Sample Category Title

Sunset Market Commentary

Markets

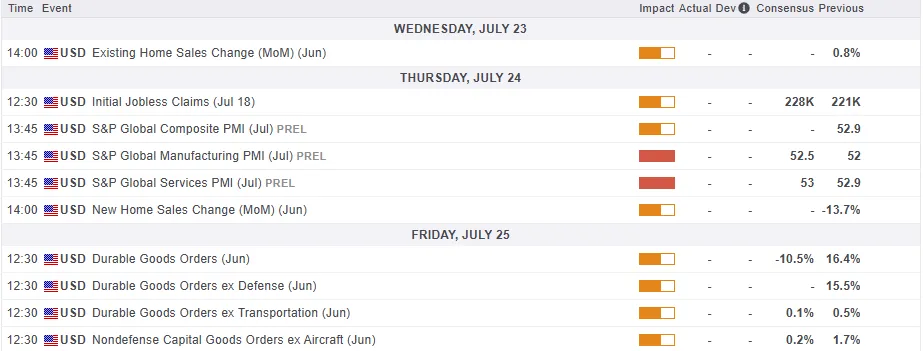

Global markets today are captured in guarded (holiday thinned) trading, awaiting more concrete news later this week/next week. US and EMU PMI’s on Thursday will give some insight on current activity and corporates’ intentions as trade negotiations between the US and its (major) trading partners are entering ‘money time’. The ECB will hold a regular policy meeting also on Thursday. However, after reducing the policy rate back to a neutral 2% level in June, the bank now is in a good position to await the outcome of the trade negotiations before giving new guidance. Markets in the meantime shifted to a more cautious risk bias as recent headlines/rumours on the negotiations between the US and its trading partners suggest that the final reciprocal tariff might be higher than the 10% level that EU (and other countries) deemed feasible. On the other hand, US Treasury Secretary Bessent turned quite constructive on trade talks with China scheduled of next week in Stockholm. After hitting an air pocket yesterday on trade-related uncertainty, US and EMU yields today are changing less than 2 bps across the curve. The ECB today published its Q2 bank lending survey. Credit standards for firm loans remained broadly unchanged. Credit standards tightened slightly for housing loans and more markedly for consumer credit. On the demand side, housing loan demand continued to increase strongly, while demand for firm loans remained weak. The impact of the survey on European interest rate markets was close to non-existent. The Eurostoxx 50 corrects further (-0.70%). US equity indices are taking a breather (S&P little changed near record levels).

On FX markets, the dollar yesterday surprisingly lost ground on trade-related uncertainty. Today, changes in major FX are very limited. DXY holding almost unchanged (97.8). EUR/USD is holding a very narrow range close to 1.17. Bessent took a softer tone on the position of Fed Chair Powell compared to other comments from the White House of late. He indicated that the Fed Chair could stay in place till the end of his term even as Bessent still calls for a review of the Fed’s non-monetary policy activities. This might provide some relief for the dollar. The yen gains modestly as Japanese markets reopen for the first trading session after the LDP led government lost its majority in the Upper House elections this weekend. The topic of fiscal sustainability is here to stay as the minority government will have to make ad hoc agreements with opposition parties to address concerns on the cost of living crisis. LT Japanese bonds and the yen remain vulnerable, but the first market reaction remains guarded. The yen in some kind of sell the rumour, buy the fact bias, rebounds modestly yesterday and also today (USD/JPY 146.8). Sterling initially underperformed today after the ONS released disappointing monthly public sector borrowing data (PSNB £20.7 bn vs £17.5 bn expected). EUR/GBP briefly ticked up to 0.868, but a test of the EUR/GBP 0.87 still proved one bridge too far for now (currently again 0.867).

News & Views

Belgian consumer confidence stabilized at -4 to remain above its long-term average, the July consumer confidence survey of the national bank of Belgium (NBB) showed. “After the marked upswing in confidence observed since May, consumers have now turned somewhat more pessimistic about macroeconomic factors”, the NBB noted. Expectations for the general economic situation worsened and concerns about an increase in unemployment have also risen slightly. But on a personal level, households appear more optimistic about their own financial situation. As was the case last month, there is no change in their savings intentions.

People familiar with the matter said the Bank of Japan see little need to shift their policy stance of gradually hiking interest rates after the ruling coalition lost its majority in the Upper House last Sunday. The risk is for a considerably looser fiscal policy amid PM Ishiba’s LDP and Komeito party caving to opposition demands, potentially lifting inflation – which is above the 2% target for three years already – even further. But for now the BoJ would simply monitor the situation rather than preemptively act on it. The central bank meets next week and the people added that the 0.5% base rate would probably stay there against the backdrop of trade negotiations with the US still ongoing.

Gold’s (XAU/USD) Price Forecast: Will Gold Gain Acceptance Above the $3400/oz Handle?

Gold prices are making a fresh play for the $3400/oz handle, but will a break prove to be sustainable or not? This question remains front and center as trade tensions rise once more.

The precious metal peaked just above the $3400 handle but failed to hold before a selloff saw the precious metals price drop to around the $3384/oz handle in the European session

Trade Tensions on the Rise

Gold prices have benefitted this week as trade tensions remain front and center especially between the US and EU. Trade tensions between the U.S. and the EU have grown as the EU plans new measures to counter tariffs threatened by President Trump.

According to a Wall Street Journal report, Trump has raised the proposed baseline tariff rate to 15-20%, up from the previously mentioned 10%. This change disrupted the EU’s plans, which were based on a 10% tariff rate.

