Sample Category Title

US Opening Bell: Robust Earnings Fails to Lead Dow Jones and S&P Higher

- US stock futures remain flat despite strong earnings reports.

- Boeing faces delivery issues in China, while the Canadian Dollar weakens following lower-than-expected inflation data.

- Gold prices stay above $3200/oz and oil prices hold steady despite downward demand forecast revisions.

U.S. stock index futures stayed flat on Tuesday as investors weighed the chances of tariff relief for the auto industry after President Donald Trump suggested more exemptions might be possible.

Robust earnings releases premarket were not enough to guide US indexes higher. On the earnings front, Johnson & Johnson is holding its profit outlook steady despite the potential for tariffs. Bank of America shares rose in premarket after its stock traders posted a record quarter, as the company reaped the benefits of volatile markets.

A Bank of America survey showed that sentiment toward the economy is the most negative in three decades.

Boeing sank in premarket trading after China ordered airlines not to take any further deliveries of the company’s jets.

In the European session market moves appeared more measured compared to recent swings, as hopes grew for possible talks on Trump’s reciprocal tariffs.

Gold prices were slightly lower heading into the US session but remain comfortably above the $3200/oz handle.

Oil prices held their ground with minimal losses despite the IEA following OPECs lead and downgrading their demand forecasts for 2025.

Canadian inflation surprised to the downside a short while ago which has led to Canadian Dollar weakness. As a result, the Bank of Canada rate cut chances on Wednesday rose to 50% from roughly 40% before CPI data - Swaps Market Data.

Economic data releases

It is a quiet day on the data front for the US session with developments around tariffs likely to be key moving forward.

On the earnings front there are United Airlines and Interactive Brokers reporting after market close.

Chart of the day - Dow Jones

From a technical standpoint the Dow Jones continues to eye further gains as market participants hope the recovery is here to stay.

A bit too optimistic in my opinion but nevertheless still possible.

The 14-period RSI is eyeing a break back above the oversold 50 handle which could be seen as a sign of changing momentum and provide bulls with some impetus.

Immediate resistance rests at 40738 before the 41000 and 41400 handles come into focus.

Immediate support rests at 40000 before the 39588 and 39000 come into focus.

Source: TradingView

Support

- 40000

- 39588

- 39000

Resistance

- 40738

- 41000

- 41400

Inflation Eases as Canadians Adjust Travel Spending and Gas Prices Fall

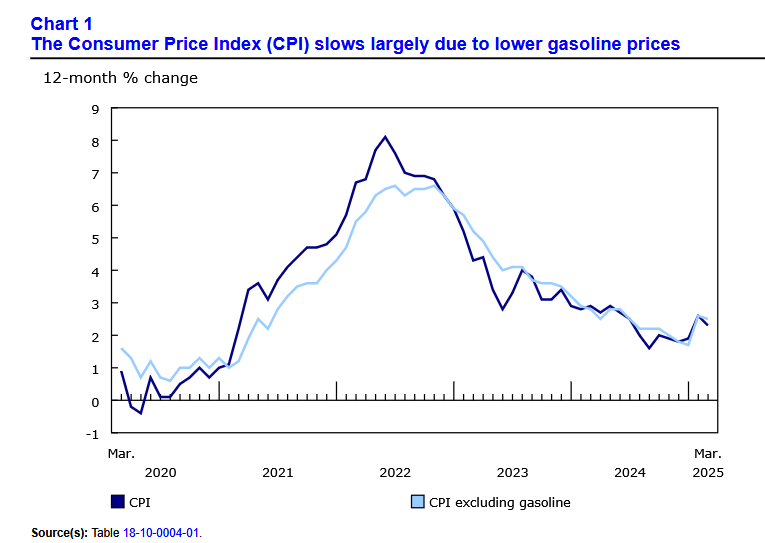

Headline CPI inflation for March came in at 2.3% year-on-year (y/y), below expectations for a 2.6% y/y print (and the February print of 2.6% y/y).

The deceleration was due to lower prices for gasoline and air travel. On the former, prices at the pump were down almost 2% on the month, and excluding this impact, inflation would have been at 2.5% y/y. The impact from travel was also notable, as travel tours and airfares fell 4.7% y/y and 12% y/y, respectively. Statcan noted that this was influenced by Canadians' forgone travel to the U.S.

Putting upward pressure on inflation was the full reinstatement of the GST/HST. This caused the prices for restaurant meals to jump to 3.2% y/y.

The Bank of Canada's (BoC) preferred "core" inflation measures held at 2.9% y/y.

Key Implications

Today's inflation report gave some reprieve from the ongoing threat of higher prices. On a three-month basis, the average of the BoC's core inflation rates eased to 2.7%, from 3.3%, while CPI ex-food and energy came in at 2.6%. This was an encouraging development. Looking forward, April should show further easing of inflation as the elimination of the carbon tax has pushed energy prices significantly lower. That should more than offset the impact of tariffs, but not forever. While inflation is expected to remain stable over the beginning of spring, the tariff impact will start pushing inflation back towards 3% starting in May/June.

