Sample Category Title

Crypto Market Pauses After Growth

Market Picture

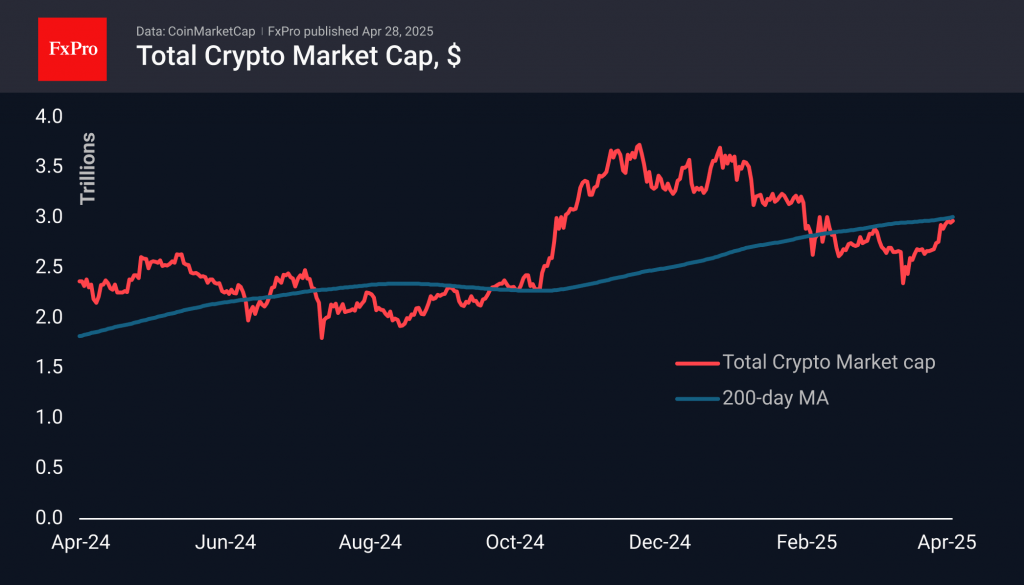

The crypto market capitalisation has been hovering around $2.97 trillion since the end of last week. The market has recovered to its 200-day moving average, but is hesitant to overcome it, as we see in the case of Bitcoin. The sentiment in the markets is neutral. It seems that players prefer to move upwards with relatively long stops.

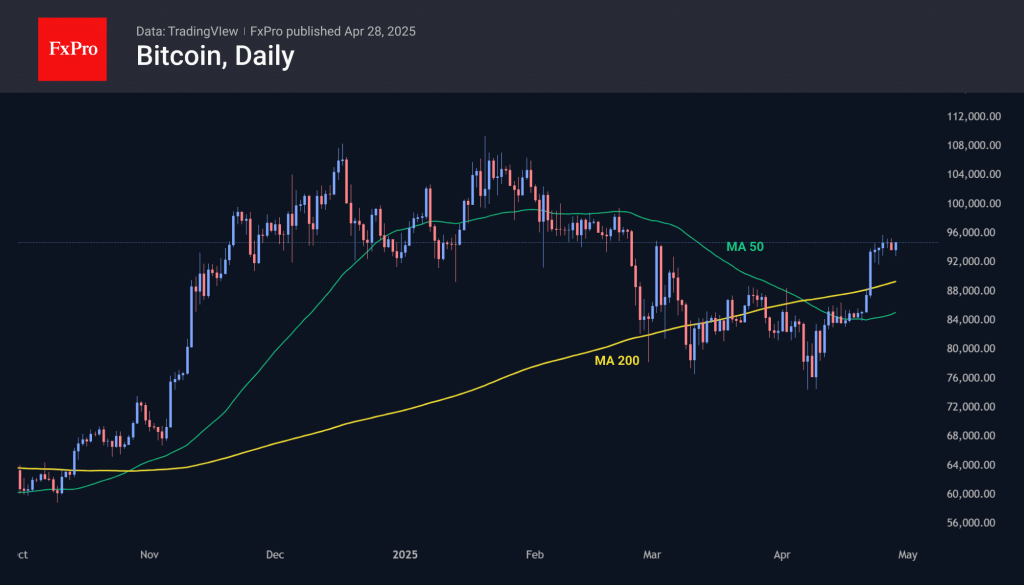

Bitcoin is stabilising near $94,500, having fully recovered to the consolidation levels seen in February before its sharp decline. The technical outlook remains bullish, with BTCUSD trading above both its 50- and 200-day moving averages. Both indicators are trending upward, and last week’s consolidation above these levels marked a strong move, reinforcing the bullish momentum.