In response, Germany, along with France and other European countries, has taken a tougher stance against the U.S. A German official reportedly said, “If they want war, they will get war.” If no trade deal is reached before the August deadline, tensions could worsen and disrupt global trade.

If these tensions do not come to a positive conclusion that could be the catalyst Gold prices need for acceptance above the $3400/oz mark.

US Dollar Struggles as DXY Breaks Trendline

Another factor working in favor of higher Gold prices comes courtesy of the US Dollar and the US Dollar Index (DXY).

As BoE President Bailey put it, Dollar shorts is the most crowded trade at present and that is showing.

Looking at the DXY on the H4 chart below, there is strong support being provided by the 100-day MA which rests at 97.67. A break of this support level could lead to further downside with support at 97.26 and 96.90 respectively.

If the DXY is to stage a recovery, a break above the 200-day MA will be needed. The RSI period 14 did bounce off the 50 neutral level which could be seen as a positive sign that could lead to a bounce for the US Dollar index.

US Dollar Index (DXY) Daily Chart, July 22, 2025

Source: TradingView (click to enlarge)

Outlook Moving Forward

Data remains sparse from the US this week with trade deals and earnings likely to drive sentiment.

Later in the week we have some US housing data which could impact the US Dollar as well as S&P PMI data which would shed further light on the US economy

However, I still see trade deals being the key to the US Dollar, market sentiment and Gold prices for the rest of the week.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Technical Analysis - Gold (XAU/USD)

From a technical standpoint, Gold has broken above the 3400/oz mark.

A daily candle close above this level is needed and this would strengthen the probability of further upside.

Gold has been printing higher highs since bottoming out on June 30. The precous metal is also trading in a triangle pattern and is approaching the upper band of the pattern.

A break and daily candle close close above this level could lead to a move of around $386 which could push Gold close to the 3800/oz handle.

A rejection of the upper band of the triangle pattern could lead to a retest of immediate support of the 3400 handle before the 3375 and 3350 handles come into focus.

Gold (XAU/USD) Daily Chart, July 22, 2025

Source: TradingView (click to enlarge)

Client Sentiment Data - XAU/USD

Looking at OANDA client sentiment data and market participants are indecisive on Gold with 51% of traders net-long. I prefer to take a contrarian view toward crowd sentiment but the current data shows the indecision and uncertainty by market participants when it comes to the direction for gold prices moving forward.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1635; (P) 1.1676; (R1) 1.1737; More...

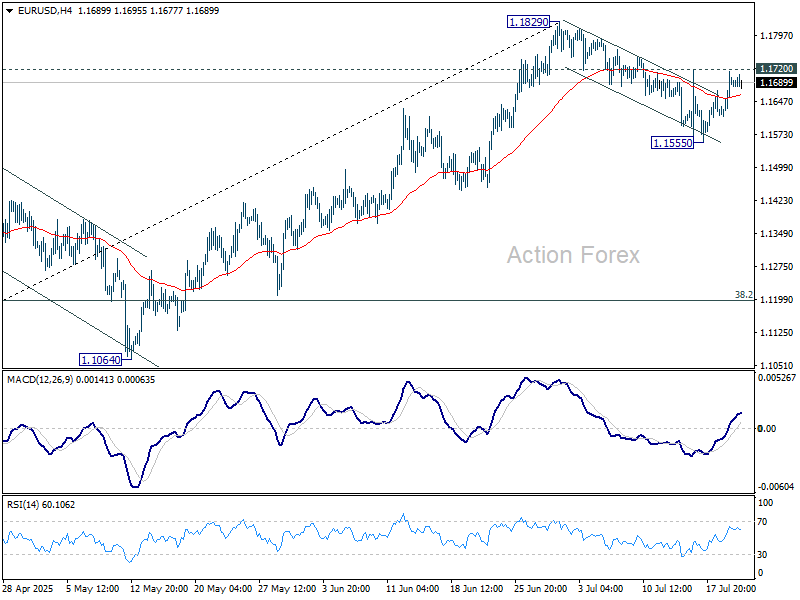

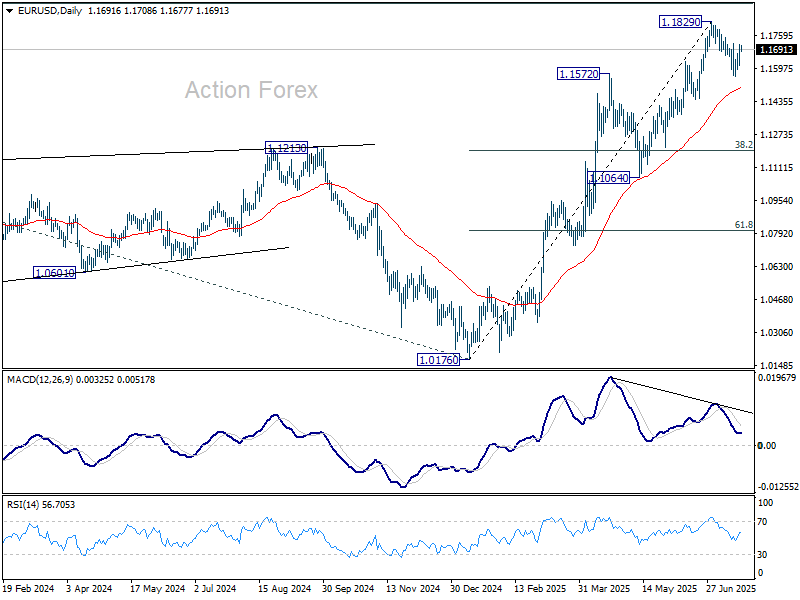

Intraday bias in EUR/USD stays neutral and outlook is unchanged. On the upside, break of 1.1720 minor resistance will suggest that corrective pullback from 1.1829 has already completed at 1.1555. Intraday bias will be back on the upside for retesting 1.1829. On the downside, below 1.1555 will extend the correction towards 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

