Sample Category Title

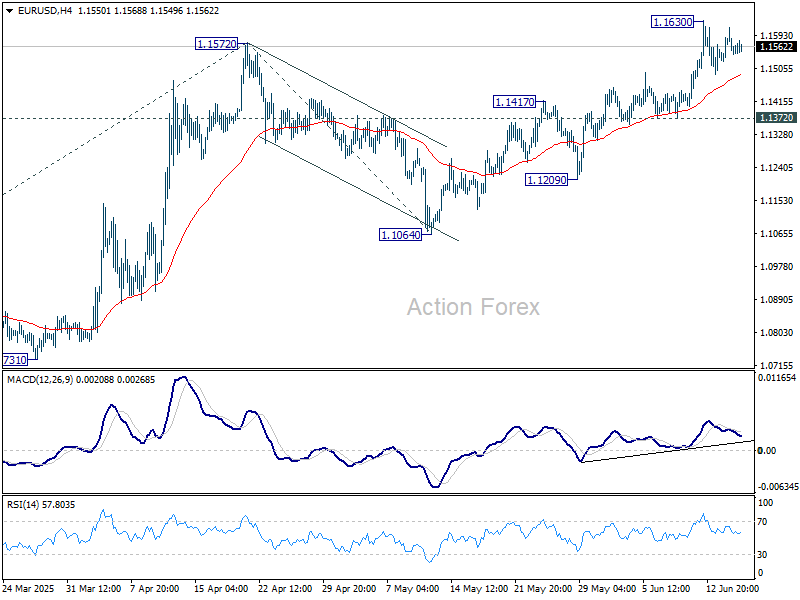

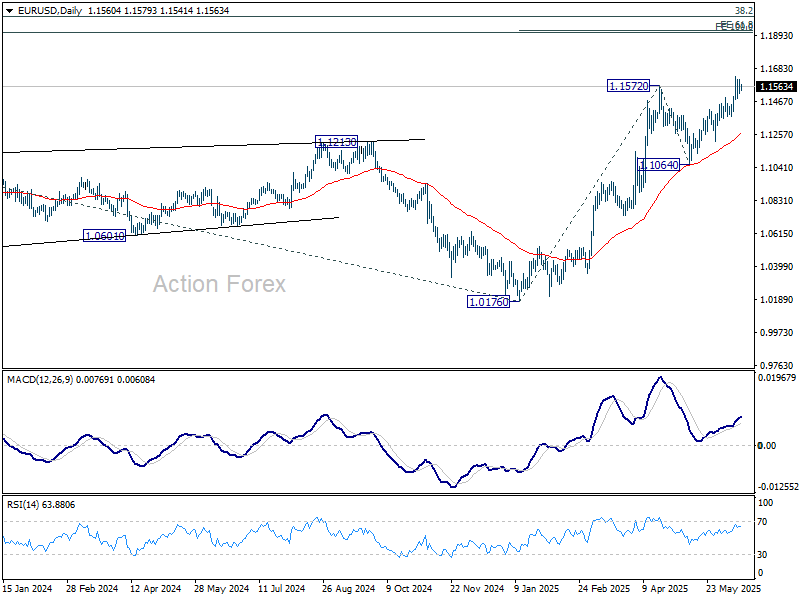

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1517; (P) 1.1566; (R1) 1.1608; More...

Intraday bias in EUR/USD remains neutral as consolidations continues below 1.1630 temporary top. With 1.1372 support intact, further rally is expected. Break of 1.1572 will extend the rise from 1.0176. Next target is 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, break of 1.1372 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

