Sample Category Title

Japan’s Manufacturing Activity Tumbled To A 20-Month Low Level In July

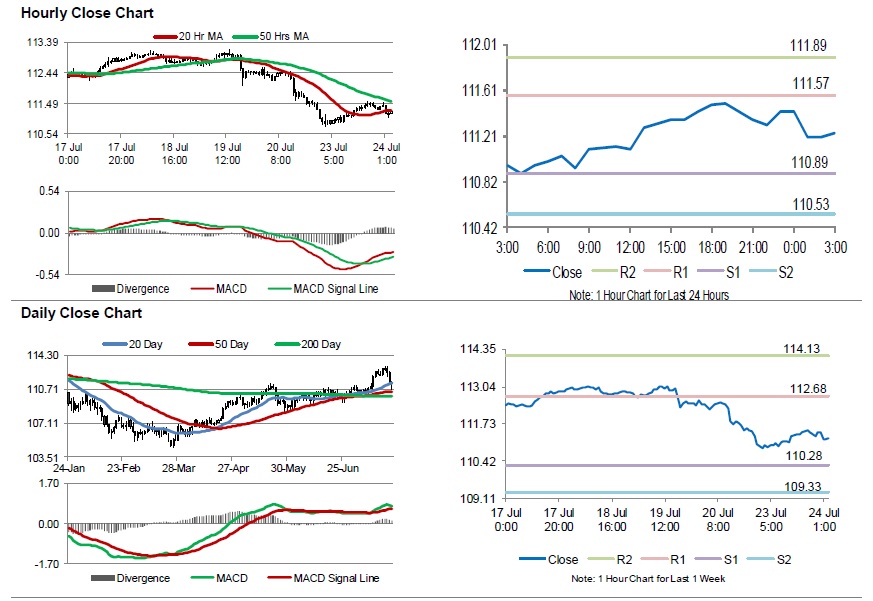

For the 24 hours to 23:00 GMT, the USD rose 0.50% against the JPY and closed at 111.42.

In the Asian session, at GMT0300, the pair is trading at 111.24, with the USD trading 0.16% lower against the JPY from yesterday's close.

Overnight data revealed that Japan's flash Nikkei manufacturing PMI eased to a 20-month low level of 51.6 in July, following a reading of 53.0 in the prior month.

The pair is expected to find support at 110.89, and a fall through could take it to the next support level of 110.53. The pair is expected to find its first resistance at 111.57, and a rise through could take it to the next resistance level of 111.89.

Moving ahead, traders will await Japan's leading index and coincident index, both for May, scheduled to release in a while.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Swiss Franc Trading A Tad Higher In The Asian Session

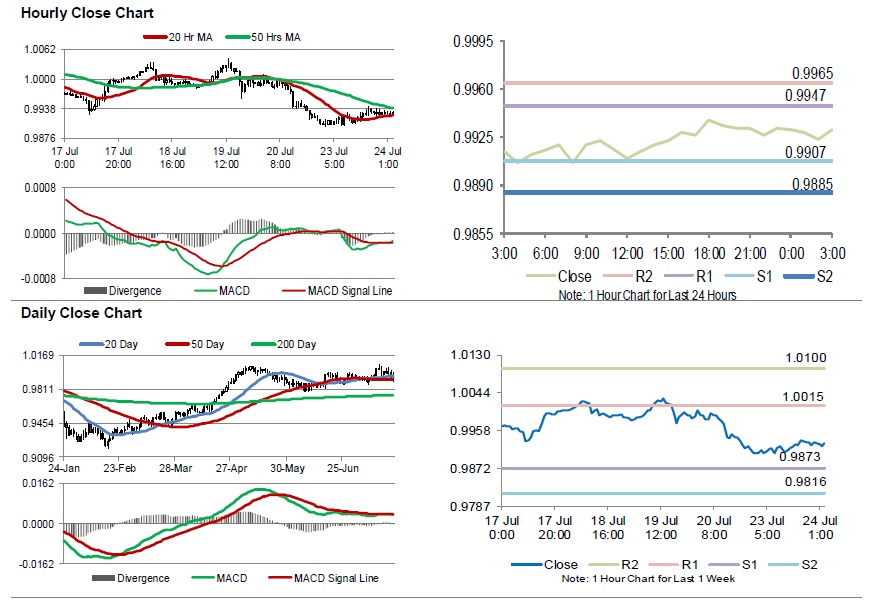

For the 24 hours to 23:00 GMT, the USD rose 0.25% against the CHF and closed at 0.9931.

