Sample Category Title

Global Core Bond Trading Developed In Tight Ranges For Most Of The Day

Markets

Yesterday, global core bond trading developed in tight ranges for most of the day as investors awaited the outcome of the meeting between US President Trump & EU's Juncker. A 5-year US Treasury auction attracted strong investor interest. However, yields jumped higher later as the EU and the US agreed to start negotiations to reduce tariff and non-tariff trade barriers between the two economies. At the end of the day, US yields rose between 3.6bp (2-y) and 2.6 bp (10-y). Changes on the German yield curve were limited as trading finished before the EU-US trade agreement. Today, the US eco calendar contains jobless claims, inventory data and the durable goods orders. The US Treasury will sell $30bln of 7-year Notes. In Europe, the focus will be on the press conference after the ECB policy meeting. We expect President Draghi to maintain the guidance that the bank gave on interest rates at the June meeting. He probably won't be more specific on the ‘through the Summer' wording. This morning, Bunds will probably open lower, joining the late session setback in the US yesterday evening. For now, the rise in US yields has stalled. Sentiment on risk became more cautious as poor results from Facebook after the close yesterday are weighing on Tech stocks. Even so, we expect US bond markets to focus on the data ahead of tomorrow's US Q2 GDP data. Today's US data probably won't question expectations for a strong Q2 growth figure. So, we see bond yields holding this week's rise. A strong US growth figure might help US 10-y yields to return to the 3% mark. We also don't expect Draghi's comments to provide additional support for Bunds.

Yesterday, the major USD cross rates traded in wait-and-see modus ahead of the outcome of the Trump-Juncker meeting. EUR/USD reversed a modest intraday loss as an escalation in the trade war was avoided. However, a break beyond first intermediate resistance at 1.1750/90 was blocked. USD/JPY hardly profited from higher US yields and a constructive risk sentiment. Yen strength prevailed ahead of next week's BOJ meeting. The positive turn in the US-EU trade talks might be slightly euro supportive this morning. However, assuming that Draghi will confirm the ECB's ‘lower for longer stance' on policy rates and with markets preparing for strong US Q2 growth tomorrow, we expect the EUR/USD 1.1850 range top to hold. The picture of USD/JPY looks fragile. A mixed risk sentiment and ongoing speculation on next week's BOJ policy meeting will probably protect the downside for the yen.

Yesterday, EUR/GBP mostly hovered in a very tight range, mostly slightly below 0.89. CBI retail data were OK but failed to inspire further sterling gains. Today, UK eco calendar is empty. More technical trading might be on the cards for sterling. We consider the reaction of sterling to May's political move earlier this week as slightly disappointing from a sterling point of view.

News Headlines

Trump and Juncker have ceased fire in the US-EU trade war. They will start negotiations to reduce transatlantic tariffs and other trade barriers related to all industrial goods, other than cars. The EU, in return, committed to start buying more soybeans and liquefied natural gas. Tariffs on steel- and aluminum, however, stay in place.

Two Saudi Arabia large crude carrier ships were attacked by Yemen's Iran-aligned Houthi movement. Saudi Arabia's energy minister Khalid al-Falih said in a statement that the country is temporarily suspending all oil shipments through that strategic shipping lane in the Red Sea. Oil prices climbed for a third day in a row.

Canadian and Mexican officials met yesterday to discuss further negotiations on NAFTA. Both countries were optimistic on a positive outcome and expressed that a trilateral agreement remains the priority, despite that US Agriculture Secretary Perdue raised the prospect that NAFTA could be negotiated separately.

Elliott Wave Analysis: DAX Ready For Rally Higher?

DAX short-term Elliott wave analysis suggests that the pullback to 6.28.2018 low ended intermediate wave (2) at 12088.56. Up from there, the rally higher to 12769.8 higher ended Minor wave 1. The internals of that rally higher took place as impulse structure with internal sub-division of 5 wave structure in Minute wave ((i)), ((iii)) & ((v)). On the other hand, Minute wave ((ii)) & ((iv)) took place in 3 waves corrective structure.

