Sample Category Title

USD/JPY Bearish Momentum Fuels Wave A of Zigzag

The USD/JPY is showing strong bearish momentum, which makes it likely that price will reach the support trend line (blue). This support zone is a new bounce or break spot for the USD/JPY but eventually a bearish ABC (red) pattern is likely to occur. When price bounces, I will place the Fib on the price swing and keep an eye on the Fibonacci resistance levels for a bearish bounce.

The USD/JPY has been moving lower as part of a 5th wave pattern within wave A (red) after breaking multiple support trend lines (dotted green) and bouncing at the -27.2% Fib target (see 4 hr chart). Eventually price is expected to complete wave 5 (orange) of wave A (red) and start a potential wave B (red).

The USD/JPY has been moving lower as part of a 5th wave pattern within wave A (red) after breaking multiple support trend lines (dotted green) and bouncing at the -27.2% Fib target (see 4 hr chart). Eventually price is expected to complete wave 5 (orange) of wave A (red) and start a potential wave B (red).

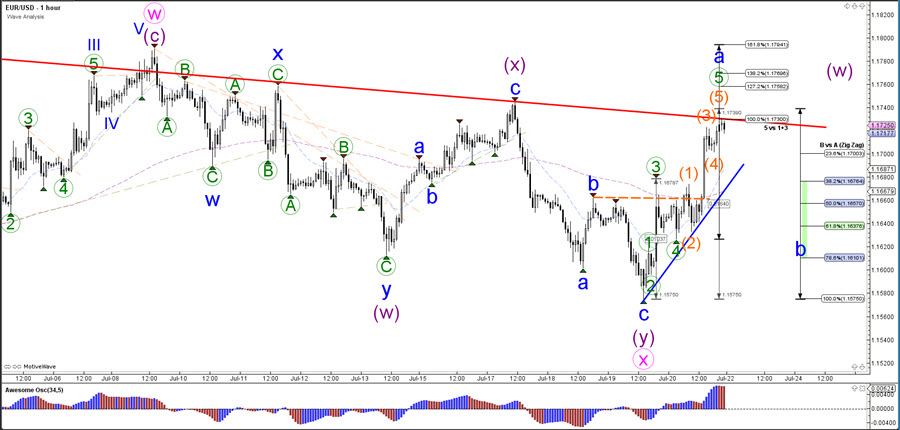

EUR/USD Impulsive Price Action Creates Bullish ABC Zigzag

The EUR/USD bounced at the bottom of the triangle pattern and made a strong and impulsive bullish reversal back to the top and resistance zone of the same corrective chart pattern.

The EUR/USD has reached a decision zone where a bullish breakout could see price move up towards the previous top (red box) whereas a bearish pullback could see price move towards the Fibonacci levels of wave B as mentioned on the 1 hour chart.

The EUR/USD seems to be completing 5 waves (orange) within a 5th wave (green) of wave A (blue). A bearish bounce could indicate a pullback to the Fibonacci levels of wave B (blue), which could act as potential support levels. A shallow and corrective pattern at this point could indicate a wave 4 correction rather than a wave B (with wave 3 finishing at the recent high). A break below the bottom of wave B (100% level) invalidates the bullish ABC potential.

EUR/USD Bounced Above 1.17

Market movers today

The markets will digest the G20 Finance minister meeting over the weekend. Not least comments on the currency front after Trump's tweets criticising the strengthening of the USD and repeating that China and the EU have been ‘manipulating their currencies. Trump seems increasingly keen on taking on a big battle with the EU and China and it seems more evident that the US-China trade war is here to stay for some time. Tariffs on autos could still hit the EU (not least Germany).

On the data front, we have euro consumer confidence and US existing home sales today. Especially, US home sales may attract some attention after weak housing starts and permits last week flagged a potential housing slowdown.

For the rest of the week, we have euro Flash PMI and German Ifo (Tuesday), the ECB rate meeting, US durable goods orders (Thursday) and Q2 GDP for the US (Friday).