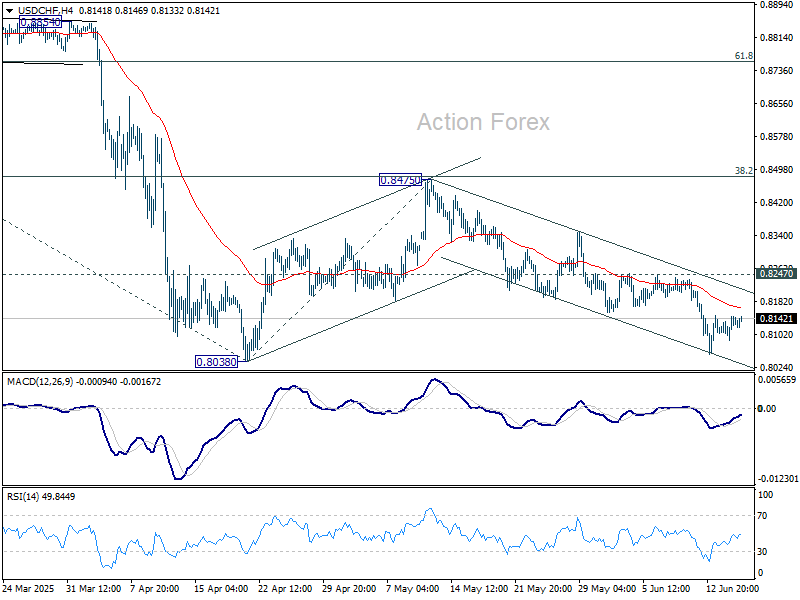

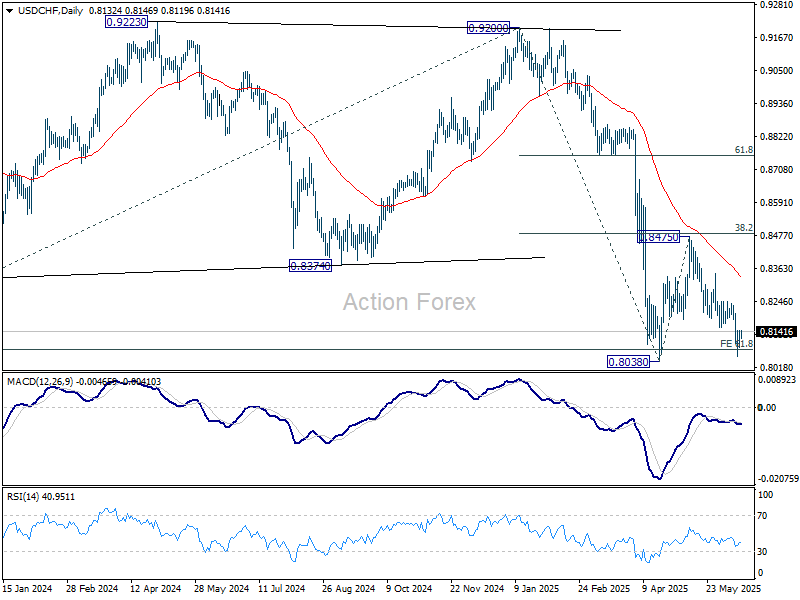

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8103; (P) 0.8125; (R1) 0.8161; More….

Intraday bias in USD/CHF stays neutral and outlook is unchanged. On the upside, break of 0.8247 resistance will argue that corrective pattern from 0.8038 is starting the third leg. Bias will be turned back to the upside for 0.8475 resistance again. However, firm break of 0.8038 will resume larger down trend. Next target will be 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8656) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

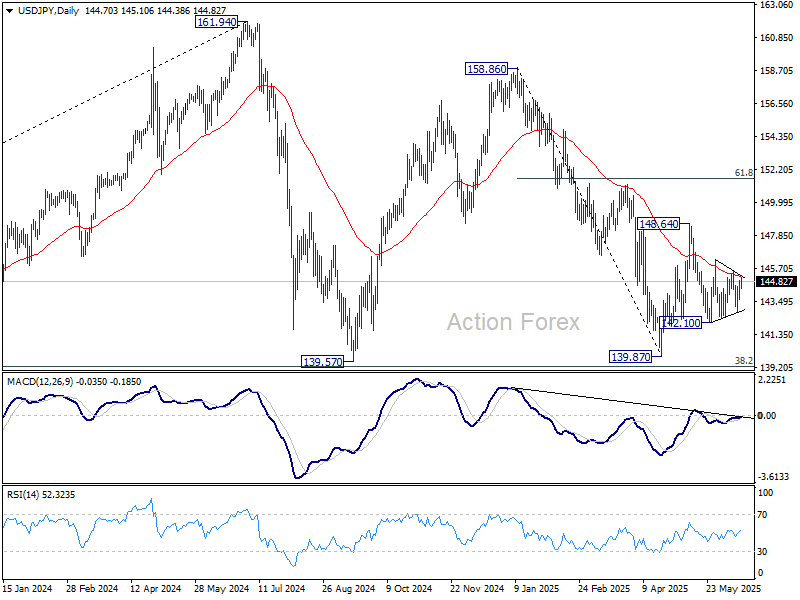

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.00; (P) 144.44; (R1) 145.23; More...

