Sample Category Title

U.S. Q2 GDP Growth Rebounds Strongly

Highlights:

- US Q2 GDP growth rose an expected 4.1% following the 2.2% growth in Q1.

- The strengthening in GDP largely reflected consumer spending growth rising to 4.0% from the 0.5% increase recorded in Q1 with additional support coming from a bounce in export growth to 9.3% from 3.6%.

- The annual increase in the core PCE deflator rose to 1.9% in Q2 from 1.7% in Q1 and thus inched even closer to the Fed’s 2% inflation objective.

Our Take:

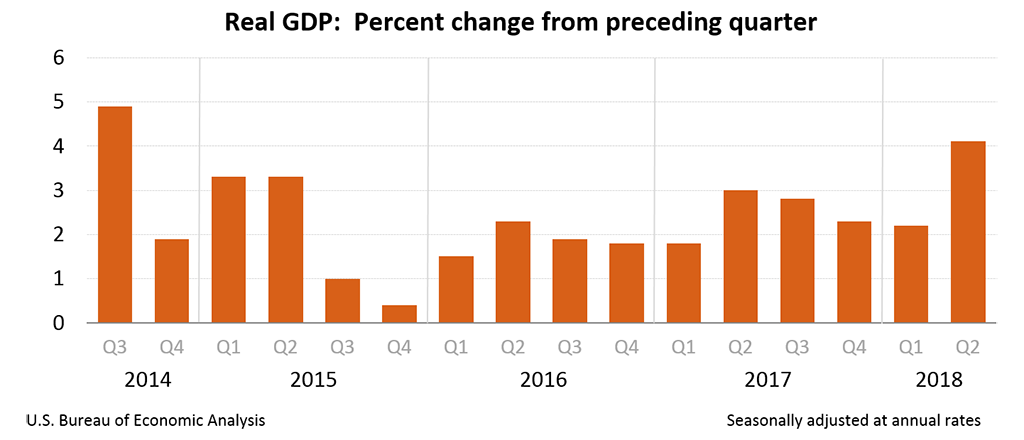

The U.S. economy, as expected, rebounded strongly in the second quarter rising 4.1% which was almost double the 2.2% increase recorded in Q1. Thus growth over the first half of this year remained well above the economy’s long-run potential rate of 1.8%. The strengthening in Q2 was relatively broadly based with solid increase in key expenditure areas such as consumer spending (4.0%) and business investment (7.3%). On a quarterly basis there was no indication of trade protectionism weighing on activity with exports up a strong 9.3% though the monthly detail is indicative of some slowing through the quarter. This solid overall pace of growth is a reflection of still accommodative monetary conditions being overlaid by the recent highly stimulative fiscal measures by the Trump Administration in the form of both tax cuts and expenditure increases.

With the economy operating at capacity, the above-potential growth presents the risk of pushing the economy into excess demand with attendant unwanted inflationary pressures. This risk is expected to keep the Fed tightening policy. However, the pace is likely to remain gradual as the central bank seems prepared to test the economy’s perceived capacity limits. Thus after raising the fed funds range 25 basis points in June to 1.75% to 2.00%, we are assuming it will remain on the sidelines at next week’s FOMC meeting. Future rate increases are expected at a rate of once a quarter through the end of next year. Though rising trade protectionism did not seem to have any dampening impact on quarterly growth in Q2, comments by Fed officials have indicated they see this as a potential downside risk going forward.

