Sample Category Title

Weekly Focus – Cautious Optimism

Early, yet still uncertain rumours of de-escalating tariffs between the US and China sparked a cautious rebound in markets' risk appetite. Sources story from the Wall Street Journal suggested that the White House was considering cutting the tariff rate to 50-65% from the current 145%. US Treasury Secretary Scott Bessent affirmed that the current tariffs against China are 'unsustainable' but also that any reductions would have to be agreed mutually. China's foreign ministry denied that the two countries are currently in any negotiations, even if the door for talks is still open. In any case, US equities, Treasuries and the USD recovered ground after the broad-based sell-off over recent weeks.

Markets also found comfort in sources suggesting that Trump decided not to fire Fed Chair Powell after Bessent and Commerce Secretary Howard Lutnick cautioned him against such a move. The FOMC is set to enter a blackout tomorrow ahead of its May meeting, where consensus expects rates to remain on hold. Cleveland Fed's Beth Hammack echoed many of her colleagues yesterday when she said policymakers 'need to be patient' when setting rates in the near-term. FOMC's influential member Christopher Waller was more dovish, as he believed any price increases from tariffs would remain transitory and that the risk of unemployment from tighter profit margins was on the rise. We still expect the Fed to continue cutting rates quarterly from June onwards and until 3.00-3.25%.

While the April flash PMIs were not particularly strong, they were also not as weak as one could have feared based on the recent tariff uncertainty. Notably, the manufacturing indices increased modestly across both the euro area and the US, while the decline in composite indices was mostly due to weaker growth in services activity.

This week we also lifted our 12M EUR/USD forecast all the way to 1.22 in our latest FX Forecast Update - Gravitational forces have shifted for USD - not for Scandies, 23 April. We first shifted the profile higher in early April after Trump's 'Liberation Day' and overall, the past month has marked a profound turnaround in our earlier bullish view on the USD, which we maintained ever since early 2022. In our view, the seismic shift in US politics and the weakening structural growth outlook point towards further USD depreciation not just in the near-term but also looking further ahead.

Next week comes with a lengthy list of key data releases. We think the euro area flash HICP for April will show inflation slowing down to 2.1% y/y (Mar. 2.2%) solely due to lower energy prices. Core inflation will likely remain steady at 2.4%. PMI data from China is due for release on Wednesday, and we look for a modest decline amid the trade war. Bank of Japan will likely maintain its monetary policy unchanged on Thursday, even if domestic factors still point towards further rate hikes at the coming meetings.

We think the US April Jobs Report will show nonfarm payrolls growth slowing down to 130k (Mar. +228k). Tightening labour supply due to slowing immigration will constrain employment growth even if latest weekly data on jobless claims and job postings has remained surprisingly stable despite the tariff uncertainty. We also think US Q1 GDP will contract by -0.1% q/q AR due to front-loading of imports but emphasize that underlying demand has so far remained stronger than the weak headline figure suggests.

Gold Probes Again Through Key Supports But Initial Signals Still Need Confirmation

Gold price fell on Friday after recovery attempts previous day failed to regain pivotal barriers at $3371 (broken Fibo 23.6% of $2956/$3500) and $3400 (psychological) and signal that corrective phase off new all-time high is over.

Fresh weakness probes again through lower triggers at $3300 (psychological) and $3292 (Fibo 38.2% of $2956/$3500) with weekly close below here to generate fresh bearish signal and open way for deeper correction.

The metal is on track for weekly closing in red after two weeks of strong rally, with long upper shadow on weekly candle pointing to growing offers.

Gold is also on track for the fourth consecutive monthly gain, although long shadows of monthly candle signal indecision among investors as favorable fundamentals which strongly fueled safe-haven demand, started to change.

The yellow metal’s price was quickly deflated by easing trade tensions between the US and China, following the latest much softer tones from the US President Donald Trump, when he sidelined the story with enormous tariffs and signaled that talks between two countries already started.

However, the news are still conflicting as China denied all from Trump’s statement that keeps the overall situation heated.

Expect bearish signal on firm break and weekly close below $3292 Fibo level that would open way for deeper correction of the latest $2956/$3500 bull-leg and expose targets at $3228 (daily Kijun-sen / 50% retracement) and $3200 (psychological).

Conversely, repeated failure to take out $3300/$3292 triggers would add to scenario of prolonged consolidation and potential basing, although the latter would require bounce above $3371 for confirmation.

