Sample Category Title

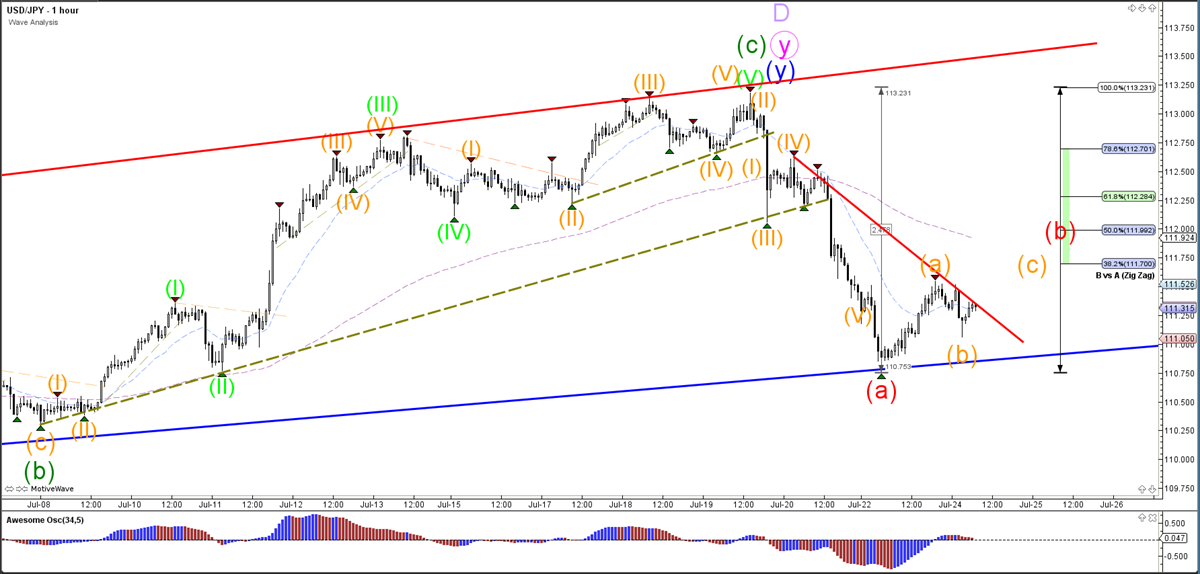

USD/JPY Bullish ABC Pattern In Bearish Wave B

Eventually a bearish bounce is expected due to the ABC zigzag pattern. Price should stop at the Fibonacci levels of wave B vs A whereas a break above 100% Fib level invalidates the bearish ABC.

Despite the strong bearish momentum on the USD/JPY, price made a bullish bounce at the support trend line (blue). This could confirm the end of wave A (red) and the start of wave B (red). Eventually a bearish bounce and break is expected due to a potential ABC (red) zigzag pattern. Price should stop at the Fibonacci levels of wave B vs A whereas a break above the 100% Fibonacci level invalidates the bearish ABC.

The USD/JPY seems to be building an ABC pattern (orange) within wave B (red). A bullish breakout could indicate above the resistance trend line (red) could indicate a larger bullish wave C (orange) pattern in wave B (red).

GBP/USD Bearish Price Action Challenges Support Fibs

The GBP/USD remains in a downtrend despite yesterday’s bullish momentum. The impulsive price action however could indicate a larger reversal if price manages to stay above a key support level.

The GBP/USD needs to stay above the green trend line if it wants to confirm a bullish wave A (blue) as part of a larger ABC zigzag pattern. A bearish break below this line could indicate a larger bearish push lower and a retest of the previous bottom and perhaps channel support (blue).

The GBP/USD could be building a 5 wave (green) pattern within wave A (blue) if price manages to stay above the top of wave 1 (green line). A break below it could either mean a new downtrend or a that the bullish 5 waves were already completed at the recent high. Price is now challenging the Fibonacci levels of wave 4 vs 3 (green) which could be bouncing spots if price is indeed in a wave 4. The confirmation of a potential wave 4 occurs when price is able to break above the resistance trend lines marked in the chart by a red and orange line. In that case a wave 5 of wave A could be starting.