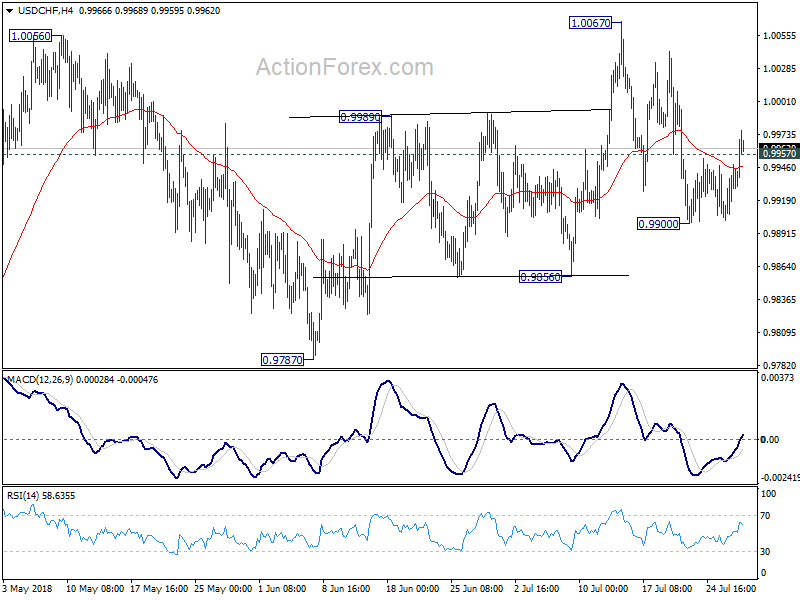

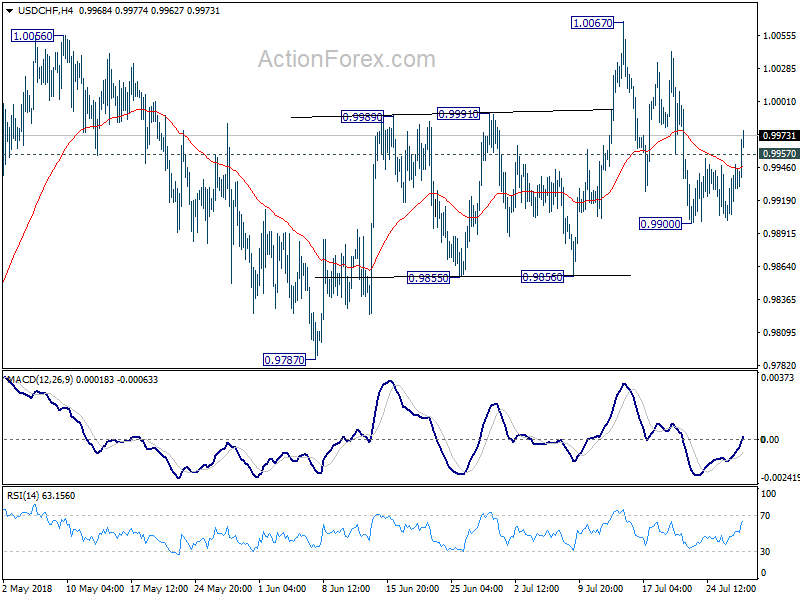

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9899; (P) 0.9925; (R1) 0.9942; More...

USD/CHF's rebound and break of 0.9957 minor resistance suggests that pull back from 1.0067 has completed at 0.9900. More importantly, the actions from 0.9787 maintain a higher-low, higher-high pattern and near term bullishness is retained. Intraday bias is back on the upside for retesting 1.0067 first. Break will resume whole rally from 0.9186.

In the bigger picture, as long as 0.9787 support holds, we're still favoring the bullish case. That is, rise fro 0.9787 is resuming the whole up trend from 0.9186 and should target 1.0342 key resistance on resumption. However, break of 0.9787 will indicate medium term reversal and turn outlook bearish.

Dollar Firm But Lacks Upside Momentum after Solid Yet Unspectacular GDP

Dollar stays firm in early US session after US delivered a solid yet unspectacular GDP report. While the greenback attempts strengthen today, so far, it's held in range against all other major currencies. There is no committed buying in Dollar up to this point. Yen is trading as the strongest for today as 10 year JGB yield closed solidly at 0.1000, up 0.0087. For the week, Canadian Dollar is the strongest one. On the other hand, Swiss Franc is the weakest one for today, following the strong rally in European stocks. But for the week, Euro is the weakest one after uninspiring ECB press conference yesterday.

