Sample Category Title

Silver: White Metal Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, Silver declined 1.38% against the USD and closed at USD15.42 per ounce, tracking losses in gold prices.

In the Asian session, at GMT0300, the pair is trading at 15.45, with silver trading 0.19% higher against the USD from yesterday’s close.

The pair is expected to find support at 15.34, and a fall through could take it to the next support level of 15.23. The pair is expected to find its first resistance at 15.60, and a rise through could take it to the next resistance level of 15.75.

The white metal is trading below its 20 Hr and 50 Hr moving averages.

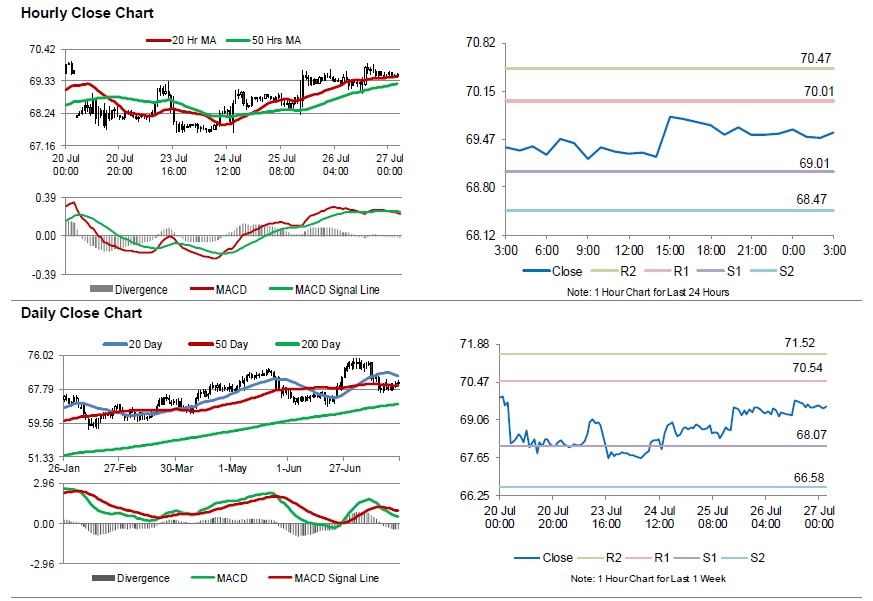

Crude Oil: Oil Trading Slightly Higher In The Asian Session

For the 24 hours to 23:00 GMT, Crude Oil rose 0.29% against the USD and closed at USD69.55 per barrel, supported by Saudi Arabia’s halt on transporting crude through the Red Sea waterway, falling US inventories and easing trade tensions between the US and EU.

In the Asian session, at GMT0300, the pair is trading at 69.56, with oil trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 69.01, and a fall through could take it to the next support level of 68.47. The pair is expected to find its first resistance at 70.01, and a rise through could take it to the next resistance level of 70.47.