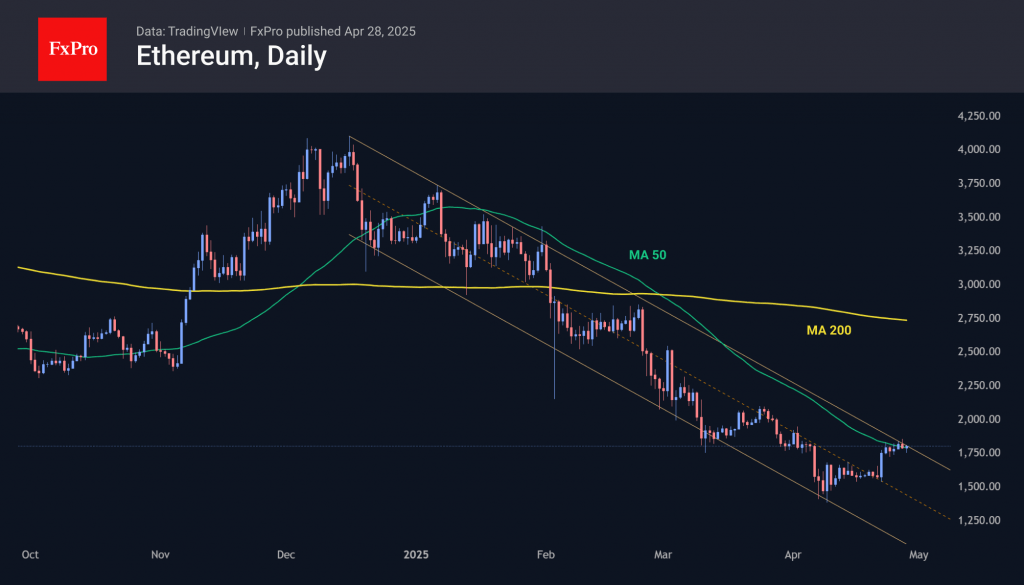

Ethereum is struggling with resistance in the form of the 50-day moving average near $1800 for the sixth day. Over the past couple of years, ETH has reacted strongly to movements around this curve: accelerating gains when breaking above it and facing significant pressure when falling below it. At the same time, there is a test of the resistance line of the descending channel, within which the movement has been going on since the second half of December.

News Background

QCP Capital noted that the bitcoin options market is currently dominated by call options with $95,000 strike prices for the end of April and May, suggesting that risk appetite remains strong. Meanwhile, President Trump softened his stance last week, reassuring investors about Fed Chairman Powell’s position and announcing plans to reduce tariffs on Chinese goods.

Bitcoin could rise to $2.4 million by the end of 2030 amid the growing adoption of the asset by institutions and sovereign wealth funds, ARK Invest forecasts in its bullish scenario. BTC will reach $1.2m in the baseline scenario and $500,000 in the bearish scenario. The analysis is based on calculations of the total target market (TAM), penetration rate and issuance of the first cryptocurrency.

The year 2025 could be a breakthrough year in institutional adoption of blockchain technology, with stablecoins being one of the drivers. Citigroup forecasts that their capitalisation by 2030 could grow to $1.6 trillion in a base case scenario and $3.7 trillion in a bullish scenario.

The US Federal Reserve announced the cancellation of guidelines that have deterred banks from dealing with digital assets. According to the statement, the regulator will stop requiring prior notification from financial institutions about plans or ongoing transactions with cryptocurrencies.

IMF warns US tariffs to outweigh Germany’s stimulus, recommends just one more ECB cut

Higher infrastructure spending in Germany will offer some support to Europe’s growth outlook, but it won’t be enough to offset the damage caused by US tariffs, according to Alfred Kammer, director of the European department at the IMF.

Speaking to CNBC, Kammer stressed that "it’s the tariffs and the trade tensions which weigh on the outlook rather than the positive effects on the fiscal side."