Elliott Wave Analysis: Amazon May Start Another Extension Higher

Amazon ticker symbol: $AMZN short-term Elliott wave analysis suggests that pullback to $1646.48 low ended intermediate wave (2). Above from there, the stock is rallying higher in intermediate wave (3) higher. The internals of that extension higher is unfolding as Elliott wave impulse structure with sub-division of 5 waves structure in lesser degree Minor wave 1, 3 and 5.

Above from $1646.48 low, the rally to $1858.88 high ended Minor wave 1. The internals of that rally higher took place in another 5 waves impulse sequence in lesser degree cycles. The first leg of a rally to $1725 high ended Minute wave ((i)) as Leading diagonal structure. Then the pullback to $1682.15 low ended Minute wave ((ii)) pullback as a Zigzag correction. Up from there, the rally higher to $1841.95 ended Minute wave ((iii)) in 5 waves. Minute wave ((iv)) pullback ended at $1791 low, and Minute wave ((v)) of 1 ended at $1858.88 high.

Below from there, the stock did a 3 wave pullback in Minor wave 2, which is proposed to have completed the correction against $1646.48 cycle low. After reaching the blue box 100%-123.6% Fibonacci extension area at $1786.77-$1775.40. However, a break above $1858.88 high remains to be seen to validate this view & until then, a double correction lower in Minor wave 2 can’t be completely ruled out. Near-term, while dips remain above $1769.99 low and more importantly above $1646.88 low the stock is expected to resume the upside. We don’t like selling it.

Amazon 1 Hour Elliott Wave Chart

Currencies: USD Dollar To Receive Additional Interest Rate Support?

Rates: Core bond sell-off accelerates

Upside risks to EMU PMI's, the start of the US Treasury's end-of-month refinancing operation, positive risk sentiment and technical factors all suggest that the two-day sell-off on core bond markets isn't over yet. US Treasuries could underperform German Bunds.

Currencies: USD dollar to receive additional interest rate support?

Yesterday, core yields jumped higher after a long consolidation period. The move mainly favoured the yen and the dollar even as the moves in the major USD cross rates remained modest. The dollar might remain well supported going into the publication of the USD Q2 GDP later this week

The Sunrise Headlines

- US stock markets closed mixed on Monday with marginal gains and losses. Asian markets all opened in green, with China out performing marking gains around 1.5% on its major indices.

- After its central bank injected a monetary stimulus of $74bn yesterday in its banking system, China unveiled a package of fiscal policies to boost domestic demand as trade tensions threaten to worsen the economic slowdown.

- BoE's Broadbent yesterday stated that reversing QE would not be a hawkish signal as interest rates remain the central bank's main policy tool. He also said not to have decided on his voting intentions for the policy meeting next week.

- Eurozone consumer confidence remains unchanged at -0.6 in July (-0.7 expected) after the June number was revised from -0.5 to -0.6, indicating economic growth may be stabilizing going into the third quarter.

- Japan's manufacturing sector grew at its slowest pace since November 2016, with its preliminary PMI dropping from 53.0 to 51.6 in June. Output and new orders grew at a slower pace while export orders decreased at a slower rate.

- Italy's Deputy Premier Matteo Salvini stated that he would flout EU budget rules if it were “for the good of the Italians”, causing a struggle within the government where finance minister Tria preached to stay within those EU limits.

- Today's eco calendar contains the Richmond Fed Manufact. Index for July in the US and PMI numbers in the eurozone

Currencies: USD Dollar To Receive Additional Interest Rate Support?

Dollar to receive additional interest rate support?