Crude oil is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

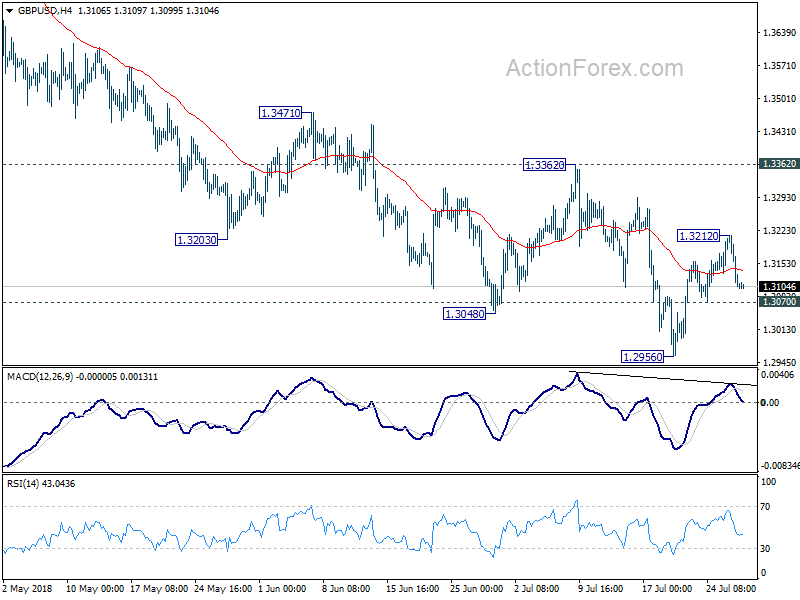

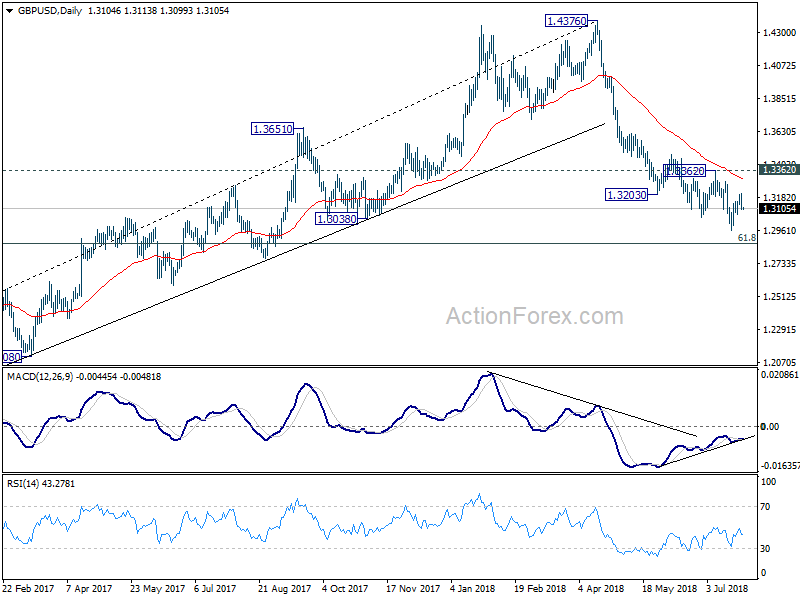

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3071; (P) 1.3143; (R1) 1.3180; More...

Intraday bias in GBP/USD remains neutral at this point, with focus on 1.3070 minor support. Break will indicate completion of rebound form 1.2956 and turns bias back to the downside for this low. Firm break there will resume larger decline from 1.4376 for 1.2874 fibonacci level next. On the upside, above 1.3212 will bring another rebound. But after all, price actions from 1.2956 are seen as a correction. Hence, upside should be limited by 1.3362 resistance to bring larger decline resumption eventually.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3362 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Yen Firm as JGB Yield Rally Persists, Dollar Looks into Q2 GDP

Yen remains generally firm today with help from strength in JGB yields. 10 year JGB yields hit as high as 0.113 and is now hovering at around 0.10. Nonetheless, Yen is outperformed by Canadian Dollar, which is lifted by NAFTA optimism. While the greenback is softer today, downside is relatively limited as it's supported by the surge in long yields overnight. The greenback will look into US Q2 GDP today. Euro, on the other hand, while recovers, is the weakest one for the week after lackluster ECB press conference. Slowed than expected French GDP growth provides no lift to the common currency too.

In other markets, DOW closed up 0.44% or 112.97 pts to 25527.07. However, thanks to Facebook, NASDAQ dropped -1.01% or -80.06 pts to close at 7852.18. At the time of writing, Asian markets are mixed with, Nikkei up 0.33% at 22661.73. Hong Kong HSI is downside -0.25%, China Shanghai SSE is down -0.16%. Singapore Strait Times is down -0.21%. US 10 year yield closed up 0.039 to 2.975, making a near high for the week. 30 year yield also gained 0.036 to 3.10. Both are on track for near term resistance at 3.009 and 3.140.

Technically, the dip in EUR/USD and GBP/USD yesterday puts near term minor support at 1.1574/1.3070 into focus. Break there will firstly indicate Dollar is regaining near term strength. Secondly, the development could spread dollar buying to other pairs. EUR/CHF's break of 1.1593 temporary low yesterday indicates resumption of recent fall from 1.1713. 1.1478 support is next target.

Mexico Guajardo has constructive and very positive NAFTA talk with US Lighthizer

Overnight, Mexican Economy Minister Ildefonso Guajardo had "constructive" and "very positive" talks with US Trade Representative Robert Lighthizer on NAFTA renegotiation. He added that both sides agreed to work towards hammering a deal in principal some time in August. And he said "We agree that in order to align the times and to eventually reach an agreement in principle, we should give ourselves the opportunity to move forward and try to bring this to fruition."

The final format of the agreement remains to be seen as both Canada and Mexico insists on trilateral deal while the US is known for pushing bilateral deals. Another sticky point is the US push for a "sunset clause" which the other two sides firmly disagree to.

US Mnuchin: We're very focused on the EU trade relationship

US Treasury Secretary Steven Mnuchin said yesterday the US is "very focused on the EU" on strengthening the trade relationship. He said that after Meeting of Trump and Juncker, there is an agreement in principal and the officials planned to move forward to "turn it into real agreement".

