Sample Category Title

XAU/USD Forms Triangle

Downside risks prevailed on Thursday, thus guiding Gold past the 55-, 100– and 200-hour SMAs and down to 1,223.00. This has revealed the existence of an ascending triangle. The upper boundary of this pattern is a weekly resistance at 1,235.00, while lower one is a channel line.

In line with this pattern, the pair should reverse back to the upside and test the aforementioned resistance in this session. However, the strong cluster at 1,230.00 could prevent the yellow metal from appreciation. In this scenario, there is no support until the monthly S2 at 1,206.00.

USD/CAD Preparing For A Breakout

The USD/CAD has formed a consolidation triangle within the boundaries of W L4 support. We can even spot a bullish divergence at the bottom. Breakout might happen at the breakout of 1.3060-70 zone towards 1.3095-1.3114. If the price gets there it will either bounce or continue further up. Above 1.3115 we could see 1.3145.

If there is no breakout look for a break below 1.3040 towards 1.3008.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Euro Slips after ECB Statement, US GDP Next

EUR/USD has steadied in the Friday session, after recording considerable losses on Thursday. Currently, the pair is trading at 1.1646, up 0.03% on the day. On the release front, French indicators missed their forecasts. French GDP for the second quarter dropped 0.2%, short of the estimate of 0.3%. This marked the lowest gain since Q3 in 2016. French consumer spending dropped sharply 0.1%, short of the forecast of 0.6%. In Germany, import prices dropped 0.5% in June, down sharply from the 1.6% gain a month earlier. Still, this beat the estimate of 0.5%. The U.S will release Advance GDP for Q2, with the markets expecting a strong gain of 4.2%. As well, UoM Consumer Sentiment is forecast to drop to 97.1 points.

There were no surprises from the ECB, which made no changes to monetary policy at its Thursday meeting. The main refinancing rate remains at 0.0%, which has been pegged since January 2016. In a policy statement, policymakers reiterated that rates would remain at current levels “through the summer of 2019”, and “as long as necessary to boost inflation to the target of just under 2.0%. There has been some discussion as to the exact meaning of “through the summer”, but what is clear is that the ECB plans to keep rates at a flat 0.00% after winding up its bond-purchase scheme at the end of the year. This weighed negatively on the euro, which dropped 0.07% on Thursday. The exact timing of a rate hike will depend on the strength of the eurozone economy and inflation levels – if the second half of 2018 is marked by stronger growth and higher inflation, there will be pressure on the ECB to raise rates earlier rather than later in 2019.

Investors remain concerned over global trade tensions, as tit-for-tat tariffs between the U.S and its trading partners have been weighing on the euro. However, the mood brightened on Wednesday, as the U.S. and the European Union surprised the markets, talking “reconciliation” rather than “retaliation”. On Wednesday, EU Commission President Jean-Claude Juckner met with President Trump, and the two leaders agreed to take concrete steps to eliminate tariffs and improve the trade relationship between the U.S and the EU, which has been battered in recent weeks. President Trump agreed to hold back on any further tariffs while talks are ongoing. This is a major concession from Trump, who just last week had threatened to impose tariffs on European car imports. U.S tariffs on European aluminum and steel will remain in place, but Juckner pointed out that the U.S has agreed to reassess these measures. The surprise agreement eases fears of a full-blown transatlantic trade war and the markets are hopeful that the flexibility the U.S has shown to the EU will also apply towards China and the NAFTA talks with Canada and Mexico.

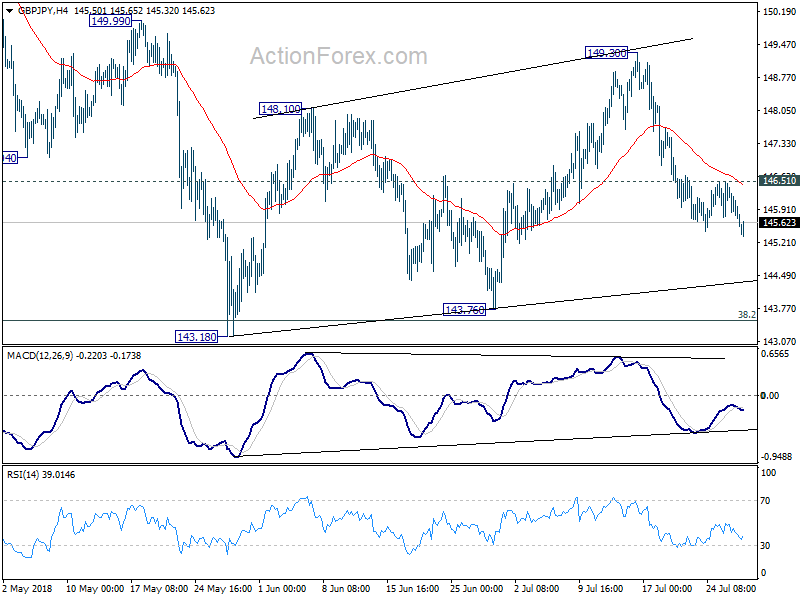

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.53; (P) 146.04; (R1) 146.31; More...

