Sample Category Title

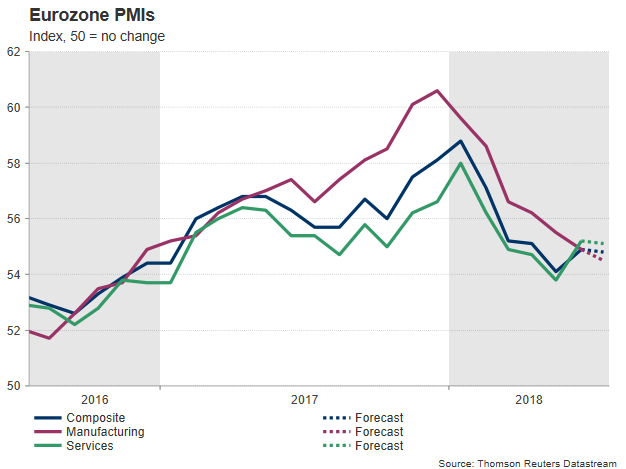

Eurozone Flash Manufacturing PMI Next to Drive Euro

Eurozone economic performance has been in question in the second half of 2018 ever since a row of soft data raised concerns that the slowdown registered in the first quarter could be more than temporary. Markets will now shift focus to July’s flash Purchasing Managers Index (PMI) figures due on Tuesday which are the last evidence on the economy before the European Central Bank policy meeting takes place on Friday. Yet, analysts believe that businesses have experienced another bearish run this month as rising trade risks around the US trade policy keep business leaders worried about the extent their exports orders could narrow.

In June, IHS Markit found that activity in the manufacturing industry turned to be the weakest since January 2017, with the manufacturing PMI index retreating for the sixth consecutive month from 55.5 in May to 54.9 as business expectations about future production deteriorated to the lowest since November 2015. That was also 6 points below the record high of 60.6 reached in December. For the month of July analysts now believe that the story is the same, expecting the measure to inch lower to 54.6, while regarding the services PMI this is forecasted to retreat from 55 to 54.8. Overall, the composite PMI, is projected to ease to 54.8 from 54.9 in the previous month.

Indeed, Eurozone factories could have been under stress in July as their supplies to the US were restricted for the second month by steel and aluminum import tariffs, while this month they also faced extra costs to buy products from the US as the EU took the decision to retaliate, targeting iconic products such as Harley Davidson motorcycles and Levi’s jeans (in effect since early July). But on top of that, the White House announced that it would add further pressure to its EU allies, hiking tariffs on imported cars and auto parts from 2.5% to 20% if they don’t remove their duties on US products. A move that has raised stronger oppositions as the auto industry holds the largest share of the manufacturing sector in the EU, while the US is their biggest export destination (followed by China which is also subject to US metal tariffs).

Indeed, Eurozone factories could have been under stress in July as their supplies to the US were restricted for the second month by steel and aluminum import tariffs, while this month they also faced extra costs to buy products from the US as the EU took the decision to retaliate, targeting iconic products such as Harley Davidson motorcycles and Levi’s jeans (in effect since early July). But on top of that, the White House announced that it would add further pressure to its EU allies, hiking tariffs on imported cars and auto parts from 2.5% to 20% if they don’t remove their duties on US products. A move that has raised stronger oppositions as the auto industry holds the largest share of the manufacturing sector in the EU, while the US is their biggest export destination (followed by China which is also subject to US metal tariffs).

After all, the EU showed the willingness to lower its barriers on US car imports, with the German Chancellor, Angela Merkel, saying she would support such a decision. But tensions have remained high since then and the G20 ministers meeting in Buenos Aires during the weekend did little to break the ice, leaving businesses in the dark about their future growth plans. Instead, the US Treasury Secretary, Steven Mnuchin, defended the US trade strategy, reiterating that any trade deal with the EU should go beyond tariffs cuts, such as the elimination of non-tariff barriers and subsidies. In response the French and German finance ministers signaled that talks on a trade agreement would not be possible if the US do not lift its metal tariffs, leaving the ball into the European Commission President, Jean-Claude Junker’s hands to ease tensions. Note that Junker is scheduled to meet Trump in Washington on Wednesday to discuss security and economic matters.