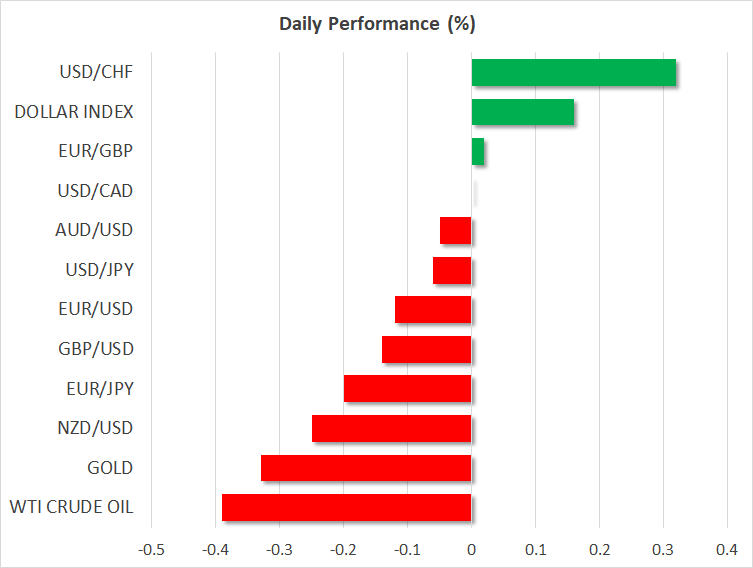

Technically, USD/CHF's break of 0.9957 minor resistance suggests that recent pull back from 1.0067 has completed. More upside is now in favor to retest 1.0067 high. GBP/USD is still having its sight on 1.3070 minor support but there is no determined selling in the pair yet. EUR/USD and AUD/USD are also staying in familiar range as recent consolidation could extend. USD/JPY and USD/CAD are both held below 111.53 minor resistance and 1.3114 minor resistance respectively. More downside is in favor in these two pairs.

U.S. Economy Grew 4.1% Rate in Q2

US GDP grew 4.1% annualized in Q2, much better than prior quarter's 2.0% but slightly missed expectation of 4.2%. GDP price index rose 3.0%, way above expectation of 2.3%. The growth was was highest since Q4 2014. But it's way off the 5% finalized annual rate in Q3 2014, and can't even match the 4.6% rate back in Q2 2014. The data is solid but unspectacular comparing to recent history.

It's noted in the release that "The acceleration in real GDP growth in the second quarter reflected accelerations in PCE and in exports, a smaller decrease in residential fixed investment, and accelerations in federal government spending and in state and local spending." But "these movements were partly offset by a downturn in private inventory investment and a deceleration in nonresidential fixed investment. Imports decelerated."

Professionals revised up inflation forecast in ECB survey

ECB released the latest Survey of Professional Forecasters (SPF) today. On Eurozone inflation, SPF respondents raised their headline HICP inflation forecast to 1.7% in 2018 (from 1.5%) , 1.7% in 2019 (from 1.6%) and 1.7% in 2010 (unchanged). They now matched Eurosystem staff projection of 1.7% through 2018 to 2020.

On Core HICP inflation, SPF projections were unchanged at 1.2% in 2018, 1.5% in 2019 and 1.7% in 2020. That compares to Eurosystem staff forecasts of 1.1% in 2018, 1.6% in 2019 and 1.9% in 2020. That is, SPF respondents expect faster pickup in core inflation in 2018 but the slowed the rise slows quickly.

On growth, SPF respondents revised down GDP forecast to 2.2% in 2018 (from 2.4%), 1.9% in 2019 (from 2.0%) and 1.6% in 2020 (unchanged). That compares to Eurosystem staff projections of 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020.

Majority of British voters want a referendum on the final Brexit deal

According to a YouGov poll for the Times, 42% British voters would like to have a referendum on the final terms of Brexit deal with the EU. Only 40% said there should not be, and the rest didn't know.

Among the votes, 58% of labor supporters, 67% of Lib-dem supporters and 21% of Conservative supported wanted a second referendum on the terms.

In the event of another referendum on Brexit tomorrow, 45% said they would vote to remain, 42% would vote to leave, 4% wouldn't vote and 9% said they didn't know.

It's a poll of 1653 adults in the UK conducted on Wednesday and Thursday this week.