Intraday bias in USD/JPY remains neutral for the moment. On the downside, break of 142.10 support will resume the fall from 148.64 to retest 139.87 low. On the upside, above 145.46 will turn bias to the upside for 146.27 first. Firm break there will target 148.64 resistance.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

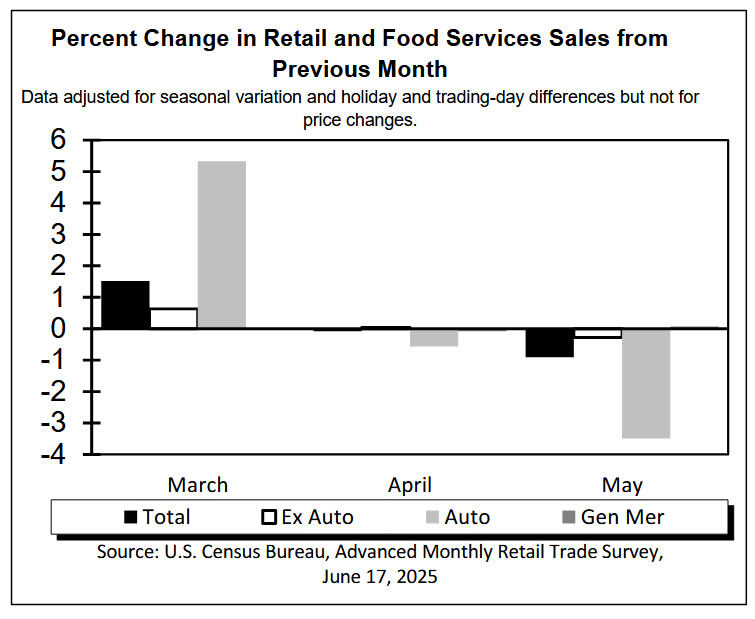

Retail Sales Decline in May as Auto Sales Cool Off

Retail and food services sales declined in May, falling by 0.9% month-on-month (m/m). The headline sales were dragged lower by a drop in motor vehicle and parts sales (-3.5% m/m). April's figures were also revised lower from a 0.1% gain to -0.1% decline.

Sales at gasoline stations were lower on the month, declining for the fourth consecutive month (-2.0% m/m) due to lower prices at the pump. Sales of building materials and equipment stores have also pulled back (-2.7% m/m), following two months of gains ahead of the tariffs.

Sales in the "control group", which excludes the three volatile components mentioned above (i.e., autos, gasoline and building supplies) edged slightly lower (-0.1% m/m). Sales were mixed across most of the remaining categories. Sales pulled back at electronics and appliance stores as tariff front-loading on these goods normalized. However, there were some good gains in other categories, led by miscellaneous stores retailers (+2.9% m/m), sporting goods and book stores (+1.3% m/m) and clothing stores (+0.8% m/m).

Sales at bars and restaurants – the only service category in the report – declined by 0.9% m/m, but this comes on the heels of two months of strong gains.

Key Implications

A flurry of activity in anticipation of tariffs boosted consumer spending earlier this year, but that momentum is now looking to have run its course, with retail sales declining in both April and May. Car sales came back to earth in May, following outsized gains in the prior two months as consumers rushed to replace their vehicles ahead of the tariffs. The same is also true for purchases of building materials, electronics and appliances. Consumers have shown more caution recently, with saving rate moving higher in April - potentially signalling rising precautionary savings. A pullback in spending on dining out, which also eased in May, may further suggest that consumers' willingness to spend on discretionary items might be waning.

Despite the heightened policy uncertainty, key consumer fundamentals, such as the labor market, have shown more resilience than previously expected. The same is true for inflation, which has continued to cool on trend through most of this year. However, we anticipate job growth to slow in the coming months, while inflation is likely to turn higher as higher prices of goods are likely to more than offset the cooling in services inflation. Taken together, we expect that these forces will meaningfully slow consumer spending through the second half of this year.

