Sample Category Title

European Markets React To Trump Tweet

Donald Trump: Iran would suffer consequences never seen in history

The UK parliament will be going into a six-week recess

The overall sentiment for gold is negative

Spat between the US and China is at its peak level

US futures and European markets are trading lower as investors are reacting to late night tweet by Donald Trump, which stated that Iran should never ever threaten the US. Mr Trump even went one step further to say that Iran would suffer consequences never seen in history before.

Clearly, the tension has increased between the two countries, the US and Iran. The question is if the US can really afford to have a situation where it is not only losing its allies but also destroying its relations with other major countries. The spat between the US and China is at its peak level and there isn’t any solution in sight any time soon. Moreover, the US’s relations with the EU isn’t great at all.

If the economic engines of growth start to stall because of the trade war, there is little hope for peace. Yes, for now, the global growth is robust and even looking at the earning’s season, one could easily see that not only the companies over in Europe and US are beating the estimates, but the forward guidance is also encouraging. Donald Trump’s approach to trade negotiations is creating a major threat for the world economic growth and the world leaders have voiced their concern that putting the gun to their head isn’t going to work. Mr. Trump needs to be more reasonable with his approach.

Back in the UK, sterling traders had a hectic week and the focus remains on Brexit. The parliament will be going into a six-week recess on Tuesday and Theresa May’s hope is for the threats to her leadership to fade during this recess period. However, sterling traders might not have time to enjoy the recess period as the Bank of England will have to make a decision about their interest rate hike.

As for gold, the overall sentiment is negative. This is despite the fact that we have seen more tension between the US and Iran. Both countries have made some hot comments towards each other. However, the net impact isn’t that big at all. The dollar weakness has brought some life to gold but nothing major there either. In terms of levels, we are looking at the $1215 mark for now and a break of this would open the floor towards the next support level of $1200.

China said it won’t devaluate Yuan to stimulate exports, but how about intervention to halt Yuan’s fall?

China Foreign Ministry spokesman Geng Shuang said in a regular press briefing today that "China does not intend to stimulate exports through the currency competitive devaluation" and added that's China's consistent position. He went further to emphasize that the "RMB exchange rate is mainly determined by the market supply and demand." And for now, "China's economic fundamentals continue to improve, providing strong support for the RMB exchange rate to remain basically stable."

However, Geng didn't directly say China has not intervene in the markets. It's suspected that a state own-bank has stepped in last Friday selling US Dollar to halt the decline of the yuan when USD/CNY (on shore yuan) breached the government's red line of 6.8. US Treasury Steven Mnuchin said last Friday that the US will monitor if China has manipulate the Yuan exchange rate. Mnuchin has to deliver his promise and come out to warn China for not intervening in the markets again, and just let Yuan falls against Dollar, if he didn't lie.

EUR/USD – Euro Pauses After Strong Gains Following Trump Comments

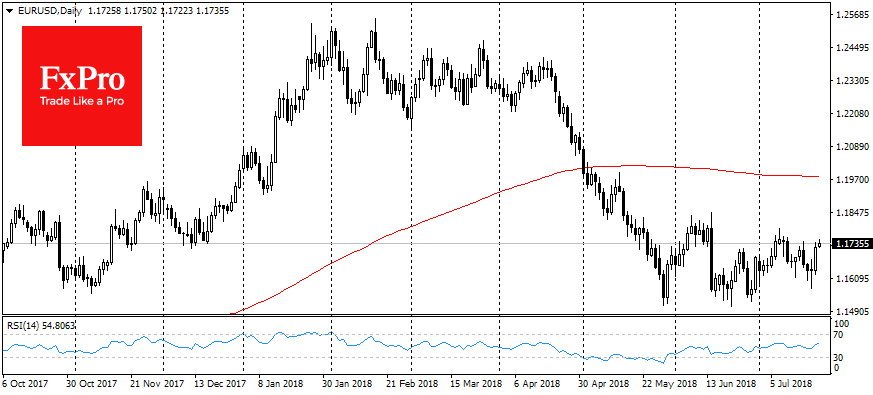

EUR/USD has posted slight losses in the Monday session after strong gains on Friday. Currently, the pair is trading at 1.1731, up 0.07% on the day. On the release front, it’s a quiet start to the week. Eurozone Consumer Confidence, which hasn’t posted gains since January, is expected to dip to -1 point. In the U.S, Existing Home Sales is forecast to climb to 5.46 million. On Tuesday, Germany and the eurozone will release service and manufacturing PMIs.

