Sample Category Title

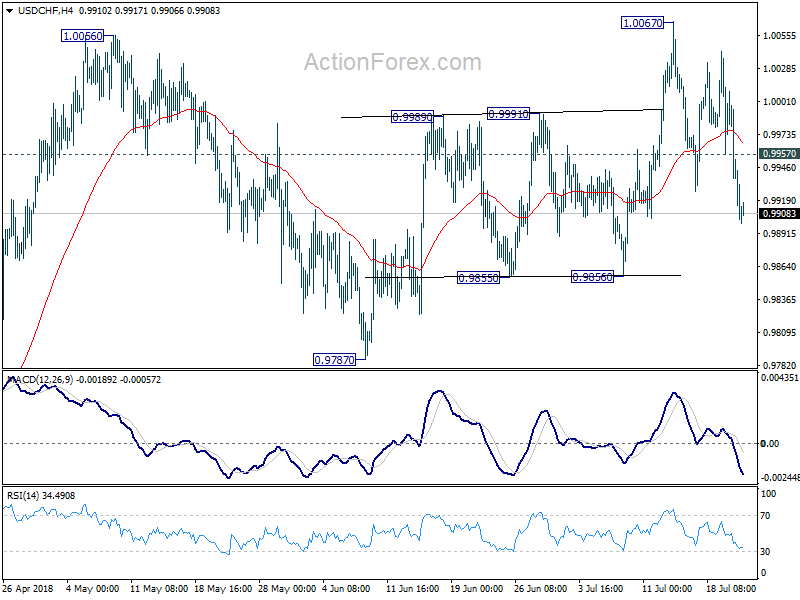

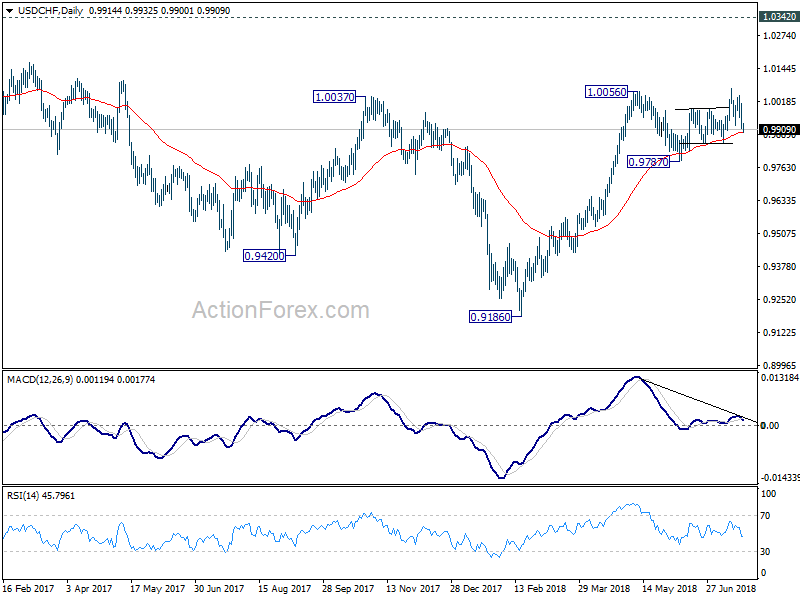

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9888; (P) 0.9950; (R1) 0.9987; More...

USD/CHF's fall fro 1.0067 is still in progress and intraday bias stays mildly on the downside for 0.9856 support first. Break there will pave the way to key support level at 0.9787. On the upside, above 0.9957 minor resistance will turn bias back to the upside for retesting 1.0067.

In the bigger picture, as long as 0.9787 support holds, we're still favoring the bullish case. That is, rise fro 0.9787 is resuming the whole up trend from 0.9186 and should target 1.0342 key resistance on resumption. However, break of 0.9787 will indicate medium term reversal and turn outlook bearish.

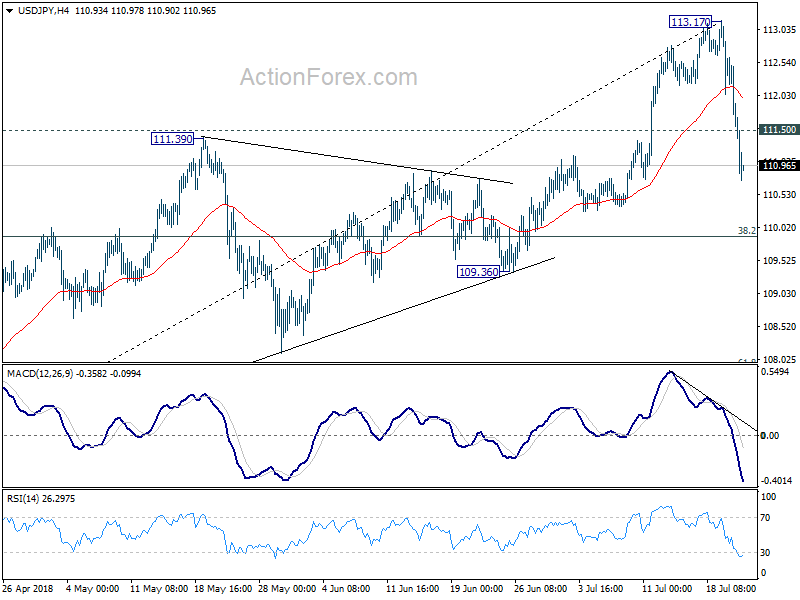

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.02; (P) 111.83; (R1) 112.26; More...