Macroeconomic data showed that, Switzerland’s total sight deposits rose to a level of CHF576.3 billion in the week ended 20 July, from CHF576.1 billion in the previous week. Moreover, the nation’s M3 money supply grew 2.4% on a yearly basis in June, after registering a revised advance of 2.8% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9930, with the USD trading slightly lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9907, and a fall through could take it to the next support level of 0.9885. The pair is expected to find its first resistance at 0.9947, and a rise through could take it to the next resistance level of 0.9965.

With no macroeconomic releases in Switzerland today, investors would look forward to global macroeconomic releases for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average

Loonie Trading Marginally Higher In The Morning Session

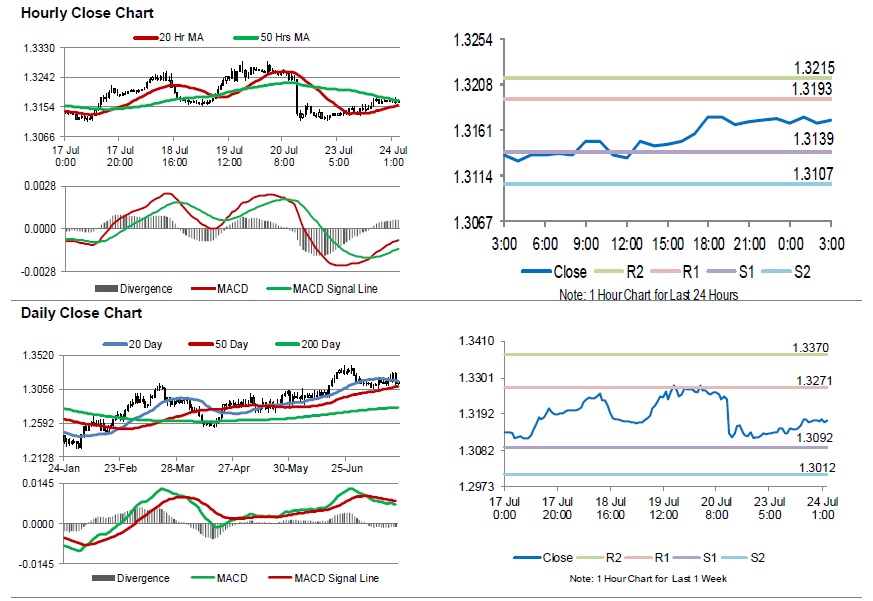

For the 24 hours to 23:00 GMT, the USD rose 0.34% against the CAD and closed at 1.3173.

In the Asian session, at GMT0300, the pair is trading at 1.3172, with the USD trading slightly lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.3139, and a fall through could take it to the next support level of 1.3107. The pair is expected to find its first resistance at 1.3193, and a rise through could take it to the next resistance level of 1.3215.

Amid lack of economic releases in Canada today, traders would focus on global macroeconomic events for further direction.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

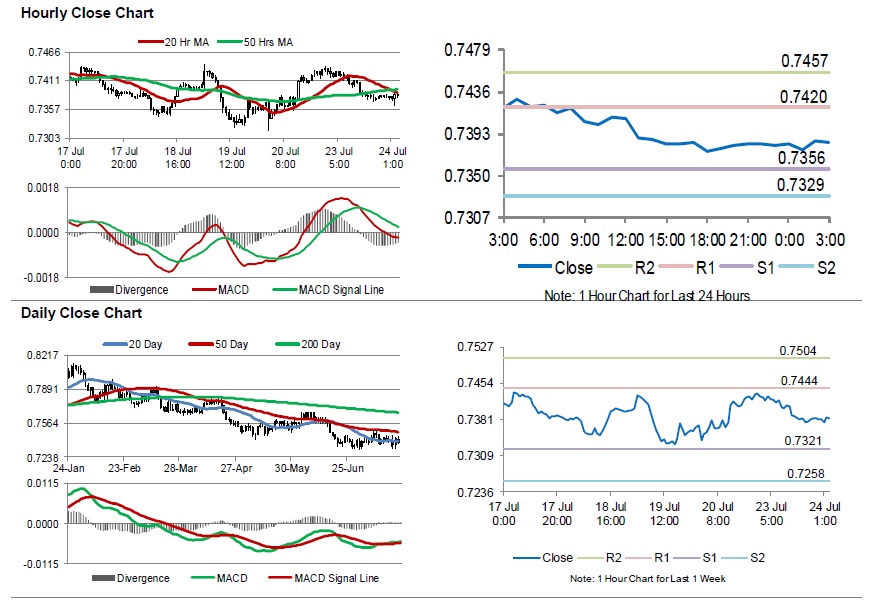

Aussie Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, the AUD declined 0.59% against the USD and closed at 0.7381.

