Sample Category Title

Dollar Rebounds In Anticipation Of Q2 GDP Release

The US dollar is higher across the board against major pairs on Thursday. The first estimate of second quarter gross domestic product (GDP) in the US will be published on Friday, July 27 at 8:30 am EDT by the Bureau of Economic Analysis. The dollar gained ground on the euro after the European Central Bank (ECB) held interest rates unchanged as expected but said rates would be steady a year from now. The first release of GDP data for the second quarter is released 30 days after the end of the quarter with economists and analysts expecting it to be one of the best quarters in recent years. How good will the final number be has been the subject of commentary from President Trump and other members of his administration while some forecasters are lowering their estimates after a disappointing durable goods order data point.

- US 2Q GDP forecasted at 4.1 percent

- President Trump has told associates GDP is around 4.8 percent

- Some forecasters have cut their estimates due to recent soft data

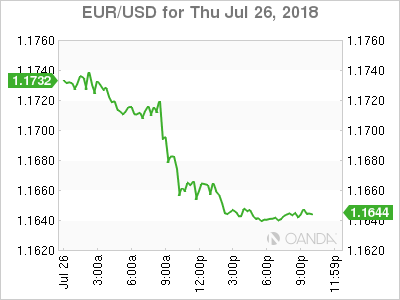

EUR Lower as ECB Plays it Safe

The EUR/USD lost 0.57 percent on Thursday. The single currency is trading at 1.1661 after the central bank kept rates and the quantitive easing program unchanged. The July meeting was almost a beat for beat replay of the June meeting, leaving investors with almost no new information. There was no clear guidance on the vague meting of summer of 2019 as the time horizon to lift rates.

The US GDP release will be the main market event of the week as it could come in above 4 percent. There is an open debate between economists on how much did the Trump tax cuts influenced the positive momentum. The U.S. Federal Reserve is scheduled to meet for two days next week. There are no expectations of a rate lift, but the data has so far validated the two rate hikes and more to come.

The meeting between Donald Trump and Jean-Claud Juncker was a win for the USD as it seemed Europe had conceded to American demands even if the goal is to reach zero tariffs. With trade tensions easing the market turned to monetary policy and growth divergence ahead of the Q2 GDP release on Friday morning.

The USD will face a serious challenges in August. Central banks are expected to close the monetary policy gap and retaliations from China on trade could end up hurting the American economy in the long term. Politics will also add some uncertainty to the US dollar as midterm elections approach with a forecasted Democratic win that change the power dynamics in Washington.

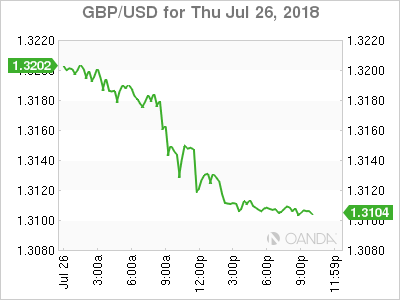

Brexit Fears Overpower BoE Rate Hike Expectation

The GBP/USD lost 0.59 percent on Thursday. The currency pair is trading at 1.3110 as the USD rebounded from yesterday’s losses. The Bank of England (BoE) is heavily anticipated to lift rates next week after the last monetary policy committee had three members who dissented from holding rates. Investors are pricing in a 81 probability of higher interest rates on Thursday but the divorce between the United Kingdom and Europe put more pressure on sterling.

The lack of an unified front within the Conservative party on which Brexit to pursue has left Prime Minister Theresa May with just eight months to figure out a lot of issues. The GBP has fallen as more uncertainty grips investors hopes of a comprehensive trade deal that keeps the UK as a participant of the single market.

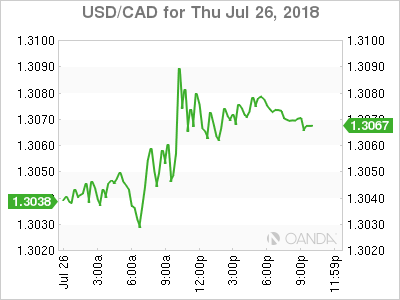

Loonie Lower Despite NAFTA Optimism

The USD/CAD gained 0.20 percent in the last 24 hours. The currency pari is trading at 1.3072 ahead of the release of the second quarter GDP data in the US. The pair almost touched 1.32 at the at the beginning of the week, but a rebound from the loonie took the currency to near 1.3050. The optimism surrounding the NAFTA renegotiation was behind most of the move with the Canadian currency touching a six week high. The meeting between US President Trump and EU Commission chief Jean-Claude Juncker had a positive outcome although it was scarce on details and did not directly address the tariffs on steel and aluminum that will remain in place.