Yesterday, bond yields at once rose from Japan to the US. Speculation on a policy adjustment at next week's BOJ meeting initially propelled the yen. However, the USD/JPY decline was reversed as US (and European) yields joined the rise. US-German spreads are again nearing the cycle peak (especially for the 2-y). At the end of the day, the moves in the major USD cross rates were modest, given the swings in yields. USD/JPY closed the day little changed at 111.35. EUR/USD closed at 1.1692, reversing part of Friday's 'Trump-driven' USD decline. Overnight, Asian equities show good gains, with China outperforming. Investors see more room for PBOC stimulation if necessary. The yuan dropped to the lowest level in more than a year (USD/CNY 6.82). USD yields are marginally lower after yesterday's rise. USD/JPY stabilizes in the lower half of 111. EUR/USD is losing a few ticks (1.1680 area).

Today, EMU PMI's and the Richmond Fed manufacturing index will be published. The EMU composite PMI is expected to ease marginally to 54.8. Markets will still look for further impact from trade tensions on sentiment. We also keep an eye at the US bond auctions, starting with the sale of 2-year Notes. Question is whether core yields will continue yesterday's rise and whether the US/German spread will rise further. Investor anticipation on a strong Q2 US GDP on Friday might support US yields. This might be a USD supportive in the shortterm. A positive risk sentiment might be slightly in favour of the euro. Headlines on trade remain a wildcard ahead of tomorrow's meeting between US president Trump and EU's Juncker. Of late, USD/USD hovered in the 1.15/1.1850 trading range. This range won't be easy to break. In a day-to-day perspective, EUR/USD might again drift a bit lower in this range. However, last week's Trump comments might still cap a big leap higher of the USD. The upside momentum of USD/JPY also looks to be broken.

Yesterday, sterling regained slightly ground against the euro. Cable declined on a stronger dollar. New UK foreign Secretary Hunt said that there is a real risk of no Brexit deal. However, the headlines didn't hurt sterling anymore after last week's decline. BoE's Broadbent didn't give a clear hint on his vote for next week's BOE meeting. Today, CBI order data/sentiment will be published. If data are OK and in case of no high profile negative Brexit headlines, a further modest technical comeback of sterling (against the euro) might be on the cards.

EUR/USD: Dollar receives interest rate support, despite last week's comments from president Trump

German PMI hit 5 month high, growth regains momentum

German PMI manufacturing rose to 57.3 in July, up from 55.9, way above expectation of 55.7. PMI services dropped to 54.4, down from 54.5 and missed expectation of 54.5. PMI composite rose to 55.2, up from 54.8, and hit a 5- month high.

Commenting on the flash PMI data, Trevor Balchin, Economics Director at IHS Markit said:

"Private sector output growth in Germany continued to regain momentum in July, having previously sank to a 20-month low in May. The manufacturing sector was the source of stronger growth in the latest month, after services had driven the expansion in June.

"Private sector employment continued to expand at a historically sharp rate in July, with the pace unchanged from June's five-month high. Manufacturers added staff at a faster pace than service providers for the seventeenth consecutive month.

"Data on new business were less positive than the trends for total activity and jobs, however. This mainly reflected new orders in manufacturing not rising as fast as output, resulting in the slowest rise in backlogs in the sector for two years.

"The latest survey also signalled greater inflationary pressures in July, with both input and output prices rising more steeply. Manufacturers widely reported higher steel prices, and supply shortages from China in general. Meanwhile, service providers hiked their own charges at the second-fastest rate on record."

Equities Rally As Yuan Extends Declines

China's Yuan is back under pressure,as the dollar bulls returned and the People's Bank of China seems to be shifting towards a looser monetary policy to offset the impact of U.S. trade tariffs &slowingdomestic economy. The PBoC injected a record $74 billion of Medium-Term Lending Facility credit into major banksyesterday. This stepcomes after the central bank has already cut its reserve requirements three times in 2018,with furthercuts expected in the next couple of months.

It is becoming evident that China is on the path towards a looser monetary and fiscal policy. Such steps will eventually support the domestic financial markets. The CSI 300 Index traded 2% higher on Tuesday, afteritfell into a bear market earlier in June. Meanwhile, the Yuan weakened to a 13-month low totrade past 6.8 per dollar. The Yuan's fall and Dollar's strength come despite President Trump's accusation last week that China and the E.U. are manipulating their currencies. Although a weaker Yuan may offset some of the trade tariffs'impact, further sharp declines will likely lead to capital outflows and another round of panic selling in emerging markets equities &debt. After breaking 6.8, all eyes will be on thepsychological level 7, which most likely be the trigger for the selloff.

