Sample Category Title

US April CPI Preview: The Trend Is Your Friend

Summary

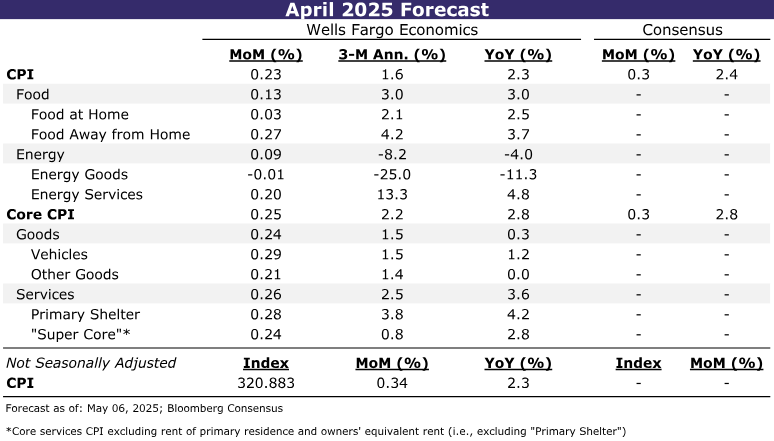

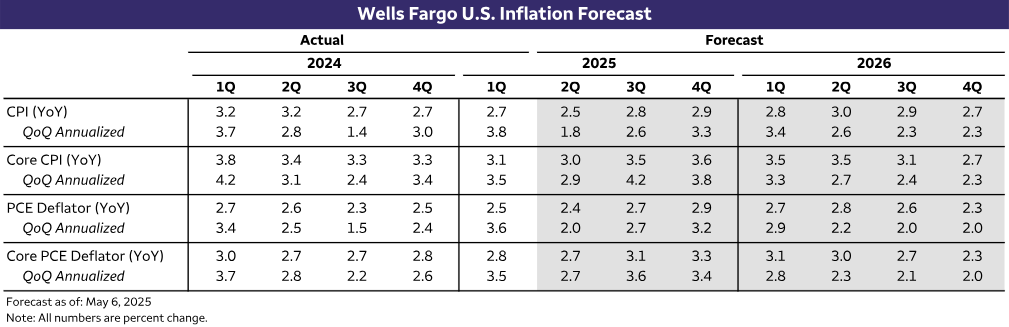

After an unexpected slide in March, the monthly change in the CPI in April is likely to rebound to its six-month trend. We look for the headline CPI to rise 0.2% in April, leading the year-ago rate to dip to a four-year low of 2.3%. We would not be shocked to see a 0.3% rise if some volatile components bounce back more than expected. Excluding food and energy, we forecast the core CPI to rise 0.25%, keeping the annual rate unchanged at 2.8%. Preemptive inventory building and fears of consumer pushback should keep the anticipated acceleration in consumer prices at bay until at least May. Yet beneath the surface, the subsiding trend in core services inflation will be juxtaposed with core goods inflation that is incrementally strengthening.

Sticker Shock on Hold

The March CPI report delivered the best of both worlds. There were few signs of tariffs igniting a widespread pickup in goods prices, while the downward trend in services inflation intensified. A repeat of March's quiescent figures will be hard to come by in April. After slipping 0.1% in March, we estimate headline CPI rebounded 0.23% last month. Core CPI similarly looks set to bounce back from what was the smallest gain in four years (0.06%) with a 0.25% increase in April.

