Sample Category Title

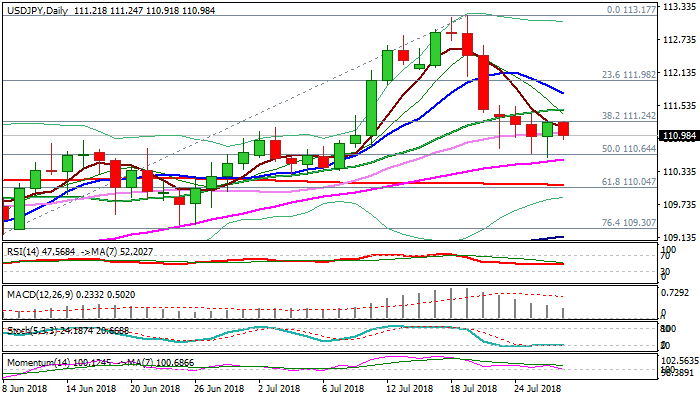

USDJPY Outlook: Break Out Of Congestion Between Kijun-Sen And 55SMA To Provide Direction Signal

The pair holds around 111 handle in early European trading on Friday, down from Asian high at 111.24, which also marks the high of Thursday’s rally.

Daily Kijun-sen capped upside attempts for the third straight day, marking strong resistance (reinforced by broken Fibo 38.2% of 108.11/113.17 upleg).

Long-tailed candles in past two days marked strong downside rejections after rising 55SMA offered footstep for the bear-leg from 113.17 (19 July six-month high) but provided little support in recovery attempts for now.

Near-term downtrend from 113.17 is still intact and risk of bearish continuation exists, as momentum is weakening.

On the other side, slow stochastic is reversing from oversold territory and gives positive signal while daily MA are in mixed setup, marking overall picture mixed and suggesting the pair may hold in extended consolidation before establishing in fresh direction.

The dollar enjoys support from strong fundamentals but is pressured by political factors, adding to mixed near-term signals.

Bearish signal could be expected on firm break below 110.64/55pivots (50% of 108.11/113.17 / rising 55SMA) which would open way towards strong supports at 110 zone (200SMA / Fibo 61.8% / daily cloud top).

The pair is on track for the second consecutive bearish weekly close, which supports negative scenario.

Conversely, close above daily Kijun-sen would generate bullish signal, which requires confirmation on break and close above 111.57 (Fibo 38.2% of 113.17/110.58 bear-leg).

