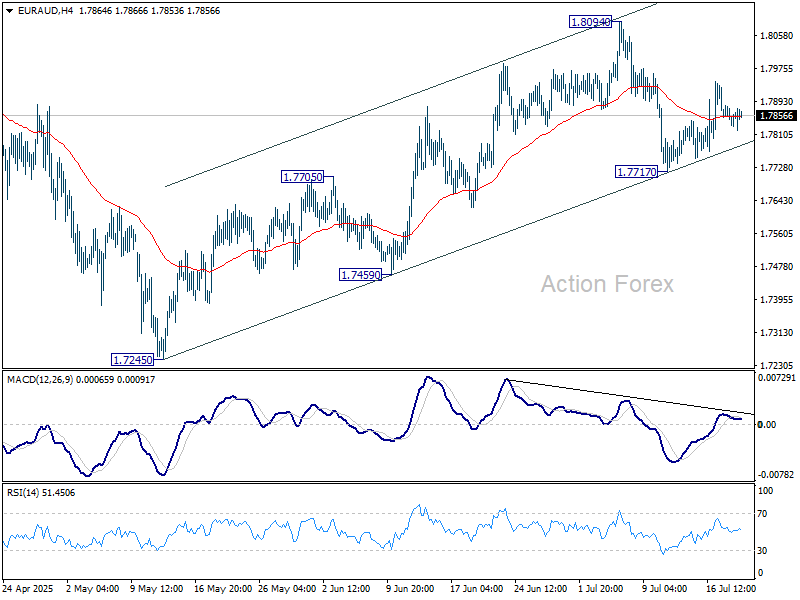

Intraday bias in EUR/AUD remains neutral for the moment. On the upside, break of 1.8094 will resume the choppy rise from 1.7245 towards 1.8554 high. However, break of 1.7717 support will revive the case that rise from 1.7245 has completed, and turn bias back to the downside for 1.7459 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.