The dollar was broadly lower on Friday, after U.S President Trump made comments critical of Federal Reserve monetary policy. U.S presidents traditionally do not comment on moves by the Fed, but that did not prevent Trump from tweeting on Thursday that “tightening now hurts all that we have done”. On the weekend, Treasury Secretary Steven Mnuchin engaged in damage control, saying at the G-20 meeting that Trump was not interfering with the Fed policy of gradually raising rates. However, investors weren’t buying Mnuchin’s apologetics, and the U.S dollar continued to lose ground in Monday’s Asian session. There was more for investors to fret over, as Trump also attacked the EU and China for manipulating their currencies and keeping interest rates lower. This has raised concerns that the current global trade war could be followed by a currency war.

The euro posted marginal gains last week and continues to stay close to the 1.17 line. Traders should be prepared for some stronger movement in the Tuesday session, with the release of service and manufacturing PMIs for Germany and the eurozone. Both manufacturing PMIs have shown a troubling downward trend for the past six months – will this continue in June? Although the PMIs continue to show expansion in Germany and the eurozone, investors remain nervous that the escalating trade war is having a negative impact on the manufacturing sector. If the readings continue to head lower on Tuesday, the euro could lose ground.

EU Schinas: There are no offers when Juncker visits US

European Commission spokesman Margaritis Schinas said in a news conference today that President Jean-Claude Juncker will not bring a trade offer to the US when he visits Washington on July 25. Schinas said "I do not wish to enter into a discussion about mandates, offers because there are no offers. This is a discussion, it is a dialogue and it is an opportunity to talk and to stay engaged in dialogue."

This is an echo of the comments by EU Trade Commissioner Cecilia Malmstrom last week. She said that the visit was to "try to establish a good relations, try to see how we can de-escalate the situation, avoiding it going further and see if there is a forum where we can discuss these issues." She added that "we don't go there to negotiate anything."

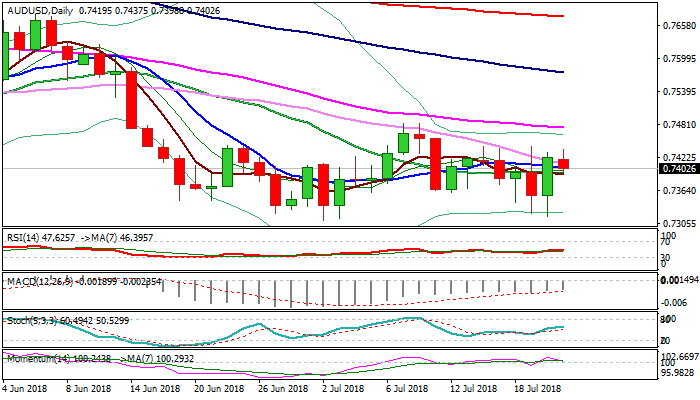

AUDUSD Outlook: Risk Of Break Below 20SMA Pivot After Another Rejection At 0.7440 Barrier

The Australian dollar stands at the back foot on Monday and eases below 0.74 handle, following another rejection at strong 0.7440 resistance zone (triple failure was registered last week), as attempts to extend Friday’s strong rally lacked strength to eventually break higher. the pair is losing momentum and probes back below a cluster of MA’s (10,20,30) between 0.7411 and 0.7394, with break lower (20SMA marks pivotal support at 0.7394) to generate bearish signal for deeper fall towards key supports at 0.7317/10 (20/2 July base). Bullish scenario requires firm break above 0.7440 platform to expose key barriers at 0.7476 (55SMA) and 0.7483 (09/10 July double-top).

Res: 0.7411, 0.7442, 0.7476, 0.7483

Sup: 0.7394, 0.7360, 0.7317, 0.7310

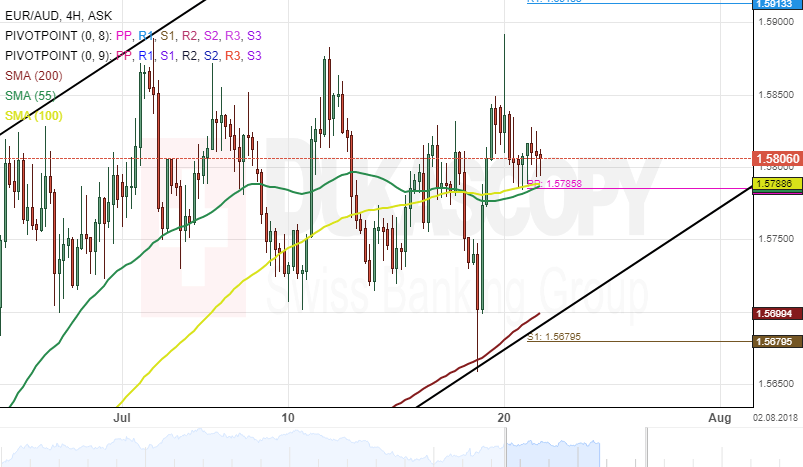

EUR/AUD 4H Chart: Finds Support Cluster

The common European currency has been gradually appreciating against the Australian Dollar since it bounced off the lower boundary of a junior channel at 1.5306 early June.