Selected market news

The Bank of Japan (BoJ) is in focus this morning as the yen appreciated and yields on Japanese government bonds surged with the 10Y benchmark bond yield jumping 6bp on opening amid speculation that the BoJ might modify its yield control policy. The sell-off in the Japanese fixed income market triggered a fixed-rate operation announcement from the BoJ where the bank offers to buy an unlimited amount at a fixed price of 0.1%. The fixed rate announcement has helped stabilise the yen market for now, but price actions are likely to remain volatile ahead of the BoJ meeting next week on 27-28 July.

USD sold off substantially on Friday and EUR/USD bounced above 1.17 on comments from US President Donald Trump saying that he is ‘ready to go' with additional tariffs and that China, the EU and others have been manipulating their currencies. On Saturday, US Treasury Secretary Steven Mnuchin tried to ease currency war concerns in a press conference and reiterated that America's longstanding commitment to a strong USD remains intact and that the US is not trying to intervene in the dollar market. EUR/USD has continued higher and trades at 1.1735 this morning. The currency issue was not discussed at the G20 meeting this weekend, according several media sources, but the statement from the G20 meeting concluded that ‘risks to the world economy have increased' with main risks being ‘rising financial vulnerabilities, heightened trade and geopolitical tensions, global imbalances, inequality and structurally weak growth', according to the statement.

The US curve for 2Y10Y steepened on Friday after Trump also lashed out at the Fed, saying that higher rates were undermining America's competiveness. Even though few believe the Fed will bow to demands from Trump, the curve steepened as the long end sold off, with yields on 10Y US Treasuries rising about 4bp. The sell-off in the long end of the US yield curve might also be due to the reports that the BoJ is considering tweaking its yield control policy. If this story gains more attention, it might also weigh on European fixed income, given the sizeable Japanese flows into European bonds over the past two years.

