Sample Category Title

China unveiled fine-tuning policies measures to boost growth

China unveiled fine-tuning policies measures to boost growth yesterday. Firstly, there will be targeted tax reduction for research and development spending, that could lower around CNY 65B in taxes. Secondly, monetary policy have to ensure ample liquidity in the markets. Financial institutions will be guided to use the RRR cuts to support small and micro businesses. Thirdly, the funding of the National Financing Guarantee fund will be speeded up to achieve the goal of supporting 150,000 small and micro businesses with CNY 140B in loans per annum. Fourthly, "zombie businesses" will be cleared out resolutely to manage systematic risks.

BoE Broadbent unsure of his August Bank Rate vote yet

BoE Deputy Governor Ben Broadbent said yesterday that he hasn't decide on his vote on the Bank rate in the upcoming meeting on August 2 yet. Markets were pricing in 80% chance of an August hike two weeks ago. But the chance dropped to around 50% after last week's CPI miss. CPI had slowed notably from 3.0% in January to 2.4% in May, then stayed there in June. And, the impact of import inflation has faded much quicker than BoE has expected. Even if BoE does hike in August, it will be a one and done for the year.

Broadbent's comment came after a speech on "The history and future of QE". There he reiterated that the "framework" for unwinding QE was set out for some time in the November 2015 Inflation Report. That is, BoE would begin to start shrinking the balance sheet "only once the official Bank Rate had risen some way". And that's because "conventional policy is more flexible, better suited to responding to short-term economic fluctuations".

At the initial guidance, Broadbent noted that the meaning of "well underway" means Bank Rate at "around 2%". But in the June Monetary Policy Summary this year, the estimated threshold was lowered to "around 1.5%". He also noted that "we don't know exactly when that will be". But, "the framework is designed to ensure that, should inflationary pressures weaken after that date, the first response would be to cut interest rates." And,

"in principle, those disinflationary influences might include the process of QE unwind itself."

Market Morning Briefing: Gold Came Down Again To Test 1220

STOCKS

Overall the equity indices look bullish except Dow and Dax which could dip in the coming sessions before again starting to move up.

Dow (25044.29, -0.055%) and Dax (12548.57, -0.10%) have both dipped slightly and continue to head towards 24750 and 12400 respectively as mentioned yesterday. The dip is slow and gradual indicating that the current fall could be short lived. Dow and Dax could get some support near 24750 and 12400 levels. For now, near term looks bearish.

Nikkei (22534.03, +0.61%) has bounced back from support at 22400, on line with our expectations and could be headed higher towards 22800-23000 levels again while the rise sustains. Immediate view is bullish. This could also pull up Dollar Yen (111.23) to higher levels in the coming sessions.

Shanghai (2906.11, +1.63%) has risen finally above 2850, which could possibly mean that the immediate bottom has been made. Resistance is now visible at 2950 which if holds could produce a small rejection within an overall medium term uptrend.

Nifty (11084.75, +0.68%) closed higher yesterday and while above 10950, the index could continue to move up towards 11100-11200 in the coming sessions. Near term looks bullish.

COMMODITIES

Not much strength is visible in the commodities just now. Crude and Gold prices look bearish while Copper could remain ranged for a few sessions.

Nymex WTI (67.66,-0.34%) has dipped a bit and has room on the downside towards 66-65 levels while Brent (72.77, -0.36%) could also be pushed lower towards 71 to test immediate supports before resuming the rise in the longer run.

Gold (1223.20, -0.20%) came down again to test 1220. While below 1240, there is scope of testing 1200 in the next few sessions. Near term could be bearish to sideways in the 1200-1240 region.

Copper (2.7590, +0.46%) is unable to rise above 2.80 just now and could remain ranged in the 2.80-2.65 region for some more time.

FOREX

Euro (1.1685): Resistance near 1.175 held well for the Euro and it might now move down towards support near 1.16. It looks like the Euro could break out of its contracting range (since May) very soon. The ECB Meeting is on Thursday and could help in deciding the next course of movement for the Euro. In the recent past, Draghi has been persistently maintaining a dovish tone while talking about the QE's end or about the rate hike in 2019 - if that continues on 26th July, the Euro's break of range could be downward ie below 1.160-1.155.

Dollar Index (94.63): The support near 94 held well for Dollar Index yesterday. It is now trading near the 21 days MA near 94.6. A further rise towards 95.00-95.25 in the next 2-3 sessions could take place. Resistance @ 95.5 is the crucial level which needs to be watched. A decisive breach above that would correspond with a break below 1.155 for the Euro.