Both sides would immediately focus on steel and aluminum tariffs first "so that there can be no tariffs in either direction". The issue is expected to be resolved "very quickly". Mnuchin also said there is an outline already, "in agriculture, in chemicals, in medical devices, in industrial LNG" and so "we're going to make a lot of progress.

Regarding China, Mnuchin said "if they're willing to make serious changes just as the EU did yesterday, we'll negotiate with China any time." And on NAFTA, he said "hopeful that we'll have an agreement in principal in the near future." He also noted that "whether it's one deal or two deals, so long as we get the right agreement, we're indifferent."

US Trade Representative Robert Lighthizer said that the US was close to reaching a broad agreement on NAFTA renegotiations. And he added that "we are in the finishing stages of achieving an agreement in principle that will benefit American workers, farmers, ranchers, and businesses." And talks were being done at an "unprecedented speed".

Japan FM Aso wants G20 to promote infrastructure investments to boost growth next year

Japanese Finance Minister Taro ago said the G20 meeting in Osaka next year should play the role to " nip crises in the bud before they develop further." He also wanted G20 to focus "to promote investment in high-quality infrastructure to ensure economic growth."

Aso also noted that the G20 finance minister and central banker meeting last week discussed the downside risks to the global economy and reaffirmed the consensus over current issues. However, it should be noted that there was no consensus of the resolutions on US tariffs actions. And the situation could only worsen next year and protectionism rises and spreads.

IMF: Shift from high-speed to high-quality growth in China key for decades to come

IMF said in a report that China's economy continues to "perform strongly", with growth projected at 6.6% this year. But it also warned that the country is at a "historic juncture". The shift from "high-speed" to "high-quality" growth will determine China's "development path for decades to come". Risk of "near-term abrupt adjustment" was reduced by recent strong growth momentum and "significant financial de-risking progress". While there were accelerated rebalancing in some dimensions, "progress slowed" in many other dimensions. Also, while credit growth has slowed, "it remains excessive.

In the latest projections, IMF projected China GDP growth to be at 6.6% in 2018, slow to 6.4% in 2019, 6.3% in 2020, 6.0% in 2021, 5.7% in 2022 and 5.5% in 2023. Current account surplus as to GDP is projected to be at 0.9% in 2019, to close to 0.8% in 2019, at 0.8% in 2020, then slow to 0.7% in 2021, 0.5% in 2022 and 0.4% in 2023.

IMF also summarized the report in six charts. - China's strong GDP growth continues. - A focus on high-quality growth. - Credit growth has slowed but remains too fast. - China, a global digital leader. - Rebalancing efforts should be accelerated. -6. The benefits of faster reform.

ECB Draghi reiterated the policy path, rates to stay at current level at least through 2019 summer

Yesterday, ECB left interest rates unchanged as widely expected. Main refinancing rate is held at 0.00%, marginal lending facility rate at 0.25%, deposit facility rate at -0.40%. In the introductory statement to the press conference, ECB President Mario Draghi reiterated that the asset purchase target will be lowered to EUR 10B per month after September, subject to data confirmation to economic forecasts. The program will end after December. Interest rates are expected state at present levels through the summer of 2019.

Draghi also said latest stabilization in economic data is inline with forecasts and points to ongoing growth. Risk to growth outlook remains broadly balanced despite prominent threat of protectionism. Meanwhile, underlying inflation remains muted for now but is expected to rise gradually in medium term. And, ample degree of monetary policy stimulus is still needed at present.

In the Q&A section, Draghi acknowledged that the EU-US trade talks this week was a "good sign" but it's too early to assess the content of the agreement. Regarding question on Trump's attack on Eurozone's currency manipulation, Draghi said it's known that exchange rate isn't a policy target of the ECB.

On the data front

Japan Tokyo CPI rose 0.8% yoy in July, up from prior month's 0.7% yoy and beat expectation of 0.7% yoy. Australia PPI rose 0.3% qoq 1.5% yoy in Q2, slowed from prior 0.5% qoq, 1.7% yoy. French GDP rose 0.2% qoq in Q2, below expectation of 0.3% qoq. US Q2 GDP is the highlight of today. It's expected to show stellar 4.2% annualized growth.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3071; (P) 1.3143; (R1) 1.3180; More...