Intraday bias in GBP/JPY remains on the downside for 143.18/76 support zone. Break will resume larger decline from 156.59. On the upside, though, above 146.51 minor resistance will turn bias back to the upside for 149.30/99 resistance zone instead.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

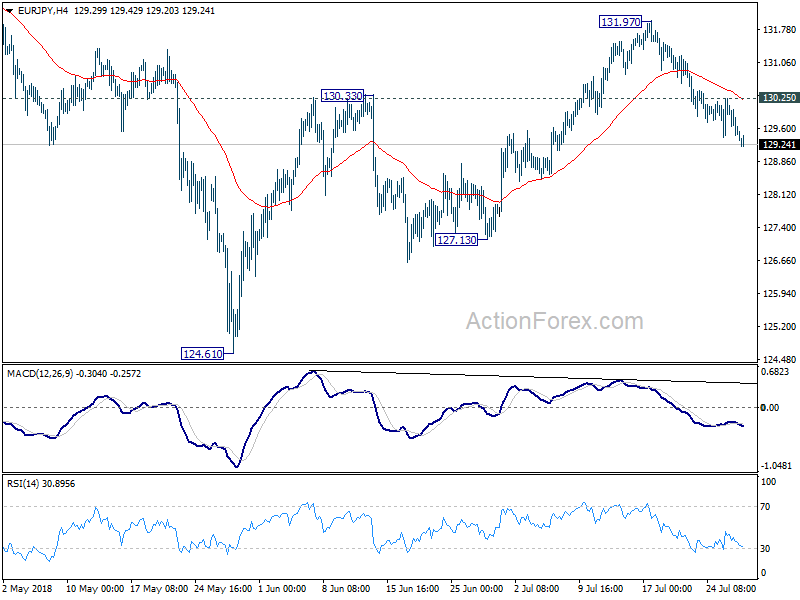

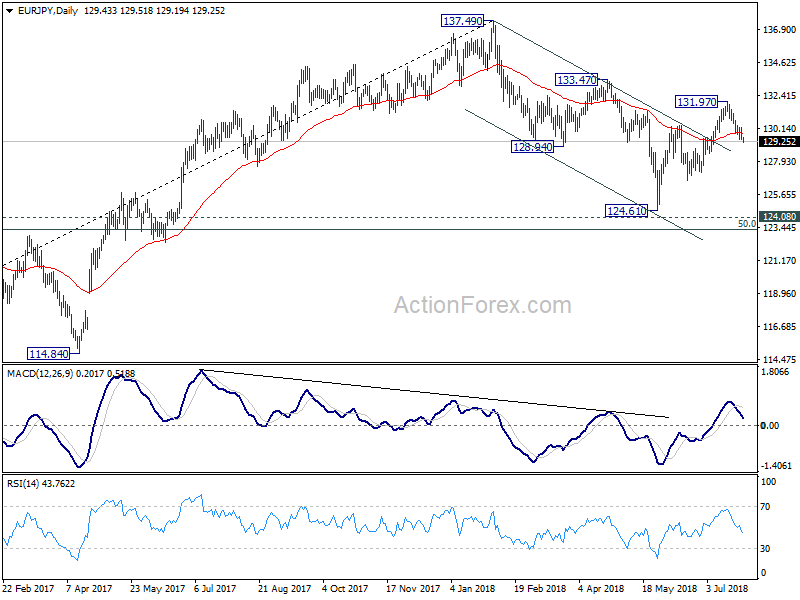

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.18; (P) 129.76; (R1) 130.09; More....

EUR/JPY's decline from 131.97 is in progress and intraday bias stays on the downside. As noted before, the rebound from 124.61 should have completed with three waves up to 131.97 already. Deeper fall should be seen to 127.13 support first. Break will confirm this bearish case and target 124.61 low. On the upside, above 130.25 minor resistance will turn bias to the upside for retesting 131.97 resistance instead.

In the bigger picture, the strong break of channel resistance from 137.49 suggests that the decline from there has completed. The three wave structure suggests that it's a correction. With 124.08 key resistance turned support intact, medium term bullishness is also retained. Break of 133.47 will affirm this bullish case and target 137.49 and above. This will now be the favored case as long as 127.13 support holds.