The BoC is meeting tomorrow and the likelihood of another cut has shifted dramatically over the last week. The central bank will be weighing the inflation risk from tariffs against the downside risk coming from consumer/business sentiment surveys, a loosening job market, and a very weak real estate market. We are maintaining our call for another cut from the bank, as it should take out more insurance against the mounting downside risks to the economy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1289; (P) 1.1357; (R1) 1.1418; More...

EUR/USD dips mildly today as consolidation continues below 1.1472. Deeper pull back might be seen but downside should be contained by 1.1145 resistance turned support to bring another rally. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.

Euro Softens on ZEW Shock, Loonie Dips on CPI, Kiwi Leads

Euro is trading on the softer side in relatively quiet markets today, weighed down by a fresh round of weak economic data. The sharp plunge in German and Eurozone ZEW economic sentiment, triggered largely by mounting uncertainty over US trade policy, has deepened concerns about the region’s growth outlook. Adding to the dovish tone, ECB’s latest bank lending survey revealed that credit standards tightened and corporate loan demand weakened further in Q1, even before the tariff-driven turmoil of early April. Together, these developments strengthen the case for another ECB rate cut when the Governing Council meets this Thursday.

Canadian Dollar is also under some pressure following the latest CPI data, which showed headline inflation slowing more than expected. Core measures, including trimmed and common CPI, also came in softer than forecast. The figures mark a welcome reversal from February's surprise inflation spike and give BoC added flexibility to stay on hold at its policy meeting tomorrow. However, having already lowered rates from a peak of 5.00% to the current 2.75%, BoC may opt to preserve remaining policy ammunition while assessing the broader impact of US tariffs.

Overall in the currency markets, the New Zealand and Australian Dollars are leading gains for today, buoyed by stabilization in risk sentiment. Sterling is also firmer, as mixed UK labour market data is unlikely to derail BoE’s slow and steady approach to policy normalization. On the weaker end, the Swiss Franc is underperforming the most, followed by Loonie and Euro. Dollar and Yen are trading closer to the middle of the pack.

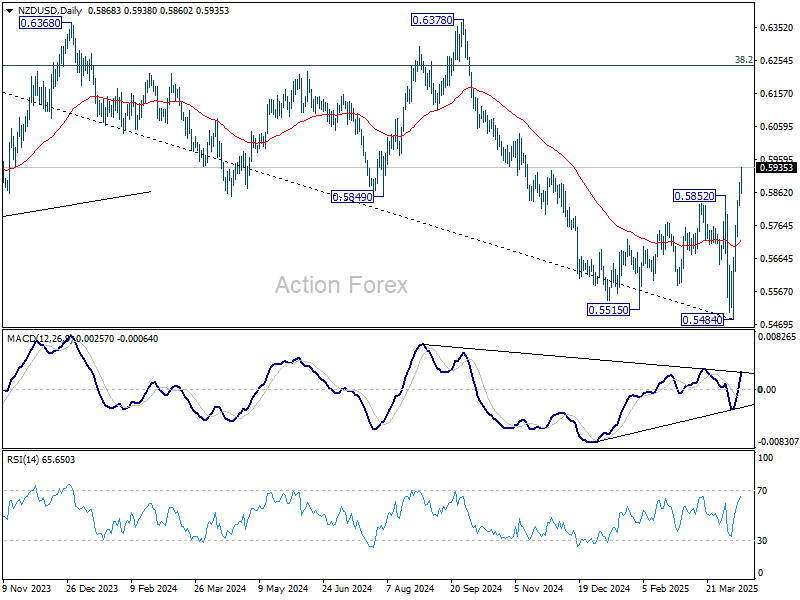

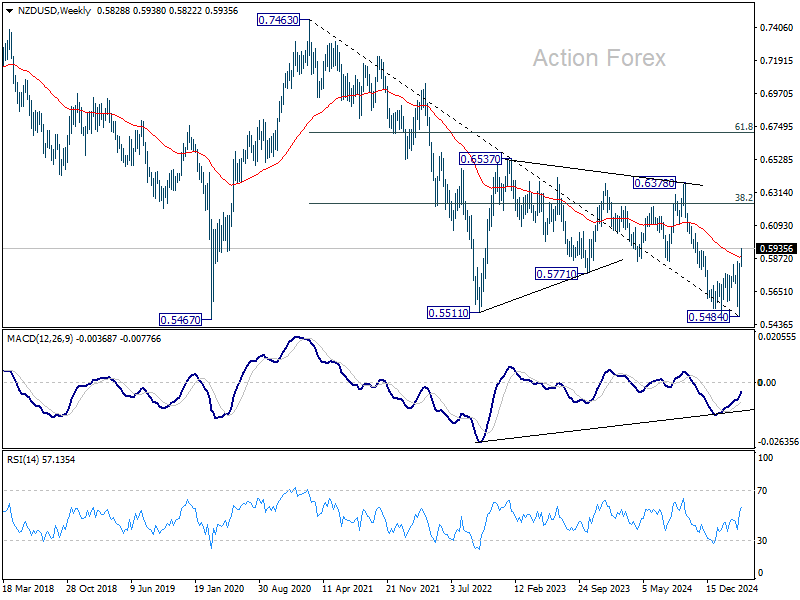

Technically, NZD/USD's strong break of 0.5852 resistance this week firstly confirms short term bottoming at 0.5484. More importantly, the break of 55 W EMA also suggests that a medium term bottom was formed, just ahead of 0.5467 key support (2020 low). Rise from 0.5484 could now be heading back to 38.2% retracement of 0.7463 to 0.5484 at 0.6240, even as a corrective bounce.