LME Copper prices rose 1.3% or $ 80.0/MT to $ 6153.0/MT. Aluminium prices rose 2.7% or $ 55.0 /MT to $ 2130.0 /MT.

In the Asian session, at GMT0300, the pair is trading at 0.7384, with the AUD trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7356, and a fall through could take it to the next support level of 0.7329. The pair is expected to find its first resistance at 0.7420, and a rise through could take it to the next resistance level of 0.7457.

Trading trend in the Aussie will be determined by the release of consumer price index for Q2, slated to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

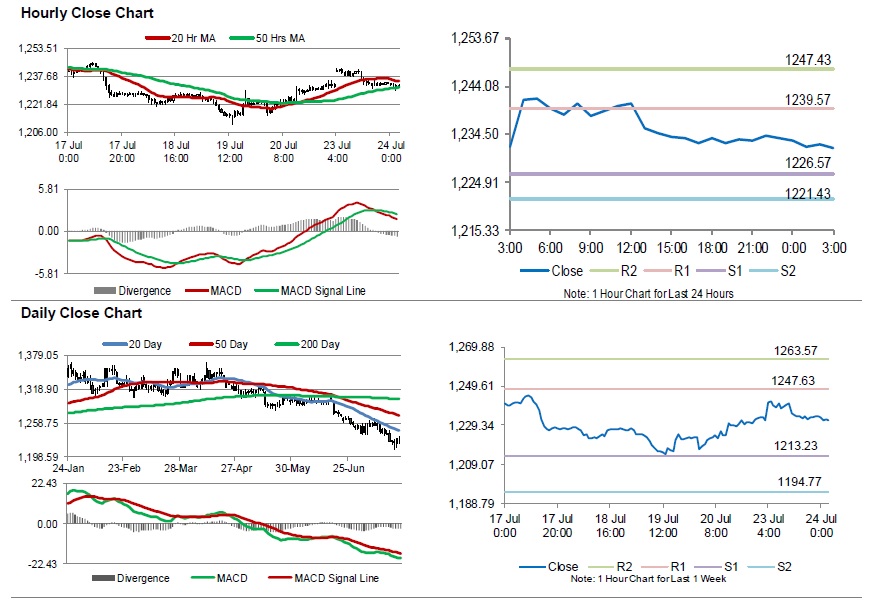

Gold: Yellow Metal Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, Gold rose 0.08% against the USD and closed at USD1234.20 per ounce.

In the Asian session, at GMT0300, the pair is trading at 1231.70, with gold trading 0.20% lower against the USD from yesterday’s close.

The pair is expected to find support at 1226.57, and a fall through could take it to the next support level of 1221.43. The pair is expected to find its first resistance at 1239.57, and a rise through could take it to the next resistance level of 1247.43.