Daily studies are still predominantly bullish (strong positive momentum / Tenkan / Kijun-sen in bullish setup), but initial reversal signal may be developing on weekly chart (red weekly candle with long upper shadow / fading bullish momentum / RSI turned south in deep overbought territory).

Expect clearer direction signal on break of either key level ($3300/$3400).

Res: 3307; 3346; 3371; 3400.

Sup: 3260; 3245; 3228; 3200.

Sunset Market Commentary

Markets

No dominant market moving story or headlines to guide broader markets today. President Trump’s communication on next steps in the developing (or non-developing) trade negotiations with trading partners are not unequivocal and subject to debate. In an interview with Time, the US President indicates that he expects to conclude trade deals with partners in the next three to four weeks. That of course tells little about the concrete outcome. Communication on talks with China is even more complicated. Chinese officials are denying quotes from the US President that the US and China are engaged in talks on trade. This morning, market saw some positives in headlines that China is considering to exempt some (crucial) goods from the 125% tariff on imports from the US. Question remains whether this is de-escalation or just outright self-interest. The China Politbureau further preparing emergency plans also at least is an ambiguous signal. In the end, market take a cautious wait-and-see approach. The EuroStoxx 50 adds a decent 0.8%. US Indices open little changed. On European interest rate markets the debate on the room and timing of additional ECB easing continues. ECB Holzmann, a notable hawk with the MPC, indicated next policy steps are completely open, but acknowledged that the net impact of tariffs so far is rather disinflationary. However, European interest rate markets have already gone (very? too?) far in anticipating further ECB easing. A 25 bps June cut is fully discounted and with the cycle low seen between 1.50% and 1.75% next year, markets already seen ECB policy in ‘supportive’ territory. Despite these ‘perceived dovish’ comments, German yields today even add between 3.5 bps (2-y) and 1.0 bp (30-y). US yields are easing further. However, contrary to yesterday’s bull steeping on also soft interpretated Fed comments, easing today mainly occurred at the long end of the curve (30-y -5.5 bps, 2-y -0.5 bp). Especially LT yields are testing first support levels (e.g. 4.70/66% for the the30-y, 4.25% area for the 10-y). The fact that the decline is mainly driven by real yields might suggest some easing of underlying stress, at least short-term.

FX markets showed mostly technical trading in the major USD cross rates. DXY is going nowhere in the upper half of the 99 big figure (99.65). Idem for EUR/USD with the pair holding in the 1.13 big figure. At 1.1345, the week low of 1.1308 still isn’t ‘safe’. The dollar also tries to build some ST bottoming against the yen (USD/JPY 143.5 vs correction low just below 140 earlier this week). A more neural risk sentiment and a third consecutive month of ‘remarkably’ solid UK retail sales (March 0.4% M/M vs -0.4% expected and after a strong 0.7% in February) also slightly supported sterling. EUR/GBP is testing recent ST lows near 0.852. For now, we also still mainly see this a technical correction. Next support comes in at 0.8404 (50% retracement Dec 2024 low/April top) and at 0.8474 (previous range top).

News & Views

The US and India earlier this week agreed on The Terms of Reference for a Bilateral Trade Agreement, which both countries aim to conclude by the end of 2025. News agency Bloomberg today cites sources suggesting that 19 categories are under discussion including enhanced market access for US agricultural products and Indian labor-intensive exports, provisions to facilitate smoother e-commerce transactions and address data storage regulations but also collaboration on energy and critical minerals. Other so-called “chapters” covered in the trade deal are corruption and rules of origin and strengthening defense trade collaboration. Agreeing on a deal could significantly impact tariffs in both directions, with India lowering historically high agricultural taxes and the US lowering the steep 26% tariffs announced on “Liberation Day”. India and the US have pledged to boost bilateral trade to $500bn by 2030 from $127.6bn last year.

French business confidence more or less stabilized in April (96 from 97). Details showed a rebound in manufacturing (99 from 96) and services (98 from 97) while sentiment deteriorated in building construction (97 from 98) and has strongly retreated in retail trade (95 from 100). The latter is mainly due to a weakening general business outlook and lower ordering intentions. An employment climate indicator increased slightly, from 96 to 97 mainly due to the increase in the balance on future workforce size in services (including temporary work agencies).