Res: 111.24, 111.46, 111.57, 111.88

Sup: 110.91, 110.55, 110.10, 109.99

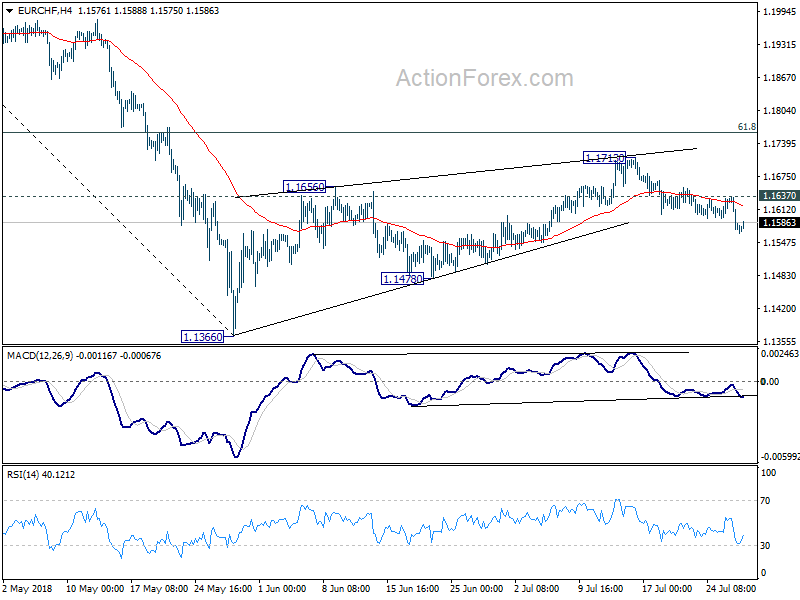

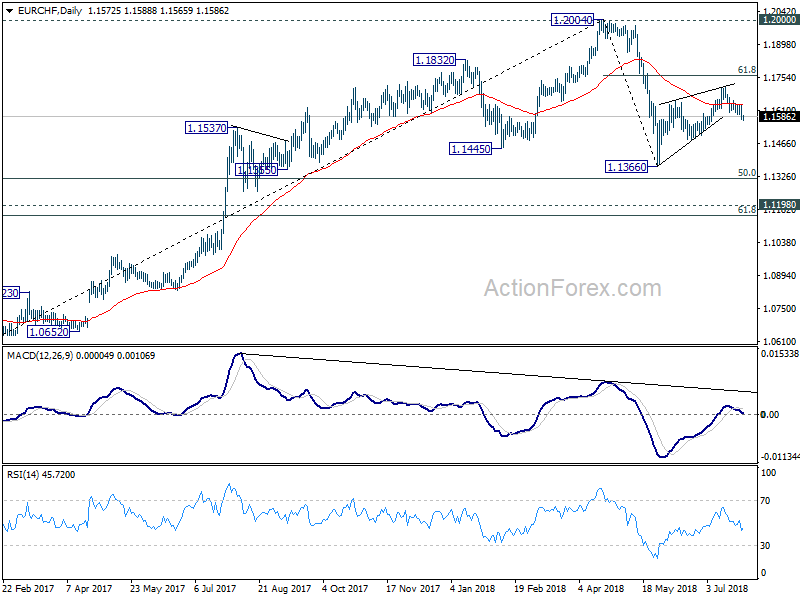

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1552; (P) 1.1596; (R1) 1.1619; More...

EUR/CHF's fall from 1.1713 resumes quickly after brief consolidation. Intraday bias is back on the downside for 1.1478 support. We're holding on to the view that corrective rebound from 1.1366 has completed with three waves up to 1.1713 already. Break of 1.1478 will confirm and pave the way to 1.1366 low. On the upside, above 1.1637 minor resistance will turn bias back to the upside and could extend the rise from 1.1366. But even in that case, we'd expect strong resistance from 61.8% retracement of 1.2004 to 1.1366 at 1.1760 to bring near term reversal.

In the bigger picture, 1.2004 is seen as a medium term top with bearish divergence condition in daily and weekly MACD. 1.2000 is also an important resistance level. Hence, the corrective pattern from 1.2004 is expected to extend for a while before completion. We're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

US-China Trade: No Deal in Sight

- The trade deal between the EU and the US has left the question of whether a similar positive development could be seen between the US and China. However, since Trump left the negotiating table at the end of May, there has been no sign of trade talks between the US and China. We do not see any deal between the two countries this side of the mid-term elections in November.

- While Trump has very little backing in the US for a confrontation with the EU and other allies, he is under a lot of pressure to stick to a tough course with China.

- We believe we are heading for further escalation, when Trump is likely to implement 10% tariffs on another USD200bn worth of Chinese goods in mid- October. It is set to trigger Chinese retaliation with similar force — followed by a Trump warning of even more tariffs.

- The key challenge is that China has little more to offer than it has done already. While Trump's strategy seems to be that more pressure will make China give him a better deal. This is unlikely to happen, in our view. It leaves a very uncertain outlook for how far the 'tit-for-tat' trade war can go.

The US-China trade spat continues to move in ebbs and flows but unfortunately with a clear direction: towards worsening. For now, the tensions have moved to the background. However, they are likely to come back into focus when the hearings for US tariffs on another USD200bn worth of Chinese imports are over and the tariffs kick in. This is likely to be in mid-October, just ahead of the mid-term elections on 6 November.

Listening to comments from both US and Chinese politicians, it is hard to see how a deal will be struck. They are too far from each other on the real cause of the US-China trade deficit, what China can do about it and what China is doing on intellectual property rights. More importantly, though, the US demand that China dismantles it's 'Made in China 2025' strategy, which focuses on technology investments, is simply a no-go for China.

On the following pages, we give a summary of the key views on both sides as stated in interviews and statements over the past months.

The US view: stop cheating and stealing or face tariffs

#1: The ball is in China's court

In a CNBC interview on 18 July, Trump's economic advisor, Larry Kudlow, said there were no talks going on between US and China at the moment and that "In so far as we know, President Xi at the moment does not wish to make a deal… I think Xi is holding the game up… The ball is in his court". Two days later Trump said in an interview also with CNBC that "Were ready to go to 500 [USDbn of Chinese imports]". It doesn't suggest to us that the US is in a mood to take the first step to restart negotiations.