The change in leadership in Mexico gave the locked NAFTA negotiations a chance for a fresh start. The comments from advisors to elected-president Andres Manuel Lopez Abrador have been pro-NAFTA and the Trump administration came out in support of a quick resolution. It is unclear if the US is willing to drop the two more contentious issues it has pushed on the table, the sunset clause and the higher American percentage of US parts on autos. U.S. Trade Representative Robert Lighthizer has said that the negotiation is in its finishing stages, but so far the biggest issues remain up in the air.

Market events to watch this week:

Friday, July 27

8:30am USD Advance GDP q/q

Gold Dips As Trade Tensions Ease Following Juckner Visit

Gold has posted losses in the Thursday session. In North American trade, the spot price for one ounce of gold is $1227.40, down 0.40% on the day. On the release front, durable goods reports rebounded in June but missed their estimates. Core Durable Goods Orders improved to 0.4%, shy of the estimate of 0.5%. Durable Goods Orders posted a gain of 1.0%, short of the estimate of 3.0%. Unemployment claims climbed to 217 thousand, above the estimate of 215 thousand. On Friday, the U.S releases Advance GDP and UoM Consumer Sentiment.

Trade tensions between the U.S and the European Union have dropped dramatically, which has sent gold prices lower on Thursday. EU Commission President Jean-Claude Juckner met with President Trump on Wednesday at the White House, and the meeting went better than expected. The parties announced that they had agreed to hold off on any further tariffs while talks are ongoing. This is a major concession from Trump, who had threatened to impose tariffs on European car imports. U.S tariffs on European aluminum and steel will remain in place, but Juckner pointed out that the U.S has agreed to reassess these measures. It’s still too early to call the trade war over, with negotiations over trade expected to be contentious. Still, market sentiment has improved, and if the Trump administration can reach agreements with China and with Canada and Mexico over NAFTA, risk appetite could rise and send gold prices downwards.

Eco Data 7/27/18

[php_everywhere instance="1"]

British Pound Dips Despite Soft US Durables

The British pound has posted losses in the Thursday session, erasing the gains made on Wednesday. In the North American session, the pair is trading at 1.3149, down 0.31% on the day. On the release front, there are no British events on the schedule. In the U.S, durable goods reports rebounded in June, but missed their estimates. Core Durable Goods Orders improved to 0.4%, shy of the estimate of 0.5%. Durable Goods Orders posted a gain of 1.0%, short of the estimate of 3.0%. Unemployment claims climbed to 217 thousand, above the estimate of 215 thousand. On Friday, the U.S releases Advance GDP and UoM Consumer Sentiment.

Retail sales growth remained strong in July with a reading of 20 points, although it was weaker than the sizzling release of 32 points in June, which was largely due to the unseasonable heat wave. However, the indicator is expected to drop in August. On Tuesday, manufacturer orders showed strong growth for a second straight month, with a reading of 11 points. The CBI Manufacturing Council welcomed the strong manufacturing data, but cautioned that “rising trade tensions and ongoing uncertainty over our future trade and customs arrangements are clearly taking their toll on manufacturers’ confidence and investment.” With U.S trade tariffs on EU products threatening to hurt British exports and the manufacturing sector, the markets are keeping a close eye on UK manufacturing indicators.

Trade tensions between the U.S and the European Union have cast a pall over relations between the sides, so the success of EU Commission President Jean-Claude Juckner’s visit to the White House was welcome news. The parties announced on Wednesday that they had agreed to hold off on any further tariffs while talks are ongoing. This is a major concession from Trump, who had threatened to impose tariffs on European car imports. U.S tariffs on European aluminum and steel will remain in place, but Juckner pointed out that the U.S has agreed to reassess these measures. It’s still too early to call the trade war over, with negotiations over trade expected to be contentious.

