Sample Category Title

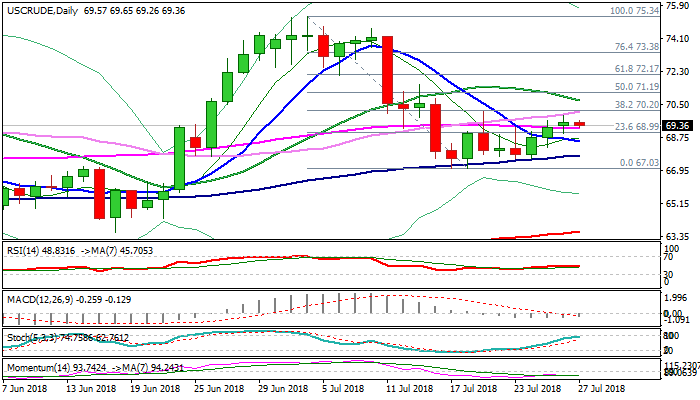

WTI OIL Outlook: Bullish Outlook Above Broken 55SMA

WTI oil eases from one-week high at $69.90 on Friday but remains constructive above broken 55SMA ($69.22).

Thursday's eventual break above 55SMA which marked the top of week-long congestion, was bullish signal. Bulls require extension above pivots at $70.00/20 (psychological / Fibo 38.2% of $75.34/$67.03 fall) to confirm break and signal continuation of recovery from $67.03.

Broken 55 SMA marks initial support at $69.22, with deeper dips expected to find ground above 10SMA ($68.53) and keep bulls in play.

Daily studies are mixed and still lacking clear direction signal, but fundamentals are supportive.

Constructive trade talks between the US and EU which move cutting trade barriers between two countries and news that Saudi Arabia is suspending oil shipments through the Red Sea, accompanied by strong falls in crude inventories, keep oil prices supported.

Focus turns on release of Baker Hughes report later today, which counts US oil rigs and could provide fresh signals for the oil price.

Res: 69.65, 69.90, 70.20, 70.73

Sup: 69.22, 68.92, 68.53, 68.19

High Expectations For US Q2 GDP Data

Notes/Observations

- BOJ firmly sticking to its zero target for 10-year JGB yields ahead of Tuesday’s rate decision.

- High expectations for US Q2 GDP with some speculation of a 5% print

Asia:

- BOJ again conducted a Fixed-rate JGB Bond purchase operation (2nd operation this week)

- Japan Finance Ministry (MOF): Confirms Masatsugu Asakawa to remain as FX Chief for 4th year; Shigeaki Okamoto named as new top bureaucrat for the Finance Ministry

- China Official stated that the Govt had a plan to retaliate against increases in US tariffs regardless of the volume of goods targeted

Europe:

- Italy Dep PM Di Maio (5-Star party leader): reiterated stance that euro and NATO memberships were not up for discussion. Did not believe that Finance Minister Tria would leave the Govt

- EU Chief Brexit Negotiator Barnier: EU would not delegate the application of its customs policy (ruled out allowing the UK to collect customs duties on its behalf); rejected UK white paper proposal on customs union

- Brexit Min Raab stated that was closer to an agreement in key areas; UK/EU would meet again in mid August and continue to weekly discussions to clear away all the obstacles that line our path to a strong deal in October

Americas:

- White House Econ Adviser Kudlow: Number on US GDP growth due on Friday 'will be big' (Reminder: On July 23rd Fox's Gasparino: White House to tout nearly 5% GDP growth for Q2 on Friday)

- President Trump stated that he believed the GDP numbers tomorrow would be terrific. “Someone predicted today that Q2 GDP would be 5.3%, but I don't think that's going to happen. Will be happy if there is a '4' in front of it; 3.9 or 3.8% will be ok”

Economic Data:

- (FR) France Q2 Advance GDP Q/Q: 0.2% v 0.3%e; Y/Y: 1.7% v 1.9%e

- (DE) Germany Jun Import Price Index M/M: 0.5% v 0.3%e; Y/Y: 4.8% v 4.5%e

- (FI) Finland July Business Confidence: 14 v 14 prior; Consumer Confidence: 22.0 v 23.0 prior

- (FR) France Jun Consumer Spending M/M: 0.1% v 0.6%e; Y/Y: 0.3% v 0.7%e

- (ES) Spain Jun Adjusted Retail Sales Y/Y: 0.1% v 0.3%e; Retail Sales (unadj): +0.6% v -0.1% prior

- (ES) Spain May House Mortgage Approvals Y/Y: 7.3% v 34.2% prior; Total Mortgage Lending Y/Y: -1.7% v +26.1% prior

- (HU) Hungary Jun Unemployment Rate: 3.6% v 3.7%e

- (CN) Weekly Shanghai copper inventories (SHFE): 197.1K v 211.3K tons prior

- (SE) Sweden Jun Retail Sales M/M: -1.8% v 0.0%e; Y/Y: 0.2% v 3.1% prior

- (SE) Sweden Jun Trade Balance (SEK): -0.5B v -5.4 prior

- (AT) Austria July Manufacturing PMI: 56.8 v 56.6 prior (30th month of expansion)

- (IT) Italy Jun PPI M/M: 0.3% v 1.0% prior; Y/Y: 3.2% v 2.7% prior

Fixed Income Issuance:

- (IT) Italy Debt Agency (Tesoro) sold €6.0B vs. €6.0B indicated in 6-month bills; Avg Yield: 0.066% v 0.092% prior ; Bid-to-cover: 1.8x v 1.98x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.1% at 391.1, FTSE +0.2% at 7681 DAX +0.3% at 12846, CAC-40 +0.0% at 5480, IBEX-35 +0.9% at 9866, FTSE MIB +0.3% at 21,932, SMI +0.1% at 9153, S&P 500 Futures flat]

- Market Focal Points/Key Themes: European Indices push higher once again continuing the positive momentum, with largely positive earnings helping fuel sentiment. Earnings from Amazon after the close yesterday helped set the tone with a big EPS beat, while profits did slightly miss the mark. In Europe shares of Carrefour rises sharply following results, with Reckitt Benckiser, LafargeHolcim, BT, Engie and Danone are among other names rising following results and guidance. BASF declines after missing its EBIT forecast, with Kering declining the most in two years after Gucci Q2 LFL sales missed estimates. Elsewhere BHP shares trade higher after selling its US shale assets to BP for just shy of $11B. Looking ahead notable earners include Merck, Colgate, Philips 66, Goodyear, Abbvie, Exxon and Chevron among others.