IMF: Shift from high-speed to high-quality growth in China key for decades to come

IMF said in a report that China's economy continues to "perform strongly", with growth projected at 6.6% this year. But it also warned that the country is at a "historic juncture". The shift from "high-speed" to "high-quality" growth will determine China's "development path for decades to come". Risk of "near-term abrupt adjustment" was reduced by recent strong growth momentum and "significant financial de-risking progress". While there were accelerated rebalancing in some dimensions, "progress slowed" in many other dimensions. Also, while credit growth has slowed, "it remains excessive.

In the latest projections, IMF projected China GDP growth to be at 6.6% in 2018, slow to 6.4% in 2019, 6.3% in 2020, 6.0% in 2021, 5.7% in 2022 and 5.5% in 2023. Current account surplus as to GDP is projected to be at 0.9% in 2019, to close to 0.8% in 2019, at 0.8% in 2020, then slow to 0.7% in 2021, 0.5% in 2022 and 0.4% in 2023.

IMF also summarized the report in six charts. - China's strong GDP growth continues. - A focus on high-quality growth. - Credit growth has slowed but remains too fast. - China, a global digital leader. - Rebalancing efforts should be accelerated. -6. The benefits of faster reform.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9899; (P) 0.9925; (R1) 0.9942; More...

USD/CHF's rebound and break of 0.9957 minor resistance suggests that pull back from 1.0067 has completed at 0.9900. More importantly, the actions from 0.9787 maintain a higher-low, higher-high pattern and near term bullishness is retained. Intraday bias is back on the upside for retesting 1.0067 first. Break will resume whole rally from 0.9186.

In the bigger picture, as long as 0.9787 support holds, we're still favoring the bullish case. That is, rise fro 0.9787 is resuming the whole up trend from 0.9186 and should target 1.0342 key resistance on resumption. However, break of 0.9787 will indicate medium term reversal and turn outlook bearish.

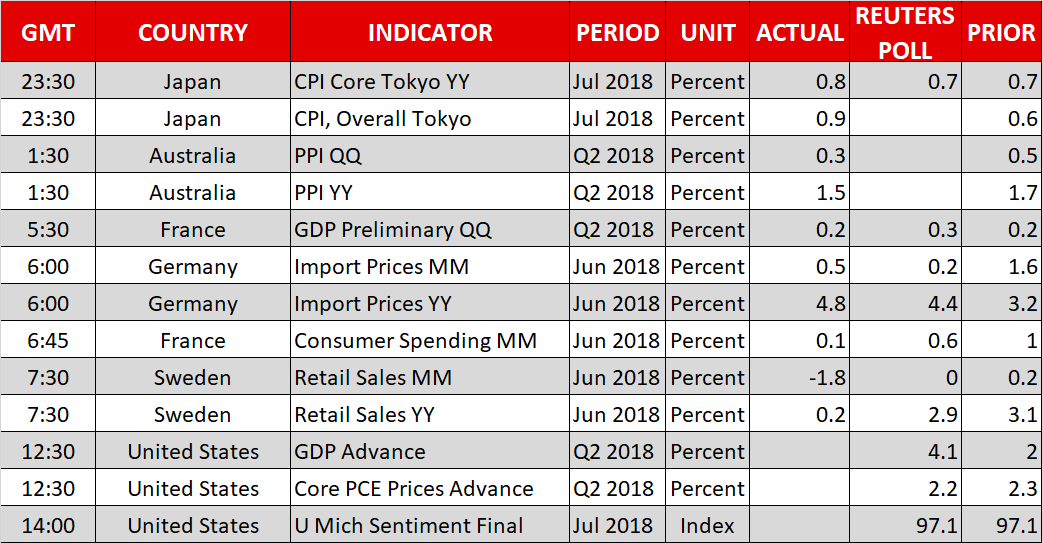

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jul | 0.80% | 0.70% | 0.70% | |

| 01:30 | AUD | PPI Q/Q Q2 | 0.30% | 0.60% | 0.50% | |

| 01:30 | AUD | PPI Y/Y Q2 | 1.50% | 1.70% | ||

| 05:30 | EUR | French GDP Q/Q Q2 A | 0.20% | 0.30% | 0.20% | |

| 12:30 | USD | GDP Annualized Q/Q Q2 A | 4.10% | 4.20% | 2.00% | |

| 12:30 | USD | GDP Price Index Q2 A | 3.00% | 2.30% | 2.20% | |

| 14:00 | USD | U. of Mich. Sentiment Jul F | 97.1 | 97.1 |

U.S. Economy Grew 4.1% Rate in Q2

The U.S economy grew at the strongest pace in nearly four-years during Q2, supported by a rebound in consumer spending, exports and firm business investment.