What Do Durable Goods Orders Say About GDP Tomorrow?

June durable goods orders increased just 1.0 percent, falling short of a consensus expectation of a 3.0 percent rise. But get under the hood of this report, and the engine of the factory sector is still running fine.

Aside from Softness in Aircraft, Orders Strengthening

It may have been a miss on the headline for durable goods orders with just a 1.0 percent increase in June, but the miss can be attributed, at least partially, to the fact that civilian aircraft orders were decidedly underwhelming.

Defense aircraft orders were up 20.2 percent in the month, but non-defense orders, which are almost three times larger, were only up 4.3 percent. After back-to-back declines in the preceding months, a bigger bounce for orders of non-defense aircraft might have lifted the headline figure higher.

Elsewhere on the transportation side of things, orders increased. Transportation-related equipment orders were up, and motor vehicles and parts orders increased 4.4 percent, nearly reversing a decline of 4.5 percent in the prior month.

Stripping out the notorious volatility of the transportation sector, durable goods orders were up 0.4 percent versus a consensus expectation of 0.5 percent. Technically, that's a miss, but a revision to May's extransportation number pushed the initially-reported 0.0 percent pick-up to a gain of 0.3 percent.

After taking revisions into account, we call that a better-than-expected print for ex-transportation orders. In fact, aside from the flub from aircraft, today's report is the latest indication that our expectation for moderate expansion in the factory sector remains on track.

What Does Today Tell Us About Tomorrow?

Tomorrow morning, financial markets will digest the first estimate of GDP growth for the second quarter, and there are some clues in today's durable goods report and a separate report on wholesale inventories as to what we can expect.

The signals on inventories were negative on balance. Wholesale stockpiles were unchanged in June, despite expectations of a 0.3 percent increase. Inventories at durable goods manufacturers actually declined 0.1 percent in June. Our expectation for tomorrow's GDP report is that inventories will add 0.4 percentage points to the headline growth rate. In light of this latest data, there is some risk that the boost from inventories will be smaller.

On the plus side, shipments of core capital goods, which tend to be a good barometer for equipment spending, increased 1.0 percent in June, which handily beat the 0.4 percent gain that had been expected by the consensus. Meanwhile, orders for this core capital goods series increased 0.6 percent on the heels of an upward revision to May's data. Taken together, these numbers suggest some upside to our call for a 5.1 percent pace of growth in equipment spending.

Our above-consensus call for tomorrow's GDP report is 4.7 percent, which, if realized, would be the fastest pace of economic growth since 2014.

Sunset Market Commentary

Markets

Facebook’s poor Q2 results probably dented US risk/equity sentiment somewhat as US Treasuries marginally recovered some of the ground lost after yesterday’s drop following the EU-US agreement (10-yr -2bps). US initial jobless claims and core durable goods were broadly in line to better than market expectations but had only limited to no impact. After opening higher in a catch-up move with the US, European yields awaited the ECB only to find out no changes to the outlook, statement and forward guidance were made. Draghi welcomed the EU-US agreement, calling it “a good sign”. He avoided questions concerning the ECB’s reinvestment policy saying the matter was not discussed. Draghi didn’t not feel the need to explain or modify the current forward guidance (“through the Summer of 2019”). However, when mentioning “markets are tightly aligned with the ECB rate guidance”, German yields did fall, completely wiping out this morning’s rise. Markets apparently concluded that, at least for now, the ECB intends to raise rates only at the end of the Summer of 2019 rather than in June.

Yesterday evening, EUR/USD rebounded to the 1.1740 area after US president Trump and EU Commission President Juncker agreed to start negotiations aiming to reduce mutual trade barriers and avoiding a further escalation of the trade conflict. However, there were few follow-through euro gains this morning even as European equities opened with good gains. EUR/USD failed to break beyond minor resistance in the 1.1750 area. At its regular meeting, the ECB left its policy and policy guidance unchanged. The June forecasts on growth and inflation were also left unchanged but the ECB president sounded rather optimistic on the economy, despite the uncertainty on trade. The euro temporarily gained a few ticks, but this gain was reversed as the ECB president kept a soft stance on the guidance for the first rate hike. Answering a question, the ECB president also dismissed remarks from US president Trump that Europe artificially weakens its currency. The US and EMU are at a different point in their economic cycle allowing a divergent policy approach. EUR/USD eased slightly during the press conference. The pair trades again below the 1.17 mark. US data were mixed, but didn’t change marked expectations for solid Q2 GDP growth, to be published tomorrow. USD/JPY regained slightly ground this afternoon and is again trading in the 111 area.