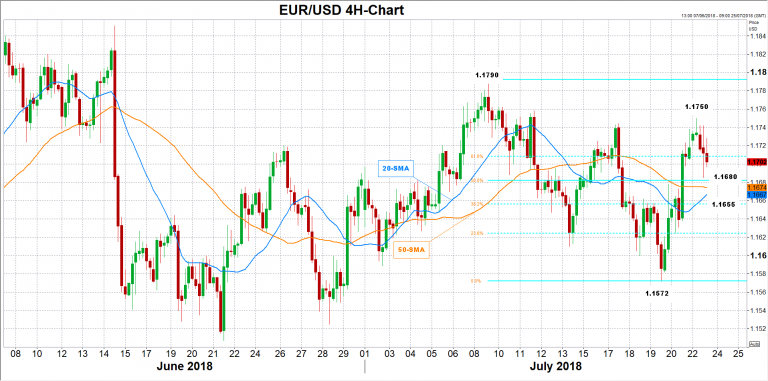

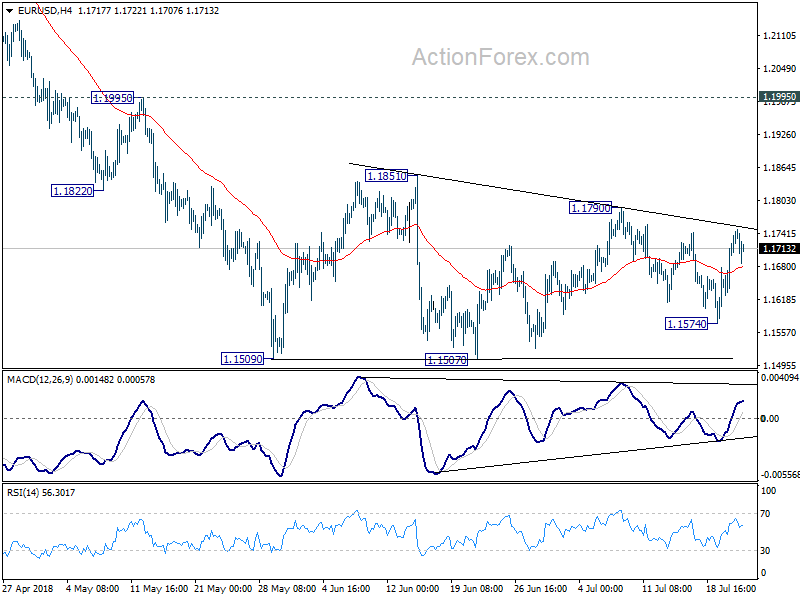

In the forex space, June’s disappointing final PMI prints had a negative impact on euro/dollar and if July’s flash PMIs turn to be lower than expected the pair could experience another bearish round. In this case, the price could probably test the 50% Fibonacci of 1.1680 of the downleg from 1.1790 to 1.1572 where the market found resistance earlier this month. A steeper downside triggered by increased speculation that economic growth in the eurozone has started to lose steam could push the pair below the 20- and the 50-period moving averages to meet the 38.2% Fibonacci of 1.1655, while the previous low of 1.1572 could also be in focus. On the other hand, a data bit could calm investors’ fears about the bloc’s outlook and send the pair up to 1.1750 peak reached early today before July’s top at 1.1790 come into view.

Following the PMI release on Tuesday as well as the German Ifo business confidence index on Wednesday, the biggest event of the week will be the European Central Bank’s policy meeting on Thursday. While policymakers are highly anticipated to keep rates unchanged and details on the termination of the quantitative program have been already published, the ECB chief, Mario Draghi, will use recent data to justify the central bank’s forward guidance on interest rates as inflation fluctuates near the ECB’s 2.0% price target. Encouraging data prints, for example, could signal that a rate hike could probably come before the end of 2019 as markets currently price in.