In Europe, at the time of writing, FTSE is up 0.88%. DAX is up 0.98%. CAC is up 0.23%. UK 10-year yield is down -0.004 at 4.662. Germany 10-year yield is up 0.037 at 2.548. Earlier in Asia, Nikkei rose 0.84%. Hong Kong HSI rose 0.23%. China Shanghai SSE rose 0.15%. Singapore Strait Times rose 2.14%. Japan 10-year JGB yield rose 0.035 to 1.376.

Canada's CPI slows to 2.6%, CPI common down to 2.3%

Canada’s headline inflation cooled more than expected in March, with the annual CPI rate easing to 2.3% yoy from 2.6% yoy, below consensus forecasts for no change. The deceleration was largely driven by falling prices in travel-related services and gasoline. On a monthly basis, CPI rose 0.3% mom, undershooting expectations of a 0.7% mom increase.

Core inflation metrics also pointed to moderation. CPI median held steady at 2.9% yoy, in line with expectations. But the trimmed mean slipped to 2.8% yoy from 2.9% yoy, and the common core fell to 2.3% yoy from 2.5% yoy, both coming in below forecast.

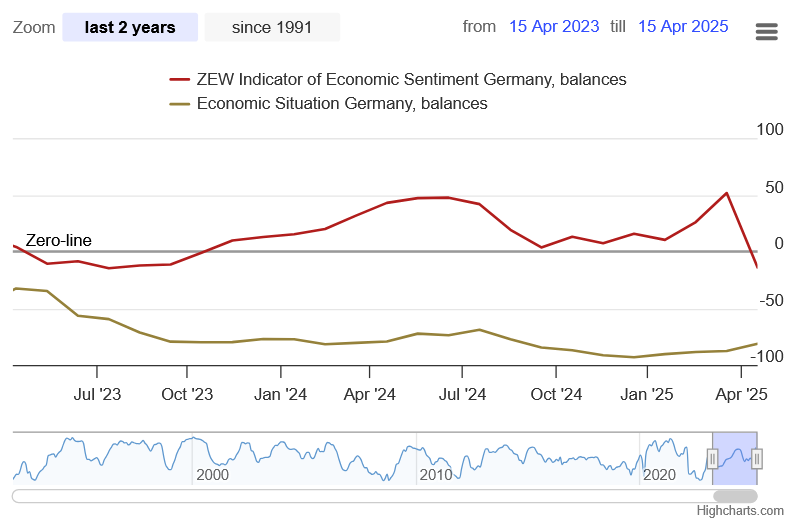

German ZEW collapses to -14 as trade uncertainty rattles outlook

Investor confidence in Germany took a sharp turn for the worse in April, with ZEW Economic Sentiment Index plummeting from 51.6 to -14, its steepest decline since the onset of the Russia-Ukraine war in 2022.

The drop came in well below expectations of 10.6 and reflects mounting concerns over US trade policy, which ZEW President Achim Wambach described as marked by “erratic changes.” The Current Situation Index, however, showed a modest improvement, rising from -87.6 to -81.2, slightly better than forecast.

Eurozone also saw a significant deterioration in investor sentiment, with ZEW expectations gauge falling from 19.8 to -18.5, missing the anticipated 14.2 reading. Current Situation Index dropped by -5.7 points to -50.9.

According to ZEW, sectors most vulnerable to trade disruptions—such as autos, chemicals, and engineering—are now under renewed pressure, despite recent signs of stabilization. The growing unpredictability in global trade dynamics is weighing heavily on future expectations, dampening optimism across the bloc.

Despite the worsening sentiment, financial market participants do not foresee a renewed surge in inflation. This perception, ZEW notes, gives ECB some room to continue its easing cycle in an effort to support growth.

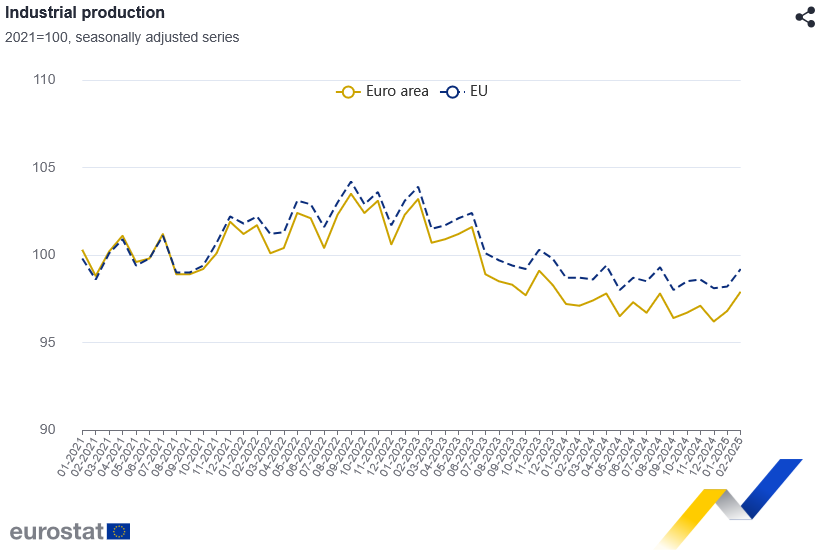

Eurozone industrial output surges in 1.1% mom in Feb, driven by consumer and capital goods

