Sample Category Title

Facebook Failure Obscured Optimism On US-EU Trade Talks

Yesterday the markets enjoyed a rare portion of good news on international trade. Trump and Juncker agreed not to introduce new tariffs for the period of negotiations. Europe promised to buy more American goods, including liquefied natural gas. In addition, policymakers from Canada and Mexico expressed optimism about negotiations on NAFTA. This positive news contributed to the demand for risky assets on Wednesday. The dollar lost 0.5% to the euro on this news, the American indices came out in positive territory and grew by 0.9% for the day.

However, the markets quickly returned to the state of alertness. For Germany, the important negative is that the issue of import duties for cars from Europe has not yet been lifted. For investors in Russia, it is important that Europe intends to expand the import of LNG from the U.S. and build the capacity for it. The meeting marked the beginning of a 'new phase', but it is not necessarily that the negotiations will be conducted easily and successfully. The examples of the negotiation failures with NAFTA and China earlier this year set on the expectation that there might be months of protracted negotiations.

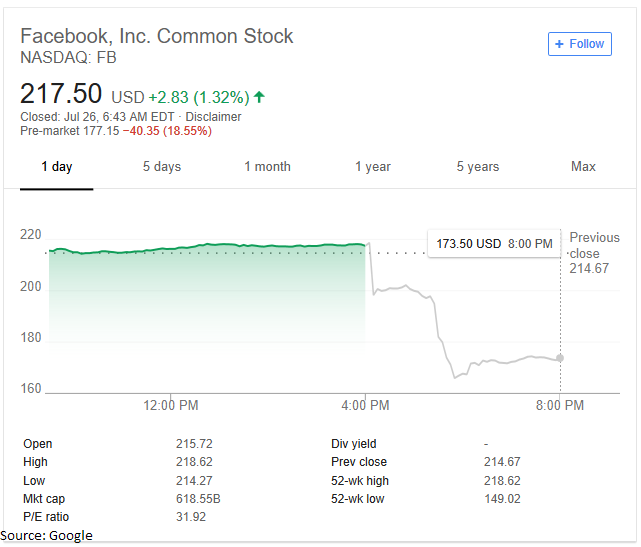

Among the important drivers in the stock markets, it is worth paying attention that the Facebook shares at OTC trades collapsed by 24%, reducing the capitalization of the company by more than $150 bln. This falling caused a decrease of Nasdaq by 2.3% and pressed seriously on the shares of other IT companies.

There were two negative events within several hours that contributed to such a strong reaction. China withdrew its permission to establish a joint company with Facebook, which puts into question the possibility of expanding the company in the most populated country in the world. Separately, the quarterly earnings report of the company showed a falling in profit margin to 44%. At the same time, the company warned that the strengthening of security measures in the next couple of years would reduce this figure to 'mid-30s', which is much lower than 47% year before. The company continues to demonstrate the revenue growth and the increase in the number of users, although the growth rate has been at its lowest ever.

It is worth noting that the market reaction seems excess. In the first quarter, there was an unexpectedly strong increase in profit and users, which has diminished considerable by now. The shares returned to the levels of the beginning of May. With 2.2 billion active users, it is problematic to find the new ones. Moreover, the sales revenue continues to increase with just a slighter slowdown than before.

ECB Decision Expected To Be A Non-Event

Notes/Observations

- European confidence data mixed (Beats: Italy; Misses: Germany, France)

- US-EU ceasefire in the trade war but likely a long negotiation period ahead

- ECB viewed as a non-event after the previously announced taper. Draghi to be quizzed on clarity for 1st potential rate hike

- Focus back on corporate earnings after Facebook shares plunged aftermarket

Asia:

- South Korea Q2 Preliminary GDP Q/Q: 0.7% v 0.7%e; Y/Y: 2.9% v 2.9%e

- BOJ expected to discuss reducing investment in exchange traded funds that track the Nikkei Stock Average in favor of those that follow broader indexes such as the Topix at its next meeting. BoJ likely to keep buying of ETF at ¥6T per year

Europe:

- UK govt said to be considering a contentious Brexit plan over the Irish border issue which would allow the EU to impose its market regulations on Northern Ireland while the rest of the UK left after Brexit. Plan would kick in as a backstop if other options fail in order to ensure there will not be a hard border on the land frontier between UK/Ireland

- UK PM May said to be planning to meet directly with EU leaders in September where she would hold direct talks in an attempt to avert a no deal Brexit Americas

- President Trump stated that had agreed to work together with Europe towards zero tariffs on non-auto industrial goods. Reportedly had received concessions from Europe to avert trade war. US agreed not to increase tariffs on cars and trucks during negotiation period. In return Europe agreed to lower industrial tariffs and to import more US soybeans and to considering importing more LNG from the US. EU also agreed to cooperate on regulatory medical products standards. Both sides agreed to set up working group to carry out joint trade agenda

- Senators introduce bill to delay auto tariffs. Bill would require the ITC study the impact of the Section 232 tariffs on automotive industry and provide results to the White House

Energy:

- Saudi Arabia suspending oil shipments through the Bab-el-Mandeb straight near Yemen after two Saudi VLCCs were attacked by Houthi militia. Would not use the straight until maritime passage was safe