#2: US can only win a trade war - and this is the time

The US administration signals it has the strongest hand in the trade war. In a tweet on 4 April Trump stated "When you're already $500 Billion DOWN, you can't lose!" His trade adviser Peter Navarro stated in a Fox News interview that "They depend on us a whole lot more than we depend on them". Trump has clearly signalled that now is a good time to take the confrontation. Responding to a question in the CNBC interview he said very clearly "This is the time" referring to the strong US economy and the stock market. The fact that the Chinese economy is slowing and stocks have plummeted in China is likely encouraging Trump to stick to the strategy.

#3: Give us a fair deal or feel the heat from tariffs

Trump faced strong criticism in the US after the initial negotiations with China and he is under a lot of pressure from both fellow Republicans as well as Democrats to be tough with China. As a deal maker he needs something to put pressure on China and tariffs is the main tool in his tool box. The view was also reflected in the tweet on 24 July stating:

"Tariffs are the greatest! Either a country which has treated the United States unfairly on Trade negotiates a fair deal, or it gets hit with tariffs. It's as simple as that…"

On 25 July Trump stated in another tweet that "China is targeting our farmers….as a way of getting me to continue allowing them to take advantage of the U.S. They are being vicious in what will be their failed attempt. We were being nice - until now! China made $517 Billion on us last year."

#4: "We have been ripped off by China for a long time"

In the CNBC interview mentioned above, Trump repeated his campaign pledge that the US has been "ripped off by China for a long time". The US administration points to higher Chinese tariffs relative to US tariffs, technology theft, state subsidies, non-tariff trade barriers and barriers to investments in China. On top of this the US wants China to back down from the "Made in China 2025" strategy, which focuses on big investments within technology over the coming years. In the announcement of new tariffs it said: "For over a year, the Trump administration has patiently urged China to stop its unfair practices... China has not changed its behaviour – behaviour that puts the future of the US economy at risk".

#5: WTO is broken – bad deal negotiated by former presidents

Finally, the Trump is a big opponent of WTO and some reports mention he wants to pull out of it - although his advisers have so far kept him from doing it, see story in Business Insider. Larry Kudlow stated again on CNBC that "The world trading system is broken. WTO is broken". As with other international deals Trump has withdrawn from, he is blaming it on previous US Presidents that made bad deals and he wants to fix it.

The China view: Trump wants tariffs and nothing can stop it

#1: The ball is in the US court

In the eyes of China, it was the US that left the negotiating table and therefore, the ball is in their court to restart negotiations. In response to Kudlow's comments that Xi Jinping was holding up the negotiations, a Chinese Foreign Ministry spokeswoman called it "bogus accusations". When Trump left the negotiation table in May, the Chinese spokeswoman said "Every flip-flop in international relations simply depletes a country's credibility". China will probably be cautious to go back to negotiations as they don't see Trump as sincere in the trade talks.

That China has lost faith in a deal and is preparing for trade war is signalled by the recent policy easing of both monetary and fiscal policy with reference to "external uncertainty". A China Daily editorial on 10 July, with the title "China ready and able to counter US trade attack", said that "The timely release of supportive policies to strengthen the protection of the legitimate rights and interests of the country's export-related enterprises and create a better investment environment shows that the Chinese authorities are expecting the maleficent actions of the United States to be both protracted and inexorable".

#2: US wants to rob China of its future — concessions will never be enough

China has over the past year and during the negotiations accommodated a range of the critique points by the US. It has: 1) offered to buy more U.S. products of a value up to around USD100bn (the exact amount is not known) primarily within agriculture and energy; 2) reduced tariff levels (implemented 1 July); 3) further opened up for investments within both services and manufacturing; 4) vowed to increase efforts to protect intellectual property rights and 5) vowed to stop forced technology transfer.

However, on one point China will not meet the US. That is the demand to dismantle the "Made in China 2025" strategy, which focuses on investments within 10 sectors, primarily high-tech sectors. It sees the strategy as legitimate and necessary for China to avoid the 'middle-income trap', as numerous studies point to the need to invest in technology and innovation to avoid growth stalling at the current level of GDP per capita. Countries like Taiwan and South Korea, which have avoided the 'middle-income trap', all focused on technological upgrade at the development stage China is now at.

In the editorial in China Daily mentioned above it says: "…its [Trump administration's] ultimate goal is not the rebalancing of trade to reduce the US' deficit with China or even greater access to the Chinese market, its fundamental objective is to hinder China's development… It wants to rob China and the Chinese people of their future. Thus China will not be able to appease Washington no matter how it manages its trade or economy."