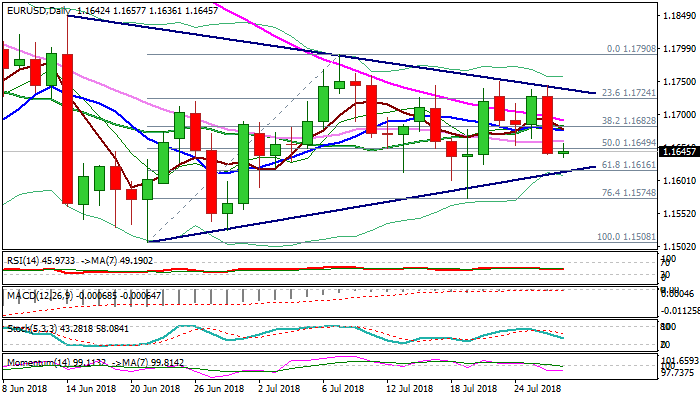

EURUSD Outlook: Bearish Pressure After Dovish ECB Could Increase On Upbeat US GDP Data

The Euro is consolidating after strong fall on Thursday when it fell 103 pips after dovish ECB disappointed traders. Strong fall and close below the base of thick daily cloud, following unsuccessful cloud penetration, was bearish signal. Fresh bears pressure key support at 1.1616 (Fibo 61.8% of 1.1508/1.1790 recovery / triangle support) break of which would generate strong bearish signal and confirm negative near-term outlook for test of supports at 1.1574 (19 July spike low) and 1.1527 (28 June trough) Daily techs are in firm bearish configuration and support scenario. Better than expected German Import data, released earlier, provided little support, with focus turning towards release of US Q2 GDP data, due later today. US Gross Domestic Product is forecasted for strong rise in Q2 (4.1% vs 2.0% in Q1) with upbeat release to boost dollar and increase bearish pressure on the single currency, which may revisit key supports at 1.1508 (21 June / 29 May lows).

Res: 1.1662. 1.1691. 1.1750. 1.1790

Sup: 1.1636. 1.1616. 1.1574. 1.1527

USD Grows On High GDP Expectations

The single currency is traded near weekly lows against the dollar, getting under pressure after maintaining the soft tone of the ECB during the regular meeting. The EURUSD sank to 1.1640 on Thursday, losing about 0.9% after Draghi’s speech. The acceleration of the inflation and the promise to keep the rates unchanged reduce the real (minus inflation) return on investment to European assets. Such softness of the ECB’s position caused a new wave of pressure on the common currency and European bonds.

Trading on the stock markets on Friday is very calm, the markets show mixed dynamics near the opening levels.

Oil continues its recovery and trades around $75 for Brent. The reason for the growth is the restriction of Saudi Arabia’s oil shipment across the Red Sea after its two tankers had been attacked.

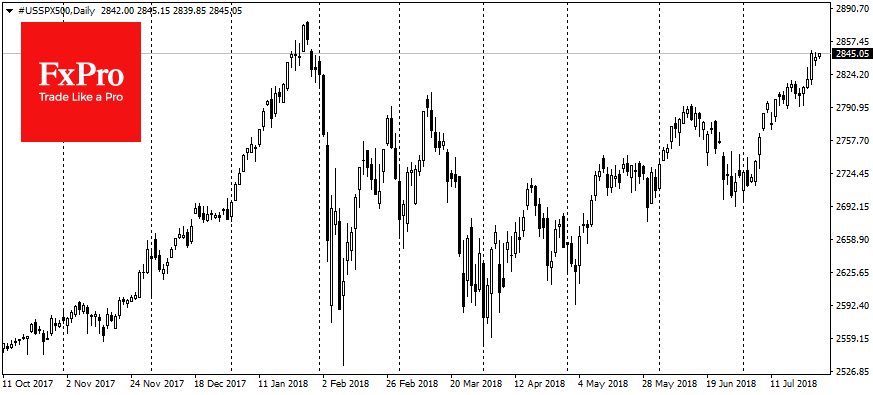

The futures for S&P500 has added 0.1% since the beginning of Friday. For July, it grew by more than 5% and now is only 1% below the historical peaks achieved in January this year. Then the markets had an impressive bull run as the economy significantly surpassed the expectations. Many economic indicators in the United States remained at a high level, but the expectations increased.