Eurozone industrial production posted a stronger-than-expected gain of 1.1% mom in February, well above the 0.1% mom forecast. The increase was largely driven by a 2.8% jump in non-durable consumer goods and a solid 0.8% rise in capital goods output. Intermediate goods also rose modestly by 0.3%, while energy production and durable consumer goods declined by -0.2% -and 0.3%, respectively.

Across the broader EU, industrial production rose 1.0% on the month, with Ireland (+10.8%), Belgium (+7.4%), and Luxembourg (+6.3%) leading the gains. Meanwhile, Croatia (-3.9%), Greece (-3.6%), and Romania (-2.1%) recorded the steepest declines.

UK payolled employment falls -78k, wage growth slows

UK payrolled employment falling -by 78k in March, down 0.3% mom. Median monthly pay growth also moderated to 4.8% yoy from 5.5% yoy, pointing to easing wage pressures. Meanwhile, claimant count rose by 18.7k, less than the expected 30.3k increase.

In the three months to February, unemployment rate held steady at 4.4%, in line with expectations. Wage growth came in slightly below forecasts across the board. Average earnings including bonuses rising 5.6% yoy (unchanged from the previous month) and those excluding bonuses up 5.9%, a touch softer than the anticipated 6.0% yoy.

RBA Minutes: Next rate move not predetermined, China’s tariff response a key variable

The minutes from RBA’s March 31–April 1 meeting revealed emphasized that it was "not yet possible to determine the timing of the next move in interest rates." The Board emphasized the importance that the "next decision was not predetermined".

Members agreed that the May meeting would offer a more "opportune time" for reassessment, as it would coincide with updated data on inflation, wages, employment, and global tariff developments, as well as a revised set of economic forecasts.

RBA highlighted that the economic outlook could be significantly shaped by how Chinese authorities respond to global tariff developments. Meanwhile, RBA acknowledged that risks to the outlook exist on both sides.

On one hand, global trade uncertainties and softening demand may pose disinflationary pressures, while on the other, risks such as supply chain disruptions and currency depreciation could fuel inflation.

RBA opted to keep the cash rate unchanged at 4.10% at the meeting.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1289; (P) 1.1357; (R1) 1.1418; More...

EUR/USD dips mildly today as consolidation continues below 1.1472. Deeper pull back might be seen but downside should be contained by 1.1145 resistance turned support to bring another rally. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.

Canada’s CPI slows to 2.6%, CPI common down to 2.3%

Canada’s headline inflation cooled more than expected in March, with the annual CPI rate easing to 2.3% yoy from 2.6% yoy, below consensus forecasts for no change. The deceleration was largely driven by falling prices in travel-related services and gasoline. On a monthly basis, CPI rose 0.3% mom, undershooting expectations of a 0.7% mom increase.

Core inflation metrics also pointed to moderation. CPI median held steady at 2.9% yoy, in line with expectations. But the trimmed mean slipped to 2.8% yoy from 2.9% yoy, and the common core fell to 2.3% yoy from 2.5% yoy, both coming in below forecast.

USD/CHF Outlook: Swiss Franc at 15-Year Highs on Safe-Haven Flows

- With tariff disruption boosting safe-haven inflows, USD/CHF currently trades at around 0.81562, a level last seen in September 2011

- Rapid appreciation of the Swiss franc’s value could prove a cause for concern for the SNB, with already some suggestion of intervention

- US treasury yields in sharp decline amid market uncertainty and volatile trading conditions

With FX markets heating up considerably in recent weeks, the Swiss franc remains one of the best-performing major currencies amid a flight to safety and wavering risk appetite.

Starting the year somewhat unremarkably, heightened geopolitical tensions, especially regarding tariffs and global trade, are currently weighing heavily on the USD/CHF exchange rate.

With last week being the pair’s worst performance in over 125 months, recent bear pressure saw USD/CHF break previous monthly support held around ~0.84414. Now trading at a level last seen during the height of the Greek government debt crisis, USD/CHF will need to find support or risk a further leg down towards 0.81000.

A chart showing the recent price action of USD/CHF. OANDA, TradingView, 15/04/2024.

USD/CHF: Tariffs, trade wars and global trade

The announcement of sweeping global tariffs and their potential impact on international trade has undeniably been the most significant deciding factor in USD/CHF in recent weeks.

