Sample Category Title

Silver Spot Aim @ 15.3000

Pivot (invalidation): 15.5000

Our preference Short positions below 15.5000 with targets at 15.3000 & 15.2300 in extension.

Alternative scenario Above 15.5000 look for further upside with 15.5800 & 15.6600 as targets.

Comment The RSI is mixed to bearish.

Gold Spot Under Pressure

Pivot (invalidation): 1228.50

Our preference Short positions below 1228.50 with targets at 1221.00 & 1218.00 in extension.

Alternative scenario Above 1228.50 look for further upside with 1230.50 & 1235.00 as targets.

Comment The RSI is mixed to bearish.

EUR/CHF Under Pressure

Pivot (invalidation): 1.1590

Our preference Short positions below 1.1590 with targets at 1.1565 & 1.1545 in extension.

Alternative scenario Above 1.1590 look for further upside with 1.1620 & 1.1640 as targets.

Comment A break below 1.1565 would trigger a drop towards 1.1545

EUR/GBP Turning Up

Pivot (invalidation): 0.8875

Our preference Long positions above 0.8875 with targets at 0.8895 & 0.8905 in extension.

Alternative scenario Below 0.8875 look for further downside with 0.8865 & 0.8855 as targets.

Comment The RSI calls for a new upleg.

Bitcoin/Dollar The Downside Prevails

Pivot (invalidation): 8175

Our preference Short positions below 8175 with targets at 7690 & 7560 in extension.

Alternative scenario Above 8175 look for further upside with 8330 & 8500 as targets.

Comment The RSI has broken down its 30 level.

The Curve Showed A Slight Bear Flattening

Markets

Yesterday, changes in US yields were limited (about 1 bp or less). The curve showed a slight bear flattening. US data were OK, leaving market expectations for a 4% + Q2 GDP growth intact. European yields declined slightly during the ECB press conference. ECB’s Draghi maintained a positive tone on the EMU economy, despite the potential negative impact of trade tensions. The ECB also confirmed its ‘Through Summer 2019 commitment’, suggesting that a rate hike is more likely after summer next year than earlier. Draghi also said that the ECB didn’t discuss the reinvestment policy. After a first soft reaction, European yields reversed part of the initial decline, with the 30 year slightly underperforming, probably due to the lack of new info on the ECB reinvestment policy (no confirmation on a lengthening of maturities). This morning, the BOJ offered to buy 10-y bonds at a yield of 0.1% after the interest moved temporary above this level. Japanese yields rose this week as markets speculate that the BOJ might amend its policy at next week’s meeting. Tokyo July inflation was slightly higher than expected at 0.9% Y/Y (0.5% core), but price rises remain very far away from the BOJ’s 2% target. Later today, the market focus will turn to the first estimate of US Q2 GDP growth. Solid growth of 4.2% Q/Q annualized is expected. So, the reference is already high. Even so, a figure near (or above consensus) might reinforce expectations that there is no reason for the Fed to slow the pace of quarterly rate hikes. Such a scenario should at least put a floor for US yields. The US 10-y yields might revisit/surpass the 3.0% barrier. A breach of this level might bring the cycle top (3.12%) again on the radar.

Yesterday, EUR/USD failed to sustain the gains recorded after the Trump-Juncker agreement on trade on Wednesday evening. The pair already lost some ground during the morning session. The decline accelerated during/after the ECB press conference as markets concluded that the ECB maintains a scenario of a rate hike only at the end of the Summer of 2019. The pair closed at 1.1643. USD/JPY succeeded a cautious intraday rebound (close at 111.23). This morning, the BOJ capped the rise in (10-y) yields. This move also blocked a further rise of the yen. USD/JPY stays in wait-and-see modus (111 area). Later today, the US Q2 GDP report will probably also be the key factor for USD trading. A strong report is already expected. Even so, 4% + growth might still reinforce the idea of ongoing policy divergence between the US and the EMU. Yesterday morning’s price action (after the Turmp-Juncker agreement) was also slightly disappointing from a euro point of view and suggests that the topside of the EUR/USD 1.15/1.1850 range is rather well protected. So, EUR/USD might still drift somewhat lower in this range. Strong growth in theory should also be positive for USD/JPY. However, the market reaction might be guarded ahead of next week’s BOJ meeting.