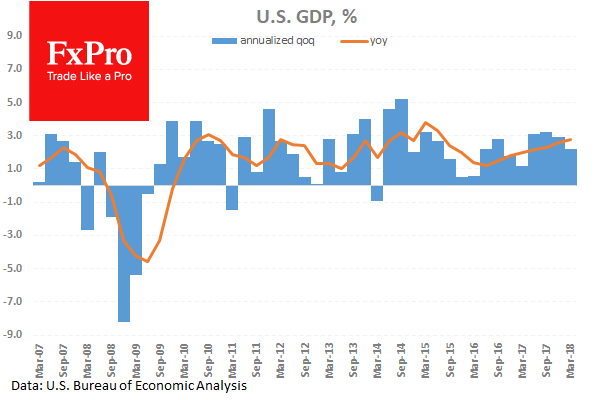

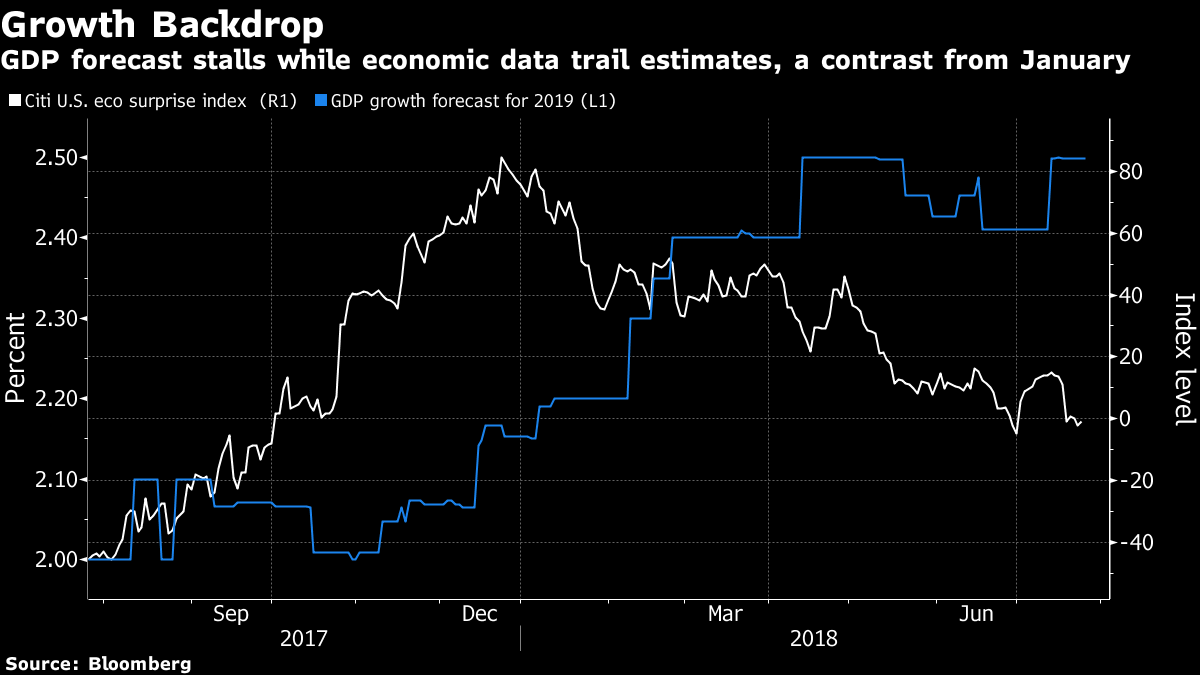

The main event for today will be the first US GDP estimate for the 2nd quarter. This figure is expected to exceed 4%, which will be the highest value in almost 4 years. These are very high expectations of the market. Since the beginning of the year the index of economic surprises in the U.S. (the difference between the expectations and the fact) has declined significantly and approached to the zero mark. This may have a negative impact on the dynamics of the market, which often moves at the expense of such a difference between expectations and actual numbers.

We are coming into a period when the threats of tariff introduction and the first fruits of realized measures could influence the economic data. At this stage, we are likely to see an increase in the business activity of producers who will rush to buy the goods which are potentially subject to the tariffs influence. We have seen this pattern in the China trade figures this month. However, these indicators can later fall considerably

Euro Drops On ECB Optionality, US Q2 GDP On The Radar

Here are the latest developments in global markets:

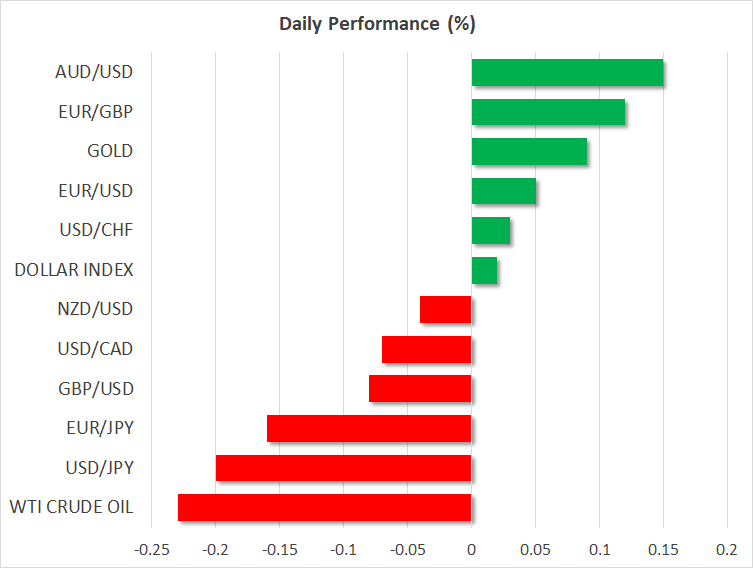

FOREX: The US dollar index – which tracks the greenback’s performance against a basket of six major currencies – was practically unchanged on Friday, after it posted considerable gains in the previous session. The surge came as the currency with the heaviest weight in that index by far – the euro – tumbled following the ECB policy meeting.