USD/JPY's fall from 113.17 extends today and hits as low as 110.74 so far. Intraday bias stays on the downside for 55 day EMA (now at 110.45) and below. However, such decline is seen as correcting whole rally from 104.62. Hence, we'd expect strong support from 38.2% retracement of 104.62 to 113.17 at 109..90 to contain downside and bring rebound. On the upside, above 111.50 minor resistance will turn intraday bias neutral first. But break of 113.17 is needed to confirm up trend resumption. Otherwise, more condition would be seen with risk of another fall.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds.

Sharp Rally in 10 Year JGB Yield Takes Yen Higher, Dollar Stays Weak

Yen trade broadly higher today as boosted by the steep rally in 10 year JGB yield. That also sends Nikkei sharply lower as it's down -333 pts or -1.47% at the time of writing. Other Asian markets are steady thought with China Shanghai SSE trading up 0.37% and Hong Kong HSI up 0.15%. Swiss Franc follow as the second strongest one. Dollar, on the other hand, is extending Friday's sharp selloff and is trading broadly lower today. It's followed by Australian Dollar and Canadian Dollar as the next weakest.

Yen lifted as 10 year JGB yield jumped on BoJ talks

10 year yield in Japan jumped as much as six basis points to 0.090%, hitting the highest level since February. It's also the largest daily rally in nearly two years. The sharp movement prompted an unscheduled operation by BoJ to buy 10 year JGB at a yield of 0.11%. That's the same level as at last intervention but no bid was tendered.

The movements were based on reports that BoJ is discussing changes to its monetary policy, including the interest-rate targets and stocks-buying techniques. The objective is to make the stimulus program more sustainable. Currently, under the Yield Curve Control framework, BoJ is buying JGBs to keep 10 year yield at around 0%. And the central bank could allow 10 year yield to rise higher to 0.10% to give more flexibility to monetary policy.

But when asked about the reports at G20 meeting in Argentina, BoJ Government Haruhiko Kuroda said "I know absolutely nothing about the basis for those reports." And so far, reports suggested that BoJ policymakers are only in preliminary discussion on the way to tweak the policy. And it's highly unlikely for any significant decision at the July 31 meeting.

G20 pledged to strengthen contribution of trade to the economies

G20 finance ministers and central bankers stepped up their language regarding trade tension in the communique after the meeting in Argentina. The communique noted that "risks over the short and medium term have increased". And the risks include "financial vulnerabilities, heightened trade and geopolitical tensions, global imbalances, inequality and structurally weak growth, particularly in some advanced economies." The group pledged to "continue to monitor risks, take action to mitigate them and respond if they materialise."

The communique also noted that "international trade and investment are important engines of growth, productivity, innovation, job creation and development." The group reaffirmed the conclusions on trade at the Hamburg Summit and "recognise the need to step up dialogue and actions to mitigate risks and enhance confidence". And "we are working to strengthen the contribution of trade to our economies."

Japan Suga: Returning to TPP is in the best interest of Japan and US

Japan Chief Cabinet Secretary Yoshihide Suga insisted over the weekend that returning to the Trans-Pacific Partnership trade agreement is in the best interests of both Japan and the US. The comments came in before meeting of Economy Minister Toshimitsu Motegi and US Trade Representative Robert Lighthizer for bilateral trade later this month. And that's a clear indication that Japan is not interested in bilateral trade deal that the US is keen on pursuing. Suga added that "Japan is not going to do anything with any country that harms the national interest." And, "with FTA negotiations too, we'll handle them in that way."

Finance Minister Taro Aso also said that "inward-looking policies would benefit no country." And added that "excessive current account imbalances should be resolved through multilateral, not bilateral, framework. " Also, "the matter should be dealt with through macroeconomic policy and a structural reform by rebalancing savings and investments, instead of imposing tariffs."

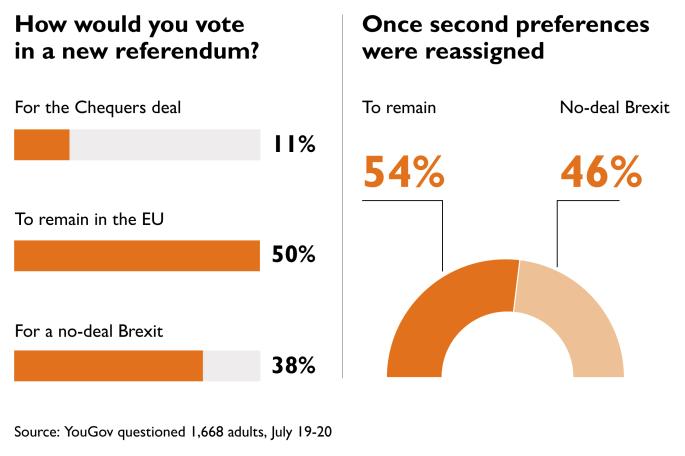

Poll shows May's Brexit plan overwhelmingly rejected

A latest poll showed that UK Prime Minister Theresa May's current Brexit plan is rejected by the British, in rather overwhelming way. The poll was conducted by YouGov for the Sunday Times between July 19-20. It showed that in case of a new referendum, only 11% would support the so-called "the Chequers deal". 38% would vote for a "no-deal Brexit". And 50% would vote for remaining in the EU. Giving a second preference, 54% would vote for "remain" while 46% will vote for a "no-deal Brexit".