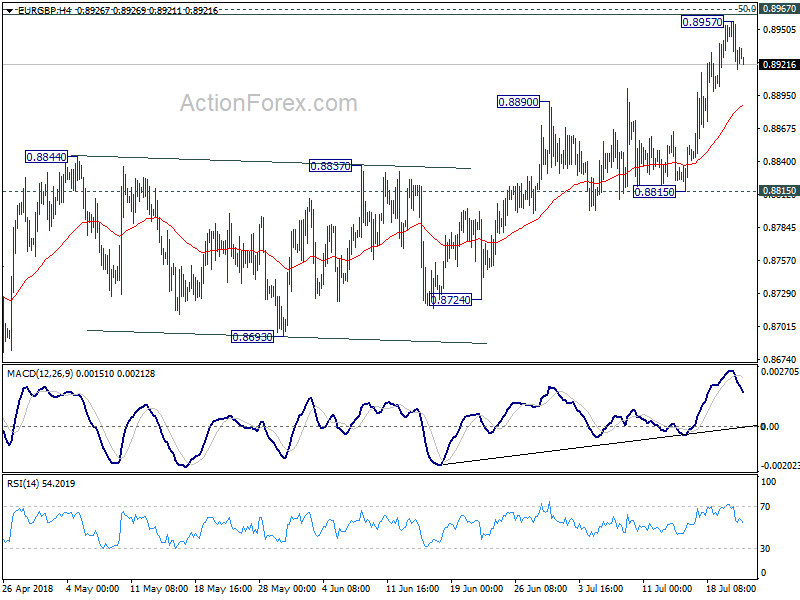

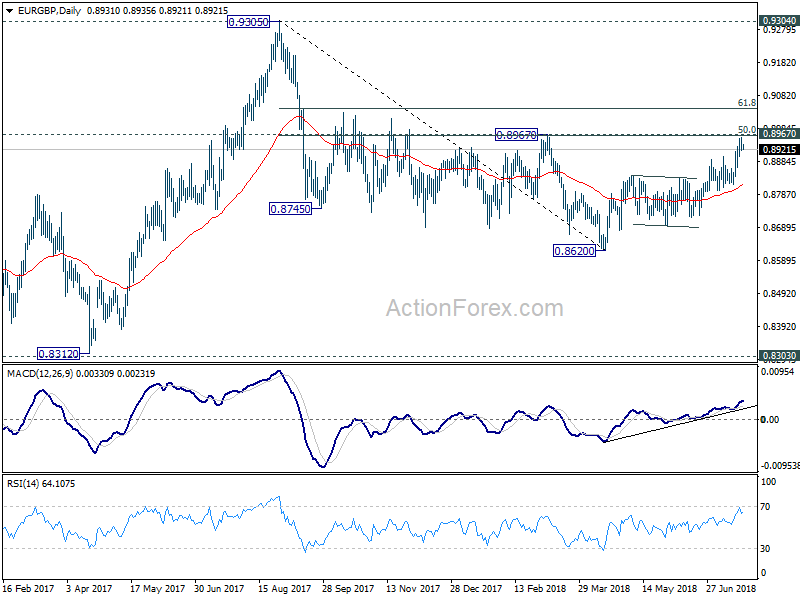

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8909; (P) 0.8934; (R1) 0.8953; More...

Intraday bias in EUR/GBP remains neutral for consolidation below 0.8957 temporary top. For now, as long as 0.8815 support holds, further rally is expected in the cross. Sustained break of 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) should confirm completion of whole decline from 0.9305. EUR/GBP should then target 61.8% retracement at 0.9043 next.

In the bigger picture, EUR/GBP is staying in long term range pattern from 0.9304 (2016 high). The corrective structure of the fall from 0.9305 to 0.8620 is raising the chance that rise from 0.8312 to 0.9305 is an impulsive move. But we're not too confident on it yet. In any case, we'd stay cautious on strong resistance from 0.9304/5 to limit upside in case of further rally. Meanwhile, if there is another medium term decline, strong support will likely be seen from 0.8303 to contain downside.

China Uses 1-Yr MLF For The 2nd Time In July

General Trend:

- Asian equity markets trade generally lower

- Shanghai Composite moves between gains and losses

- Shanghai Property index rises over 2%

- Nikkei component Fast Retailing declines on speculation the BoJ could make changes to its ETF purchases

- South Korean chipmaker Hynix declines over 4%, expected to report earnings on Thursday (July 26th)

- Japanese megabanks outperform on higher JGB yields

- Tokyo Steel declines over 6% after quarterly earnings report

- Posco Steel rises ahead of expected earnings report

- Rusal rises over 10%: The company has approached the Treasury with a plan that could remove it from the US sanctions list, according to US Treasury Sec Mnuchin

- China companies begin to launch trade suits versus the US: Wanshun Package [300057.CN] said to launch suit against the US anti-dumping and anti-subsidy duties

- Currencies in focus amid recent G20 meeting and comments from US President Trump

- No comments from China regarding the G20 meeting have been seen in the press

- Yen rises amid speculation the BoJ mulling policy changes to make easing measures sustainable; BoJ’s July meeting in focus (July 30-31st)

- BoJ launches fixed-rate JGB operation amid rise in JGB yields

- PBoC set the yuan stronger for the first time in 8 sessions

- PBoC conducts second medium-term lending facility this month, steps up size of the facility

- China 10-yr bond yield extends the gain seen on Friday’s session

- Japanese corporate earnings expected to pick up this week

- Hitachi Chemical expected to report results today

- US and European companies seen reporting earnings on Monday include Alphabet, Haliburton, Hasbro, Illinois Tool Works, Philips, Ryanair and Whirlpool.

- Japan prelim manufacturing PMI due for release on Tuesday

Headlines/Economic Data

Japan

- Nikkei 225 opened -1.0%

- TOPIX Electric Appliances index -0.9%, Real Estate -0.9%; Securities +1.1%

- Japanese automakers decline amid rise in the yen

- (JP) Japan Fin Min Aso: Discussed auto and steel tariffs with US Treasury Sec Mnuchin, not allowed to say what was discussed

- (JP) BoJ Gov Kuroda commented on Saturday at the G20: Said it was inappropriate to say anything predictive on the outcome of the BoJ’s July policy meeting.