Trading around ~7.35% lower since President Trump’s now-infamous “Liberation Day,” the outcome of recent announcements has been decidedly clear for USD/CHF exchange pricing - a weaker dollar and stronger franc.

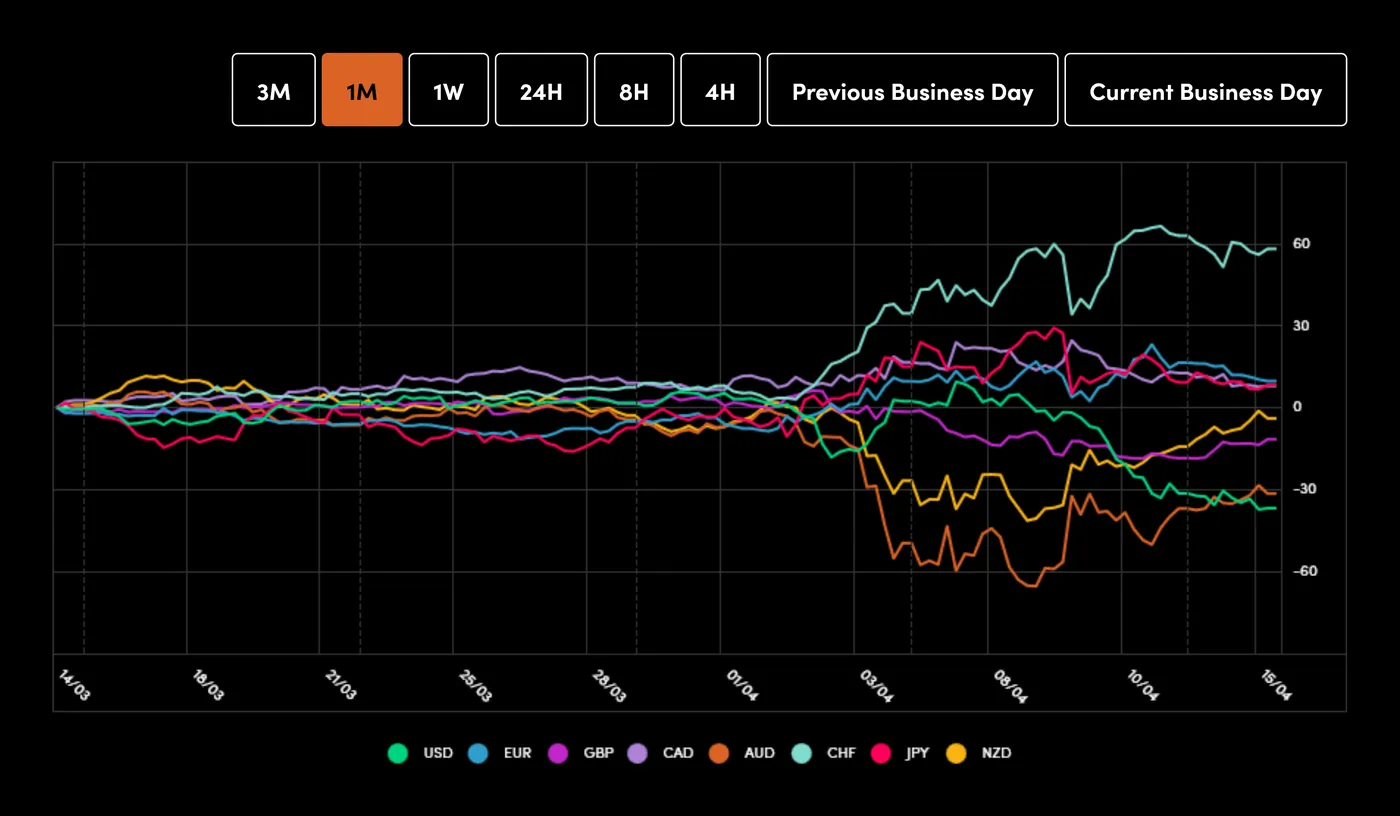

Fig 1: Currency Power Balance tool (Source: OANDA Global Markets)

Benefiting from broader safe-haven inflows and general market uncertainty, recent announcements of a 90-day deferment of “reciprocal” tariffs bar China have done little to slow USD/CHF’s descent to new lows, with market attention focused on how the United States will navigate trade relations with some of its key trading partners, namely the European Union and China.

The latter has only recently been subject to a staggering 145% levy on most imports to the US, with fears of an escalating ‘trade war’ between the US and China being more prevalent now than in recent memory, with key imports like semiconductors, lithium-ion batteries, and steel to be caught in the crossfire.

As for USD/CHF pricing, any worsening of trade tensions or a general widening of tariff restrictions globally will increase market risk aversion and likely weigh negatively on USD/CHF in the short term.

USD/CHF: How will the SNB approach a stronger franc?

Playing second fiddle to the euro for much of Q1, the sudden appreciation in the franc’s value will undoubtedly have caught the watchful eye of the Swiss National Bank (SNB).

