Sample Category Title

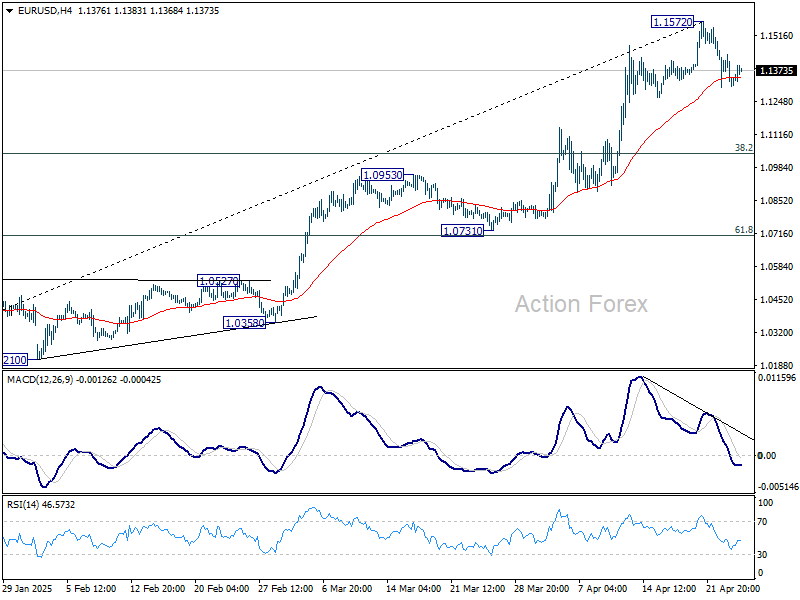

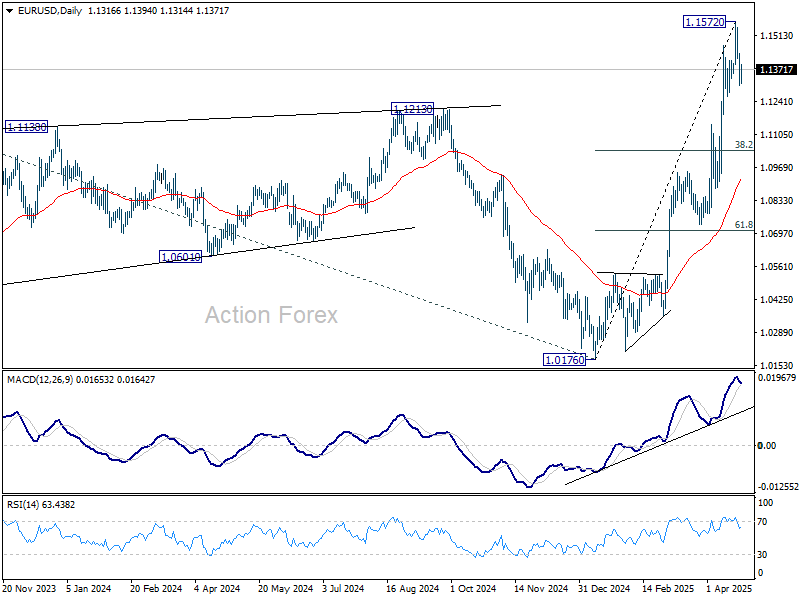

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1269; (P) 1.1354; (R1) 1.1401; More...