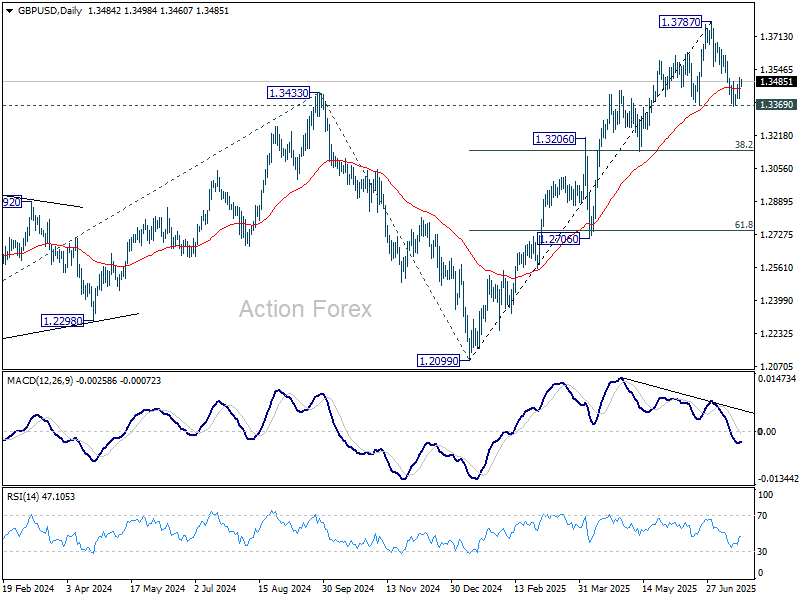

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3426; (P) 1.3468; (R1) 1.3535; More...

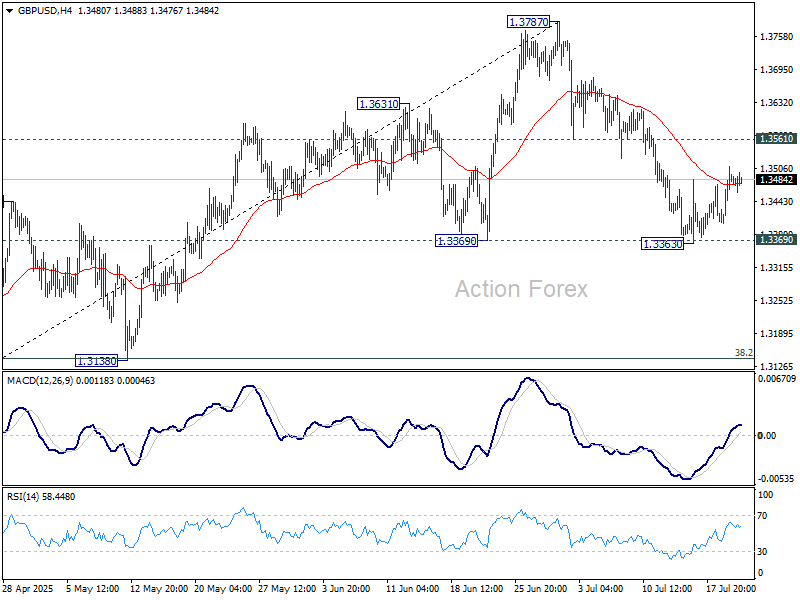

No change in GBP/USD's outlook and intraday bias stays neutral. On the upside, firm break of 1.3561 support turned resistance will argue that correction from 1.3787 has already completed after hitting 1.3369 support. Intraday bias will be back on the upside for retesting 1.3787. Nevertheless, firm break of 1.3363/9 will bring deeper correction to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142).

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3017) holds, even in case of deep pullback.