As was the case yesterday, it was again an uneventful session for sterling trading today. There was no high profile news on Brexit and no eco data. EUR/GBP is holding a tight sideways range just below the 0.8 big figure. Cable lost some ground this afternoon on overall USD strength (1.3150 area).

News Headlines

China’s central bank is again easing capital requirements for commercial banks to boost lending to businesses, as its economy is slowing and the trade war remains in play. Sources told Reuters that specific capital requirements will be eased, adding to three previous cuts in banks’ required reserve ratios.

US jobless claims have increased to 217,000 last week (215,000 expected). The small increase comes after a historic low (208,000 ) the week before, unmatched since 1969. Shipments of non-military capital goods rose 1% (0.4% expected) after a 0.2% increase in May indicating that trade war concerns only have a weak influence.

The EU has flagged a key part of Theresa May’s plan, how customs will operate after the split, as unsatisfactory. The idea was devised to keep all groups in PM May’s divided cabinet happy. Even as the EU welcomed the overall blueprint, some details raised concerns. Brexit Secretary Dominic Raab meets EU negotiator Barnier later today.

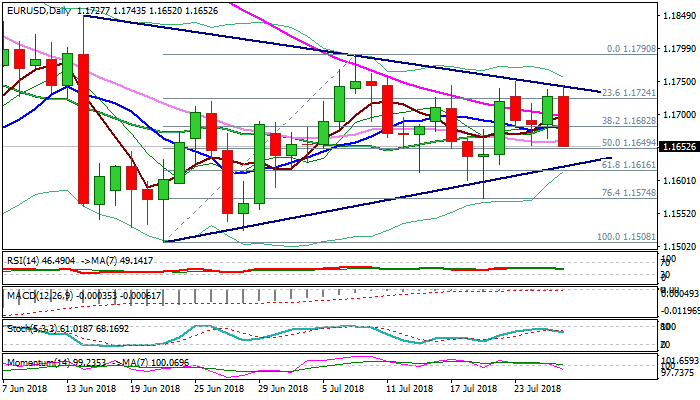

EUR/USD Outlook – Downside Pressure Increases after Dovish ECB; Thick Daily Cloud Continues to Weigh

The Euro entered US session in red and extends losses after dovish comments from ECB’s chief Draghi.

Despite markets expected some hawkish steer, Draghi’s comments on post-rate decision meeting press conference showed no changes from the previous meeting.

Draghi reiterated that interest rates in the Eurozone will remain unchanged until the end of summer 2019 and stressed that the EU economy is still in need for strong stimulus, which would also sideline expectations that the central bank may start winding down the stimulus by the end of this year.

Dovish tone from the central bank head added negative near-term tone after repeated failure to clearly penetrated thick daily cloud, as gains were capped by tringle resistance line (1.1743).

Fresh weakness returned below daily cloud and is on track for strong bearish close today, which could generate bearish signal and risk attack at triangle support line (1.1620).

Close below triangle support line would further weaken near-term structure and risk test of 19 July spike low at 1.1574.

Weakening momentum and a cluster of converged daily MA’s (10;20;30;55) returned to bearish setup, support negative near-term outlook.