Trading at multi-year highs versus the dollar, yen, and pound, the SNB has previously warned of the dangers of a too-strong franc. Citing the competitiveness of exports, the SNB is now faced with the unique challenge of managing rates while the threat of tariffs as high as 31% on most Swiss exports loom, further compounded by a stronger currency.

With excessive inflation a non-issue in the Swiss economy, the recent bout of franc strength has some already speculating that the SNB may explore the possibility of zero percent or even negative interest rates in an attempt to halt a runaway strengthening of the currency.

While this remains somewhat unlikely for now, an interest rate cut in the SNB’s June decision may become a stronger possibility should USD/CHF pricing continue its current trajectory.

USD/CHF: Technical analysis & outlook

- Having broken previously held support around ~0.84414, USD/CHF now flirts with the key level of 0.81000. Should the price break down further, bears will likely target 0.80202

- According to the daily 14-period ATR, USD/CHF markets are currently rated ‘oversold’ for the first time since August 2024. When taken at face value, this could suggest the current move is exhausted and will need to consolidate before a further leg down. US treasury yields in sharp decline amid market uncertainty and volatile trading conditions

- For only the fourth time in ten years, USD/CHF currently trades with a daily ATR reading in excess of 120 pips, suggesting markets are highly volatile

GBP/USD Analysis: Labor Data, Inflation Watch & Key Trading Levels

- GBP/USD is trading at levels last seen in October 2024, with recent UK labor data showing wage growth.

- Market participants are watching for cues on the Bank of England's potential rate cut at the May 8, 2025 meeting, particularly focusing on upcoming inflation data.

- Key technical levels for GBP/USD include resistance at 1.3261, 1.3433, and 1.3500, and support at 1.3100, 1.3000, and 1.2864.

GBP/USD continues to advance, now trading at levels last seen in October 2024. Earlier this morning the Office of National Statistics (ONS) released labor data which showed that wage growth ticked higher.

Regular pay in the UK, not counting bonuses, rose 5.9% year-on-year to £670 per week in the three months leading to February 2025. This was slightly more than the revised 5.8% growth seen before and close to the 6% forecast. Wages in the private sector grew by 5.9%, while public sector wages hit 5.7%, the highest since mid-2024, thanks to recent pay raises showing up in the data.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

By industry, the biggest pay increases were in wholesale, retail, hotels, and restaurants (6.8%), followed by construction (6.2%), services (5.9%), manufacturing (5.7%), and finance/business services (4.8%). After factoring in inflation, real wages went up by 2.1%, the same as in the prior period.

Market participants were no doubt looking for cues and hints at what the Bank of England (BoE) policymakers might do at the upcoming BoE meeting on May 8, 2025. As things stand markets continue to price in around 91% probability of a 25 bps rate cut.

Source: LSEG

Tomorrow we have UK inflation data with a particular emphasis on the UK CPI print and services inflation in particular. Service inflation has been earmarked as the key area of concern for the BoE and another drop here will likely solidify the belief in a rate cut for the May meeting.

Economists expect the UK core CPI to have grown at a steady pace of 3.5% with the headline figure expected to come in at 2.7%.

Technical Analysis - GBP/USD

Looking at GBP/USD from a technical standpoint, the rally to the upside is now a whisker away from a key level of resistance at 1.3261 (August 2024 swing high).

Having made a new high there is a possibility that some form of pullback may occur here but this will largely depend on the US dollar's performance in the coming days.

Another warning of a potential retracement comes from the period-14 RSI which is starting to show signs of bearish divergence. The RSI has failed to make fresh highs while price action has already printed a fresh high(trading above April 3 swing high) just shy of the key 1.3261 handle. Could this level be the precursor for a retracement?

My only concern here is any retracement may prove a shallow one without a US Dollar recovery.

Immediate resistance rests at 1.3261 before the 2024 yearly high around the 1.3433 handle comes into focus. Beyond that we have to keep an eye on the 1.3500 handle.

Support on the other hand is provided by the 1.3100 and 1.3000 psychological level. A break of 1.3000 could be a sign that bearish pressure is building but a close below the 1.2700 handle would be needed for a change in structure to be confirmed on the daily timeframe. .

GBP/USD Daily Chart, April 15, 2025

Source: TradingView.com

Support

- 1.3100

- 1.3000

- 1.2864

Resistance

- 1.3261

- 1.3433

- 1.3500

German ZEW collapses to -14 as trade uncertainty rattles outlook

Investor confidence in Germany took a sharp turn for the worse in April, with ZEW Economic Sentiment Index plummeting from 51.6 to -14, its steepest decline since the onset of the Russia-Ukraine war in 2022.

The drop came in well below expectations of 10.6 and reflects mounting concerns over US trade policy, which ZEW President Achim Wambach described as marked by “erratic changes.” The Current Situation Index, however, showed a modest improvement, rising from -87.6 to -81.2, slightly better than forecast.

Eurozone also saw a significant deterioration in investor sentiment, with ZEW expectations gauge falling from 19.8 to -18.5, missing the anticipated 14.2 reading. Current Situation Index dropped by -5.7 points to -50.9.