May tried to defend the plan and said "this is a principled and practical Brexit that is in the mutual interests of the UK and EU, but it will require pragmatism from both sides." But as the Sunday Times commented, "the problem for May is that the Chequers plan is viewed as too favourable to Britain by the EU, too unfavourable to Britain by the Brexiteers and unworkable by both."

ECB meeting, US GDP and Australia CPI are highlights of the week

ECB meeting will be a highlight of the week but it's unlikely to bring something new. It's planning to taper the asset purchase program after September, and stop it after December. Interest rates will stay at present level at least through Summer 2019. The question is on whether ECB President Mario Draghi would clarify what exactly he means by Summer. But it's unlikely as the words are seen as a balance between precision and flexibility. Instead, Euro could have bigger reactions to PMIs and German Ifo.

Elsewhere, European Commission President Jean-Claude Juncker's visit to the US for trade will catch some headlines too. Let's see if he can achieve any results to avert auto tariffs. There are also some important data to watch including US GDP, French GDP, and Australia CPI

Here are some highlights for the week ahead:

- Monday: Canada wholesale sales; Eurozone consumer confidence; US existing home sales

- Tuesday: Japan PMI manufacturing; Eurozone PMIs; US house price index, PMIs

- Wednesday: New Zealand trade balance; Australia CPI; German Ifo business confidence ; Eurozone M3; UK CBI reported sales, BBA mortgage approval; US new home sales

- Thursday: Australia import price; German Gfk consumer climate; ECB rate decision; US durable goods orders, jobless claims, trade balance, wholesale inventories

- Friday: Japan Tokyo CPI; Australia PPI; French GDP; German import price; US GDP

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.02; (P) 111.83; (R1) 112.26; More...

USD/JPY's fall from 113.17 extends today and hits as low as 110.74 so far. Intraday bias stays on the downside for 55 day EMA (now at 110.45) and below. However, such decline is seen as correcting whole rally from 104.62. Hence, we'd expect strong support from 38.2% retracement of 104.62 to 113.17 at 109..90 to contain downside and bring rebound. On the upside, above 111.50 minor resistance will turn intraday bias neutral first. But break of 113.17 is needed to confirm up trend resumption. Otherwise, more condition would be seen with risk of another fall.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | CAD | Wholesale Trade Sales M/M May | 0.60% | 0.10% | ||

| 12:30 | USD | Chicago Fed Nat Activity Index Jun | -0.15 | |||

| 14:00 | EUR | Eurozone Consumer Confidence Jul A | -0.75 | -0.5 | ||

| 14:00 | USD | Existing Home Sales Jun | 5.47M | 5.43M | ||

| 14:00 | USD | Existing Home Sales M/M Jun | -0.20% | -0.40% |

Yen lifted as 10 year JGB yield jumped on BoJ talks

Yen trade broadly higher today as boosted by the steep rally in 10 year JGB yield. 10 year yield in Japan jumped as much as six basis points to 0.090%, hitting the highest level since February. It's also the largest daily rally in nearly two years. The sharp movement prompted an unscheduled operation by BoJ to buy 10 year JGB at a yield of 0.11%. That's the same level as at last intervention but no bid was tendered.

The movements were based on reports that BoJ is discussing changes to its monetary policy, including the interest-rate targets and stocks-buying techniques. The objective is to make the stimulus program more sustainable. Currently, under the Yield Curve Control framework, BoJ is buying JGBs to keep 10 year yield at around 0%. And the central bank could allow 10 year yield to rise higher to 0.10% to give more flexibility to monetary policy.

But when asked about the reports at G20 meeting in Argentina, BoJ Government Haruhiko Kuroda said "I know absolutely nothing about the basis for those reports." And so far, reports suggested that BoJ policymakers are only in preliminary discussion on the way to tweak the policy. And it's highly unlikely for any significant decision at the July 31 meeting.

Market Morning Briefing: Euro Has Moved Past Resistance Near 1.1715

STOCKS

Dow (25058.12, -0.025%) is holding below immediate resistance near 25250 and while that holds, we could see some correction in the near term towards 24750.

Dax (12561.42, -0.98%) also saw a sharp fall from levels near 12800 instead of rising further towards 13000. Levels near 12400 could produce a small bounce in the next few sessions, again taking the index towards 12800-13000. For now, the correction could continue for another 1-2 sessions.

Nikkei (22403.45, -1.30%) was unable to rise above 23000 last week and instead has come off in line with the movement in the other equity indices. While immediate support near 22400 holds, the index may soon bounce back to higher levels in the near term. Trade within 22400-23000 is possible in the coming sessions.

Shanghai (2836.02, +0.24%) has risen from 2750 and while the rise sustains, the index needs to break above 2850 to turn bullish for the near to medium term. A break above 2850, would open up chances of a rise towards 2900-2950 in the medium term.