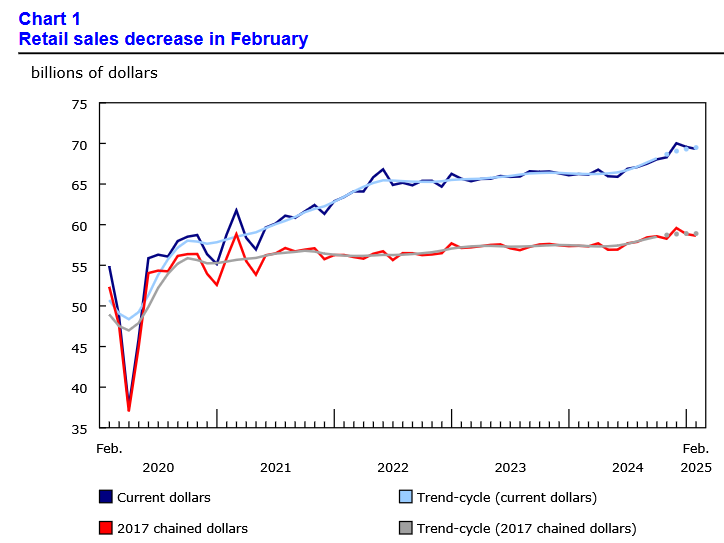

Canada: Retail Sales Decline for the Second Consecutive Month amid Tariff Storm

Retail sales contracted by 0.4% month-on-month (m/m) in February, in line with the Statistics Canada's advanced estimate.

After adjusting for inflation, the volume of retail sales posted a 0.4% m/m decline.

The biggest drag came from motor vehicle and parts dealers, where sales fell 2.6% m/m, building on January's weakness. Ex-autos, sales were flat.

Receipts at gas stations and fuel vendors rose 0.3% m/m in nominal terms and 0.8% m/m in volumes terms, suggesting the increase was demand-driven.

Excluding auto sales and receipts at gas stations, core retail sales increased 0.5% m/m in February, driven primarily by a 2.5% increase at food and beverage stores. This may reflect an last minute bump in demand prior to the expiration of to the HST/GST holiday mid-February.

Gains were partially offset by a sharp contraction in furniture & home furnishings stores (-4.4% m/m), which continue to struggle amid a collapse in home sales.

E-commerce sales fell 0.3% m/m in February.

Statistics Canada's advanced estimate for March points to a 0.7% m/m rebound.

Key Implications

Retail sales remained sluggish in February, weighed down by weaker car sales, but March data point to a bounce back, likely driven by Canadians pulling forward major purchases and stockpiling non-discretionary items ahead of incoming tariffs.

Even so, March's rebound is expected to be short-lived. Consumers remain wary and may curb spending further until there is more certainty around employment, income prospects and inflation. The Bank of Canada's latest consumer survey suggests that the negative sentiment in response to tariff-related fears has surpassed even that experienced during the pandemic, leading households to revise down their overall spending plans. We've penciled in a +2% (annualized) growth rate in consumer spending for Q1, with a contraction in the following quarters.

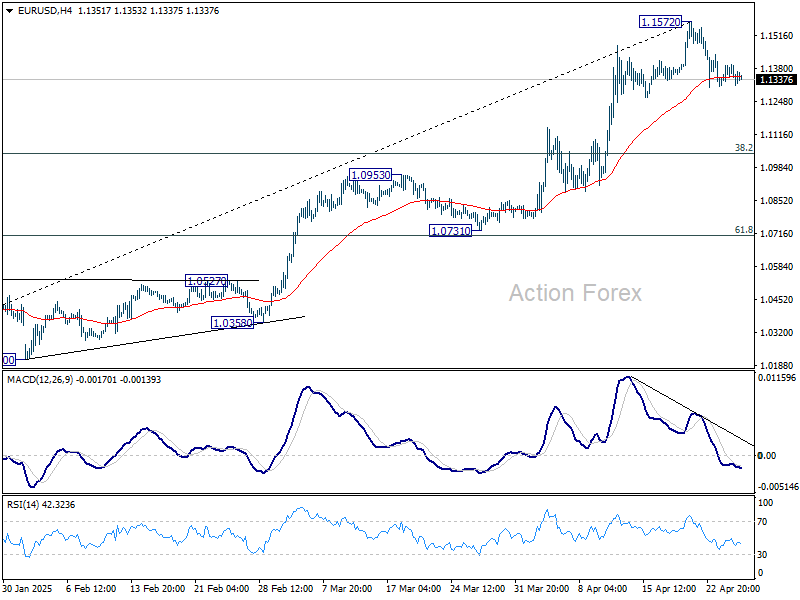

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1337; (P) 1.1367; (R1) 1.1420; More...