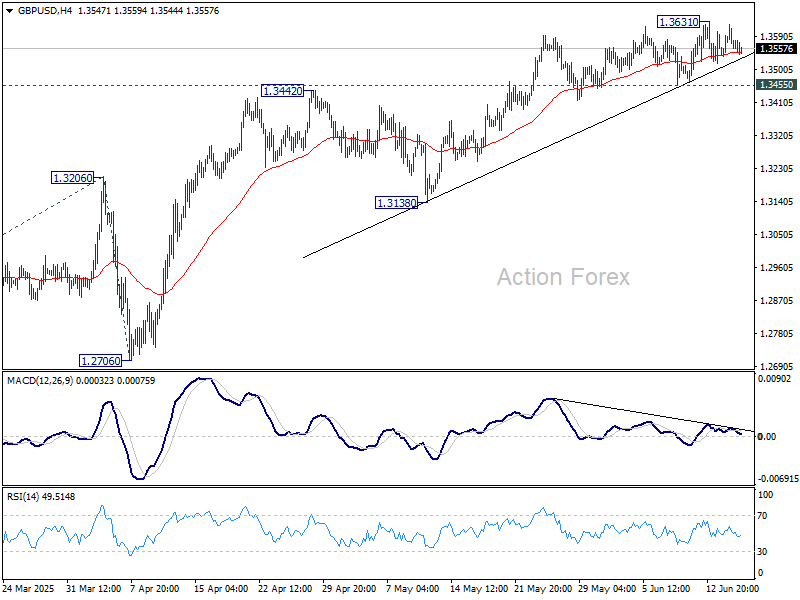

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3534; (P) 1.3578; (R1) 1.3621; More...

Intraday bias in GBP/USD stays neutral as consolidations continue below 1.3631 temporary top. With 1.3455 support intact, further rally is in favor. On the upside, break of 1.3631 will resume the rally from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. On the downside, break of 1.3455 support should confirm short term topping, and bring deeper correction to 55 D EMA (now at 1.3320) instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.

Cautious Calm Holds as Israel-Iran Conflict Continues

Tuesday’s Asian and European sessions saw little conviction across even when geopolitical conflicts in the Middle East persisted. The Israel-Iran conflict, now into its fifth day, is generating concern but not yet panic. Oil and gold, typically sensitive to regional instability, remain rangebound, and equities are slightly softer with no meaningful follow-through on the downside.

Currency markets are similarly directionless. Kiwi and Aussie are leading the day, followed by Yen. Sterling is underperforming, alongside Dollar and Euro. Swiss Franc and Loonie sit in the middle of the pack. This mixed profile speaks to an underlying sense of hesitation.

BoJ’s meeting produced little market reaction, but the newly outlined bond tapering plan has drawn some quiet praise. By mapping out a gradual reduction in JGB purchases for fiscal 2026, BoJ has signaled a willingness to act should long-end yields rise sharply again. While the move is more of a gesture at this stage, it has added to the perception that BoJ full ready a more flexible stance.

With the BoJ out of the way, investor focus now shifts firmly to Fed. While rates are expected to remain unchanged, markets will be parsing Chair Powell’s language closely for any signs of movement on timing for next rate cuts. Meanwhile, BoE and SNB will follow on Thursday, rounding out a critical week for central bank actions.