Intraday bias in EUR/USD remains mildly on the downside, and pullback from 1.1572 short term top could extend lower. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1572 will resume larger up trend.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

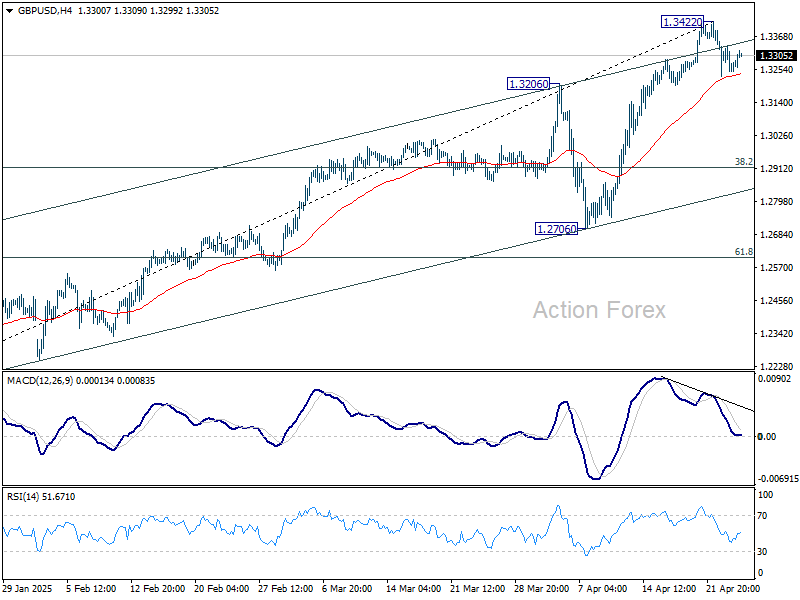

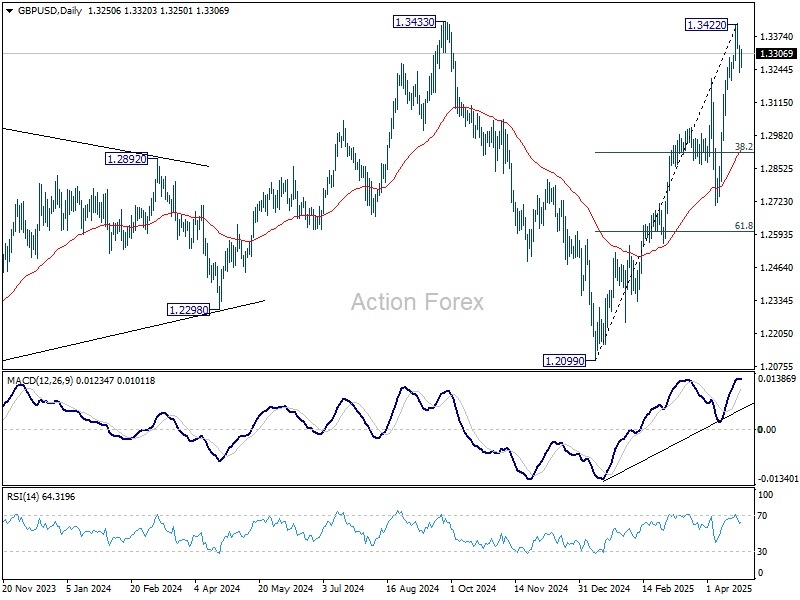

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3212; (P) 1.3276; (R1) 1.3319; More...

Intraday bias in GBP/USD remains mildly on the downside, and pullback from 1.3422 short term top would continue lower. But downside should be contained by 38.2% retracement of 1.2099 to 1.3422 at 1.2917. On the upside, firm break of 1.3433 will resume larger up trend.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