Yesterday, EUR/GBP hovered in the high 0.88 area. Sterling reversed a slight intraday gain after EU’s Barnier indicated that the EU couldn’t agree with the PM May’s new customs proposal. Today, there are again no UK eco data. So sterling traders will probably have to look for guidance from the broader euro and dollar moves.

News Headlines

China’s industrial profit growth slowed down to 20% in June, from 21.1% in May, due to a slowdown in factory production and China’s efforts to cut pollution and debt. Overnight, however, the IMF confirmed that the Chinese economy continues to perform strongly with growth expected at 6.6% this year, from 6.9% growth last year.

Leaders of the BRICS bloc have signed a declaration supporting an open and inclusive multilateral trading system under WTO rules, after a summit held in South Africa yesterday. The bloc wants to avoid escalating trade tensions to derail a global upswing that is already losing momentum.

Tokyo’s core consumer prices, a leading indicator for the nation, rose for a second time in a row to 0.8% in July from a year earlier, while 0,7% was expected. The acceleration, however, is still far from the Bank of Japan’s 2% inflation target who is said considering to tweak its policy framework at next week’s BOJ meeting.

Cautious Trading Session In Asia Ahead Of Upcoming US GDP Data

General Trend:

- Asian equity markets trade mixed, in line with Thursday’s US session

- BHP rises over 2% after agreeing to sell US shale assets for higher than speculated amount

- Nomura declines by over 5%, reported lower Q1 profits

- Australia’s AMP drops over 3% on H1 guidance

- Japan July Tokyo CPI higher than expected ahead of next week’s BoJ policy meeting (July 30-31st)

- 10-year JGB yields trade above 0.10%, BoJ again acts

- China PBoC skipped daily open market operation for the 6th straight session, drained liquidity for the week

- China PBoC set the yuan weaker on the session

- The Yuan currency has moved relatively quickly vs the US dollar in recent weeks, according to an IMF official

- New Zealand July Consumer Confidence hits lowest level since 2016

- Upcoming US Q2 Advance GDP in focus

- Japanese companies which may report earnings later today include Komatsu, Hitachi, Ricoh, Seiko Epson, NGK Insulator, Tokyo Gas, GungHo Online Entertainment and Yahoo Japan.

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.4%

- ASX 200 Telecom index +1.4%, Energy +1.2%, Consumer Discretionary +1%, Utilities +1%, Resources +0.9%, Financials +0.8%, REIT +0.7%

- (AU) AUSTRALIA Q2 PPI Q/Q: 0.3% V 0.5% PRIOR; Y/Y: 1.5% V 1.7% PRIOR

- (AU) Australia to sell A$1.0B in Nov 2029 bonds on Aug 1st

- (NZ) New Zealand ANZ Jul Consumer Confidence Index: 118.4 v 120.0 prior; m/m: -1.3% v -0.8% prior (lowest level since 2016)

China/Hong Kong

- Shanghai Composite opened -0.1%, Hang Seng -0.2%

- Hang Seng Services index -0.8%, Utilities -0.5% Financials -0.2%; Property/Construction +0.4%

- (CN) China PBoc sets yuan reference rate at 6.7942 v 6.7662 prior

- (CN) China Jun Industrial Profits Y/Y: 20.0% v 21.1% prior

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 6th consecutive session

- (CN) China Official: China Govt has a plan to retaliate against increases in US tariffs regardless of the volume of goods targeted - US press

- (CN) China to plan to establish asset restructuring fund for state-owned coal companies in H2 - Chinese Press

- (CN) Approx 50% of China company Hong Kong IPOs in July were under-subscribed - Chinese Press

Japan

- Nikkei 225 opened +0.3%

- TOPIX Marine Transportation index +0.9%, Iron & Steel +0.6%; Securities -3.4%

- (JP) JAPAN JUL TOKYO CPI Y/Y: 0.9% V 0.7%E; EX-FRESH FOOD (CORE): 0.8% V 0.7%E (both figures were the highest since March)

- (JP) BOJ AGAIN CONDUCTS A FIXED-RATE JGB PURCHASE OPERATION: Offers to buy unlimited amount of 10-year JGBs at 0.100% v 0.11% prior (2nd operation this week)

- (JP) Japan Finance Ministry (MOF): Confirms Masatsugu Asakawa to remain as FX Chief for 4th year; Shigeaki Okamoto named as new top bureaucrat for the Finance Ministry

- (JP) Japan Fin Min Aso: At recent G-20 discussed downside risks to the global economy, reaffirmed commitments on foreign exchange

