Sample Category Title

Will US Retail Sales Show Consumers Retreating?

In focus today and over the holidays

Today the US March retail sales and industrial production data is due for release in the afternoon. Markets will pay extremely close attention to especially retail sales, which provides hard evidence of how consumer behaviour has evolved after Trump's tariffs began to take effect. Keep in mind that the data has been collected before the 'Liberation Day' announcements. In the evening, the Fed chair Powell is scheduled to speak at the Economic Club of Chicago at 19.30CET.

From the euro area, we receive the final March inflation data. We expect the data to confirm the flash release, leading to no market reaction as focus has shifted from inflation towards growth concerns and the trade war.

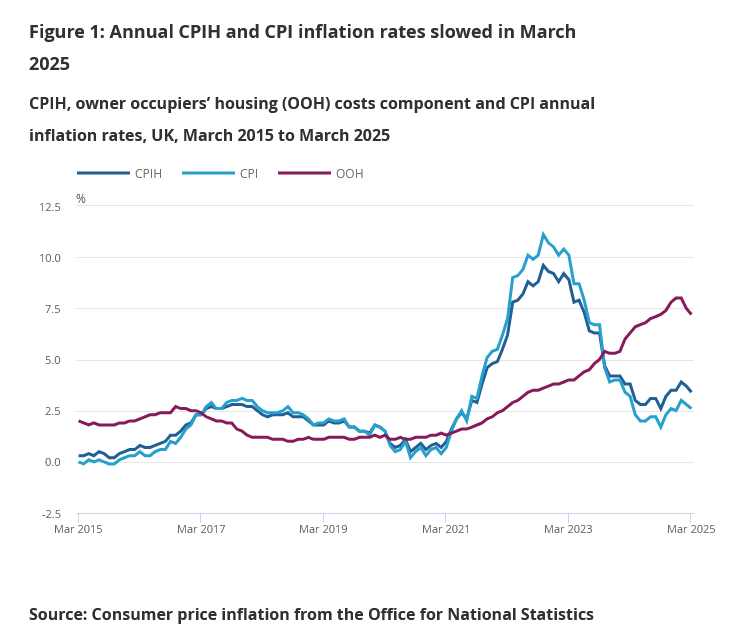

UK CPI is also being released bringing in inflation data for March. Consensus expects a drop in both headline to 2.7% y/y from 2.8% y/y, core to 3.4% y/y from 3.5% y/y and service inflation to 4.8% y/y from 5.0% y/y. If consensus estimates hold, the Bank of England should stay on track to ease monetary policy at its next meeting in May.

The Bank of Canada meeting takes place today at 15:45 CEST. Markets and consensus are leaning towards an unchanged rate decision, with markets pricing in approximately 9bp of cuts. We project that the BoC will deliver a 25bp rate cut, bringing the policy rate to 2.50%. Tariff uncertainty remains elevated and is slowly passing through to soft data, as evidenced, by the relatively downbeat Q1 Canadian business and consumer sentiment reports - supporting the case for a rate cut.

On Thursday, all eyes are on the ECB meeting, where we expect the ECB to cut the policy rate by 25bp to 2.25%, in line with market pricing and consensus. We expect the statement to repeat "monetary policy is becoming meaningfully less restrictive" and Lagarde to highlight the downside risks to growth from the trade war while abstaining from giving any clear guidance on future rate decisions. We expect Lagarde to communicate that the ECB is ready to use all instruments if financial market turmoil increases but currently do not see signs of markets not working in orderly fashion. Going forward, we expect the ECB to deliver three 25bp cuts at the upcoming meetings, bringing the deposit rate to 1.50% by September 2025.

Economic and market news

What happened overnight

In China, quarterly GDP data printed at a very strong level of 5.4% y/y over consensus expectations of 5.1% y/y. Both industrial output at 7.7% y/y and retail sales at 5.9% y/y also significantly exceeded expectations showing significant increases in domestic consumption. However, we are now in Q2 and looking ahead Chinese growth is bound to take a big hit from the massive increase in US tariffs, which is set to lead to a nosedive in exports and also GDP.

What happened yesterday

In the euro area, the ECB Bank Lending Survey pointed to continued stabilising lending conditions following gradual improvements over the past years and balance is to the dovish side. Banks noted an additional tightening of credit standards for companies while also noting a more muted demand for loans. Likewise, risk perceptions and credit quality deterioration continues to weigh on lending to firms and consumers. Credit growth remains muted and combined with the negative impact from the trade war, this should keep ECB on track to deliver further easing. Please note the survey was conducted before Liberation Day.

