Sample Category Title

Fed to holds fire as markets look to July for next cut

Fed is widely expected to leave its benchmark interest rate unchanged at 4.25–4.50% today. With no update to its economic projections or dot plot this time, attention will turn squarely to the post-meeting statement and Chair Jerome Powell’s press conference.

The prevailing message is likely to be one of patience, as policymakers face mounting uncertainties tied to the unresolved tariff war and its eventual economic impact.

Central to Fed's wait-and-see approach is the need for clarity on two fronts: whether US President Donald Trump’s reciprocal tariffs are fully enacted, and how inflation expectations evolve in response. These factors, especially in light of ongoing geopolitical and trade risks, argue against any near-term policy moves.

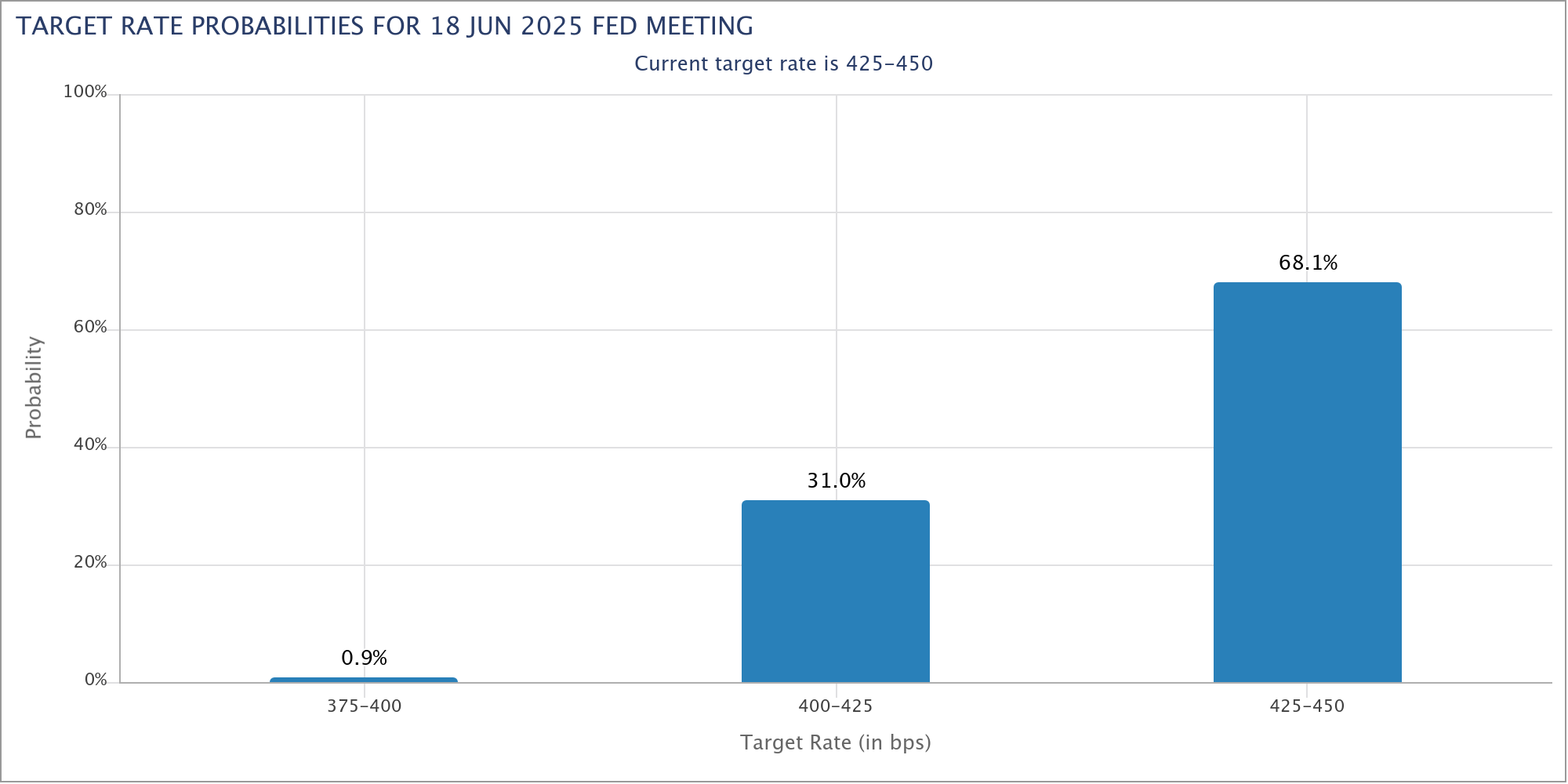

As such, June is seen as too soon for a shift, with the expected to remain on hold until more definitive clarity emerge, probably not until the tariff ceasefire expires in early July.