Q2 GDP rose at a seasonally and inflation-adjusted annual rate of +4.1% – a pickup from Q1 growth rate of +2.2%. Compared to the second quarter a year ago, output grew 2.8%.

Note: Market expectations were looking for a +4.4% growth rate.

Today’s report again suggests that the Fed will continue to “gradually” raise short-term interest rates to prevent economic overheating.

The Fed is widely expected to leave its benchmark rate unchanged at its policy meeting next week (Aug. 1) and increase it by +25 bps in September to +2.25%.

Immediate reaction sees some pressure on the U.S dollar.

US GDP grew 4.1% in Q2, only a near 4 year high

US GDP grew 4.1% annualized in Q2, much better than prior quarter's 2.0% but slightly missed expectation of 4.2%. GDP price index rose 3.0%, way above expectation of 2.3%. The growth was was highest since Q4 2014. But it's way off the 5% finalized annual rate in Q3 2014, and can't even match the 4.6% rate back in Q2 2014.

It's noted in the release that "The acceleration in real GDP growth in the second quarter reflected accelerations in PCE and in exports, a smaller decrease in residential fixed investment, and accelerations in federal government spending and in state and local spending." But "these movements were partly offset by a downturn in private inventory investment and a deceleration in nonresidential fixed investment. Imports decelerated."

Into US session: USD/CHF strong rebound ahead of US GDP

Entering into US session, Yen is the strongest one for today. 10 year JGB yield had another rally today and hit as high as 0.113 before closing at 0.100. Canadian Dollar follows as the second strongest on optimism that there will be a NAFTA agreement in principal in August. Dollar follows as the third strongest ahead of Q2 GDP report.

Meanwhile, Swiss Franc is notably the weakest one. Part of the reason is probably the strong rally in European stocks. The rally was fueled after European Commission Jean-Claude Juncker scored in his visit to the US and persuaded Trump to hold off on auto tariffs. The removed an immediate threat to the German economy as well as other automakers.

At the time of writing, DAX is up 0.43%, CAC up 0.27%. FTSE is also up 0.43%. Earlier today, Nikkei closed up 0.56%, HK HSI was up 0.08%. China Shanghai SSE was down -0.3%. Singapore Strait Times was down -0.11%.

USD/CHF takes the lead ahead of US GDP data. The break of 0.9957 minor resistance argues that pull back from 1.0067 has completed at 0.9900 already. The move since 0.9787 maintains pattern of higher lows, higher highs, and thus retain near term bullishness in the pair. Intraday bias is turned back to the upside with 1.0067 back in focus.

GBPJPY in Small Upside Retracement But Outlook Remains Bearish

GBPJPY is trading slightly higher over the past few hours after the rebound on the 145.32 support level. The price is trying to pare some ground of the previous red sessions, however, it is still developing below the short-term moving averages in the 4-hour chart.

The Relative Strength Index (RSI) is currently increasing positive momentum towards its neutral threshold of 50, while the stochastic oscillator posted a bullish crossover within the %K and %D lines in the oversold levels, both hinting that the next move in prices could be on the upside rather than on the downside.

If the pair bounces further up, immediate resistance could be met at the 20- and then at the 40-simple moving averages (SMAs) at 145.95 and 146.14 respectively. Jumping above these levels, the pair could challenge the 146.50 resistance level, which holds near the 200-SMA.

However, should the market extend losses, immediate support could come from the 145.32 barrier. A leg below this area could increase downside pressure and push the price until the 143.75 hurdle.

In the bigger picture, the pair is bearish as it posted a sharp sell-off following the touch on the 149.30 resistance obstacle and bears are still have the upper hand.