Above from 6.28 low cycle, the rally higher to 12369.5 high ended Minute wave ((i)). Down from there, the pullback to 12115 low ended Minute wave ((ii)). The rally higher from there took place in 5 waves structure & ended the Minute wave ((iii)) at 12630 high. Below from there, the pullback to 12513.5 ended Minute wave ((iv)) as a contracting triangle. The final rally higher from there ended Minute wave ((v)) of 1 at 12769.5 peak. Down from there, the correction against 6.28.2018 low cycle completed Minor wave 2 at 12454.5 low after reaching the blue box area at 12540.50-12446.86 100%-161.8% Fibonacci extension area. Near-term, while dips remain above 12454.5 low and more importantly above 12088.56 low, expect the Index to resume the upside in Minor wave 3 higher. We don’t like selling it.

DAX 1 Hour Elliott Wave Chart

Fundamental Analysis in Forex Trading

In terms of Forex trading, Fundamental analysis aims at analyzing group of countries’ economic data and performance in order to compare them. The use and study of this data helps traders forecast future price movements of currencies. Fundamental analysis tends to focus on how macroeconomic elements affect the exchange rate.

Forex fundamentals

When one country or group of countries (in case they share a common currency) has much more solid economic data and performance compared to another, then an increase in value of the stronger one is expected; When one country or economic block has weaker economic data and performance compared to another, then an increase in value of the stronger one is expected.

Such expectations are based on the behavior of central banks that could change interest rates depending on the performance of the economy. Central banks will increase the interest rates if the economy is improving as to avoid higher levels of inflation. At the same time, it will increase the interest rates if the economy is in recession or stagnating as to spur economic growth. Subscribe JustForex free analytics to stay informed.

There is another one, higher interest rates traditionally increase demand for a currency. The reason is simple: buyers are better rewarded for owning a currency if the interest rate is higher. A trader or investor is always buying one currency and selling a second. A change of an interest rate alters this relationship and the price will reflect this change. Most often the currency which increases its rates will see an increase in its price.

Measuring indicators

Investors and traders monitor news releases, economic data, press conferences, policy statements and speeches to assess the overall economic situation of each country. As mentioned earlier, the central banks are actually responsible for making the decision how the interest rate will be changed. What economic measuring points should be considered:

- Gross Domestic Product (GDP);

- Employment;

- Trade balance;

- Consumer Price Index (CPI);

- Retails sales;

- Interest rates;

- Monetary policy;

- Manufacturing;

- Housing;

- Purchasing Managers’ Index (PMI).

All this data could be used as clues and signals for potential decisions of the central banks.

Understand the direction of the interest rates

In essence, the balance between GDP and the monetary base could be seen as key. Basically, this equation shows “available” money in an economic zone versus the current economic activity.

- If the monetary base increases more than the GDP, each unit of currency is worthless and this will have a negative impact on the exchange rate of that currency;

- If the monetary base decreases more than the GDP, each unit of currency is worth more and this will have a positive impact on the exchange rate of that currency;

- If the GDP increases more than the monetary base, each unit of currency is worth more and this will have a positive impact on the exchange rate of that currency;

- If the GDP decreases more than the monetary base, each unit of currency is worthless and this will have a negative impact on the exchange rate of that currency.

Forex traders can use fundamental analysis to make decisions on a long-term basis, because the fundamentals do not change that rapidly from day to day. Many of them combine fundamental with technical analysis in order to execute trades with precise time i.e. to know entry, take profit & determine stop loss level. High impact data releases, news events, press conferences and speeches have the potential of moving price for duration of time with a lot of volatility.

Practice Forex trading on JustForex Demo account with virtual money having real trading conditions. Once you complete a few trading sessions on the forex trading practice account, you feel confident about it.