Nifty (11010.20, +0.48%) was stuck in the 11100-10900 region last week without any major movement. A break on either side this week would indicate on further direction on the Nifty. A rise towards 11150-11200 looks more likely while above 10900-10950 levels.

COMMODITIES

Nymex WTI (68.10, -0.23%) has some more room in the downside towards 65 and if the price falls, it could drag Brent (72.85, -0.30%) also to lower levels in the next few sessions. Note that 70-71 is an important support region for Brent and is likely to hold in the medium term.

Gold (1231.90, +0.06%) has bounced sharply from 1210 but could face some resistance near 1240. If rejection is seen from 1240, Gold could continue to looks bearish for the near term with a possibility of testing 1200 in the medium term. A rise above 1240, if seen in the current rally would be bullish for the longer term.

Copper (2.7465, -0.34%) is stuck in the 2.68-2.80 region and a break on either side is needed to bring in the next leg of movement. A break above 2.80 would open up chances of testing 2.95-3.00 again in the coming sessions; else some range trade in the 2.80-2.68 region is possible.

FOREX

Euro (1.1739): Euro has moved past resistance near 1.1715 and is now trading near higher resistance on 3 day candles near 1.174-1.175. A breach of this level could take it up towards 1.185 (previous high). However if 1.175 holds, Euro might again dip towards 1.16 to continue its ranging. A break out from the range in either direction seems likely in the coming 1-2 weeks. Currently, the preference is shifting towards the upside.

Dollar Index (94.296): Dollar Index is breaking support on daily and 3 day candles near 94.5. It has lower support near 94 on daily line chart which it could test in the next 1-2 sessions. A test of 94 by Dollar Index could correspond with a test of 1.18 by Euro.

Dollar Yen (110.94): Against our expectation, Dollar Yen has seen a sudden downturn and is close to crucial support near 111 on daily candles. The strength in Yen might have been a result of the rise in Japanese bond yields (see Interest Rates below). If Dollar Yen breaks below 111 decisively, then 113 might be a medium term top and it might become bearish here onwards.

Euro Yen (130.24): Euro Yen has dipped along with Dollar Yen and could test support on daily candles near 129.50 in the next 1-2 sessions. Below 129.50, there is strong horizontal support on weekly line chart near 127.

Pound (1.3142): After testing channel support on daily candles near 1.295 last week, the Pound is gaining strength and could move towards 1.32 in the next 1-2 sessions. The broader trend currently looks bearish. A decisive break below the 89 weeks MA on weekly line chart would confirm bearishness in the medium term.

Dollar Rupee (68.70): Dollar Rupee opened at 68.7050 today (as was forecasted in Friday's evening comments). There is support near current levels which could push it back up towards levels near 69. However current preference is for a break of this support.

INTEREST RATES

Japanese yields have shot up with the 10 year yield seeing a high near 0.09%. This has happened due to speculation that the Bank of Japan might be contemplating to modify its interest rate targets. Till now the BoJ had been ensuring that the 10 year bond yield doesn't breach 0.10%-0.11%. On the short term chart, the Japanese 10 Year yield (0.075%) has breached resistance trendline near 0.05% and might stay above this level in the days to come.

US yields also rose on Friday inspite of Trump again expressing his disapproval towards the Fed's tightening. The rise in US Yields and Japanese yields might be linked - investors might have moved out of US bonds and towards Japanese bonds, leading to a rise in yield for US bonds.

US 10 year yield (2.89%), 30 Year (3.023%), 5 Year (2.763%), 2 Year (2.5952%):

As mentioned previously, a breach above 2.9% for the US 10 Year yield could negate the downside possibility of a test of 2.70%-2.65% in the next 1-2 months. Recent US economic data releases have also continued reflecting a strong US economy, which would be helpful for a rise in yields. The talk around the US-China trade war could still be the primary market mover for yields in the weeks to come. Any increase in the rhetoric would be supportive for a fall in yields.

Poll shows May’s Brexit plan overwhelmingly rejected

A latest poll showed that UK Prime Minister Theresa May's current Brexit plan is rejected by the British, in rather overwhelming way. The poll was conducted by YouGov for the Sunday Times between July 19-20. It showed that in case of a new referendum, only 11% would support the so-called "the Chequers deal". 38% would vote for a "no-deal Brexit". And 50% would vote for remaining in the EU. Giving a second preference, 54% would vote for "remain" while 46% will vote for a "no-deal Brexit".

May tried to defend the plan and said "this is a principled and practical Brexit that is in the mutual interests of the UK and EU, but it will require pragmatism from both sides." But as the Sunday Times commented, "the problem for May is that the Chequers plan is viewed as too favourable to Britain by the EU, too unfavourable to Britain by the Brexiteers and unworkable by both."

EUR/USD In Slow And Steady Uptrend

Key Highlights

- The Euro found a strong support near 1.1580 and recovered against the US Dollar.

- There is a key bullish trend line in place with support at 1.1600 on the 4-hours chart of EUR/USD.

- The pair is placed nicely above the 1.1650 support and the 100 SMA (red, 4-hour).

- The US Existing Home Sales for June 2018 will be released today, which is forecasted to increase 1.5% (MoM).