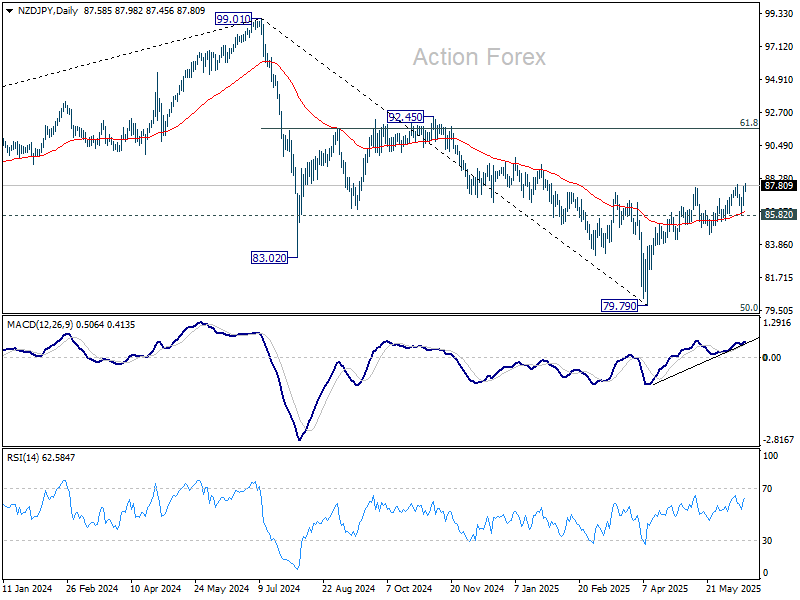

Technically, NZD/JPY is trying to resume the rebound from 79.79. The strong support from 55 D EMA (now at 86.07) keeps near term outlook mildly bullish. The development also affirms the case that whole corrective fall from 99.01 has completed with three waves down to 79.79. Further rally is expected as long as 85.82 support holds, towards 61.8% retracement of 99.01 to 79.79 at 91.66.

In Europe, at the time of writing, FTSE is down -0.33%. DAX is down -0.78%. CAC is down -0.59%. UK 10-year yield is down -0.003 at 4.531. Germany 10-year yield is down -0.002 at 2.523. Earlier in Asia, Nikkei rose 0.59%. Hong Kong HSI fell -0.34%. China Shanghai SSE fell -0.04%. Singapore Strait Times rose 0.57%. Japan 10-year JGB yield rose 0.019 to 1.473.

US retail sales drop sharply by -0.9% mom in May

US retail sales declined more than expected in May, falling -0.9% month-on-month to USD 715.4B, well below the forecasted -0.6% mom drop.

The weakness was broad-based, with ex-auto sales falling -0.3% mom and ex-gasoline sales down -0.8% mom. Even the core control group—excluding autos and gasoline—registered a -0.1% mom decline, suggesting slowing momentum in discretionary consumption.

Despite a solid 4.5% yoy gain for the March–May period, today’s figures raise fresh doubts about the strength of US consumer spending heading into the summer.

German ZEW surges to 47.5, points to post-stagnation recovery

Investor confidence in the Eurozone surged in June, with ZEW Economic Sentiment readings for both Germany and the wider region easily beating expectations.

Germany’s headline sentiment index jumped from 25.2 to 47.5, well above the expected 34.5, while the current situation gauge improved from -82 to -72. Eurozone-wide, sentiment rose from 11.6 to 35.3, and the current conditions index climbed 11.7 points to -30.7.

ZEW President Achim Wambach attributed the "tangible improvement" to growth in investment and consumer demand, adding that fiscal policy announcements from Germany’s new government appear to be supporting confidence.

The data suggests that the prolonged period of stagnation in Europe’s largest economy may be nearing an end. Combined with the ECB’s recent interest rate cuts, momentum may be building toward a long-awaited recovery.

BoJ maintains policy, expects gradual rebound in inflation after near term weakness

BoJ kept its short-term interest rate unchanged at 0.5% in a unanimous decision today, while sticking with its current bond tapering program through March 2026. Looking further out, the central bank introduced a new bond purchase schedule for fiscal 2026, planning to reduce monthly purchases by JPY 200B each quarter, bringing the total to JPY 2T per month by March 2027.

In its statement, the BoJ downgraded its growth outlook, noting that Japan’s economy is “likely to moderate” in the near term as overseas economies slow and domestic corporate profits weaken. While accommodative financial conditions should provide some support, the central bank only expects a modest recovery later as global growth returns.

On inflation, the impact from food and import price increases is "expected to wane", while underlying CPI is likely to remain “sluggish” due to a slowing economy. However, the bank anticipates that inflation will gradually pick up over time, supported by rising medium- to long-term inflation expectations and a growing “sense of labor shortage” as the economy recovers.

BoJ also acknowledged “extremely uncertain" outlook around the global trade and policy environment, warning of spillovers to Japan’s financial markets and inflation outlook. The statement emphasized the need to closely monitor foreign exchange developments and their broader implications.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3534; (P) 1.3578; (R1) 1.3621; More...