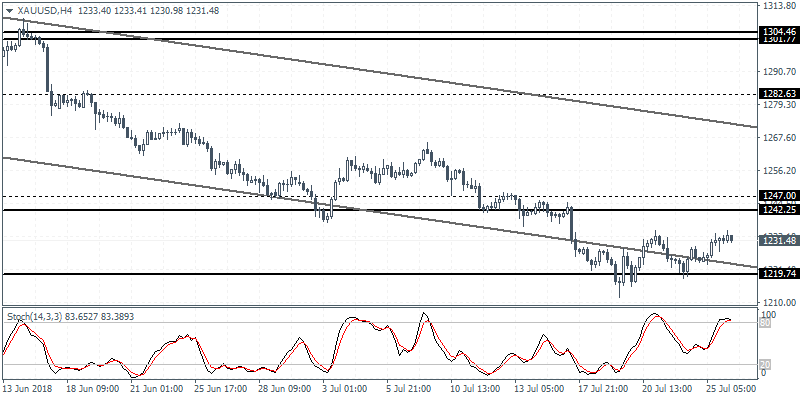

XAUUSD Intraday Analysis

XAUUSD (1231.48): Gold prices were seen moving higher but overall price action remains subdued. The precious metal is expected to maintain the range within 1242 resistance and 1219 support. Further gains or declines are likely to be maintained on a breakout off this range. The bias remains to the upside if price action can break past the resistance level of 1247 - 1242 region. To the downside, a close below 1219 could see further declines pushing the precious metal down to 1200 level of support.

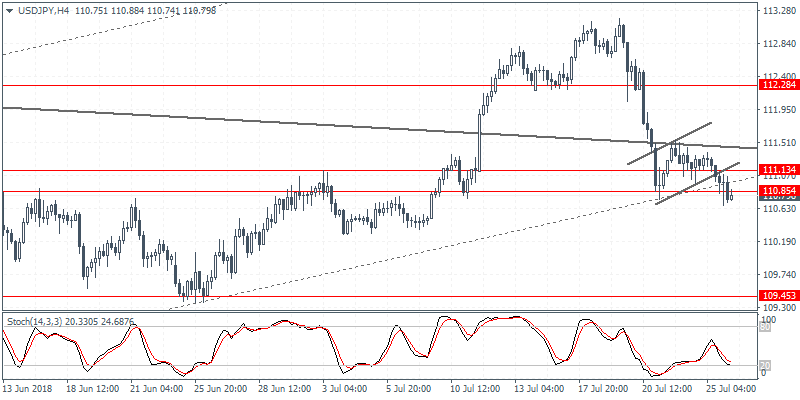

USDJPY Intraday Analysis

USDJPY (110.79): The USDJPY currency pair was seen closing lower on Wednesday. Price action broke past the minor bearish flag pattern clearing the support level at 111.13 - 110.85. Further declines could be triggered on the downside momentum. The lower support at 109.45 forms the next main target. However, in the event of a rebound to the upside, USDJPY will need to reclaim the level above 111.13. This will keep the currency pair trading back within the range of 112.28 level of resistance.