South Korea

- Kospi opened +0.1%

- (KR) North and South Korea agree to hold military talks on July 31st - Korean press

- Hynix Semiconductor [000660.KR]: Announces KRW1.83T stock buy back; To spend KRW3.49T to build additional production line in South Korea

North America

- US equities ended mixed: Dow +0.4%, S&P500 -0.3%. Nasdaq -1%, Russell 2000 +0.6%

- S&P500 Utilities +1.1%, Energy +1.1%; Telecom -3.8%, Tech -1.5%

- (US) Pres Trump: believe the GDP numbers tomorrow will be terrific

Europe

- BP [BP.UK]: Confirms to acquire BHP US assets; raises dividend 2.5% to $0.1025 (first dividend increase in 15 quarters); Planning up to $5-6B in additional divestments to fund share buybacks of up to $5-6B over time.

Levels as of 01:30ET

- Nikkei 225, +0.3%, ASX 200 +0.8%, Hang Seng -0.3%; Shanghai Composite -0.1%; Kospi +0.1%

- Equity Futures: S&P500 flat; Nasdaq100 +0.2%, Dax +0.3%; FTSE100 +0.1%

- EUR 1.1637-1.1656 ; JPY 110.91-111.26; AUD 0.7372-0.7395 ;NZD 0.6774-0.6788

- Aug Gold -0.2% at $1,223/oz; Sept Crude Oil flat at $69.64/brl; Sept Copper +0.5% at $2.822 /lb