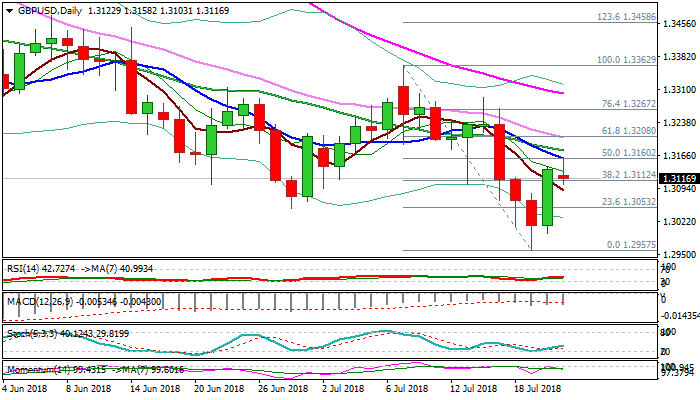

GBPUSD – Heavy Tone after Bulls Capped by Falling 10SMA

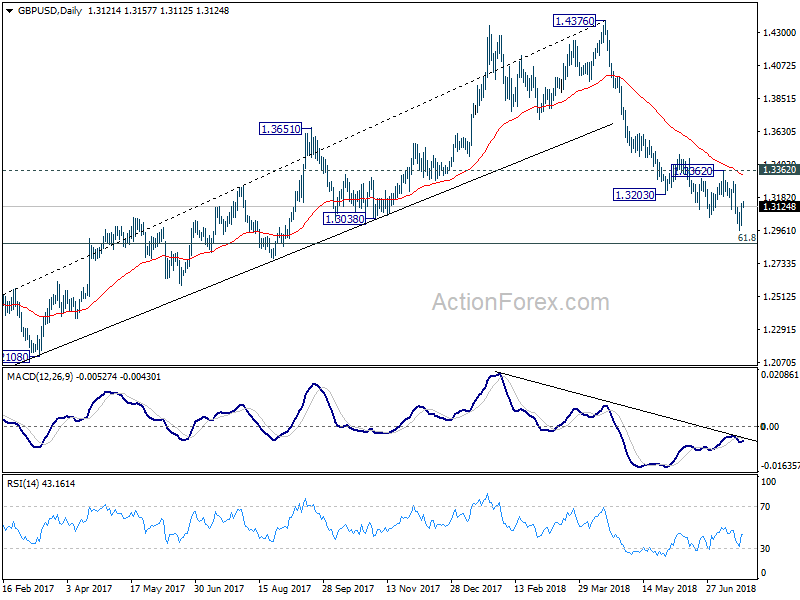

Cable holds at the back foot in early hours of the US trading after attempts to extend strong rally of last Friday were capped by falling 10SMA (1.3158) also 50% retracement of 1.3362/1.2957 bear-leg.

Bids at 1.31 zone (round-figure, reinforced by 5SMA) so far hold, but downside at risk.

Strong words from UK PM May today, regarding Brexit talks, produced mild reaction as markets look for more evidence.

Weakening momentum maintains pressure after a cluster of MA’s (10;20;30) stayed intact and continues to weigh, with larger picture showing strong pressure from falling thick daily cloud.

Look for fresh negative signal on close below 1.3100 zone, which would open way fro test of former key support at 1.3049 and psychological 1.30 support.

Bullish scenario needs close above 10SMA as minimum requirement to sideline downside threats and signal further recovery towards next pivot at 1.3207 (falling 20SMA / Fibo 61.8% of 1.3362/1.2957 bear-leg).

Res: 1.3158; 1.3176; 1.3207; 1.3267

Sup: 1.3112; 1.3087; 1.3049; 1.3000

US treasury yields surge, dollar trying to rebound

Dollar is apparently helped by surge in US treasury yields today, especially at the long end. While the momentum of the rebound isn't too strong yet, the development is worth a note.