#3: China to continue one-to-one retaliation to what is seen as unfair tariffs.

China sees the tariffs as illegitimate and the strategy has so far been to retaliate one-to-one, both in terms of amount and timing. China has not yet been specific about how it will respond if Trump implements the 10% tariff on another USD200bn of Chinese imports. But the Commerce Ministry stated after the US announcement that "To protect the core interests of the nation and its people, China's government is, as in the past, forced to retaliate". As Chinese imports of US goods is only USD130bn, it's not able to match on amount. But there are a range of other ways it can hit the U.S. China can raise tariff rates to more than 10%, inhibit US investments in the US or start a consumer boycott (the latter has been used against Japan and South Korea previously).

#4: Trade deficit does not measure relative benefits of economic relationship

China disagrees with the US on both the causes of the trade deficit as well as the significance of the trade deficit as a measure of the relative benefits of US-Chinese economic cooperation.

First, the trade deficit is overestimated because it doesn't take into account that only a small part of the export value from China is actually created in China. Today's global supply chain often has China as the end point of production, or assembly, as components produced in other countries are imported to China, assembled and then shipped off to the U.S. and other countries. This makes Chinese exports vastly overestimated, because it is not based on the value that is added in China but instead on the full value of the product when it leaves China, see this paper from China Business Review for further elaboration on this issue.

Second, the US runs a USD40bn surplus on the service balance with China (a lot of it due to Chinese tourists in the US). There is no good reason why one should only look at goods' trade, but not include service trade when gauging trade between two countries.

Third, sales of US subsidiaries in China are not captured by the trade balance. In 2015 US companies within China had a turnover of USD221.9 bn. There are no data for turnover of Chinese companies in the US but there are generally few Chinese companies in the US selling to US consumers. The turnover should be included when evaluating the relative benefits of US-China economic relations.

Fourth, the US could export to China if it didn't have controls on exports of technology goods. Products that China has a high demand for as they are needed in the upgrade of its production. But these are protected for security reasons in the US. Fifth, the US trade deficit is to a large extent due to the low savings rate of the US, something that China cannot affect. A rising public deficit is only worsening the savings balance and will work to increase the trade deficit. For the same reason China cannot commit to a specific reduction of the trade deficit. Trump has asked for a reduction in the deficit of USD200bn by 2020 in the negotiations.

#5: China will not accept tariffs not based on WTO rulings

China does not accept tariffs that are based on the US' own investigations and not on independent rulings by the WTO. On 29 June 2018, China released a white paper called "China and the World Trade Organization", which concludes that China has "faithfully fulfilled its WTO Accession Commitments" and that China "firmly supports the Multilateral Trading System".

Conclusion: A deal is still far away

With a still big gap in what Trump is demanding and what China is willing to give, we see little scope for a deal anytime soon. Lack of trust on China's side and the fact that it has already eased policy to counter the negative effects of a trade war suggests that things still have to get worse.

We believe we at least have to get beyond the mid-term elections in the US on 6 November before any deal is back on the table. And even after that it is not clear how Trump is going to get a deal that he can present as a victory. China will not give in to demands to change its "Made in China 2025" strategy and this will keep the China hawks on both the Democratic as well as Republican sides in favour of a tough stance on China.

A caveat is, of course, that Trump sometimes changes his mind fast and could suddenly go back to the negotiation table again. The case with North Korea showed how he can turn quickly. But it was on the back of Kim Jong-Un making big concessions and we doubt that China will do the same.