Movers

- Consumer Discretionary Carrefour [CA.FR] +9.8% (Earnings), L'Oreal [OR.FR] -3.5% (Earnings), Kering [KER.FR] -6.6% (Earnings)

- Consumer staples Danone [BN.FR] +1.9% (Earnings)

- Material Lafarge Holcim [LHN.CH] +3.0% (Earnings), BHP [BHP.AU] +3.7%, BP [BP.UK] -0.8% (Divests shale assets to BP)

- Healthcare Reckit Benckiser [RB.UK] +7.0% (Earnings)

- Financials Flow Traders [FLOW.NL] -11% (Earnings)

- Industrials BASF [BAS.DE] -2.8% (Earnings)

- Telecom SES [SESG.FR] +8.1% (Earnings), BT [BT.A.UK] +3.5% (Earnings) -Energy Engie [ENGI.FR] +2.2% (Earnings)

Speakers

- Italy Interior Min Salvini (also Dep PM): Italy budget law would set fundamentals for a flat tax

- South Africa Central Bank (SARB) Gov Kganyago reiterated view that policy stance remained accommodative. Current stance remaineds appropriate given the state of the economy and would look through the 1st round of inflation effects

- Bank of Korea (BoK) Gov Lee: See a need to adjust interest rates should inflation target be kept near 2% and if economy grows at potential growth rate

- Indonesia Central Bank official Hendarsah stated that it had again intervened in FX market

- Russia Energy Min Novak: OPEC+ to maintain the plan of no more thn 1M bpd boost; did agree back in Jun to review supply situation again in Sept

Currencies

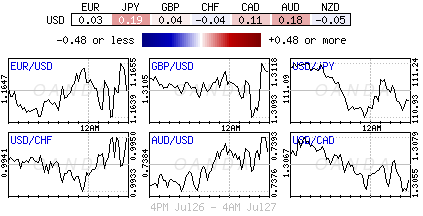

- USD was firmer on high expectations for upcoming US Q2 GDP with some speculation of a 5% print.

- FX focus was on next week’s BOJ policy meeting on Tuesday and could prove to be significant for the JPY currency (yen) as some analysts believe that BOJ could opt to raise the 10-year government bond yield target from 0.0% to 0.1%. The consensus remained that the BOJ would keep its policy steady after the central bank again conducted a Fixed-rate JGB Bond purchase operation (2nd operation this week) to keep the Yield Control target around 0.00%.

- EUR/USD was listless in the aftermath of the ECB policy decision with the pair remaining stuck in the tight 1.16-1.17 range it has been in for weeks

Fixed Income

- Bund Futures trades at 162.00 little changed in the post-European Central Bank meeting environment, even as the central bank stopped short of providing details on reinvestments. A move back above 162.75 would target 163.47 then 163.63, with a move below 161.75 targeting 161.45 then 160.45.

- Gilt futures trades at 123.06 down 12 ticks following the move in Treasuries with continuing upside targeting 124.18 then 124.44, with a move lower seeing initial support at 123.23 then 122.85.

- Friday's liquidity report showed Thurssday's excess liquidity rose from €1.817T to €T. Use of the marginal lending facility rose from €73M to €M.

- Corporate issuance saw 3 high-grade issuers raise $1.7B in the primary market . For the week ended July 25th Lipper fund flows reported IG funds show outflows of $0.6B, with US-based domestic equity funds attracting $474M in a second straight week of inflows.

Looking Ahead

- 05:30 (PL) Poland to sell Bonds

- 05:30 (IN) India to sell combined INR100B in 2023, 2028, 2035 and 2045 bonds

- 05:30 (ZA) South Africa to sell ZAR600M in I/ L 2022, 2033 and 2050 bonds

- 06:00 (IE) Ireland Jun Retail Sales Volume M/M: No est v 0.1% prior; Y/Y: No est v 4.3% prior

- 06:00 (UK) DMO to sell €5.0B in 1-month, 3-month and 6-month bills (£1.0B, £2.0B and £2.0B respectively)

- 06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to leave Key Rate unchanged at 7.25%

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil July FGV Inflation IGPM M/M: 0.5%e v 1.9% prior; Y/Y: 8.2%e v 6.9% prior

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Q2 Advance GDP Annualized (1st reading) Q/Q: 4.2%e v 2.0% prior; Personal Consumption: 3.0%e v 0.9% prior

- 08:30 (US) Q2 Advance GDP Price Index: 2.3%e v 2.2% prior; Core PCE Q/Q: 2.2%e v 2.3% prior

- 09:00 (MX) Mexico Jun Trade Balance: -$0.3Be v -$1.6B prior

- 09:30 (BR) Brazil Jun Total Outstanding Loans (BRL): No est v 3.11T prior; M/M: No est v 0.5% prior, Personal Loan Default Rate: No est v 5.0% prior

- 10:00 (US) July Final University of Michigan Confidence: 97.1e v 97.1 prelim

- 11:00 (CO) Colombia Jun National Unemployment Rate: No est v 9.7% prior; Urban Unemployment Rate: 10.3%e v 10.1% prior

- 11:00 (EU) Potential sovereign ratings after the EU close (Cyprus and Netherlands Sovereign Debt to Be Rated by Moody's; Sweden Sovereign Debt to be rated by Fitch - 13:00 (US) Weekly Baker Hughes Rig Count data

- 13:30 (BR) Brazil Jun Central Govt Budget Balance (BRL): No est v -11.0B prior

- 15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to leave Overnight Lending Rate unchanged at 4.25%

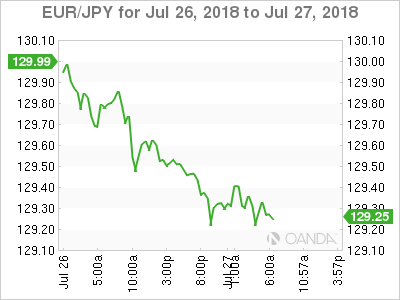

King Dollar Stands Tall Ahead Of GDP, Gold Drops

Global risk sentiment remains somewhat supported by easing trade tensions between Washington and Brussels with stock markets poised to conclude the trading week on a firm footing.

Asian stocks have already closed on a mixed note this morning, with European markets stabilizing ahead of the anticipated US GDP report this afternoon. Although the gut-wrenching selloff in Facebook shares weighed on Wall Street yesterday, US stocks could recover if US GDP data paints a positive picture of the US economy.

The trading week has undoubtedly been dominated by global trade developments and we may see this theme rollover into next week. Now a trade truce has been secured with the EU, will the United States be able to find a middle ground on trade with China? This remains a recurrent question on the minds of many investors.