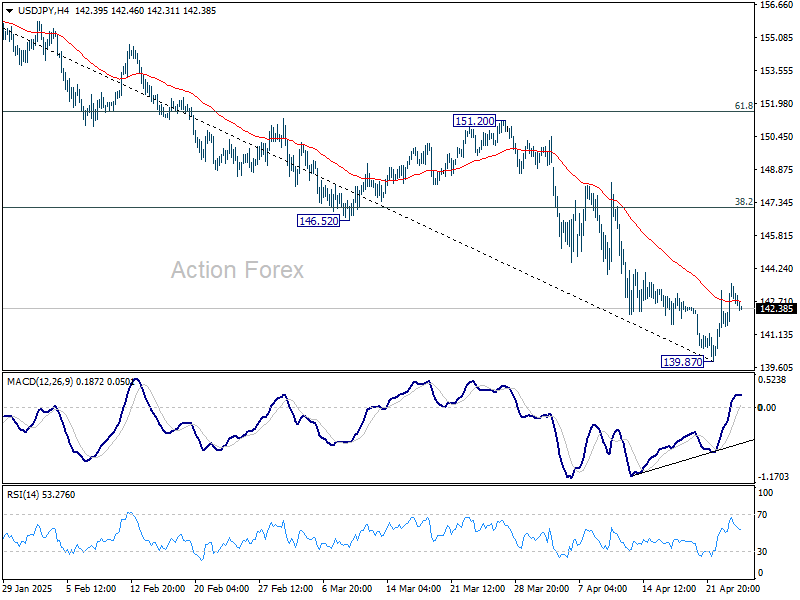

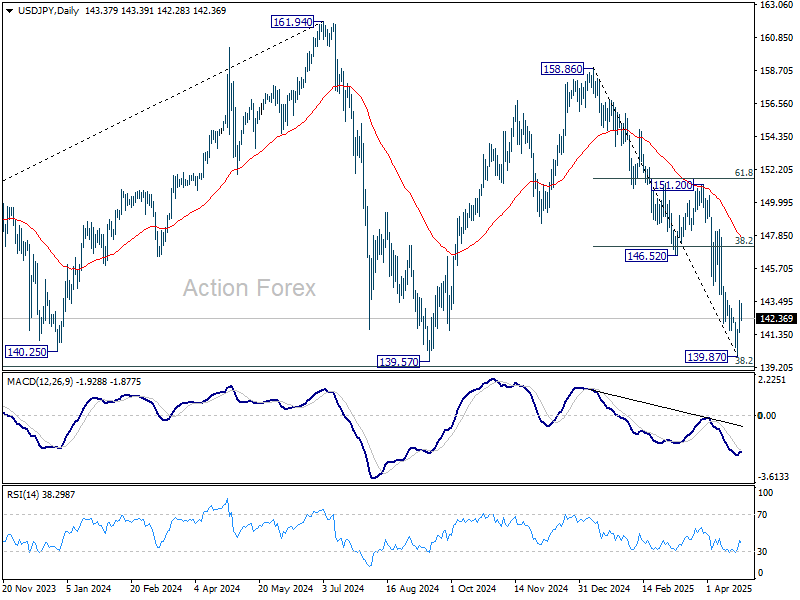

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.07; (P) 142.82; (R1) 144.19; More...

Intraday bias in USD/JPY remains mildly on the upside for the moment. Rebound from 139.87 short term bottom could extend higher. But overall risk will stay on the downside as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, decisive break of 139.26 will carry larger bearish implications.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