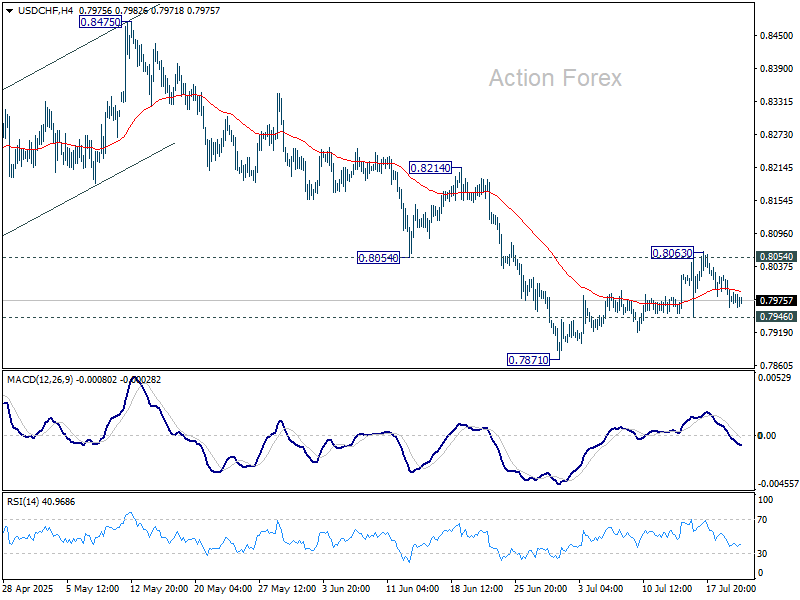

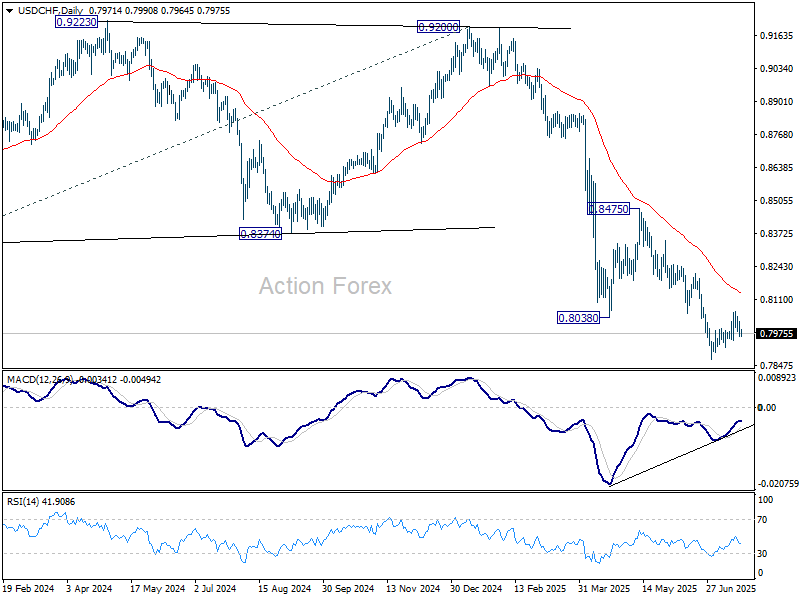

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7957; (P) 0.7990; (R1) 0.8014; More….

No change in USD/CHF's outlook and intraday bias stays neutral. On the downside, break of 0.7946 support will argue that correction from 0.7871 has completed at 0.8063 after rejection by 0.8054 support turned resistance. Intraday bias will be back on the downside for retesting 0.7871. Nevertheless, firm break of 0.8054/63 will bring stronger rebound to 55 D EMA (now at 0.8139).

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

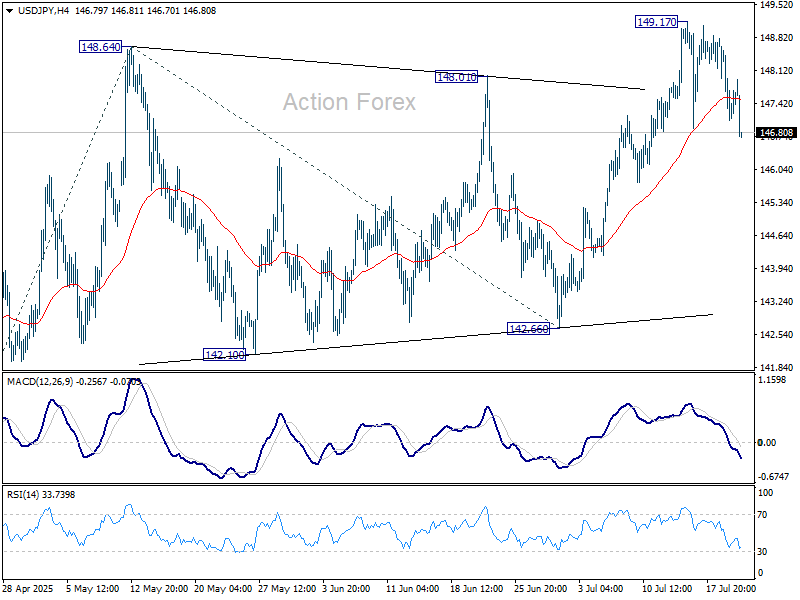

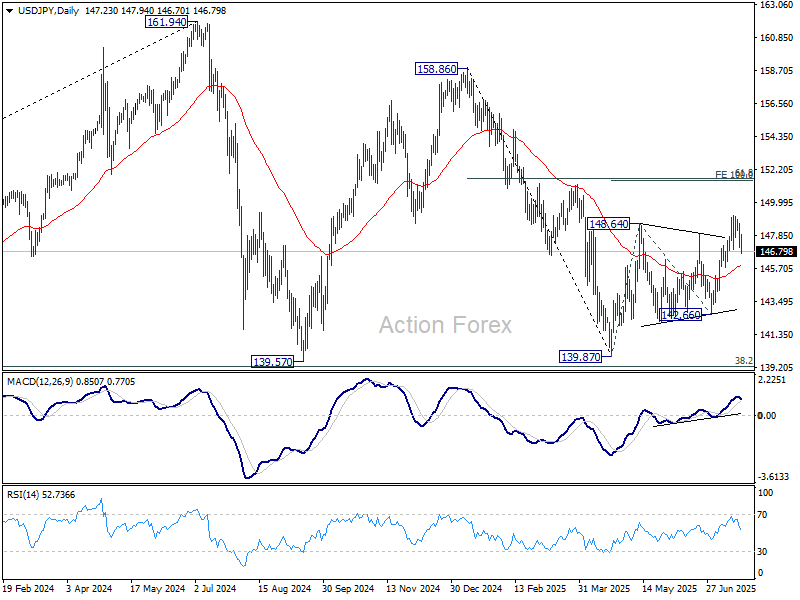

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.72; (P) 147.70; (R1) 148.31; More...