- (JP) On Saturday a Japan MoF official said Japan told China at the G20 to explain about yuan (CNY) currency policy; need to be careful about Trump's FX remark and may need to explain if necessary to the US again about the purpose of the BoJ's easing – financial press

- (JP) Japan PM Abe is expected to formally declare his candidacy for third and final term as PM at event due to be held in the Yamaguchi Prefecture in Aug – Japanese Press

- (JP) BANK OF JAPAN (BOJ) HOLDS FIXED-RATE OPERATION ON 5-10-YR JGBS (1ST TIME SINCE FEB); Offers to buy unlimited amount of 10-yr JGBS at 0.11%; Received no takers in buying

- (JP) BoJ Official: Confirms today's special operation is in response to 'sharp' rise in JGB yields

- (JP) MUFG Bank analyst comments on possible ways BOJ could adjust policy: shortening duration for JGB purchases, making interest rate operations more flexible, expanding dollar operations to maximize yen strengthening risk

Korea

- Kospi opened flat

- Samsung Electronics, 005930.KR Consents to conclusive arbitration on leukemia victims’ dispute including compensation for the victim

- (KR) South Korea Fin Min Kim asked for exemption from 25% US tariff on autos on sidelines of G20 to Sec Mnuchin

- (KR) South Korea July 1-20 Exports Y/Y: +9.3% v -4.8% prior; Imports y/y: 21.6% v 13.0% prior - Customs

- (KR) President Trump has been asking for daily updates on the status of North Korea negotiations; said to be privately expressed frustrations to aides as pace of talks, even as he publicly tweets about how well talks are going - US press

China/Hong Kong

- Hang Seng opened +0.3%, Shanghai Composite -0.5%

- Hang Seng Property/Construction index +1.2%, Services +1%, Energy +0.9%, Financials +0.6%

- (CN) China PBoC publishes draft rules on wealth management products. Wealth management products should be managed based on their net value and banks must standardize the management of their fund pools to prevent shadow banking risk, according to an online statement. (Friday after the close)

- (CN) China PBOC sets yuan reference rate at 6.7593 v 6.7671 prior (1st stronger setting in 8 sessions)

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the second consecutive session

- (CN) China PBOC reports June property loans to individuals CNY23.8T, +18.6% y/y – Xinhua

- Rusal, {+14%], 486.HK (US) Treasury Sec Mnuchin: Rusal has approached the Treasury with a plan that could remove it from the US sanctions list

- (CN) China Commerce Ministry (MOFCOM): Launches anti-dumping probe related to stainless steel billet and hot-rolled stainless steel plate imports; relates to countries including EU, Japan, South Korea and Indonesia

- (CN) CHINA PBOC CONDUCTS CNY502B IN 1-YEAR MEDIUM-TERM LENDING FACILITY (MLF) V CNY188.5B PRIOR AT 3.30% V 3.30% PRIOR (2nd MLF operation in July)

Australia/New Zealand

- ASX 200 opened -0.2%

- ASX 200 REIT index -1.2%, Consumer Discretionary -1.1%, Telecom -1%, Utilities -1%, Financials -0.9%, Resources -0.7%

- Nufarm,[-8.5%], NUF.AU Guides FY18 underlying EBIT A$255-270M (prior +5% y/y, implied A$317.4M)

- Wesfarmers,[-1%], WES.AU Expect demerger of Coles to be completed in Nov 2018; to retain 15% of Coles and 50% of flybuys

- (AU) Australia 3-month bank bill fixed 1.9850% v 1.9910% prior (2nd straight fix below 2%)

- (NZ) New Zealand Acting PM Peters: Inflation is not sole issue facing economy

North America

- (US) US Treasury Sec Mnuchin: Hope to get a NAFTA agreement negotiated in near future; See light at the end of the tunnel on trade disputes

- (US) Companies including Amazon, GM, Toyota, and Alcoa are making efforts to counter Trump Administration's tariff plans - press

- SYNT To be acquired by Atos for $41.00/shr, $3.57B ,including debt; Guides Q2 $0.49 v $0.44e; Rev $249.7M v $233Me