Intraday bias in EUR/USD stays mildly on the downside at this point. Pullback from 1.1572 short term top could extend lower. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1572 will resume larger up trend.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

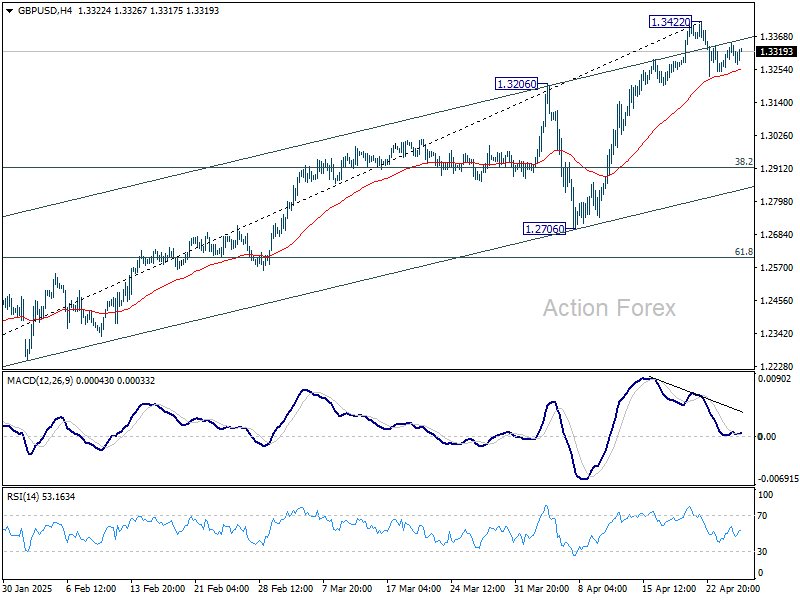

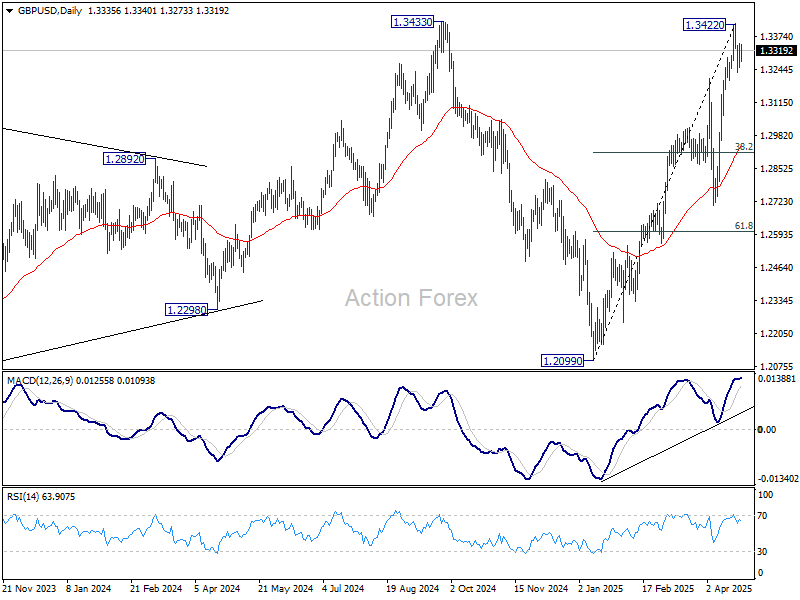

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3277; (P) 1.3313; (R1) 1.3375; More...

Intraday bias in GBP/USD is turned neutral with 4H MACD crossed above signal line. Pullback from 1.3422 short term top could still extend lower. But downside should be contained by 38.2% retracement of 1.2099 to 1.3422 at 1.2917. On the upside, firm break of 1.3433 will resume larger up trend.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

