Sample Category Title

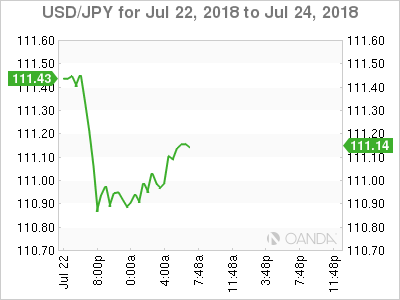

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.02; (P) 111.83; (R1) 112.26; More...

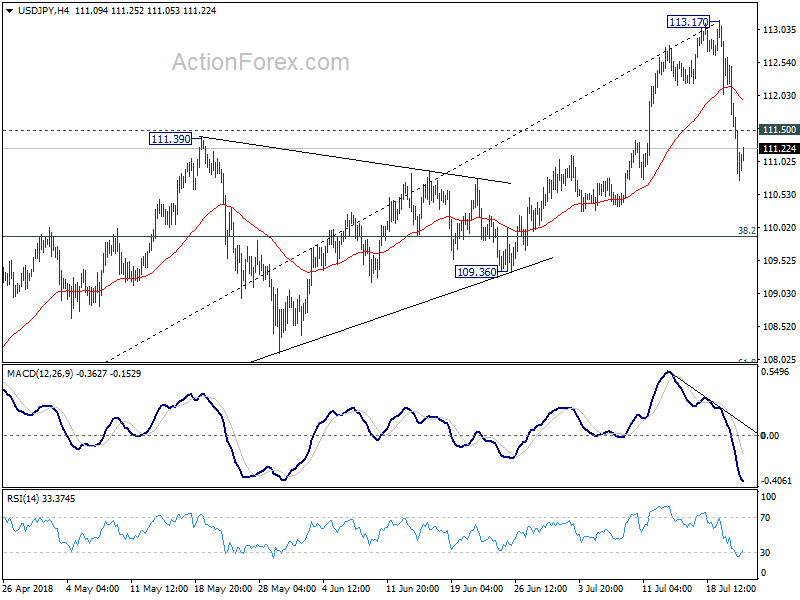

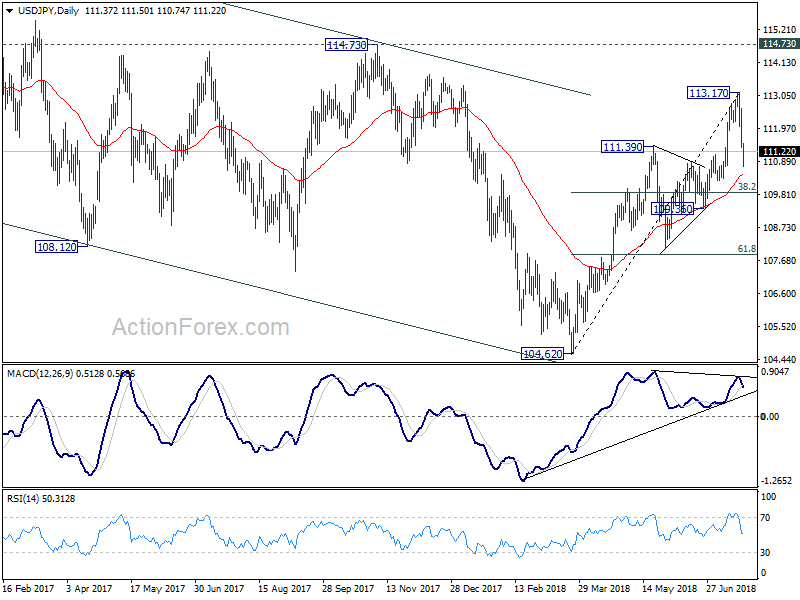

USD/JPY recovers mildly after hitting as long as 110.74. It then recovers mildly on oversold condition in 4 hour RSI. But as upside is limited below 111.50 minor resistance. intraday bias remains on the downside for 55 day EMA (now at 110.45) and below. However, as fall from 113.17 is seen as a correction to rise from 104.62, downside, should be contained by 38.2% retracement of 104.62 to 113.17 at 109.90 to bring rebound. On the upside, above 111.50 minor resistance will turn intraday bias neutral first. But break of 113.17 is needed to confirm up trend resumption. Otherwise, more consolidation would be seen with risk of another fall.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds.

Yen Pares Gain While Dollar Attempts Rebound

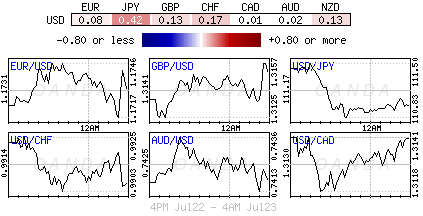

Yen is paring some gain in early US session but remains the strongest one for today, followed by Swiss Franc. Meanwhile, Australian Dollar overtakes Dollar as the weakest one. Euro follows as the second weakest as pressured in crosses. Dollar is trying to recover against other but there is no sustainable buying seen yet. The economic calendar is rather light in the US session. Hence, there shouldn't be much inspiration from data. Main focus will be on BoE MPC member Ben Broadbent's comments and markets will be keen to know his view on an August hike. Meanwhile, attention will also be on whether Yen could extend the sharp gains in the past two days.