The yellow metal is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

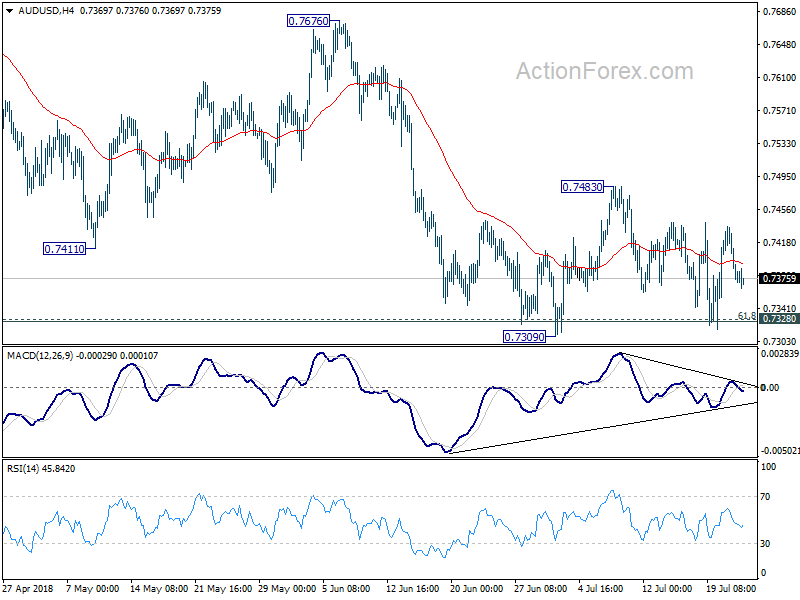

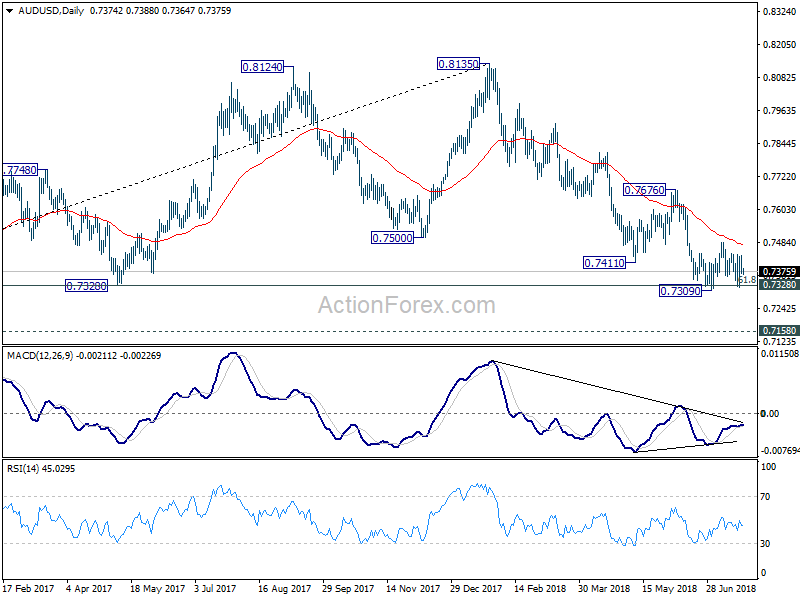

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7355; (P) 0.7397; (R1) 0.7422; More...

AUD/USD dipped notably today but stays in range of 0.7309/7483. Intraday bias remains neutral at this point and outlook is unchanged. Price actions from 0.7309 are seen as a consolidation pattern. Above 0.7483 will bring stronger rebound. But in that case, upside should below 0.7676 resistance to bring larger fall resumption. On the downside, break of 0.7309 and sustained trading below 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

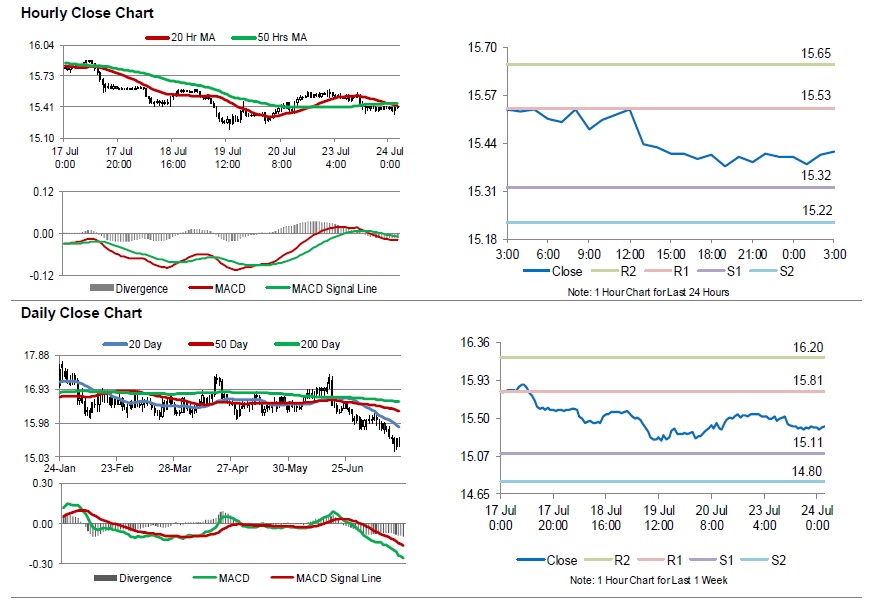

Silver: White Metal Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, Silver declined 1.00% against the USD and closed at USD15.40 per ounce.

In the Asian session, at GMT0300, the pair is trading at 15.42, with silver trading 0.10% higher against the USD from yesterday’s close.

The pair is expected to find support at 15.32, and a fall through could take it to the next support level of 15.22. The pair is expected to find its first resistance at 15.53, and a rise through could take it to the next resistance level of 15.65.