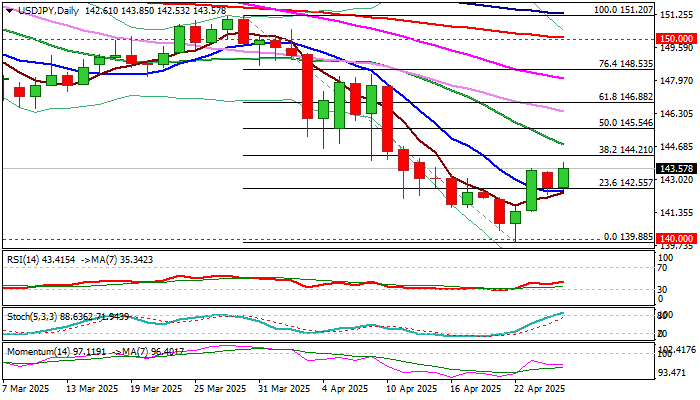

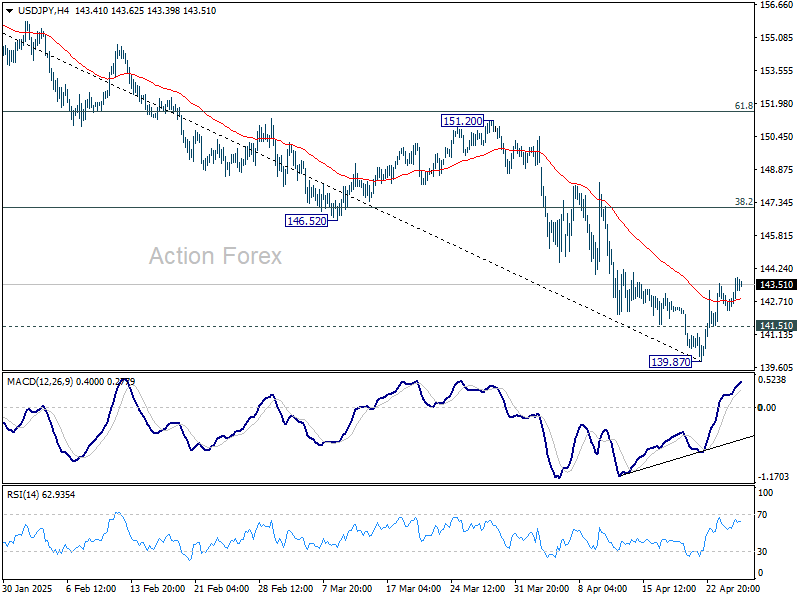

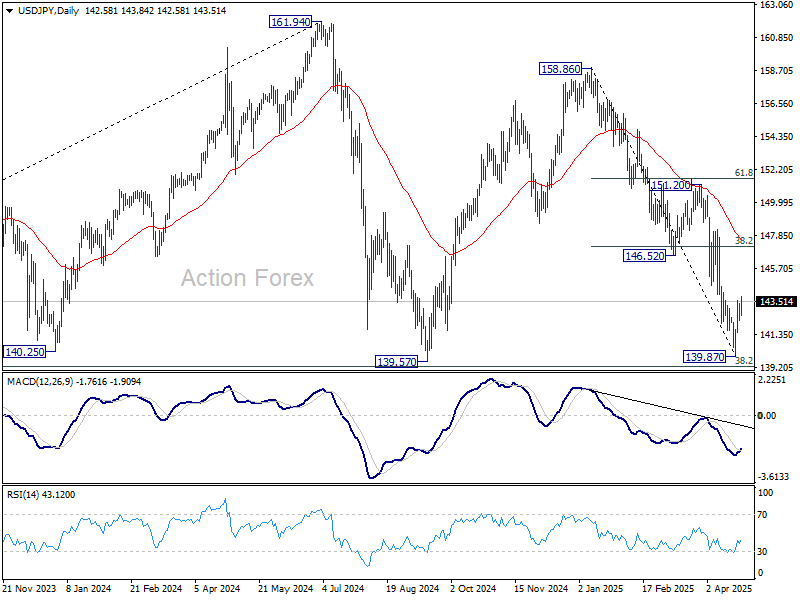

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.12; (P) 142.78; (R1) 143.29; More...