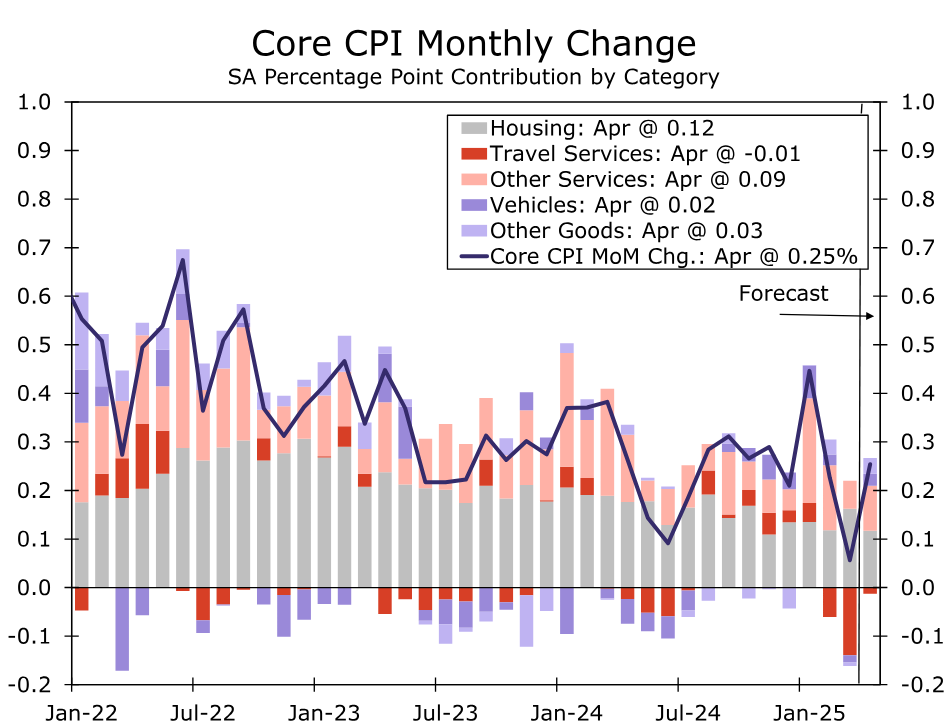

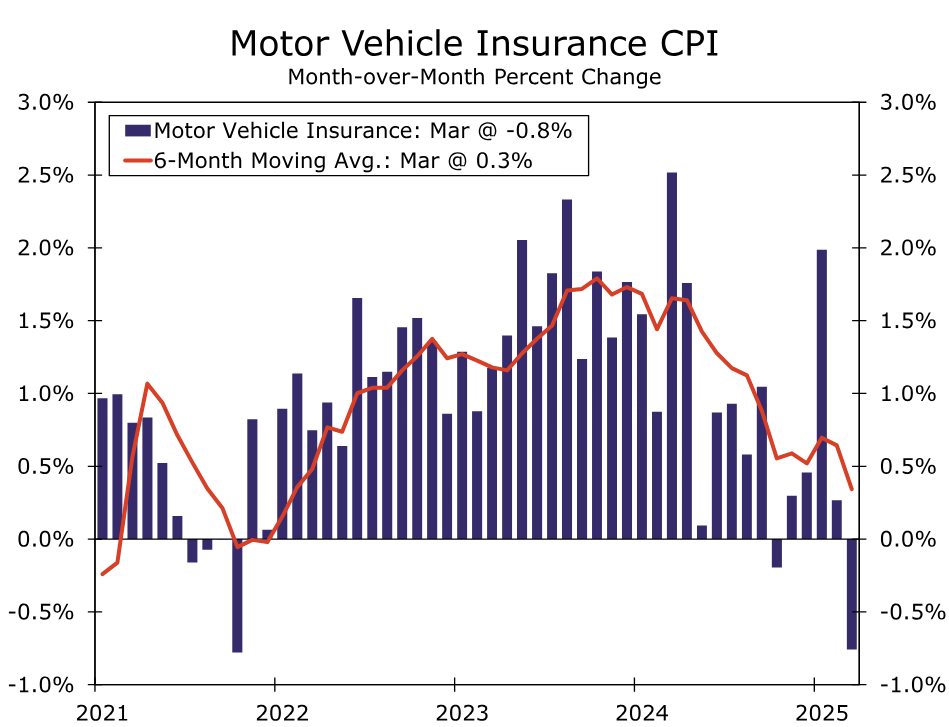

Our expectation for a rebound in April can be traced to the drivers of March's tame reading, which centered on some of the more dynamic components of the CPI. Amid the flurry of federal government cost-cutting efforts and looming "Liberation Day" announcement of tariffs, concerns about the economy sent oil prices, airline fares and hotel prices sharply lower (Figure 1). Seasonal factors exacerbated the weakness, but seasonals will not be so friendly in April. We look for energy goods prices to be flat on the month and for travel-related services prices to decline less sharply (-0.4% in April versus -3.8% in March). Vehicle and insurance prices also look set for a rebound. Auto tariffs likely led auto dealers to hold a firmer line on pricing, while March's 0.8% decline in motor vehicle insurance prices overstated the underlying trend (Figure 2).

At the same time, give-back in pricing of categories that saw outsized increases in March should keep a lid on services inflation in April. We anticipate primary shelter inflation to have eased in April after an above-trend reading in March, and we also look for a smaller increase in medical care services after hospital prices saw the largest gain in more than a year in the last report.

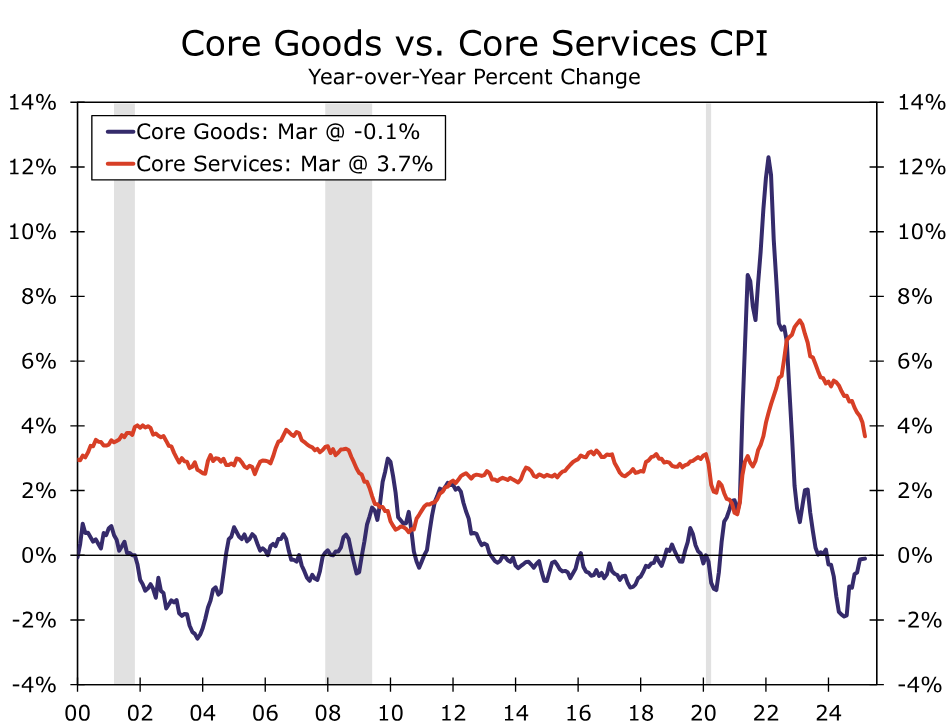

In contrast to the subsiding trend in core services, core goods inflation continues to strengthen. The announcement of sweeping increases to import duties at the start of the month stands to send the pickup in goods inflation into overdrive, although we do not expect April to be a light-switch moment. The pull-forward of imports, efforts not to alienate customers and general confusion over policy changes are likely to result in a more incremental strengthening in goods prices. We have penciled in a 0.24% increase in core goods prices for April (including the largest monthly gain in non-vehicle goods prices in more than two years) but expect the monthly pace to be double that by the summer if current trade policy remains in place. The gap between core goods and services inflation should continue to narrow as result (Figure 3).