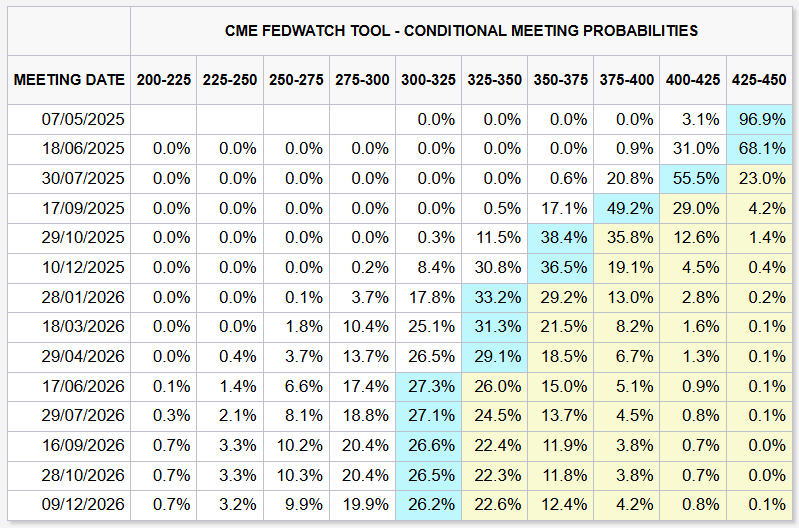

Market pricing reflects this outlook top. Fed funds futures assign just a 32% chance of a cut in June, but expectations firm up thereafter, with roughly 75% probability of three 25 bps cuts by year-end, bringing rates down to 3.50–3.75%.

GBP/USD Bounces Back—All Eyes on Fed’s Next Move

Key Highlights

- GBP/USD found support near 1.3250 and started a fresh increase.

- It cleared a key bearish trend line with resistance at 1.3300 on the 4-hour chart.

- EUR/USD is consolidating above the 1.1250 support zone.

- The Fed will announce interest rates later today (forecast 4.5%, versus 4.5% previous).