Economic Data:

- (DE) Germany Aug GfK Consumer Confidence: 10.6 v 10.7e

- (DK) Denmark Jun Retail Sales M/M: 0.0% v 1.1% prior; Y/Y: 3.1% v 3.9% prior

- (FI) Finland Jun Preliminary Retail Sales Volume Y/Y: -0.3% v +4.3% prior

- (NO) Norway May AKU Unemployment Rate: 3.8% v 3.7%e

- (FR) France July Consumer Confidence: 97 v 98e

- (ES) Spain Q2 Unemployment Rate: 15.3% v 15.8%e

- (SE) Sweden July Consumer Confidence: 99.8 v 97.1 prior; Manufacturing Confidence: 118.1 v 115.9prior, Economic Tendency Survey: 109.6 v 108.0e

- (SE) Sweden Jun Household Lending Y/Y: 6.3% v 6.6% prior

- (SE) Sweden Jun Unemployment Rate: 7.2% v 6.8%e, Unemployment Rate (Seasonally Adj): 6.3% v 6.1%e, Unemployment Rate Trend: 6.2% v 6.2% prior

- (IT) Italy July Consumer Confidence: 116.3 v 116.0e; Manufacturing Confidence: 106.9 v 106.5e; Economic Sentiment: 105.4 v 105.5 prior

- (HK) Hong Kong Jun Trade Balance (HKD): -54.1B v -52.0Be; Exports Y/Y: 3.3% v 7.9%e; Imports Y/Y: 4.4% v 8.2%e

- (IT) Italy Jun Hourly Wages M/M: 0.9% v 0.2% prior; Y/Y: 2.0% v 1.0% prior

Fixed Income Issuance:

- (IT) Italy Debt Agency (Tesoro) sold €2.0B vs. €1.5-2.0B indicated range in Zero Coupon Mar 2020 CTZ; Avg Yield: 0.647% v 0.917% prior; Bid-to-cover: 1.61x v 1.88x prior

- (IT) Italy Debt Agency (Tesoro) sold €1.25B vs. €0.75-1.25B indicated range in 1.30% May 2028 I/L Bonds (BTPei); Avg Yield: 1.55% v 1.28% prior; Bid-to-cover: 1.64x v 2.23x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.6% at 389.5, FTSE -0.1% at 7652 DAX +1.5% at 12769, CAC-40 +0.8% at 5469, IBEX-35 +0.8% at 9778, FTSE MIB +0.8% at 21,729, SMI +1.5% at 9153, S&P 500 Futures -0.2%]

- Market Focal Points/Key Themes: European Indices trade higher across the board with Auto names helping the Dax outperform as news that the US has agreed to work with the EU on lowering trade tariffs after a meeting with President Trump and EU's Juncker. BMW, Fiat, Volkswagen among names outperforming. Elsewhere in the earnings front Daimler reported a miss on earnings and lowered its EBITA outlook on raw material prices and tariffs, while Valeo, Nokia, Anheuser Busch and Ingenico trade sharply lower after results. Roche trades higher after reporting a beat and raised outlook, with Nestle, Airbus, Suez and Total trading higher on strong earnings. Royal dutch shell trades lower after an earnings miss but did announce a $25B share buyback. Looking ahead notable earners include Comcast, American Airlines, Mastercard and McDonald's.

Movers

- Consumer Discretionary Nestle [NESN.CH]+2.7% (Earnings), ABI [ABI.BE] -5.7% (Earnings)

- Utilities Suez [SEV.FR] +2.4% (Earnings)

- Healthcare Roche [ROG.CH]+2.2% (Earnings), Covestro [1COV.DE] +1.7% (Earnings), Astrazeneca [AZN.UK] +2.6% (Earnings) -Financials Ingenico [ING.FR] -4.5%(Earnings)

- Industrials Daimler [DAI.DE]+1.2% (Earnings), BMW [BMW.DE] +2.5%, VW [VOW3.DE]+2.9%, Fiat [FCA.IT]+4.2% (Senators unveil bill to delay auto tariffs), Airbus [AIR.FR] +5.6% (Earnings), Kion [KGX.DE] -7.5% (Earnings), Valeo [FR.FR] -7.6% (Earnings), Cobham [COB.UK] -10% (Earnings)

- Telecom Nokia [NOK.FI] -9% (Earnings), Telefonica [TEF.ES] +2.9% (Earnings)

- Energy Total [FP.FR] +1.3% (Earnings

Speakers

- Japan Fin Min Aso: If CNY currency (Yuan) weakens from US Fed rate hikes then it would trouble other economies; China only uses free trade 'when convenient'

- Philippines Central Bank Gov Espenilla reaffirmed its plan for strong follow through on rate hike as FX pressure could hit CPI expectations. RRR cuts could resume in 2019 as inflation returns to target. Goal would be to have single-digit RRR by the end of Gov Espenilla term

- Thailand Finance Ministry saw the central bank keeping interest rates steady for remainder of 2018. Forecasted 2018 GDP growth at 4.5%

- China PBoC said to adjust two structural parameters in its macro prudential assessment and would depend on which province

Currencies

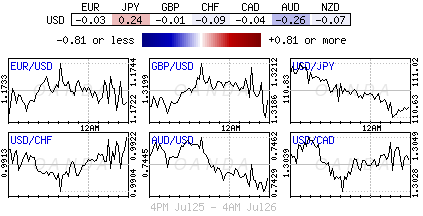

- FX markets were quiet with little fresh impetus to put on positions.