EURUSD Technical Analysis

The Euro dipped this past week, but the 1.1580 support area acted as a strong barrier against the US Dollar. The EUR/USD pair recovered and moved back above the 1.1650 resistance.

Looking at the 4-hours chart, the pair found a key bullish trend line with current support at 1.1600. A low was formed at 1.1575 and the pair started an upward move. It climbed above the 50% Fib retracement level of the last decline from the 1.1744 high to 1.1575 low.

More importantly, there was as close above the 1.1650 resistance, the 100 simple moving average (red, 4-hours) and the 200 SMA (green, 4-hours). Later, the pair attempted a close above a connecting bearish trend line with resistance at 1.1705.

It seems like the pair is placed in a nice uptrend above the 1.1650 support. Should there be a break above the last high at 1.1744, there could be more gains towards the 1.236 Fib extension level of the last decline from the 1.1744 high to 1.1575 low at 1.1784.

On the downside, supports are seen at 1.1670, 1.1650 and the 100 SMA. Below 1.1650, the pair may perhaps test the bullish trend line with support at 1.1600.

Economic Releases to Watch Today

- US Existing Home Sales for June 2018 (MoM) – Forecast +1.5%, versus -0.4% previous.

- Canadian Wholesale Sales for May 2018 (MoM) – Forecast +0.6%, versus +0.1% previous.

Forex Forecast And Cryptocurrencies Forecast

First, a review of last week’s forecast:

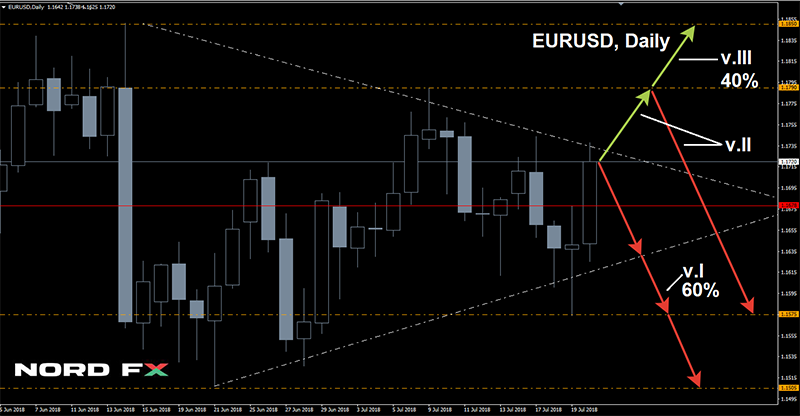

EUR/USD. Recall that in the opinion of 80% of experts who were supported by graphical analysis on D 1, the pair was supposed to continue its descent to the horizon 1.1500. An alternative point of view was presented by only 20% of analysts who expected that it could once again test the level of 1.1790. However, adjustments to all these forecasts have been traditionally made by the summer and vacation season. As a result, the pair, as if tired of lying on the beach, could only lazily rise to the level of 1.1745, and then descend to the level of 1.1574. As for the end of the week, after Donald Trump criticized the Fed policy and the strong dollar, the euro won back the losses, and the pair returned to the upper half of the summer side channel, having stopped at 1.1720;

The negative mood of the market in relation to the pair GBP/USD was supported by the majority of analysts (70%), who expected the continuation of its fall first to the level of 1.3100, and then another 50 points lower. This forecast turned out to be quite accurate: the pair reached the horizon of 1.3100 by the middle of the week, then it groped for the bottom in the support zone for the two-month downtrend channel - 1.2955, fought back and completed the five-day period near its central line at 1.3131;

USD/JPY. Here, too, most experts (70%) expected the dollar to strengthen and the pair to seek to reach the last year's highs in zone 113.50. In the first half of the week, it was really soaring 80 points. However, the correction in the US stock market caused a decline in its quotes, the pair turned around and fell to the level of 111.40by the end of the week session;

Cryptocurrencies. Two weeks ago, we listed some of the reasons that could lead to the bitcoin growth, and then assumed that the BTC/USD would hold in the range of $ 5,790-6830 for some time. But only if nothing extraordinary happens.

As it always happens with crypto-currencies, it happened - the major financial players announced their desire to enter this market. One of them was the investment giant BlackRock, the asset manager of 6.3 trillion dollars. Another locomotive was the company MasterCard, which registered a patent in the field of operations with bitcoin. All this strongly inspired the market, as a result of which the rate of this digital currency increased by about $1350 (21%), reaching $7.585.

Following the bitcoin, the main altcoins also moved up, but their growth, unlike the leader's, was short-lived, and by the end of the week the bears managed to restore their positions, if not completely, at least partially. For example, the pair XRP/USD, starting at $0.43, quickly rose to $0.52, but then as quickly fell to $0.45 per coin.

As for the forecast for the coming week, summarizing the opinions of a number of analysts, as well as forecasts made on the basis of a variety of methods of technical and graphical analysis, we can say the following:

EUR/USD. The ECB's interest rate decision and the press conference of its head Mario Draghi are expected on Thursday July 26. But neither of these are expected to cause any special surprise to the market. More serious concern for the euro is caused by the visit of the European Commission officials to Washington, where they should discuss sanctions and counter-sanctions in the trade war between the EU and the United States with President Trump. The aggravation of the situation may again upset the pair, which is why 60% of analysts are waiting for its return to the level of 1.1575, and in case of its breakdown - to the June-July low at 1.1500.