According to ZEW, sectors most vulnerable to trade disruptions—such as autos, chemicals, and engineering—are now under renewed pressure, despite recent signs of stabilization. The growing unpredictability in global trade dynamics is weighing heavily on future expectations, dampening optimism across the bloc.

Despite the worsening sentiment, financial market participants do not foresee a renewed surge in inflation. This perception, ZEW notes, gives ECB some room to continue its easing cycle in an effort to support growth.

Eurozone industrial output surges in 1.1% mom in Feb, driven by consumer and capital goods

Eurozone industrial production posted a stronger-than-expected gain of 1.1% mom in February, well above the 0.1% mom forecast. The increase was largely driven by a 2.8% jump in non-durable consumer goods and a solid 0.8% rise in capital goods output. Intermediate goods also rose modestly by 0.3%, while energy production and durable consumer goods declined by -0.2% -and 0.3%, respectively.

Across the broader EU, industrial production rose 1.0% on the month, with Ireland (+10.8%), Belgium (+7.4%), and Luxembourg (+6.3%) leading the gains. Meanwhile, Croatia (-3.9%), Greece (-3.6%), and Romania (-2.1%) recorded the steepest declines.

Gold Prices Remain Elevated Amid Concerns Over Trump’s Tariffs

On Tuesday, the price of gold climbed to 3,220 USD per troy ounce as market uncertainty surrounding US President Donald Trump’s tariff policies continued to support demand for safe-haven assets.

Key factors driving gold’s movement

The precious metal’s stability is closely tied to lingering uncertainty over Trump’s tariffs. After temporarily exempting technology products from reciprocal duties, his administration is now considering similar exemptions for auto parts.

However, the White House heightened tensions on Monday by launching a national security probe into pharmaceutical and semiconductor imports – a move that could pave the way for additional tariffs.

Further supporting gold prices were comments from Christopher Waller, a member of the Federal Reserve Board of Governors, who suggested that interest rates could be cut soon if Trump’s sweeping tariffs remain in place.

Markets are currently pricing in an 86-basis-point rate cut by the end of the year, though most investors expect the Fed to hold rates steady in May.