He noted that the IMF has delivered a "meaningful downgrade" to growth forecasts for Europe’s advanced economies and an even steeper downgrade for the emerging Eurozone countries over the next two years. The IMF cut its Eurozone growth forecasts by -0.2% for each of the next two years, now projecting growth of just 0.8% in 2025 and 1.2% in 2026.

Kammer also outlined a clear policy recommendation for ECB. Acknowledging the success of the disinflation efforts, he suggested that ECB has room for "one more 25-basis-point cut in the summer," after which it should hold rates steady at around 2%, barring major shocks.

Gold Under Pressure as Market Hopes for US-China Trade Progress

The price of gold fell on Monday, dropping to 3,290 USD per troy ounce amid easing market tensions.

Key factors driving gold’s decline

The sell-off in the safe-haven asset was driven by reduced risk aversion, as trade tensions between the US and China showed signs of easing. This weakened gold’s appeal as a traditional hedge against uncertainty.

Earlier, US President Donald Trump hinted at a potential softening of his tough trade stance towards China, signalling the possibility of tariff negotiations. On Friday, China exempted certain US goods from its 25% tariffs, though Beijing stopped short of confirming any scheduled trade talks with Washington.

Additional downward pressure came from a strengthening US dollar, which made dollar-priced gold more expensive for foreign investors.

Upcoming US economic data in focus. This week, a raft of key US economic indicators will be released, including:

- The first estimate of Q1 2025 GDP

- Core PCE inflation data for March

- April employment figures

These reports could provide fresh clues on the Federal Reserve’s next policy moves and the broader economic outlook.

Technical analysis: XAU/USD

On the H4 chart, XAU/USD is forming the fifth structure in the first wave of decline to the 3,232 level. A move to this target level seems likely. Further, a correction to the level of 3,365 is possible. After completing this correction, a new wave of decline to the 3,100 level is probable. The target is local. Technically, this scenario is confirmed by the MACD indicator, with its signal line under the zero level and directed strictly downwards.

On the H1 chart, XAU/USD has formed a consolidation range around the level of 3,300, and with an exit down, a decline to 3,232 is probable. Today, the fifth wave of the decline to at least 3,232 seems highly likely. Technically, this scenario is confirmed by the Stochastic oscillator. Its signal line is under the 50 level and directed strictly downwards to the 20 level.

Conclusion

Gold remains vulnerable to further losses amid improving US-China trade sentiment and a stronger dollar. Traders will closely monitor upcoming US data for further directional cues.

ECB’s Villeroy reaffirms gradual rate cut, sees no recession risk

French ECB Governing Council member Francois Villeroy de Galhau expressed confidence today that there is no imminent recession risk for either France or Europe, while inflation continues to decline.

Speaking to RTL Radio, Villeroy also reaffirmed that the ECB retains "a gradual margin for rate cuts", despite global uncertainties.

Villeroy also issued a strong warning about the risks stemming from US trade policies. He criticized the administration's protectionist stance, saying it was "playing against the US economy and unfortunately also against the world economy."

He stressed that protectionism ultimately leads to "less growth and more inflation."

S&P 500 Chart Analysis Ahead of the Busiest Week of Earnings Season

Despite the fact that President Trump’s earlier decision to impose tariffs (at higher rates than expected) shook the stock markets, the S&P 500 index (US SPX 500 mini on FXOpen) could still end April without significant losses (currently trading less than 2% below the month’s opening level) or even achieve a positive result.

According to media reports, around 180 S&P 500 companies are expected to release their quarterly earnings this week, including Apple (AAPL), Amazon (AMZN), Coca-Cola (KO), Eli Lilly (LLY), Meta (META), Microsoft (MSFT), and Chevron (CVX).

The share prices of these major companies — some of the largest by market capitalisation — could have a substantial impact on the S&P 500 index chart (US SPX 500 mini on FXOpen), given that their combined weight accounts for approximately a quarter of the index calculation.

Technical Analysis of the S&P 500 Chart

Based on the key price actions marked on the chart, we can identify a descending trend channel for the US stock market, which has been in effect since mid-February.

At the same time, the price has:

→ moved into the upper half of this channel, reaching its upper boundary;

→ found support around the median line (as evidenced by the price action on 21 April).