15% of oscillators that signal the pair is overbought and the graphical analysis agree. With this scenario. However, on H4, graphical analysis indicates that before it falls, the pair can still rise to resistance 1.1790.The next resistance level is 1.1850

Macroeconomic data from the British Isles, as well as the situation with Brexit, do not inspire optimism, which also affects the analysts' forecasts. 65% of them, supported by graphical analysis on D1, are waiting for the continuation of the downtrend for the pair GBP/USD. Oscillators on D1 are also Painted in red, indicating it is overbought. Support levels are 1.2955 and 1.2830.

The remaining 35% of experts, together with the graphical analysis on H4, expect a growth of the pair, although small. The pound can also be supported by the UK GDP data, which will be released on Friday 27 July. It is expected that the GDP will grow by 2% compared to the previous quarter. Target levels for the pair are1.3190, 1.3245 and 1.3270;

USD/JPY. Here a slight advantage is on the side of the bulls, if we talk of experts - they are 50%.45% side with the bears and 5% abstained. {0Graphical analysis on H4 and 80% of oscillators on D1 are for the growth of the pair as well. The nearest targets are 112.20 and 112.65, then 113.15 and 114.00.

An alternative point of view, apart from 45% of experts, is supported by graphical analysis on D 1 and most oscillators on H4. The support levels are 110.75, 110.30 and 109.75;

Cryptocurrencies. If last week the crypto market capitalization was close to the 2018 lows and amounted to about $240 billion, by Wednesday July 18 it was close to $300 billion. But more importantly, the share of buyers at that moment increased to 27%. The last time this happened was on April 8 this year.

However, the increase in volumes occurred too sharply - the first jump lasted only 20 minutes. And even though the bears suffered very significant losses - many short positions closed on stop-losses with significant losses, there is still no confidence in the change in the main trend for an increasing one for the BTC/USD.

By the end of Friday July 20, the pair continues to hold within a strong support/resistance zone of 7,270-7,730, which can be called Pivot Point of spring-summer 2018. It is possible that, despite being overbought, it will still attempt to break through its upper limit. Although, experts believe its decline to support 6,830 to be more likely.

Japan Suga: Returning to TPP is in the best interest of Japan and US

Japan Chief Cabinet Secretary Yoshihide Suga insisted over the weekend that returning to the Trans-Pacific Partnership trade agreement is in the best interests of both Japan and the US. The comments came in before meeting of Economy Minister Toshimitsu Motegi and US Trade Representative Robert Lighthizer for bilateral trade later this month. And that's a clear indication that Japan is not interested in bilateral trade deal that the US is keen on pursuing. Suga added that "Japan is not going to do anything with any country that harms the national interest." And, "with FTA negotiations too, we'll handle them in that way."

Finance Minister Taro Aso also said that "inward-looking policies would benefit no country." And added that "excessive current account imbalances should be resolved through multilateral, not bilateral, framework. " Also, "the matter should be dealt with through macroeconomic policy and a structural reform by rebalancing savings and investments, instead of imposing tariffs."

G20 pledged to strengthen contribution of trade to the economies

G20 finance ministers and central bankers stepped up their language regarding trade tension in the communique after the meeting in Argentina. The communique noted that "risks over the short and medium term have increased". And the risks include "financial vulnerabilities, heightened trade and geopolitical tensions, global imbalances, inequality and structurally weak growth, particularly in some advanced economies." The group pledged to "continue to monitor risks, take action to mitigate them and respond if they materialise."

The communique also noted that "international trade and investment are important engines of growth, productivity, innovation, job creation and development." The group reaffirmed the conclusions on trade at the Hamburg Summit and "recognise the need to step up dialogue and actions to mitigate risks and enhance confidence". And "we are working to strengthen the contribution of trade to our economies."

Below is the full communique.

Communiqué

G20 Finance Ministers and Central Bank Governors

July 23, 2018, Buenos Aires, Argentina

- Global economic growth remains robust and unemployment is at a decade low. However, growth has been less synchronised recently, and downside risks over the short and medium term have increased. These include rising financial vulnerabilities, heightened trade and geopolitical tensions, global imbalances, inequality and structurally weak growth, particularly in some advanced economies. We will continue to monitor risks, take action to mitigate them and respond if they materialise. Although many emerging market economies are now better prepared to adjust to changing external conditions, they still face challenges including market volatility and reversal of capital flows.

- We will continue using all policy tools to support strong, sustainable, balanced and inclusive growth. Monetary policy will continue to support economic activity and ensure price stability, consistent with central banks' mandates. Fiscal policy should be used flexibly and be growth-friendly, prioritise high quality investment, while enhancing economic and financial resilience and ensuring debt as a share of GDP is on a sustainable path. Continued implementation of structural reforms will enhance our growth potential. We reaffirm our exchange rate commitments made in March. We will clearly communicate our macroeconomic and structural policy action. International trade and investment are important engines of growth, productivity, innovation, job creation and development. We reaffirm our Leaders' conclusions on trade at the Hamburg Summit and recognise the need to step up dialogue and actions to mitigate risks and enhance confidence. We are working to strengthen the contribution of trade to our economies.