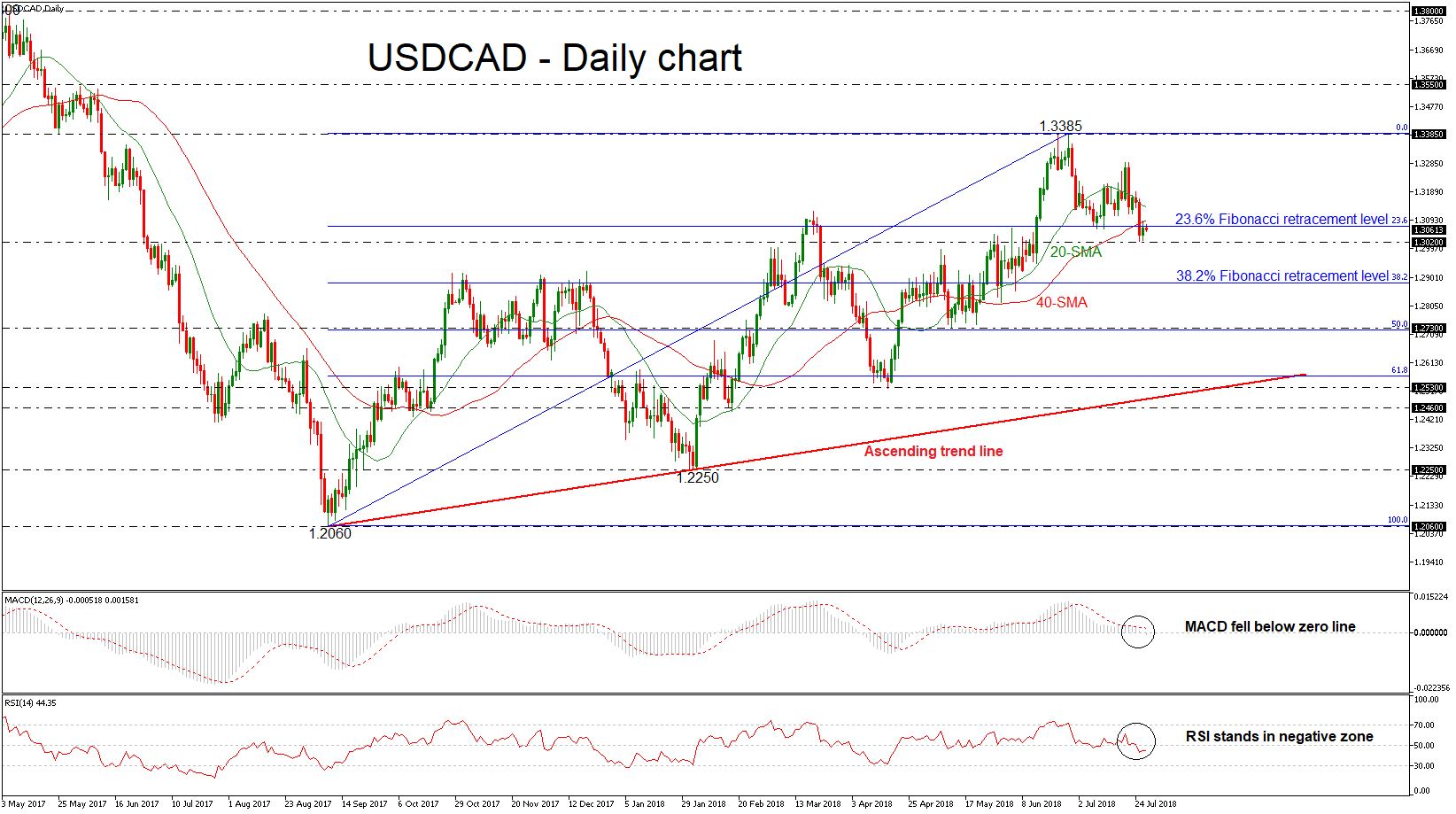

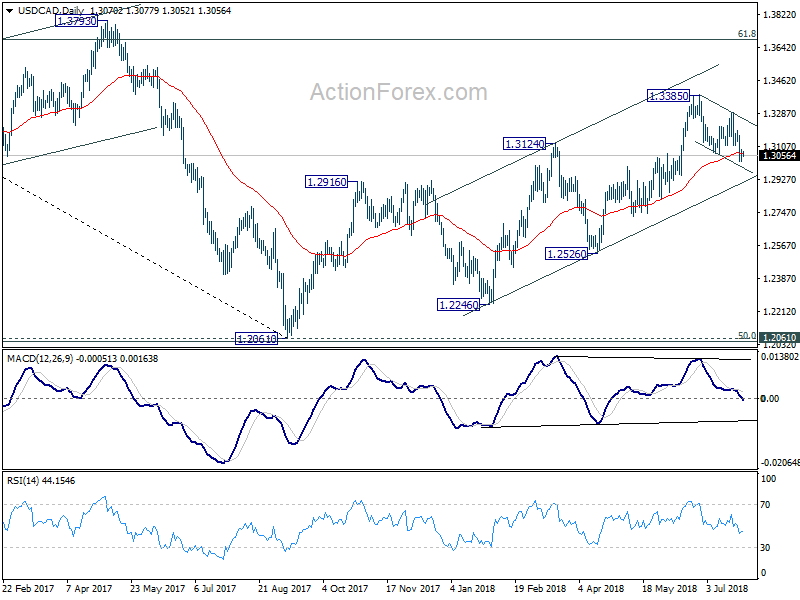

USDCAD Slips Below 23.6% Fibonacci, Bearish Correction Is Possible

USDCAD remains under pressure as it holds below the 23.6% Fibonacci retracement level of the upleg from 1.2060 to 1.3385, around 1.3073. Moreover, the price plummeted below the 20- and 40-simple moving averages (SMAs) on Wednesday in the daily timeframe, indicating for a possible bearish correction.