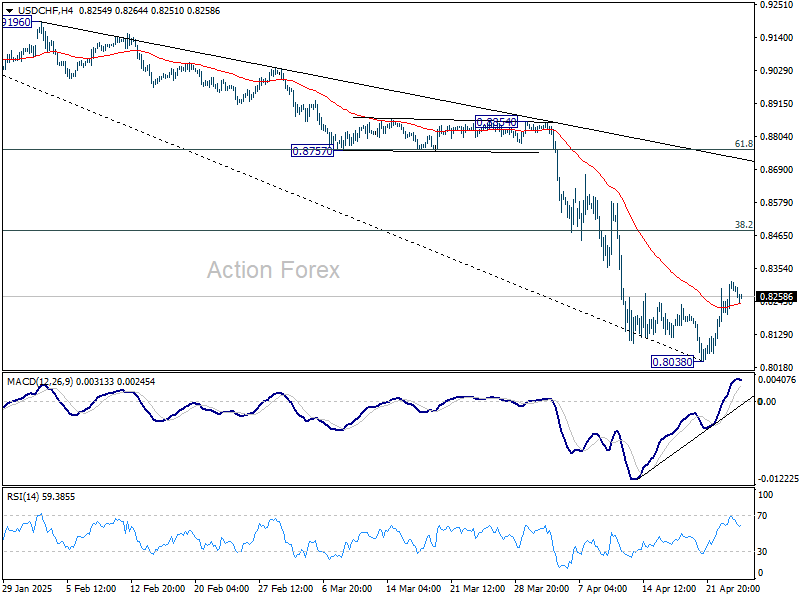

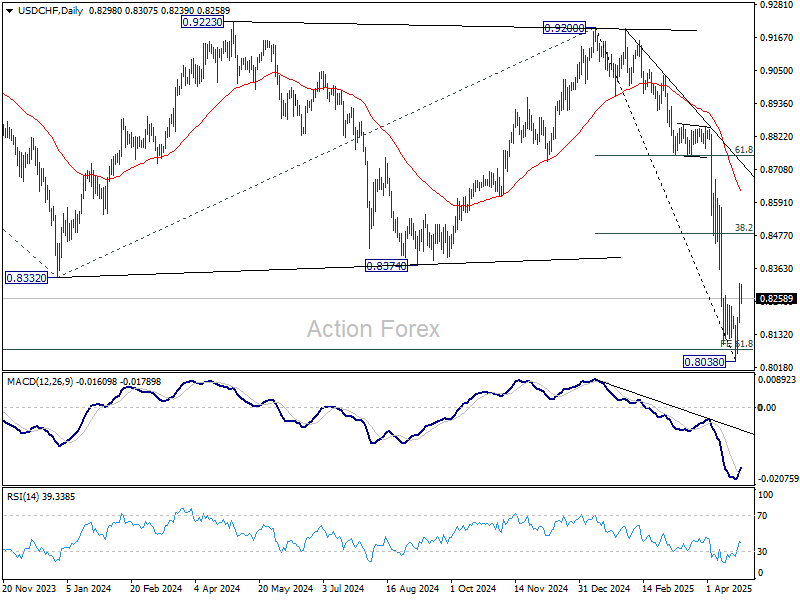

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8215; (P) 0.8264; (R1) 0.8355; More….

USD/CHF's rebound from 0.8038 is still in progress and intraday bias stays mildly on the upside. However, strong resistance should be seen from 38.2% retracement of 0.9200 to 0.8038 at 0.8482 to limit upside. On the downside, break of 0.8038 will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

Dollar Rebound Stalls as US-China Trade Talks Hit a Wall

The forex markets remain subdued today, with all major pairs and crosses trading inside yesterday's range. After a brief bounce, Dollar’s recovery appears to be losing momentum. While it’s too soon to confirm whether the rebound has fully run its course, fading trade optimism is clearly starting to weigh on sentiment, especially as the broader macro picture continues to be dominated by uncertainty surrounding US trade policy.

One of the key sources of hesitation remains the unresolved state of US trade negotiations. Despite market hopes earlier in the week for progress, there has been no meaningful development between the US and its key trading partners regarding tariff reductions. More critically, the much-anticipated talks with China appear not to have even started at all—deflating sentiment that had briefly lifted risk assets and commodity currencies earlier in the week.

China’s Ministry of Commerce poured cold water on any speculation of near-term breakthroughs, stating unequivocally that there are “absolutely no negotiations” currently underway with the US on trade. The Foreign Ministry further emphasized that reports of ongoing talks or agreements are “false news,” and reiterated that Washington must first cancel its unilateral measures for talks to begin. The firm stance from Beijing signals a hardening of positions, making the path toward de-escalation far less certain than previously hoped.