- As we embrace technological transformation, we will ensure its benefits are widely shared and address the challenges it creates for individuals, businesses, and governments. We endorse the Menu of Policy Options for the Future of Work (the Menu) which will help us to: harness technology to strengthen growth and productivity; support people during transitions and address distributional challenges; secure sustainable tax systems; and ensure that the best possible evidence informs our decision-making. The Menu also reinforces the importance of international cooperation and promoting gender equality. We will draw on the Menu to respond to the impacts of technological change, considering individual country circumstances.

- To further boost infrastructure investment, and support growth and development, we welcome progress on the Roadmap to Infrastructure as an Asset Class. We endorse the G20 Principles for the Infrastructure Project Preparation Phase which will help deliver a pipeline of well-prepared and bankable projects that are attractive to private investors by improving assessments of project rationale, options appraisal, commercial viability, long-term affordability, and deliverability. We look forward to key progress being achieved under the Roadmap in the areas of risk mitigation and credit enhancements, data availability, and contractual and financial standardisation by the end of 2018. The Private Sector Advisory Group will continue informing the work on the key challenges in attracting private investment to infrastructure. We agree to extend the mandate of the Global Infrastructure Hub to 2022. We call for coordination among current initiatives sponsored by MDBs and others to avoid duplication of efforts.

- Against the backdrop of recent volatility in financial markets and capital flows, we continue our work as agreed in March, including on monitoring cross-border capital flows and examining available tools to help countries harness their benefits while also managing risks.

- We reaffirm our commitment to further strengthening the global financial safety net with a strong, quota-based, and adequately resourced IMF at its centre. We are committed to concluding the 15th General Review of Quotas and agreeing on a new quota formula as a basis for a realignment of quota shares to result in increased shares for dynamic economies in line with their relative positions in the world economy and hence likely in the share of emerging market and developing countries as a whole, while protecting the voice and representation of the poorest members by the Spring Meetings and no later than the Annual Meetings of 2019.

- We continue to monitor debt vulnerabilities in Low Income Countries (LICs) with concern. Accurate and comprehensive debt data are essential in ensuring sound borrowing and lending practices. We welcome again the Operational Guidelines for Sustainable Financing and we agree that building capacity in public financial management, strengthening domestic policy frameworks, and enhancing information sharing would help avoid new episodes of debt distress in LICs. We support ongoing work by the IMF, WBG and Paris Club on LICs debt. We will work towards enhancing debt transparency and sustainability, and improving sustainable financing practices by debtors and creditors, both official and private.

- We are looking forward to the report by the G20 Eminent Persons Group on Global Financial Governance.

- The financial system must remain open, resilient and supportive of growth. We remain committed to the full, timely and consistent implementation and finalisation of the post-crisis reforms, and the evaluation of their effects. We welcome progress on the evaluations by the FSB and standard setting bodies (SSBs) of the effects of the reforms on infrastructure financing and incentives to centrally clear over-the-counter derivatives and we expect the final results by the Leaders' Summit. We look forward to the FSB's continued progress on achieving resilient market-based finance. We continue to monitor and, if necessary, address emerging risks and vulnerabilities in the financial system.

- Technological innovations, including those underlying crypto-assets, can deliver significant benefits to the financial system and the broader economy. Crypto-assets do, however, raise issues with respect to consumer and investor protection, market integrity, tax evasion, money laundering and terrorist financing. Crypto-assets lack the key attributes of sovereign currencies. While crypto- assets do not at this point pose a global financial stability risk, we remain vigilant. We welcome updates provided by the FSB and the SSBs and look forward to their further work to monitor the potential risks of crypto-assets, and to assess multilateral responses as needed. We reiterate our March commitments related to the implementation of the FATF standards and we ask the FATF to clarify in October 2018 how its standards apply to crypto-assets.

- We support a globally fair, sustainable, and modern international tax system. We reaffirm the importance of the worldwide implementation of the Base Erosion and Profit Shifting package. We remain committed to work together to seek a consensus-based solution to address the impacts of the digitalisation of the economy on the international tax system by 2020, with an update in 2019. We call on all jurisdictions to sign and ratify the multilateral Convention on Mutual Administrative Assistance in Tax Matters. Jurisdictions scheduled to commence automatic exchange of financial account information for tax purposes in 2018 should ensure that all necessary steps are taken to meet this timeline. We support the OECD strengthened criteria to identify jurisdictions that have not satisfactorily implemented the internationally agreed tax transparency standards. Defensive measures will be considered against listed jurisdictions. We support enhanced tax certainty and tax capacity building, including through the Global Knowledge-Sharing Platform for Tax Administration under the umbrella of the Platform for Collaboration on Tax, and welcome the Latin America Academy for Tax Crime Investigation in Buenos Aires.

- Mobilising sustainable finance and strengthening financial inclusion are important for global growth. We welcome the G20 Sustainable Finance Synthesis Report 2018 which presents voluntary options to support deployment of sustainable private capital. We endorse the G20 Financial Inclusion Policy Guide on Digitisation and Informality, which provides voluntary policy recommendations to facilitate digital financial services, taking into account country contexts. While significant progress has been made to lift financial inclusion through the Global Partnership for Financial Inclusion, we ask that it streamlines its work program and structure so it continues to support economic growth, financial stability and reducing inequality.