In Germany, optimism about the economy has waned amid trade war uncertainties. The ZEW Economic Sentiment Index fell sharply to -14.0 in April from 51.6 in March, marking the lowest since summer 2023. Despite a slight improvement in current economic conditions, they remain low at -81.2 (cons: -86.8). Trade tensions, especially with the US and China, significantly impact Germany, with the automotive industry facing a 25% tariff in the US.

In the UK, the labour market report for February/March was fairly in line with expectations with a slight tilt to the soft side. Unemployment rate remains unchanged at 4.4% as expected. Wage growth excluding bonuses was lower than expected at 5.9% for both the whole economy and the private sector with downward revisions for the previous month. Payrolls for March dropped by 78k, with a downward revision of 8k for February. This should keep the BoE set to deliver its next cut in May in line with our expectations.

In Sweden, the spring budget bill was an expected non-event, as most of its contents had already been pre-announced. The additional spending of SEK 11.5 billion is about 0.2% of GDP, but it should be added to the SEK 60 billion announced in September last year for 2025. The new proposals in the spring budget (announced back in March) centre around an extended tax cut for home renovations, which is rather narrow in terms of target group. The spring bill also comes in the context of increased defence spending, which will be formalised for the upcoming autumn bill and will, in our view, result in an upward revision of the borrowing requirement when the Debt Office presents a new borrowing forecast in May.

Equities: Global equities edged slightly higher yesterday, although the real headline was Europe outperforming the U.S. by over 1 percentage point. European markets closed broadly higher, while most major U.S. indices ended the day flat or marginally down. Cyclicals slightly outperformed defensives, and the VIX remains elevated around 30.

In the U.S. yesterday, the Dow declined by 0.4%, the S&P 500 by 0.2%, the Nasdaq by 0.1%, and the Russell 2000 rose by 0.1%.

This morning, Asian markets are trading lower, led by a sharp 2.5% drop in Hong Kong. This comes despite stronger-than-expected Chinese macro data, as industrial production, retail sales, and GDP all surpassed forecasts, with GDP coming in at 5.4% year-on-year.

Futures in both the U.S. and Europe are pointing lower this morning. U.S. tech futures are under particular pressure after Nvidia warned of a $5.5 billion write-down this quarter, citing repercussions from the ongoing trade war.

FI&FX: In an otherwise relatively quiet week so far, EUR/USD slipped below 1.13 as the broad USD paused its five-day slide and Treasury bonds climbed, after Treasury Secretary Scott Bessent downplayed the recent sell-off. Risk-on sentiment in markets provided support for European yields during yesterday's session, leading to a bearish steepening of the German curve. Positive market sentiment and equities tracking higher further supported GBP FX ahead of the release of UK CPI this morning.

Don’t Expect Powell to Cave to Market Expectations of Growth-Supporting Rate Cuts

Markets

The first two sessions of the trading-shortened Easter week developed orderly, with markets recovering somewhat from last week’s mayhem. News flow of the last 24 hours or so suggests that the risk rebound will face a tough test. Markets initially seemed to turn a blind eye to them, until the Trump administration extended the list of export controls to Nvidia’s tailormade H20 chips for China in another escalation of the trade conflict between the US and China. Other worrying headlines included US probes into semiconductor, pharmaceutical and possibly critical minerals imports which are a prelude of more sectoral tariffs, China ordering airlines not to take further deliveries of Boeing jets, rumours on scant progress being made in trade talks between the EU and the US and disappointing Q1 ASML earnings. The negative trade headlines start to outweigh the reprieve coming from the 90-day pause in reciprocal tariffs and from some product exemptions (eg certain electronics or car parts). Asian stock markets dive 1% to 2% lower this morning with European and US equity futures also spelling trouble ahead. In last week’s market sell-off, German Bunds significantly outperformed US Treasuries. We expect those dynamics to hold as investors come to terms with higher US risk premia. In the same vein, we stick to our positive view for EUR/USD. In yesterday’s vacuum, the pair tested last week’s broken resistance (now turned into support) at 1.1274/76. That level held with the pair currently changing hands around 1.1370. The Japanese yen outperforms this morning with USD/JPY testing the YTD low this morning just above 142. The Swiss franc is also heading back to the EUR/CHF 0.9220/10 support area.