Intraday bias in GBP/USD remains neutral at this point, with focus on 1.3070 minor support. Break will indicate completion of rebound form 1.2956 and turns bias back to the downside for this low. Firm break there will resume larger decline from 1.4376 for 1.2874 fibonacci level next. On the upside, above 1.3212 will bring another rebound. But after all, price actions from 1.2956 are seen as a correction. Hence, upside should be limited by 1.3362 resistance to bring larger decline resumption eventually.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3362 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jul | 0.80% | 0.70% | 0.70% | |

| 01:30 | AUD | PPI Q/Q Q2 | 0.30% | 0.60% | 0.50% | |

| 01:30 | AUD | PPI Y/Y Q2 | 1.50% | 1.70% | ||

| 05:30 | EUR | French GDP Q/Q Q2 A | 0.20% | 0.30% | 0.20% | |

| 12:30 | USD | GDP Annualized Q/Q Q2 A | 4.20% | 2.00% | ||

| 12:30 | USD | GDP Price Index Q2 A | 2.30% | 2.20% | ||

| 14:00 | USD | U. of Mich. Sentiment Jul F | 97.1 | 97.1 |

Yen stays strong as 10 year JGB breaches 0.11, US yield limits dollar downside

Yen trades in a broadly firm tone today as helped by resilient in JGB yield. JGB 10 year yield hit as high as 0.113 today and is hovering around 0.10 at the time of writing. JGB yield could remain firm ahead of tomorrow's highlight anticipated BoJ meeting. There are speculations that BoJ is considering to tweak its monetary policy to probably target 10 year yield at 0.1%, rather than 0.0%. But so far, it's believed the discussions are preliminary. And, there is very likely chance of any announce of any sort that carries significance next week.

While Dollar is mixed this in Asia, it's trading as the third strongest one for the week, next to Canadian Dollar and Yen. The rebound in US treasury yields overnight reaffirmed underlying near term upside momentum. 10 year yield closed up 0.039 to 2.975, making a near high for the week. 30 year yield also gained 0.036 to 3.10. Both are on track for near term resistance at 3.009 and 3.140. The development will, at least, limit downside attempts of Dollar.

Asian markets are mixed today, following US. DOW closed up 0.44% or 112.97 pts to 25527.07. However, thanks to Facebook, NASDAQ dropped -1.01% or -80.06 pts to close at 7852.18. At the time of writing, Nikkei is up 0.33% at 22661.73. Hong Kong HSI is downside -0.25%, China Shanghai SSE is down -0.16%. Singapore Strait Times is down -0.21%.

IMF: Shift from high-speed to high-quality growth in China key for decades to come

IMF said in a report that China's economy continues to "perform strongly", with growth projected at 6.6% this year. But it also warned that the country is at a "historic juncture". The shift from "high-speed" to "high-quality" growth will determine China's "development path for decades to come". Risk of "near-term abrupt adjustment" was reduced by recent strong growth momentum and "significant financial de-risking progress". While there were accelerated rebalancing in some dimensions, "progress slowed" in many other dimensions. Also, while credit growth has slowed, "it remains excessive.

In the latest projections, IMF projected China GDP growth to be at 6.6% in 2018, slow to 6.4% in 2019, 6.3% in 2020, 6.0% in 2021, 5.7% in 2022 and 5.5% in 2023. Current account surplus as to GDP is projected to be at 0.9% in 2019, to close to 0.8% in 2019, at 0.8% in 2020, then slow to 0.7% in 2021, 0.5% in 2022 and 0.4% in 2023.

IMF also summarized the report in six charts.

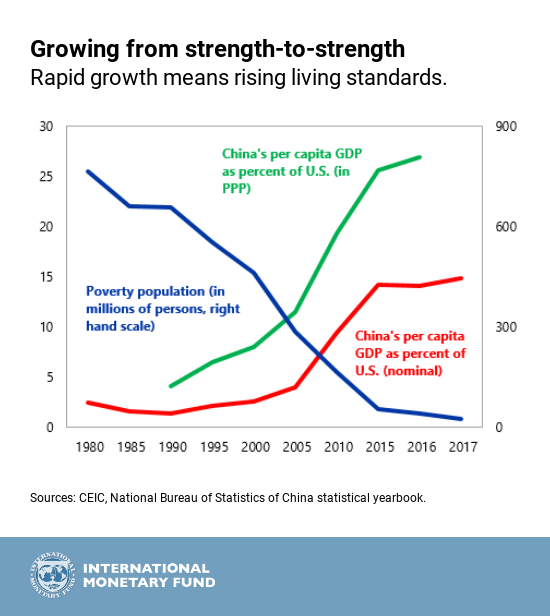

1. China's strong GDP growth continues. The country now accounts for one-third of global growth. Over 800 million people have been lifted out of poverty and the country has achieved upper middle-income status. China's per capita GDP continues to converge to that of the United States, albeit at a more moderate pace in the last few years.