Dollar appreciates ahead of US GDP

Dollar bulls were injected with a renewed sense of confidence yesterday after positive economic data boosted sentiment towards the US economy and reinforced rate hike expectations.

The encouraging jobless claims figures and durable goods orders stimulated buying sentiment towards the Dollar, consequently sending prices higher. With the attraction for the Greenback rolling over into Friday’s trading session, the Dollar Index has rallied towards the 94.90 level as of writing. Investors will direct their attention towards the pending US Q2 GDP report which could shape Fed rate hike expectations. A solid pickup in US economic growth during the second quarter of 2018 could send the Dollar Index back above 95.00 and beyond.

Euro more concerned with Dollar than ECB

The Euro’s recent weakness has more to do with an appreciating Dollar rather than the European Central Bank.

Market players hoping the ECB wouldcreate some fireworks were left empty-handed after the central bank offered no surprises during July’s policy meeting. As widely expected, interest rates were left unchanged, while the central bank reiterated its pledgeto end QE by the end of 2018. The highlight of July’s meeting was when the ECB repeated that interest rates will be left on hold until “at least through summer of 2019”.

The divergence in monetary policy between the Federal Reserve and European Central Bank is likely to keep a lid on the EURUSD in the medium to longer term.

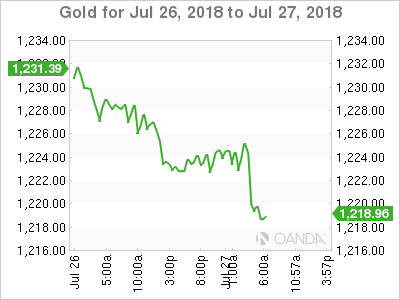

Commodity spotlight – Gold

It has been another bearish trading week for Gold mostly due to a stabilizing US Dollar.

Easing trade tensions between the United States and European Union have eroded appetite further for the precious metal with prices trading around $1218 as of writing. With the Dollar likely to remain buoyed by Fed hike expectations, the outlook for Gold remains grim.

Much attention will be directed towards the pending US GDP report this afternoon which could deal Gold the knockout blow. A strong US GDP print may ultimately strengthen the Dollar, inevitably translating into further downside for the precious metal. In regards to the technical picture, a breakdown below $1213 could inspire a decline towards $1200.

Easing Trade Fears Provide Boost Ahead Of US GDP Data

- Markets buoyed by easing trade war risks;

- Strong week of earnings despite Facebook horror show;

- US GDP eyed as Trump hopes for more than 4%.

European markets are trading in the green once again on Friday, with futures pointing to a similar open in the US, as an apparent easing in trade tensions between the US and European Union boosts risk appetite.

While only the outline of an agreement on trade between the two – which account for more than half of global GDP – was released, it was widely viewed as an important first step towards more cooperation and closer ties, and away from protectionism. For Donald Trump, the concessions offered by the EU represent an important victory at home ahead of the midterm elections – although the real benefits of them may not be known for some time.

Juncker on the other hand will be a relieved man, returning to Europe having avoided tariffs being imposed on the auto industry and with apparent assurances both sides will work towards removing those already imposed, while lowering other tariffs and non-trade barriers in the future. This was also ultimately the goal of Trump as well when imposing the tariffs so both will feel they have come out of this better off.

Ultimately, the biggest winner here may be investors as the meeting now potentially sets a precedent for how other trade conflicts can be resolved, although the feud with Beijing is more complex and may take much longer to repair. The protectionist measures adopted by Trump as a tool to fight other countries on trade – and then by those countries in retaliation – have weighed on markets since the start of the year, keeping the S&P 500 and Dow off their highs despite companies having reported huge earnings growth – primarily driven by tax cuts – in the first two quarters.

It’s been a big week for earnings season, with a third of S&P 500 and Dow companies reporting on the second quarter. While the general trend has remained, with companies reporting strong figures, it hasn’t passed without its casualties, with Facebook closing almost 20% lower yesterday after reporting disappointing numbers and forecasts. Today is looking a little quieter on the earnings front, although there are still 18 S&P 500 companies reporting, including Exxon Mobil and Twitter.

On the data side, the US will release GDP figures for what is expected to be a bumper second quarter after a modest first few months of the year. The economy is expected to have grown 4.1% on an annualised basis, which will naturally be championed by Trump as being rewards for his hard work. It will be interesting to see how markets react, should the economy outperform expectations, with the Federal Reserve already on course to raise rates twice more this year.

U.S Dollar Firmer On GDP Expectations

Friday July 27: Five things the markets are talking about

Euro stocks have found some traction after a mixed performance overnight in Asia, as investors remain upbeat over the tentative trade truce between the U.S and the E.U.

President Trump and E.C Commission President Juncker agreed, in principle, not to impose new tariffs while the two economies sorted out their differences. The truce comes as Sino-U.S trade relations remain on edge.

Aside from corporate balance sheets, capital markets remains focused on trade and central bank policy – BoJ (July 30), Fed (Aug. 1) & BoE (Aug. 2).

Today’s advanced U.S GDP will be an important print (08:30 am EDT) – Trump and his economic team are convinced that the GDP numbers will be strong.

Trumps advisers have been privately telling associates that GDP growth should rise to +4.3% or +4.4% for Q2. The President is even more optimistic, telling anyone who will listen he expects a +4.8% headline – anything close and the president will be accused of leaking data. The danger for the U.S dollar is a weaker headline print below +4%.

This morning’s U.S data may provide support for the Fed’s tightening path, while in Japan, reports suggest the BoJ is debating ways to reduce the side effects of their yield-curve control policy.

Note: The ECB indicated yesterday that it will stick to its plan to end bond purchases and pledged to keep interest rates unchanged “at least through the summer of 2019.”

1. Stocks mixed results

In Japan, equities closed higher overnight, taking solace from signs of reconciliation between the U.S and Europe over trade issues. The benchmark Nikkei share average hit a one-week closing high and ended the week +0.56% firmer. The broader Topix ended +0.57% higher.

Down-under, the Aussie’s stock benchmark topped early July’s best in notching another eleven-year closing high – the S&P/ASX 200 rose +0.9% as BHP Billiton rose +2.3%. In S. Korea, the Kospi cooled following Thursday’s outperformance, but still rose further, allowing the index to narrowly avoid a sixth-decline in seven-weeks. It rose +0.3%, both today and on the week.

In Hong Kong, stocks ended flat as expectations of more stimuli from Beijing offset worries over a China economic slowdown. The Hang Seng index rose +0.1%, while the China Enterprises Index gained +0.2%.

