Sample Category Title

ECB press conference live stream, ready to start

ECB press conference live stream, ready to start. Introductory statement below.

https://www.youtube.com/watch?v=qCY48Os7WEg

INTRODUCTORY STATEMENT

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, we will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of September 2018. We anticipate that, after September 2018, subject to incoming data confirming our medium-term inflation outlook, we will reduce the monthly pace of the net asset purchases to €15 billion until the end of December 2018 and then end net purchases. We intend to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of our net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

While uncertainties, notably related to the global trade environment, remain prominent, the information available since our last monetary policy meeting indicates that the euro area economy is proceeding along a solid and broad-based growth path. The underlying strength of the economy confirms our confidence that the sustained convergence of inflation to our aim will continue in the period ahead and will be maintained even after a gradual winding-down of our net asset purchases. Nevertheless, significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. This support will continue to be provided by the net asset purchases until the end of the year, by the sizeable stock of acquired assets and the associated reinvestments, and by our enhanced forward guidance on the key ECB interest rates. In any event, the Governing Council stands ready to adjust all of its instruments as appropriate to ensure that inflation continues to move towards the Governing Council's inflation aim in a sustained manner.

Let me now explain our assessment in greater detail, starting with the economic analysis. Quarterly real GDP growth moderated to 0.4% in the first quarter of 2018, following growth of 0.7% in the previous three quarters. This easing reflects a pull-back from the very high levels of growth in 2017 and is related mainly to weaker impetus from previously very strong external trade, compounded by an increase in uncertainty and some temporary and supply-side factors at both the domestic and the global level. The latest economic indicators and survey results have stabilised and continue to point to ongoing solid and broad-based economic growth, in line with the June 2018 Eurosystem staff macroeconomic projections for the euro area. Our monetary policy measures, which have facilitated the deleveraging process, continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by growing household wealth. Business investment is fostered by the favourable financing conditions, rising corporate profitability and solid demand. Housing investment remains robust. In addition, the broad-based expansion in global demand is expected to continue, thus providing impetus to euro area exports.

The risks surrounding the euro area growth outlook can still be assessed as broadly balanced. Uncertainties related to global factors, notably the threat of protectionism, remain prominent. Moreover, the risk of persistent heightened financial market volatility continues to warrant monitoring.

Euro area annual HICP inflation increased to 2.0% in June 2018, from 1.9% in May, reflecting mainly higher energy and food price inflation. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around the current level for the remainder of the year. While measures of underlying inflation remain generally muted, they have been increasing from earlier lows. Domestic cost pressures are strengthening and broadening amid high levels of capacity utilisation and tightening labour markets. Uncertainty around the inflation outlook is receding. Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

Turning to the monetary analysis, broad money (M3) growth increased to 4.4% in June 2018, up from 4.0% in May. M3 growth continues to benefit from the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid deposits. The narrow monetary aggregate M1 remained the main contributor to broad money growth.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations rose to 4.1% in June 2018, after 3.7% in the previous month, while the annual growth rate of loans to households remained unchanged at 2.9%. The euro area bank lending survey for the second quarter of 2018 indicates that loan growth continues to be supported by easing credit standards and increasing demand across all loan categories.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing – in particular for small and medium-sized enterprises – and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed that an ample degree of monetary accommodation is still necessary for the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute more decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, the ongoing broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

We are now at your disposal for questions.

Chinese Xi urged to safeguard the rule-based multilateral trading regime

Chinese President Xi Jinping called for joint effort in fighting protectionism at a BRICS summit in South Africa today. He told BRICS leaders that "we must work together ... to safeguard the rule-based multilateral trading regime; promote trade and investment, globalization and facilitation; and reject protectionism outright."

But Xi should be reminded that EU and US have agreed on a joint position. That is, both EU and US agreed to join forces against "unfair global trade practices". And specifically, they the practices include "intellectual property theft, forced technology transfer, industrial subsidies, distortions created by state owned enterprises, and overcapacity." They clearly target China and it's time for Xi to step up reforms.