Dollar Yen (111.25): Support on daily candles has held perfectly for the Dollar Yen. This indicates that a last leg of upmove in the rally since March might be still left, which might end near 114-115. With some correction expected in Japanese yields as well, we could see Dollar Yen rise towards 112 in the next couple of sessions. Note that on weekly candles it might again have to face the resistance near 112.5. A breach of 112.5 would make us more confident of a rise to 114 in the weeks ahead.

Euro Yen (130.01): With the Euro expected to move towards 1.16 and Dollar Yen expected to rise towards 112, Euro Yen could stay within the 131.5-129.5 range in this week. There is support on daily candles near 129.5, which should hold unless the Euro breaks below 1.155.

Pound (1.3097): A slight upmove towards channel resistance near 1.32 in this week is still possible. However the broader trend remains bearish. If it closes below the 89 weeks MA (1.3114) this week, then a gradual downmove to 1.29 in the next week would be quite possible.

Dollar Rupee (68.86): Support at 68.65-60 holding. See a range of 68.60-69.00 this week, with growing chances of a run up to 69.30-60 after that. It could open higher near 68.90-95 since its trading higher on NDF.

INTEREST RATES

The Bank of Japan's indication that it might modify its interest rate target has led to a steep rise in Japanese yields with the 10 year yield (0.078) testing resistance on short term chart near 0.09%-0.10% yesterday. Till now, the Bank of Japan has been firm in keeping yields below the 0.10%-0.11% level. Till there is some further indication from the BoJ about its new target level, Japanese 10 Year yield could see some correction towards 0.07%-0.06% in the days ahead.

Since inflation in the Japanese economy is yet to reach the 2% target set by the BoJ, it is expected that there won't be much tightening ie the interest rate upper targets might not be too different from the current 0.10%-0.11% levels.

As mentioned yesterday, the rise in Japanese yields has led to a rise in US Yields as well - investors might have moved out of US bonds and towards Japanese bonds, leading to a rise in yield for US bonds.

US 10 year yield (2.956%), 30 Year (3.093%), 5 Year (2.8176%), 2 Year (2.6245%):

Both US 10 Year and 5 Year yields are close to short term resistance levels. US 10 year yield near 2.95%-3.00% has tended to attract investors, quickly driving down the yield again. If the 10 year yield falls quickly again or stays stable around 2.95%, it would be an indication that the 3% barrier is still strong and a gradual downmove towards 2.75%-2.70% could still be possible. However, a quick rise above 3% from here would imply that the 3% barrier has lost some of its strength and that, we may expect the 10 year to move beyond the previous high of 3.125% in the rest of 2018.

GBP/USD Recovery Above 1.3050 Looks Real

Key Highlights

- The British Pound recovered nicely from the 1.2958 low against the US Dollar.

- There is a major bearish trend line in place with resistance at 1.3190 on the 4-hours chart of GBP/USD.

- The US Existing Home Sales in June 2018 declined 0.6%, whereas the market was looking for a 0.5% rise.

- The US Manufacturing PMI for July 2018 (Prelim) will be released today, which is forecasted to remain at 55.4.

GBPUSD Technical Analysis

The British Pound was under pressure this past week below 1.3100 against the US Dollar. The GBP/USD pair declined below the 1.3000 support before buyers took a stand near 1.3160.

Looking at the 4-hours chart, the pair formed a low near 1.2958 and started a recovery. It bounced back above the 1.3050 resistance and the 38.2% Fib retracement level of the last decline from the 1.3292 high to 1.2958 low.

However, the pair is now facing a crucial resistance near the 1.3190-1.3200 zone. There is also a major bearish trend line in place with resistance at 1.3190 on the same chart.

The 100 simple moving average (red, 4-hours) is positioned near the trend line at 1.3185. Above the trend line, the next resistance is at 1.3213 and the 76.4% Fib retracement level of the last decline from the 1.3292 high to 1.2958 low.

Once the pair closes above the 1.3220 resistance and the 200 SMA (green, 4-hou), there could be more gains towards 1.3300. On the other hand, if the pair declines from the current levels, it may perhaps find support near 1.3050 and 1.3010.

Recently in the US, the Existing Home Sales report for June 2018 was released by the National Association of Realtors. The market was looking for a rise of 0.5% in sales compared with the previous month.