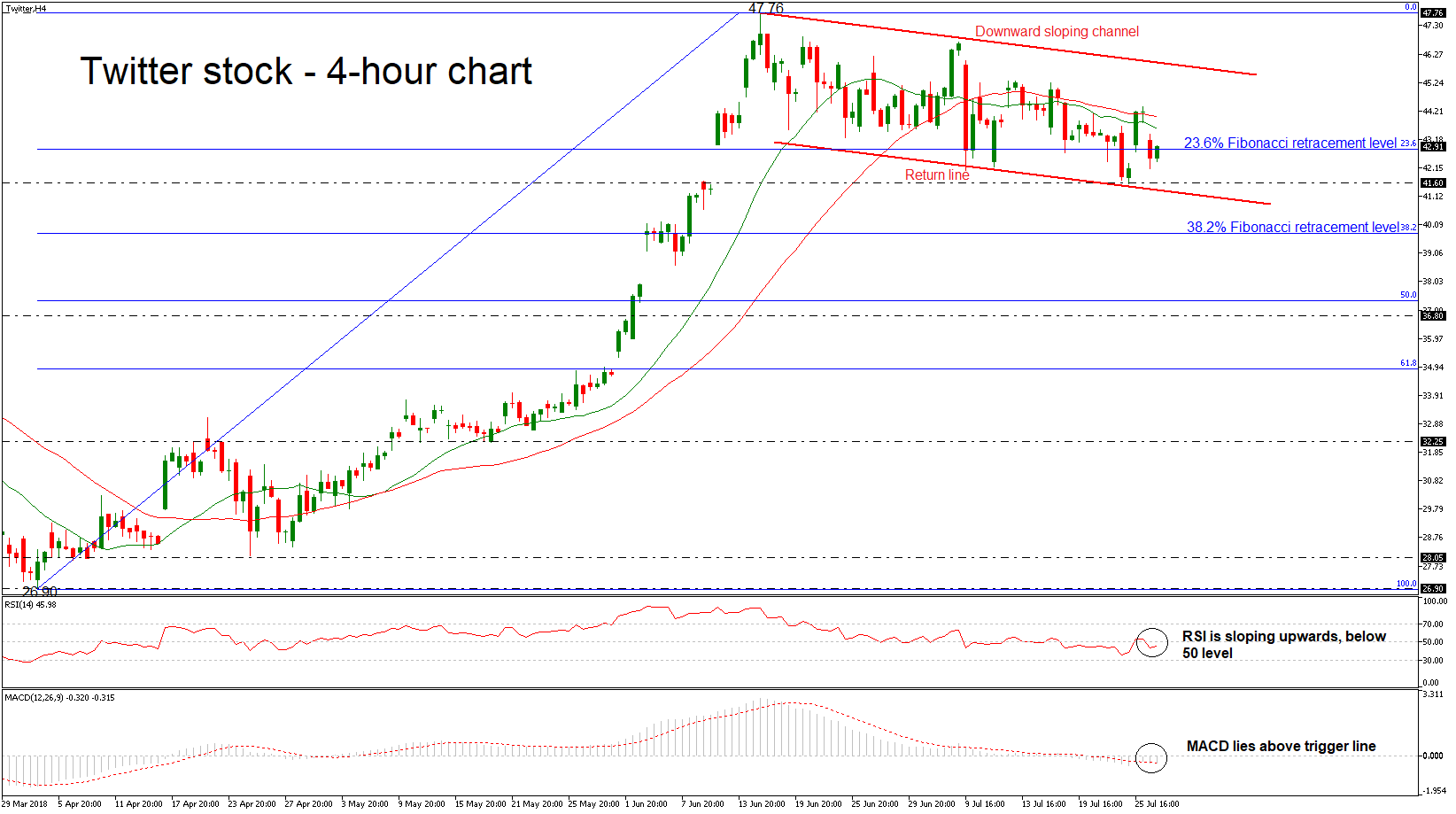

Twitter Stock Stands Within Negatively Aligned Channel In Near Term

Twitter stock has declined considerably after it touched a more than three-year high of 47.76 on June 15 and has been developing within a downward sloping channel since then. Additionally, over the previous couple of sessions, the price dipped below the 20- and 40-simple moving averages (SMAs) in the 4-hour chart but is currently trading near the 23.6% Fibonacci retracement level of the upleg from 26.90 to 47.76, around 42.85.