Today’s eco calendar contains March US retail sales and industrial production figures, together with a $13bn 20-yr US bond auction and a keynote speech by Fed Chair Powell on the economic outlook. Especially the latter could hurt sentiment further as we don’t expect Powell to cave to market expectations of growth-supporting rate cuts, sticking to the anti-inflation line instead. US Treasuries could in such scenario lose new ground. This morning’s UK inflation numbers (March) were slightly lower than feared (0.3% M/M & 3.4% Y/Y for headline; core CPI 3.4% Y/Y; services CPI 4.7% Y/Y) and suggest that the BoE for now can stick to its quarterly cutting pace in May. EUR/GBP rises from 0.8525 to 0.8570 this morning.

News & Views

China’s economy expanded by 1.2% q/q and 5.4% year-over-year in the first quarter of 2025. The solid growth was supported in part by frontloading exports before widely expected tariffs kicked in. In the accompanying monthly data set, industrial production for example quickened sharply in March to 7.7% y/y. Retail sales also accelerated and more than expected. The 5.9% in March was the fastest pace since December 2023. Since US president Trump’s Liberation Day, however, circumstances dramatically changed and makes repeated solid expansions increasingly difficult. China’s statistics bureau noted that “the external environment is becoming more complex and severe, the drive for growth of effective domestic demand is insufficient, and the foundation for sustained economic recovery and growth is yet to be consolidated.” Calls on the government for additional fiscal stimulus will likely continue ahead of the Politburo meeting end of April. China’s yuan this morning shrugs at the decent but outdated GDP numbers and is caught in the broader risk off move. USD/CNY jumps to 7.327.

Hungary’s freshly appointed central bank deputy governor Kurali vowed to conduct an orthodox monetary policy during his confirmation hearing before parliament yesterday. “In the current economic environment, we need an interest rate policy that can guarantee price stability in tandem with financial and market stability.” He said the central bank needs to maintain a positive real interest rate to have inflation slowing down to the 3% +/- 1 ppt target range. The central bank’s policy rate today stands at 6.5% compared with 4.7% inflation (March). Kurali also noted the government needs to reduce deficits and debt in order to have sustained economic growth. Rating agency S&P last week downgraded Hungary’s rating outlook to negative from stable over fiscal concerns after PM Orban ramped up pre-election spending. Hungary’s rating is just one notch above junk (BBB-). The Hungarian forint appreciated after Kurali’s comments but continues to trade at weak levels around EUR/HUF 408.