- TSLA Said to have asked suppliers to return cash in order to help the company turn a profit. seeking price cuts from suppliers - US financial press

Europe

- (G20) France Fin Min Le Maire: a trade war has already started; if the US imposes more tariffs, the EU will have no choice but to retaliate - comments from G20

- (G20) G20 Communique: Short and medium term risks to growth have increased including heightened trade the geopolitical tensions; Affirms exchange rate commitments made in March statement to avoid competitive devaluation and refrain from targeting exchange rates for competitive advantage

Levels as of 01:30ET

- Hang Seng +0.2%; Shanghai Composite +0.7%; Kospi -0.6%; Nikkei225 -1.4%; ASX 200 -0.9%

- Equity Futures: S&P500 -0.1%; Nasdaq100 -0.3%, Dax -0.1%; FTSE100 -0.2%

- EUR 1.1724-1.1750; JPY 110.75-111.51; AUD 0.7417-0.7438;NZD 0.6794-0.6825

- Aug Gold +0.1% at $1,232/oz; Sept Crude Oil -0.2% at $68.16/brl; Sept Copper +0.2% at $2.76/lb

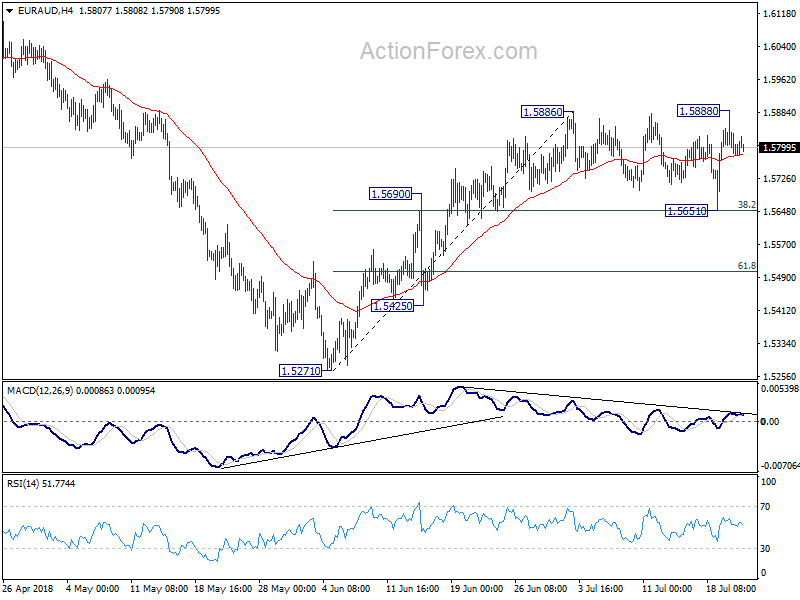

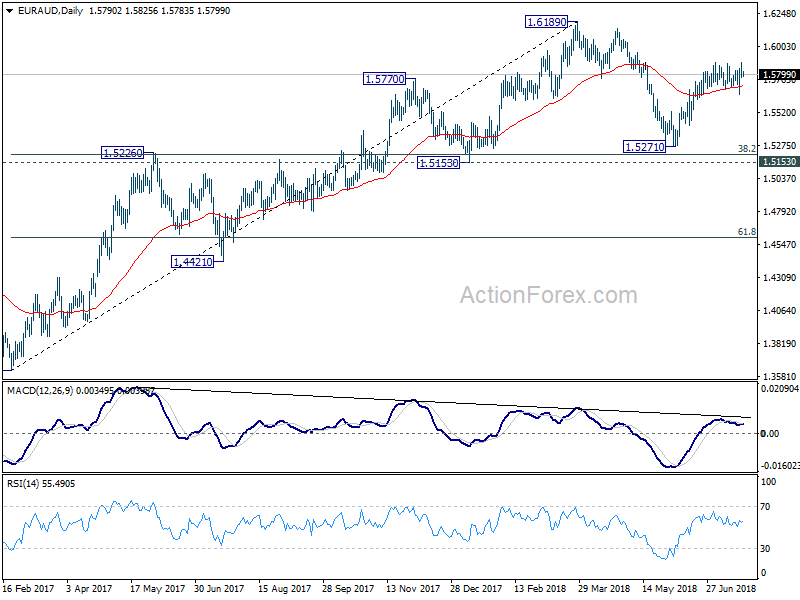

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5757; (P) 1.5825; (R1) 1.5868; More....