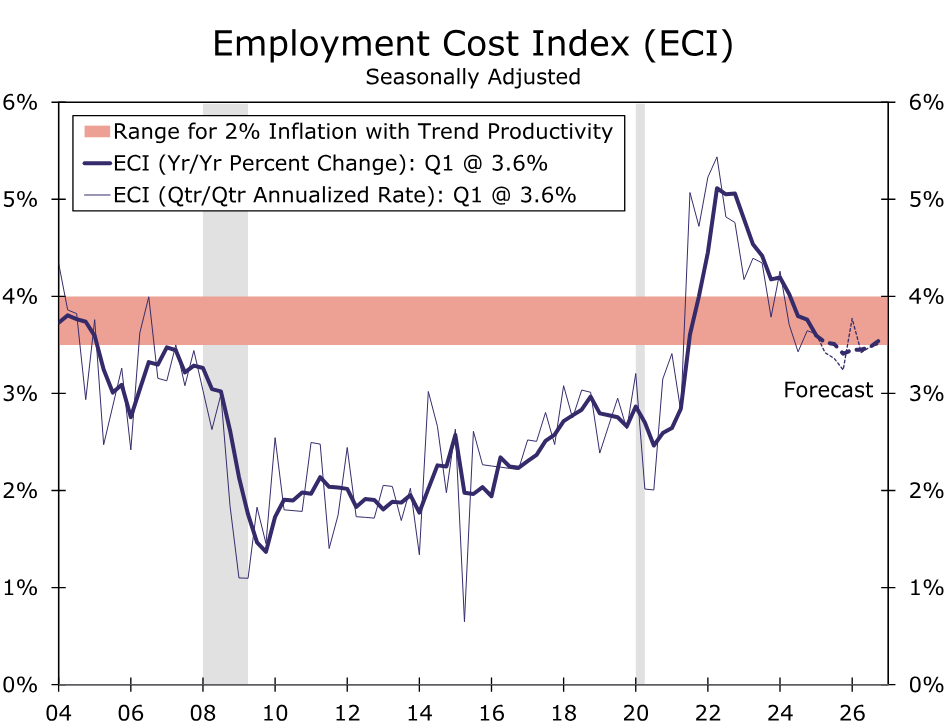

Stepping back, April's monthly gain in headline CPI should push the year-over-rate rate down to a four-year low of 2.3%. The downward trend in core inflation is also likely to appear intact, with the year-ago rate unchanged at 2.8%. But with tariffs no longer merely a threat but a reality, we view it as only a matter of time before higher import costs filter through to consumer prices. We expect the inflationary impulse of tariffs to ramp up in the coming months, leading the core CPI back up to 3.6% by the fourth quarter (Table). Unlike the most recent price shock of the pandemic, trade changes are not occurring in combination with a positive shock to consumer demand and a historic scramble for workers. The less-flush position of households, slower growth in labor compensation costs and lower energy and transportation costs amid the weaker growth backdrop should help to mitigate the tariff-related rise in inflation (Figure 4). But that may be cold comfort to consumers, businesses and the Fed, as ground is lost in the nearly five-year battle to quell inflation.

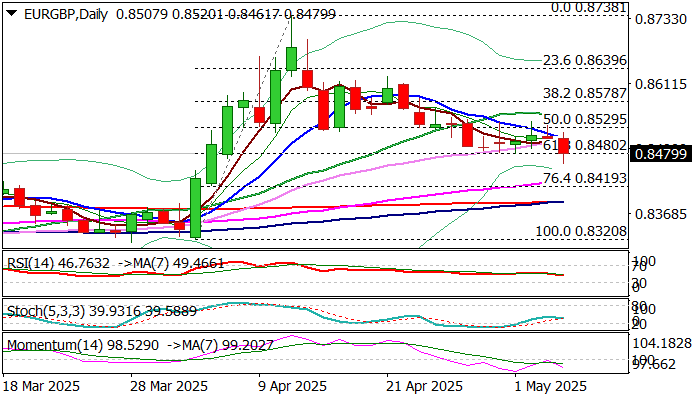

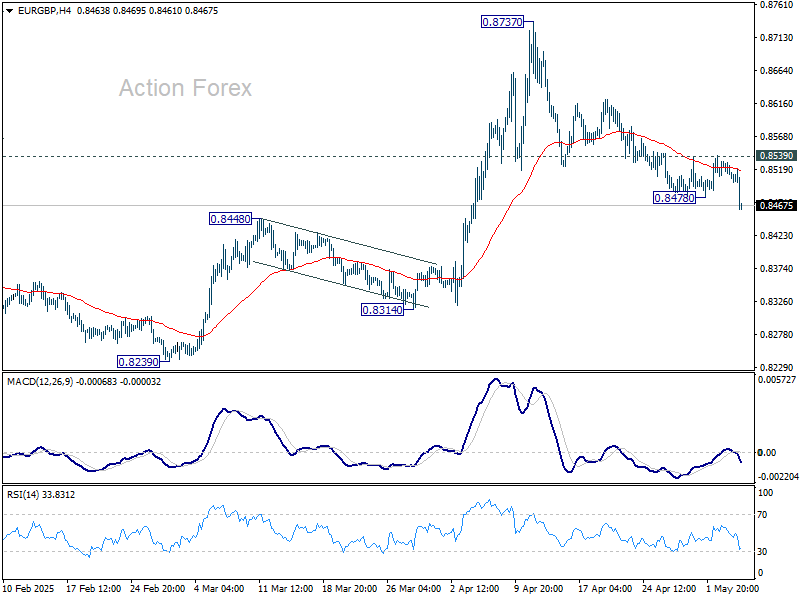

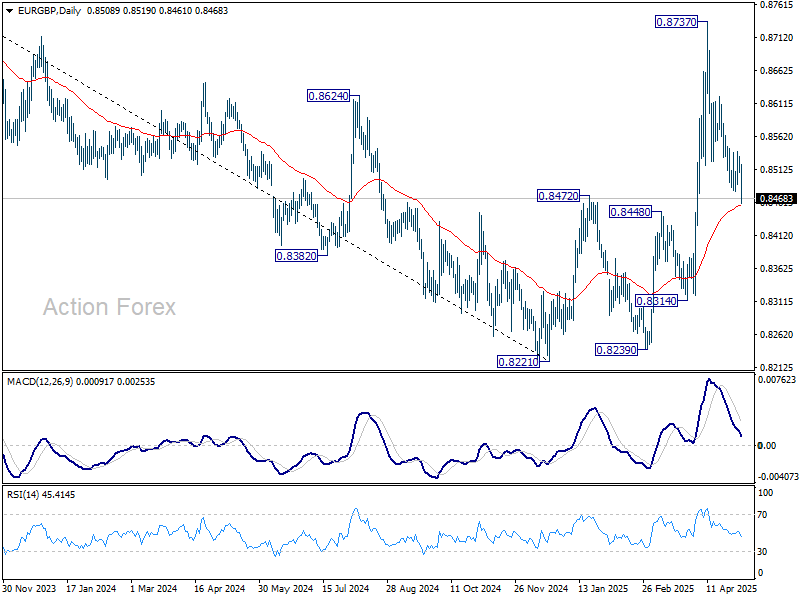

EUR/GBP: Falls to One Month Low on Fresh Political Tremors from Germany

EURGBP lost ground on Tuesday after surprise failure of Germany’s Merz to win support from parliament to become a chancellor on the first round of voting.