USD/JPY's fall from 149.17 extends lower today, but it's still viewed as a correction to rise from 142.66 only. Intraday bias remains neutral and further rally is expected as long as 55 D EMA (now at 145.91) holds. On the upside, break of 149.17 will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. However, sustained trading below 55 D EMA will argue that the whole rebound from 139.87 might have completed and target 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. in case of another fall.

Trade War Fears Pressure Euro Stocks as EU Retaliation Risks Grow

European Markets are increasingly uneasy over signs that the EU is preparing serious retaliatory measures ahead of the August 1 US tariff deadline. The Anti-Coercion Instrument is increasingly in the spotlight, as EU leaders weigh how to respond to US President Donald Trump’s threat of sweeping 30% import tariffs. European equities are firmly in the red, with DAX and CAC losses amplified by soft earnings, while US futures remain relatively stable.

According to reports, the EU is open to negotiating a tariff framework that resembles the UK’s deal—swallowing a 10% base rate while preserving core industries such as autos and aerospace. However, anything above 15% could prompt a forceful response, especially given the political sensitivity of industrial exports in member states like Germany and France.

Brussels is now openly discussing activating the ACI, which grants the EU power to impose a wide range of retaliatory measures. These could target public procurement, limit access for US companies in agriculture and chemicals, and extend to services where the US runs surpluses. While seen as a last resort, sentiment is shifting toward actual deployment if Trump follows through. The ACI is increasingly viewed as more than a symbolic threat.

In currency markets, the risk-off mood is visible. Aussie and Kiwi are underperforming, joined by a weaker British Pound. Yen is the top performerm with Loonie and Swiss Franc close behind. Euro and Dollar are positioning in the middle.

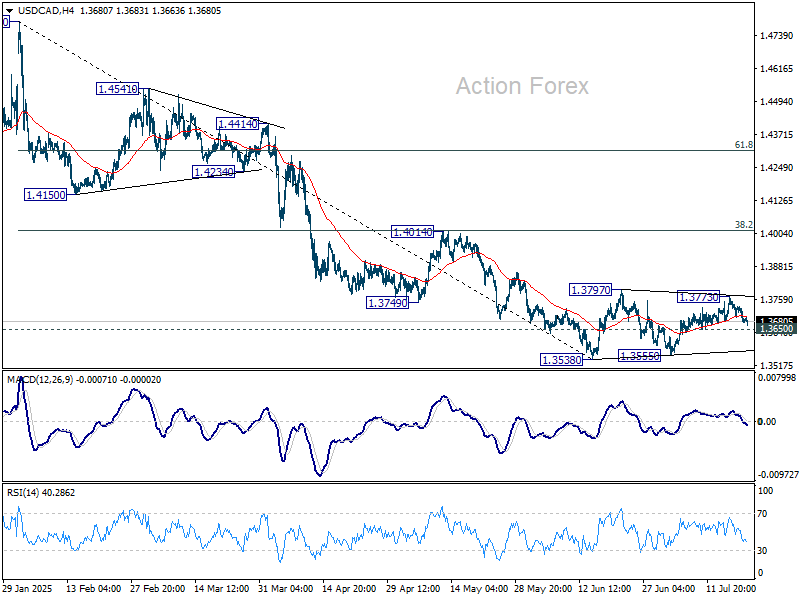

Technically, USD/CAD is worth a watch as the fall from 1.3772 extends today. Break of 1.3650 support will argue that corrective pattern from 1.3538 might have completed already. Larger fall from 1.4791 might then be ready to resume through 1.3538 low.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is down -1.16%. CAC is down -0.82%. UK 10-year yield is up 0.006 at 4.613. Germany 10-year yield down -0.007 at 2.612. Earlier in Asia, Nikkei fell -0.11%. Hong Kong HSI rose 0.54%. China Shanghai SSE rose 0.62%. Singapore Strait Times rose 0.03%. Japan 10-year JGB yield fell -0.025 to 1.507.

Fed’s Bowman: Independence also requires listening, transparency

Fed Vice Chair for Supervision Michelle Bowman reaffirmed the central bank’s commitment to policy independence during an interview with CNBC, stating that "it's very important... that we maintain our independence with respect to monetary policy."

Meanwhile, she stressed that this autonomy must be matched by a commitment to openness. “We have an obligation for transparency and accountability as well,” she noted.

Bowman also stressed the importance of listening to a wide range of voices in forming monetary policy. Since joining the Board in 2018, she said the Fed has consistently engaged with diverse viewpoints to better understand how different segments of the economy are affected.

"That should influence our decisions in monetary policymaking," she said.

BoE's Bailey: Rising gilt yields part of global trade and fiscal uncertainty

BoE Governor Andrew Bailey told the Treasury Committee that the recent rise in long-term borrowing costs reflects global trends rather than UK-specific issues. Responding to questions on the growing cost of government debt, Bailey emphasized that similar, or even steeper, yield increases have occurred in other advanced economies.

He attributed the shift to heightened uncertainty on two key fronts: "one is uncertainty around what is going on in trade policy at the moment. The second thing is uncertainty globally around fiscal policy he said.

Bailey noted that unpredictable tariff strategies and widening fiscal deficits are contributing to volatility in fixed income markets worldwide, driving up yields across the curve. “It is greater uncertainty, clearly,” he said.

RBA minutes: Case for easing intact, but timing still debated

Minutes from the RBA’s July 7–8 meeting reveal a Board broadly aligned on the view that there will be "some additional reduction in interest rates over time". Yet, the board is divided on the "appropriate timing and extent of further easing". The majority ultimately judged it prudent to keep the cash rate steady at 3.85%.