These are bullish signs, reinforced by the aggressive nature of the rebound from the psychological 5,000-point level, which acted as significant support in the first few days following the tariff announcement. Bears may still see an attractive opportunity to attempt to resume the downward momentum of the S&P 500 index (US SPX 500 mini on FXOpen), but will the fundamental backdrop support such a move?

From an optimistic perspective, sharp impulses driven by corporate news could lead to a breakout above the upper boundary of the red channel. This would likely be facilitated by important announcements (particularly from senior officials in the US, China, and Europe) regarding de-escalation of the tariff situation.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

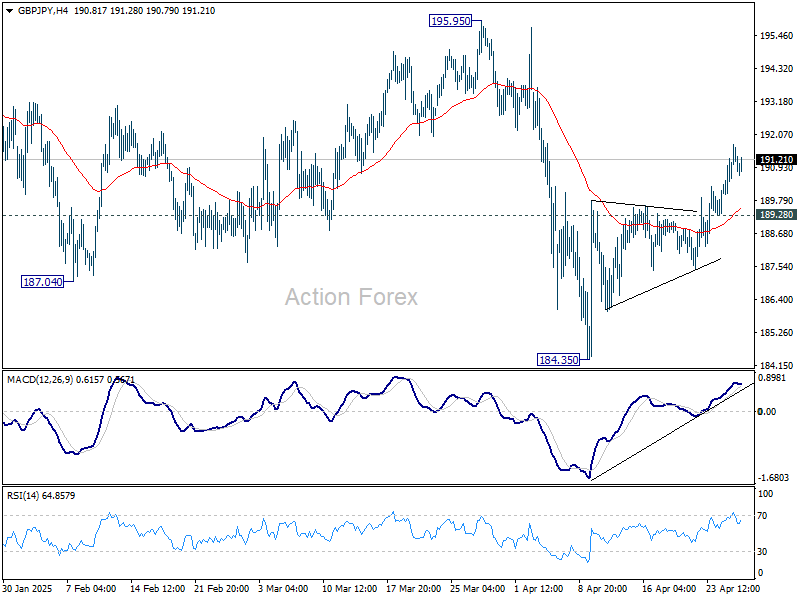

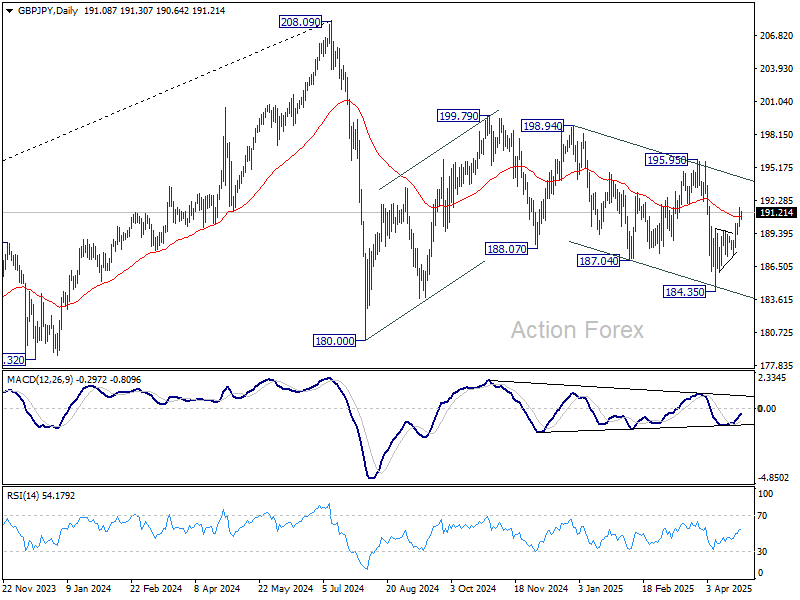

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.23; (P) 190.98; (R1) 192.00; More...