30 year yield is still the most impressive one like last Friday. It's up 0.05 and breaches 3.08 handle. The development further affirms the case that the pull back from 3.247 has completed at 2.925. We'd likely seen further rise through 3.14 resistance in near term.

10 year yield is also finally showing meaningful movement. It's up 0.045 at 2.941. Rebound from is likely resuming based on current momentum. And, break of 3.009 resistance should be seen in near term.

Sunset Market Commentary

Markets

Global core bonds trade marginally lower today in an uninspiring, low volume trading session. Sentiment is gradually turning negative. Losses are mostly technically inspired in the Bund, following Friday’s bearish engulfing pattern. The US Note future heads to the lower bound of the July sideways trading range (119-30 to 119-27+). The calendar heats up later this week with EMU PMI’s (tomorrow), the US Treasury’s end-of-month refinancing operation, ECB meeting (Thursday) and US Q2 GDP release (Friday). The German yield curve shifts 0.4 bps (2-yr) to 1.9 bps (10-yr) higher. The US yield curve bear steepens with yield changes ranging between +0.9 bps (2-yr) to +2.2 bps (30-yr). 10-yr yield spread changes vs Germany range between -5 bps (Portugal) and +3 bps (Spain). The Belgian debt agency tapped 4 bonds today: OLO 82 (€0.7bn 0.5% Oct2024), OLO 85 (€1.1bn 0.8% Jun2028), OLO 84 (€1.2bn 1.45% Jun2037) and OLO 80 (€0.6bn 2.15% Jun2066). The combined amount sold was the maximum of the targeted €3.1-3.6bn. The total auction bid cover was 2, but demand was especially strong for the two shorted-dated OLO’s. The Belgian debt agency already raised 85% (€26.28bn) of this year’s €31bn OLO funding need.

Today, the dollar failed to develop a clear directional trend. Last week’s decline of the (trade-weighted) USD bottomed, but there was not one, unequivocal new driver. This morning, USD/JPY dropped (temporarily?) below 111, but this move was mainly yen strength on rumours that the BOJ could change the implementation of its policy. This change could de facto lead to higher yields, supporting the yen. The USD/JPY decline slowed later in the session. At the same time, EUR/USD also eased after the ‘Trump-driven’ decline of last week. Uncertainty on the trade conflict between the US and China, but also between the US and the EU remains high. In this respect, it remains highly uncertain whether this week’s meeting between US president Trump EC president Juncker will turn out favourable for the dollar rather than for the euro. A failure to find a solution on the key automobile tariffs could be a negative fort the euro rather than for the dollar. Markets also doubt that this week’s ECB meeting will yield much support for the euro. To summarize, last week’s call from US president Trump for a weaker dollar has apparently been working out for now. From here next steps in trade war sage remain highly uncertain, leaving USD traders in some kind of no-man’s-land. EUR/USD is trading in the 1.1715 area. USD/JPY struggles not to fall back below the 111 area.

There was also little news to guide sterling trading today. At a meeting with its German counterpart, new UK foreign Secretary Hunt said that there is a real risk of no Brexit deal. To avoid such a scenario he expects the EU to do concessions first. The meeting only illustrates that the UK and the EU are still far away from a detailed Brexit deal. However, the headlines didn’t hurt sterling after last week’s decline. The UK currency even regained slightly ground. EUR/GBP trades currently in the 0.8915/20 area. Cable trades in the 1.3135 area. This evening, BoE’s Broadbent will speak in London. Markets will look out whether he supports the case for an August rate hike.

News Headlines

New British foreign secretary Jeremy Hunt has stated that “there is a very real risk of the UK crashing out of the EU without a deal” in March next year. These comments feed further desire for both parties, as well as companies, to work on contingency planning for a no-deal scenario.

Brent crude oil gained around 1% today to test $74 a barrel after a three-week slump. Reason is US President Trump’s warning at the address of Iran that they would suffer consequences if it kept threatening the US. Iranian president Rouhani earlier warned the US of a potential confrontation between Washington and Tehran.