The pair fell to one-month low and dented strong supports at 0.8480 (Fibo 61.8% of 0.8320/0.8738 upleg/daily lower base).

Firm break here is needed to validate fresh bears and generate initial signal of continuation of larger downtrend from 0.8738 (2025 peak, posted on Apr 11) which extends into fourth consecutive week.

Although bears faced headwinds at 0.8480 pivot, presented by quick bounce from new low at 0.8461, technical picture on daily chart is weak and expected to support bears.

Near-term action has been repeatedly capped by falling 10DMA after it crossed below 20DMA last week, while 14-d momentum is heading deeper into negative territory.

Loss of 0.8480 trigger to expose 55DMA (0.8430) and Fibo 76.4% (0.8416) which guard converged 100/200DMA’s (0.8389).

Upticks should stay under 10DMA (0.8509) to keep bears fully in play, but caution on further hesitation at 0.8480 zone, which may keep the price action in extended consolidation.

Res: 0.8509; 0.8529; 0.8548; 0.8578.

Sup: 0.8461; 0.8430; 0.8416; 0.8389.

Sunset Market Commentary

Markets

After the publication of mostly stronger (activity)/higher (price) than expected data in Europe and the US last week and yesterday, markets relapsed into wait-and-see modus. Waiting, in the first place for multiple central bank decisions later this week, including a Fed and a BoE meeting tomorrow and on Thursday. Enjoying current relative calm in headlines on US trade initiatives, markets are also keen to get some insight in the process/outcome of first potential new trade deals. What might be a ‘final’ level of the tariffs? Will it be closer to the 10% bottom or closer to the upper bound of reciprocal tariffs? How stable/sustainable is the outcome expected to be? This waiting game today was disturbed by upheaval in the German Parliament as Friedrich Merz completely unexpectedly failed to get parliamentary approval to become Chancellor. A new vote is scheduled this afternoon. Even if Merz then gets the parliamentary backing needed, the failed first attempt is raising questions on the ability of the new government to convincingly execute its (reflationary) agenda. Even so, except for some intraday swings, the impact on Bunds was limited. German yields currently are even rising between 0.5 bps (2-y) and +4.0 bps (30-y). Counting down to tomorrow’s Fed meeting, the US yield curve in technical trading again bull steepens with the 2-y yield easing 3.5 bps (2-y) and the 30-y adding 2.0 bps. The failure of Friedrich Merz to secure a majority in a first reaction triggered losses of up to 2.0% of the Dax, but a big part of is already undone (Dax -0.6%, Eurostoxx 50 -0.5%). US equities after recent rebound also reverse back into correction mode (S&P open -0.75%). Oil for now sees no (further) losses from this weekend’s OPEC+ decision to further raise output levels. Brent even rebounds back north of the $60 p/b barrier (currently $ 61.6).

Still mainly technical trading in the major USD cross rates. The German headlines only had a limited and temporary impact on EUR/USD. USD rather than euro weakness prevails. DXY eased further to 99.4. EUR/USD easily holds well north of 1.13 (1.134). The yen both outperforms the dollar (USD/JPY 142.7 from 143.7) and the euro (EUR/JPY 161.6 from 162.6). Sterling also shows remarkable strength ahead of Thursday ‘s expected BoE rate cut (EUR/GBP 0.847 from 0.85.1). The Swiss franc eases slightly (EUR/CHF 0.9345) after SNB governor Schlegel commented on recent franc strength. SNB remains prepared to intervene in FX markets if necessary to guarantee price stability.

News & Views

Czech inflation unexpectedly declined by 0.1% M/M in April. Consensus anticipated a steady pace of +0.1% M/M in line with March. The annual figure, which was set for a steep setback because of base effects (sharp rise in food prices in April last year), fell below the 2% CNB inflation target as a result (2.7% to 1.8% vs 2.1% expected). In its February monetary policy report, the CNB penciled in a 2% Y/Y pace for April. Details showed negative monthly contributions from energy (-0.9% M/M & -6.3% Y/Y), food, alcohol &tobacco (-0.6% M/M & 3.3% Y/Y) and goods (-0.3% M/M & 0.2% Y/Y). Core CPI (excl. energy, food, alcohol & tobacco) rose by 0.3% M/M (2.9% Y/Y) with services inflation increasing by 0.2% M/M (4.7% Y/Y). The latter remain a concern for the CNB who meets tomorrow to decide on its policy rate. Recently, CNB members pushed back against markets discounting aggressive rate cuts related to tariff/growth uncertainty given that upside inflation risks still prevail. Tomorrow ‘s decision will be a close call. We err on the side of a hawkish 25 bps rate cut to 3.50%. The Czech 2-y swap rate fell back from 3.27% to 3.22% today after rising from the 3.1% area the past fortnight on the back of the CNB comments. The Czech koruna is marginally weaker at EUR/CZK 24.97 (from 24.92).

Bloomberg reports that the EU is planning tariffs on about €100bn of US goods if trade talks fail to yield a satisfactory result. They come on top on the €21bn of levies already in place (but not yet implemented to match the 90-day reciprocal tariff pause) as a counter to Trump’s duties on steel and aluminum exports. Member states will be consulted over the next month to come up with a detailed list. Separately, the EC will probably this week try to kickstart negotiations with the US by sharing a paper that handles trade matters. Proposals include lowering trade an non-tariff barriers and boosting investments in the US. The EU said earlier today that the US administration’s ongoing trade investigations will boost the amount of affected goods facing tariffs to €549bn.