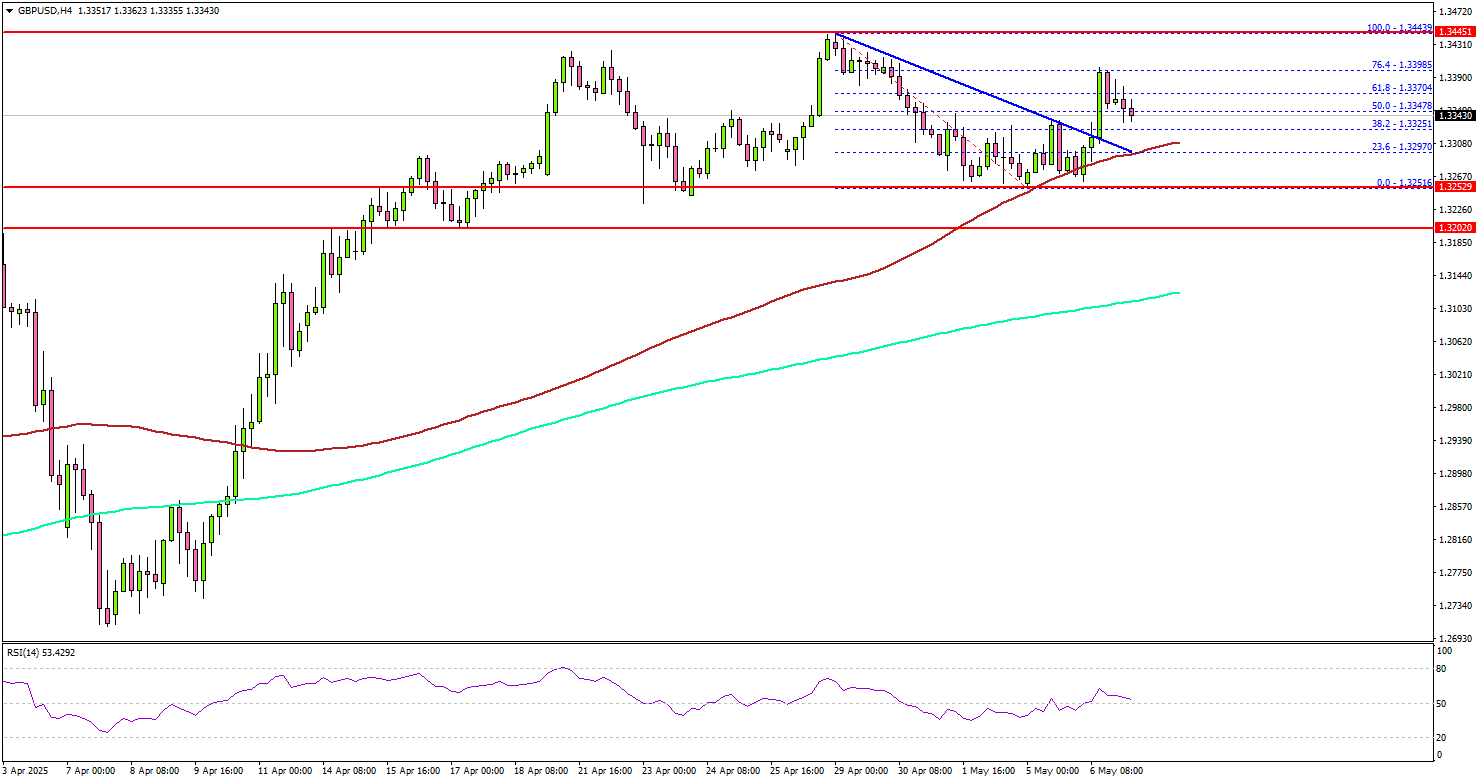

GBP/USD Technical Analysis

The British Pound corrected gains from 1.3445 and tested 1.3250 against the US Dollar. GBP/USD is again rising and aims for a move to a new multi-month high.

Looking at the 4-hour chart, the pair remained well bid above the 1.3250 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). There was a clear move above the 50% Fib retracement level of the downward move from the 1.3443 swing high to the 1.3251 low.

Besides, it cleared a key bearish trend line with resistance at 1.3300 on the same chart. The pair is now facing resistance near the 1.3420 level. The next major resistance is near the 1.3450 zone.

A close above the 1.3450 level could set the tone for another increase. In the stated case, the pair could even clear the 1.3500 resistance. The next major stop for the bulls could be near the 1.3620 level.

On the downside, immediate support sits near the 1.3300 level and the 100 simple moving average (red, 4-hour). The next key support sits near the 1.3250 level. Any more losses could send the pair toward the 1.3120 level.

Looking at EUR/USD, the pair started a consolidation phase above 1.1250 and might struggle to clear the 1.1420 resistance.

Upcoming Economic Events:

- Fed Interest Rate Decision - Forecast 4.5%, versus 4.5% previous.

PBoC unleashes broad-based monetary easing including rate and RRR cuts

China’s central bank has announced a sweeping set of monetary policy measures to support its economy, starting with a 10bps cut in the seven-day reverse repo rate to 1.40%, effective May 8. In a more aggressive move, the PBoC will also slash the reserve requirement ratio by 50bps, releasing approximately CNY 1T into the banking system.

The new package is structured into three categories: quantitative, price-based, and structural tools. The quantitative arm focuses on long-term liquidity via the RRR cut. The price-based measures involve lowering benchmark and structural policy rates. The structural component aims to channel credit into strategic areas such as technological innovation, consumption, and inclusive finance.