Intraday bias in GBP/JPY remains on the upside at this point. Rise from 184.35 would target 195.95 resistance next. Firm break there will suggest that choppy decline from 199.79 has also finished too. On the downside, below 189.28 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

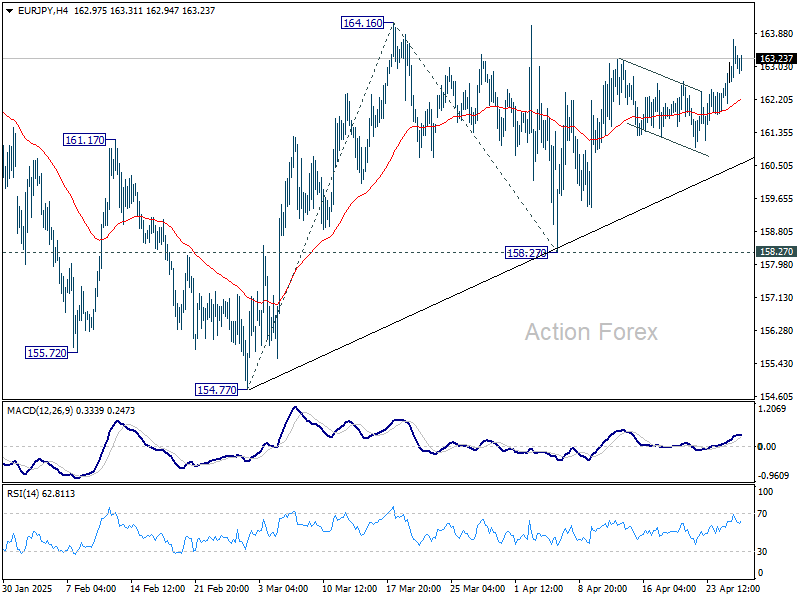

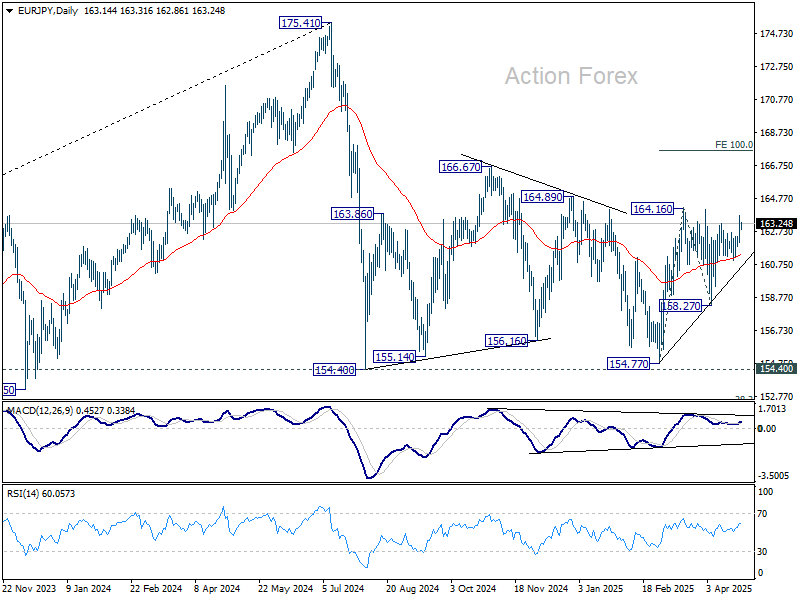

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.27; (P) 163.01; (R1) 164.02; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the upside, firm break of 164.16 will resume whole rise from 154.77. Next target will be 100% projection of 154.77 to 164.16 from 158.27 at 167.66. However, break of 158.27 will bring deeper fall back to 154.40/77 support zone.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