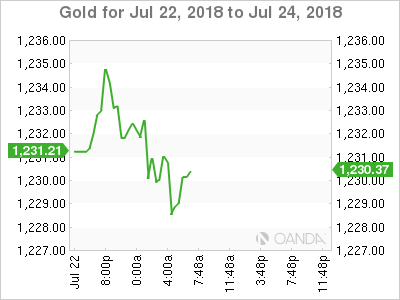

In other markets, European indices are trading generally lower at the time of writing but loss is limited. FTSE is down -0.16%, DAX down -0.20%. CAC is the biggest sufferer and is down -0.51%. Nikkei closed down sharply by -1.33% earlier today but could be trading to draw support from 55 day EMA. Meanwhile, as Chinese Yuan stabilized after suspected intervention, Chinese stock extended recent rebound. Gold edged higher to 1235 earlier today but struggles to find follow through buying above 1230. WTI crude oil is trading above 69 for the momentum but hasn't made up its mind to get through 70 handle.

EU Schinas: There are no offers when Juncker visits US

European Commission spokesman Margaritis Schinas said in a news conference today that President Jean-Claude Juncker will not bring a trade offer to the US when he visits Washington on July 25. Schinas said "I do not wish to enter into a discussion about mandates, offers because there are no offers. This is a discussion, it is a dialogue and it is an opportunity to talk and to stay engaged in dialogue."

This is an echo of the comments by EU Trade Commissioner Cecilia Malmstrom last week. She said that the visit was to "try to establish a good relations, try to see how we can de-escalate the situation, avoiding it going further and see if there is a forum where we can discuss these issues." She added that "we don't go there to negotiate anything."

Bundesbank: German economy regaining some lost momentum

Bundesbank said in the latest monthly report released today that the German economy is regaining some momentum currently. It noted that "the economy has likely showed better momentum in the spring than at the start of the year." Nonetheless " it is unlikely that the high growth rates of the past year will be repeated, manufacturing was once again the key economic driving force."

The report noted that car production increased sharply with pharmaceutical products. But intermediates goods remained weak. Household consumption remained a cornerstone for growth. Government consumption also rebounded. Also, "activity in the booming construction sector likely increased significantly, despite capacity constraints."

China said it won't devaluate Yuan to stimulate exports

China Foreign Ministry spokesman Geng Shuang said in a regular press briefing today that "China does not intend to stimulate exports through the currency competitive devaluation" and added that's China's consistent position. He went further to emphasize that the "RMB exchange rate is mainly determined by the market supply and demand." And for now, "China's economic fundamentals continue to improve, providing strong support for the RMB exchange rate to remain basically stable."

Yen lifted as 10 year JGB yield jumped on BoJ talks

10 year yield in Japan jumped as much as six basis points to 0.090%, hitting the highest level since February. It's also the largest daily rally in nearly two years. The sharp movement prompted an unscheduled operation by BoJ to buy 10 year JGB at a yield of 0.11%. That's the same level as at last intervention but no bid was tendered.

The movements were based on reports that BoJ is discussing changes to its monetary policy, including the interest-rate targets and stocks-buying techniques. The objective is to make the stimulus program more sustainable. Currently, under the Yield Curve Control framework, BoJ is buying JGBs to keep 10 year yield at around 0%. And the central bank could allow 10 year yield to rise higher to 0.10% to give more flexibility to monetary policy.

G20 pledged to strengthen contribution of trade to the economies

G20 finance ministers and central bankers stepped up their language regarding trade tension in the communique after the meeting in Argentina. The communique noted that "risks over the short and medium term have increased". And the risks include "financial vulnerabilities, heightened trade and geopolitical tensions, global imbalances, inequality and structurally weak growth, particularly in some advanced economies." The group pledged to "continue to monitor risks, take action to mitigate them and respond if they materialise."

The communique also noted that "international trade and investment are important engines of growth, productivity, innovation, job creation and development." The group reaffirmed the conclusions on trade at the Hamburg Summit and "recognise the need to step up dialogue and actions to mitigate risks and enhance confidence". And "we are working to strengthen the contribution of trade to our economies."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.02; (P) 111.83; (R1) 112.26; More...