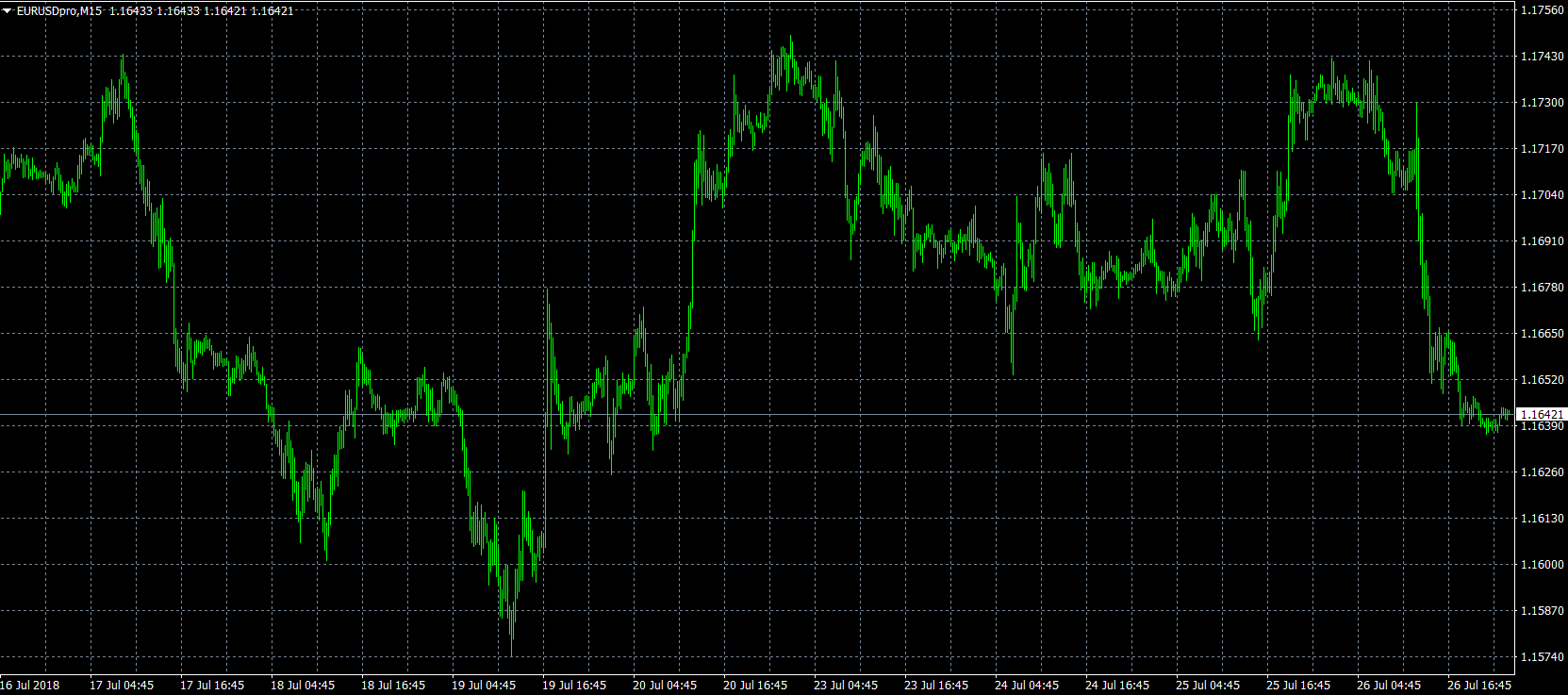

EURUSD Intraday Bearish Below 1.1650 Level

The euro has erased weekly gains against the US dollar, after ECB President Mario Draghi confirmed that the European Central Bank will leave eurozone rates unchanged until at least September 2019. The EURUSD pair is likely to weaken even further if price continues to trade below the key 1.1650 support level. Sellers will likely target a strong break below the 1.1600 level, while buyers will try to move price above the 1.1680 resistance level.

The EURUSD pair is intraday bearish while trading below the 1.1650 level, key support is found at the 1.1600 and 1.1540 levels.

If the EURUSD pair holds above the 1.1650 level, buyers will likely target the 1.1680 and 1.1700 resistance levels.