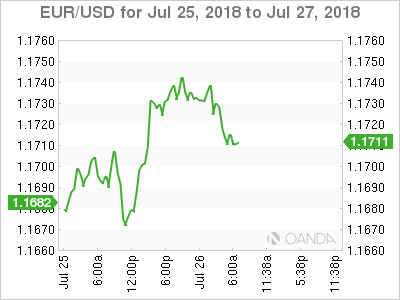

- EUR/USD probed multi-day highs and the upper end of the July trading range as the US-EU seemed to reach a ceasefire in the looming trade war. The pair was holding above the 1.17 handle. ECB viewed as a non-event after the previously announced taper. Draghi likely to be quizzed on clarity for 1st potential rate hike language.

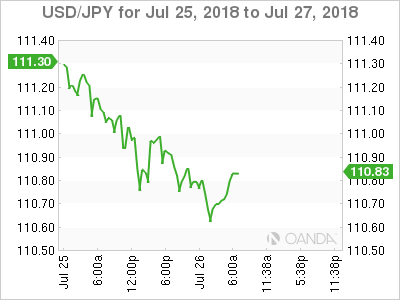

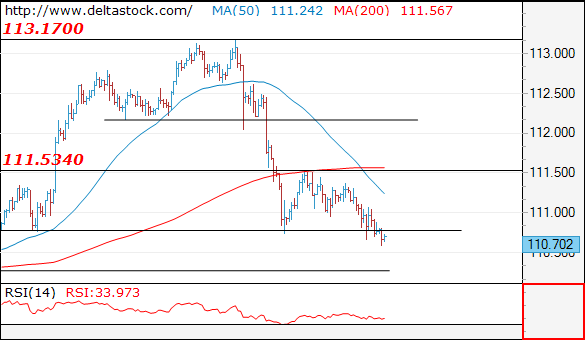

- USD/JPY softer by 0.2% and back below the 111 level as market try to anticipate possible moves by the BOJ at next week’s policy decision. BoJ seen keeping buying of ETF at ¥6T per year but said to be discussing reducing investment in exchange traded funds that track the Nikkei Stock Average in favor of those that follow broader indexes such as the Topix

Fixed Income

- Bund Futures trades at 162.04 up 2 ticks ahead of the ECB rate decision. A move back above 162.75 would target 163.47 then 163.63, with a move below 161.75 targeting 161.45 then 160.45.

- Gilt futures trades at 123.09 down 17 ticks following hte move in Treasuries with continuing upside targeting 124.18 then 124.44, with a move lower seeing initial support at 123.23 then 122.85.

- Thursday's liquidity report showed Wednesday's excess liquidity rose from €1.809T to €1.817T. Use of the marginal lending facility rose from €50M to €73M.

- Corporate issuance saw 4 high-grade issuers raise $3.1B in the primary market

Looking Ahead

- (AR) Argentina July Consumer Confidence: No est v 35.97 prior

- (BR) Brazil Jun Central Govt Budget Balance (BRL): No est v -11.0B prior

- (PT) Portugal YTD Budget Report

- (ZA) BRICS members hold summit in South Africa

- (US) NAFTA negotiations between Mexico, Canada and US in Washington

- 05:30 (ZA) South Africa Jun PPI M/M: 0.3%e v 0.7% prior; Y/Y: 5.2%e v 4.6% prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills; Avg Yield: % v 0.56% prior; bid-to-cover: x v 1.25x prior (July 12th 2018)

- 06:00 (IL) Israel May Manufacturing Production MoM: No est v 2.2% prior

- 06:00 (CA) Canada July CFIB Business Barometer: No est v 62.2 prior

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil July FGV Construction Costs M/M: 0.8%e v 0.8% prior

- 07:45 (EU) European Central Bank (ECB) Interest Rate Decision: Expected to leave 7-Day Main Refinancing Rate unchanged at 0.00%

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Jun Preliminary Durable Goods Orders: +3.0%e v -0.4% prior; Durables Ex Transportation: 0.5%e v 0.0% prior, Capital Goods Orders (Non-defense/ex-aircraft): 0.5%e v 0.3% prior, Capital Goods Shipments (Non-defense/ex-aircraft): 0.4%e v 0.2% prior

- 08:30 (US) Initial Jobless Claims: 215Ke v 207K prior; Continuing Claims: 1.73Me v 1.751M prior

- 08:30 (US) Jun Advance Goods Trade Balance: -$66.9Be v -$64.8B prior

- 08:30 (US) Jun Preliminary Wholesale Inventories M/M: 0.3%e v 0.6% prior; Retail Inventories M/M: No est v 0.4% prior