STOCKS: US markets closed mixed yesterday, as an 18.96% plunge in Facebook’s share dragged down the tech-heavy Nasdaq Composite (-1.01%) and to a lesser extent the S&P 500 (-0.30%). The Dow Jones, meanwhile, managed to gain 0.44%, as Facebook is not a constituent stock in that index. Futures suggest the Dow, S&P, and Nasdaq 100 are set to open higher today, albeit not significantly so. Asia was mixed as well, with both of the major Japanese indices – the Nikkei 225 and the Topix –advancing, but the Hang Seng in Hong Kong dropping marginally. European benchmarks were set to open higher across the board today, according to futures.

COMMODITIES: Oil prices were somewhat lower on Friday, with WTI and Brent dropping by 0.23% and 0.11% respectively, both giving back some of the gains they posted yesterday. News that Saudi Arabia halted shipments of crude through a shipping lane in the Red Sea kept a floor under prices. Interestingly, there was little market reaction to reports in Australian press overnight that the US is prepared to bomb Iran’s nuclear facilities, perhaps as early as next month. In precious metals, gold is up by a marginal 0.08% on Friday, hovering just above the $1,244 per ounce mark. The dollar-denominated yellow metal dropped notably yesterday as the US currency regained some ground.

Major movers: Draghi 'keeps options open', euro drops

All eyes were on the ECB meeting yesterday, which even though did not provide much new in the way of forward guidance, still managed to generate a decent reaction in the euro. The single currency initially spiked a little higher as President Draghi’s press conference got underway, after he noted the Bank remains confident on the inflation outlook amid a pick-up in wage growth. However, the euro soon gave back all its gains to trade lower overall, after the ECB chief said markets had understood correctly the message that interest rates will remain unchanged at least 'through the summer' of 2019.

He implied that current market pricing was close to where it should be, which investors took as a dovish signal. Draghi was essentially applauding the fact there is some uncertainty involved with current pricing, highlighting that the Bank wants to keep its options open with regards to the timing of the first hike. The probability for a 10bps rate increase in September 2019 was around 70% prior to the meeting, EONIA swaps suggested. It dropped to 58% in the aftermath.

The dollar managed to pare all the losses it had posted earlier in the day to trade much higher, drawing strength both from the tumble in the euro and from another uptick in longer-term US Treasury yields. The 10-year US bond yield touched 2.97%, rendering the greenback more attractive from a relative rates perspective, amid speculation for a strong US GDP print for Q2, due out later today.

Meanwhile, yen bulls remain in the driver’s seat, with the Japanese currency trading a little higher against the dollar, euro, and pound on Friday. The theme that the Bank of Japan may make hawkish adjustments to its ultra-loose policy framework as early as at next week’s policy meeting remains at the forefront.

In emerging markets, the Turkish lira took another hit yesterday, after US President Trump tweeted his nation 'will impose large sanctions on Turkey' unless it freed an American pastor that has been detained for nearly two years on terrorism charges.