Canadian Trade Deficit Narrows in March

Canada's trade deficit narrowed from a revised $1.4 billion in February to $506 million in March.

Merchandise exports edged lower (-0.2% m/m) continuing the slide from February's larger contraction (5.4% m/m). Exports of consumer goods (-4.2% m/m) and energy products (-2.2% m/m) contributed most to the monthly decline. Motor vehicle and parts exports (+7.7% m/m) bounced back after posting a double digit decline the month prior. In total 6 of 11 product categories registered a pullback in February.

Merchandise imports reversed last month's gain, falling by 1.5% m/m in March. Imports of energy products (-18.8% m/m) and metal/non-metallic minerals (-15.8% m/m) contributed most to the decline, partially offset by gains in industrial machinery (2.0% m/m) and aircrafts/other transportation (3.7% m/m).

In volume terms, merchandise exports were up by 1.8% m/m while imports edged down 0.1% m/m.

Canada's merchandise trade surplus with the United States shrunk to $8.4 billion in March from 10.8 billion the month prior.

Key Implications

With first quarter trade data under the belt, net trade is tracking effectively flat in terms of contribution to Q1-2025 real GDP growth. More importantly, the trade data in the coming months should begin reflecting the impacts of tariffs. Steel and aluminum tariffs that came into effect in mid-March did not appear to impact trade flows of affected products, so far.

Total trade volumes slowed in February and March after six consecutive months of solid gains, suggesting that tariff-related front-running and inventory stockpiling is coming to a halt. Canada was fortunately spared from Trump's reciprocal tariff plan but is still subject to the 25% “fentanyl/illegal immigration” tariff (10% on energy), with carve outs for USMCA compliant goods, which is likely to create ongoing frictions with the U.S. In the meantime, Canada will continue to brace for increasing headwinds to trade as the worst of the trade conflict is expected to take place over the coming quarters.

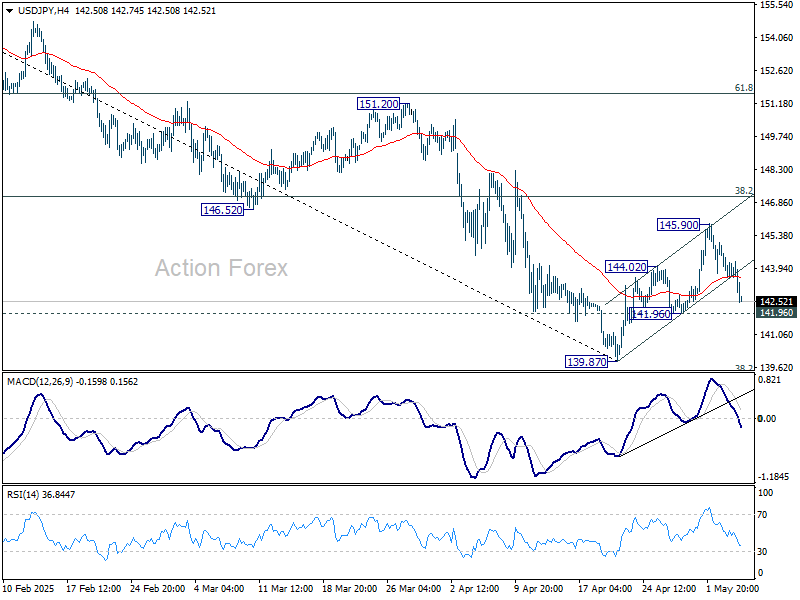

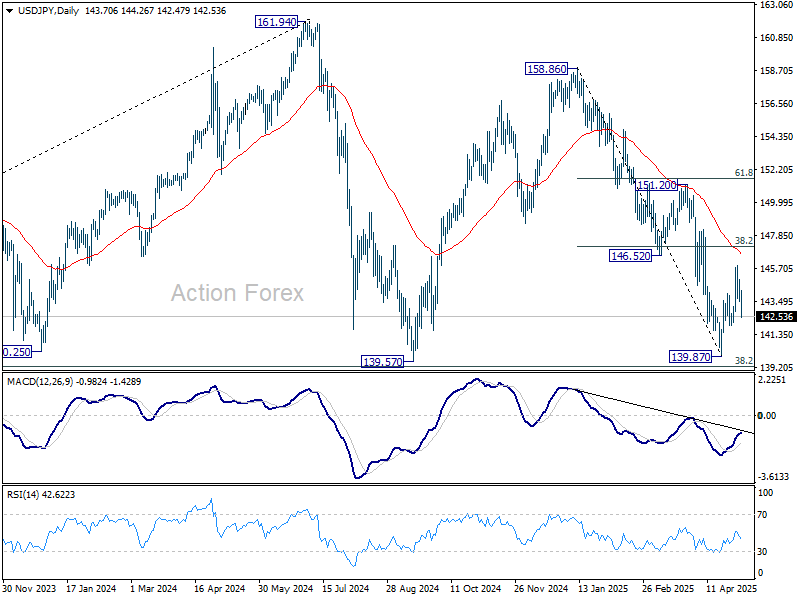

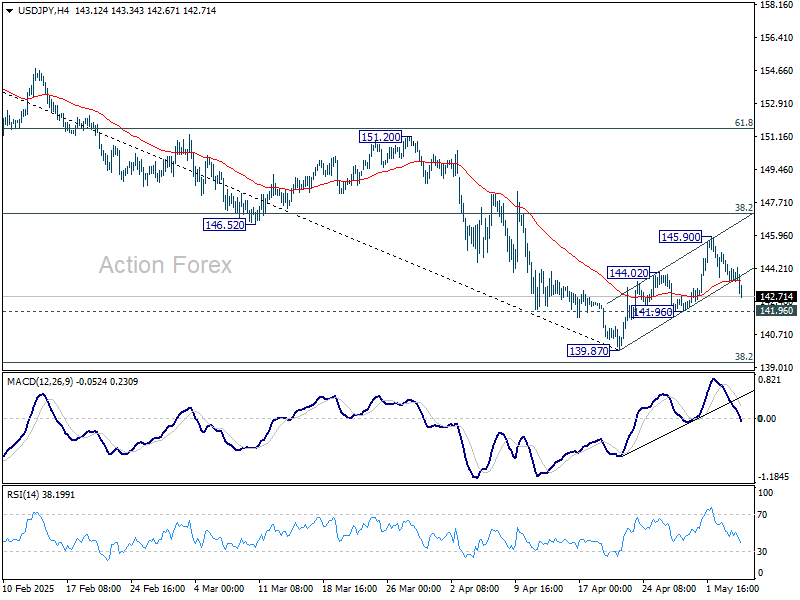

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.16; (P) 144.08; (R1) 144.61; More...