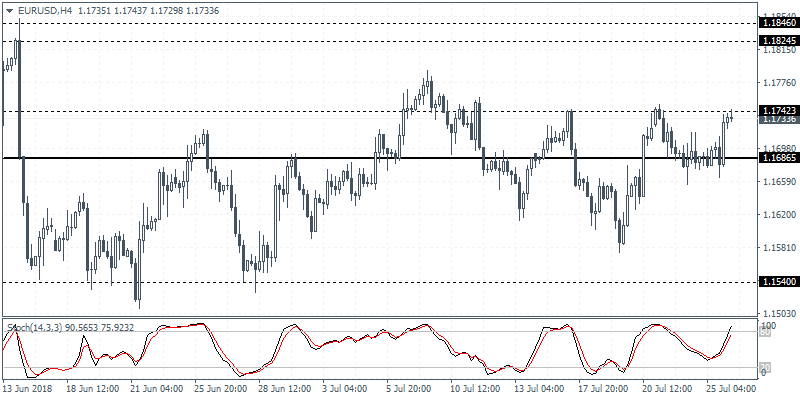

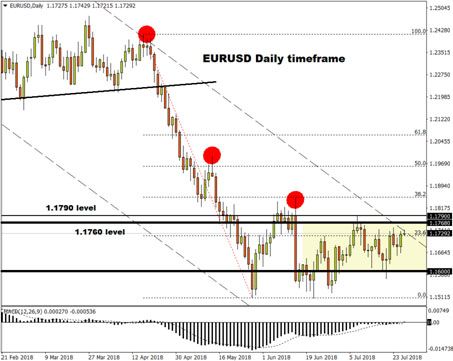

EURUSD Intraday Analysis

EURUSD (1.1733): The EURUSD closed with modest gains by Wednesday's close as price action closed back near the daily resistance level of 1.1730. With price still at the resistance, a breakout off this level is required to maintain the upside. The daily chart is showing the consolidation shaping into a triangle pattern. On the 4-hour chart price action is forming an inverse head and shoulders pattern with a minor neckline forming at 1.1742. A breakout above this level is required to push the currency pair toward the 1.1846 - 1.1824 level of resistance in the near term. Alternately, failure to break past the neckline resistance could push the currency pair back to 1.1688.

ECB Meeting In Focus

The euro currency posted gains toward the close of business on Wednesday. The gains came after the U.S. and the Eurozone reached an agreement on industrial tariffs. The agreement came as the U.S. President Trump met with Juncker from the EU.

Economic data on the day saw the U.S. new home sales rising 631k on the month. This was lower than the forecasts.

The ECB’s monetary policy meeting will remain the key event for the day amid lack of any other fundamentals. No changes are expected from the central bank at this week’s meeting. Still, investors will be sifting through the data for clues on the forward guidance.

The ECB President, Mario Draghi is expected to maintain the status quo. Today’s meeting comes just after the ECB announced its QE tapering plans at the last month’s monetary policy meeting. The recent downtick in core inflation is expected to keep policymakers taking a cautious approach.

Elsewhere, the U.S. durable goods report will be coming out. The median forecasts point to a 0.5% increase on the core durable goods orders while headline durable goods are expected to rise 3.0% on the month.

Euro Steady Ahead Of ECB Meeting, Dollar Sags

Market sentiment received a solid boost after US President Donald Trump obtained concessions from the European Union to avert a transatlantic trade war.

The United States and Europe have reached a deal to work towards “zero tariffs, barriers and subsidies on non-auto industrial goods” in a bid to defuse escalating trade tensions. Investors took comfort in the encouraging meeting outcome, with Asian stocks edging higher this morning following overnight gains on Wall Street. While the positivity from Asia could carry over into European markets, caution ahead of the looming ECB policy meeting may restrict the upside momentum.

Will the European Central Bank surprise markets?

Today’s main event risk for the Euro will be the European Central Bank monetary policy decision, which is widely expected to conclude with interest rates left unchanged at 0.00%.

Although July’s meeting will not include fresh economic projections, investors should not be quick to expect the meeting to be a snoozer. Much of the attention will be directed towards Mario Draghi’s press conference for further insight into rate hike timings and thoughts on global trade developments.

With the ECB already unveiling its tapering blueprint and stating that interest rates would remain at ultra-low levels, "at least through the summer of 2019", Draghi may simply reiterate the message of June’s policy meeting. While economic data from Europe remains positive with inflation hitting the golden 2% level, global trade tensions continue to weigh on sentiment.

Will Draghi be able to maintain a positive stance on the Eurozone economy without causing the Euro to appreciate aggressively? Alternatively, the Euro could take a hit if he decides to strike a cautious tone by focusing purely on global trade tensions and reiterate how interest rates will remain unchanged until Summer 2019.

Regarding the technical picture, the EURUSD continues to find comfort within a wide range on the daily charts. However, the breakout above 1.1700 could encourage an incline towards 1.1768 and 1.1790, respectively.

Dollar bulls take a short break

King Dollar tumbled to a two-week low against a basket of major currencies after the US and the European Union agreed on steps to de-escalate trade tensions.