Bond markets also seemed to bechallenging Trump's criticism of the Federal Reserve's tightening stance. Not only did the U.S.10-year yields bounced to a 5-week high of 2.97%, but the shorter term 2-year yields also hit a new decade high of 2.64%, suggesting that the Fed will raise interest rates two more times in 2018.

Despite the war of words between President Trump and his Iranian counterpart Hassan Rouhani, gold and oil prices edged lower on Monday and during early Tuesday trade. The fall in both commodities suggests that investors are not expecting further escalation in tensions and are insteadfocusing on market fundamentals.

The precious metal is likely to remain under pressure if emerging market currencies continue to plunge, particularly the Yuan. The correlation between the Yuan and the Gold has been so strong recently and I think this will continue to be the case for the foreseeable future.Gold has been on a downtrend since April, and last week managed to break below the uptrend line from December 2015. The next critical level to watch is 1,200 as a break below may lead to further selling pressure.

Speculation Continues On BOJ’s Next Move

General Trend:

- Asian equity markets trade generally higher

- Chinese equities rise amid government pledge to make fiscal policy more proactive; Shanghai Composite Property index rises over 5%

- Alphabet rises over 3.5% post earnings

- Mitsubishi Motors rises over 3%, may report Q1 earnings later today

- Weaker than expected earnings weigh on South Korean shipping-related companies

- Japan Manufacturing PMI hits 1.5 year low amid deterioration in export demand

- Offshore Yuan (CNH) weakens, PBoC set the yuan at the weakest since July 2017

- China 10-year bond yield rises for the 3rd straight session

- Australia Q2 CPI data due on Wednesday’s session

- US and European companies which may report results on Tuesday include 3M, AT&T, Biogen, Eli Lilly, Harley Davidson, Lockheed Martin, LVMH, Norsk Hydro, Peabody Energy, Peugeot, Randstad, Robert Half, Sherwin-Williams, Technicolor, Telecom Austria, UBS, UPM and Verizon.

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.7%

- TOPIX Real Estate index +1.5%, Iron & Steel +1.3%, Marine Transportation +1.3%, Securities +0.8%, Electric Appliances +0.6%

- (JP) Nikkei suggests politics could be a factor at the BoJ upcoming July policy decision. Suggests political considerations could pressure the central bank to take action at the July meeting, as a policy decision at the Sept meeting could influence the Liberal Democratic Party’s leadership elections.

- 8306.JP Mitsubishi UFJ Morgan Stanley Securities in a series of fake bond transactions that gained ¥1.58M in profits, now facing ¥218M in fines – Nikkei

- 8058.JP Regional Jet got no orders at Farnborough – Nikkei

- (JP) Japan ruling Liberal Democratic Party (LDP) lawmaker Shigeru Ishiba: sales tax above 10% may be needed - Nikkei

- (JP) JAPAN JUL PRELIM PMI MANUFACTURING: 51.6 V 53.0 PRIOR (1.5-yr low); New orders growing at weakest pace since Sept 2016

- (JP) Japan MoF sells ¥400B v ¥400B indicated in 0.80% (prior 0.90%) 40-yr bonds, yield at highest price 0.8800%; bid to cover 3.30x v 3.92x prior

- (JP) Those familiar with BOJ thinking expect BOJ to keep the same outline of its current policy at its next meeting despite complaints from banks - financial press

- (JP) Japan June BoJ Core CPI Y/Y: 0.4% v 0.5% prior

Korea

- Kospi opened +0.2%

- (KR) According to economists South Korea President Moon's expansionary fiscal policy will probably prove unsustainable in a couple of years due to a possible decline in tax revenue that might stem partly from reduced corporate profits - Korean press