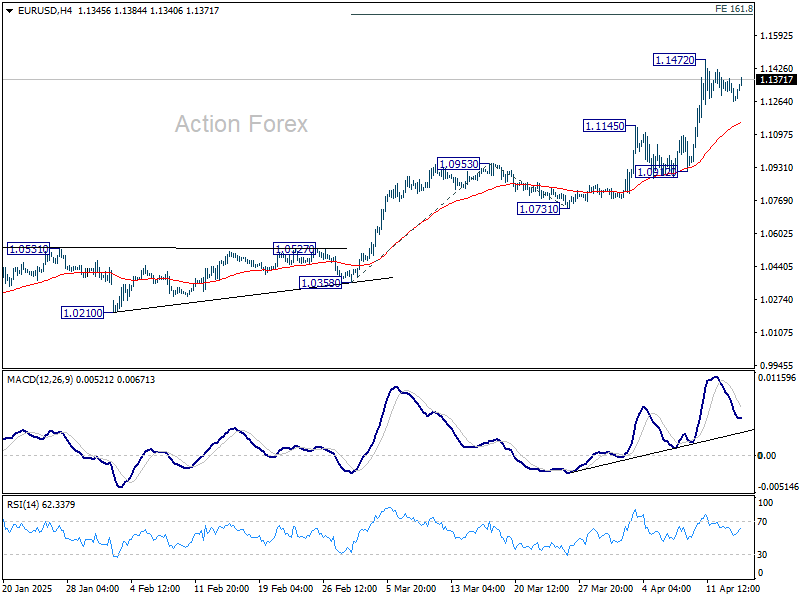

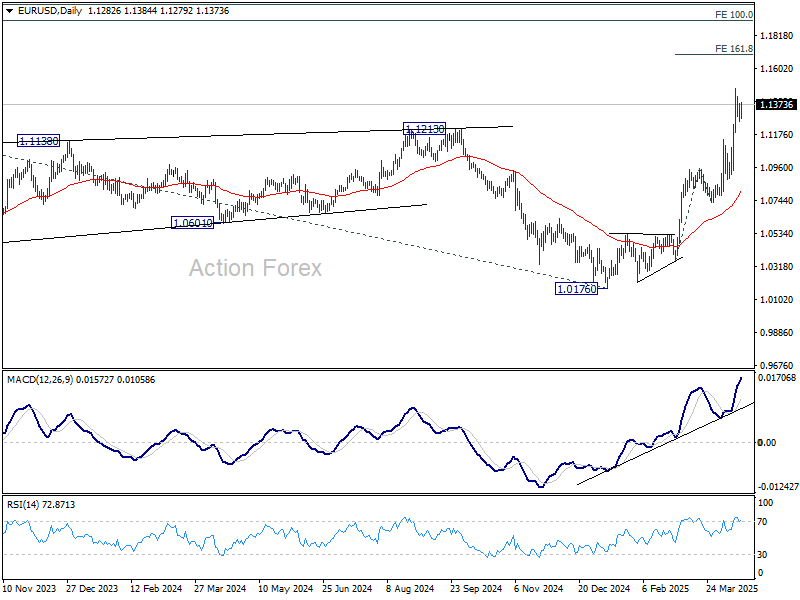

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1238; (P) 1.1308; (R1) 1.1353; More...

Intraday bias in EUR/USD remains neutral for the moment. More consolidations could be seen below 1.1472 and deeper pullback cannot be ruled out. But downside should be contained by 1.1145 resistance turned support to bring another rally. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.

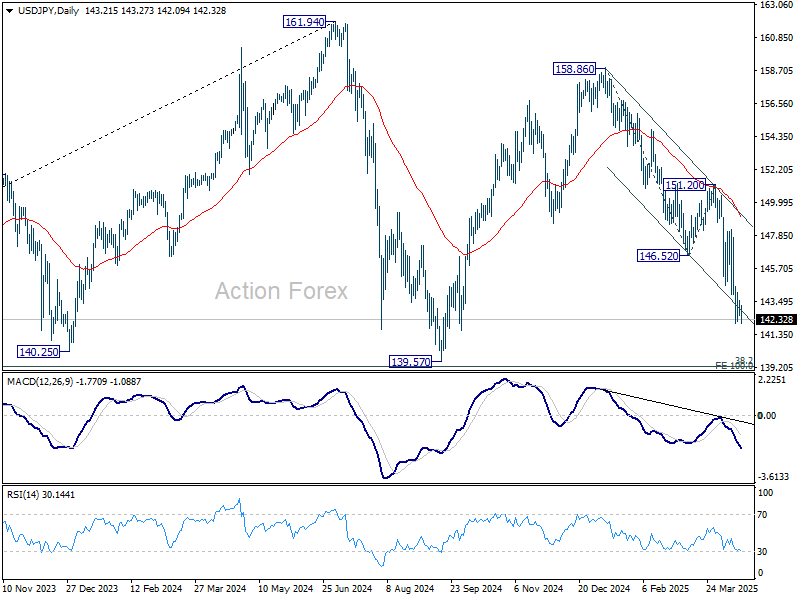

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.71; (P) 143.15; (R1) 143.70; More...

Intraday bias in USD/JPY remains neutral as consolidations continue above 142.05 temporary low. Stronger recovery might be seen but outlook will stay bearish as long as 151.20 resistance holds. Below 142.05 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

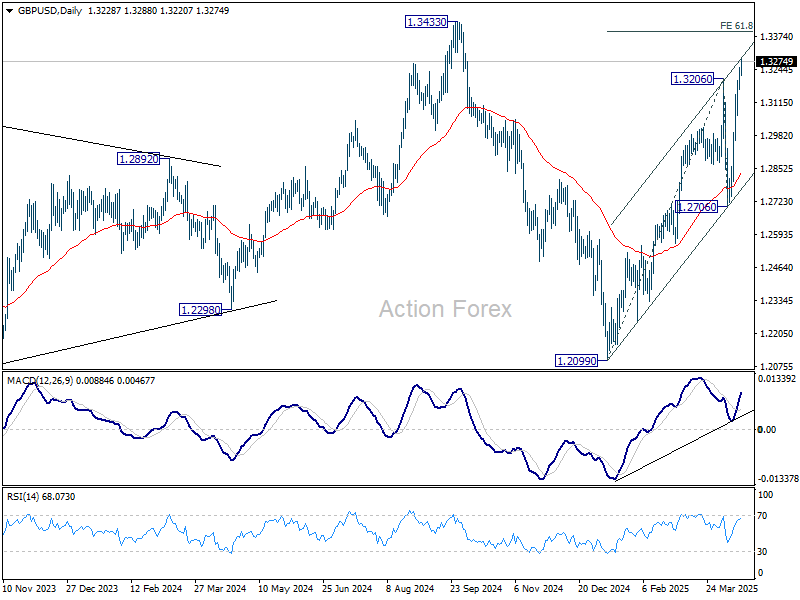

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3180; (P) 1.3216; (R1) 1.3268; More...