The downside was complimented by disappointing new homes sales data from the United States which encouraged sellers to attack. There is also a suspicion that the Dollar’s depreciation could beattributed to a bout of profit taking ahead of Friday’s highly anticipated US GDP report. While the Dollar could depreciate further in the near term, market speculation of higher US interest rates this year islikely to limit the downside losses. Focusing on the technical picture, the Dollar Index has scope to hit 94.00 in the near term.

Commodity spotlight – WTI Oil

Oil prices edged higher on Thursday morning after the Energy Information Administration reported a large drawdown in US Crude inventories. A softer US Dollar has also complemented the upside with prices trading around $69.30 as of writing. Focusing purely on the technical picture, WTI Crude could appreciate back towards $70.00 if bulls are able to conquer the $69.60 level.

Japan 10-Yr And 40-Yr JGB Yields Rise

General Trend:

- Asian equity markets trade generally lower amid weakness in China

- US earnings in focus: Facebook drops over 20% post earnings, Ford cut FY EPS forecast

- Declines in Facebook weigh on Nasdaq Futures

- Japan Nikkei index underperforms the TOPIX amid speculation related to the BOJ’s ETF buying program

- Large Nikkei component Fast Retailing declines

- Japanese automation company Fanuc declines following earnings

- Eisai weighed down by disappointing Alzheimer’s data

- South Korean chipmaker Hynix rises after its earnings and guidance

- Australian mining updates in focus: Iron ore producer Fortescue declines, while gold miner Newcrest rises following production updates

- Australian media companies Fairfax and Nine Entertainment to merge

- Macquarie Group declines over 2%, issued Q1 guidance and announced CEO succession plan

- South Korea Q2 GDP data meets ests

- Australia Q2 import prices rise at the quickest pace since 2014

- Japan June PPI Services data rises at the fastest pace since 2015

- PBoC skipped its daily open market operation (OMO) for the 5th straight session, cites the need to ensure 'reasonably ample' liquidity

- China’s Tianjin Realty noted high bond redemption pressure

- JGB yields remain elevated ahead of next week’s BoJ policy meeting (July 30-31st)

- The EU and US reached a ‘breakthrough’ on trade, according to Germany’s Econ Min

- The later today ECB meeting in focus

- Japanese companies which may report earnings later today include Tokyo Electron, Omron, Nomura, Nissan Motor, Canon Inc, KAO Corp, Fujitsu and Fuji Electric.

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.4%

- TOPIX Securities index -0.2%; Iron Steel +0.9%, Real Estate +0.8%, Retail trade +0.7%, Marine Transportation +0.7%

- (JP) Japan and the US to hold new trade talks by as soon as Aug - Japanese Press

- (JP) Japan Jun PPI Services y/y: 1.2% v 1.0%e

- (JP) Japan Investors Net Buying of Foreign Bonds: -¥209.2B v -¥8.2B prior; Foreign Buying of Japan Stocks: +¥173.5B v +¥601.9B prior

- (JP) Bank of Japan (BOJ) expected to discuss reducing investment in exchange traded funds that track the Nikkei Stock Average in favor of those that follow broader indexes such as the Topix at next meeting - Nikkei

- (JP) Japan planning to raise FY18 minimum wage benchmark by ~3% (3rd consecutive raise) amid a severe labor shortage - Nikkei

- (JP) Japan MoF sells ¥2.1T v ¥2.1T indicated in 0.10% (prior 0.10%) 2-yr JGBs; avg yield -0.117% v -0.128% prior; bid to cover 4.38x v 4.88x prior

- Nintendo: 7974.JP 2018 shipments of the Switch device seen at 19.8M units; 2019 shipments seen rising to 29.7M units - IHS

Korea

- Kospi opened +0.5%

- (KR) SOUTH KOREA PRELIM Q2 GDP Q/Q: 0.7% V 0.7%E; Y/Y: 2.9% V 2.9%E

- Hynix,[+1%], 000660.KR Reports Q2 (KRW) Net 4.33T v 3.4Te; Op 5.57T v 5.3Te; Rev 10.37T v 10.2Te