- 08:30 (US) Weekly USDA Net Export Sales

- 08:30 (EU) ECB’s Draghi post rate decision press conference

- 09:00 (MX) Mexico Jun Unemployment Rate: 3.3%e v 3.2% prior, Unemployment Rate (Seasonally Adj): 3.2%e v 3.2% prior

- 09:00 (RU) Russia Gold and Forex Reserve w/e July 20th: No est v $460.3B prior

- 09:30 (BR) Brazil Jun Current Account: $0.3Be v $0.7B prior; Foreign Direct Investment (FDI): $6.0Be v $3.0B prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (US) July Kansas City Fed Manufacturing Activity: 25e v 28 prior

- 13:00 (US) Treasury to sell 7-Year Notes

U.S-E.U Calls A Ceasefire In The Trade War

Thursday July 26: Five things the markets are talking about

In early trading, Euro bourses have advanced following a mixed Asian session overnight as capital markets contend with a host of stimuli, including an apparent easing of trade tension between the U.S and Europe and a flood of corporate earnings.

U.S President Trump has reached an agreement yesterday with E.C President Juncker aimed at avoiding a transatlantic trade war. The so-called compromise has gone some ways to ease market tensions fuelled by Trump’s threat to impose tariffs on Euro auto imports. Both parties have agreed to expand European imports of liquefied natural gas and soybeans and lower industrial tariffs on both sides.

U.S Treasures have edged up while the 'big’ dollar trades steady after falling yesterday ahead of this morning European Central Bank (ECB) monetary policy announcement (07:45 am EDT). Elsewhere, crude prices have climbed as stockpiles fell, while gold has lost some of its lustre.

On tap: As the week continues, more corporate earnings come on line. After Draghi’s press conference this morning, market focus will shift to tomorrow’s U.S GDP print – Trump and his economic team are increasingly convinced the GDP numbers will be strong – he expects Q2 GDP to rise as much as +4.8%! If so, it will be a very interesting last session of the week.

1. Stocks mixed results

In Japan, most stocks closed higher overnight on upbeat earnings and easing concerns about trade tensions. However, the Nikkei benchmark softened on speculation that the BoJ might trim their buy of ETF’s linked to the index. The Nikkei average shed -0.12%, while the broader Topix ended the day at a five-week high, rallying +0.7%.

Down-under, the Aussie stock benchmark quickly reversed initial weakness to spend the afternoon right round Wednesday’s closing level. As stock-specific news dominated the session, the S&P/ASX 200 finished down -0.05%. In South Korea, the Kospi was amongst Asia’s best performers, helped by gains in the country’s biggest stock. The index rose +0.7% as Samsung bounced +1.6% following the overnight strength in U.S tech stocks.

In China and Hong Kong, stocks ended lower as the Sino-U.S trade friction fuelled uncertainties over both countries economic growth. In China, the blue-chip CSI300 index ended down -1.2%, while the Shanghai Composite Index closed down -0.7%. In Hong Kong, the Hang Seng index fell -0.5%, while the China Enterprises Index lost -0.5%.

In Europe, regional bourses trade higher across the board with auto names helping the DAX outperform as news that the U.S has agreed to work with the E.U on lowering trade tariffs.

U.S stocks are set to open in the 'red’ (-0.2%).

Indices: Stoxx600 +0.6% at 389.5, FTSE -0.1% at 7652 DAX +1.5% at 12769, CAC-40 +0.8% at 5469, IBEX-35 +0.8% at 9778, FTSE MIB +0.8% at 21,729, SMI +1.5% at 9153, S&P 500 Futures -0.2%

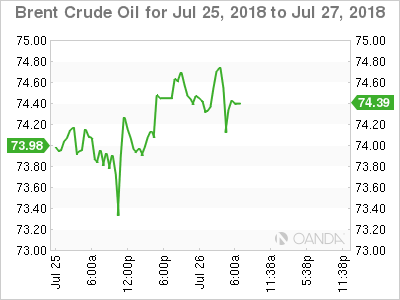

2. Brent oil higher as some Saudi Red Sea shipments suspended, gold lower

Brent crude prices are rallying after Saudi Arabia suspended its oil shipments through a key Red Sea strait in response to an attack on two of its tankers and as data showed U.S inventories at a four-year low.

Brent crude futures have rallied +55c to +$74.48 a barrel, hitting a ten-day high, while U.S West Texas Intermediate (WTI) crude futures are -4c lower at +$69.26.

Saudi Arabia said today that it was 'temporarily halting; all oil shipments through the strategic Red Sea shipping lane of Bab al-Mandeb after an attack on two oil tankers by Yemen’s Iran-aligned Houthi movement.

Note: An estimated +4.8M bpd of crude oil and refined petroleum products flow through this waterway towards Europe, the U.S and Asia.

Yesterday’s EIA report showed that crude inventories fell -6.1M barrels in the week to July 20, compared with a market expectation for a decrease of -2.3M barrels.