Into US session: Euro loses some ground, ECB press conference awaited

Entering into US session, Euro trades mildly softer after ECB left interest rates unchanged as widely expected. Main refinancing rate is held at 0.00%, marginal lending facility rate at 0.25%, deposit facility rate at -0.40%. Yen remains the strongest one as supported by strength in JGB yields. 10 year JGB yield hit as high as 0.099 before closing at 0.09. Australian Dollar and New Zealand reversed earlier gain and turn broadly lower. On the other hand, Dollar is regaining some ground for today.

But for the week, Canadian Dollar remains the strongest one, followed by Yen. Euro and Dollar are taking turn to be the weakest. ECB President Mario Draghi holds the key to unlock a direction in EUR/USD. But he's likely hold it to his chest in today's press conference.

In other markets, stocks are mixed. Germany responds very well to the EU Juncker's assessment and Trump's concessions. At the timing of writing, DAX is up 1.38%, CAC is up 0.35%. FTSE, on the other hand, is flat. Risk aversion was dominant in Asia though. China Shanghai SSE closed down -0.74%, Hong Kong HSI down -0.48%. Nikkei also lost -0.12%.

The offshore Chinese yuan continues to stabilize against dollar today. USD/CNH once dipped to as low as 6.733 earlier today but recovered to above 6.78. For now, there is no clear sign of a trend reversal yet. That is Yuan is still technically in a near term down trend. But at least, it's past the climax of selloff. And we'd likely see more consolidation below 6.85.

(ECB) Monetary Policy Decisions

At today's meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, the Governing Council will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of September 2018. The Governing Council anticipates that, after September 2018, subject to incoming data confirming the Governing Council's medium-term inflation outlook, the monthly pace of the net asset purchases will be reduced to €15 billion until the end of December 2018 and that net purchases will then end. The Governing Council intends to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

ECB kept main refinancing rate unchanged at 0.00%, full statement

Monetary policy decisions

At today’s meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, the Governing Council will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of September 2018. The Governing Council anticipates that, after September 2018, subject to incoming data confirming the Governing Council’s medium-term inflation outlook, the monthly pace of the net asset purchases will be reduced to €15 billion until the end of December 2018 and that net purchases will then end. The Governing Council intends to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

More responses on EU-US trade negotiations

Finance Minister Bruno Le Maire urged that "each side, the Europeans and the Americans, must find something in these discussions", and, "any trade deal must be based on reciprocity". He also emphasized that agriculture must be excluded from the trade negotiations. To him, Europe could not ease its food safety and environmental norms. Also, he seems to prefer more focus in the negotiation and said "we don't want to enter into a negotiation a wide-ranging deal."

German Foreign Minister Heiko Maas welcomed the results even though "this is not yet the result we are aiming for". He acknowledged that "it has made a positive result in the whole discussion...on free trade or protectionism more likely than before." Economy Minister Peter Altmaier also expressed his optimism that " we can get a good result in the coming weeks and months."

Department for International Trade said in statement that "we welcome the agreement by the U.S. and the EU to work together to reduce barriers to trade and to further increase trade and investment." And, "we look forward to progress towards the removal of steel and aluminum tariffs and de-escalation of the tit-for-tat action that could harm businesses and jobs on both sides of the Atlantic."