Intraday bias in GBP/USD remains on the upside for the moment. Current rise from 12099 should target 61.8% projection of 1.2099 to 1.3206 from 1.2706 at 1.3390, and possibly further to 1.3433 high. On the downside, below 1.3121 minor support will turn intraday bias neutral first. But overall near term outlook will stay bullish as long as 1.2706 support holds.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

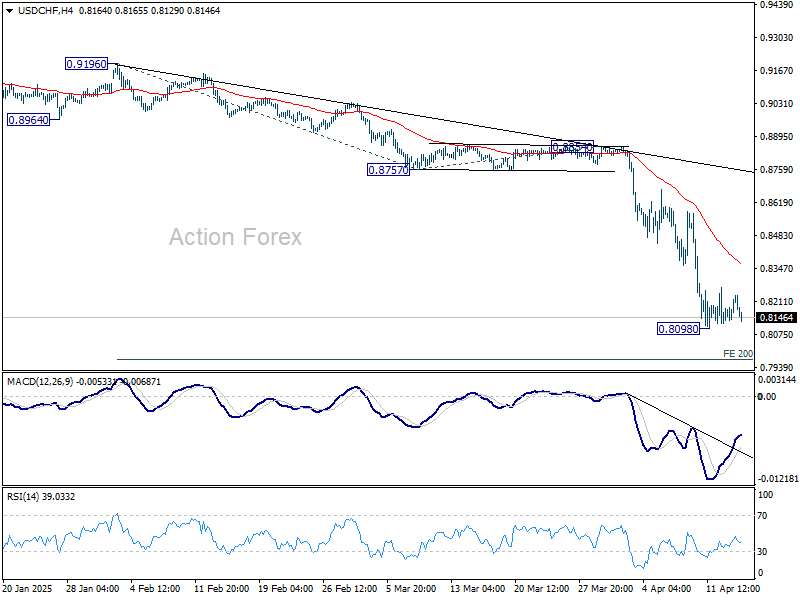

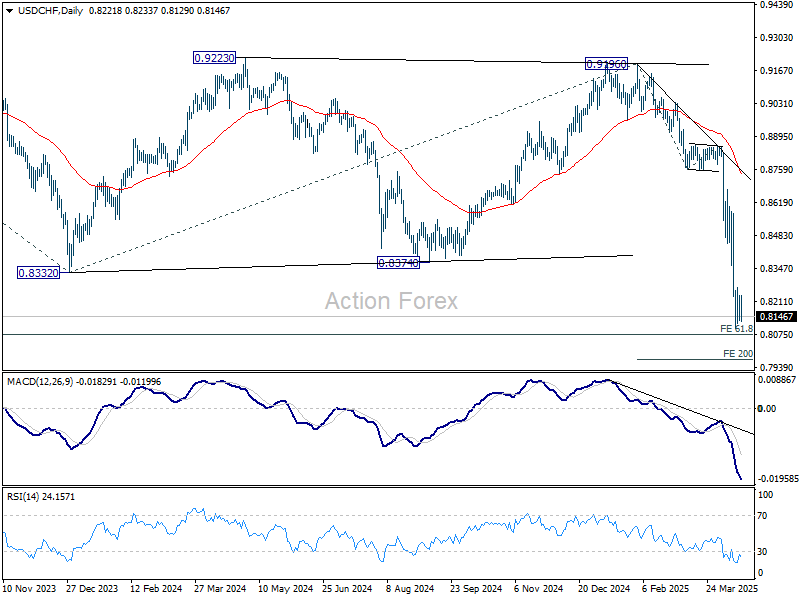

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8163; (P) 0.8201; (R1) 0.8273; More…

Intraday bias in USD/CHF remains neutral for consolidations above 0.8098 temporary low. While stronger rise might be seen, upside should be limited by 55 4H EMA (now at 0.8363) to bring another fall. On the downside, break of 0.8098 will resume recent down trend to 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