In China, bourses ended down overnight, as investors remain cautious amid concerns over the Sino-U.S trade friction. The blue-chip CSI300 index ended -0.4% down, while the Shanghai Composite Index closed -0.3% lower.

In Europe, regional bourses are pushing higher, continuing the positive momentum, with largely positive earnings helping fuel sentiment.

U.S stocks are set to open ‘unchanged’.

Indices: Stoxx600 +0.1% at 391.1, FTSE +0.2% at 7681 DAX +0.3% at 12846, CAC-40 +0.0% at 5480, IBEX-35 +0.9% at 9866, FTSE MIB +0.3% at 21,932, SMI +0.1% at 9153, S&P 500 Futures flat

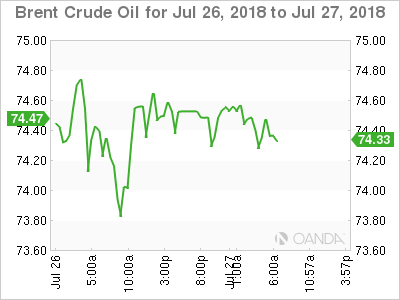

2. Oil markets ease after three days of gains, gold higher

Oil prices are a tad lower in quiet trading after three-days of gains, but took support from Saudi Arabia halting crude transport through a key shipping lane, falling U.S stock levels and easing global trade tensions.

Brent futures are down -5c at +$74.49 a barrel – it’s heading for a near +2% gain this week, the first weekly increase in four. U.S West Texas Intermediate (WTI) futures are -5c lower at +$69.56, after rising nearly +0.5%on Thursday. The contract is heading for a -1.3% weekly loss, a fourth-week of declines.

On Thursday, Saudi Arabia said that it was “temporarily halting” all oil shipments through the strategic Red Sea shipping lane of Bab al-Mandeb after an attack on two oil tankers by Yemen’s Iran-aligned Houthi movement.

Note: An estimated +4.8M bpd of crude oil and refined petroleum products flow through this waterway towards Europe, the U.S and Asia.

This week’s EIA report showed that crude inventories fell -6.1M barrels in the week to July 20, compared with a market expectation for a decrease of -2.3M barrels.

Ahead of the U.S open, gold prices have edged a tad higher overnight as the dollar slipped against G10 pairs ahead of U.S GDP data that could shed light on the pace of rate hikes stateside. Spot gold is up +0.1% at +$1,223.96 an ounce. U.S gold futures, for August delivery are -0.2% lower at +$1,223.20 an ounce.

Note: The ‘yellow’ metal is on track for its third consecutive weekly decline.

3. Euro yields barely move

Eurozone government bond yields have barely moved in this week’s post-ECB meeting environment, even as the central bank stopped short of providing details on reinvestments. The 10-year Bund yield is trading at +0.40%, unchanged on the day.

Note: Later this morning, both France and Spain are scheduled to announce details of their respective auctions for next week.

Stateside, U.S bond prices are a tad weaker, falling after the ECB said it would hold its benchmark interest rate steady and the U.S. reported progress on a revamped Nafta agreement.

The yield on the benchmark 10-year Treasury note is at +2.975%, up from 2.936% Thursday.

Yesterday, Draghi confirmed the ECB’s plans to gradually phase out easy-money policies, but signalled the central bank would likely hold interest rates steady until the end of next summer. The move continues to highlight a widening policy divergence with the Fed.

4. Dollar firmer on GDP expectations

The USD is firmer on high expectations for this morning’s U.S Q2 GDP with some speculation of a +4.4 to +5% print.

After this morning’s release, the markets focus will quickly shift to next week’s BoJ’s policy meeting (July 30/31), which could prove to be significant for the JPY (¥111.19) as some analysts believe that BoJ could opt to raise the 10-year government bond yield target from +0.0% to +0.1%. Nevertheless, the majority believes that Japanese policy makers will keep its policy steady after authorities again conducted a fixed-rate JGB Bond purchase operation (second operation this week) to keep their yield control target around +0.00%.

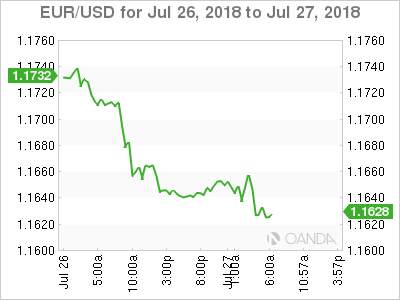

EUR/USD (€1.1625) trades sideways in the aftermath of the ECB policy decision with the pair remaining stuck in the tight €1.16-1.17 range it has been for the past month.

5. French consumer spending sluggish in June

Data this morning showed that French consumer spending was lethargic last month, with household expenditure staying ‘virtually flat,’ according to statistics agency Insee.

Digging deeper, consumer spending rose +0.1% on month in June, well below market expectations for a rise of +0.5%.

Spending was up +0.3% on year – the agency also revised May’s figure for household expenditure on goods to +1.0% from +0.9%. Consumption in food and energy was stable in June, with a slight rise in engineered goods and a slowdown in durables.

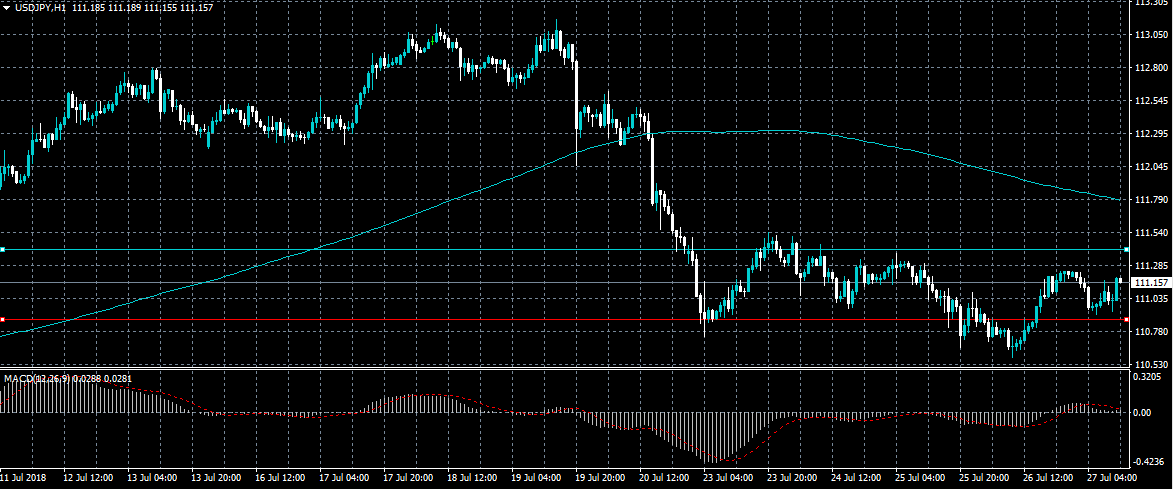

USDJPY Only Intraday Bullish ABove 110.87

The US dollar continues to hold above the 111.00 level against the Japanese yen currency after sellers failed to sustain downside pressures on Thursday. The USDJPY pair now has a bullish intraday bias while trading above the key 110.87 technical level. Traders now look to key second fiscal quarter Gross Domestic Product and Inflation data from the United States economy.