From the technical point of view, the momentum indicators seem to be negative and the market could ease a little bit more in the short-term. The RSI indicator is in negative territory after declining sharply in recent days. Also, the MACD oscillator dropped below the zero line and stands far below the trigger line.

Should prices decline further, immediate support could be found at the 1.3020 bottom, taken from the lows in the last few days. Then a leg below that level, the price could meet the 38.2% Fibonacci mark of 1.2880, increasing chances for further bearish movements.

If the market manages to pick up speed and jump above the 23.6% Fibonacci and the 20- and 40-SMAs, the one-year high of 1.3385 could offer nearby resistance for the bulls. A significant close above this level would drive the pair towards the next hurdle of 1.3550 taken from the highs on June 2017.

Having a look at the bigger picture, the greenback seems to be in a strong bullish rally against the loonie as it has been holding within an ascending movement since September 2017.

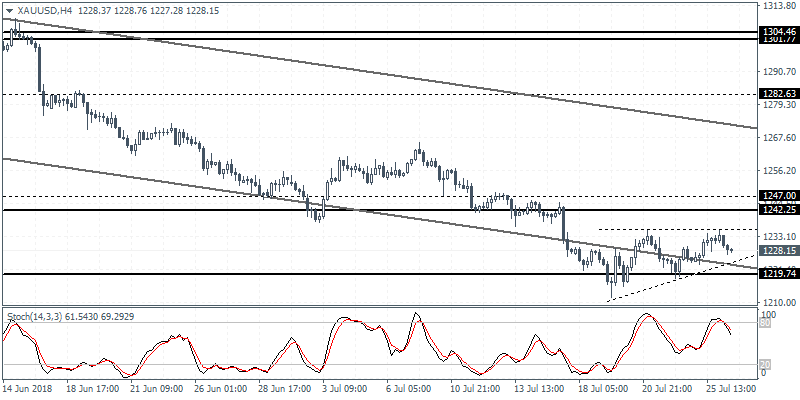

XAUUSD Intraday Analysis

XAUUSD (1228.15): Gold prices continue to consolidate around the 1225 - 1219 levels. However, on the 4-hour chart, the ascending triangle pattern is signaling a potential upside breakout. With the resistance level formed at 1235 region and the minor rising trend line that is holding the higher lows being formed, a potential upside breakout could trigger gains toward the 1250 handle. To the downside, a breakout from the rising trend line could send gold prices to test the horizontal support formed at 1219.

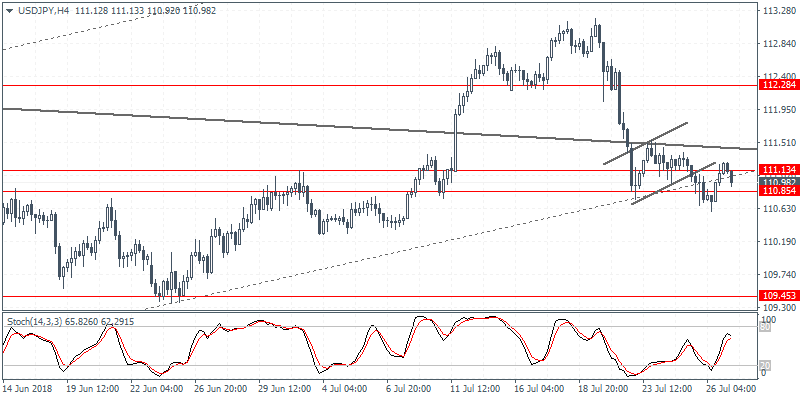

USDJPY Intraday Analysis

USDJPY (110.98): The USDJPY was seen trading somewhat flat on the day as price action managed to post a minor bounce. This brief retracement was met with the resistance level at 111.13 before the currency pair is starting to give up the modest gains. A close below the previous low at 110.71 is required in order to confirm the downside bias. This would also validate the bearish flag pattern and set USDJPY on stage for further declines. The support at 109.45 remains a key level of interest to the downside. The bearish flag pattern projects the minimum price target around this level.