Intraday bias in EUR/AUD remains neutral at this point. Rise from 1.5271 is likely still in progress. ON the upside, break of 1.5888 resistance will extend the rally towards 1.6139/89 resistance zone. However, break of 1.5651 cluster support (38.2% retracement of 1.5271 to 1.5886 at 1.5651) will indicate near term reversal and turn bias back to the downside for 1.5271.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5271 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is still in progress. Break of 1.6189 will target 1.6587 key resistance (2015 high).

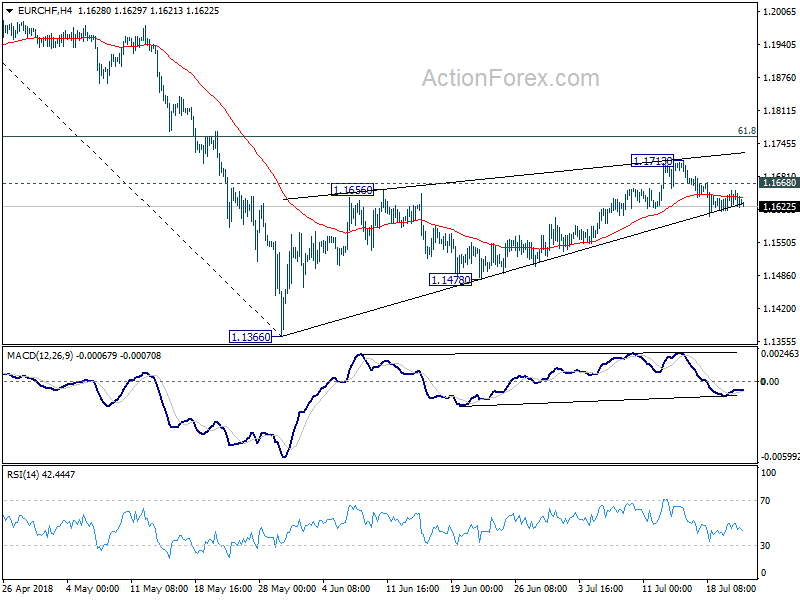

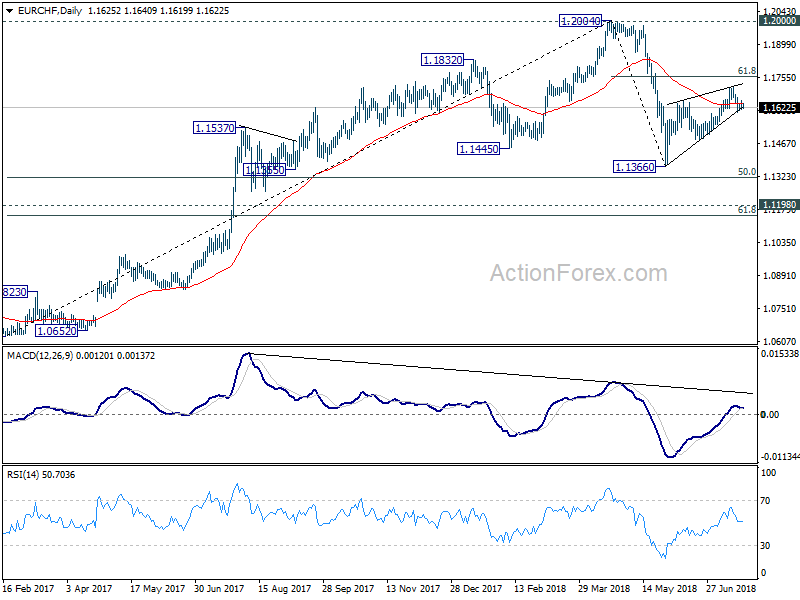

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1619; (P) 1.1637; (R1) 1.1654; More...