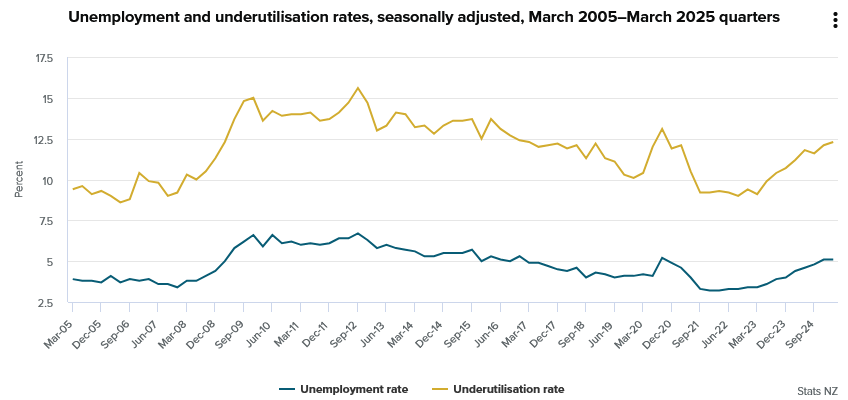

NZ employment grow 0.1% in Q1, wages growth cool

New Zealand’s employment grew just 0.1% qoq as expected, while the unemployment rate held steady at 5.1%, better than forecast of 5.3%.

However, the quality of employment deteriorated, with a notable shift from full-time to part-time roles. Over the year, full-time employment dropped by -45k while part-time roles increased by 25k.

Participation rate edged down to 70.8% and the employment rate slipped to 67.2%, both suggesting a gradual loss in labor market momentum.

Wage growth also moderated, with the labour cost index rising 2.9% annually, down from 3.3% in the previous quarter.

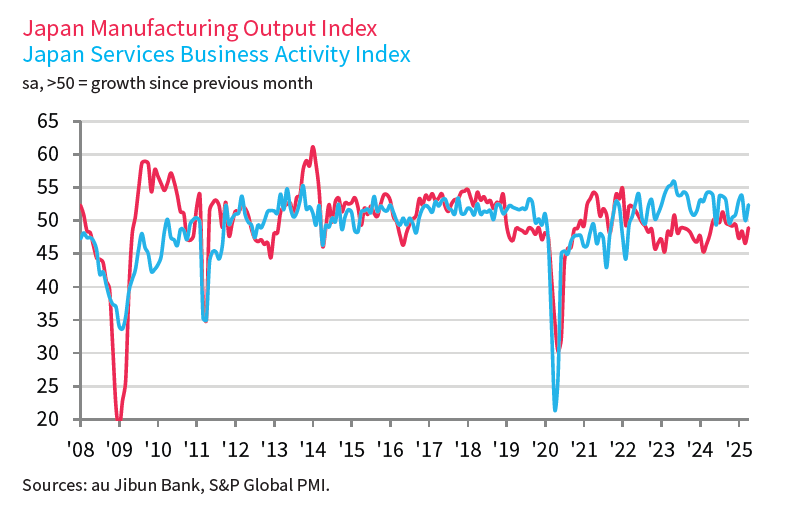

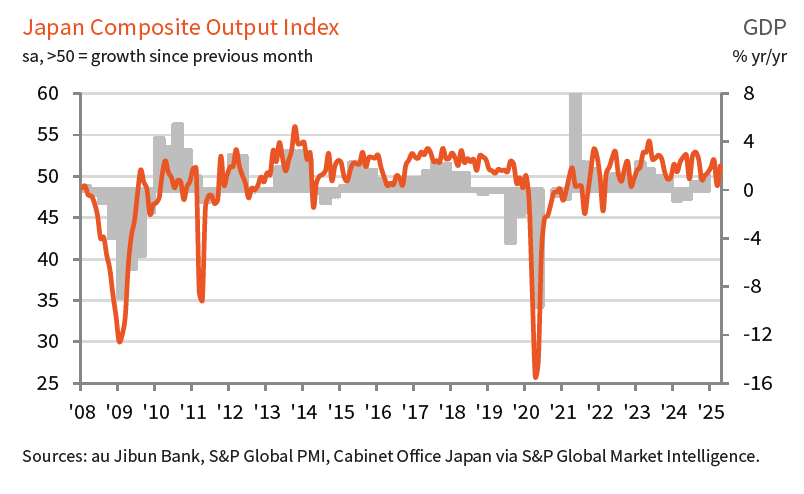

Japan’s PMI composite finalized at 51.2, input inflation jumps to 2-year high

Japan’s private sector returned to expansion in April, as the final PMI Composite rose to 51.2 from March’s 48.9. The improvement was driven entirely by the services sector, with its PMI climbing to 52.4, while manufacturing remained in contraction.

According to S&P Global’s Annabel Fiddes, stronger services activity helped offset the drag from factories, where new orders fell sharply in response to the global tariff environment.