The currency pair tested the 200-hour simple moving average on July 19 and reversed to the upside. A cluster formed by the combination of the 55– and 100-hour SMAs and the weekly pivot point at 1.5785 was providing support for the rate at the time of this analysis.

Everything being equal, it is likely that the EUR/AUD currency exchange rate continue moving in the ascending channel during the following trading sessions.

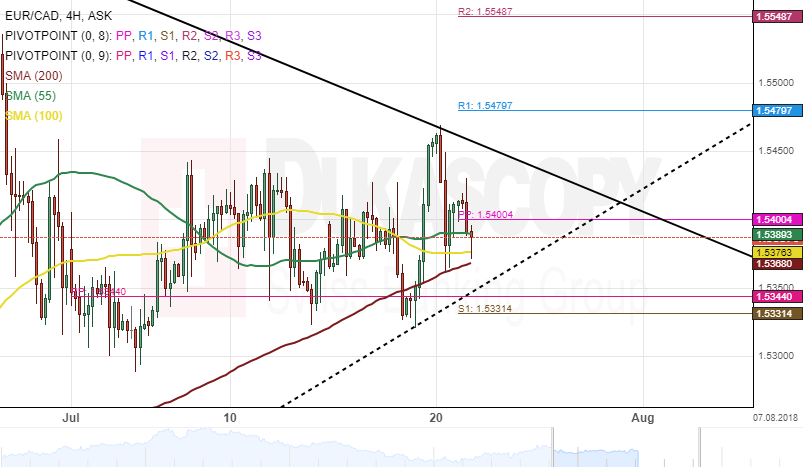

EUR/CAD 4H Chart: Bullish Signals Today

The movement of the EUR/CAD currency pair has been guided by a junior ascending channel. The pair tested the upper boundary of the channel on June 22 and has since made a temporary retracement down.

The exchange rate has been trading along the 55-, 100-, and 200– hour simple moving averages since the beginning of this month as both bulls and bears traders are unable to move the rate to either direction.

Technical indicators suggest that bullish momentum is likely to come into play during the following trading sessions. If and when this scenario occurs, the currency exchange rate could breakout from a triangle pattern today.

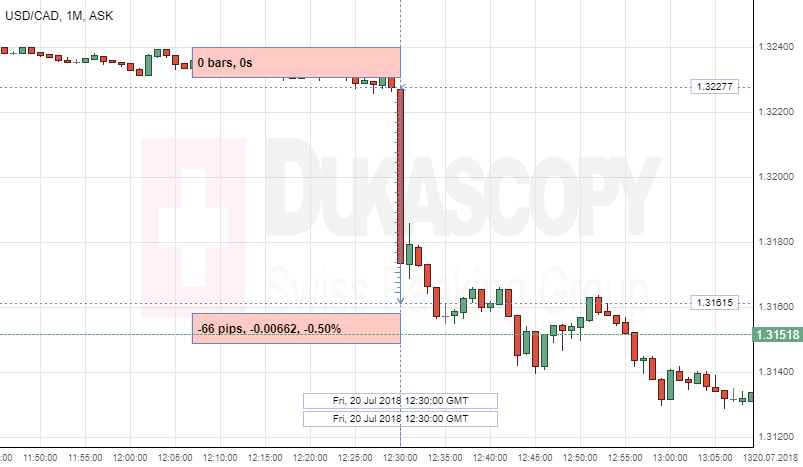

USD/CAD: Canadian CPI

The Canadian dollar srtengthened against the Greenback, following the Canadian CPI data release. The USD/CAD currency pair lost 66 pips, or 0.50%, to continue fluctuating in the 1.3159 area.

The Statistics Canada released Consumer Price Index data that came in line with expectation of 0.1%, but lower from the previous period 0.1%.

The data was published together with Canadian Retail Sales, which came out better-than-expected of 1.4% compare to 0.4% forecasted, which boost the pair downward. A senior economist at CIBC World Markets Royce Mendes have said: "The biggest surprise was the ex-autos reading in retail sales," and added "It blew past expectations. This was a lot of people coming back to stores after weather affected April's numbers."