The European Commission has said that EC President Jean-Claude Juncker will not bring a specific trade offer to the table in Washington on Wednesday. The purpose of the meeting is “to stay engaged in dialogue”. The comments were released after Trump’s top economic adviser, Kudlow, said to be expecting a ‘significant’ trade offer.

UK Hunt, Some wait for UK to blink on Brexit talk, but that won’t happen

UK Foreign Minister Jeremy Hunt warned that there is "now a very real risk of a Brexit no-deal by accident". He said that alongside German Foreign Minister Heiko Maas in a visit to Germany today. Hunt added that "many people in the EU are thinking that they just have to wait long enough and Britain will blink", but "that's not going to happen". Also, "without a real change in approach from the EU negotiators we do now face a real risk of no deal by accident and that would be incredibly challenging economically,"

Maas said in the same occasion that "we know that everyone has to make mutual concessions to get this deal." And, "European Union has its interests, overall interests, so not just individual member-states but EU institutions."

According to a YouGov poll for Sunday Times, only 11% of British support Theresa May's Brexit plan. 50% would choose to remain in the EU while 38% would choose a no-deal Brexit.

China’s GDP Advances 6.7% in Q2 2018

China's second-quarter GDP growth was seen advancing at a pace of 6.7% in line with estimates, official data showed last week. The second quarter GDP growth was, however, slightly below the 6.8% growth registered in the first quarter of 2018.

The slight slowdown in growth came as China's authorities have been clamping down on rising credit risk alongside uncertainty on the trade war escalations with the United States.

The headline GDP figures did not surprise the market. However, the third quarter GDP numbers are expected to show the full impact of the U.S. trade tariffs as well as the retaliatory measures taken by China.

Investors are already bracing for a slowdown in both China and the U.S. economies. Economists, however, expect that China could take the worst hit due to the large number of jobs also affected. The U.S. hiked tariffs on steel and aluminum imports across most of its trading partners including China.

As late as July, the trade wars continued to escalate. The U.S. was seen imposing more tariffs on China. It imposed a 25% border tax on goods worth $34 billion in imports to the U.S.

Meanwhile, China retaliated by imposing tariffs on an equal amount of goods imported from the U.S.

While there were some positive developments surrounding the trade tensions with both sides appearing to reach a compromise, the optimism quickly fell following the U.S. issuing renewed threats on more trade tariffs on Chinese goods.

With rising trade tensions between the world's first and second largest economies, the global trade is also expected to take a hit. Furthermore, the sentiment is also expected to affect the housing market in China.

Experts believe that while China remains committed to financial deleveraging, growth is also expected to slow in the coming months.

Data so far pointed to the fact that fixed asset investment during the first half of the year hit a record low of 6.0%. Industrial output for the month of June was also the slowest growth rate witnessed.

The slower economic conditions are expected to see China's authorities ease up the monetary policy. But this would require a balancing act as the authorities continue to deleverage the financial risks.

Last week, China's commerce ministry reported that it had filed a complaint to the World Trade Organization (WTO) regarding the newly issued threat of the U.S. imposing further tariffs on goods worth $200 billion.

While the tariffs have not yet been implemented, the U.S. authorities are expected to review the plans for two months with the hearing expected to be held in August.

U.S. officials maintain that the number of tariffs imposed was equivalent to China's exports to the U.S. Some of the sectors taking a hit also include sectors that are part of China’s initiative of Made in China 2025.

This initiative was started with an aim to position China as a global player in the industrial sector. The initiative was however met with criticism by officials in the U.S. which later saw the nation soften its message about the initiative.

The People's Bank of China was seen lowering the reserve requirements ratio nearly three times this year.

The GDP report comes following the previous week's inflation and PPI numbers. Data showed that producer prices rose at the fastest pace in six years. Producer prices advanced 4.7% in June on an annualized basis. This was higher than the previous month's increase of 4.1%.