- (KR) South Korea's Kospi has experienced the weakest H1 in 5-years, -5.7% - Korean press

- POSCO, 005490.KR Reports Q2 (KRW) Net 581.8B v 815Be; Op 1.25T v 1.35Te; Rev 16.1T v 15.9Te; Raises FY18 outlook

- 051910.KR To invest KRW2.8T to expand manufacturing facilities to raise the capacities of the Naphtha Cracking Center and high value metallocene polyolefin by 800Kt each at its Yeosu plant in South Jeolla Province

- (KR) North Korea appears to have begun dismantling part of Sohae station, a key rocket launch site – press

China/Hong Kong

- Hang Seng opened +0.1%, Shanghai Composite +0.1%

- Hang Seng Materials index +5.6%, Property/Construction +2.9%, Industrial Goods +2.5%, Financials +2.1%

- (CN) China State Council agreed that a more proactive fiscal policy will be pursued; will focus on introducing deeper tax and non-tax fee cuts, and more companies will be eligible for the preferential policies of the additional deduction of R&D spending in taxable income – Xinhua

- (CN) China foreign ministry spokesman Shuang: China has no desire to boost its exports through competitive devaluation, sound economic fundamentals are providing support to the currency

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 3rd consecutive session; Drains net CNY70B

- (CN) CHINA PBOC SETS YUAN REFERENCE RATE AT 6.7891 V 6.7593 PRIOR (weakest setting since July 11th, 2017)

- (CN) China H1 State Owned Enterprises (SOE) Profits CNY1.72T, +21.1% y/y; Rev CNY27.8T, +10.2% y/y

- (CN) China Ministry of Industry and Information Technology (MIIT): To appropriately help handle China/US trade dispute; to boost steady growth of industrial economy

Australia/New Zealand

- ASX 200 opened +0.2%

- ASX 200 Consumer Discretionary index +0.9%, Resources +0.8%, Financials +0.4%

- (AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 118.9 v 121.5 prior

- (AU) Australia Foreign Exchange Committee April Turnover report: Total avg daily OTC FX turnover A$122.6B

- IOF.AU Blackstone bid deemed 'not fair but reasonable' by independent expert KPMG - Australian

- Looking ahead: In tomorrow’s session will receive Aussie Q2 CPI and June Trade Balance

North America

- US equity markets ended mixed: Dow -0.1%, S&P500 +0.2%, Nasdaq +0.3%, Russell 2000 +0.1%

- S&P500 Financials +1.3%; Utilities -0.7%

- SPDR Gold Trust ETF daily holdings +0.6% at 802.55 metric tonnes

- Whirlpool, [-8%], WHR Reports Q2 $3.20 v $3.63e, Rev $5.14B v $5.22Be

Europe

- (UK) BOE's Broadbent: unwinding QE may create disinflationary pressures itself; QE unwinding won't start until rates are higher

- (UK) White Paper on Brexit plan would give ministers more power to block foreign takeovers of domestic firms on a national security basis - UK press

Levels as of 01:30ET

- Hang Seng +1.6%; Shanghai Composite +1.7%; Kospi +0.5%; Nikkei225 +0.5%; ASX 200 +0.6%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.3%; FTSE100 +0.2%

- EUR 1.1675-1.1702; JPY 111.06-111.52; AUD 0.7366-0.7389;NZD 0.6771-0.6797

- Aug Gold -0.5% at $1,219/oz; Sept Crude Oil -0.4% at $67.64/brl; Sept Copper +0.7% at $2.76/lb

France PMIs: Growth at a decent lick at the start Q3

France PMI manufacturing rose to 53.1 in July, up from 52.5 but missed expectation of 53.9. PMI services dropped to 55.3, down from 55.9, but beat expectation of 54.3. PMI composite dropped 0.4 to 54.5, hitting a two month low.

Commenting on the Flash PMI data, Alex Gill, Economist at IHS Markit said:

"The French private sector continued to grow at a decent lick at the start of the third quarter. The rate of expansion, however, remains far weaker than seen around the turn of the year.