USD/JPY recovers mildly after hitting as long as 110.74. It then recovers mildly on oversold condition in 4 hour RSI. But as upside is limited below 111.50 minor resistance. intraday bias remains on the downside for 55 day EMA (now at 110.45) and below. However, as fall from 113.17 is seen as a correction to rise from 104.62, downside, should be contained by 38.2% retracement of 104.62 to 113.17 at 109.90 to bring rebound. On the upside, above 111.50 minor resistance will turn intraday bias neutral first. But break of 113.17 is needed to confirm up trend resumption. Otherwise, more consolidation would be seen with risk of another fall.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | CAD | Wholesale Trade Sales M/M May | 1.20% | 0.60% | 0.10% | |

| 12:30 | USD | Chicago Fed Nat Activity Index Jun | 0.43 | -0.15 | -0.45 | |

| 14:00 | EUR | Eurozone Consumer Confidence Jul A | -0.75 | -0.5 | ||

| 14:00 | USD | Existing Home Sales Jun | 5.47M | 5.43M | ||

| 14:00 | USD | Existing Home Sales M/M Jun | -0.20% | -0.40% |

Euro Trades Flat ahead of Eurozone Consumer Confidence Index

Here are the latest developments in global markets:

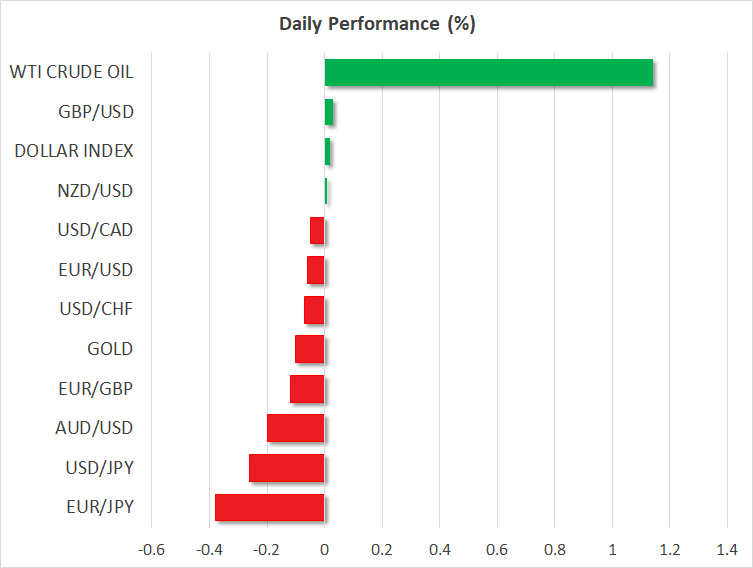

FOREX: The US dollar edged sharply lower over the last three straight days against the Japanese yen as the movements were based on reports the Bank of Japan (BOJ) is discussing changes to its monetary policy, including changes in interest rates and stock buying techniques. The 10-year yield in Japan climbed as much as six basis points to 0.090%, hitting the highest level since February. Dollar/yen continued the bearish move today as well, losing 0.25%. However, the US dollar index advanced by 0.04%, erasing some previous losses. Pound/yen retreated to a 3-week low (-0.24%), while pound/dollar moved up by 0.04%. In Brexit-related news, the new British foreign minister, Jeremy Hunt, said on Monday that there was a real risk of a no-Brexit deal if the EU waited too long for Britain to “blink” Also, euro/yen dipped by 0.36% and euro/dollar fell by 0.08%. In the antipodean sphere, aussie/dollar slipped by 0.19% near 0.7400, while kiwi/dollar stood near its opening level at 0.6806. Meanwhile, dollar/loonie fell marginally by 0.07% after another strong sell-off day on Friday.

STOCKS: European stocks were in the red on Monday. The benchmark European STOXX 600 dived by 0.20% at 1100 GMT as travel companies were the biggest losers after Ryanair posted a 20% decline in first-quarter profit. The blue-chip Euro STOXX 50 was down by 0.33%, while the German DAX 30 fell by 0.30% after two consecutive negative days. The French CAC 40 and the British FTSE 100 were down by 0.55% and 0.37% respectively, while the Spanish IBEX 35 moved lower by 0.28%. In Asia, Japan’s Nikkei 225 closed down by 1.33% after reports said that BOJ is looking to pull back on stimulus. In the US, even though the S&P, Dow Jones, and the Nasdaq all fell slightly on Friday, futures tracking these indices are currently in the red again, pointing to a lower open today.

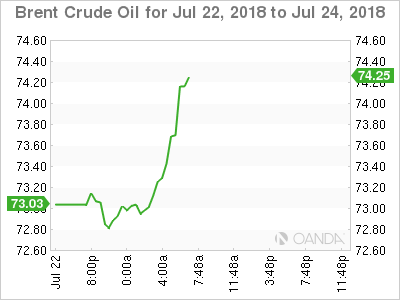

COMMODITIES: Oil prices surged in the early European session, taking advantage of the weaker greenback amid worries over stronger demand prospects in some of the world’s biggest economies. On Saturday, the Iranian Supreme leader Ayatollah Ali Khamenei echoed President’s Hassan Rouhanis suggestion to block Gulf oil exports if Iran’s exports were restricted, while he characterized talks with the US an “obvious mistake”. WTI and Brent crude were rising, trading not far below $69 and $74 a barrel and adding 1.17% and 1.68% respectively. Gold was down, though not by much (-0.08%), trading around $1230.4 per ounce.