The USDJPY pair is intraday bullish while trading above the 110.87 level, key resistance is found at the 111.39 and 111.70 levels.

If the USDJPY pair falls back below the 110.87 level, sellers will likely test towards the 110.55 and 110.25 levels.

EURUSD Further Bearish Below 1.1630 Level

The euro currency continues to trade lower against the greenback, as the US Dollar Index advances back towards the 95.00 level. The EURUSD pair now trades with a strong bearish intraday bias while price trades under the 1.1630 level. Sellers will now target losses below the 1.1600 level, while EURUSD buyers need to force price back above the 1.1680 resistance level.

The EURUSD pair is strongly bearish below the 1.1630 level key support is found at the 1.1600 and 1.1540 levels.

If the EURUSD pair trades above the 1.1680 level, buyers will likely target the 1.1700 and 1.1724 levels.

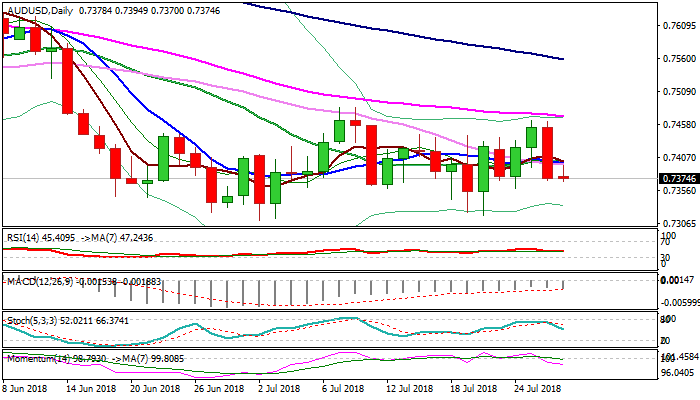

AUDUSD Outlook: Thursday’s Long Red Candle Weighs Heavily, US GDP Eyed For Fresh Signal

The Australian dollar consolidates within narrow range on Friday, following 1% fall previous day, with prevailing negative near-term outlook.

Repeated upside rejection left a double-top (0.7464), generating negative signal, reinforced by Thursday's massive bearish candle, which weighs heavily.

Converged daily MA's 10, 20, 30) are in bearish setup and cap today's recovery attempt, accompanied with weak momentum and south-heading slow stochastic.

Falling daily cloud maintains pressure and completes negative picture.

US GDP data are in focus as key event today, with strong reading expected to further boost the greenback and push the Aussie towards key supports at 0.7310/17 (02 / 20 July lows).

Alternative scenario requires close above a cluster of daily MA's at 0.7400 zone to ease bearish pressure, while extension above falling 55SMA (0.7468) which repeatedly capped recovery attempts, is needed to neutralize bears and shift focus higher.

Res: 0.7394, 0.7408, 0.7440, 0.7464

Sup: 0.7359, 0.7325, 0.7310, 0.7283

Weak Ahead: US Dollar In A Bullish Trend

ECB left rates unchanged as expected. US President Donald Trump and European Commission President Jean-Claude Juncker have announced that the eurozone and the US will launch a new round of trade negotiations. 10Y rates spreads suggests investors have positioned for a possible policy twist from the BoJ at the 31 July meeting.

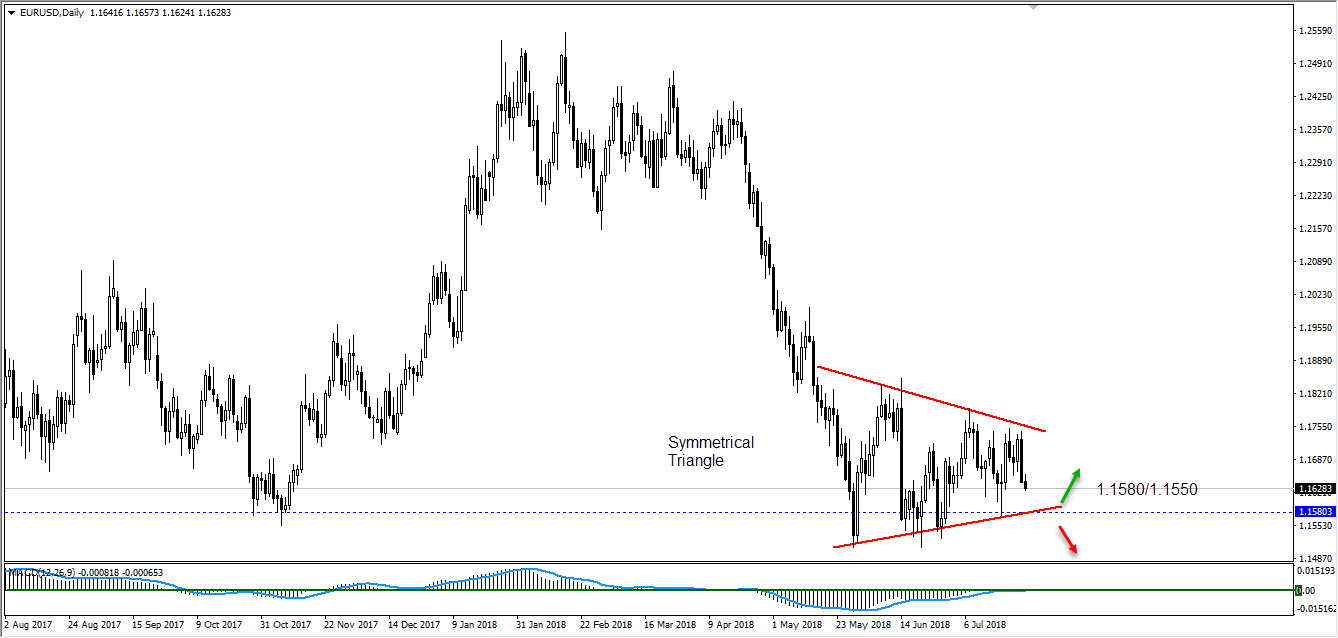

EURUSD

Trading within a symmetrical triangle. As shown in the chart the market is targeting the major support (area @ 1.1580/1.1550. If the support held then we would see a rebound to the 1.1750 resistance area. However, if market successfully broke the pattern then our target will be 1.1250.