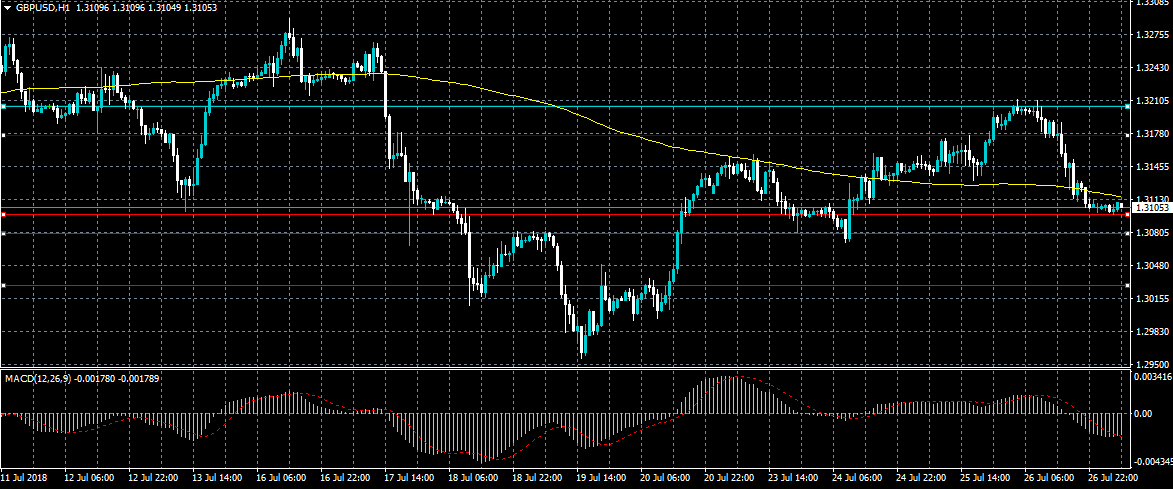

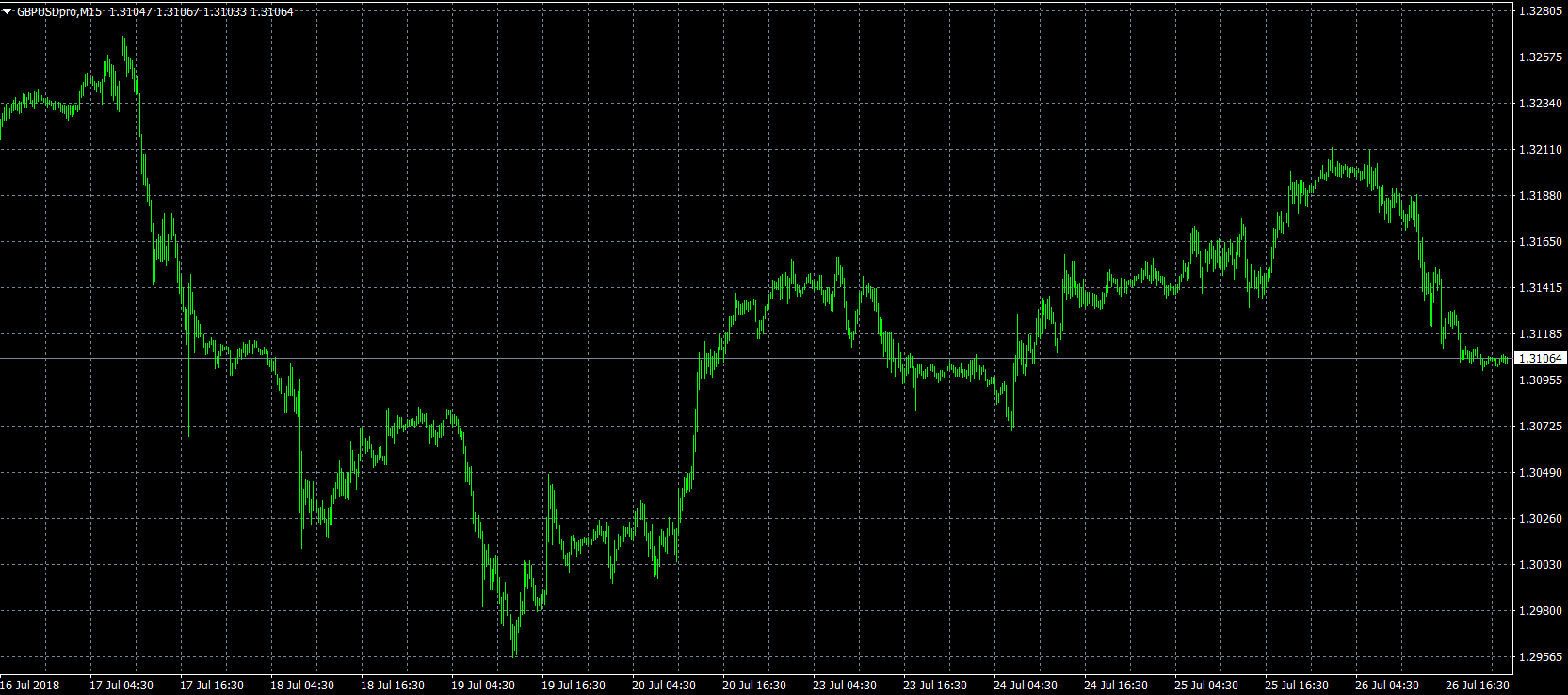

GBPUSD Further Bearish Below 1.3101 Level

The British pound has fallen sharply lower against the US dollar after Chief EU Negotiator Michel Barnier rejected a key part of the United Kingdom’s Brexit trade proposal. The GBPUSD pair is now testing key support and is likely to weaken even further if the price falls below the 1.3101 level. Sellers will try to target the 1.3000 support level, while buyers will try to stabilize price back above the 1.3177 level.

The GBPUSD pair is strongly bearish while trading below the 1.3101 level, key support is now found at the 1.3050 and 1.3000 levels.

If the GBPUSD pair holds above the 1.3101 level, buyers may test towards the 1.3177 and 1.3211 resistance levels.

US GDP On Deck For Friday

US gross domestic product (GDP) – the broadest measure of economic health – will headline an active session in global finance on Friday. The report will provide key insight to policymakers, business leaders and investors about the status of the world’s largest economy.

Action begins at 06:00 GMT with a report on German import prices. The import price index is forecast to rise 0.2% for June, which translates into a year-over-year gain of 4.4%.

Forty-five minutes later, the French government will report on national consumer spending for the month of June. Spending at the consumer level likely rose 0.6% last month.

Over the next hour, reports on Spanish retail sales and Italian producer inflation will make their way through the financial markets. At the time of writing, there was no consensus on how either of these data sets will pan out.

The start of North American trade will feature a speech by James Bullard, who serves as President of the Reserve Bank of St. Louis. Bullard is not a member of the Federal Open Market Committee (FOMC but could provide insight on the health of the domestic economy and the path of monetary policy.

Bullard’s speech is set to begin 10 minutes before the Department of Commerce issues its preliminary estimate of first quarter GDP. The world’s largest economy under President Donald Trump is forecast to surge 4.1% year-over-year, more than double the rate of the first quarter.

The report will also contain the quarterly core personal consumption expenditures (PCE) index, which is the Fed’s preferred measure of inflation. The core PCE index likely slipped to 2.2% in the second quarter compared with 2.3% in January-March.

At 14:00 GMT, the University of Michigan will release the final consumer sentiment index for July.