Day ahead: Eurozone flash Consumer Confidence Index in the spotlight; trade developments eyed

On Monday, July’s flash figures on consumer confidence due at 1400 GMT will attract the most attention in the Eurozone as investors are eagerly looking for signs showing that the bloc’s economic slowdown in the first quarter was a temporary blip. The European Commission, however, is expected to say that the measure remained in negative territory for the second month running, with analysts predicting the index to deteriorate to -0.7 from -0.5 in June, a bearish growth evidence that could keep growth prospects for the second quarter pessimistic ahead of the preliminary PMI readings on Tuesday and the ECB monetary policy meeting on Thursday. While the central bank has already announced its decision to terminate its asset purchasing program at the end of this year, a miss in data this week could turn policymakers cautious on future rate hikes as the central bank is planning to shift focus back to rate adjustments after ending its QE program, with markets projecting the first rate rise to come not until the end of 2019. Should today’s data indicate that consumers have lower-than-expected prospects on their future spending, euro/dollar could start erasing Friday’s gains. On the other hand, a surprising improvement in the numbers could help the pair to continue its recovery.

At the same time (1400 GMT) in the US, the calendar is scheduled to deliver stats on existing home sales for the month of June. After contracting by 0.4% month-on-month (m/m) in May and plunging by 2.7% in April, forecasts are now for a growth of 0.5%. The number of existing residential buildings sold in the previous month is anticipated to inch up from 5.43 million to 5.44mn. Still, new potential developments on the trade front could offset any data impact today as the G20 meeting between finance ministers and central bank delegates during the weekend did little to ease tensions. Instead, the US backed its import tariffs and urged its allies to ease their barriers on US products, a few days after the US president said he was ready to impose tariffs on all goods imported from China. European finance ministers were also on the defensive, claiming that no trade deal is possible with the US unless the US removes its duties. On Wednesday, all eyes will turn to Washington, where Trump and the President of the European Commission, Jean-Claude Junker will meet to discuss on security and economic matters such as tariffs on metals and imported cars, with markets being interested to see whether Junker could achieve some progress in the countries’ relations.

Meanwhile in neighboring Canada, May’s wholesale trade figures will gather some attention at 1230 GMT.

On the monetary front, the Bank of Japan will be in the spotlight after reports stated that the central bank is holding preliminary talks regarding changes in interest rates and stock-buying that could remove a layer of stimulus. The headline pushed Japanese bond yields up to levels not seen since February and the yen to 3-week highs, persuading the BoJ to engage in a special bond-buying operation. Moreover, the news came a week before the central bank decides on interest rates, raising speculation that policymakers could signal the start of a stimulus reduction phase. Still, investors worry that a subdued inflation could refrain policymakers from announcing any policy adjustments. Early during the Asian session at 0030 GMT, traders will see the release of Japanese preliminary manufacturing PMIs for the month of July, though the impact on the yen could be minimal as the safe-haven currency tends to react little on data.

US relations with Iran would be also in focus after the Iranian and the US presidents unleashed war of words yesterday with the former warning that “peace with Iran is the mother of all peace, and war with Iran is the mother of all wars” while the latter responded with harsh tone, advising Iran to “never threaten the US”. Recall that Trump recently withdrew the US from the 2015 Iranian nuclear deal, while the US government is set to reimpose sanctions on Tehran.

As for today’s, public appearances, Bank of England’s Deputy Governor Ben Broadbent will give a speech to the Society of Professional Economists in London at 1700 GMT.

In stock markets, earnings releases continue, with Google’s parent Alphabet being among companies to report quarterly reports after the market close. The company is expected to report higher earnings per share year-on-year.

Quiet Start To Trading Week

Notes/Observations

- Trade war seen spouting the seeds of a potential currency war; China deflected recent criticism from Trump

- Japanese yen currency forms, JGB yields higher on policy stimulus unwind bets

- ECB meeting on Thursday, no policy stance expected but markets looking for clarification on the 1st potential rate hike

- USD maintained a soft tome after President Trump criticized the Fed for raising interest rates and suggested the USD was too strong.

- Corporate earnings season ramping up this week

Asia:

- BOJ held a Fixed-rate operation on the 5-10-year JGB bonds (1st time since Feb ); Received no takers in buying (Note: BoJ announcement related to daily bond buying operation was unchanged)

- On Friday reports circulated that the BOJ might consider changes to interest rate targets. Measure to create policy sustainability, and not as 'tightening' (Note: analysts noted on possible ways BOJ could adjust policy: shortening duration for JGB purchases, making interest rate operations more flexible, expanding dollar operations to maximize yen strengthening risk)

- China PBoC conducted CNY502B in 1-year medium-term Lending Facility (MLF) for the 2nd time in July (prior size was CNY188.5B prior; Interest Rate at 3.30% (unchanged from prior)

- BoJ officials said to be looking for ways to keep stimulus program sustainable while reducing the harm it causes to markets and bank profits. Officials were focused on making adjustments to mitigate harm w/out doing anything that resembles a move to normalize policy (Note: Analysts saw little chance of significant changes to YCC or asset purchases at July 31st meeting)