- (KR) South Korea Party and government said to reach agreement on increase in the coal tax; also agreed to cut the LNG tax - South Korean Press

China/Hong Kong

- Hang Seng opened +0.6%, Shanghai Composite +0.1%

- Hang Seng Info Tech index -1.8%, Materials -1%, Financials -1%, Consumer Goods -0.9%, Industrial Goods -0.7%, Industrials Goods -0.7%, Property/Construction -0.2%

- (CN) China PBOC said to have eased capital requirements form some banks in order to support lending in an effort to mitigate increasing risks to the economy from the trade war – press

- (CN) China Jun Swift Global Payments (CNY): 1.81% v 1.88% prior

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 5th consecutive session; Net drains CNY70B v drains CNY60B prior

- (CN) China PBOC sets yuan reference rate at 6.7662 v 6.8040 prior

- (CN) China State Planner (NDRC) researcher Guo Liyan: Inflation to moderate in H2, expected to avg 1.8% in 2018; trade frictions will have a relatively small impact - Xinhua

Australia/New Zealand

- ASX 200 opened flat

- ASX 200 Financials index -0.3%; Energy +0.7%, Resources +0.4%

- Fairfax, [+16.6%], FXJ.AU To be acquired by Nine Entertainment in cash and stock transaction, shareholders to receive 0.3627 Nine shares and A$0.025/share in cash

- FMG.AU Reports Q4 total ore shipped 46.5Mt v 44.7Mt y/y; Ore mined 49.8Mt v 53.5 /yy; C1 costs $12.17/WMT v $13.14 q/q

- NCM.AU Reports Q4 gold production 653K oz, +10% q/q; AISC $795/oz v $826 q/q

- (AU) AUSTRALIA Q2 EXPORTS PRICE INDEX Q/Q: +1.9% V -1.3%E; IMPORTS PRICE INDEX Q/Q: 3.2% V 1.9%E

- (AU) According to NAB, there are some bets in the market for the Reserve Bank of Australia (RBA) to not raise rates until early 2020 – US financial press

- (NZ) New Zealand sells NZ$150M v NZ$150M indicated in April 2025 bonds, avg yield 2.4386%, bid to cover 3.42x

- (NZ) New Zealand Fin Min Robertson: Expects growth to pick up in H2, expect investment to hold up despite confidence slump; sees CPI rising to 2% over time

Other Asia

- (PH) Philippines Central Bank (BSP) Chief Espenilla: 'Done' with bank reserve ratio requirement (RRR) cuts, could be resumed in 2019; can deploy arsenal of tools for price stability

- (IN) US said to consider waiver for India regarding 25% steel tariff - Local Press

[Singapore IP ]

North America

- US equity markets ended higher: Dow +0.7%, S&P500 +0.9%, Nasdaq +1.2%, Russell 2000 +0.3%

- S&P500 Industrials +1.5%, Health Care +1.3%, Tech +1.3%

- (VE) Venezuela President Maduro: FX redenomination has been delayed until Aug 20th; the new currency overhaul plan to remove '5 zeros' from the Bolivar currency rather than 3

- (US) President Trump: European Union representatives told me that they would start buying soybeans from our great farmers immediately. Also, they will be buying vast amounts of LNG! - tweet

- (US) DOE CRUDE: -6.2M V -1ME

- FB Reports Q2 $1.74 v $1.75e, Rev $13.2B v $13.4Be; Total revenue growth rate expected to continue to decelerate in H2 2018, down in high single digits during Q3 and Q4 - earnings call comments (-20% after hours)

Europe

- (US) Pres Trump: US and EU will be winners, have agreed to work together toward zero tariffs on non-auto industrial goods - press conf with EU's Juncker

- (UK) Reportedly UK govt is considering a contentious Brexit plan over the Irish border issue - press

Levels as of 01:30ET

- Hang Seng -0.7%; Shanghai Composite -0.7%; Kospi +0.7%; Nikkei225 -0.1%; ASX 200 +0.0%