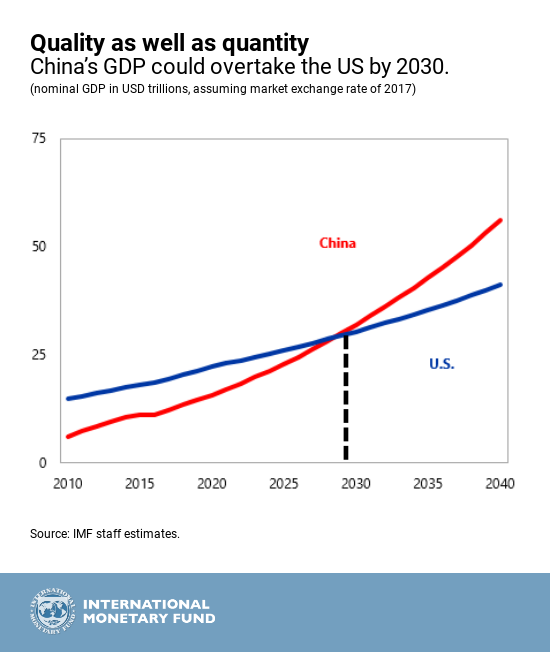

2. A focus on high-quality growth. China is at an historic juncture. After decades of high-speed growth, the government is now focusing on high-quality growth. The authorities will need to build on the existing reform agenda and take advantage of the current growth momentum to "fix the roof while the sun is shining." Key elements are: continuing to rein in credit growth, accelerating rebalancing efforts, increasing the role of market forces, fostering openness, and modernizing policy frameworks. Even with a gradual slowdown in growth, China could become the world's largest economy by 2030.

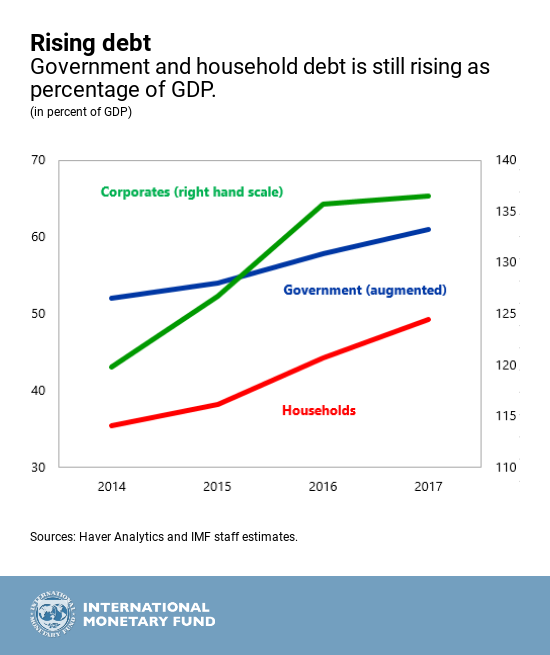

3. Credit growth has slowed but remains too fast. Despite the sharp rebound in nominal GDP and industrial profits, total nonfinancial sector debt still rose significantly faster than nominal GDP growth in 2017. While the corporate debt to GDP ratio has stabilized, government and especially household debt is rising, driven by continued strong off-budget investment spending and a rapid increase in mortgage and consumer loans. It may take determined actions over an extended period of time to address underlying vulnerabilities.

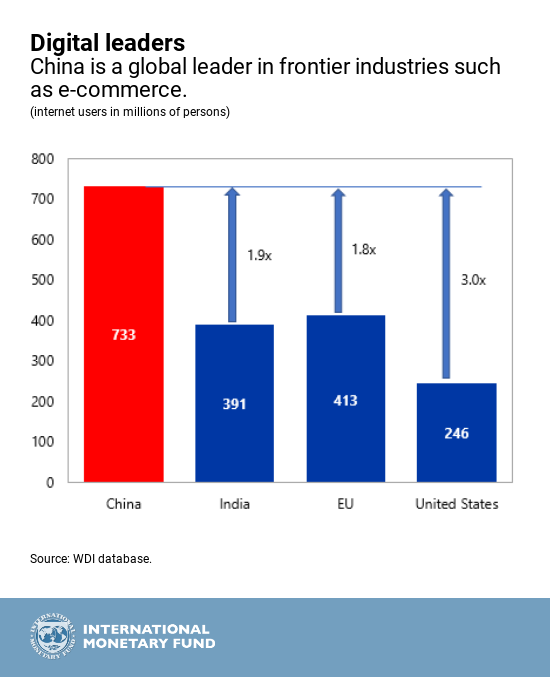

4. China, a global digital leader. China has around 700 million internet users and 282 million digital natives (internet users less than 25 years old) eager to adopt new technology. The massive scale of the Chinese market and a supportive regulatory and supervisory environment in the early years of digitalization made China a global leader in frontier industries such as e-commerce and fintech. Digitalization will continue to reshape the Chinese economy by improving efficiency, softening—but not reversing—slowing growth as the economy matures.