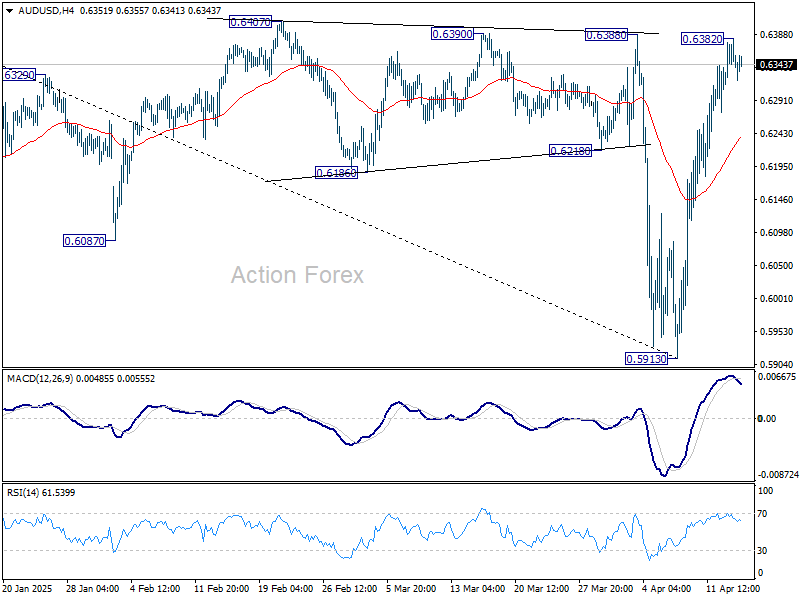

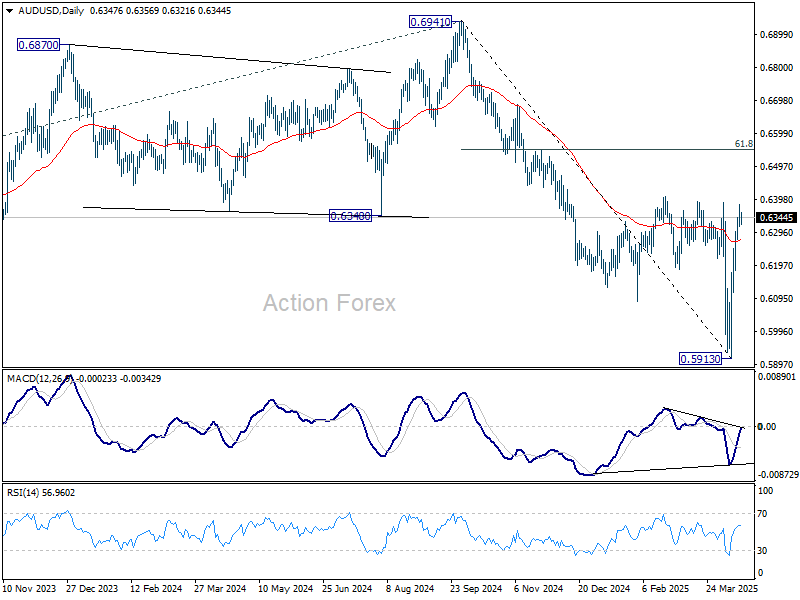

AUD/USD Daily Report

Daily Pivots: (S1) 0.6313; (P) 0.6348; (R1) 0.6380; More...

Intraday bias in AUD/USD is turned neutral first with current retreat. Further rally is expected as long as 55 4H EMA (now at 0.6239) holds. Firm break of 0.6407 resistance will extend the rise from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548, even still as a corrective move.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6441) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

UK CPI falls to 2.6%, both goods and services inflation ease

UK consumer inflation continued to ease in March, with headline CPI slowing to 2.6% yoy, slightly below the expected 2.7% and down from 2.8% yoy in February. On a monthly basis, prices rose 0.3%, also under consensus 0.4% mom forecast.

The decline was broad-based, with annual goods inflation falling to 0.6% yoy from 0.8% yoy and services inflation easing to 4.7% yoy from 5.0% yoy.

Core CPI (excluding energy, food, alcohol and tobacco) edged down to 3.4% as expected, from 3.5% previously.

Spreading Beyond Tariffs

Although sentiment across the European assets was strong yesterday – on the tariff relief, remember? – things started looking less optimistic toward the end of the session and the futures are in the negative this morning on the back of a few not-so-optimistic news on the trade front.