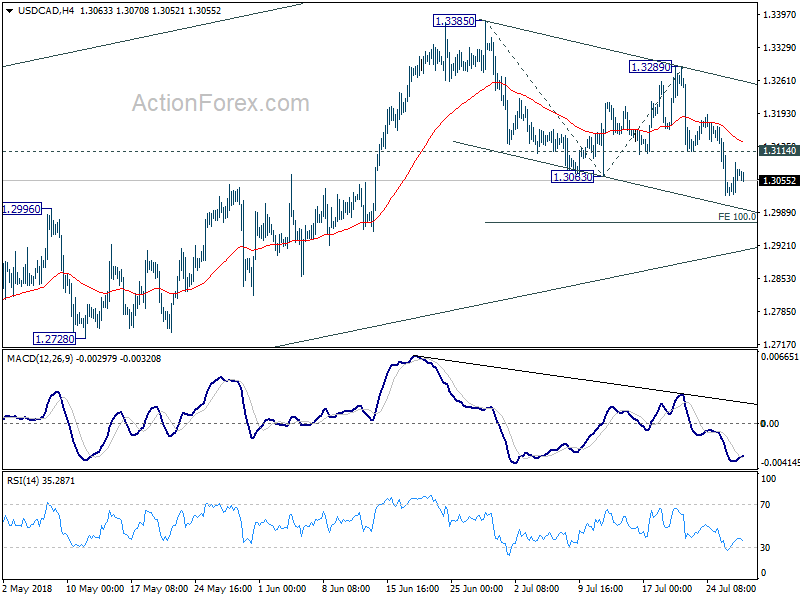

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3037; (P) 1.3066; (R1) 1.3106; More...

With 1.3114 minor resistance intact, deeper fall is still expected. Corrective decline from 1.3385 would extend to 100% projection of 1.3385 to 1.3063 from 1.3289 at 1.2967 and possibly below. But still, we'd expect strong support from rising channel line (now at 1.2912) to contain downside and bring rebound. On the upside, above 1.3114 is the first sign of bottoming and will turn bias back to the upside for 1.3289 resistance. Overall, the larger rally from 1.2061 is still expected to resume later.

In the bigger picture, as long as channel support (now at 1.2912) holds, we're holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

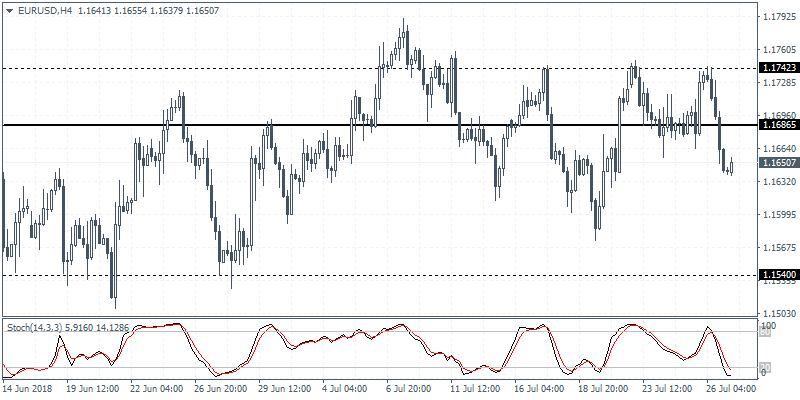

EURUSD Intraday Analysis

EURUSD (1.1650): The euro currency posted strong losses on the day after the ECB's meeting. The declines came as the currency pair failed to clear the resistance level of 1.1730 resulting in a bearish candlestick being formed. Price action however remains trading sideways in the long term bearish trend. On the 4-hour chart, the declines look to have stalled for the momentum. A bullish follow through is required as the EURUSD could potentially be forming an inverse head and shoulders pattern. The neckline resistance is formed at 1.1742. A breakout above this level will trigger gains to 1.1824 - 1.1846 level. Alternately, a close below the previous lows at 1.1584 could however invalidate the bullish view.

U.S. Advance Q2 GDP Forecast To Rise 4.1%

The ECB's monetary policy meeting was uneventful as the central bank left interest rates and QE unchanged. The ECB president Mario Draghi stuck to the comments from the June meeting. Although the ECB did not surprise the markets, the euro was seen posting strong losses on the day.