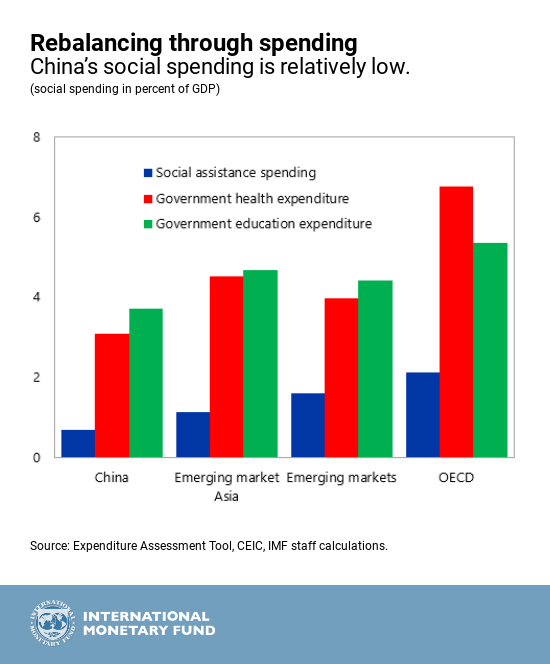

5. Rebalancing efforts should be accelerated. Increases in health, education, and social transfers—financed by taxes on income, property and carbon emissions—would support consumption, and reduce income inequality and pollution. A more comprehensive approach to structural reforms, such as increasing transfers to the regions most affected by overcapacity reduction or pollution control, could help address the tensions across rebalancing dimensions.

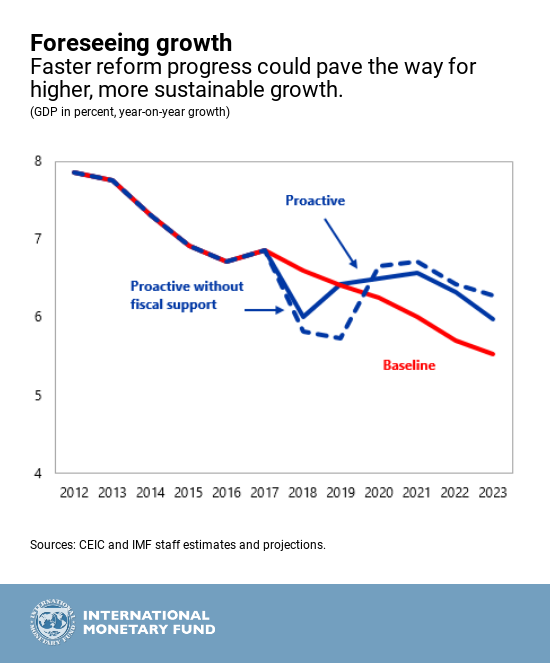

6. The benefits of faster reform. In the baseline, real GDP growth is projected at 6.6 in 2018, reflecting the lagged effect of regulatory tightening and softer external demand. Risks are tilted to the downside, with tightening global financial market conditions and rising trade tensions. If the authorities move more decisively to resolve the policy tensions now and focus on higher-quality growth and a greater role for the market, near-term growth would be weaker but longer-term growth would be stronger and more sustainable. An illustrative "proactive" scenario features faster reform progress, particularly state-owned enterprises (SOE) reform and resolving zombie firms, which also accelerates rebalancing from investment to consumption. If there is a risk of a too sharp slowdown, a temporary fiscal stimulus package with resources to support rebalancing could help cushion the near-term adverse impact.

Japan FM Aso wants G20 to promote infrastructure investments to boost growth next year

Japanese Finance Minister Taro ago said the G20 meeting in Osaka next year should play the role to " nip crises in the bud before they develop further." He also wanted G20 to focus "to promote investment in high-quality infrastructure to ensure economic growth."

Aso also noted that the G20 finance minister and central banker meeting last week discussed the downside risks to the global economy and reaffirmed the consensus over current issues. However, it should be noted that there was no consensus of the resolutions on US tariffs actions. And the situation could only worsen next year and protectionism rises and spreads.