Technically, the momentum indicators are supporting the slightly positive momentum. Specifically, the RSI indicator is pointing north near the threshold of 50, while the MACD oscillator jumped above its trigger line, creating a bullish cross and is moving towards the positive territory.

Should the price decisively close above the 23.6% Fibonacci seen at 42.85, it could extend the upward movement until the 20- and then the 40-SMA at 43.59 and 44.00 respectively. Further advances above these levels, could then target the falling trend line of the negatively aligned channel, around 45.60. A break of this area could drive the price above the aforementioned pattern and challenge the 47.76 high.

On the other side, a decline could meet the 41.60 support, which the market was unable to break through from mid-June. Slightly lower, the price could retest the 38.2% Fibonacci region of 39.79.

Overall, an upward move could also post a clear step above the channel and endorse the scenario for an aggressive bullish rally. However, a penetration of the pattern would drive the price towards a bearish retracement.

Draghi Avoids The Tough Questions, US Data In Focus

Draghi avoids the tough questions, US data in focus

As broadly expected, the European Central Bank held interest rates unchanged yesterday. The marginal lending facility and the deposit facility rates will remain at 0.25% and -0.40%, respectively. Despite the euro zone enjoying solid growth, Mario Draghi didn't change his tune as he declared that it still needs 'significant monetary policy stimulus.' The ECB is still expected to maintain its €2.4 trillion bond-buying program until the end of the year, while interest rates should remain on hold 'through the summer' of 2019. During the question-and-answer session, journalists tried to get more clarity about the significance of 'through the summer.' Draghi didn't budge as he refused to provide a deadline. It shows that the ECB is eager to keep its leeway should things not turn out as expected. Finally, the central bank didn't provide further information regarding the reinvestment process of cash from its bond-buying program. Draghi said the matter was not discussed by the Governing Council.

However, the market knew very well that the ECB wouldn't provide further information about monetary policy tightening. The main topic of the day was trade relations between the US and the European Union. Indeed, higher tariffs by the US could dampen economic growth. Again, Draghi refused to comment – he just acknowledged it is 'a good sign' – and said that the ECB 'took note' and that it was 'too early to assess the actual content.'

Draghi's cautiousness triggered a broad-based dollar rally. During the press conference, EUR/USD fell more than 0.70% to 1.1640. Even the disappointing economic data from the US didn't prevent the dollar index from surging more than 0.60% to 94.76. June durable goods orders increased 1%m/m versus 3% expected. Excluding transportation, the gauge advanced 0.4%m/m versus 0.5% anticipated. Traders will be watching US second quarter GDP growth today (forecast 4.2% q/q annualized and 2% previous), Q2 core PCE (2.2% exp.) and personal consumption (3% exp. and 0.9% previous).

Brexit negotiations with Barnier are difficult

Brexit negotiations continue with Theresa May taking control of discussions. As communicated on Tuesday in a ministerial statement, PM May has taken full responsibility for the negotiations with the EU, accompanied by Dominic Raab, her new Brexit Secretary, who replaces David Davis. Following the late-afternoon announcement, the cable surged from 1.3116 to 1.3189 the day after (+0.67%), a trend that did not last as talks with the EU continue to pose challenges for May's Brexit team, thus creating further uncertainties with regard to the 3-month deadline related to the customs relationship with the Single Market.

Indeed, the euphoria seems to have disappeared as the pair lost intraday gains from the beginning of the week amid tough European rhetoric and a slowdown in economic fundamentals. After having agreed a Brexit white paper with her cabinet at Chequers two weeks ago, EU Commission negotiator Michel Barnier declared being unsatisfied with May's solution for the Customs Union, one of the nerve centres of the plan, thus putting further pressure on the PM. The discussions, however, ended on a positive note with Barnier expressing support for a continued security relationship with the UK. The next meeting is expected to take place in mid-August.