Res: 1.1679; 1.1697; 1.1743; 1.1790

Sup: 1.1649; 1.1616; 1.1574; 1.1527

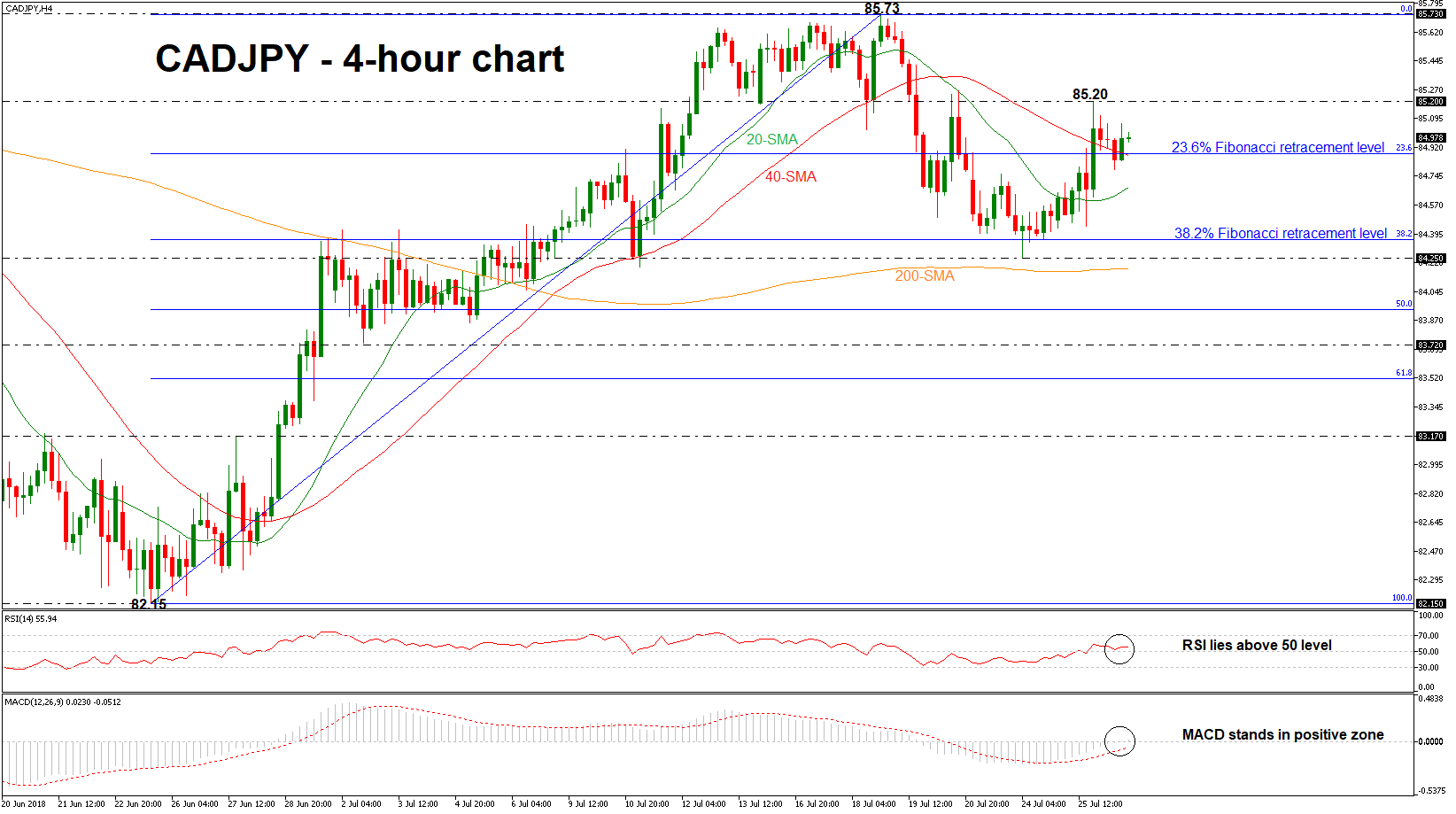

CADJPY Erases Negative Rally; Could Strengthen Further in Short Term

CADJPY has finally returned to the upside after the rebound on the 84.25 support, completing a bearish correction of the short-term uptrend movement. Also, the price climbed above the 23.6% Fibonacci retracement level of the upleg from 82.15 to 85.73, around 84.88 over the last hours and holds above the 20- and 40-simple moving averages (SMAs) in the daily timeframe.

Momentum indicators in the daily chart though are currently supporting that positive momentum is likely to strengthen in the short-term. Specifically, the RSI lies above 50 and the MACD continues to distance itself above its red signal line and entered into the positive zone.