Europe:

- EU Chief Brexit Negotiator Barnier said to have European Affairs Min on Friday, July 20th the UK plan for financial services would violate the principle that access rights to the bloc’s financial services market are a gift from Brussels that can be freely withdrawn

- Brexit Sec Raab said to stated that Britain would refuse to pay its £39B Brexit deal if the EU fails to agree on trade deal

- Italy’s Former Fin Min Padoan: New govt’s goal was the dismantling of policies that helped put the country on a path to recovery during his term

- S&P revised Greece sovereign outlook to Positive from Stable; affirms B+ rating

- S&P affirmed Russia sovereign rating at BBB-; outlook stable

- Fitch affirmed France sovereign rating at AA; outlook stable

- Fitch affirmed Canada sovereign rating at AAA; outlook stable

- Fitch raised Austria sovereign outlook to Positive from Stable; affirms AA+ sovereign rating

Americas

- G20 Finance Ministers Communique: Short and medium term risks to growth have increased including heightened trade the geopolitical tensions. Needed to step up dialogue and actions to mitigate risks

- US Treasury Sec Mnuchin: Hoped to get a NAFTA agreement negotiated in near future; Saw light at the end of the tunnel on trade disputes. Did not have substantive discussions with Chinese officials on trade at G20 but added any time China wanted to negotiate meaningful changes to its trade practices, he was available. Said to have noted that he would not minimize the possibility that the US will impose tariffs on all $500B worth of goods that the US imports from China

- US President Trump via tweet to Iran President Rouhani: “Never, never threaten the United States again or you will suffer consequences the likes of which few throughout history have ever suffered before; we are no longer a country that will stand for your demented words of violence and death, be cautious!” – tweet (Note: Tweet followed comments from Iran President Rouhani who warned Trump not to 'play with the lion's tail', as it would only lead to regret. US should know peace with Iran was mother of all peace, and war with Iran was mother of all wars

Economic Data:

- (DK) Denmark July Consumer Confidence: 9.7 v 10.6 prior

- (CH) Swiss Jun M3 Money Supply Y/Y: 2.4% v 2.8% prior

- (TR) Turkey July Consumer Confidence: 71.3 v 70.3 prior

- (CH) SNB Total Sight Deposits for Week Ended July 20th (CHF): 576.4B v 576.1B prior

- (TW) Taiwan Jun Industrial Production Y/Y: 0.4% v 5.0%e

- (TW) Taiwan Jun Unemployment Rate: 3.7% v 3.7%e

- (GR) Greece May Current Account: +€0.2B v -€1.3B prior

- (HK) Hong Kong Jun CPI Composite Y/Y: 2.4% v 2.2%e

- (IS) Iceland July CPI M/M: 0.0% v 0.6% prior; Y/Y: 2.7% v 2.6% prior

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.1% at 385.1, FTSE -0.4% at 7651, DAX -0.1% at 12549, CAC-40 -0.3% at 5382, IBEX-35 +0.2% at 9743, FTSE MIB -0.1% at 21,775, SMI -0.5% at 8947, S&P 500 Futures -0.1%]

- Market Focal Points/Key Themes: European Indices trade mostly lower across the board but off the earlier lows, following a mixed session in Asia and slightly lower futures in the US. The Italian FTSE MIB is in focus following weakness in shares of Fiat after the stepping down of its long standing CEO Marchionne due to health complications. Shares of Ferrari and and Exor also fall following the news. Elsewhere Ryanair, Philips and Julius Baer are among notable names trading lower after earnings. Atos trades over 5% lower after its weaker H1 results offset the positive read from its acquisition of Syntel for $3.6B. Looking ahead notable earners include Haliburton, Illinois Toolworks and Lennox International.

Movers

- Consumer Discretionary Ryanair [RYA.UK] -4% (Earnings), McColls [MCLS.UK] -12% (Earnings, CFO to step down), Fiat [FCA.IT] -1.2%, Exor [EXO.IT] -2.2%, Ferrari [RACE.IT] -2.5% (CEO Marchionne to step down due to ill health)

- Healthcare Philips [PHIA.NL] -2.3% (Earnings), Txcell [TXCL.FR] +150% (To be acquired)

- Financials Julius Baer [BAER.CH] -4% (Earnings), Binckbank [BINCK.NL] +4.8% (Earnings)

- Technology Atos [ATO.FR] -6.3% (Earnings, Acquisition)

Speakers

- Italy League party official Borghi (budget committee): Italy needed expansive economy policies, said to ask why Italy could not overlook the EU budget rule (**Reminder: Italy Interior Min Salvini (also Dep PM) also urged the EU to review budget rules)

- Russia Central Bank changes reserve requirement ratios as it raised the RRR on FX liabilities by 100bps; effective Aug 1st

- Poland Central Bank official Lon: MPC to help govt policy with CPI under control noting that real negative rates might help boost investments