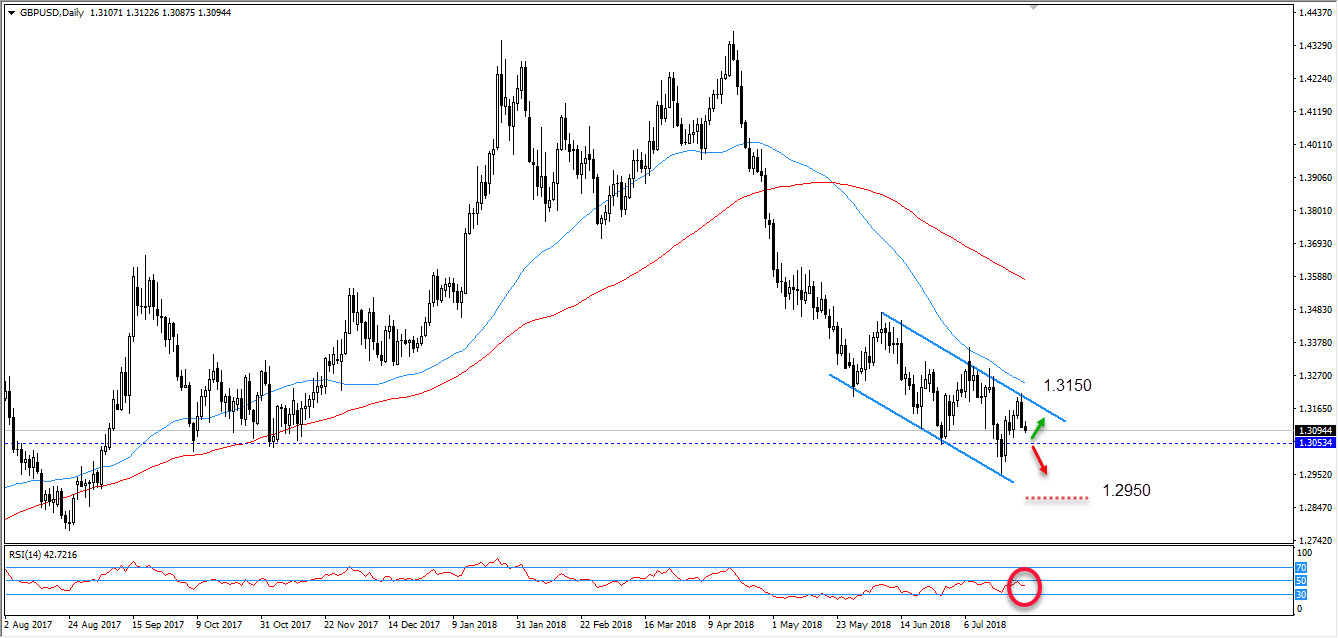

GBPUSD

Declining channel still valid. The pair failed to break the upper band of the shown channel, which increased the selling pressure on the pair. Market now will target the support area at 1.2920/1.2880.

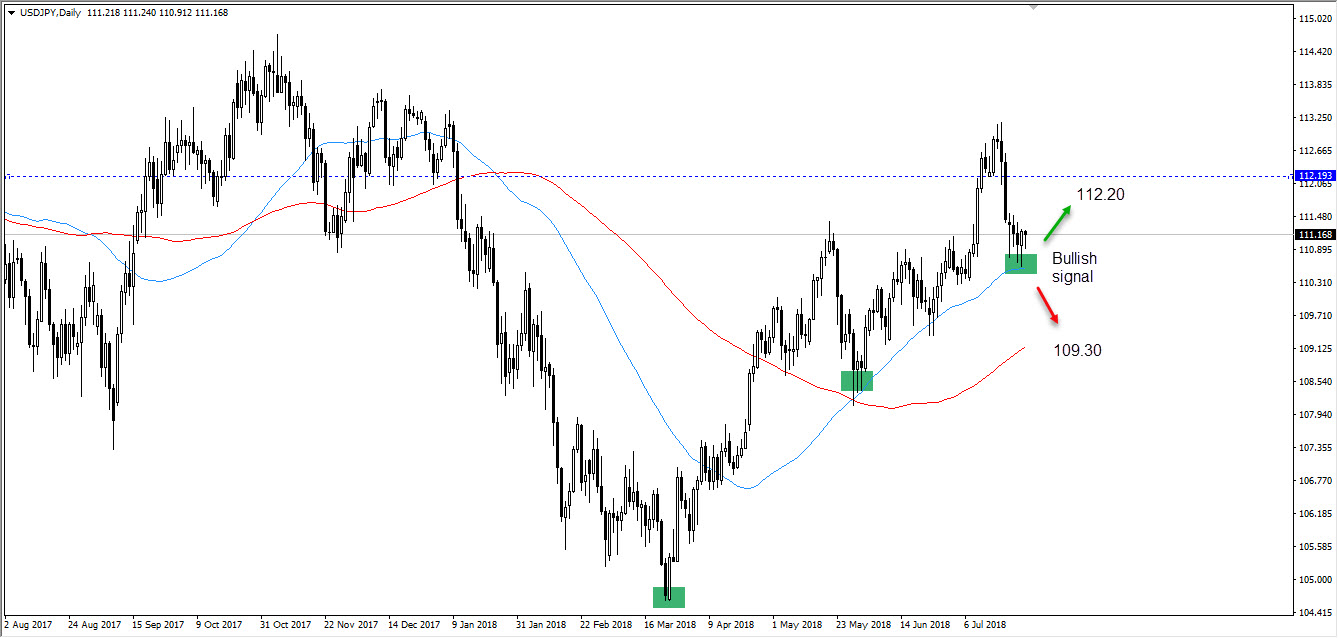

USDJPY

Renewed buying momentum. The 50-days SMA hold and we see a bullish signal. The next resistance will be at 112.20/112.50. However, an close below 110.50 hen the downside risk would be increased and the drop will be toward 109.30.