While services firms reported stronger demand, confidence among both services and manufacturing sectors deteriorated. Businesses expressed concern about the broader global outlook and the negative implications of recent US tariff moves on growth potential.

Adding to the pressure, input price inflation accelerated to a two-year high, prompting firms to raise selling prices to protect margins.

First Impressions: NZ Labour Market Statistics, March Quarter 2025

The unemployment rate was steady at 5.1% in the March quarter, better than market expectations. Wage growth continues to slow.

- Unemployment rate: 5.1% (prev: 5.1%, Westpac f/c: 5.3%, RBNZ f/c 5.2%)

- Employment change: +0.1% (prev: -0.2%, Westpac f/c: +0.1%, RBNZ f/c 0.0%)

- Labour costs (private sector): +0.4% (prev: +0.6%, Westpac f/c: +0.4%, RBNZ f/c +0.6%)

The March quarter surveys confirmed that the New Zealand labour market remains subdued, although they weren’t quite as soft in the details as we were expecting. The implications for the Reserve Bank are mixed, with slightly better employment figures but a greater slowdown in wage growth than they had assumed in their February Monetary Policy Statement.

The unemployment rate held steady at 5.1% in the March quarter, against market forecasts for another small rise. The number of people employed rose by 0.1%, much in line with what had been signalled by the Monthly Employment Indicator (MEI). That followed a 0.2% fall in the December quarter (revised down from an initial reading of -0.1%), and leaves employment down 0.7% on a year earlier.

The small rise in employment was almost in line with the 0.2% rise in the working-age population (less than the 0.3% that we had assumed). A further drop in the labour force participation rate accounted for the remainder, leaving the unemployment rate unchanged. While this was only a partial factor in the March quarter results, we’ve seen a marked drop in youth participation in particular in recent quarters, with the tougher jobs market seeing young people returning to or spending longer in study rather than actively looking for work.

The Labour Cost Index (LCI) rose by 0.4% for the private sector, in line with our forecast but below the RBNZ’s expectation of 0.6%. The public sector LCI rose by 0.9%, led by a collective pay agreement for teachers. On an annual basis, the private sector LCI slowed from 2.9% to 2.5%.

The analytical unadjusted LCI, which includes pay increases that are related to higher productivity, rose by 0.7% for the private sector, the smallest quarterly rise since December 2020. Fewer roles have seen pay increases over the last year, and the average size of those increases has moderated.

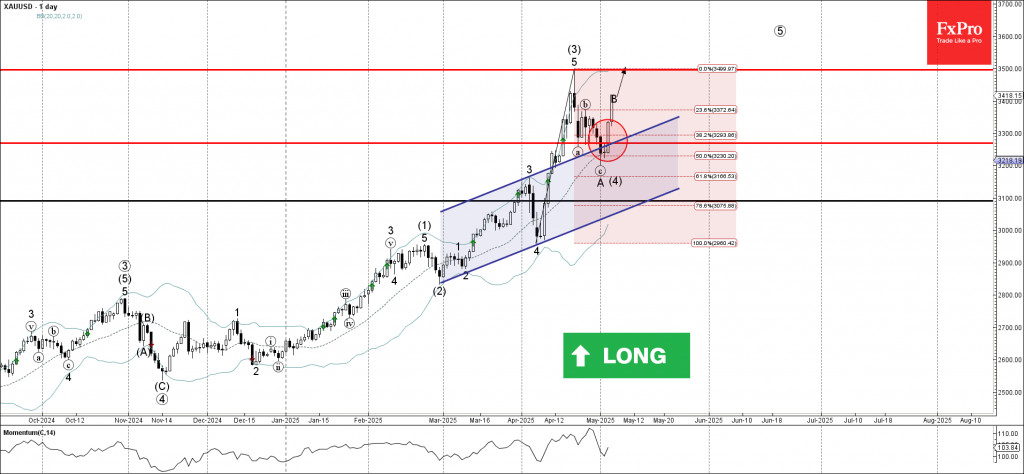

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold reversed from support level 3270,00

- Likely to rise to resistance level 3500.00

Gold recently reversed up the support area between the support level 3270,00 (low of the previous correction a), 20–day moving average and the 50% Fibonacci correction of the upward impulse 5 from April.

The upward reversal from this support area created the daily Japanese candlesticks reversal pattern, Morning Star, which stopped the previous minor ABC correction A.