First, the US and the EU made little progress in trade negotiations; for now, the 20% tariffs remain for both sides. Then, China is not only NOT calling Trump to talk about tariffs but they also announced that they will not buy Boeing planes - we are talking about 29 planes that China decides not to buy in 2025. And, finally, Trump administration decided to restrict the export of Nvidia’s H20 chips to China. Note that these chips are specifically designed for China – they are good for inference but not as powerful as the premium chips for AI training. Concretely, Nvidia warned that it will report $5.5 in writedowns during this quarter and Bloomberg Intelligence estimates that the total revenue miss for the company could be between $14 and 18bn for the year. Consequently, Nvidia lost more than 6% in the afterhours trading, and Nasdaq futures are looking worse than the others. ASML is set to report weaker orders in the Q1 due to tariff uncertainty and TSM is expected to announce around 56% profit growth in Q1 thanks to a 42% increase in sales but forecasts will probably matter more than the actual numbers this earnings season because of tariff uncertainties.

Tariff uncertainties on earnings

There are three major challenges with the tariff situation.

1. We don’t know the size of the tariffs, we don’t know how long they stay, will they be increased, decreased, rolled back.

2. The potential strength of the Q1 earnings is partly due to frontloading in demand before the tariffs hit, and could be followed by a quarter – or two – of below-trend growth as companies delay their capex and AI investment plans due to uncertainties.

3. The trade escalation between the US and China continues at full speed, and is spreading into other measures. In this context, the US just requested Nvidia to stop selling its chips designed for China to the Chinese, and in response the China could well restrict its exports of rare earth metals and other commodities essential to building chips and machines to the US.

In summary, risks prevail. Note that the latest GDP data released in China this morning topped analyst estimates showing that the country grew 5.4% yoy in Q1, retail sales jumped nearly 6% compared to 4.2% expected by analysts and the new home prices dropped the least in 9 months. The stronger the Chinese data, the less likely it is to bend to US demands. iShares MSCI China ETF was down yesterday after a more than 10% rebound since April 8th. The companies included in this ETF have less than 3% revenue exposure to the US, meaning that the impact of the trade war and cancelled US orders will remain limited, while these companies will benefit from the Chinese stimulus measures and the weaker yuan.

Death cross formation for S&P500 and Nasdaq

The S&P500’s daily chart is now flashing red with a death cross formation – where the 50-DMA crossed below the 200-DMA. While some traders see the death cross formation as a lagging indicator, the last time we saw a golden cross formation – the opposite of death cross formation – in the beginning of 2023, the S&P500 rallied up to 48% in months that followed the golden cross formation. Of course, technicals don’t guarantee a future price action, but the 50-DMA is below the 200-DMA for the S&P500, for the Nasdaq 100, and soon for the Dow Jones.

Gold and FX

Unsurprisingly, the escalating trade tensions continue to boost appetite in gold. The price of an ounce just hit a fresh record this morning at $3283 per ounce. The US dollar remains under the pressure of the trade war that starts having concrete consequences for the US companies and fuels the recession fears in the US. Good news – if you are looking for good news – is that the selloff across the US treasuries is more contained now than it was a week ago, and that’s important to judge how severe the risks of a financial crisis is. For now, bond holders are holding tight.

In the FX, the decline in US dollar appetite continues to push the major currencies higher. The EURUSD was bid below the 1.13 yesterday, as Cable extended gains to 1.3266 despite a decent fall in UK payroll numbers in March due to the scheduled rise of employment costs this month. Wages were slightly below expectations but the fact that spending increased in March despite the rise in bills was seen as encouraging news. Inflation and growth uncertainties prevail due to the tariff uncertainties. But if inflation remains under control, the Benk of England (BoE) could support the economy through turbulence. If inflation rises however, the BoE support will be limited and the latter could weigh on UK growth expectations and sterling. Cable, of course, looks strong due to a sharper downside revision of US growth expectations, but the recent rally of the EURGBP warns that appetite in sterling is not as strong against the euro.