- Our fight against terrorist financing, money laundering and proliferation financing continues. We call for full, effective and swift implementation of FATF standards. We call on FATF to further enhance its efforts to counter proliferation financing. We commit to further our individual and collective efforts to eliminate the financial networks supporting terrorist groups.

Communiqué Annex

Issues for Further Action

We welcome the MDB Infrastructure Cooperation Platform, which will report to the Infrastructure Working Group, and ask that advice be provided to us by the 2018 Leaders' Summit on its activities to improve MDB project preparation, standardisation of guarantees and credit enhancement tools, and data availability. We call on the IWG to study the feasibility of new mechanisms to create portfolios of infrastructure assets, including brownfield infrastructure projects, that can be purchased by institutional investors.

We ask the OECD to report by the 2018 Leaders' Summit on the number of jurisditions that are at risk of being considered as not having satisfactorily implemented internationally agreed tax transparency standards. We also ask the OECD to prepare a list by the 2019 Leaders' Summit of the jurisdictions that have not yet sufficiently progressed toward a satisfactory level of implementation. We ask the OECD and the IMF to report to Finance Ministers and Central Bank Governors in 2019 on progress made on tax certainty.

We reiterate our call for the Platform for Collaboration on Tax to develop its workplan on its commitments by the IMF/WBG Annual Meetings this year and provide a progress report in 2019.

We look forward to the report by the FSB on policy development under its action plan to assess and address the decline in correspondent banking relationships by the 2018 Leaders' Summit. To ensure the GPFI continues to make a positive contribution to financial inclusion, we ask that it considers where its work could be rationalised and prioritised. We also ask the GPFI to consider its current structure with a view to more closely aligning it with other working arrangements in the G20 finance track. This includes combining the work of the four GPFI sub groups into one working group, appointment of working group co-chairs and changing its membership arrangements. We expect the the GPFI to provide a roadmap by the Leaders' Summit in December on the path to achieving the requested changes in 2020.

We look forward to the implementation of the outcomes of the April Paris Conference on Counter Terrorist Financing.

Reports and Documents Received

Global Economy

- G20 Surveillance Note, IMF

Future of Work

- G20 Menu of Policy Options for the Future of Work, FWG

- Future of Work: Measurement and Policy Challenges, IMF

- Tax Policies for Inclusive Growth in a Changing World, OECD

- Maintaining Competitive Conditions in the Era of Digitalisation, OECD

- Financing Social Protection and Lifelong Learning for the Future of Work: Fiscal Aspects and Policy Options, ILO

- Policy Options to Support Innovation in Developing Countries, WBG

Infrastructure

- G20 Principles for the Infrastructure Project Preparation Phase, G20, IWG 3

- G20/OECD/WB Stocktake of Tools and Instruments Related to Infrastructure as an Asset Class, Background Document, OECD and WBG

- G20/OECD Effective Approaches for Implementing the G20/OECD High-Level Principles on SME Financing, OECD

Financial Regulation

- Evaluation of the Effects of Reforms on Infrastructure Finance Consultative Document, FSB

- Evaluation of Incentives to Centrally Clear OTC Derivatives Draft Executive Summary of Consultative Document, FSB

- Cyber Lexicon Consultative Document, FSB

- Crypto-Assets Report on Work by the FSB and Standard-Setting Bodies, FSB

International Financial Architecture

- IMF Institutional View in Practice, IMF

- The OECD Code of Liberalisation of Capital Movements: Update on Developments, OECD

- Joint Note on Strengthening Public Debt Transparency — the Role of the IMF and the World Bank, IMF and WBG

- Joint Note on Improving Public Debt Recording, Monitoring and Reporting Capacity in Low and Lower Middle-Income Countries, IMF and WBG

- Joint Note Updating on the Implementation of the G20 Principles for Effective Coordination between the IMF and MDBs, IMF, WBG, IADB

International Taxation

- Secretary-General Report to Finance Ministers, OECD, Buenos Aires, Argentina, July 2018

Anti-Money Laundering and Terrorist Financing

- Report to Finance Ministers and Central Bank Governors, FATF, July 2018

Financial Inclusion

- G20 Policy Guide. Digitisation and Informality: Harnessing Digital Financial Inclusion for Individuals and MSMEs in the Informal Economy, GPFI

- G20 Digital Identity Onboarding, WBG

- Achieving Development and Acceptance of an Open and Inclusive Digital Payments Infrastructure, BTCA

- Use of Alternative Data to Enhance Credit Reporting to Enable Access to Digital Financial Services by Individuals and SMEs operating in the Informal Economy, ICCR

- Data Protection and Privacy for Alternative Data, WBG

- G20/OECD Policy Guidance — Financial Consumer Protection Approaches in the Digital Age, OECD

- G20/OECD INFE Policy Guidance — Digitalisation and Financial Literacy, OECD

Sustainable Finance

- G20 Sustainable Finance Synthesis Report — 2018, Sustainable Finance Study Group