"Diverging trends remained between the two main sectors, with activity growth at manufactures lagging behind service providers. A notable trend in this regard was a fall in goods exports for the first time in 22 months amid reports that global trade tensions is weighing on external demand.

"Nevertheless, the rate of job creation and degree of business confidence remained strong at both manufacturers and service providers, suggesting the French private sector is poised for further solid near-term growth."

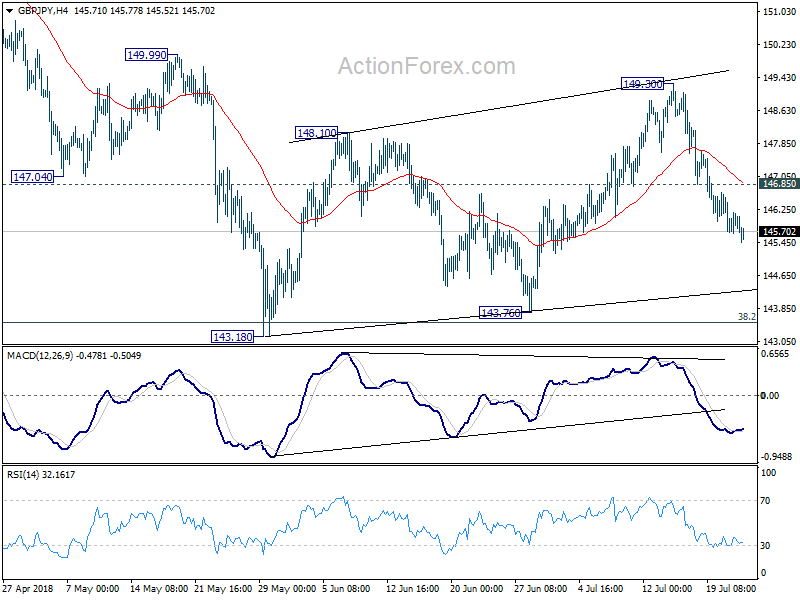

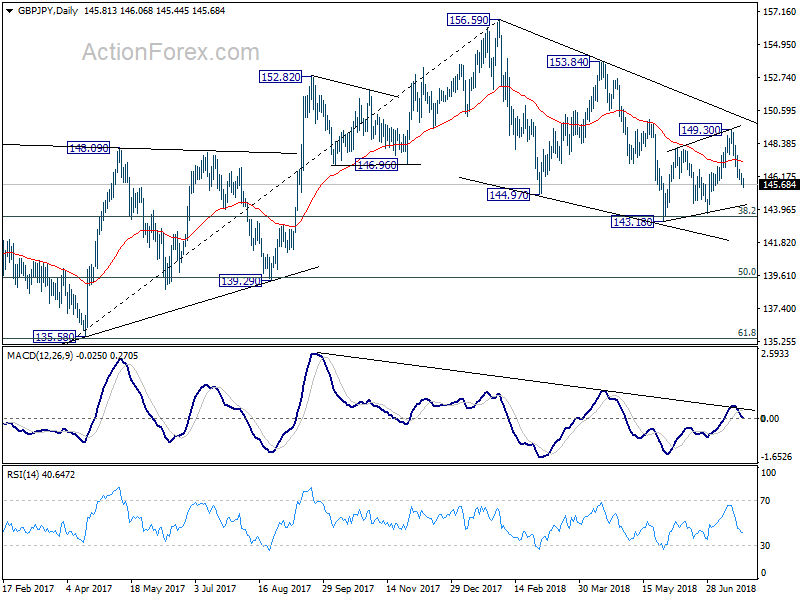

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.54; (P) 145.99; (R1) 146.30; More...