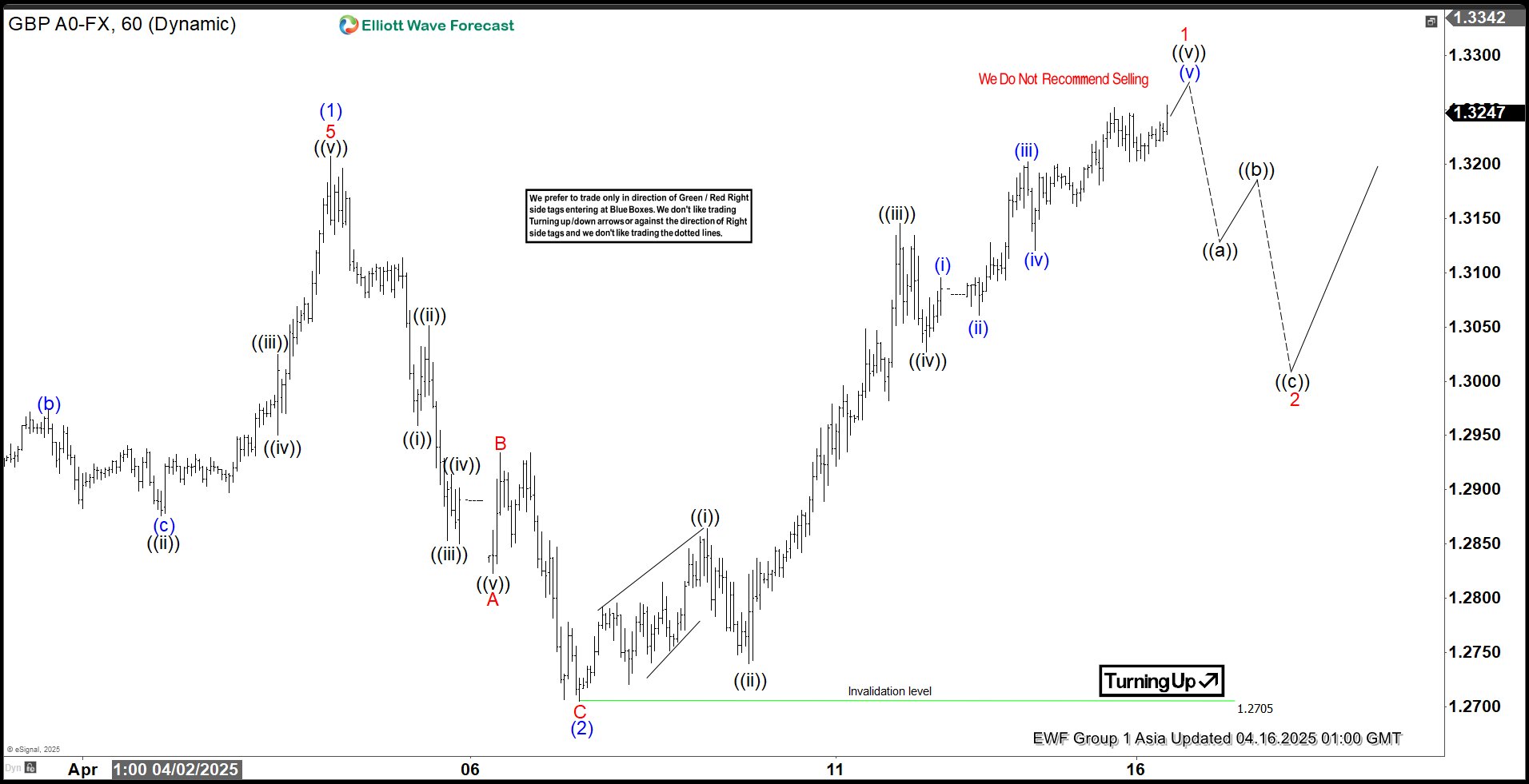

Elliott Wave Outlook Confirms That GBPUSD Has Resumed Its Upward Move

GBPUSD has recently broken above its April 3, 2025 peak of 1.3207, which we identified as wave (1) in the chart. This breakout signals a bullish trend starting from the January 13, 2025 low of 1.2705, suggesting more upward movement ahead. The rally from this low follows a five-wave Elliott Wave pattern. This is a common structure in technical analysis indicating a strong trend.

Starting from the January 13 low, the first wave or wave (1) reached 1.3207.,A pullback in wave (2) then followed which ended at 1.2705. This pullback formed a zigzag pattern. Wave A dropped to 1.2823, wave B rose to 1.2934, and wave C fell to 1.2705, completing wave (2).

The pair has now moved higher into wave (3). From the wave (2) low, the first sub-wave (wave ((i))) peaked at 1.2864, followed by a dip in wave ((ii)) to 1.274. The third sub-wave (wave ((iii))) climbed to 1.314, and the fourth (wave ((iv))) dipped to 1.3027. The fifth sub-wave (wave ((v))) is expected to finish soon, completing wave 1 of a larger pattern.

After this, the pair is likely to pull back in wave 2, correcting the upward move from the April 8, 2025 low. This correction could unfold in 3, 7, or 11 smaller swings before the pair resumes its upward trend. In the short term, as long as the 1.27 low holds, any dips should attract buyers in 3, 7, or 11 swings, supporting further gains.

GBPUSD 60 Minute Elliott Wave Chart

GBPUSD Video

https://www.youtube.com/watch?v=ghD1ZV5_E5A