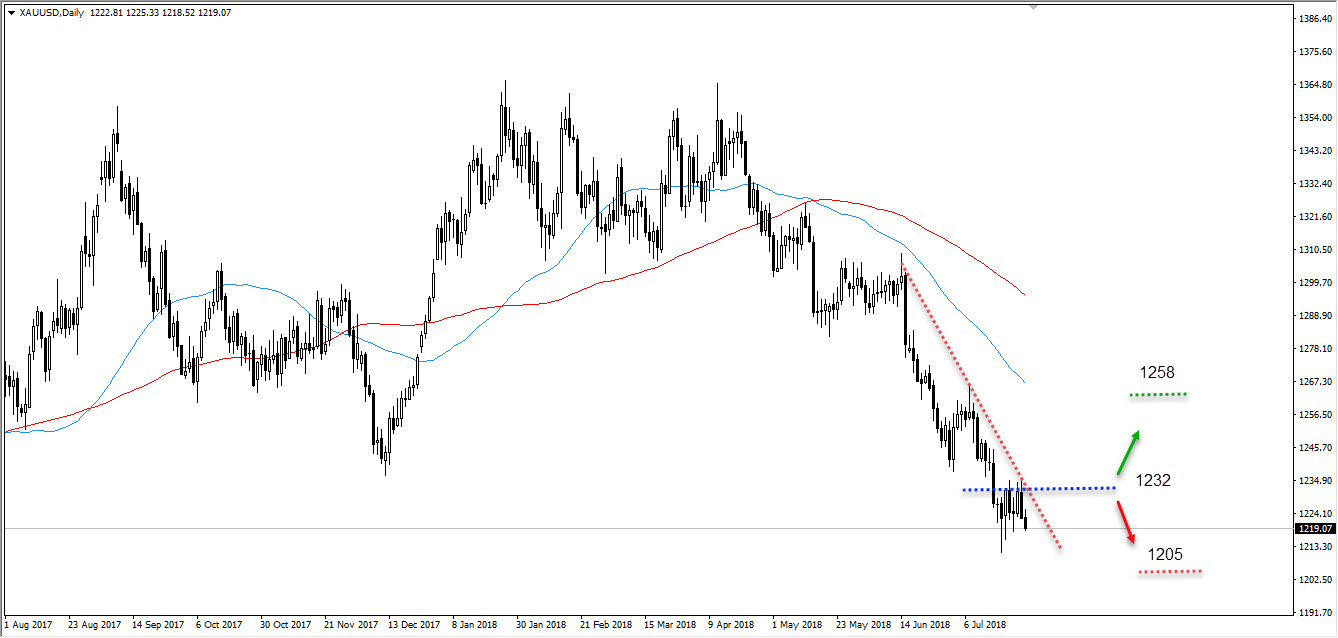

XAUUSD

The risk to break the support at 1212 is high. If the break occurred this would trigger a drop toward 1205/1198.

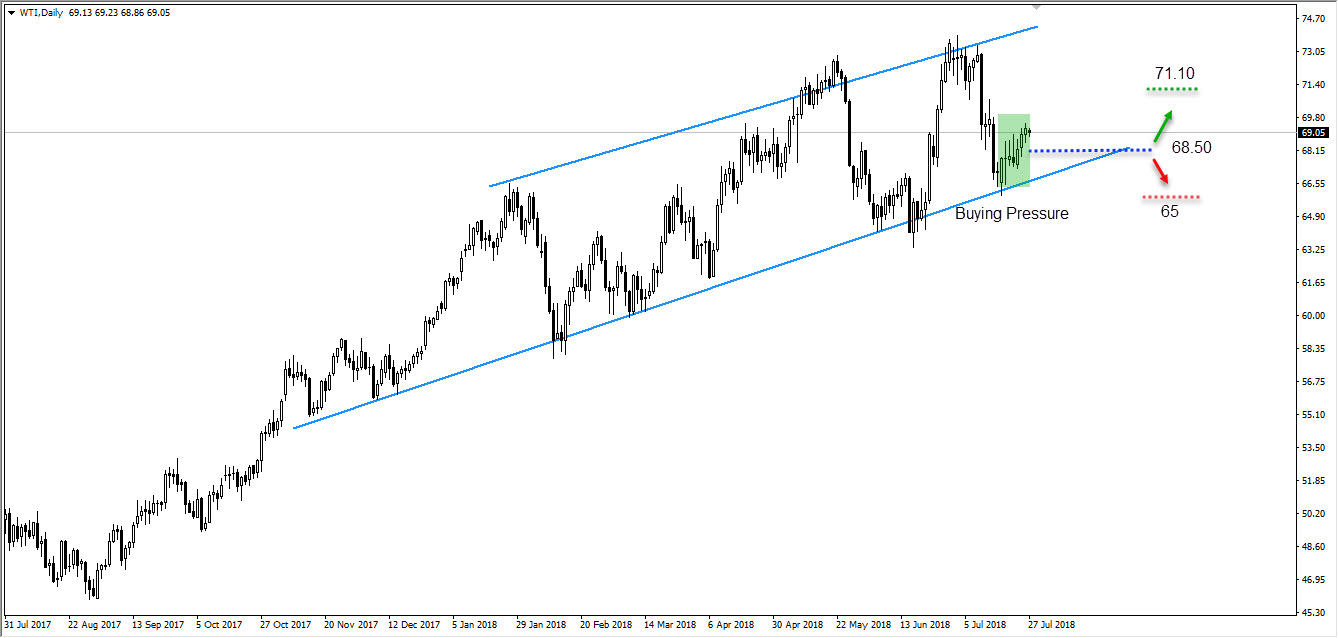

WTI

The bias remains bullish, has a target at 71.10. However, a move and close below 68.20 would signal a more of drop toward 65.