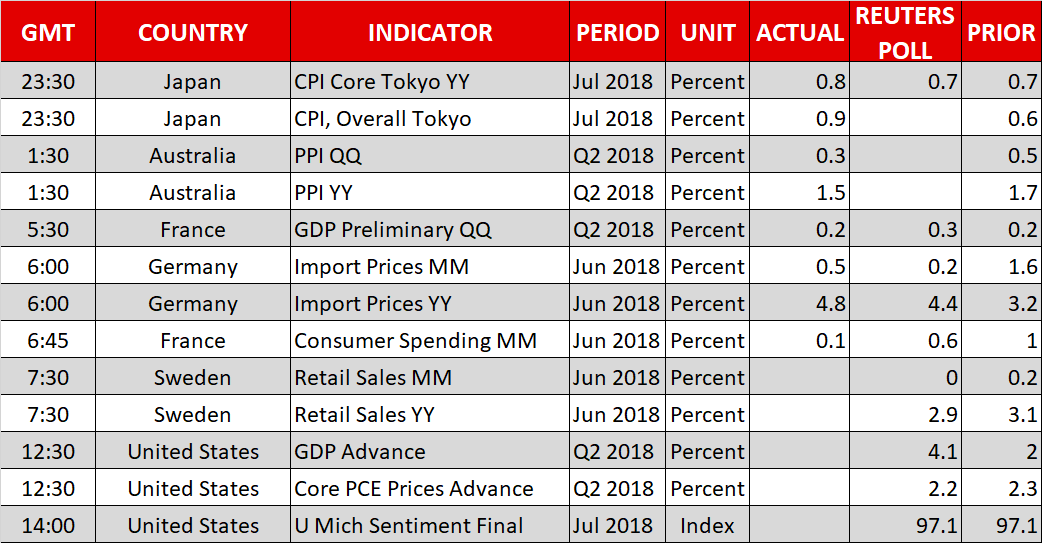

Day ahead: US GDP firmly in focus

The advance estimate of US GDP growth for the second quarter of the year is undoubtedly the highlight out of Friday’s calendar.

Retail sales data out of Sweden are due at 0730 GMT, bringing krona pairs to the fore.

The initial estimate of US GDP growth during Q2 will be made public at 1230 GMT. The economy is expected to have expanded by 4.1% on an annualized basis, a far higher pace relative to Q1’s 2.0% and at its highest since Q3 2014. Fed funds futures currently project that market participants have fully priced in an additional rate hike by the US central bank in 2018, while they assign a 66% probability for a second one. A more upbeat reading than forecasted is likely to push those odds even higher, consequently boosting the greenback; the opposite holds true as well. Meanwhile, advance data on core PCE prices for Q2 will be released alongside numbers on economic growth.

Also out of the US will be the University of Michigan’s final survey on consumer sentiment for the month of July; the relevant reading is expected to be confirmed at 97.1, below June’s 98.2.

Mexican Economy Minister Ildefonso Guajardo’s visit to Washington will conclude today, with any updates on the future of NAFTA to be closely watched.

In equities, Chevron, Exxon Mobil, Merck & Co and Twitter will be releasing quarterly earnings on Friday.

Oil traders will be keeping an eye on the Baker Hughes count of active US oil rigs due at 1700 GMT.