The white metal is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Treasury Yields Continue to Support Yen and Dollar, Risk Appetite Ignored

Yen and Dollar are trading as the strongest ones for today and the week, as boosted by treasury yields. In particular, the Yen shrugs off strong risk appetite in Asia, as led by Chines stock markets. 10 year JGB yield opened higher at 0.088 and stays firm at around 0.086 at the time of writing. It has been bounded in range of 0.023 and 0.049 in July up until this Monday. Judging from the current momentum, 10 year JGB yield is having 1% in sight. And that could provide the Yen with extra support.

Dollar also benefits from surging treasury yield, especially at the long end. It started with the strong rally in 30 year yield last Friday. Overnight, five year yield gained 0.060 to 2.828. 10 year yield rose 0.070 to 2.965. 30 year yield rose 0.073 to 3.104. Yield curve is clearly steepening again and that should ease the worries of some Fed officials. They'll be more comfortable to continue with monetary policy normalization for the rest of the year, with two more rate hikes.

In other markets, China Shanghai SSE is rising 1.64% at the time of writing, breaking 2900 handle. We'd continue to expect strong resistance from 3000 to limit upside. But let's see if it will slow down ahead. Strength in Chinese stock led Hong Kong HSI up 1.52%. Nikkei also pared back some of yesterday's -300 pts loss, trading up 122 pts or 0.54%. Singapore Strait Times is up 0.26%. Gold is back below 1220 as Dollar regains strength. WTI crude oil is back below 68, at 67.65. 70 handle is still too much for WTI.

Technically, USD/JPY's breach of 111.50 minor resistance indicates temporary bottoming in the pair. But for the near term, more downside is still mildly in favor. Other Dollar pairs are basically stuck in familiar range and more consolidations will be likely in near term.

BoE Broadbent unsure of his August Bank Rate vote yet

BoE Deputy Governor Ben Broadbent said yesterday that he hasn't decide on his vote on the Bank rate in the upcoming meeting on August 2 yet. Markets were pricing in 80% chance of an August hike two weeks ago. But the chance dropped to around 50% after last week's CPI miss. CPI had slowed notably from 3.0% in January to 2.4% in May, then stayed there in June. And, the impact of import inflation has faded much quicker than BoE has expected. Even if BoE does hike in August, it will be a one and done for the year.

Broadbent's comment came after a speech on "The history and future of QE". There he reiterated that the "framework" for unwinding QE was set out for some time in the November 2015 Inflation Report. That is, BoE would begin to start shrinking the balance sheet "only once the official Bank Rate had risen some way". And that's because "conventional policy is more flexible, better suited to responding to short-term economic fluctuations".

At the initial guidance, Broadbent noted that the meaning of "well underway" means Bank Rate at "around 2%". But in the June Monetary Policy Summary this year, the estimated threshold was lowered to "around 1.5%". He also noted that "we don't know exactly when that will be". But, "the framework is designed to ensure that, should inflationary pressures weaken after that date, the first response would be to cut interest rates." And, "in principle, those disinflationary influences might include the process of QE unwind itself."

Japan PMI manufacturing dropped to 51.6, slowing of growth momentum

Japan PMI manufacturing dropped to 51.6 in July, hitting a 20-month low. That's also below expectation of 52.7. Markit economist Joe Hayes noted in the release that the flash data pointed to a "slowing of growth momentum for Japan's manufacturing sector at the beginning of the third quarter, following a robust performance so far this year." New business grew at a "much weaker rate". And export demand "deteriorated for a second month running."

China unveiled fine-tuning policies measures to boost growth

China unveiled fine-tuning policies measures to boost growth yesterday. Firstly, there will be targeted tax reduction for research and development spending, that could lower around CNY 65B in taxes. Secondly, monetary policy have to ensure ample liquidity in the markets. Financial institutions will be guided to use the RRR cuts to support small and micro businesses. Thirdly, the funding of the National Financing Guarantee fund will be speeded up to achieve the goal of supporting 150,000 small and micro businesses with CNY 140B in loans per annum. Fourthly, "zombie businesses" will be cleared out resolutely to manage systematic risks.

PMIs to highlight the day

Looking ahead, PMI data are the main focuses today. Eurozone PMI manufacturing and services will be featured in European session. US will also release PMI manufacturing and services, as well as house price index.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7355; (P) 0.7397; (R1) 0.7422; More...