Intraday bias in GBP/JPY remains on the downside for the moment. Consolidation pattern from 143.18 has completed with three waves up to 149.30 already. Deeper fall should be seen back to 143.18/76 support zone. On the upside, above 147.65 minor resistance will turn bias back to the upside for 149.30/99 resistance zone instead.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

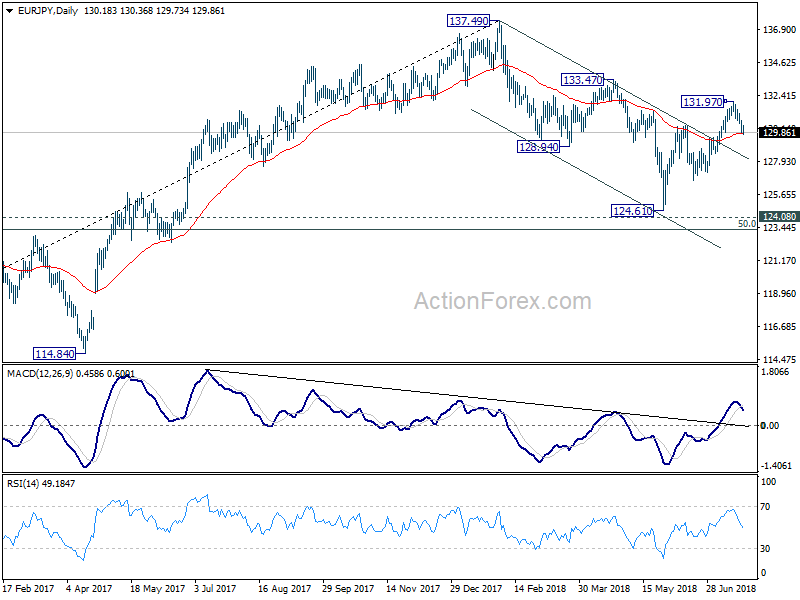

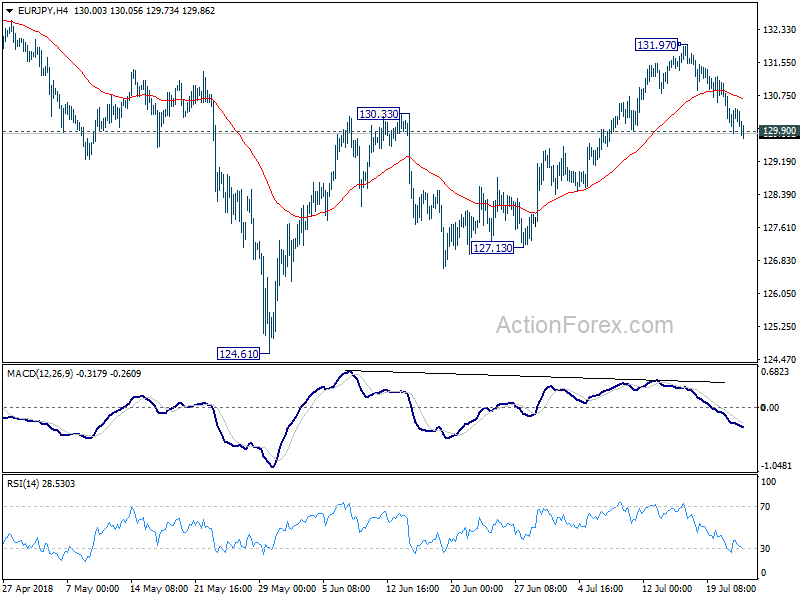

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.78; (P) 130.27; (R1) 130.67; More....

EUR/JPY's break of 129.90 argues that rise from 124.61 has completed at 131.97 already, on bearish divergence condition in 4 hour MACD. Intraday bias is back on the downside for 127.13 support first. Break there will confirm this bearish case and target 124.61 low. On the upside, break of 131.97 is now needed to indicate resumption of rise from 127.13. Otherwise, risk will stay mildly on the downside even in case of rebound.

In the bigger picture, the strong break of channel resistance from 137.49 suggests that the decline from there has completed. The three wave structure suggests that it's a correction. With 124.08 key resistance turned support intact, medium term bullishness is also retained. Break of 133.47 will affirm this bullish case and target 137.49 and above. This will now be the favored case as long as 127.13 support holds.