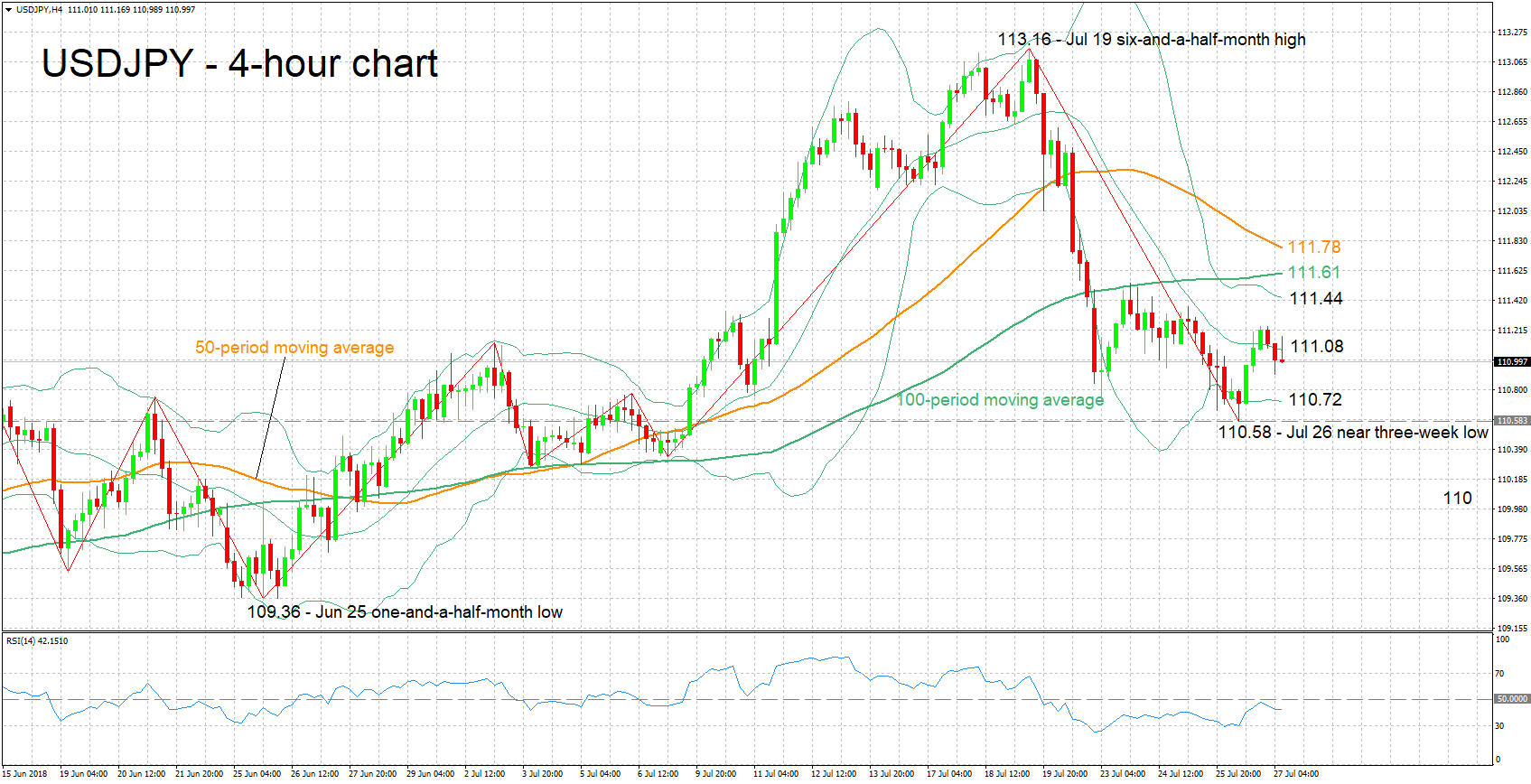

Technical Analysis: USDJPY looking neutral in the short-term

USDJPY has eased after a previous rise from a near three-week low of 110.58 touched on Thursday. The RSI is moving sideways at the moment, projecting a neutral picture in the short-term.

A better-than-anticipated GDP reading out of the US is likely to boost the pair. Given a break above the middle Bollinger line (a 20-period moving average line) at 111.08, the pair may next meet resistance from the region around the upper Bollinger band at 111.44. Notice that the current levels of the 100- and 50-period moving average lines lie not far above, at 111.61 and 111.78 respectively.

On the downside and in case of a data miss, support may come from the area around the lower Bollinger band at 110.72, which also encapsulates yesterday’s near three-week low of 110.58. Steeper losses would increasingly bring into scope the 110 round figure.

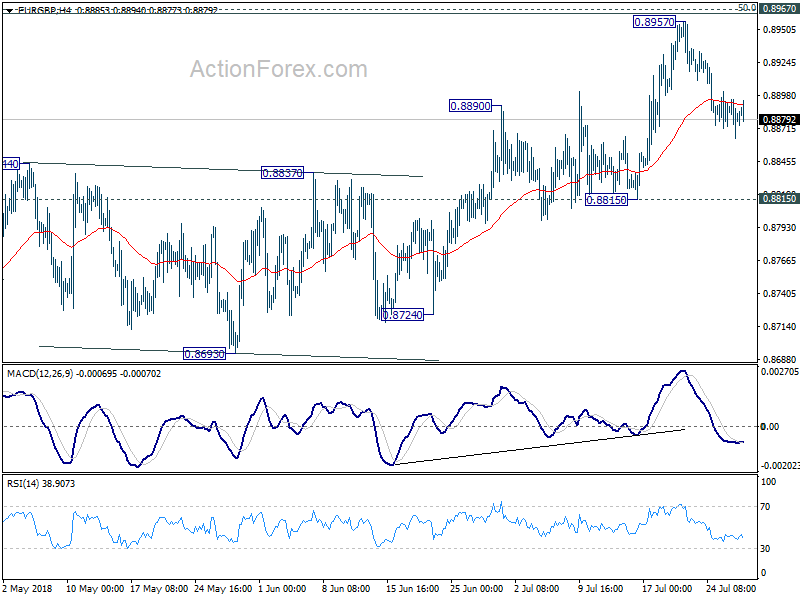

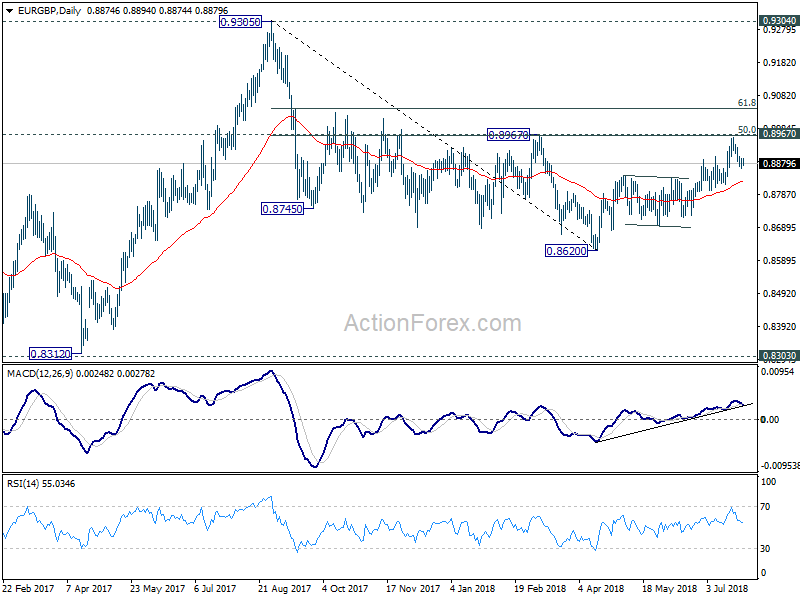

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8865; (P) 0.8882; (R1) 0.8899; More...