Intraday bias in USD/JPY remains on the upside as rebound from 139.87 short term bottom is in progress. While further rise could be seen, overall risk will stay on the downside as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, below 141.51 minor support will bring retest of 139.87. Decisive break of 139.26 key support will carry larger bearish implications.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

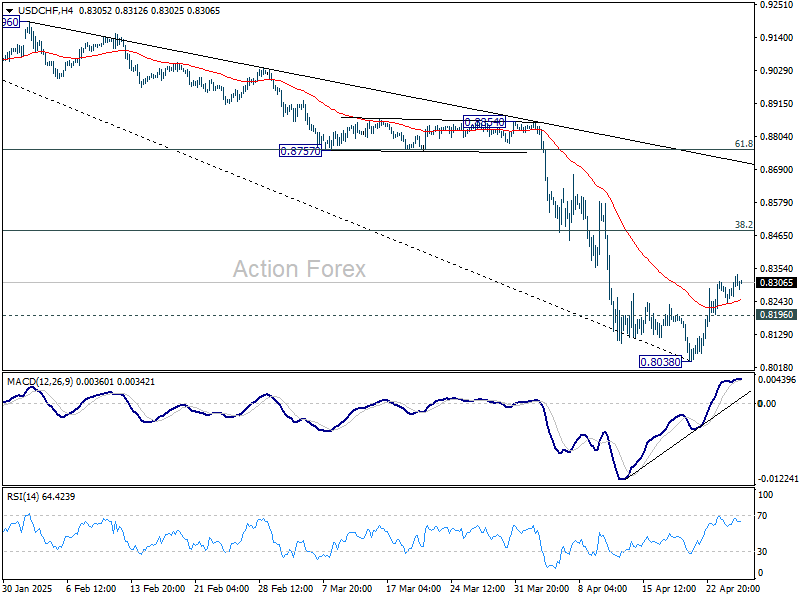

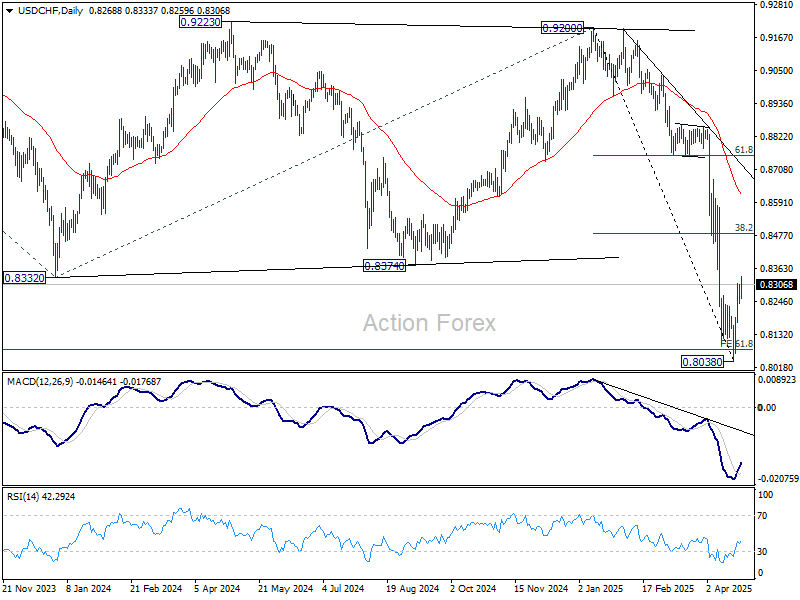

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8237; (P) 0.8273; (R1) 0.8306; More….

USD/CHF's corrective recovery from 0.8038 is still in progress and intraday bias stays on the upside. Further rise would be seen but upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

Markets Steady as US Yields Dip Amid Continuous Tariff Rumors

Global financial markets are relatively stable heading into the end of the week, with risk appetite showing further signs of improvement. European equities are trading modestly higher, following rebounds seen earlier in Japan and Hong Kong. However, US futures are slightly in the red despite strong earnings reports from tech heavyweights Alphabet and Intel. Still, one supportive development is the continued pullback in US Treasury yields, with the 10-year dipping below 4.3% mark—viewed as a positive sign for US assets.

Meanwhile, the trade war front is seeing renewed speculation, especially regarding US-China tariff relations. According to multiple media reports, China has quietly granted tariff exemptions on some US goods—including integrated circuits—previously subject to its 125% retaliatory duties. While no formal statement has been issued by Chinese authorities, there are reports of internal government consultations with foreign businesses. A list of 131 product categories is circulating on social media is believed to outline those under consideration for exemption. These steps signal a possible softening of Beijing's stance and a willingness to preserve critical supply chains.

Meanwhile, US President Donald Trump told Time magazine that China is actively engaging in talks with Washington to strike a tariff deal, and claimed that President Xi Jinping had recently called him. However, China’s Foreign Ministry declined to comment on Trump’s statement and previously warned the US to stop “misleading the public” about the status of bilateral negotiations. The conflicting narratives underscore the fog of uncertainty surrounding trade diplomacy, though market participants appear cautiously hopeful that both sides are seeking a path to de-escalation.