Meanwhile, consumer prices also advanced at a pace of 1.9% which was in line with the estimates. Still, inflation is seen falling short of the 3% target that was set for this year.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1652; (P) 1.1696 (R1) 1.1766; More.....

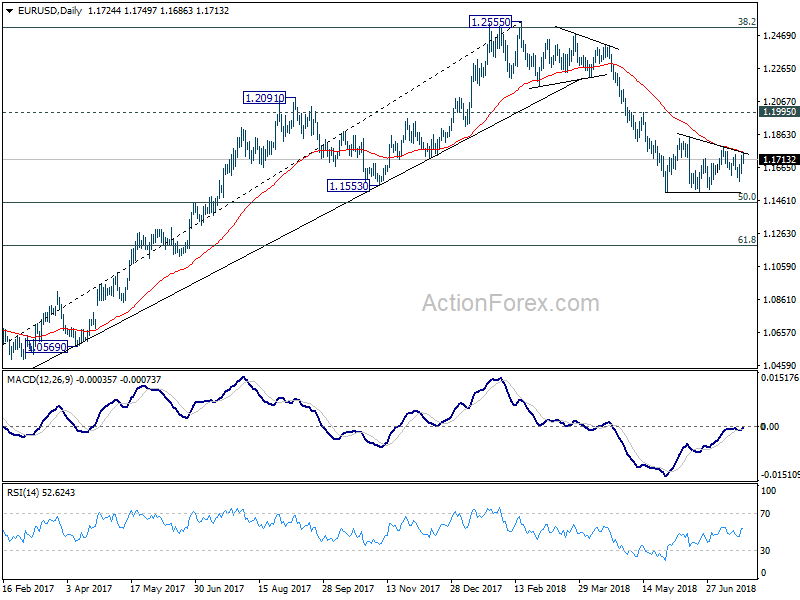

Outlook is EUR/USD is unchanged. Further rise cannot be ruled out as consolidation from 1.1509 extends. But upside should be limited by 1.1851 resistance to bring fall resumption eventually. On the downside , firm break of 1.1507 will resume larger down trend through 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3038; (P) 1.3089; (R1) 1.3183; More...

No change in GBP/USD's outlook. Recovery from 1.2956 could extend higher. But upside should be limited below 1.3362 resistance to bring fall resumption eventually. On the downside, break of 1.2956 will resume the decline from 1.4376 to 1.2874 fibonacci level

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3362 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