The decision to hold reflected stronger-than-expected recent data, including "a little stronger than expected" private demand in Q1 and resilient labor market that " has not eased as anticipated". Monthly inflation readings had also been "marginally higher" than staff projections. Additionally, Members noted that reduced global risks allowed greater confidence in the RBA’s baseline forecasts, rather than the worst-case scenario.

Still, the minutes make clear that the RBA remains on an easing path. Some members argued there was already enough evidence to justify a cut now, but the Board as a whole leaned toward keeping a cautious, gradual approach, which is inconsistent with a third rate cut within the space of four meetings at that time.

New Zealand imports jump 19% yoy in June, while exports rise 10% yoy

New Zealand posted a trade surplus of NZD 142m in June, falling well short of market expectations for NZD 1.02B. The softer balance came despite solid annual growth in both exports and imports. Goods exports rose 10% yoy to NZD 6.6B and imports surging 19% to NZD 6.5B.

Regionally, exports to the EU jumped 38% yoy, followed by gains to China (11% yoy) and Australia (16% yoy). However, exports to the US and Japan declined -8.8% yoy and -4.7% yoy respectively.

The strength in exports was not enough to offset the broader pressure from surging imports, particularly as US ( 21% yoy) and South Korean (40% yoy) shipments rose sharply. Imports from EU (0.8% yoy), Australia (6.8% yoy) and China (9.1% yoy) also grew.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.72; (P) 147.70; (R1) 148.31; More...

USD/JPY's fall from 149.17 extends lower today, but it's still viewed as a correction to rise from 142.66 only. Intraday bias remains neutral and further rally is expected as long as 55 D EMA (now at 145.91) holds. On the upside, break of 149.17 will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. However, sustained trading below 55 D EMA will argue that the whole rebound from 139.87 might have completed and target 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. in case of another fall.

Fed’s Bowman: Independence also requires listening, transparency

Fed Vice Chair for Supervision Michelle Bowman reaffirmed the central bank’s commitment to policy independence during an interview with CNBC, stating that "it's very important... that we maintain our independence with respect to monetary policy."

Meanwhile, she stressed that this autonomy must be matched by a commitment to openness. “We have an obligation for transparency and accountability as well,” she noted.

Bowman also stressed the importance of listening to a wide range of voices in forming monetary policy. Since joining the Board in 2018, she said the Fed has consistently engaged with diverse viewpoints to better understand how different segments of the economy are affected.

"That should influence our decisions in monetary policymaking," she said.

BoE’s Bailey: Rising gilt yields part of global trade and fiscal uncertainty

BoE Governor Andrew Bailey told the Treasury Committee that the recent rise in long-term borrowing costs reflects global trends rather than UK-specific issues. Responding to questions on the growing cost of government debt, Bailey emphasized that similar, or even steeper, yield increases have occurred in other advanced economies.

He attributed the shift to heightened uncertainty on two key fronts: "one is uncertainty around what is going on in trade policy at the moment. The second thing is uncertainty globally around fiscal policy he said.

Bailey noted that unpredictable tariff strategies and widening fiscal deficits are contributing to volatility in fixed income markets worldwide, driving up yields across the curve. “It is greater uncertainty, clearly,” he said.