Intraday bias in EUR/GBP remains neutral as correction from 0.8957 is in progress. As long as 0.8815 support holds, further rally is expected. On the upside, sustained break of 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) should confirm completion of whole decline from 0.9305. EUR/GBP should then target 61.8% retracement at 0.9043 next.

In the bigger picture, EUR/GBP is staying in long term range pattern from 0.9304 (2016 high). The corrective structure of the fall from 0.9305 to 0.8620 is raising the chance that rise from 0.8312 to 0.9305 is an impulsive move. But we're not too confident on it yet. In any case, we'd stay cautious on strong resistance from 0.9304/5 to limit upside in case of further rally. Meanwhile, if there is another medium term decline, strong support will likely be seen from 0.8303 to contain downside.

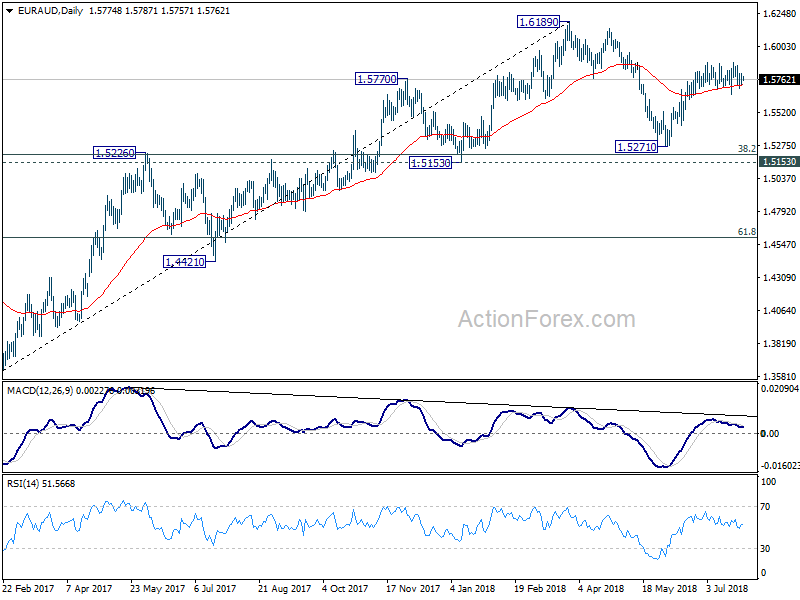

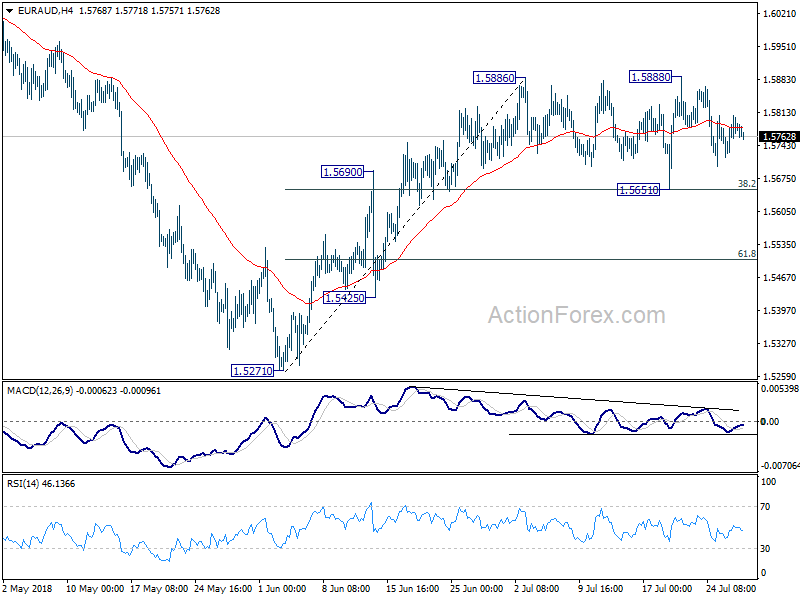

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5739; (P) 1.5774; (R1) 1.5817; More....

EUR/AUD is staying in consolidation from 1.5886 and intraday bias remains neutral first. With 1.5651 minor support intact, further rise would be seen. On the upside, break of 1.5888 resistance will extend the rally towards 1.6139/89 resistance zone. However, break of 1.5651 cluster support (38.2% retracement of 1.5271 to 1.5886 at 1.5651) will indicate near term reversal and turn bias back to the downside for 1.5271.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5271 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is still in progress. Break of 1.6189 will target 1.6587 key resistance (2015 high).