As USD/JPY's fall from 145.90 extends, focus is back on 141.96 support. Firm break there will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case. Overall, near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

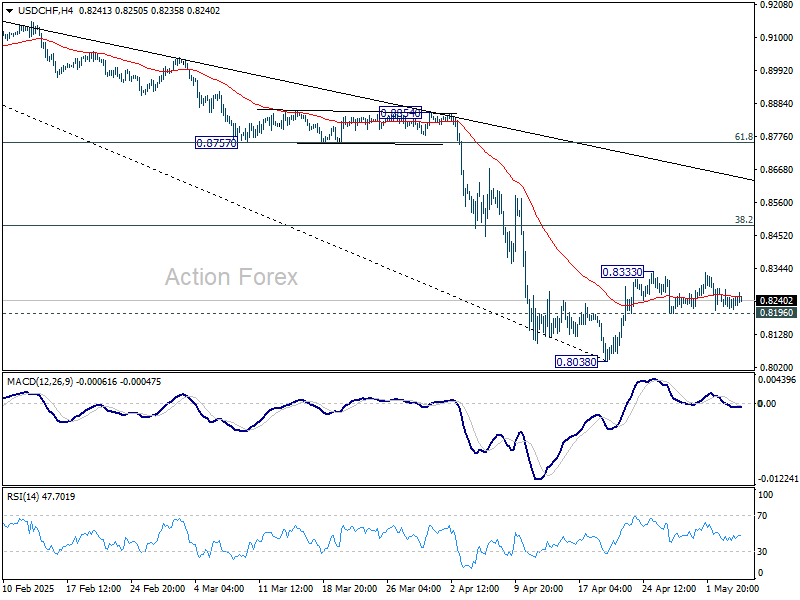

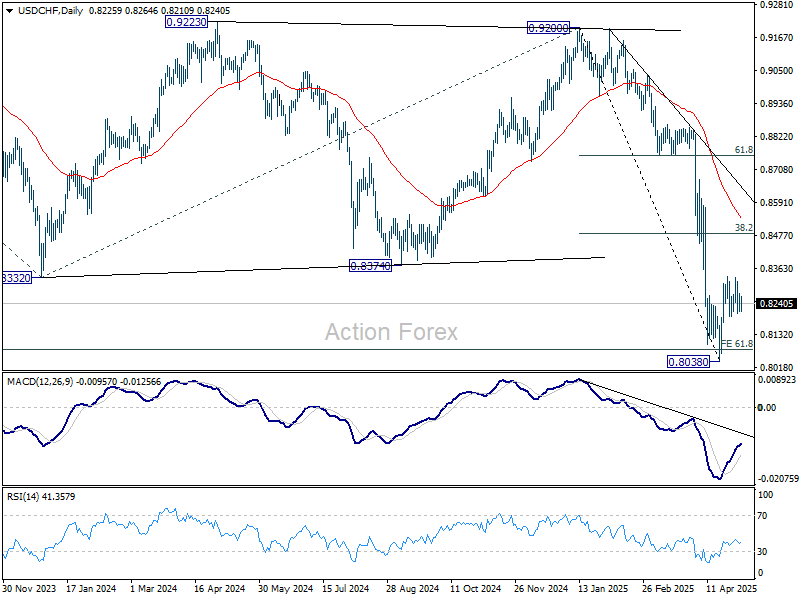

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8200; (P) 0.8237; (R1) 0.8261; More….

No change in USD/CHF's outlook as range trading continues. Intraday bias remains neutral for the moment. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