AUD/USD dipped notably today but stays in range of 0.7309/7483. Intraday bias remains neutral at this point and outlook is unchanged. Price actions from 0.7309 are seen as a consolidation pattern. Above 0.7483 will bring stronger rebound. But in that case, upside should below 0.7676 resistance to bring larger fall resumption. On the downside, break of 1.7309 and sustained trading below 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | PMI Manufacturing Jul P | 51.6 | 52.7 | 53 | |

| 07:00 | EUR | France Manufacturing PMI Jul P | 53.9 | 52.5 | ||

| 07:00 | EUR | France Services PMI Jul P | 54.3 | 55.9 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jul P | 55.7 | 55.9 | ||

| 07:30 | EUR | Germany Services PMI Jul P | 54.5 | 54.5 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | 54.6 | 54.9 | ||

| 08:00 | EUR | Eurozone Services PMI Jul P | 55.1 | 55.2 | ||

| 13:00 | USD | House Price Index M/M May | 0.30% | 0.10% | ||

| 13:45 | USD | US Manufacturing PMI Jul P | 55.5 | 55.4 | ||

| 13:45 | USD | US Services PMI Jul P | 56.3 | 56.5 |

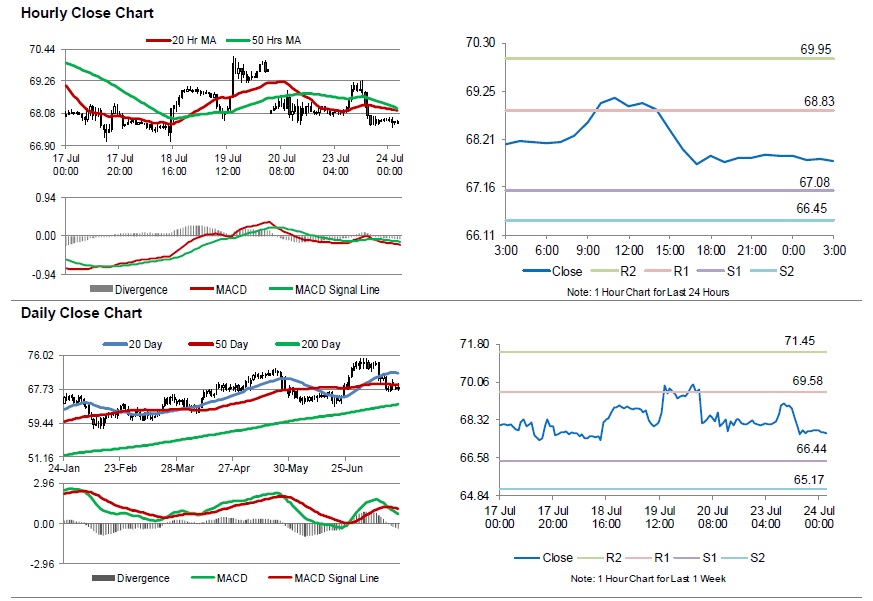

Crude Oil: Oil Trading Lower, Ahead Of API’s Weekly Crude Oil Inventories Data

For the 24 hours to 23:00 GMT, Crude Oil declined 0.34% against the USD and closed at USD67.83 per barrel, amid concerns of oversupply overshadowed worries over mounting tension between the US and Iran.

In the Asian session, at GMT0300, the pair is trading at 67.72, with oil trading 0.16% lower against the USD from yesterday's close.

The pair is expected to find support at 67.08, and a fall through could take it to the next support level of 66.45. The pair is expected to find its first resistance at 68.83, and a rise through could take it to the next resistance level of 69.95.

Crude oil is trading below its 20 Hr and 50 Hr moving averages.

Yen and Dollar strong on treasury yields, shrug off risk appetite

Yen and Dollar are trading as the two strongest ones today, and for the week, as supported by strength in treasure yields. 10 year JGB yield opened higher at 0.088 today and stays firm at 0.085 at the time of writing. It was bounded between 0.023 and 0.049 in July up until this Monday. Judging from the current momentum, 10 year JGB yield is having 1% in sight. Note that Yen is having little reaction to the China led Asian markets rally. It will continue to "listen" more to JGB yield than stocks/risk sentiments.

Meanwhile, US 10 year yield gained 0.70 overnight to close at 2.965. The strong rise, as led by 30 year yield's jump since last Friday, should set the stage for 3.000 handle and above. For now, we'd not seeing any decisiveness for a break of 3.115 high yet. But it's something that's worth monitoring. While Dollar seemed to be talked down by Trump's comment last week, surging yield would bring it back to life.