DAX Jumps On Trump-Juckner Agreement

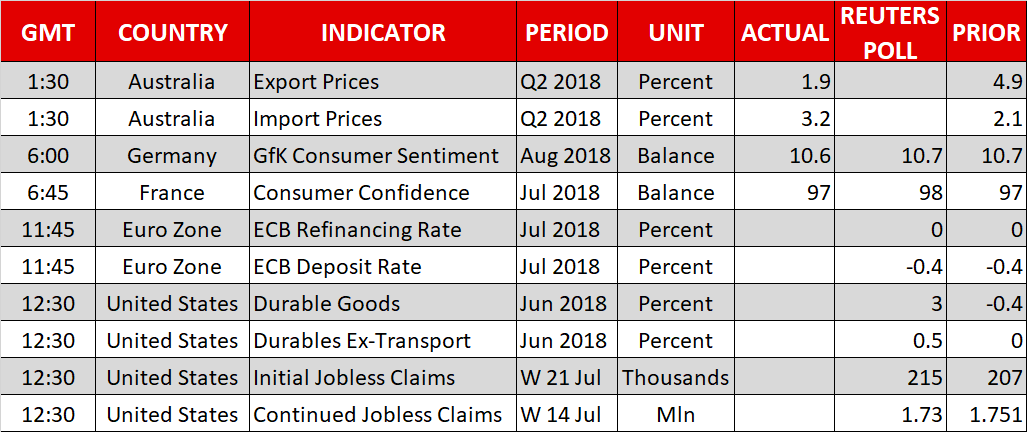

The DAX index has posted strong gains in the Thursday session. Currently, the DAX is at 12,722, up 1.12% on the day. On the release front, German GfK Consumer Climate edged lower to 10.6, just shy of the estimate of 10.7 points. Later in the day, the ECB sets its minimum bid rate, followed by a rate conference with ECB President Mario Draghi.

Trade tensions between the U.S and the European Union have cast a pall over relations between the sides, so the success of EU Commission President Jean-Claude Juckner’s visit to the White House was welcome news. The parties announced on Wednesday that they had agreed to hold off on any further tariffs while talks are ongoing. This is a major concession from Trump, who had threatened to impose tariffs on European car imports. U.S tariffs on European aluminum and steel will remain in place, but Juckner pointed out that the U.S has agreed to reassess these measures. The news boosted the DAX index, as automaker shares have jumped. BMW has climbed 3.20%, Daimler is up 2.80% and Volkswagen has risen 3.53%. Bank shares are also higher, with Commerzbank up 1.46% and Deutsche Bank up 1.73%.

The markets are not expecting anything dramatic from ECB policymakers, with interest rates expected to remain at 0.00%. In June, the ECB decided to end its massive bond-purchase scheme by the end of the year, which has amounted to some 2.6 trillion euros. However, the ECB is playing it very cautious regarding any interest rate hikes, with the ECB saying it would maintain record-low rates “through the summer” of 2019. Trade tensions between the EU and U.S have dampened growth forecasts for the eurozone, although the Juckner-Trump meeting has considerably improved market sentiment. The ECB could tweak its guidance but is unlikely to make any changes to current monetary policy.

ECB Meeting Front And Center, Yen Bulls Return

Here are the latest developments in global markets:

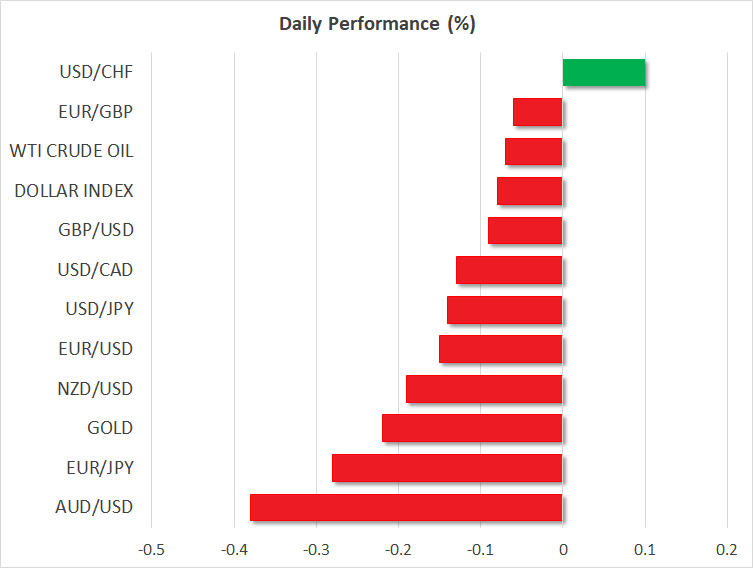

FOREX: The dollar index was down by 0.08% on Thursday, extending the losses it posted in the previous session following the meeting between European Commission President Jean-Claude Juncker and US President Donald Trump. The two agreed to lower industrial tariffs and increase US natural gas and soybean exports to Europe. Also, they decided to harmonize regulatory standards to allow for medical devices to have better access in Europe. Dollar/yen is one of the weakest pairs for the week so far. It fell by 0.14% today and is set to post the seventh red day in a row, as speculation that the BoJ may appear hawkish next week continues to dominate. Euro traders will now turn their focus to Mario Draghi’s press conference today as no change to policy is expected later in the day. Euro/dollar moved lower by 0.16%, hovering slightly above the 1.1700 handle. Moreover, pound/dollar edged slightly lower (-0.08%) amid uncertainties over Brexit, while investors are waiting for the BoE interest rate decision next week. In the antipodean sphere, aussie/dollar and kiwi/dollar are paring some of yesterday’s gains, losing 0.38% and 0.18% respectively. Finally, the Canadian dollar was set to extend the gains it posted in the previous days amid hopes for a NAFTA deal. Dollar/loonie was lower by 0.13% towards 1.3032, creating a 6-week low.

STOCKS: European equities edged mostly higher on Thursday after Trump agreed with Juncker to suspend new tariffs and continue to negotiate over trade. The benchmark European STOXX 600 was up by 0.52% at 1000 GMT, led by industrials. It reached its highest level in six weeks. Meanwhile, the blue-chip Euro STOXX 50 increased by 0.75%. The Italian FTSE MIB jumped by 0.10%, the French CAC 40 rose by 0.74% and the German DAX 30 moved considerably higher by 1.31%. However, the British FTSE 100 traded lower by 0.03%. The Dow Jones and S&P 500 are poised to open higher, while the Nasdaq 100 is expected to open lower today according to US stock futures.

COMMODITIES: Oil prices were mixed today as West Texas Intermediate (WTI) crude dropped by 0.07% to $69.25 per barrel. However, Brent prices rose by 0.65% to $74.41 per barrel, hitting a 10-day high after Saudi Arabia postponed its oil shipment through a Red Sea strait. As for gold, the yellow metal moved sideways in the previous days and on Thursday, it slipped by 0.23% to $1,228 per ounce.

Day ahead: ECB takes center stage, all eyes on Draghi’s Q&A

The main event will undoubtedly be the ECB policy decision at 1145 GMT, and the subsequent press conference by President Draghi at 1230 GMT. With the Bank having outlined its plans for ending QE at the June meeting, markets have started to focus on the timing of a potential rate increase. Back then, policymakers said rates would stay at present levels “through the summer of 2019”, which is a rather vague guidance that keeps open both the prospect of a hike as early as July next year, or as late as October. Market pricing is currently leaning towards the latter, with a 10bps hike being fully factored in for October 2019, according to EONIA swaps.

Hence, any optimistic remarks from Draghi that suggest a hike may come before October are likely to benefit the euro. Conversely, anything that pushes the anticipated timing of the first hike further into the future, could weigh on the currency. To be fair, one should not expect any clear comments from Draghi on this – after all, the phrasing was probably kept vague on purpose to allow the Bank some flexibility. Still, his overall tone, as well as any other comments – on trade for instance – could give investors a sense of direction on the matter. On balance, the prospect for a positive euro reaction appears slightly more likely, considering that the market is already quite pessimistic on the timing of a rate increase, and also that trade risks may have subsided a little following the constructive meeting between Juncker and Trump.

On the data front, the only noteworthy release still to come are US durable goods orders for June, slated for 1230 GMT. Forecasts are pointing to a strong rebound in the headline print, which is expected to rise by 3.0% in monthly terms, following a 0.4% decline in May. Most of the improvement appears to have come from volatile items though, as the core print that excludes transportation equipment is only expected to rise by 0.5%, after posting no growth previously. Weekly data on initial and continued jobless claims are also due out of the US at the same time.