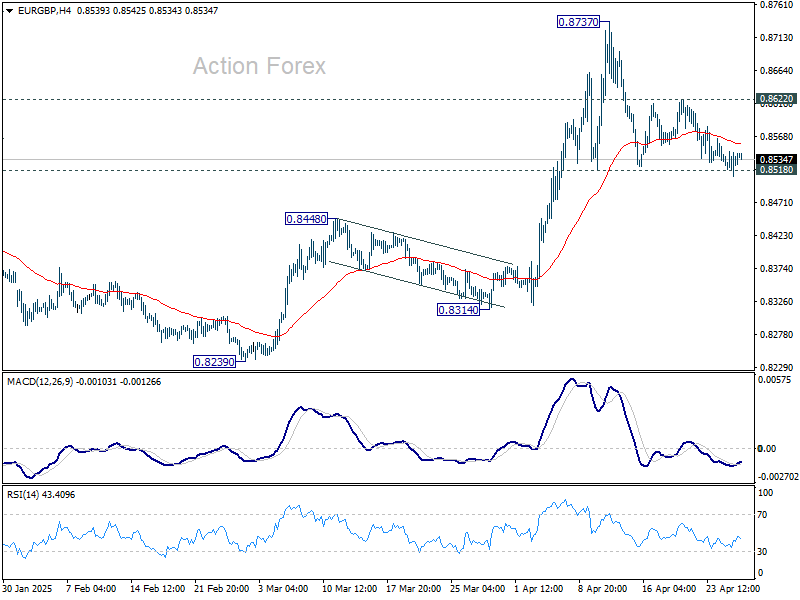

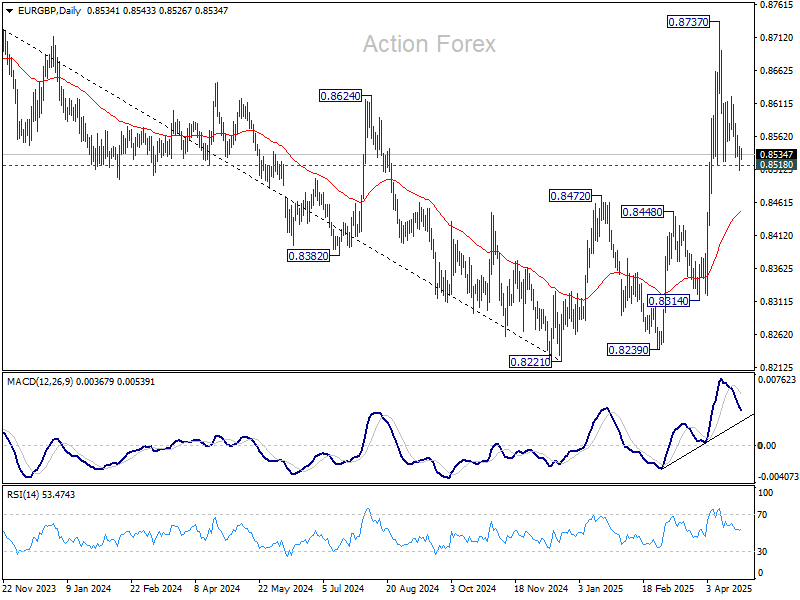

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8515; (P) 0.8532; (R1) 0.8552; More...

Intraday bias in EUR/GBP stays neutral for the moment. Further rise is expected as long as 0.8518 support holds. On the upside, 0.8622 minor resistance will bring retest of 0.8737 first. Firm break there will resume the larger rally from 0.8221. However, sustained break of 0.8518 will bring deeper fall back to 55 D EMA (now at 0.8450).

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds.

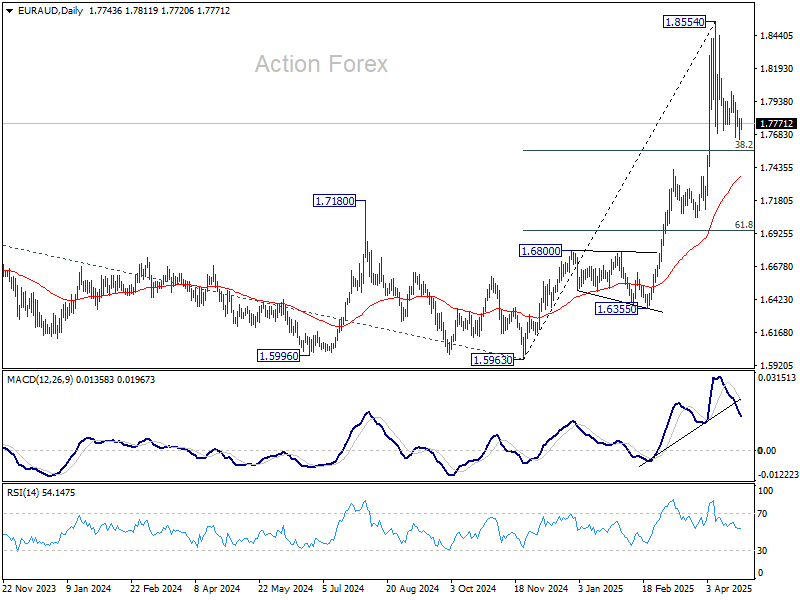

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7672; (P) 1.7743; (R1) 1.7835; More...