- Equity Futures: S&P500 -0.2%; Nasdaq100 -0.9%, Dax -0.4%; FTSE100 -0.4%

- EUR 1.1665-1.1744; JPY 110.70-111.05; AUD 0.7433-0.7463;NZD 0.6830-0.6851

- Aug Gold -0.1% at $1,230/oz; Sept Crude Oil +0.0% at $69.33/brl; Sept Copper -0.8% at $2.84/lb

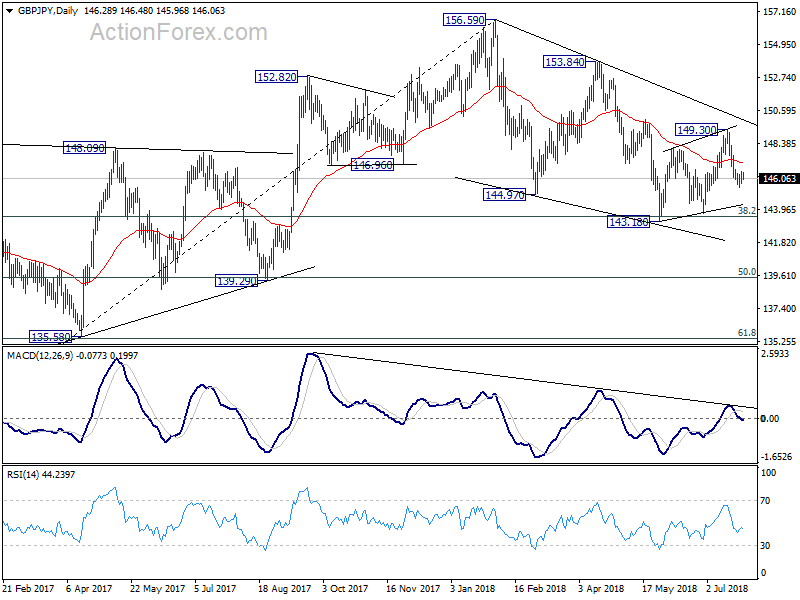

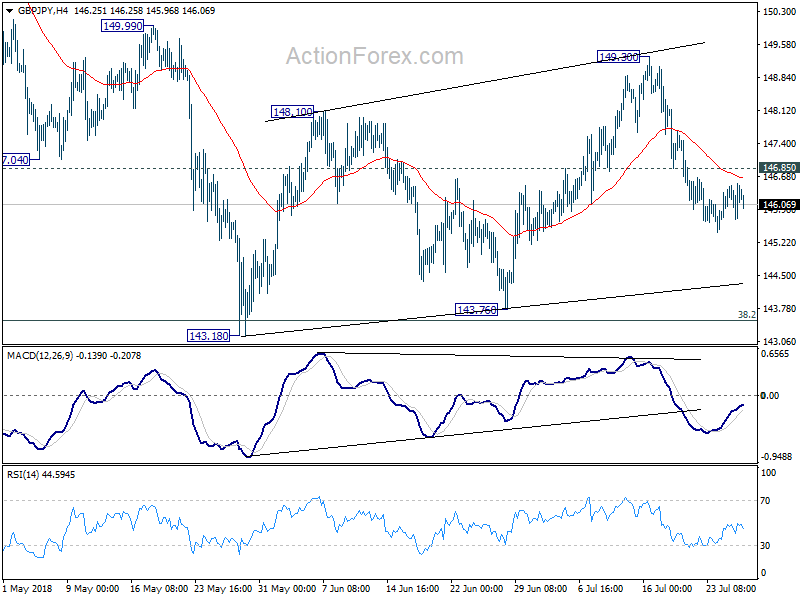

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.92; (P) 146.23; (R1) 146.67; More...

No change in GBP/JPY's outlook. Deeper fall is expected to 143.18/76 support zone. Break will resume larger decline from 156.59. On the upside, though, above 147.65 minor resistance will turn bias back to the upside for 149.30/99 resistance zone instead.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.