The common currency fell 0.73% against the U.S. dollar. Gold managed to post strong gains on the day rising 0.59% by Thursday's close.

From the overnight trading session, data from Japan showed that Tokyo core CPI advanced 0.8% on the year beating estimates of a 0.7% increase.

In Australia, the producer prices were seen rising 0.3% on the quarter ending June 2018. This was below estimates of a 0.5% increase and marked a slower pace of increase compared to the first quarter's print of 0.5%

Looking ahead, the economic calendar today will see the release of the German import prices and French consumer spending details. In the NY trading session, the U.S. department of commerce will be releasing the advance GDP report for the second quarter. Estimates show that the U.S. economy grew at a pace of 4.1% in the second quarter ending June 2018. This comes following a 2.2% increase in the first quarter.

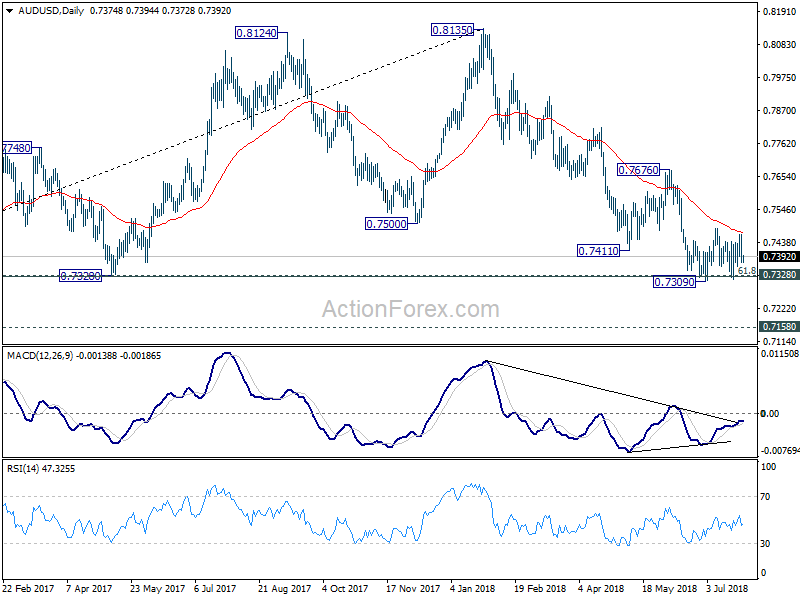

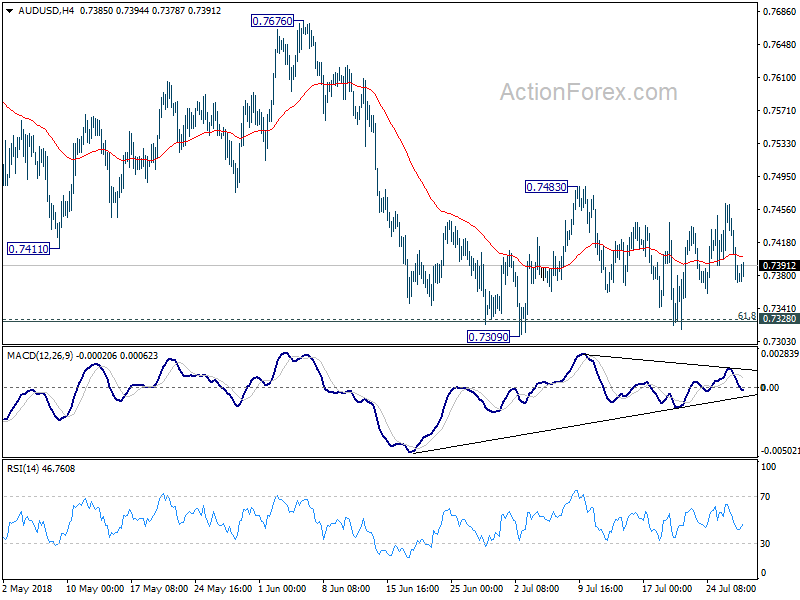

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7345; (P) 0.7404; (R1) 0.7436; More...

Outlook in AUD/USD remains unchanged as it's bounded in consolidation from 0.7309. Intraday bias remains neutral at this point. In case of stronger recovery, upside should be limited below 0.7676 resistance to bring larger fall resumption. On the downside, break of 0.7309 and sustained trading below 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.