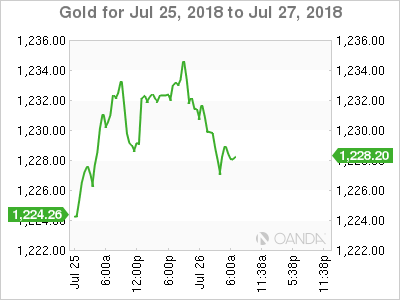

Ahead of the U.S open, gold prices have shed their early gains overnight, as the dollar remains firm against the yuan amid a grim outlook for the world’s second-largest economy. Spot gold is down -0.3% at +$1,227.61 an ounce. U.S gold futures, for August delivery, are -0.3% lower at +$1,227.70 an ounce.

3. Sluggish economy to keep ECB dovish

Soft economic data in recent months should allow the European Central Bank (ECB) to remain cautious in its unwinding of its loose monetary policy and reason why today’s policy meeting is expected to be a non-event.

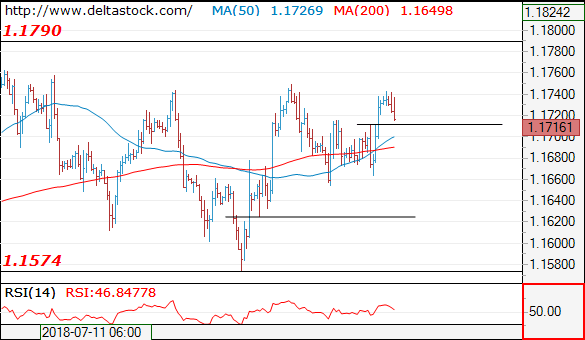

Eurozone PMI readings disappointed in July, showing a further decline from Q3 peaks in 2017. Data like this should keep the ECB in relatively 'dovish; mood. Euro policy makers have no reason to second-guess markets, with EUR (€1.1715) strength an 'unappealing; prospect. However, given the fact that the ECB did not amend its forward guidance on reinvestments at last months meeting, suggests that is still a lot to discuss and agree too in the other policy areas.

The yield on 10-year Treasuries has declined -1 bps to +2.96%, the largest fall in a week. In Germany, the 10-year Bund yield has increased +2 bps to +0.42%, while in the U.K, the 10-year Gilt yield climbed +2 bps to +1.274%.

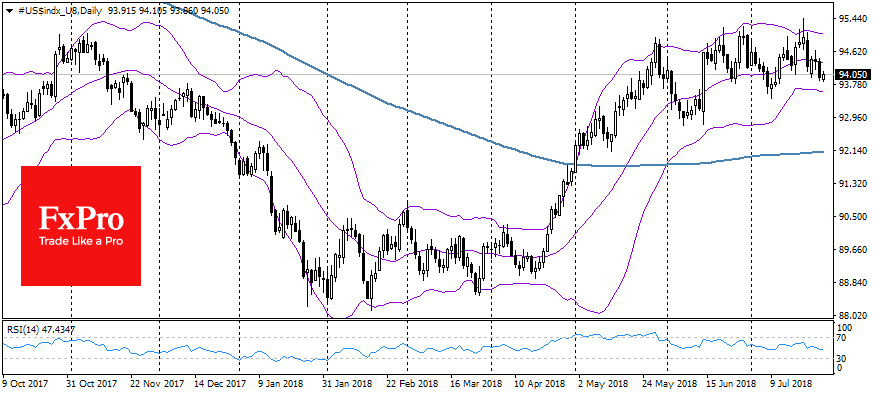

4. The 'big’ dollar is little changed

The DXY index is down by -0.2% ahead of the U.S open. To date, the USD had been the biggest winner of the trade war disputes and it’s not surprising to see the currency lower across the board on the back of easing global trade war risks.

Note: The dollar was trading at a +2-3% premium against most currencies relative to interest rate differentials and global risk sentiment.

EUR/USD (€1.1716) probed multi-day highs and the upper end of the July trading range, as the U.S-E.U seemed to reach a ceasefire in the looming trade war. Today’s ECB decision is being viewed as a 'non-event; after the previously announced taper. Expect Draghi to be quizzed on clarity for the first potential rate hike language.

USD/JPY softer by -0.2% and back trading below the psychological ¥111 level at ¥110.78 as the market tries to anticipate possible moves by the BoJ at next week’s policy decision (July30-31).

The BoJ is expected to keep buying of ETF’s at ¥6T annually, but are said to be discussing reducing investment in ETF’s that track the Nikkei Stock Average in favour of those that follow broader indexes such as the Topix.

5. Venezuela to remove five-zeroes from ailing currency

Venezuela will remove five-zeroes from its bolivar currency rather than the three-zeroes originally planned.

President Nicolas Maduro said yesterday, 'in an effort to keep up with inflation projected to reach +1M percent this year.

The OPEC nation’s economy has basically collapsed since the crash of oil prices left it unable to maintain its socialist economic system.