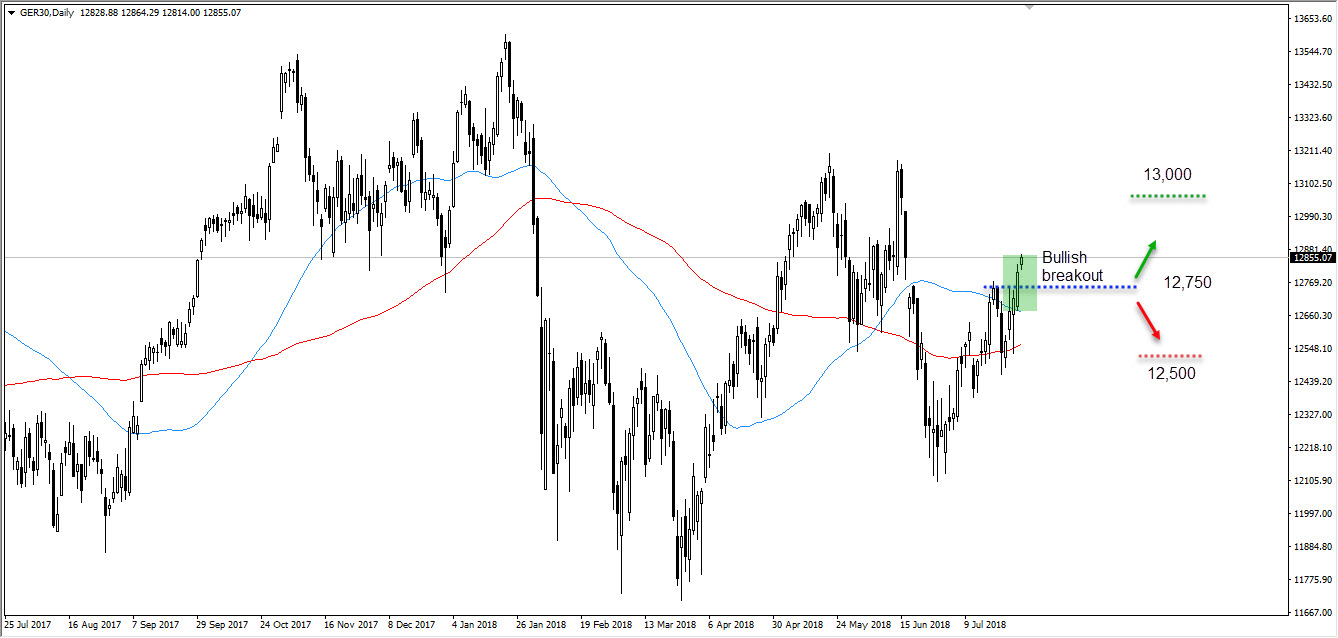

DAX

Bullish bias above 17,750 and markets now will target 13,000s levels.

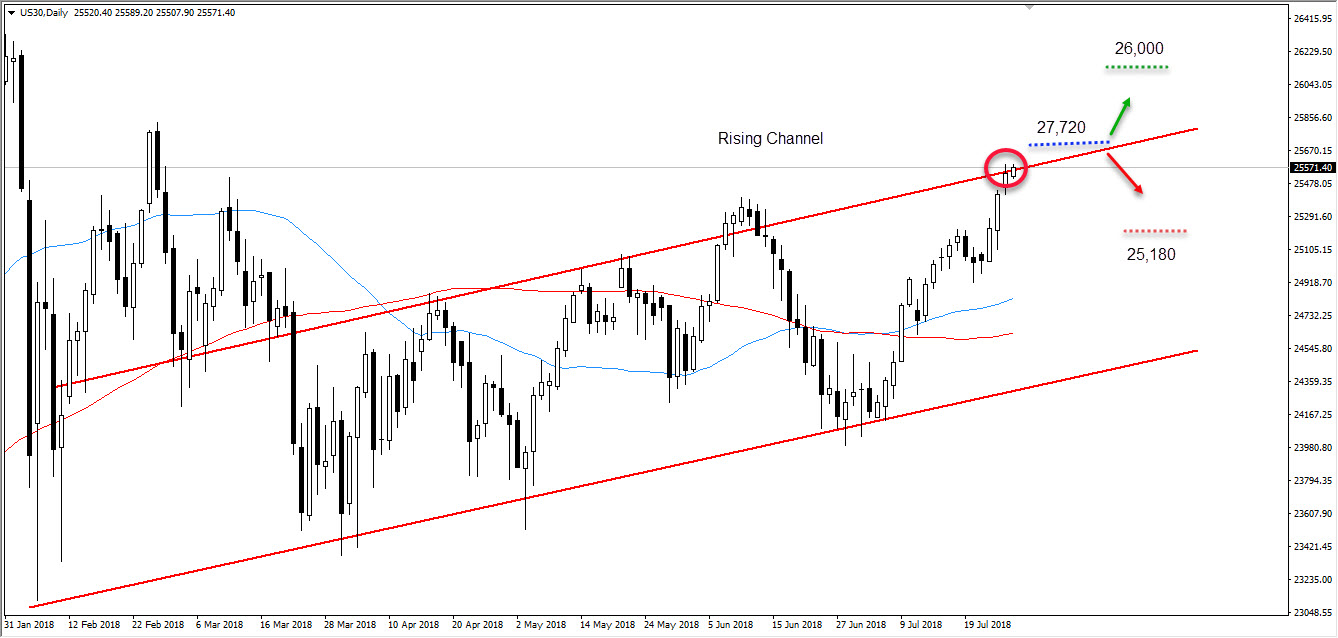

Dow Jones

As Long as the resistance at 25,720 is not broken, the risk to move back toward 25,180 remains high.

USD/CAD – Canadian Dollar Steady Ahead Of US Advance GDP

The Canadian dollar has ticked higher in the Friday session. Currently, USD/CAD is trading at 1.3074, down 0.03% on the day. On the release front, there are no Canadian indicators on the schedule. The U.S will release Advance GDP for the second quarter, with the markets expecting a strong gain of 4.2%. As well, UoM Consumer Sentiment is forecast to drop to 97.1 points.

Investors remained worried about the prospect of a full-blown trade war, as the U.S and its trading partners have in engaged in a tariff battle. However, the mood last week was one of “reconciliation” rather than “retaliation”, at least between the U.S and the European Union. A meeting between EU Commission President Jean-Claude Juckner and U.S President Trump was successful, as the two leaders agreed to take concrete steps to eliminate tariffs and improve the trade relationship between the U.S and the EU, which has been battered in recent weeks. President Trump agreed to hold back on any further tariffs while talks are ongoing. This is a major concession from Trump, who just last week had threatened to impose tariffs on European car imports. The agreement with the Europeans showed some surprising flexibility on the part of Trump, and Canadian policymakers are hoping that the conciliatory U.S stance will extend to the NAFTA negotiations with Canada and Mexico. The U.S has insisted on far-reaching changes to the pact, including its renegotiation in five years. If its demands aren’t met, the Trump administration has said it could pursue separate free trade agreements with Canada and Mexico. However, the latter two countries would like to maintain a trilateral arrangement. If the parties do reach a new agreement, the Canadian dollar would likely move higher.

The Canadian dollar posted strong gains on Wednesday, following an Energy Information Administration (EIA) report which showed a huge decline of 6.1 million in U.S crude inventories. This is the second decline in three months, and was much higher than the estimate of 2.6 million. Growing tensions between Iran on the one hand and the U.S and Saudi Arabia on the other have also raised concerns about oil supplies, and higher crude prices have boosted the Canadian dollar.