In the currency markets, the week’s performance leaderboard remains largely unchanged. Kiwi is holding firmly at the top. Sterling and Aussie are also among the week’s better performers. On the other end of the spectrum, Swiss franc, Japanese Yen, and Euro are lagging—reflecting fading safe-haven demand. Dollar and Loonie sit in the middle.

In Europe, at the time of writing, FTSE is up 0.28%. DAX is up 0.87%. CAC is up 0.65%. UK 10-year yield is down -0.021 at 4.482. Germany 10-year yield is up 0.018 at 2.471. Earlier in Asia, Nikkei rose 1.90%. Hong Kong HSI rose 0.32%. China Shanghai SSE fell -0.07%. Singapore Strait Times fell -0.21%. Japan 10-year JGB yield rose 0.03 to 1.34.

Canada retail sales fall -0.4% mom in Feb, but core spending offers rebound hopes

Canadian retail sales declined by -0.4% mom to CAD 69.3B in February, in line with market expectations. The overall weakness was driven primarily by a -2.6%mom drop in motor vehicle and parts dealers, with all four store categories in the subsector posting declines.

However, beneath the surface, the data showed encouraging signs. Core retail sales—which exclude fuel and vehicle-related sales—rose by 0.5% mom.

Looking ahead, Statistics Canada's advance estimate points to a 0.7% mom increase in total sales for March.

SNB’s Schlegel: Growth may miss forecasts due to trade uncertainty

Swiss National Bank Chairman Martin Schlegel warned at the central bank's annual general meeting that high levels of trade policy uncertainty continue to cloud the economic outlook.

“It remains very uncertain how inflation and the economy in Switzerland will develop,” Schlegel said, adding that “an economic slowdown cannot be ruled out.”

Growth forecasts are already under pressure, with SNB's March projection of 1% to 1.5% GDP growth this year falling below Switzerland’s long-term average of 1.8%.

Schlegel reiterated that SNB stands ready to adjust policy if needed, including interest rate changes and foreign exchange interventions. However, he acknowledged the limits of monetary policy in addressing deeper structural uncertainty.

“Price stability cannot prevent trade policy uncertainty,” he cautioned, but emphasized that maintaining stable prices provides an essential foundation for the broader economy.

UK retail sales rise 0.4% mom in March, 1.6% qoq in Q1

UK retail sales surprised to the upside in March, rising by 0.4% mom, defying market expectations for a -0.3% mom decline.

The unexpected strength was attributed largely to favorable weather conditions, which lifted sales at clothing and outdoor retailers. However, this gain was partially offset by weaker performance at supermarkets.

Looking beyond the monthly figure, the broader quarterly performance painted an encouraging picture of consumer resilience. Retail sales volumes grew by 1.6% qoq 1.7% yoy in Q1. These results indicate that UK consumers remain relatively active despite broader economic uncertainties.

Tokyo CPI core surges to 3.4% in April, strengthening case for BoJ June hike

Inflation in Japan’s capital city surged in April, with Tokyo core CPI (excluding food) accelerating from 2.4% yoy to 3.4% yoy, above the 3.2% yoy forecast. The more domestically focused core-core measure (excluding food and energy) also rose sharply, from 2.2% yoy to 3.1% yoy. Headline CPI jumped from 2.9% yoy to 3.5% yoy.

Despite the upside surprise, BoJ is still expected to hold rates steady at its May 1 policy meeting as it gauges the broader impact of recent US tariffs and awaits progress in ongoing trade negotiations. However, with inflation gathering pace across key categories, market expectations are shifting toward a rate hike as soon as June.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8237; (P) 0.8273; (R1) 0.8306; More….

USD/CHF's corrective recovery from 0.8038 is still in progress and intraday bias stays on the upside. Further rise would be seen but upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

Canada retail sales fall -0.4% mom in Feb, but core spending offers rebound hopes

Canadian retail sales declined by -0.4% mom to CAD 69.3B in February, in line with market expectations. The overall weakness was driven primarily by a -2.6%mom drop in motor vehicle and parts dealers, with all four store categories in the subsector posting declines.

However, beneath the surface, the data showed encouraging signs. Core retail sales—which exclude fuel and vehicle-related sales—rose by 0.5% mom.

Looking ahead, Statistics Canada's advance estimate points to a 0.7% mom increase in total sales for March.