Intraday bias in GBP/USD stays neutral as consolidations continue below 1.3631 temporary top. With 1.3455 support intact, further rally is in favor. On the upside, break of 1.3631 will resume the rally from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. On the downside, break of 1.3455 support should confirm short term topping, and bring deeper correction to 55 D EMA (now at 1.3320) instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.

US retail sales drop sharply by -0.9% mom in May

US retail sales declined more than expected in May, falling -0.9% month-on-month to USD 715.4B, well below the forecasted -0.6% mom drop.

The weakness was broad-based, with ex-auto sales falling -0.3% mom and ex-gasoline sales down -0.8% mom. Even the core control group—excluding autos and gasoline—registered a -0.1% mom decline, suggesting slowing momentum in discretionary consumption.

Despite a solid 4.5% yoy gain for the March–May period, today’s figures raise fresh doubts about the strength of US consumer spending heading into the summer.

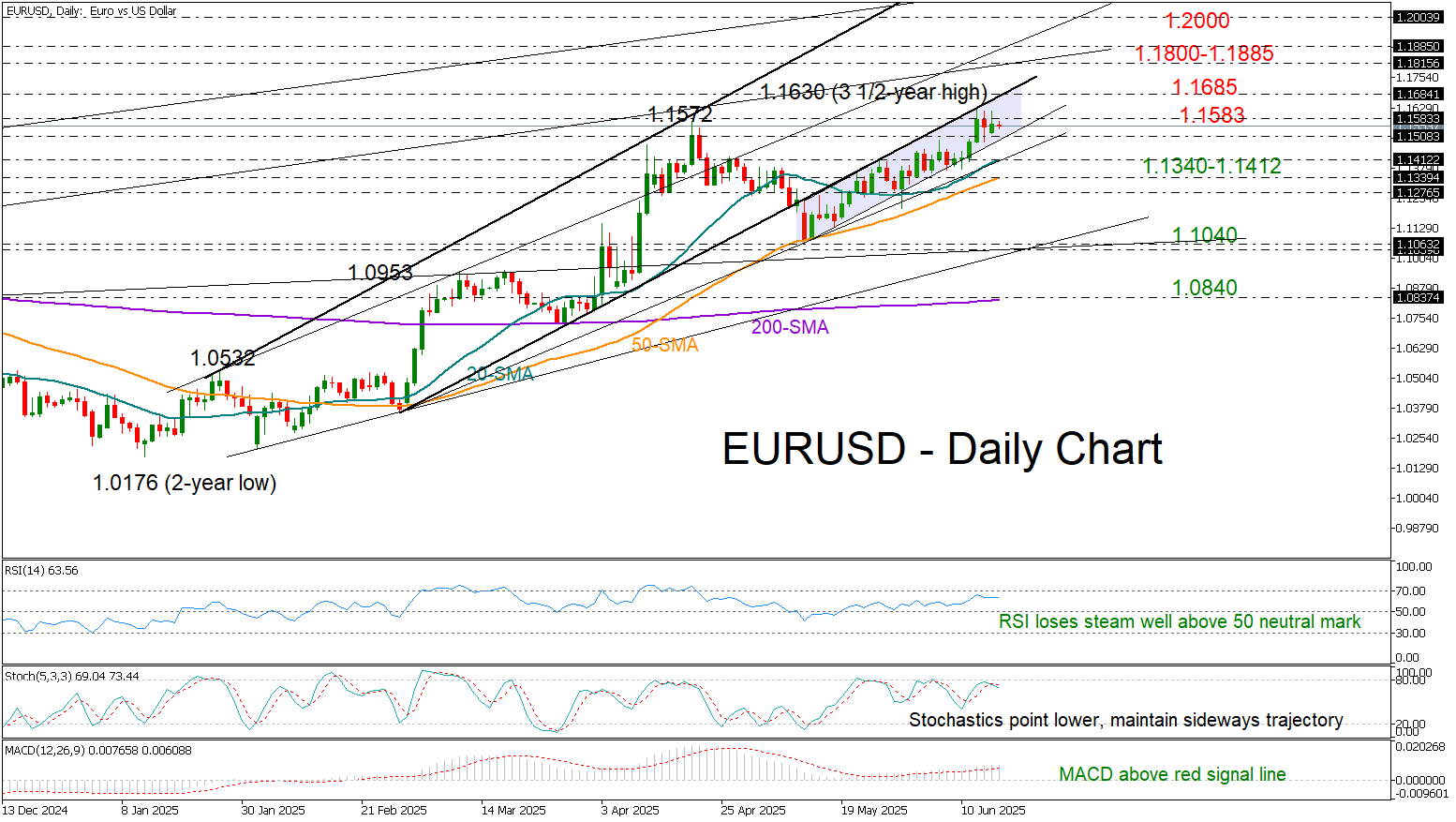

EUR/USD Takes a Breather, But Bullish Bias Intact

- EURUSD stabilizes after 3½-year high as Middle East tensions escalate.