EUR/USD

Europe’s common currency swung sharply lower on Thursday as the US dollar regained momentum. EUR/USD fell from a high near 1.1760 all the way back down to the mid-1.16 range. The pair now sits at 1.1644, where it faces immediate support at 1.1575, the low from 19 July. On the opposite side of the spectrum, immediate resistance is located at 1.1800.

GBP/USD

Cable’s stint at one-week highs was short-lived, as prices fell more than 100 pips on Thursday all the way back down to the low 1.3100 US region. At the time of writing, GBP/USD was trading at 1.3107. The pair faces immediate support at 1.3070, the current low for the week. On the flipside, immediate resistance is located at 1.3266.

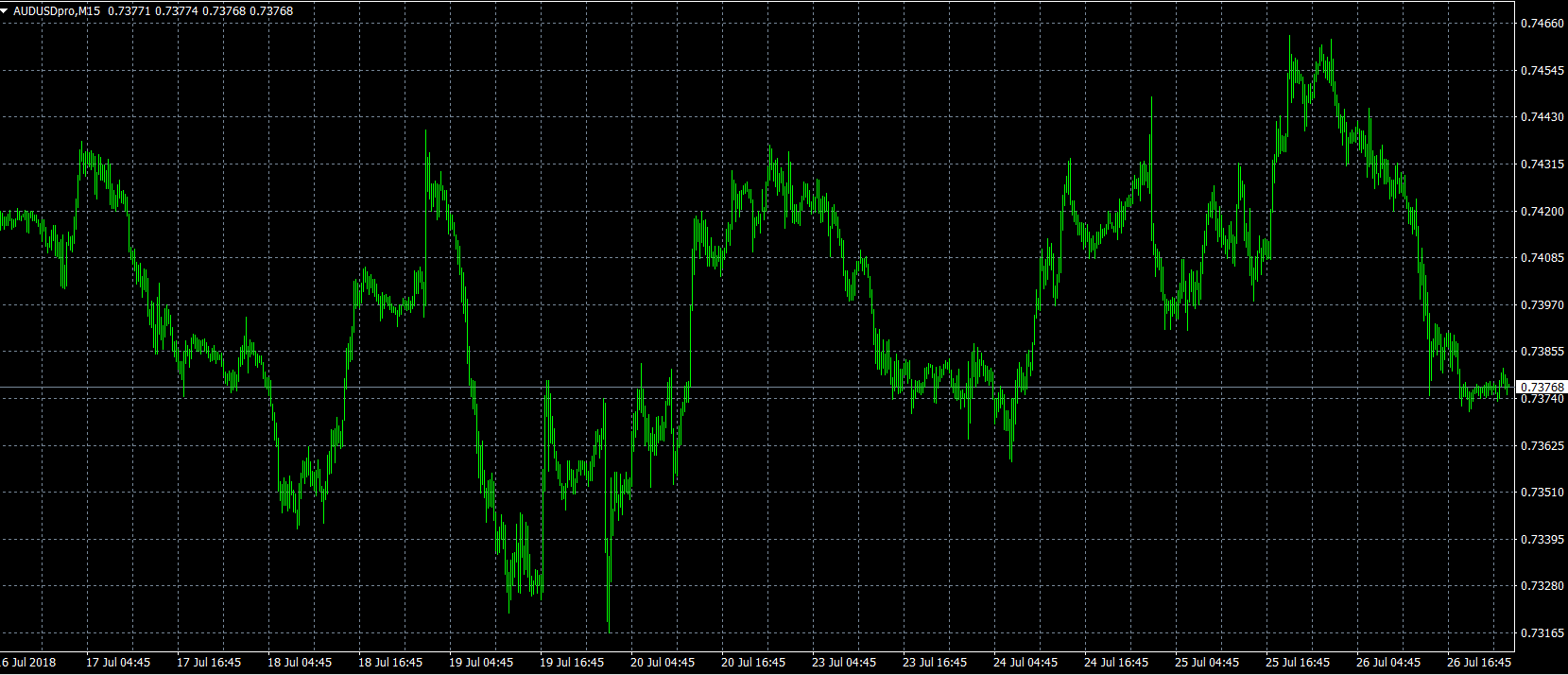

AUD/USD

The Australian dollar pivoted sharply lower on Thursday, as prices recoiled from multi-week highs. After peaking at 0.7461, the AUD/USD exchange rate plunged all the way back down to 0.7378, where it now trades. Immediate support is located at 0.7370. Resistance is likely up ahead at 0.7445.