Last month, annual inflation topped +46K percent. The IMF said this week it could hit seven-digits in 2018, putting it on par with the crises of Zimbabwe in the 2000’s and Germany in the 1920’s.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1716

The dip to 1.1660 should be the finale of the consolidation pattern and the outlook is positive, for a rise towards 1.1790. Initial intraday support is projected at 1.1710.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1750 | 1.1750 | 1.1710 | 1.1510 |

| 1.1790 | 1.1830 | 1.1660 | 1.1300 |

USD/JPY

Current level - 110.70

The slide below 110.80 low signals a risk of a further depreciation, towards 110.25 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.50 | 114.50 | 110.25 | 110.25 |

| 112.10 | 114.50 | 109.30 | 109.30 |

GBP/USD

Current level - 1.3185

The uptrend remains intact, heading towards 1.3300 area and crucial on the downside is 1.3130 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3300 | 1.3460 | 1.3130 | 1.2960 |

| 1.3360 | 1.3620 | 1.3080 | 1.2770 |

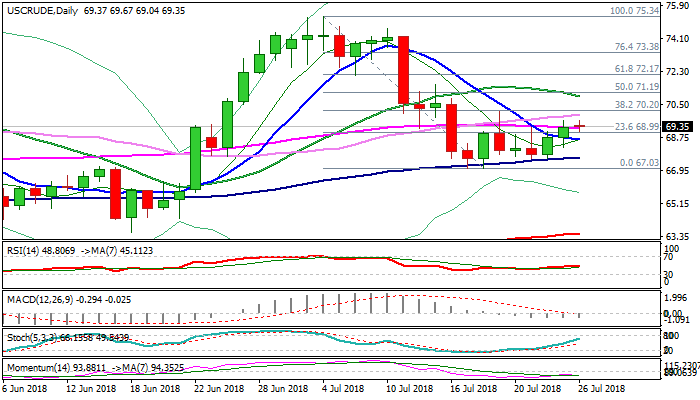

WTI Oil Outlook: Bullish Signal On Probe Above 55SMA Needs Confirmation On Break Above $70.00/20 Pivots

WTI oil consolidates on Thursday after strong two-day rally, triggered by fresh draw in crude stocks and reduced Saudi Arabia oil shipments through Red Sea.

EIA report on Wednesday showed draw in crude inventories of 6.14 million barrels vs forecast for 2.6 million barrels fall, bringing crude stocks to the lowest levels in over three years.

Daily structure improved following probe above pivotal 55SMA ($69.23) which generates bullish signal, but close above is needed to confirm and expose next pivots at $70.00/20 (psychological barrier / Fibo 38.2% of $75.34/$67.03 bear-leg).

Sustained break above $70.00/20 pivots is needed to turn daily techs from mixed to bullish mode and support further recovery.

Conversely, repeated failure to close above 55SMA would signal further range trading, but bullish bias would remain intact while the price holds above broken 10SMA ($68.63).

Res: 69.68, 70.00, 70.20, 70.86

Sup: 69.04, 68.63, 68.19, 67.66

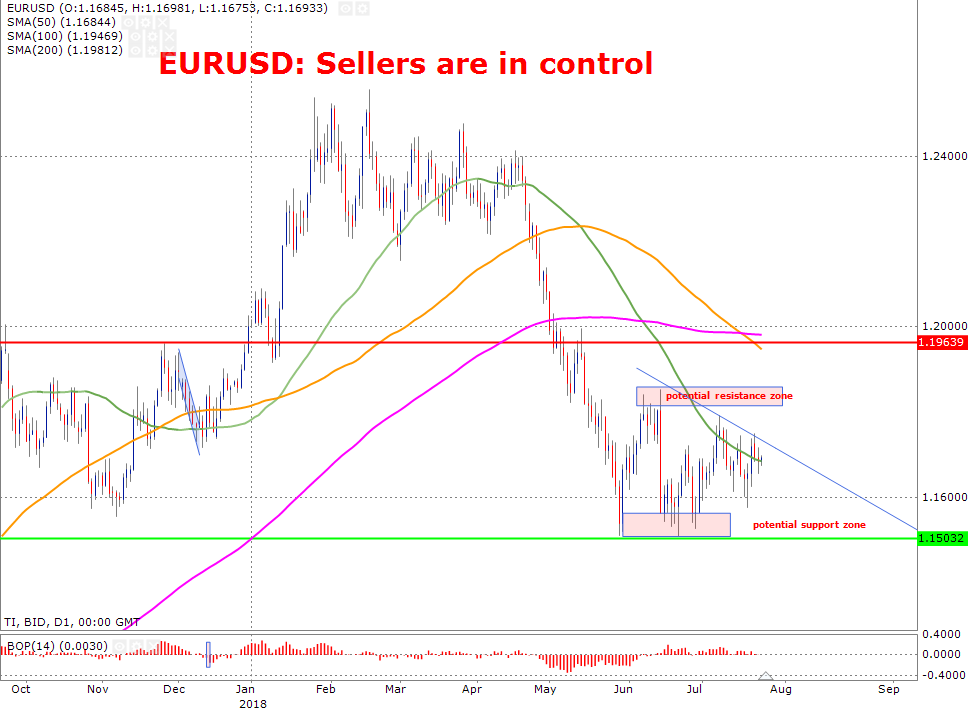

Where The Euro Can Go

By looking at the Euro-dollar pair, one can clearly say that the bulls are not willing to give up. The support at 1.15 is not only robust but we think that the price has formed a bottom for 2018.