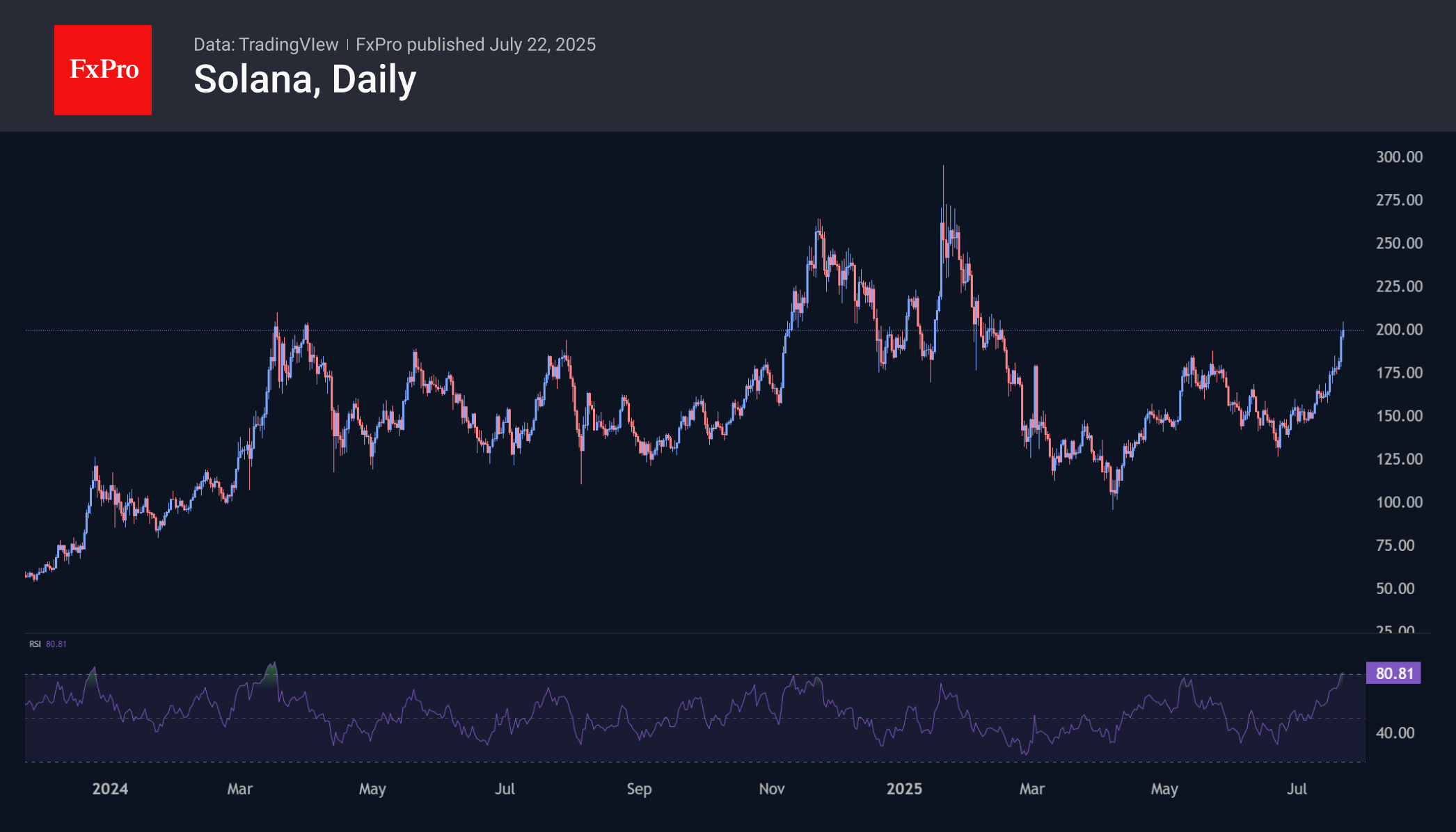

Bitcoin Bounces Off Support, Solana Enters Overbought Territory

Market Overview

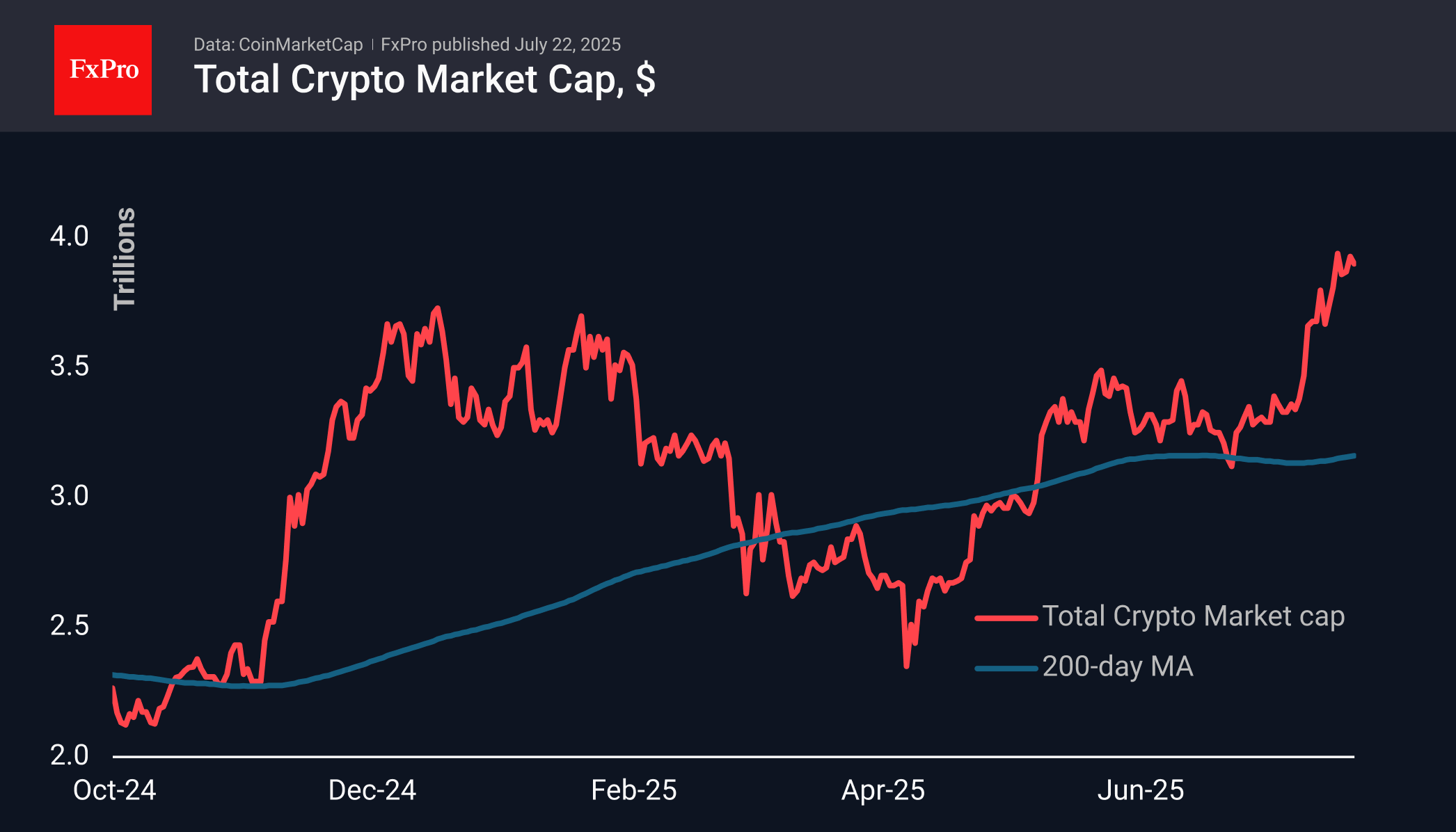

The crypto market capitalisation has declined by 1.4% over the past 24 hours to $3.9 trillion. At the end of Monday, pressure on Bitcoin spread to the market, halting growth in several altcoins.