- China Foreign Ministry spokesperson Hua Chunying: Treats and intimidation would never work out; reiterated view that Yuan exchange rate was determined by the market. No need to use competitive devaluation of its currency to support its exports. Needed to see credibility before it could begin talks with the US on trade

- North Korea said to seek a bold move by the US regarding a peace treaty. If the US was unwilling to replace the armistice agreement that ended the Korean War with a permanent peace that would ensure the survival of North Korean leader Kim Jong Un's regime, Pyongyang would likely not proceed further with denuclearization talks

- Iran Revolutionary Guards senior commander: Trump's anti-Iran remarks are psychological war

Currencies

- The USD maintained a soft tome after President Trump criticized the Fed for raising interest rates and suggested the USD was too strong.

- JGBs have sold-off across the board following reports late Friday that the BOJ might consider changes to interest rate targets. BoJ might be willing to let 10-yearJGB yields rise to some degree including a possible hike of the target level (which is currently “around 0%”). During the Asian session earlier today JGB 2-year, 10-year and 30-year yields were higher (apporx+1.8bps, +4.5bps, and +8.0bps respectively while the Yen formed approx. 0.5%. The BoJ stepped in to o?er to buy unlimited bonds at a ?xed rate of 0.11%, helping to cap the move for the time being. USD/JPY hovering around the 111 area just ahead of the NY morning.

- Focus on ECB rate decision and press conference on Thursday with analysts not expecting any policy changed at this time. Rather the markets to be on the lookout on any clarification on the 1st potential rate hike. EUR/USD holding above the 1.17 level in quiet trading.

- GBP remained susceptible to headline risk but a lot of negativity seemed to be already priced. With parliament in recess the GBP could stage a modest retracement from the current 1.3125 area.

Fixed Income

- Bund Futures trades at 162.38 down 8 ticks and near the session lows. A move back above 162.50 would target 163.47 then 163.63, with a move below 161.95 targeting 161.65 then 160.45.

- Gilt futures trades at 123.54 down 9 ticks on the day consolidating the recent run up, with continuing upside targeting 124.18 then 124.44, with a move lower seeing initial support at 123.23 then 122.85.

- Monday's liquidity report showed Friday's excess liquidity rose from €1.802T to €1.806T. Use of the marginal lending facility climbed from €45M to €65M.

- Corporate issuance saw $32B raised by high-grade issuers last week.

Looking Ahead

- 05:30 (DE) Germany to sell €2.0B in 6-Month BuBills

- 05:30 (BE) Belgium Debt Agency (BDA) to sell €3.1-3.6B in 2024, 2028, 2037 and 2066 OLO bonds

- Sells € in 0.50% Oct 2024 OLO; Avg Yield: % v 0.371% prior; Bid-to- 06:00 (IL) Israel to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 08:00 (PL) Poland Jun M3 Money Supply M/M: 0.6%e v 1.3% prior; Y/Y: 7.4%e v 6.6% prior - 08:00 (UK) Baltic Dry Bulk Index

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:30 (US) Jun Chicago Fed National Activity Index: +0.25e v -0.15 prior

- 08:30 (CA) Canada May Wholesale Trade Sales M/M: 0.7%e v 0.1% prior

- 08:55 (FR) France Debt Agency (AFT) to sell combined €3.6-4.8B in 3-month, 6-month and 12-month BTF Bills

- 09:00 (MX) Mexico May IGAE Economic Activity Index (monthly GDP) Y/Y: 2.1%e v 4.5% prior

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 10:00 (US) Jun Existing Home Sales: 5.45Me v 5.43M prior

- 10:00 (EU) Euro Zone July Advance Consumer Confidence: -0.7e v -0.5 prior

- 11:30 (US) Treasury to sell 3-month and 6-month Bills

- 13:00 (IT) Italy Debt Agency (Tesoro) announcement on upcoming CTZ and BTPei auctions for Thursday, July 26th

- 13:00 (UK) BOE’s Broadbent

- 15:00 (CO) Colombia May Economic Activity Index (monthly GDP) Y/Y: 2.8%e v 3.5% prior

- 16:00 (US) Weekly Crop Progress Report

Nikkei lost -1.33% on Yen’s strength, China SSE gained 1% as government manipulate halted Yuan’s slide

In tandem with the strong rally in the Japanese yen today, Stocks were sold off deeply. Nikkei 225 ended the day down -300.89 pts, or -1.33%, at 22396.99. Technically, 23050.39 proves to be too strong a resistance level for Nikkei.

But still, for now, we're favoring the bullish case that rise from 21462.94 is resuming whole rebound from 20347.59. Hence, we'd expect strong support at around 55 day EMA (now at 22345.59) to contain downside and break rally resumption. Firm break of 23050.93 will confirm rise resumption for 100% projection of 20347.49 to 2305039 from 21462.92 at 24165.84. That is close to 24129.34 high.

However, sustained break of the 55 day EMA will extend the sideway pattern inside 21462.94/23050.39 in near term.