But if the bottom is in play now, this isn’t so much of good news for the ECB. The ECB members believe that lower currency promotes drives up the inflation. Thus, this leaves the door wide open that any rally in the Euro-dollar is prone to short squeeze. But the jawboning of President Trump towards the dollar (as he thinks that the dollar is too high) could provide a little more breathing room for the bulls.

Technically speaking, the price in a battle with the 50-day moving average and it seems like it is struggling to stay above this. Something also noteworthy here is there is also a downward trend line and the price would need some serious momentum to break this trend line and the 100-day moving average. As long as we are below the 1.17 resistance level, the downward pressure would impact the price more.

Juncker And Trump Averted A Catastrophe | Facebook Lost Its Charm? | ECB Needs To Deliver A Goldilocks Statement

Another catastrophe was averted, and transatlantic trade war was saved last night as Juncker and Trump reached a deal. Traders celebrated this news on Wall Street and pushed the stocks higher. The same momentum is filtering into the European futures today however there is also a strong influence of disappointing earnings result which is impacting the overall indices.

Traders do have every right to celebrate Juncker and Trump meeting because the tensions were high before the meeting as it was pretty much clear that we are heading towards a real trade war. But thanks to common sense which prevailed last night, and it eased tensions stoked by threats coming from both side.

Under the agreement, both sides would hold off on other tariffs as the negotiation process continues. The joint statemen by leaders did look like a fairy tale, both sides agreed to work towards zero tariffs. For Trump it does not matter what the final deal would like, but for now, it is enough for him to show the world that he delivered on his promise and he brought the Europeans to a point where he thinks that things are fair.

In short and simple words, the EU does not want to be part of any resistance and Donald Trump has another victory to talk about.

The most popular stock among hedge funds got slammed last night and entered in to a bear market territory. Yes, we are talking about Facebook facing growth challenges. The stock wiped out nearly $130 billion in market cap and it has erased all of its gain for the current year. Even during the conference, Mark Zuckerberg failed to rescue the stock as the element which haunted traders is that Facebook isn’t confident about the growth rate. The forecast for Q3 and Q4 wasn’t charming at all and the stock collapsed.

The other main reason for disappointment for Facebook investors was in the massive increase in the operating cost due to rise in the headcount. Smart money failed to factor in the impact of Facebook’s scandals on user agreement which resulted in higher headcounts. The increase in cost effected the operating margin. The operating profit declined to 44% from its previous reading of 47% one year ago. The net effect comes to free cash flow which plummeted.

Back in the Eurozone, currency traders are focused on the ECB press conference and all eyes would be Draghi once again. It is all about the risk assessment today and how the president of the European Central bank read the current situation given the trade war (which is diffused). You can see that the economic growth muscles for the eurozone are looking fatigue and a lot of this has to do with the matters which are just beyond the ECB control- the trade war and tariffs. Both; trade war and high tariff impose a serious threat and the ECB is mind of this fact. Economic data published on Tuesday confirmed that the business activity is being impact due to the protectionism policies. The purchasing manager’s index for services dropped unexpectedly this week. The ECB has said that it would end the QE this year and would not touch the interest rate for another year and we do not think there will be any new buzz word when it comes to this particular statement.

The ECB needs to extremely vigilant about its monetary policy because it is winding down its QE when protectionism is at its peak and growth isn’t flexing its muscles. Draghi would have to strike a balance tone today, he cannot be overly dovish just like recent meeting back in June.