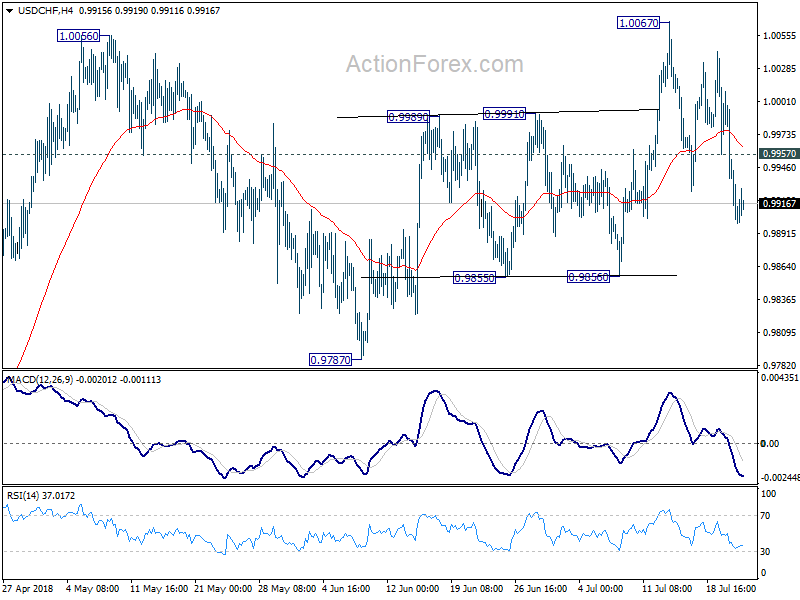

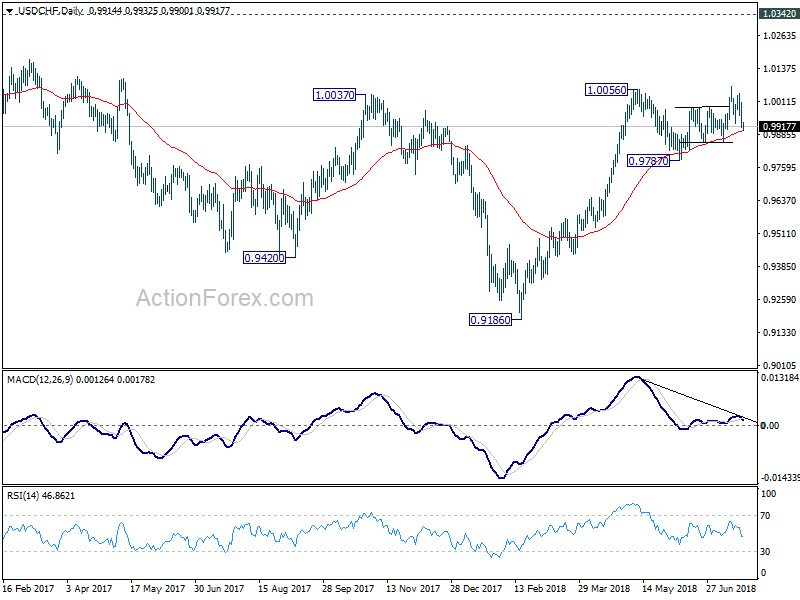

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9888; (P) 0.9950; (R1) 0.9987; More...

With 0.9957 minor resistance intact, intraday bias in USD/CHF remains on the downside. Current fall from 1.0067 is in progress and would target 0.9856 support. Break there will pave the way to key support level at 0.9787. On the upside, above 0.9957 minor resistance will turn bias back to the upside for retesting 1.0067.

In the bigger picture, as long as 0.9787 support holds, we're still favoring the bullish case. That is, rise fro 0.9787 is resuming the whole up trend from 0.9186 and should target 1.0342 key resistance on resumption. However, break of 0.9787 will indicate medium term reversal and turn outlook bearish.

Canadian Dollar Jumps after Sharp Retail Sales Reports

The Canadian dollar is almost unchanged in the Monday session, after strong gains on Friday. Currently, USD/CAD is trading at 1.3139, down 0.02% on the day. On the release front, it’s a quiet start to the week. Canadian Wholesale Sales jumped 1.2%, crushing the estimate of 0.6%. This marked the strongest gain since October. In the U.S, the sole indicator is Existing Home Sales, which is expected to rise to 5.46 million.

Canadian retail sales indicators for May sparkled on Friday, boosting the Canadian dollar 1.0 percent. Core Retail Sales jumped 1.4%, after failing to post a gain for three straight months. This easily beat the forecast of 0.6%. Retail Sales rebounded 2.0%, above the forecast of 1.0%. This follows a decline of 1.2% in April. Consumer inflation remained pegged at 0.1%, matching the forecast.

The U.S. dollar was broadly lower on Friday, after U.S President Trump made comments critical of Federal Reserve monetary policy. U.S presidents traditionally do not comment on moves by the Fed, but that did not prevent Trump from tweeting on Thursday that “tightening now hurts all that we have done”. On the weekend, Treasury Secretary Steven Mnuchin engaged in damage control, saying at the G-20 meeting that Trump was not interfering with the Fed policy of gradually raising rates. However, investors weren’t buying Mnuchin’s apologetics, and the U.S dollar continued to lose ground in Monday’s Asian session. There was more for investors to fret over, as Trump also attacked the EU and China for manipulating their currencies and keeping interest rates lower. This has raised concerns that the current global trade war could be followed by a currency war.