On the other hand, China Shanghai SSE composite gained 30.27 pts also 1.07% to close at 2859.54. the break of 2848.37 resistance confirm resumption of rebound from 2691.02 low. Sentiments have clearly improved on talks that China has intervened last week to halt the Yuan's recent free fall.

Further rise should be seen to 55 day EMA (now at 2946.10) and possibly above. But at this point, we're seeing no prospect of sustained break of 3000 handle. Hence, we'd expect another fall back to retest key support zone between 2016 low at 2638.30 and 2700 at a later stage.

EURUSD Moving Back Towards Key Support

The euro currency has started to turn-lower against the US dollar after the pair found strong resistance from the 1.1750 level earlier today. Despite the correction lower during the European trading session, the EURUSD pair still retains a bullish bias while trading above the 1.1681 level. EURUSD buyers will continue to look for further upside above the 1.1750 level, while sellers will look to break below the 1.1681 level.

The EURUSD pair is only intraday bullish while trading above the 1.1681 level, key resistance is now found at the 1.1750 and 1.1800 levels.

If the EURUSD pair falls below the 1.1681 level, sellers will target the 1.1650 and 1.1630 support levels.

USDJPY Further Bearish Below 111.00

The US dollar remains under heavy selling pressure against the Japanese yen currency on Monday, as the sell-off on the US dollar index gathers pace. The USDJPY pair has tumbled below the 111.00 level and has so far found support from the 200-period moving average on the four-hour time frame. Sellers will target the 110.10 level, while buyers will look to move the price back above the 111.40 level.

The USDJPY pair is strongly intraday bearish while trading below the 111.00 level, key support is found at the 110.10 and 109.50 levels.

If the USDJPY pair moves above the 111.40 level, buyers may test towards the 112.20 and 112.80 levels.

DAX Under Pressure After Trump Threatens Currency War

The DAX index has posted losses in the Monday session. Currently, the DAX is at 12,510, down 0.41% on the day. On the release front, there are no key German or eurozone indicators. Eurozone Consumer Confidence, which hasn’t posted gains since January, is expected to dip to -1 point. On Tuesday, Germany and the eurozone will release service and manufacturing PMIs.

President Trump made waves on Friday, after attacking the Federal Reserve’s monetary policy and also taking shots at the EU. Trump criticized the EU and China for manipulating their currencies and keeping interest rates lower. The escalating trade war, which started with Trump slapping tariffs on China, the EU and other trading partners, has weighed on global equity markets. Investors now have a new concern, which is that Trump could once again show that he is not afraid to lock horns with the EU and China, and the result could be a global currency war.

Investors are keeping a close eye on the June service manufacturing PMIs for Germany and the eurozone, which will be released on Tuesday. The manufacturing PMIs have weakened for six straight months – will this continue in June? Although the PMIs continue to show expansion in Germany and the eurozone, the markets remain nervous that the escalating trade war is having a negative impact on the manufacturing sector. If the readings continue to head lower on Tuesday, European equity markets could respond with losses.

After years of monetary stimulus to boost the eurozone economy, the ECB is close to phasing out its asset-purchase program. The ECB plans to trim its monthly purchases from EUR 30 billion to 15 billion in September and wind up the program in December. Is a rate hike next on the menu? Any clues of a change in monetary policy are bound to affect the euro, as the ECB has not raised rates since 2011. Many analysts are predicting a rate hike in the second half of 2019. However, growing global trade tensions could put a wrinkle in plans to raise rates. The European Commission and the International Monetary Fund have lowered 2018 growth forecasts for the eurozone and for Germany. If the tariff slugfest continues, the markets could lose ground.

Bundesbank: German economy regaining some lost momentum

Bundesbank said in the latest monthly report released today that the German economy is regaining some momentum currently. It noted that "the economy has likely showed better momentum in the spring than at the start of the year." Nonetheless " it is unlikely that the high growth rates of the past year will be repeated, manufacturing was once again the key economic driving force."

The report noted that car production increased sharply with pharmaceutical products. But intermediates goods remained weak. Household consumption remained a cornerstone for growth. Government consumption also rebounded. Also, "activity in the booming construction sector likely increased significantly, despite capacity constraints."

Trade And Currency Wars A Market Threat

Monday July 23: Five things the markets are talking about

A new week starts with equities under pressure as capital markets digest warnings from G20 finance ministers about the impact of protectionism on growth – “risks to the world economy have increased.”

Also raising concerns is the Sino-U.S trade war is now spilling over into currency markets with President Trump rhetoric supporting the U.S administration preference for lower U.S dollar interest rates and a weaker currency.

Elsewhere, the yen (¥111.00) has found support while JGB's slid on speculation about Bank of Japan's (BoJ) stimulus. Crude prices trade a tad softer amid concern the escalating trade rows will destabilize energy demand.