The actual result was disappointing as there was a decline of 0.6% in the US Existing Home Sales. Moreover, the last reading was revised from -0.4% to -0.7%. However, there was no major impact on the US Dollar and GBP/USD corrected a few points lower.

Economic Releases to Watch Today

- Germany’s Manufacturing PMI for July 2018 (Preliminary) – Forecast 55.5, versus 55.9 previous.

- Germany’s Services PMI for July 2018 (Preliminary) – Forecast 54.3, versus 54.5 previous.

- Euro Zone Manufacturing PMI July 2018 (Preliminary) – Forecast 54.7, versus 54.9 previous.

- Euro Zone Services PMI for July 2018 (Preliminary) – Forecast 55.0, versus 55.2 previous.

- US Manufacturing PMI for July 2018 (Preliminary) – Forecast 55.4, versus 55.4 previous.

- US Services PMI for July 2018 (Preliminary) – Forecast 56.5, versus 56.5 previous.

Japan PMI manufacturing dropped to 51.6, slowing of growth momentum

Japan PMI manufacturing dropped to 51.6 in July, hitting a 20-month low. That's also below expectation of 52.7.

Commenting on the Japanese Manufacturing PMI survey data, Joe Hayes, Economist at IHS Markit, which compiles the survey, said:

"Flash survey data pointed to a slowing of growth momentum for Japan's manufacturing sector at the beginning of the third quarter, following a robust performance so far this year.

"New business grew at a much weaker rate and was broadly flat, while export demand, despite further yen depreciation, deteriorated for a second month running.

"Slowing demand presents a worrying development given input delivery times lengthened to the sharpest extent in over seven years. Supply chain difficulties reportedly contributed to the fastest rate of input price inflation in since March 2011. Although output prices were raised at a relatively notable pace, the rate of increase was far weaker than that of costs, implying profit margin erosion."

Eco Data 7/24/18

[php_everywhere instance="1"]

US: Existing Home Sales Continue to Disappoint, Decline for the Third Straight Month in June

Existing home sales disappointed expectations again, falling 0.6% to 5.38 million in June from a slightly downwardly-revised 5.41 million in May. Economists had expected a slight uptick of 0.2% in June.

The pullback was again concentrated in the single-family segment, where sales fell by 0.6% on the month to 4.76 million, marking the third consecutive monthly decline. Meanwhile, sales of condos and co-ops were flat on the month at 620k.

Activity was mixed across the country. Sales continued to fall in the South (-2.2% m/m) and West (-2.6%), with both extending their losing streaks to four straight months. On the other hand, activity improved in the Midwest (+0.8%) and Northeast (+5.9%) – the latter coming on the back of a healthy gain in the prior month after subdued activity in the first quarter.

The number of homes available for sale rose 4.3% to 1.95 million in June, up slightly (+0.5%) from a year ago, but is still quite low relative to current demand levels. Homes listed for sale continued to be snapped up quickly, spending just 26 days on the market – the same as the last three months but down 2 days from a year ago. Given this dynamic, median home prices continued to rise at a brisk pace, with price growth accelerating to 5.2% y/y in June from 5.0% in the month prior.

Today's data for June brings the second quarter to a close, with activity falling 1.7% on a quarter-on-quarter basis, the fourth such decline in the past five quarters.

Key Implications

While the report did include a few bits of positive information, such as rebounding activity in the Northeast and improved inventory levels which are up for the first time year-over-year since mid-2015, altogether this is undoubtedly another disappointing housing report with existing home sales extending their losing streak to three straight months.

There are few signs of a turnaround in the near-term, with the June print providing a weak handoff to third quarter activity. Moreover, a weakening trend in pending home sales suggests that the soft prints are likely to continue.

Looking further ahead, the housing market will continue to face headwinds on both the supply and demand side. An improving economy, which is at or near full employment and is generating upward pressure on wages, should help households to continue to overcome the challenges of rising prices and higher interest rates. On the other hand, builders are facing bigger challenges, such as rising material costs (partly due to recent tariffs) and labor shortages, that are likely to continue to hold back supply and thus remain the determining factor over the evolution of the housing market over the medium term.