Intraday bias in EUR/CHF remains mildly on the downside at this point. The corrective rebound from 1.1366 could have completed with three waves up to 1.1713 already. Deeper fall should be seen to 1.1478 support first. Break there should resume the whole decline from 1.2004 through 1.1366 low. On the upside, above 1.1668 will bring another rise. But in the case, we'd continue to expect strong resistance from 61.8% retracement of 1.2004 to 1.1366 at 1.1760 to bring near term reversal.

In the bigger picture, 1.2004 is seen as a medium term top with bearish divergence condition in daily and weekly MACD. 1.2000 is also an important resistance level. Hence, the corrective pattern from 1.2004 is expected to extend for a while before completion. We're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

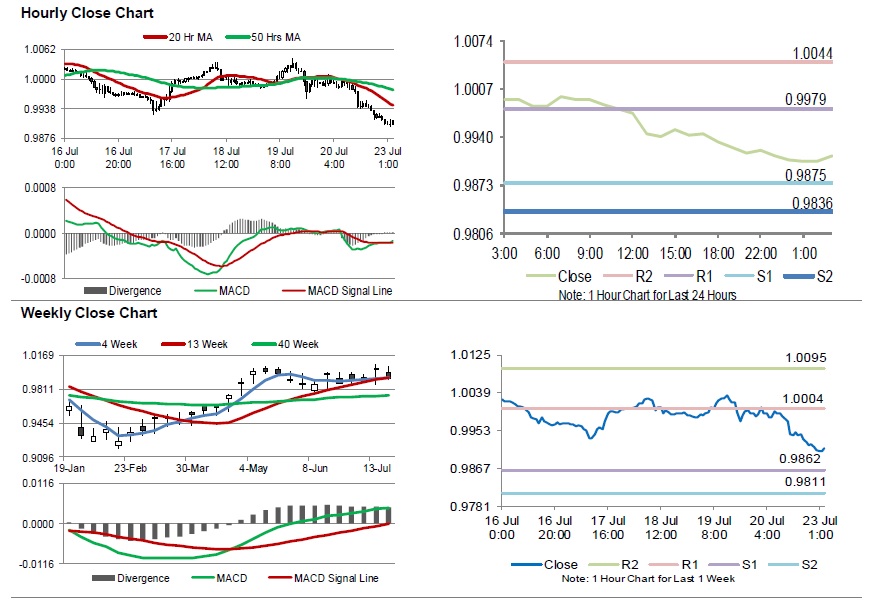

Swiss Franc Trading On A Stronger Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.74% against the CHF and closed at 0.9919 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9914, with the USD trading 0.05% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9875, and a fall through could take it to the next support level of 0.9836. The pair is expected to find its first resistance at 0.9979, and a rise through could take it to the next resistance level of 1.0044.

Trading trend in Swiss Franc will be determined by the release of M3 money supply for June, scheduled to release in a while.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