In equities, the earnings season continues with some of the biggest firms reporting their results today being Amazon, Comcast, Intel, McDonald’s, Starbucks, Under Armour and Xerox.

As for the speakers, Mexican Economy Minister Guajardo is due to visit Washington to meet with US Trade Representative Lighthizer to discuss NAFTA. There are some hopes that a deal can be reached in the next months ahead of the US midterm elections, so any optimistic comments on the matter could benefit the loonie. The opposite holds true as well.

EUR/USD – Euro Down Slightly Ahead Of ECB Announcement

EUR/USD is slightly lower in the Thursday session. Currently, the pair is trading at 1.1712, down 0.13% on the day. On the release front, German GfK Consumer Climate edged lower to 10.6, just shy of estimate of 10.7 points. Later in the day, the ECB sets its minimum bid rate. The U.S will release durable goods reports and unemployment claims.

After weeks of a bruising trade war, the EU and U.S have agreed to take steps to reduce tensions. On Wednesday, EU Commission President Jean-Claude Juckner met with President Trump, and the talks appear to have been more successful than expected. The parties agreed to hold off on any further tariffs while talks are ongoing. This is a major concession from Trump, who had threatened to impose tariffs on European car imports. U.S tariffs on European aluminum and steel will remain in place, but Juckner pointed out that the U.S has agreed to reassess these measures. The surprise agreement eases fears of a full-blown transatlantic trade war. Will the goodwill displayed by Trump extend into some kind of agreement with China as well?

All eyes are on the ECB, which will set interest rates later on Thursday. The markets are not expecting anything dramatic from policymakers, with rates expected to remain at 0.00%. In June, the ECB decided to end its massive bond-purchase scheme by the end of the year, which has amounted to some 2.6 trillion euros. However, the ECB is playing it very cautious regarding any interest rate hikes, with the ECB saying it would maintain record-low rates “through the summer” of 2019. Trade tensions between the EU and U.S have dampened growth forecasts for the eurozone, although the Juckner-Trump meeting has considerably improved market sentiment. The ECB could tweak its guidance, but is unlikely to make any changes to current monetary policy.

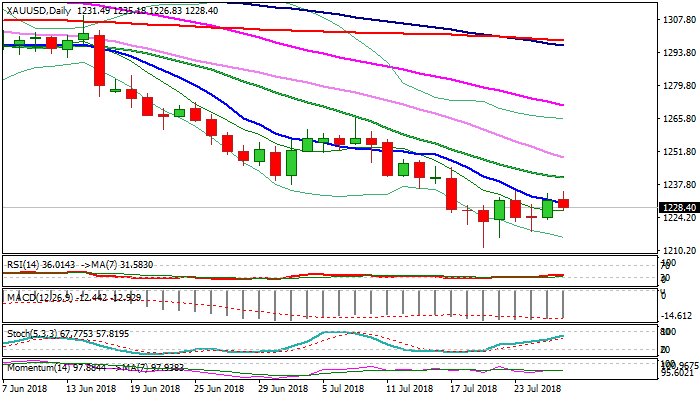

XAUUSD Outlook: Gold Price Moves Lower As Trade Tensions Ease

Spot Gold price eased from recovery high at $1235 on Thursday, failing to extend strong advance of previous day, as positive tone from US/EU trade talks lowered tensions about trade war. Gold dipped despite weaker dollar as safe-haven demand eased on constructive trade talks.

The price returned below falling 10SMA, which was repeatedly attacked but without clear break, generating initial negative signal that will be confirmed on daily close below 10SMA.

Weak momentum studies and falling daily MA’s in full bearish configuration maintain pressure, with close below Wednesday’s low at $1223 to signal double-top ($1235) and open way for further easing. Close below $1218 (Tuesday’s spike low) would confirm reversal and risk return towards $1211 (19 July low).

On the other side, bullish scenario requires close above 10SMA to keep bullish near-term bias for recovery extension towards falling 20SMA ($1240).

Res: 1235, 1238, 1240, 1249

Sup: 1226, 1223, 1218, 1215