In case of an upward attempt, the price would likely meet resistance at the 85.20 barrier. A break above this would ease the downside pressure and push the pair further higher until the 85.73 hurdle. A potential upside rally would help turn the short-term bias to a more bullish one.

Immediate support is being provided by the 23.6% Fibonacci of 84.88, which stands near the 40-day SMA. However, should prices dip lower again, the next support would likely come from the 20-day SMA, near 84.67. A drop below this level would signal the start of a deeper bearish phase until the 38.2% Fibonacci region of 84.36.

Overall, both the short- and medium-term outlooks are currently looking neutral to bullish, though caution is warranted in the near-term as there are signs of a bullish extension.

ECB Research: Steady as it Goes

- No new policy signals from a rather uneventful meeting.

- Mario Draghi said the main risks still stem from protectionism/the trade war but this said he is generally at ease with the development on the trade war.

- The market reaction to the meeting was muted.

No news

The decision released at 13:45 CEST contained no major surprises, just like the rest of the press conference (starting 14:30 CEST). To our knowledge, it was the shortest press conference in ECB history, with reporters having no further questions after 25 minutes of questions. On the details, there was a little change in the decision but we attribute this to headline inflation being 2.0% in June.

Growth is perceived to be 'solid and broad based', with risks being broadly balanced. Draghi was at ease with the effects of a looming trade war. He also pointed to stabilising survey results, which all in all should be interpreted on the hawkish side.

The ECB was a little more confident on inflation and, in particular, domestic price pressures, which now are not only 'strengthening' but 'strengthening and broadening'. In particular, we find it interesting that Draghi mentioned negotiated wages several times as an underlying component of wage growth. Negotiated wages have recently crept higher and stood at 1.8% in March 2018 (most recent) but country heterogeneity prevails (for example, Germany 2.9% and 1.3%). Other than this, Draghi continued the previous assessment of the inflation outlook.

There were no new signals on the reinvestments to which Draghi said that 'they didn't discuss'. That means that we do not have more colour on smoothing the reinvestments (our expectation) or the deviating of the capital key (very unlikely in our view). They did not even discuss when to discuss the change (recall that in June, he said that 'important decision that we'll take in the months ahead'). In addition, he gave no further guidance on rates, as the English version 'at least through the summer of 2019' prevailed.

Limited market impact

Consequently, markets saw a relatively muted reaction today. In our view, this supports our view that we are currently in a carry-friendly environment.

Specifically for rates, Draghi gave no new colour on the reinvestment policy despite the 'operation twist' speculation ahead of the meeting. It could be seen as marginally negative for the long-end of the curve, which has performed in ASW-terms relative to the short end of the curve over the past month. However, in the end, we doubt many market participants had really thought that Draghi would discuss a change in reinvestments today and the impact should be modest. Draghi also clearly underlined that the 'capital key' remains the guiding principle. Hence, there is no support for speculation that an 'operation twist' could also mean bigger reinvestments in high debt countries at the expense of low-debt countries.

US Mnuchin: We’re very focused on the EU trade relationship

US Treasury Secretary Steven Mnuchin said the US is "very focused on the EU" on strengthening the trade relationship. He said that after Meeting of Trump and Juncker, there is an agreement in principal and the officials planned to move forward to "turn it into real agreement".

Both sides would immediately focus on steel and aluminum tariffs first "so that there can be no tariffs in either direction". The issue is expected to be resolved "very quickly". Mnuchin also said there is an outline already, "in agriculture, in chemicals, in medical devices, in industrial LNG" and so "we're going to make a lot of progress.

Regarding China, Mnuchin said "if they're willing to make serious changes just as the EU did yesterday, we'll negotiate with China any time."

And on NAFTA, he said "hopeful that we'll have an agreement in principal in the near future." He also noted that "whether it's one deal or two deals, so long as we get the right agreement, we're indifferent."

US Trade Representative Robert Lighthizer said that the US was close to reaching a broad agreement on NAFTA renegotiations. And he added that "we are in the finishing stages of achieving an agreement in principle that will benefit American workers, farmers, ranchers, and businesses." And talks were being done at an "unprecedented speed".