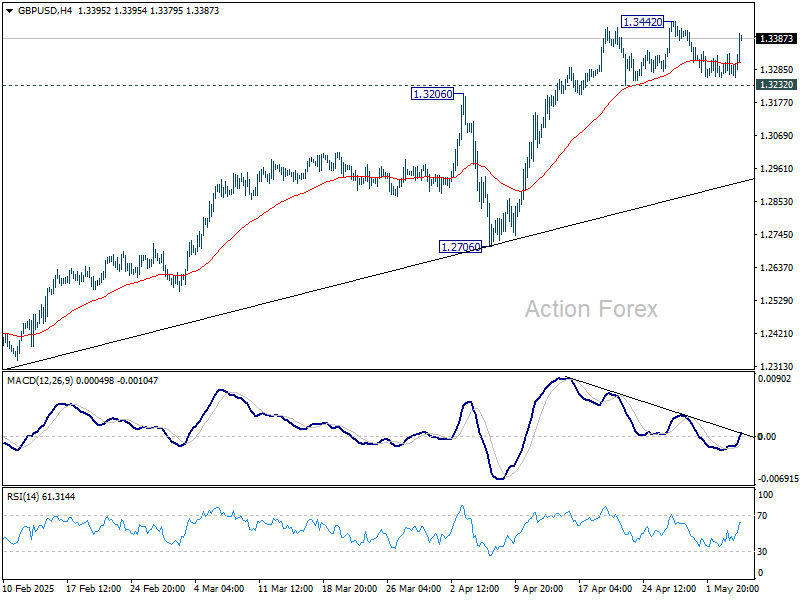

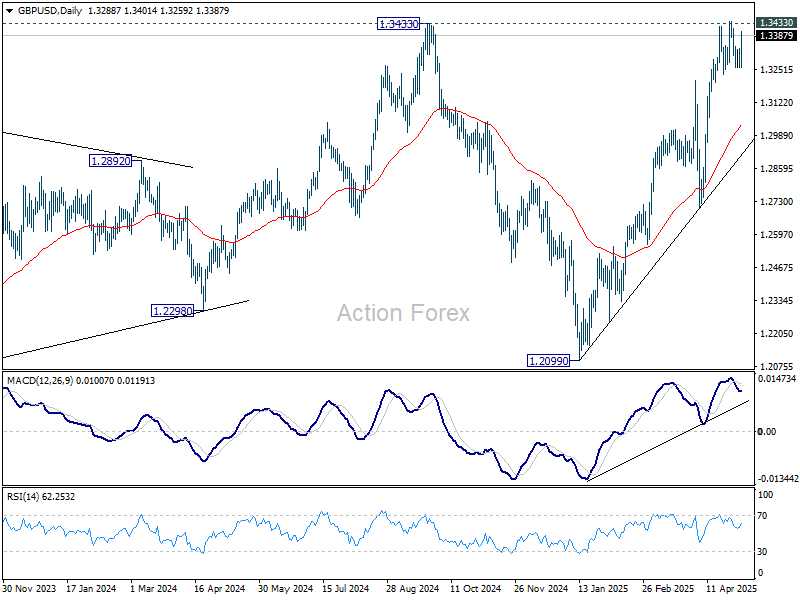

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3258; (P) 1.3298; (R1) 1.3335; More...

GBP/USD recovered notably today but stays below 1.3442. Intraday bias remains neutral first. On the downside, firm break of 1.3232 support will indicate short term topping and rejection by 1.3433 key resistance. Intraday bias will be back on the downside for deeper pullback to 55 D EMA (now at 1.3030) and possibly below. On the upside, decisive break of 1.3433 key resistance will confirm larger up trend resumption.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

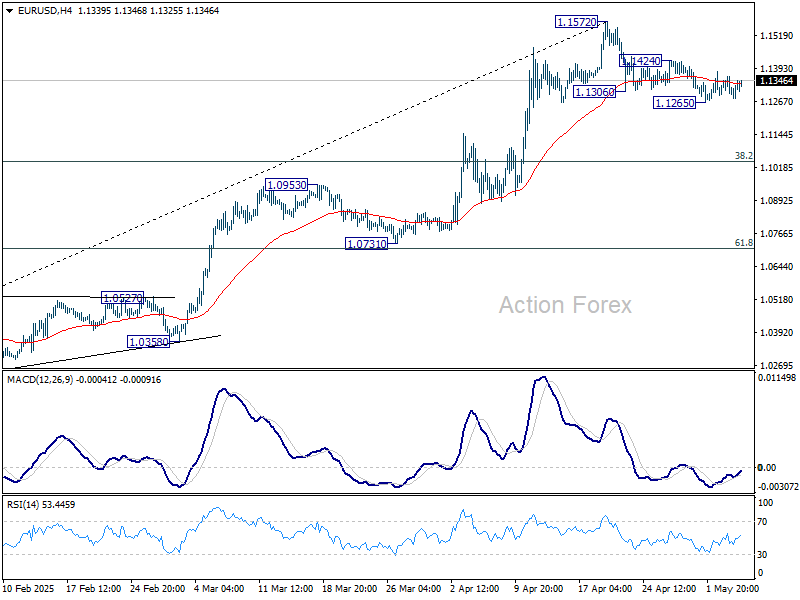

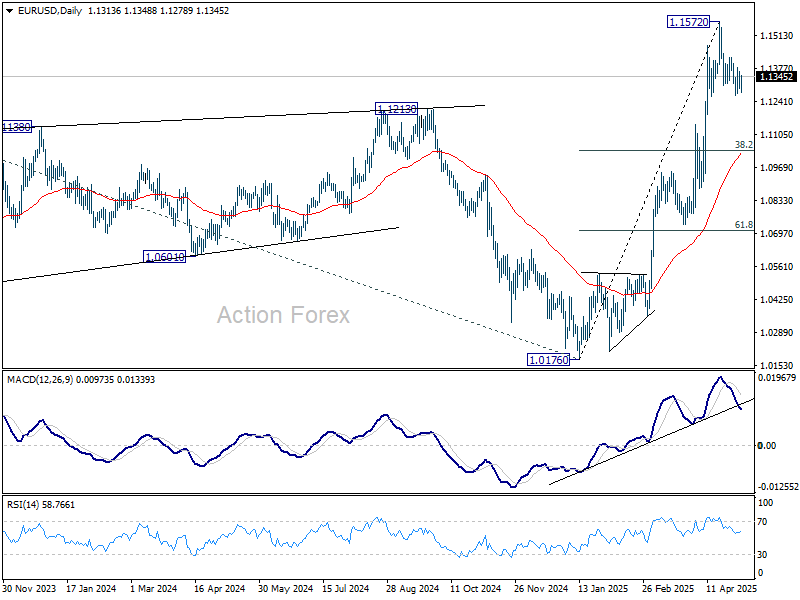

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1285; (P) 1.1324; (R1) 1.1354; More...

No change in EUR/USD's outlook as range trading continues. Intraday bias stays neutral at this point. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8504; (P) 0.8518; (R1) 0.8527; More...

EUR/GBP's fall from 0.8737 resumed after brief consolidations and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 0.8457) will suggest that whole rise from 0.8221 has already complete and turn outlook bearish. Nevertheless, rebound from current level, followed by break of 0.8539 resistance, will suggest that the correction from 0.8737 has completed, and retain near term bullishness.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds. However, firm break of 0.8472 will argue that the down trend hasn't completed yet.

Franc and Euro Falter, Yen Strengthens as Risk-Off Returns

Both Swiss Franc and Euro are under some selling pressure today, especially against Sterling. The Franc suffered after SNB Chair Martin Schlegel signaled the willingness to reintroduce negative interest rates if deflationary risks persist. Meanwhile, Euro came under pressure as fresh political instability emerged in Germany

CDU/CSU leader Friedrich Merz’s failure to secure a parliamentary majority in his bid to become chancellor. Merz’s defeat highlighted cracks within his coalition and prompted concern across Europe. Eighteen coalition lawmakers reportedly broke ranks. European observers warned that Berlin’s political instability could have ramifications for EU-wide cohesion, especially at a time when coordinated responses to US tariffs are essential.