- Technical picture continues to favor the bulls; next barrier likely near 1.1685.

EURUSD surged to a three-and-a-half-year high of 1.1630, following weaker-than-expected U.S. inflation data and a relatively more hawkish commentary from ECB policymakers. However, the outbreak of bombings between Israel and Iran has rekindled risk aversion, pushing the pair to the sidelines.

Yet, the sideways movement has not eliminated hopes for a bullish continuation. Although the RSI and MACD have lost some momentum, both indicators remain comfortably above their neutral levels. Meanwhile, the upward trajectory of the simple moving averages (SMAs) continues to support the bullish trend.

Upcoming U.S. retail sales data will be in focus, with euro bulls hoping for a negative surprise to break above the nearby 1.1583 barrier and advance toward the support-turned-resistance line at 1.1685. Beyond that, the trendline zone between 1.1800 and 1.1885 could delay any further extensions toward the psychological 1.2000 level, last seen in June 2021.

On the downside, a break below the support trendline at 1.1500 could prompt the 20- and 50-day SMAs to provide support in the 1.1340–1.1412 region. If those levels fail to hold and the 1.1275 base also gives way, the sell-off could deepen toward May’s trough and the 1.1040 support zone.

Overall, EURUSD is retaining its bullish appeal despite its recent consolidation phase. A close above 1.1583 could strengthen the uptrend, while a drop below 1.1500 may trigger some profit-taking.

XAU/USD: Gold Remains at the Back Foot But Still Above Key Supports

Gold trades within a narrow range on Tuesday morning, following almost 2% drop on Monday and daily close below psychological $3400 support (reverted to resistance and caps the action for now).

Surprise drop despite escalation of conflict between Israel and Iran still looks as correction and positioning for fresh push higher, as initial support at $3374 (Fibo 23.6% of $3120/$3452/daily Tenkan-sen) contained dip.

Technical picture on daily chart is still bullish (strong positive momentum / Tenkan/Kijun-sen in bullish setup), but Monday’s bearish engulfing warns that downside pressure exists.

Depper pullback will face a trendline support at $3350 and should not exceed $3325 zone (Fibo38.2%) to mark a healthy correction and provide better levels to re-enter bullish market.

Alternatively, key supports at $3286 (daily cloud top reinforced by Kijun-sen / 50% retracement) would come under increased pressure.

Res: 3410; 3437; 3452; 3500.

Sup: 3374; 3350; 3325; 3300.

Bank of Japan Leaves Interest Rate Unchanged

This morning, the Bank of Japan (BOJ) released its interest rate decision, keeping the rate unchanged as widely expected. According to Forex Factory, the BOJ Policy Rate remains at 0.5%.

BOJ Governor Kazuo Ueda noted the following:

→ Japan’s economy is recovering moderately.

→ The Bank will continue raising rates if economic and inflationary conditions improve.

→ The situation surrounding trade tariffs remains highly uncertain.

The fact that the decision was anticipated by markets is reflected in price action on the charts.

Technical Analysis of the USD/JPY Chart

A brief spike in volatility occurred on the USD/JPY chart this morning, but it did not significantly alter the broader structure of price movements, which in June have formed a contracting triangle pattern.

In recent days, the pair has been climbing from the lower boundary of the triangle toward the upper edge, forming a short-term ascending channel (highlighted in blue). However, in the near term, this bullish momentum may weaken as the USD/JPY rate approaches the upper boundary of the triangle, which coincides with the psychologically significant level of 145 yen to the dollar (indicated by arrows).

From a medium-term perspective, traders should watch for a potential breakout from the triangle pattern, which could trigger a meaningful trend. One possible catalyst could be news of a trade agreement between the United States and Japan.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.