Mexico Guajardo has constructive and very positive NAFTA talk with US Lighthizer

Overnight, Mexican Economy Minister Ildefonso Guajardo had "constructive" and "very positive" talks with US Trade Representative Robert Lighthizer on NAFTA renegotiation. He added that both sides agreed to work towards hammering a deal in principal some time in August. And he said "We agree that in order to align the times and to eventually reach an agreement in principle, we should give ourselves the opportunity to move forward and try to bring this to fruition."

The final format of the agreement remains to be seen as both Canada and Mexico insists on trilateral deal while the US is known for pushing bilateral deals. Another sticky point is the US push for a "sunset clause" which the other two sides firmly disagree to.

Market Morning Briefing: Dollar Yen Saw A Low Near 110.6 Yesterday

STOCKS

Rally in Dow (25527.07, +0.44%) continues while above 25250. Upside target for the near term is 26000. Note that there is a decent resistance in the 25800-26000 zone.

Dax (12809.23, +1.83%) has also moved up following the rise in Dow and could test upside resistance near 12900-13000 in the next few sessions. A fall from 13000 can be seen in the longer run. For now we do not expect a break beyond 13000.

Nikkei (22635.59, +0.22%) was almost stable yesterday with no major movement and could be found in the 22600-23000 region for a few more days. Whether it breaks above 23000 or faces a sharp rejection from 23000 would be important to watch to get some directional clarity for the longer run.

Shanghai (2889.03, +0.24%) is coming off from just above 2900. The 2900-2950 zone is an important resistance zone and while that holds, the index looks bearish towards 2850. Overall near tern trade could be seen in the 2850-2950 region for a few sessions.

Nifty (11167.30, +0.32%) closed below 11200 yesterday also and is likely to see some range-trade today. A short corrective fall is possible followed by resumption in the uptrend.

COMMODITIES

Nymex WTI (69.55) trades stable but has some scope of testing 71-72 on the upside before it could come off from there in the medium term. Overall the 3-day and weekly candles show that a bounce from current levels is possible in the longer term leading to overall bullishness; but we would have to wait and watch how far the current slow upmove take the price.

Brent (74.40) has been steadily rising from support at 71 and while that holds, near term upside is in place. The price can target 76 just now. Thereafter a dip is expected before it further moves higher towards 78-79 in the longer run.

Gold (1223.50) came off from levels just below 1240 and while the price remains below 1240, chances of a test of 1200 or lower is high. A break above 1240 is necessary to negate downside in the longer run. For now 1200-1240 region is likely continue for some more time.

Copper (2.8240) is testing immediate support on the daily charts and if that holds, the price could move up above 2.85. Failure to breach 2.85 would bring another downleg towards 2.75 or lower in the next week.

FOREX

Euro (1.1650): ECB's policy statement was perceived to be dovish, which thereby has resulted in Euro weakness. After testing resistance near 1.174 yesterday, Euro fell to a low near 1.164. It could test support on daily line chart near 1.16 in today's session. If US GDP comes out stronger than expected, Euro might break below 1.16 also. The next downside target in that case would be support near 1.145 on daily line chart.

Dollar Index (94.694): Dollar Index tested support on daily and 3 day candles yesterday near 94.08 and then bounced as the ECB continued being dovish. The US GDP release today is expected to show sharp acceleration in GDP in the 2nd quarter. If that happens, we might see Dollar Index test levels near 95.3-95.5 in today's session itself. A test of 96 next week seems possible.

Dollar Yen (110.98): Dollar Yen saw a low near 110.6 yesterday and has risen slightly from there. We again note important interim supports at 110.5 and 110.0 which might restrict the Dollar Yen's current downmove. However, next week's Bank of Japan meeting could change it all. If the BoJ decides to bring in even slight tightening to its loose monetary policy (of which, there are some rumours), then it might lead to strength in the Yen and hence, a break below 110.

Euro Yen (129.31): Euro Yen has broken support on daily candles near 129.4 but is still testing support on weekly line chart near 129.2. If it closes below 129.30-20 today, it might become bearish towards 128-127 in the next week. This could correspond with expected Euro weakness in the week ahead.

Pound (1.3106): Pound has again dipped from resistance near 1.32 on daily candles. If it closes below 1.3127 today (89 weeks MA), we might see the Pound drop towards support on 3 day candles near 1.29 next week. The broad bearish trend is expected to continue in the next week.

Dollar Rupee (68.665): Euro's weakening could prevent a break below 68.60 for USDINR and instead, it might continue the 69.10-68.60 range trade for another week. Immediate 1-2 sessions could be bullish for USDINR.