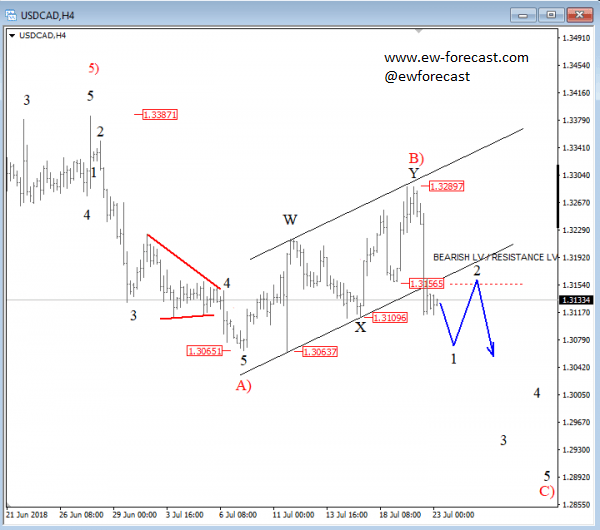

Bears Pushing USDCAD Lower

USDCAD turned beautifully lower from the upper channel line, which was expected as we were tracking a bigger, complex pattern within higher degree wave B). Current turn lower, and break below the 1.3157 level is now a confirmation for more weakness to follow in a five-wave manner for wave C). That said, we also now that pullbacks may follow, so the next one can be wave 2 which can look for resistance around the 1.316/1.320 area.

USDCAD, 4h

British Pound Quiet at Start of Week

The British pound is down slightly in the Monday session, after posting strong gains on Friday. In the North American session, the pair is trading at 1.3112, down 0.17% on the day. On the release front, it’s a quiet start to the week, with no British events. In the U.S, Existing Sales dropped to 5.38 million, missing the estimate of 5.46 million. On Tuesday, CBI Industrial Order Expectations is expected to drop to 8 points.

Is the British economy in trouble? Key British indicators hit some turbulence last week, although the pound escaped mostly unscathed, with modest losses. Employment data was weaker than expected on Tuesday, and this was followed by a soft CPI release a day later. On Thursday, retail sales declined 0.5%, surprising the markets which had expected a gain of 0.1%. This marked the first decline since March. The weak numbers have dampened expectations that the BoE will raise interest rates at its August meeting. With the May government continuing to squabble over Brexit and negotiations with the EU at a standstill, the pound could face further headwinds and drop under the symbolic 1.30 level.

The U.S. dollar was broadly lower on Friday after U.S President Trump made comments critical of Federal Reserve monetary policy. U.S presidents traditionally do not comment on moves by the Fed, but that did not prevent Trump from tweeting on Thursday that “tightening now hurts all that we have done”. On the weekend, Treasury Secretary Steven Mnuchin engaged in damage control, saying at the G-20 meeting that Trump was not interfering with the Fed policy of gradually raising rates. However, investors weren’t buying Mnuchin’s apologetics, and the U.S dollar continued to lose ground in Monday’s Asian session. There was more for investors to fret over, as Trump also attacked the EU and China for manipulating their currencies and keeping interest rates lower. This has raised concerns that the current global trade war could be followed by a currency war.

USD/JPY – Japanese Yen Dips Below 111, BoJ core CPI next

The Japanese yen has edged lower in the Monday session. In the North American session, USD/JPY is trading at 111.33, up 0.09% on the day. On the release front, U.S Existing Sales dropped to 5.38 million, missing the estimate of 5.46 million. This was the lowest level since January. Japanese Flash Manufacturing PMI is expected to tick up to 53.2 points.

The yen posted slight gains on Monday but was unable to consolidate. The brief gains were in response to a report that the Bank of Japan was considering changes to its monetary policy, in particular, its interest rate targets. This has raised speculation that the Bank could be making plans to reduce its massive stimulus program. Japan’s 10-year yield climbed to 5-month high on Monday in response to the report. If there are further signals from the BoJ that policymakers are considering reducing stimulus, the yen could move higher.

It was a strong week for the yen, as USD/JPY declined closed to one percent. The U.S. dollar was broadly lower on Friday after U.S President Trump made comments critical of Federal Reserve monetary policy. U.S presidents traditionally do not comment on moves by the Fed, but that did not prevent Trump from tweeting on Thursday that “tightening now hurts all that we have done”. On the weekend, Treasury Secretary Steven Mnuchin engaged in damage control, saying at the G-20 meeting that Trump was not interfering with the Fed policy of gradually raising rates. However, investors weren’t buying Mnuchin’s apologetics, and the U.S dollar continued to lose ground in Monday’s Asian session. There was more for investors to fret over, as Trump also attacked the EU and China for manipulating their currencies and keeping interest rates lower. This has raised concerns that the current global trade war could be followed by a currency war.