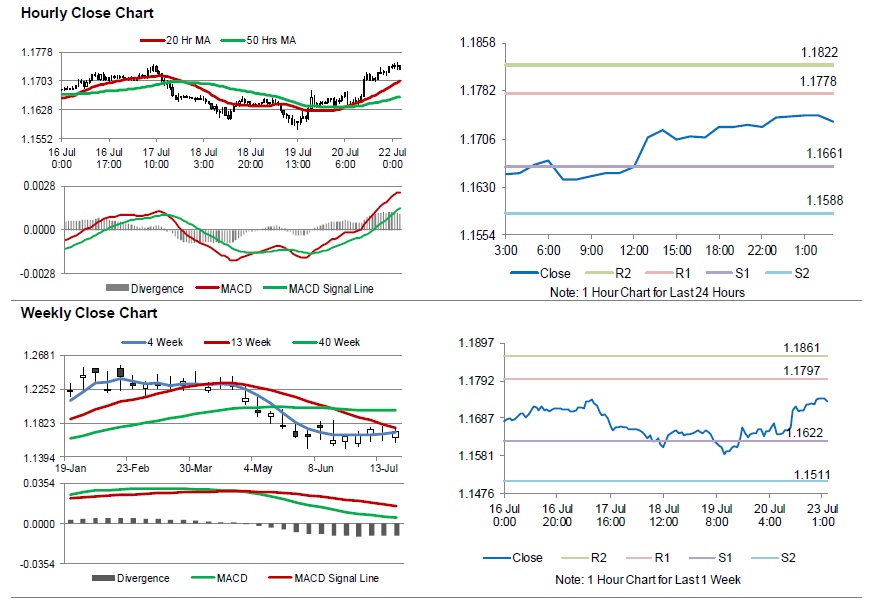

Euro Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the EUR rose 0.70% against the USD and closed at 1.1728 on Friday.

On the data front, Euro-zone’s current account surplus narrowed to €22.4 billion in May, reaching its lowest level since March 2015 and compared to a revised surplus of €29.6 billion in the prior month.

Meanwhile, in Germany, the producer price index (PPI) climbed 3.0% on a yearly basis in June, in line with market expectations and at the fastest pace in nine months. In the previous month, the index had recorded an advance of 2.7% .

In the Asian session, at GMT0300, the pair is trading at 1.1733, with the EUR trading slightly higher against the USD from Friday’s close.

The pair is expected to find support at 1.1661, and a fall through could take it to the next support level of 1.1588. The pair is expected to find its first resistance at 1.1778, and a rise through could take it to the next resistance level of 1.1822.

Moving ahead, investors would await Euro-zone’s consumer confidence index for July, set to release later in the day. Also, the US existing home sales and the Chicago Fed national activity index, both for June, will keep investors on their toes.

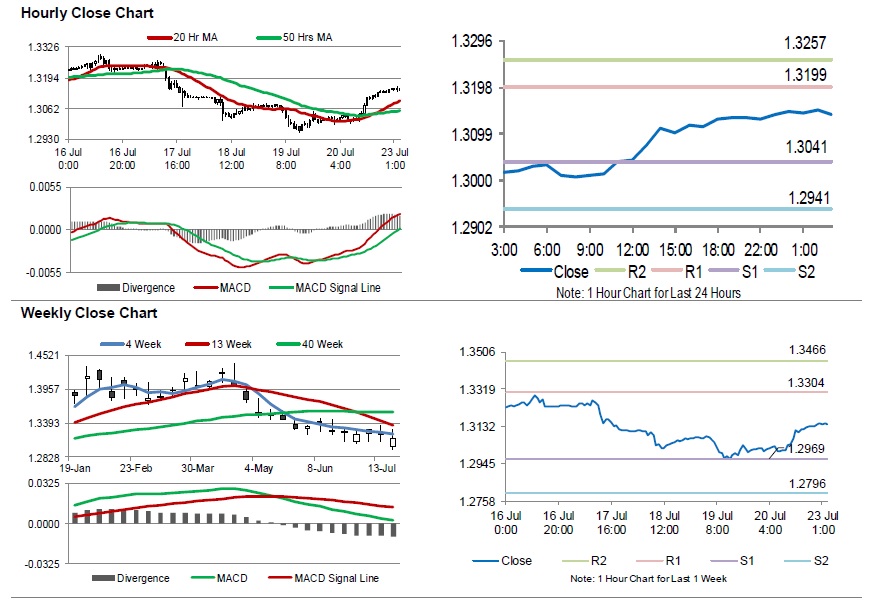

Sterling Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.91% against the USD and closed at 1.3135 on Friday.

In the economic news, UK’s public sector net borrowing fell to £4.5 billion in June, following a revised deficit of £3.9 billion in the prior month. Market expectation was for public sector net borrowing to show a deficit of £3.6 billion.

In the Asian session, at GMT0300, the pair is trading at 1.3142, with the GBP trading 0.05% higher against the USD from Friday’s close.

The pair is expected to find support at 1.3041, and a fall through could take it to the next support level of 1.2941. The pair is expected to find its first resistance at 1.3199, and a rise through could take it to the next resistance level of 1.3257.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.