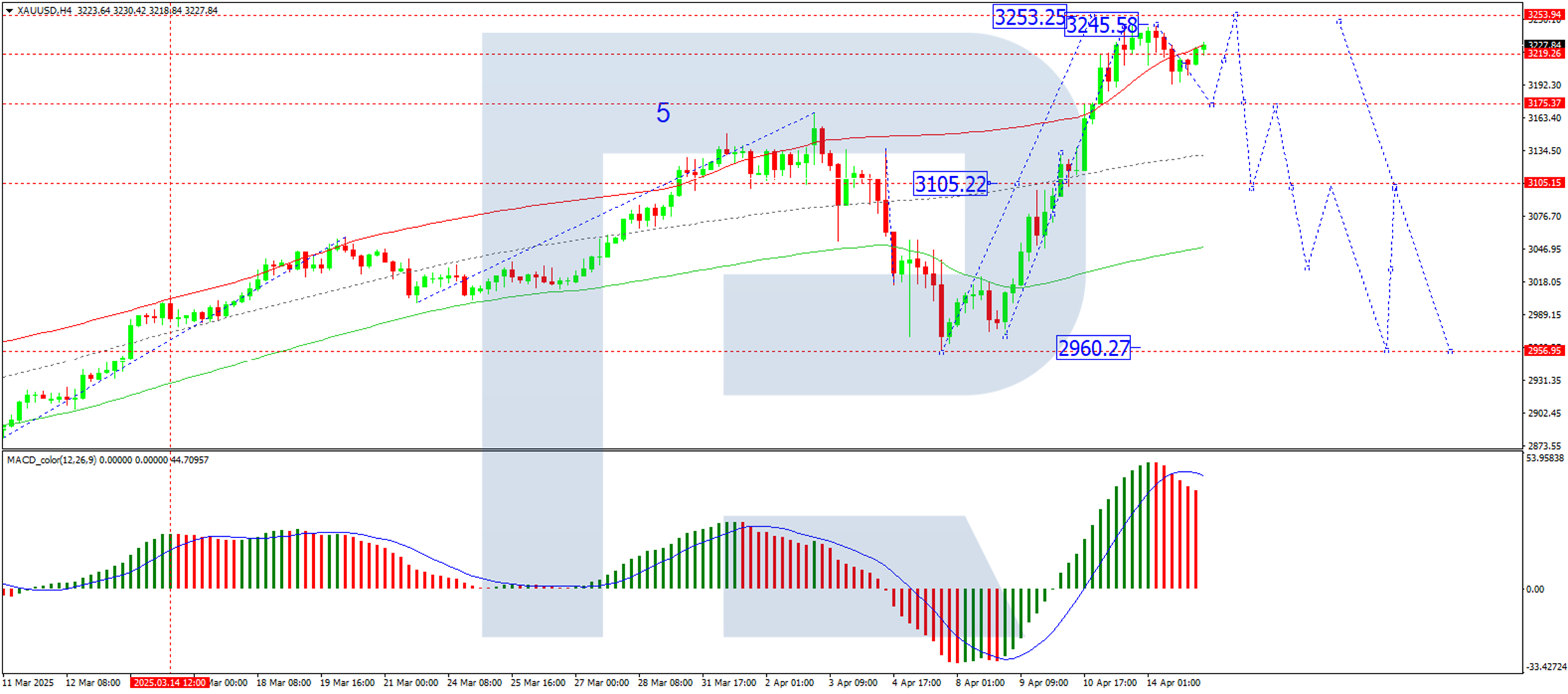

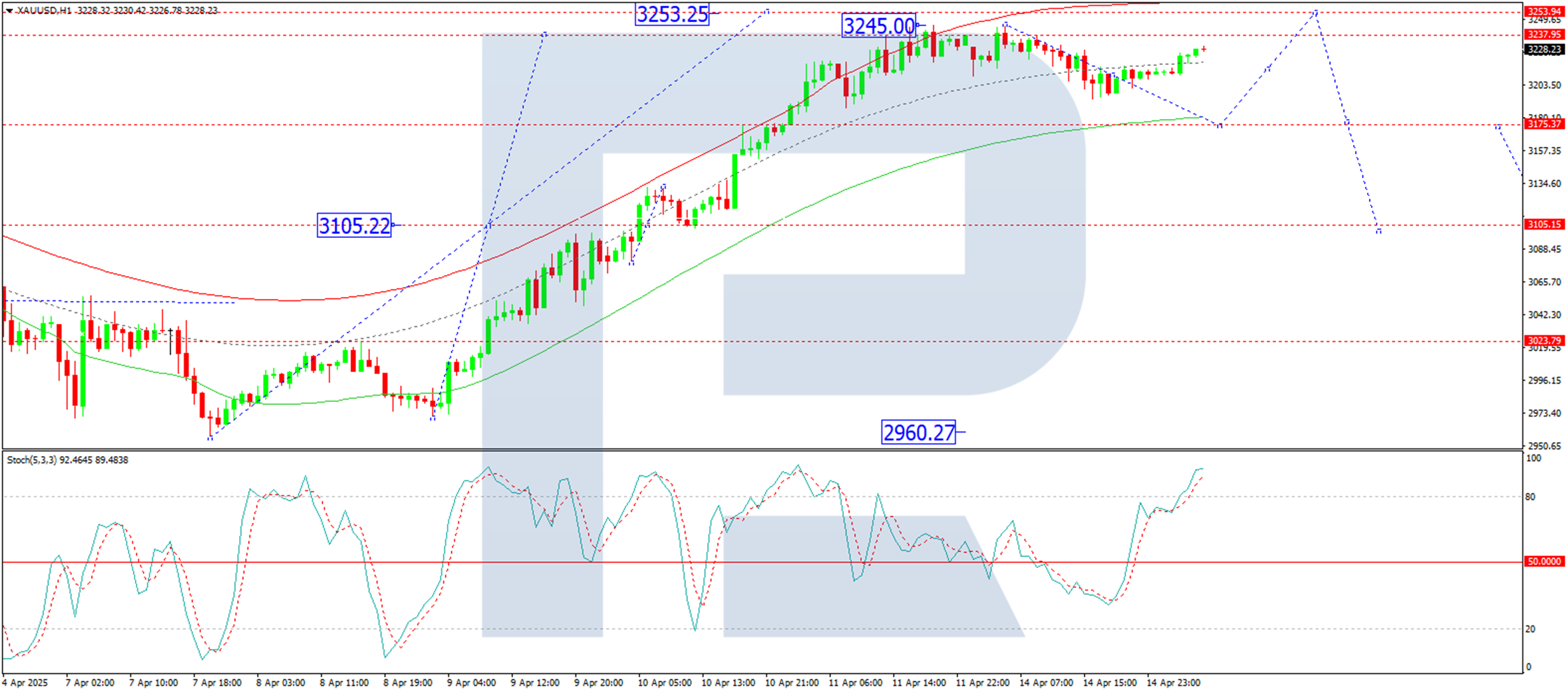

Technical analysis: XAU/USD

H4 Chart Overview

- The market saw an upward wave, peaking at 3,245, followed by a correction to 3,194

- Today, consolidation is expected around 3,220. A downside breakout could trigger a further correction towards 3,175, after which a rebound towards 3,253 may follow

- Conversely, an upside breakout may extend the rally to 3,253, the primary target of this growth wave

- A subsequent decline towards 3,105 is anticipated

- The MACD indicator supports this outlook, with its signal line at extreme highs and poised for a pullback towards zero

H1 Chart Overview

- The market completed a third-wave advance to 3,245, with consolidation now likely beneath this level

- A downside exit may initiate a correction towards 3,175, while an upside exit could extend gains to 3,253, where the uptrend may exhaust itself

- Beyond this, a deeper corrective decline towards 3,105 is possible

- The Stochastic oscillator aligns with this view, with its signal line above 80 and showing signs of an impending reversal

Conclusion

Gold remains buoyed by geopolitical and monetary policy uncertainty, with technical indicators suggesting near-term consolidation before potential further upside, followed by a corrective pullback.