Markets Get Busy Week Off To Weaker Start

- Trump $500 billion Chinese tariffs threat weighs on sentiment;

- Earnings eyed but trade could once again be key;

- May suffers further setbacks to white paper proposal.

Equity markets are trading slightly in the red at the start of the week, a reflection of the slightly risk averse tone stemming from the prospect of the trade conflict escalating in the coming months.

US President Donald Trump has continued to double down on threats against China, warning he is willing to impose tariffs on all goods imports which equates to around $500 billion. While this isn’t the first time he’s suggested this, it does seem he is becoming increasingly frustrated with the process and that he is not getting the results he expected when he first started down this path.

Unless the two countries find a solution in the next couple of months, the next $200 billion of 10% tariffs that were revealed recently will likely be imposed which could be met with similar measures on the US, if previous actions and rhetoric are anything to go by. While the market rally has stalled this year, with trade being a major contributor, they have shown a certain resilience, something that may not last once tariffs start to take their toll on the economy, with price increases for consumers sure to have an impact.

This week is likely to see focus remain on trade, with Trump not one to take a back seat and remove himself from the spotlight. Earnings season could provide a welcome distraction from the political theatre of trade wars but even here it’s going to feature as tariffs will have an impact on the outlooks of a number of companies and investors will be keen to hear their views. Around a third of S&P 500 companies report on the second quarter, including three of the four FANG stocks which will typically attract plenty of attention.

There are also a number of other events to focus on this week including the ECB meeting on Thursday – although this may be more of a low key affair with the central bank having already laid out plans for the next year. Theresa May will also meet with her cabinet on Monday for their final meeting before the summer recess, in which the Brexit white paper may be discussed, given the widespread opposition to it and apparent rejection of aspects of it by the European Union chief negotiator Michel Barnier. Needless to say, with only months to go until exit day, negotiations are not progressing as hoped.

Trump Tosses Dollar From Highs, Now Move Is Up To ECB

The dollar remained under pressure after the Trump's criticism about the strengthening of the national currency. Despite doubts that the influence of the president's comments will be long, tactically they came out at an opportune moment, not allowing the growing index of the dollar to gain momentum after touching highs for the last year. At least for the short-term the scales turned to dollar bears, and sent DXY (Dollar Index) from the recent highs.

In addition to the direct reaction of the currency market, it is worth noting the flattened yield curve for of U.S. treasuries. This is good news for the markets, mostly for the EM, that slightly decreases the degree of uncertainty around the trade wars. Besides, a company's strong reporting helped the markets last week. Now this factor is temporarily suppressed by uncertainty about the prospects of trade wars, but in general is a significant positive theme.

Despite the weakening of the dollar in the second half of last week, the upcoming ECB press conference this week has a chance to exacerbate the competition of bulls and bears on the currency markets.

After ECB head's comments on previous meeting the Euro collapsed by 2.5% and returned the EURUSD in the area of 12-month lows. However, it is more likely that there will develop the balanced-comments-scenario of Draghi in the range from neutral to positive for the currency after a portion of criticism from the American president about the active pressure on their currencies in Europe and China.

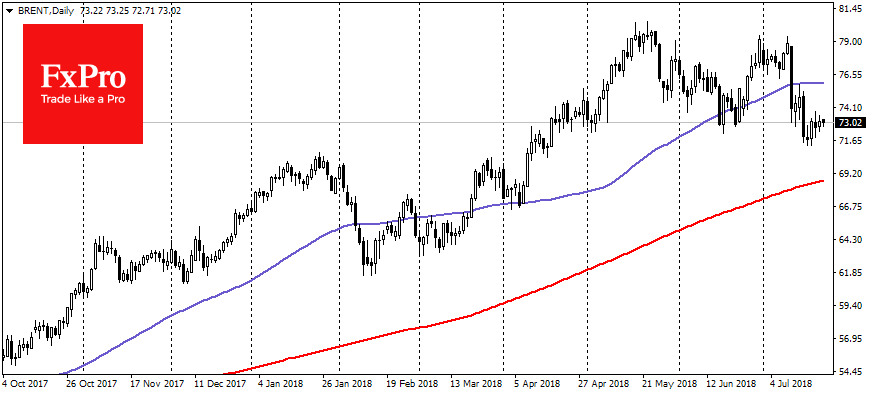

The weakening of the dollar also helped gold, oil, and Chinese exchanges to grope some support last week. On Friday, the oil also gained some help from the reports about a reduction in drilling activity.

As a result, Brent trades near $73 a barrel against last week's lows at $71.30.