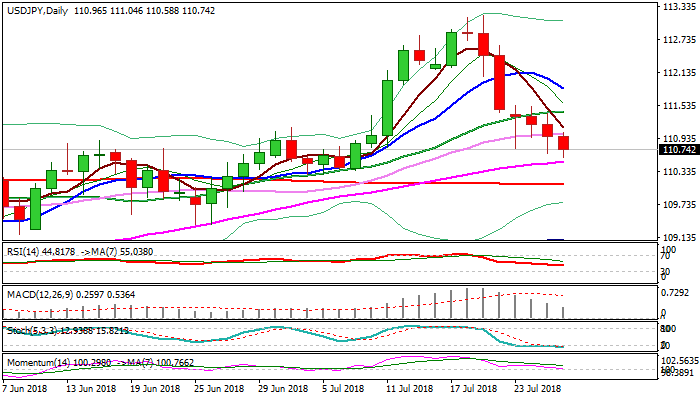

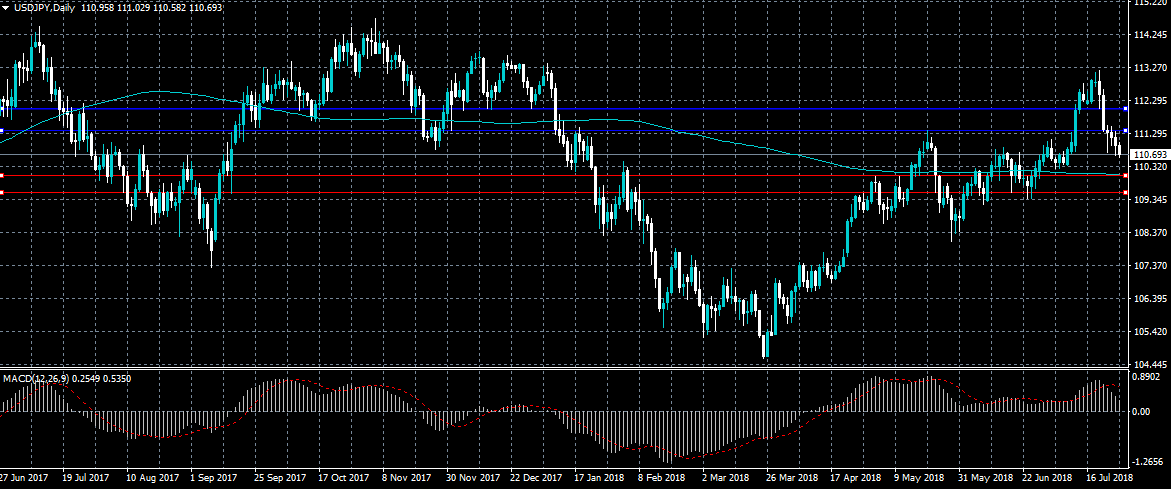

USDJPY May Weaken Towards 110.00

The US dollar continues to trade lower against the Japanese yen currency after news broke that the Bank of Japan may start to review its ETF purchases. The USDJPY may continue to weaken towards the 110.00 level, as sentiment towards the pair remains bearish. Traders now look to the release of key U.S. Durable Goods Orders data from the United States economy later today.

The USDJPY pair is strong bearish while trading below the 110.87 level, key support is found at the 110.25 and 110.00 levels.

If the USDJPY pair trades back above the 110.87 level, buyers may push the price back towards the 111.20 and 111.37 levels.

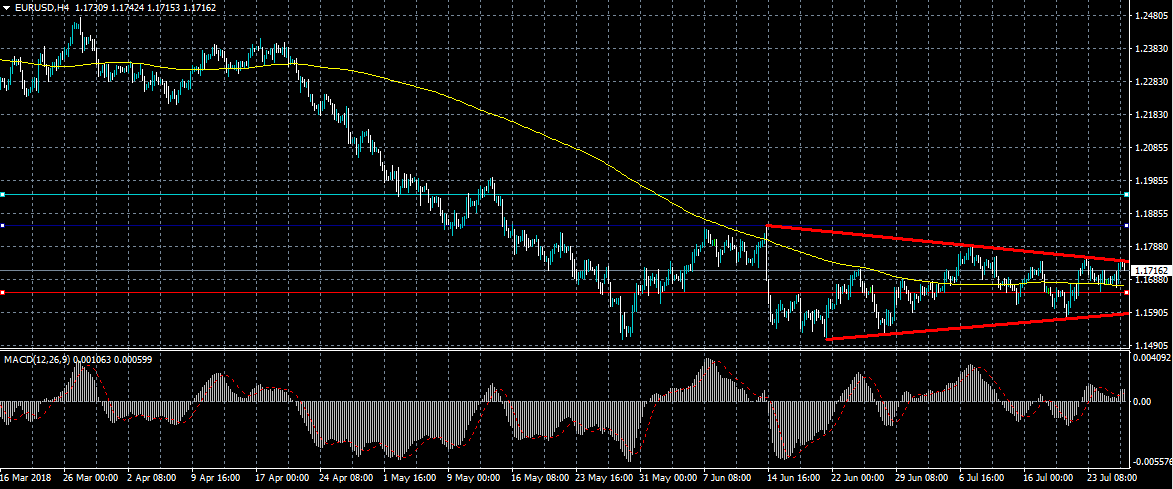

EURUSD Key Levels To Watch Ahead Of The ECB

The euro has moved back towards the 1.1700 level against the US dollar, ahead of today’s key policy decision from the European Central Bank. A key technical breakout in the EURUSD pair is possible today, as price trades within a symmetrical triangle pattern. Buyers will now attempt to break the 1.1750 level, while sellers will look to break below the 1.1600 support level.

The EURUSD pair is only intraday bullish while trading above the 1.1750 level, key resistance is currently found at the 1.1800 and 1.1851 levels.

If the EURUSD pair trades below the 1.1680 level, sellers will likely target the 1.1650 and 1.1600 support levels.

USDJPY Outlook: Bears Pressure Pivotal Supports At 110.64/51 And May Extend To 110.00 Zone On Break

The pair remains in red for the sixth straight day and extends pullback from 113.17, where larger bulls were capped by weekly 200 SMA.

The dollar was additionally pressured by positive tone from US/EU trade talks and fresh weakness attempts at strong supports at 110.64/51 (50% of 108.11/113.17 / rising 55SMA) clear break of which would trigger further bearish extension towards strong supports at 110.00 zone (200SMA / Fibo 61.8% / daily cloud top).

Weak daily techs support negative outlook, however, risk of extended consolidation / bounce exists, as slow stochastic is oversold.

Broken 30SMA (111.01) should ideally cap, with stronger upticks to stall under broken 20SMA (111.42) to keep bears intact.

Res: 111.01, 111.42, 111.84, 112.18

Sup: 110.51, 110.10, 109.92, 109.77