For now, Dollar and other major currencies are in wait-and-see mode, with traders looking for more concrete signals before re-engaging decisively. As for the week so far, Kiwi is still sitting at the top of the performance ladder, followed by Aussie, and then Sterling. On the weaker side, safe-haven currencies continue to lag, with Swiss Franc underperforming, followed by Euro and Yen. The Dollar and Loonie position in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.19%. DAX is down -0.24%. CAC is down -0.03%. UK 10-year yield is down -0.048 at 4.515. Germany 10-year yield is down -0.049 at 2.455. Earlier in Asia, Nikkei rose 0.49%. Hong Kong HSI fell -0.74%. China Shanghai SSE rose 0.03%. Singapore Strait Times fell -0.01%. Japan 10-year JGB yield fell -0.014 to 1.310.

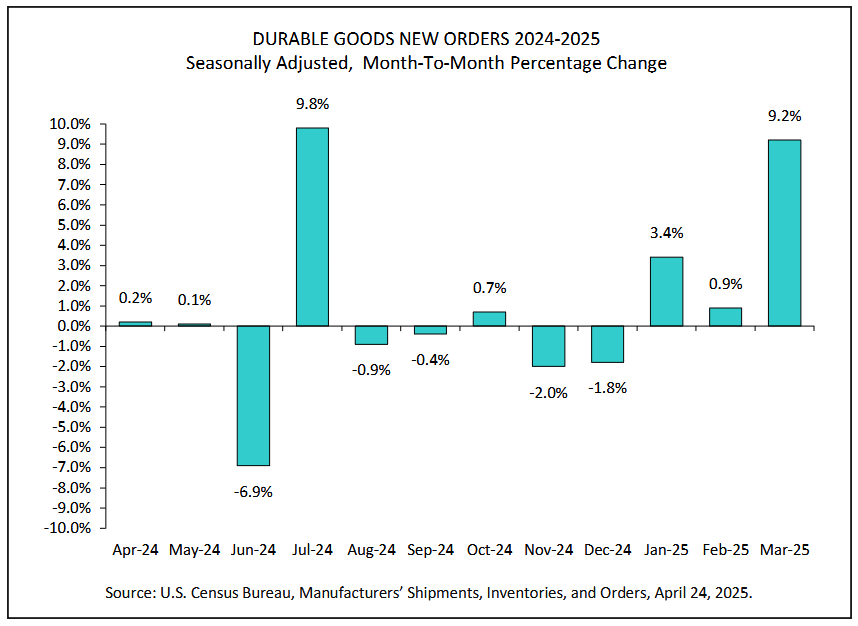

US durable goods orders surge 9.2% mom on transportation demand, but underlying momentum stalls

US durable goods orders soared by 9.2% mom in March to USD 315.7B, far surpassing expectations of a 1.5% mom gain. The sharp rise was driven almost entirely by a surge in transportation equipment, which jumped 27% mom to USD124.6B, marking a third consecutive monthly increase.

Orders excluding defense also posted a strong 10.4% mom gain to USD 300.0B, highlighting a significant boost in civilian aircraft and related components.

However, the underlying momentum in business investment appeared far less robust. Core orders excluding transportation were flat at USD 191.1B, missing forecasts for a modest 0.2% mom increase.