INTEREST RATES

Japanese 10 year yield (0.11%) has breached resistance on short-term chart near 0.09%. The bond markets now await the 30th-31st July Bank of Japan meet in which the BoJ might decide if it wants to modify its ultra-loose monetary policy. There is a chance that the BoJ might not try to bring down JGB yields by much; which thereby could lead to investment flows from US bonds to Japanese bonds. That, in turn, would raise US bond yields further.

The ECB yesterday maintained status quo and reiterated that key interest rates in the Eurozone would remain at present levels atleast through the summer of 2019. This dovish stance was more or less expected and hasn't lead to any significant movement in German yields. The German 10 year yield (0.4%) still looks like it could target 0.45%-0.50% on short term chart.

US 10 year yield (2.98%), 30 Year (3.10%), 5 Year (2.86%), 2 Year (2.69%):

The US 10 year yield continues moving higher in the 2.95%-3.00% resistance zone. Next week's BoJ meeting might just push the 10 year yield above 3%. Let's wait and watch.

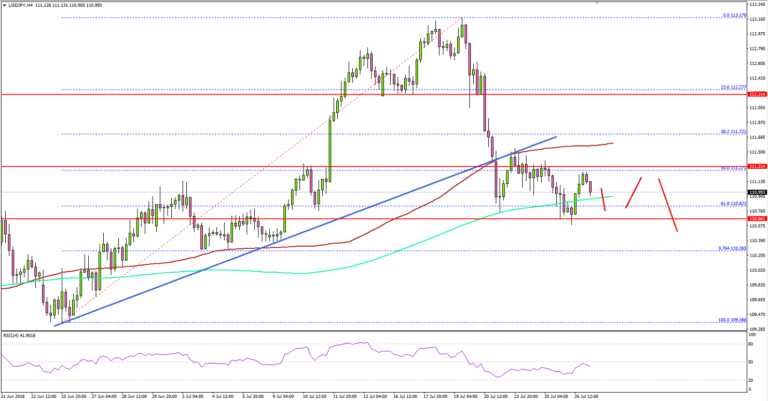

USD/JPY Likely To Extend Declines, US GDP Next

Key Highlights

- The US Dollar declined sharply after trading above 113.00 against the Japanese Yen.

- There was a break below a major bullish trend line with support at 111.50 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending July 21, 2018 increased to 217K.

- Today, the US Gross Domestic Product for Q2 2018 (Prelim) will be released, which is forecasted to increase 4.1%.

USDJPY Technical Analysis

The US Dollar was in a major uptrend before it faced a strong barrier near 113.00-113.10 against the Japanese Yen. The USD/JPY pair declined sharply and broke the 112.00 support area.

Looking at the 4-hours chart, the pair fell below the 112.40 and 112.00 support levels. During the decline, the pair broke a major bullish trend line with support at 111.50. The pair dipped below the 50% Fibonacci retracement level of the last wave from the 109.36 low to 113.17 high.

Moreover, there was a close below the 111.80 pivot level and the 100 simple moving average (red, 4-hours). However, the decline found support near the 110.60 level and the 61.8% Fibonacci retracement level of the last wave from the 109.36 low to 113.17 high.

On the downside, the next key support is around the 110.25 level, below which, the pair could trade towards the 110.00 level. On the upside, the previous support near 111.60/80 and the 100 SMA are likely to act as a resistances.

Only a successful close above the 111.80 and 112.00 resistance levels may perhaps initiate a fresh upward wave.

Recently in the US, the Initial Jobless Claims figure for the week ending July 21, 2018 was released by the US Department of Labor. The market was looking for a rise from 207K to 215K.

However, the actual result was on the lower side as there was a rise in claims to 217K. Moreover, the last reading was revised up to 208K. The report added that:

The 4-week moving average was 218,000, a decrease of 2,750 from the previous week’s revised average. The previous week’s average was revised up by 250 from 220,500 to 220,750.

The US Dollar started a short-term recovery due to the oversold conditions. However, downsides in EUR/USD and GBP/USD may possibly be limited.

Economic Releases to Watch Today

- US Gross Domestic Product Q2 2018 (Preliminary) – Forecast 4.1% versus previous 2.0%.

- US Personal Consumption Expenditures Prices for Q2 2018 (QoQ) (Prelim) – Forecast +2.0, versus +2.5% previous.

- US Core Personal Consumption Expenditures for Q2 2018 (QoQ) (Prelim) – Forecast +2.2%, versus +2.3% previous.