Euro’s fragility was further compounded by European Trade Commissioner Maros Sefcovic’s remarks in the European Parliament. He emphasized that all options remain on the table if US tariff negotiations fail. The EU is preparing contingency measures ahead of the July 8 deadline, with Sefcovic warning that US tariffs now affect 70% of EU exports and could rise to 97%.

Markets will be closely watching the results of the EU’s trade diversion task force due in mid-May, especially given the risk of redirected Chinese exports flooding European markets. While Sefcovic emphasized the EU’s preference for a negotiated settlement with the US, his tone reflected limited optimism for swift progress.

Despite Sterling rally again its European peers, it was Yen that claimed the top spot among major currencies today. The Pound is sitting at the second place, with Kiwi as the third. On the other hand, Swiss Franc is the worst performer, followed by Dollar and then Aussie. Euro and Loonie are positioning in the middle.

Technically, as USD//JPY's decline from 145.90 gathers momentum, focus is now on 141.90 support. Firm break there will suggest that recovery from 139.87 has completed as a three-wave corrective move. Larger fall from 158.86 should then be ready to resume to 139.26 key long term fibonacci support.

In Europe, at the time of writing, FTSE is down -0.01%. DAX is down -0.54%. CAC is down -0.23%. UK 10-year yield is flat at 4.524. Germany 10-year yield is up 0.023 at 2.541. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.70%. China Shanghai SSE rose 1.13%. Singapore Strait Times rose 0.19%.

SNB' Schlegel signals willingness to revisit negative rates

SNB Chairman Martin Schlegel said that while the central bank does not favor negative interest rates, it remains fully prepared to reintroduce them if necessary.

Speaking at an event today, Schlegel said "if we have to do it, the negative interest rates, we're certainly prepared to do it again".

"For the last couple of quarters, we have always said we are ready to intervene in the forex market if it's necessary," Schlegel said.

The comments come just a day after Swiss CPI data revealed that inflation slowed to 0% in April — the lowest reading in four years. The data has triggered market expectations that SNB will cut its policy rate from the current 0.25% at its upcoming meeting on June 19. Expectations are also mounting that rates could eventually fall back below zero this year.

Eurozone PPI falls -1.6% mom in March on steep energy decline

Eurozone PPI fell -1.6% mom in March, dragged down by a steep -5.8% mom drop in energy costs. Excluding energy, however, PPI ticked up 0.1% mom. Annually, PPI stood at 1.9% yoy, down from prior month's 3.0% yoy.

Modest monthly gains was seen across most segments — 0.1% mom for capital goods, 0.2% mom for durable consumer goods, and 0.5% mom for non-durable goods. Intermediate goods were unchanged.

In the broader EU, PPI also fell -1.6% m/m and rose 2.1% yoy. The largest monthly decreases in industrial producer prices were recorded in Estonia (-8.0%), Spain (-3.9%) and Italy (-3.3%). The highest increases were observed in Greece (+1.3%), Luxembourg (+0.9%) and Slovenia (+0.6%).

Eurozone PMI services finalized at 50.1, cost pressure easing, hiring hesitant

Eurozone's PMI Composite was finalized at 50.4 in April, down from 50.9 in March, confirming a sluggish start to Q2. The services sector, a critical growth engine, nearly stalled with a reading of 50.1, down from 51.0.

Nationally, Ireland (54.0) led the bloc in growth, followed by Spain (52.5) and Italy (52.1). Germany (50.1) was in slight expansion, while France (47.8) fell deeper into contraction territory.

Cyrus de la Rubia of Hamburg Commercial Bank noted that cost pressures in services remain "relatively high", but easing price trends are adding weight to expectations for an ECB rate cut in June.

Employment growth across the Eurozone has stabilized, though businesses remain hesitant to expand their workforce amid continued uncertainty.

Country-level divergence is also growing more apparent. Germany’s growth is fragile but could improve in coming months, supported by its new fiscal stimulus measures.

UK PMI servies finalized at 49.0, tariffs and wage costs hit outlook

UK PMI Services was finalized at 49.0 in April, down from 52.5 in March, its lowest level since January 2023. PMI Composite also dropped into contraction at 48.5, marking the first negative reading in 18 months.

S&P Global’s Tim Moore pointed to heightened business uncertainty as a major drag on activity. Export conditions were the weakest since early 2021. Rising payroll costs linked to National Insurance hikes and increased National Living Wage rates contributed to the sharpest input cost growth since mid-2023. Service providers responded with their steepest price increases in nearly two years.

Business confidence deteriorated significantly as "service sector firms braced for an extended period of global economic turbulence and heightened recession risks." 22% of firms forecasted a decline in activity over the next 12 months—more than triple the level seen after the 2024 general election.

China's Caixin PMI composite falls to 51.1, tariff impact to deepen in Q2–Q3

China’s Caixin PMI Services dropped to 50.7 in April, down from 51.9 and missing expectations of 51.7. PMI Composite also slipped from 51.8 to 51.1, signaling weaker momentum across both manufacturing and services.

According to Caixin’s Wang Zhe, the expansion in supply and demand has decelerated amid growing trade friction. Export-driven sectors remain under particular pressure, while job losses and muted pricing power continue to squeeze business margins. The employment component of the composite index also contracted.

Perhaps most concerning, expectations for future activity plunged to the lowest levels on record, reflecting rising uncertainty among firms. "The ripple effects of the ongoing China-US tariff standoff will gradually be felt in the second and third quarter", Wang added.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8504; (P) 0.8518; (R1) 0.8527; More...

EUR/GBP's fall from 0.8737 resumed after brief consolidations and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 0.8457) will suggest that whole rise from 0.8221 has already complete and turn outlook bearish. Nevertheless, rebound from current level, followed by break of 0.8539 resistance, will suggest that the correction from 0.8737 has completed, and retain near term bullishness.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds. However, firm break of 0.8472 will argue that the down trend hasn't completed yet.