The sentiment index remains at a comfortable level of 72, just short of the extreme greed zone. According to this metric, the market is not overheated, which preserves the potential for growth to accelerate. The optimal scenario for this would be a resumption of positive momentum in BTC.

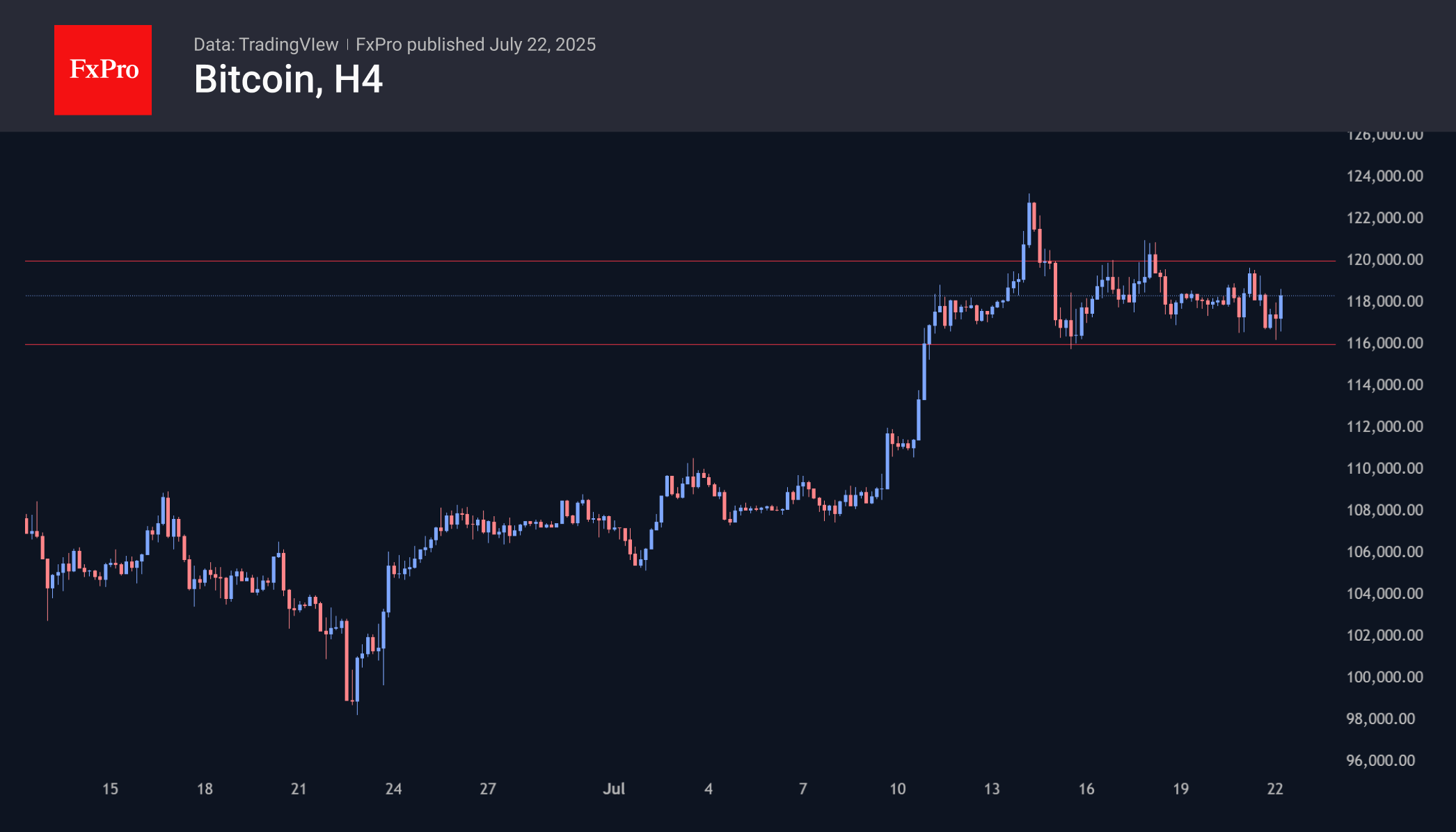

Bitcoin slipped to $116K on Tuesday morning, the lower limit of the consolidation range of the last 10 days. However, during the European session, the price returned to the centre of this range, close to $118K. We will be able to talk about the end of consolidation if the price rises above $120K, which will signal a resumption of growth after a slight shake-up. An alternative scenario would be a deepening of the correction.

The price of Solana exceeded $200, returning to levels last seen in February. The RSI rose to 80, which in recent years has often triggered corrective pullbacks when the index (not the price) began to decline.

News Background

The ethPandaOps team said the next major Fusaka update will be deployed on the Ethereum network in early November. Ethereum developers will launch public test networks in September and October.

Large holders of the first cryptocurrency increased their transfers of coins to crypto exchanges by 60% over the week, which may indicate profit-taking against the backdrop of market growth, CryptoQuant notes.

The UK government is considering selling 61,000 confiscated bitcoins ($7.1 billion) to cover the budget deficit.

According to Glassnode’s calculations, new investors have invested more than $16.75 billion in Bitcoin over the past two weeks, indicating growing optimism in the market. However, retail interest in BTC remains subdued despite reaching a new all-time high.