The Bank of England Monetary Policy Committee will most certainly confirm market expectations and raise interest rates by 25 bps next Thursday, regardless of the recent Brexit debates. Despite a slackening in economic expansion (disappointing private consumption and wage growth), inflation remains above the 2% target. In any case, a no-go situation would threaten the GBP, which would see a drastic drop.

GBP/USD fall continues, currently trading at 1.31 and expected to decline further, as recent Brexit events can only further weaken the pair. Approaching the 1.3080 range.

Dollar Modestly Higher Ahead Of Much-Awaited US GDP Report, European Stocks In The Green

Here are the latest developments in global markets:

FOREX: The dollar’s index against a basket of six major currencies was trading higher – though by less than 0.2% – building on Thursday’s notable rise. Dollar/yen was little changed ahead of the US report on Q2 GDP and with market participants eagerly awaiting to see whether the Bank of Japan will indeed tweak its policy framework when it completes its meeting on monetary policy on Tuesday. Euro/dollar was 0.1% down, extending the losses which acted as the catalyst for the dollar index’s gains yesterday after the ECB reiterated what markets seem to interpret as a relatively dovish rate-normalization guidance. Specifically, the pair traded at 1.1628 at 1014 GMT, not far above a one-week low of 1.1619 hit earlier in the day. Pound/dollar was 0.15% lower, with concerns over the progress of Brexit negotiations overshadowing optimism relating to the likely delivery of a 25bps rate increase by the Bank of England next week.

STOCKS: European equities were broadly in the green, with overall upbeat corporate earnings and the continuing positive sentiment following the Trump-Juncker meeting on Wednesday contributing to the rise. The pan-European STOXX 600 and the blue-chip euro STOXX 50 were up by 0.3% and 0.5% respectively. Meanwhile, the UK’s FTSE 100, German DAX and the French CAC 40 traded higher by 0.55%, 0.4% and 0.2% correspondingly. Some of these benchmarks may have also received a boost from the sliding euro and sterling versus the dollar, given their heavy export dependency. Turning to the US, futures markets were pointing to a marginally higher open for the Dow and the S&P 500 and an even higher open for the Nasdaq 100; contracts tracking the latter were up by 0.3%. Chevron, Exxon Mobil, Merck & Co and Twitter are expected to soon release their quarterly results; they’re all due before Wall Street’s opening bell.

COMMODITIES: WTI was 0.4% lower at $69.35 per barrel, erasing part of the gains which came after an attack on Saudi tankers spurred supply concerns, consequently boosting prices. Brent crude was down by the same proportion, trading at $74.24 a barrel. In precious metals, gold extended yesterday’s losses on the back of a stronger dollar. It was last down by 0.3% at $1,218.90 per ounce.

Day ahead: US GDP in the spotlight

All eyes will be on the preliminary estimate of US GDP growth for the second quarter of the year due at 1230 GMT.

US economic growth is expected to have risen by 4.1% on an annualized basis in Q2, at a far higher pace relative to Q1’s 2.0% and at its quickest since Q3 2014. A better-than-expected reading is likely to be seen as more conclusively putting on the table two more 25 bps rate hikes by the Fed as the year unfolds – bringing the total number for the year to four –, thus supporting the dollar. A weak reading could on the other hand cause some profit-taking for the greenback. At the moment, Fed funds futures project that market participants have fully priced in an additional rate increase, while they see a 68% probability for a second one. In the meantime, advance data on core PCE prices for Q2 will be released alongside the numbers on GDP, while the University of Michigan’s final reading on consumer sentiment for the month of July will be hitting the markets at 1400 GMT; the relevant index is expected to be confirmed at 97.1, below June’s 98.2.

Mexican Economy Minister Ildefonso Guajardo’s visit to Washington, which included meetings with US Trade Representative Robert Lighthizer, will conclude today. Following constructive talks on trade between the US and the EU earlier this week, it will be interesting to see if positive momentum carries through into NAFTA talks, something which is likely to benefit the Mexican peso and the Canadian dollar.

In energy markets, oil traders will be keeping an eye on the Baker Hughes count of active US oil rigs due at 1700 GMT.