Intraday bias in EUR/AUD remains neutral for the moment. Corrective pattern from 1.8554 could extend, but downside should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, above 1.8014 minor resistance will bring retest of 1.8554 first. Firm break there will resume larger up trend. However, firm break of 1.7750 will bring deeper fall to 55 D EMA (now at 1.7369).

In the bigger picture, up trend from 1.4281 (2022 low) is in progress for 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7062 resistance turned support (2023 high) holds even in case of deep pullback.

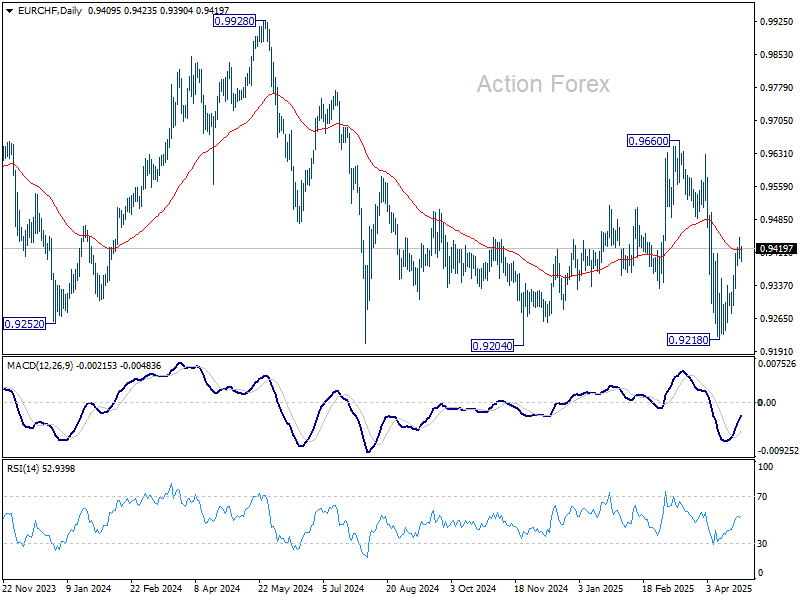

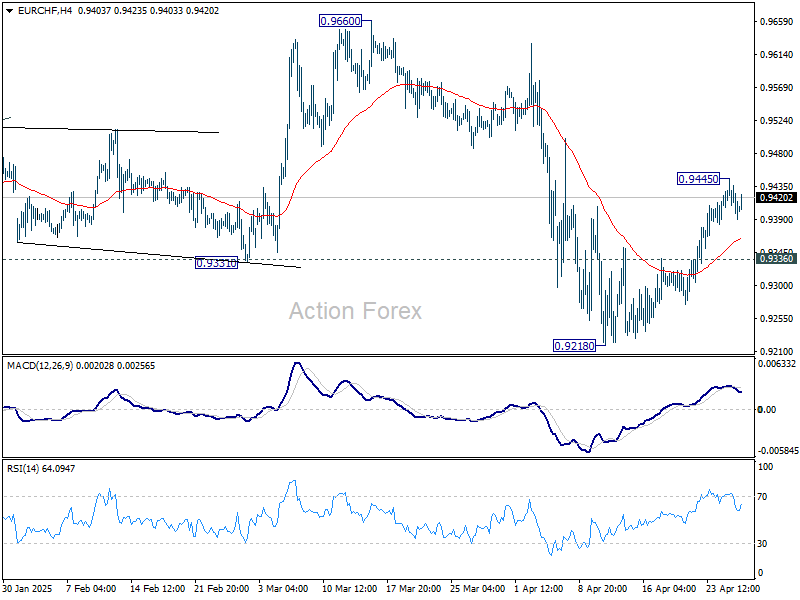

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9390; (P) 0.9418; (R1) 0.9435; More....

Intraday bias in EUR/CHF is turned neutral first with current retreat. Rebound from 0.9218 is either a corrective move, or the third leg of the pattern from 0.9204. In either case, further rally is expected this week as long as 0.9336 support holds, towards 0.9660. However, break of 0.9336 will bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.