Given the clear uptrend on the daily charts, Gold can be expected to rise to the next resistance level 3500.00 (which stopped the previous impulse wave (3)).

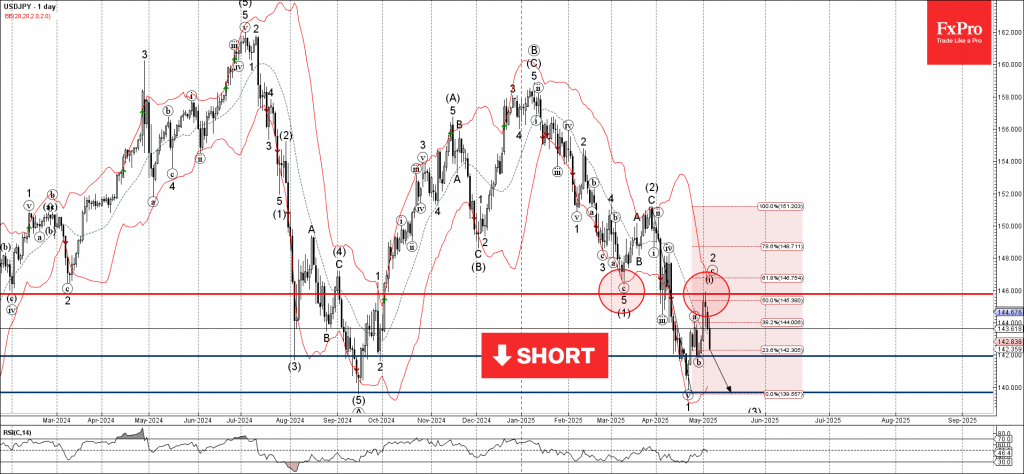

USDJPY Wave Analysis

USDJPY: ⬇️ Sell

- USDJPY reversed from resistance zone

- Likely to fall to support level 140.00

USDJPY currency pair recently reversed from the resistance zone between the resistance level 146.00 (former strong support from March) and the 50% Fibonacci correction of the previous downward impulse from March.

The downward reversal from this resistance zone stopped the previous minor ABC correction 2.

Given the strongly bullish yen sentiment seen today, USDJPY currency pair can be expected to fall to the next support level 142.00 – the breakout of which can lead to further losses toward support level 140.00.

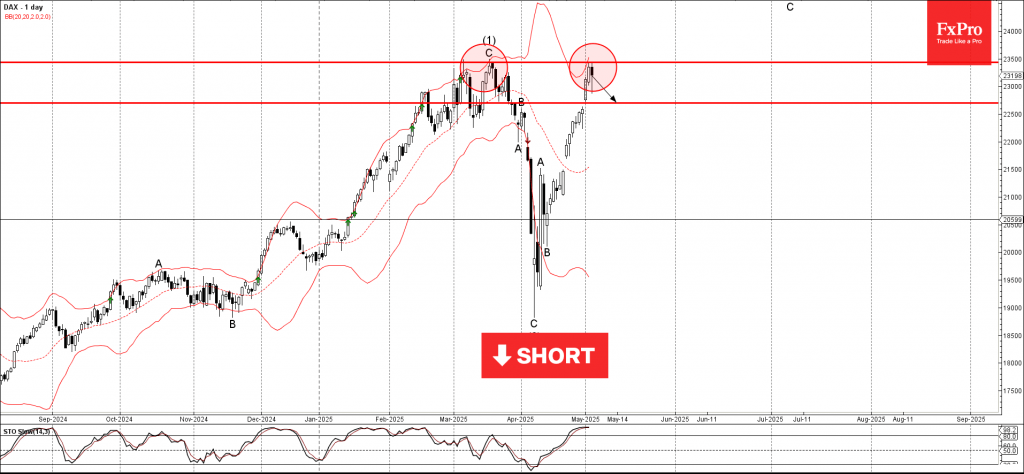

DAX Wave Analysis

DAX: ⬇️ Sell

- DAX reversed from key resistance level 23435,00

- Likely to fall to support level 22700.00

DAX index recently reversed down from the key resistance level 23435,00 (which stopped the previous impulse wave (1) in the middle of March).

The resistance level 23435,00 was further strengthened by the upper daily Bollinger Band.

Given the strength of the resistance level 23435,00 and the overbought daily Stochastic, DAX index can be expected to fall to the next support level 22700.00.