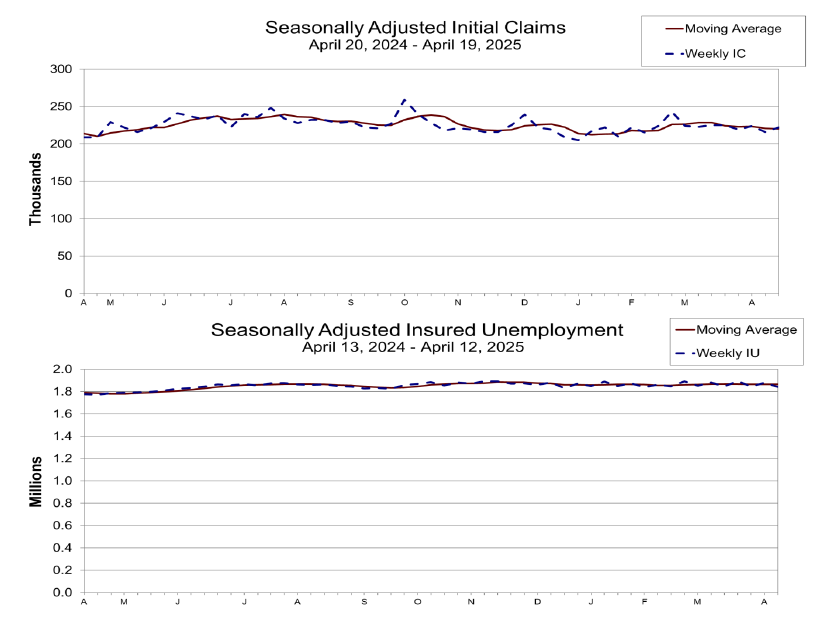

US initial jobless claims rise to 222k, matched expectations

US initial jobless claims rose 6k to 222k in the week ending April 19, matched expectations. Four-week moving average of initial claims fell -1k to 220k. Continuing claims fell -37k to 1841k in the week ending April 12. Four-week moving average of continuing claims fell -1.5k to 1864k.

ECB’s Nagel and Lane warn of growth hit from tariffs, downplay recession risk

German ECB Governing Council member Joachim Nagel acknowledged today that Germany faces significant downside risks to growth due to US tariffs.

“As far as economic growth is concerned, which of course also depends on the level of the respective tariffs, the impact in Europe will also be significant for Germany,” he warned.

But on inflation, "we are relatively certain that the impact on inflation in the US will be stronger than in the euro zone," Nagel added.

Separately, ECB Chief Economist Philip Lane told Bloomberg News that while the tariff shock will likely drag on Eurozone growth, the region is not on an automatic path toward recession.

Lane emphasized the bloc’s diversified trade relationships beyond the US, which could act as a cushion against a more severe downturn.

German Ifo climbs slightly to 86.9, but rising uncertainty signals turbulence ahead

Germany’s Ifo Business Climate Index edged higher in April, rising from 86.7 to 86.9 and beating market expectations of 85.2. Current Assessment Index climbed to 86.4 from 85.7. Expectations, while slightly lower at 87.4 compared to March’s 87.7, still surpassed the anticipated 85.0.

However, a closer look at the sectoral breakdown reveals growing divergence and fragility. Manufacturing sentiment deteriorated further, dropping from -16.6 to -18.1, while trade confidence took a notable hit, falling from -23.8 to -27.0. On the other hand, modest gains in services (from -1.1 to -0.8) and construction (from -24.3 to -21.9) offered some relief, though both remain firmly in negative territory.

The Ifo Institute cautioned that “uncertainty among the companies has increased,” adding that “the German economy is preparing for turbulence.”

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8215; (P) 0.8264; (R1) 0.8355; More….

USD/CHF's rebound from 0.8038 is still in progress and intraday bias stays mildly on the upside. However, strong resistance should be seen from 38.2% retracement of 0.9200 to 0.8038 at 0.8482 to limit upside. On the downside, break of 0.8038 will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

ECB’s Nagel and Lane warn of growth hit from tariffs, downplay recession risk

German ECB Governing Council member Joachim Nagel acknowledged today that Germany faces significant downside risks to growth due to US tariffs.

“As far as economic growth is concerned, which of course also depends on the level of the respective tariffs, the impact in Europe will also be significant for Germany,” he warned.

But on inflation, "we are relatively certain that the impact on inflation in the US will be stronger than in the euro zone," Nagel added.

Separately, ECB Chief Economist Philip Lane told Bloomberg News that while the tariff shock will likely drag on Eurozone growth, the region is not on an automatic path toward recession.

Lane emphasized the bloc’s diversified trade relationships beyond the US, which could act as a cushion against a more severe downturn.