On tap: an E.U Trade Commission is due to arrive stateside this week for trade talks. Expect some tough questions, demands and their own list of retaliatory measures in response to proposed U.S tariffs. The highlight of the week should be Thursday's European Central Bank (ECB) monetary policy meeting.

1. Stocks start the week under pressure

Japan's Nikkei fell to a ten-day low overnight, with exporters under pressure by the yen's (¥111.00) rally and by market speculation that the Bank of Japan (BoJ) could wind back its exchange-traded fund purchases. The Nikkei ended the day down -1.33%.

Note: The market is speculating that the BoJ could debate changes in its monetary policy at its upcoming meeting, with potential tweaks to its interest rate targets and stock-buying techniques on the table.

Down-under, Aussie shares fell on President Trump's threat to impose tariffs on all Chinese imports. The S&P/ASX 200 index declined -0.9% at the close of trade. The benchmark gained +0.4% on Friday. In S. Korea, it was a similar story. The Kospi fell about -1% overnight following Trump's comments about tariff's and the currency last week.

In China, stocks rallied on Monday, aided by strength in financials and industrial stocks, but a slump in healthcare shares capped the broader gains. The blue-chip CSI300 index rose +0.9% while the Shanghai Composite Index ended up +1.1%.

In Hong Kong, it was a similar story. Stocks rose slightly overnight, as declines in tech and consumer shares were offset by strength in financials. The Hang Seng index rose +0.1%, while the China Enterprises Index gained +0.5%.

In Europe, regional bourses are trading mostly lower across the board, following a mixed session in Asia. The Italian FTSE MIB is in focus following weakness in shares of Fiat and Ferrari after the stepping down of its CEO Sergio Marchionne due to health.

U.S stocks are set to open in the ‘red' (-0.1%).

Indices: Stoxx600 -0.1% at 385.1, FTSE -0.4% at 7651, DAX -0.1% at 12549, CAC-40 -0.3% at 5382, IBEX-35 +0.2% at 9743, FTSE MIB -0.1% at 21,775, SMI -0.5% at 8947, S&P 500 Futures -0.1%

2. Oil steady after G20 warns of risks to growth, gold higher

Oil prices have stabilized as worries over production losses were outweighed by concerns that trade disputes would reduce economic growth and hit global energy demand.

Benchmark Brent crude oil is up +15c at +$73.22 a barrel, while U.S light crude is unchanged at +$68.26.

G20 Finance ministers over the weekend called for more dialogue to prevent trade and geopolitical tensions from hurting growth as “downside risks over the short and medium term have increased.”

Note: Baker Hughes data on Friday showed that U.S energy companies last week cut the number of oil rigs by the most since March following recent declines in oil prices. Drillers cut five oilrigs in the week to July 20, bringing the count down to 858.

Ahead of the U.S open, gold prices are steady atop of a one-week high as the dollar eased to a two week low after President Trump criticised the Fed's interest rate tightening policy. Spot gold holds steady at +$1,231 an ounce. U.S gold futures for August delivery are nearly unchanged at +$1,231 an ounce.

3. Japan yields in focus

JGB's have sold-off along the curve on reports late Friday that the BoJ might consider changes to interest rate targets. The market is speculating that the BoJ might be willing to let 10-year JGB yields (+0%) rise to some degree including a possible hike of the target level. Overnight, JGB 2-, 10- and 30-year yields were higher (+1.8, +4.5, and +8.0 bps respectively).

BoJ officials said to be looking for ways to keep stimulus program sustainable while reducing the harm it causes to markets and bank profits.

Note: The BoJ stepped in to buy unlimited bonds at a fixed rate of +0.11%, to cap the move.

On tap for this week: The ECB monetary policy meeting is on Thursday, no policy stance expected, but the market is looking for clarification on their first potential rate hike.

Elsewhere, the yield on 10-year Treasuries gained less +1 bps to +2.90%, the highest in more than a month, while in the U.K; the 10-year Gilt yield advanced +1 bps to +1.232%.

4. Dollar under pressure from Trump rhetoric

The ‘mighty' USD maintains its softer tone after President Trump criticized the Fed for raising interest rates and suggested the USD was too strong.

Aside from currency Twitter rants, the markets focus this week will be on the ECB rate decision and press conference on Thursday. Consensus is ‘not' anticipating any policy change in the short to medium term, however, the markets will be on the lookout for any clarification on the first potential rate hike. The EUR/USD is still flipping alternately between moves towards €1.16 and over €1.17 in response to news on the trade row, given the lack of clear direction.

GBP (£1.3124) continues to remain vulnerable to “headline risk,” but consensus believes a lot of negativity seems to be already priced. With parliament in recess, sterling has the potential to stage a modest retracement from its current area.

5. G20 communiqué

In their final communiqué yesterday from their meeting in Argentina, finance ministers and central bankers from the G20 economies said, “Heightened trade and geopolitical tensions pose an increased risk to global growth” and called for greater dialogue.

“Global growth remains robust and unemployment is at a decade low. However, growth has become less synchronised recently, and downside risks over the sort and medium term have increased,” said the communiqué.