US durable goods orders surge 9.2% mom on transportation demand, but underlying momentum stalls

US durable goods orders soared by 9.2% mom in March to USD 315.7B, far surpassing expectations of a 1.5% mom gain. The sharp rise was driven almost entirely by a surge in transportation equipment, which jumped 27% mom to USD124.6B, marking a third consecutive monthly increase.

Orders excluding defense also posted a strong 10.4% mom gain to USD 300.0B, highlighting a significant boost in civilian aircraft and related components.

However, the underlying momentum in business investment appeared far less robust. Core orders excluding transportation were flat at USD 191.1B, missing forecasts for a modest 0.2% mom increase.

US initial jobless claims rise to 222k, matched expectations

US initial jobless claims rose 6k to 222k in the week ending April 19, matched expectations. Four-week moving average of initial claims fell -1k to 220k.

Continuing claims fell -37k to 1841k in the week ending April 12. Four-week moving average of continuing claims fell -1.5k to 1864k.

Japanese Yen Rebounds After Corporate Service Inflation Beats Estimate

The yen has bounced back on Thursday after a massive slide a day earlier. USD/JPY is trading at 142.44 in the European session, down 0.67% on the day.

Japan's corporate service inflation eased to 3.1% in March from the revised 3.2% gain in February. This was higher than the market estimate of 3.0%.

Tokyo Core CPI expected to jump

On Friday, Tokyo Core CPI is expected to jump to 3.2% in April, following a 2.4% gain a month earlier. A sharp acceleration in Tokyo Core CPI would support the case for the Bank of Japan to continue raising interest rates. Last week, National Core CPI for March accelerated to 3.2% from 3.0%, primarily due to rising food costs.

Wages and inflation are on the rise but the uncertainty over US tariffs has complicated matters for the central bank, which be looking for more clarity about the tariffs before raising rates. The BoJ kept rates unchanged last month and is expected to stay on the sidelines again at the meeting on May 1.

Yen slides after Trump says he'll reduce China tariffs

The US dollar pummelled the yen on Wednesday, surging 1.3%. The dollar was powered by President Trump announcing that he planned to "substantially" lower tariffs on China. The financial markets viewed the statement as a signal that the US was de-escalating the trade war with China, although talks have not yen started between the two sides.

The market also reacted positively as Trump said he had no intention of dismissing Fed Chair Jerome Powell. Trump had launched a blistering attack on Powell in recent days and the US dollar and US equity markets retreated as Trump's threats on Powell eroded confidence in the US financial system.

USD/JPY Technical

USD/JPY has pushed below support below 142.82. Below, there is support at 142.07

There is resistance at 144.19 and 144.94

USDJPY 1-Day Chart, April 24, 2025

USD/CHF Rebounds from Multi-Year Low

As the charts show, the USD/CHF exchange rate fell below 0.810 US dollars per franc earlier this week. The pair had not traded this low since the 2008 financial crisis. Demand for the Swiss franc as a safe-haven currency was driven by concerns over the escalation of the trade war between the United States and other major economies.

However, the USD/CHF pair has since rebounded and is currently trading above 0.825. This recovery was supported by yesterday’s statement from Finance Minister Bessent at the JPMorgan Private Investors Conference, where he expressed optimism about imminent de-escalation in trade tensions with China.

Technical Analysis of the USD/CHF Chart

The chart indicates that the trend remains bearish, highlighted by the descending channel marked in red. A bullish attempt to push the price into the upper half of the channel earlier this morning (as shown by the arrow) failed to produce any significant momentum.

The price is fluctuating around the median line, a level where supply and demand tend to balance. It is possible that the market has already priced in the positive news from yesterday, and the bears may attempt to reassert pressure, driving the price back towards the 0.810 support level.

Nevertheless, much will depend on the fundamental backdrop. A stronger dollar could follow in response to possible developments such as:

→ a statement from China signalling readiness to de-escalate its tariff policy;

→ signs of progress in trade deals between the United States and key partners such as Japan, South Korea, and India.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.