Sample Category Title

Japan logged JPY 721.4B surplus in June, exports grew 19th straight month

Japan trade balanced turned back into surplus at JPY 721.4B in June, above expectation of JPY 534.2B. Total exports rose 6.7% yoy, slightly below expectation of 7.0% yoy. But imports rose just 2.5% yoy, below expectation of 5.3% yoy.

Total exports logged a 19th straight month of growth. Rising trade tension with the US is not having much realized impact so far. Exports to China rose 11.1% yoy, to EU rose 9.3% yoy. Meanwhile, exports to US dropped -0.9% yoy.

Japan is still facing impacts from US steel and aluminum tariffs and threats on auto tariffs. The the blockbuster trade deal with EU just signed earlier this week should provide enough optimism to offset those threats.

Market Morning Briefing: Dollar Yen Might Be Facing Some Resistance Near 113

STOCKS

Dow (25199.29, +0.32%) has almost moved up to test immediate resistance at 25250. Dow looks bullish just now with 4-sessions of upmove. If the index manages to break above 25250, it could continue to rally towards 25600 in the medium term.

Dax (12765.94, +0.82%) is also moving up and could target 13000 in the coming sessions. Note that 13000 is an important resistance and may hold in the medium term pushing the index back towards 12400-12200 levels.

Nikkei (22870.47, +0.33%) did not further rise after breaking above 22800 but is stable in the past 2-sessions. There is enough scope on the upside while above 22800 and the index may soon move up towards 23000-23200 in the near term. View remains bullish above 22800.

Shanghai (2791.21, +0.14%) seems to be stuck in the 2850-2750 region and has been trading narrow in the last few sessions. A re-test if 2750 seems likely before rising back to 2850. Some sessions of sideways trade also looks possible just now.

Nifty (10980.45, -0.25%) has immediate support near 10950 (risen from earlier 10900-10850 levels). While 10950 holds, Nifty may see an immediate bounce back from current levels towards 11100-11200 in the next few sessions. A break below 10950, if seen would make it vulnerable to a fall towards 10850-10800 again in the medium term. Watch price action near 10950.

COMMODITIES

Nymex WTI (68.81) has risen from 67 and while the price trades higher, it could attempt a test of 72 on the upside. A fall from levels near 70, if seen could open up chances of further fall towards 66-65 in the medium term. For now while above 67, price is likely to move up.

Brent (72.83, -0.10%) has also held immediate support near 71. Lower support is visible at 69-70 region. We would be cautious to see if Brent moves up immediately towards 75+ levels or comes back to test 70-69 before resuming uptrend in the longer run.

Gold (1224.40, -0.29%) does not look as if it may pause near current levels. While the bears looks string, there could be chances of a fall towards 1200 in the medium term before the price could see a corrective rise. Near to medium term looks bearish.

Copper (2.7585, -0.0505%) is trading in a sideways narrow range of 2.80-2.70 and could continue this week. While 2.70 holds as decent support, Copper could eventually move up in the longer run.

FOREX

Euro (1.1644): In line with our expectation, Euro almost tested the support on 3 day candles by seeing a low of 1.1602. The support has held and the Euro might now try to move up towards 1.1715, which is a crucial resistance. A break above 1.1715 could suggest that a medium term bottom is in place, suggesting a rise to 1.18+. Failure to break above 1.1715 by middle of next week can create chances of fall towards 1.15 and lower.

Dollar Index (95.08): Dollar Index tested resistance (earlier support) on daily candles near 95.41 yesterday and has then dipped from there. It could now move lower towards the 21 days MA (94.67) which would also correspond well with a rise in the Euro towards 1.1715.

Dollar Yen (112.74): Dollar Yen might be facing some resistance near 113. We currently prefer further bullishness towards 114 (resistance on 3 day line chart) which might be tested in the next week. A break below 112.2-112.3 could however be bearish and the upside target of 114 would have to be re-examined.

Euro Yen (131.29): Euro Yen is continuing to respect the 55 weeks MA near 131.58. Dollar Yen’s pause below 113 is delaying the break of 131.58 by Euro Yen. A rise towards 1.17 on the Euro could however help Euro Yen rise above 131.58 in the early part of next week.

Pound (1.3071): Pound saw a low near 1.3010 yesterday and might be on course to break crucial horizontal support near 1.305 on weekly candles. A downmove to 1.295-1.290 in the next week is possible. This break is likely to make Pound bearish in the weeks ahead.

Dollar Rupee (68.615): Dollar Rupee moved up to close at higher levels yesterday. Further Rupee weakness beyond 68.70 is not envisaged just now but could be triggered if Yuan moves beyond 6.74 and Dollar Index breaks above 95.5 (less preferred).

INTEREST RATES

US yields have risen after a series of events which have reaffirmed the growing inflationary pressures in the US economy and the Fed’s inclination to hike rates at regular intervals. At first, US Retail Sales rose decently; then, the Fed Chairman appeared optimistic about US growth and inflation in front of different US government committees; after that, the Fed’s Beige book also highlighted the tightening labour market.

Consequently the US 10 year yield has risen to 2.89%. It could get some resistance near 2.9% now. If it breaches 2.9%, then it could attempt a test of 2.95% as well. We would have to revisit our view of a dip towards 2.7% in the next couple of months if the 10 year yield does manage to break above 2.9%.

US 10 year yield (2.89%), 30 Year (3.00%), 5 Year (2.78%), 2 Year (2.62%)

The German 10 year yield (0.34%) could see a rise towards resistance near 0.4% on short term chart in the next 2-3 sessions.

Australian Dollar jumps as employment data strong on all front

Australian Dollar surges broadly as June employment data came in strong on all front.

Headline job grow jumped to 50.9k seasonally adjusted , well above expectation of 16.6k. Prior month's figure was also revised slightly up by 12k to 13.5k. Full time jobs grew 41.2k while part time jobs also rose 9.7k. Together with the surge in full time jobs, total hours worked rose 0.6%

Unemployment rate remained unchanged at 5.4%. But without rounding, it's actually the at its lowest since November 2012. Labor force participation rate rose 0.2% to 65.7%. Employment to population ratio also rose 0.2% to 62.1%.

Also from Australia, NAB Quarterly Business Confidence dropped to 7 in Q2.

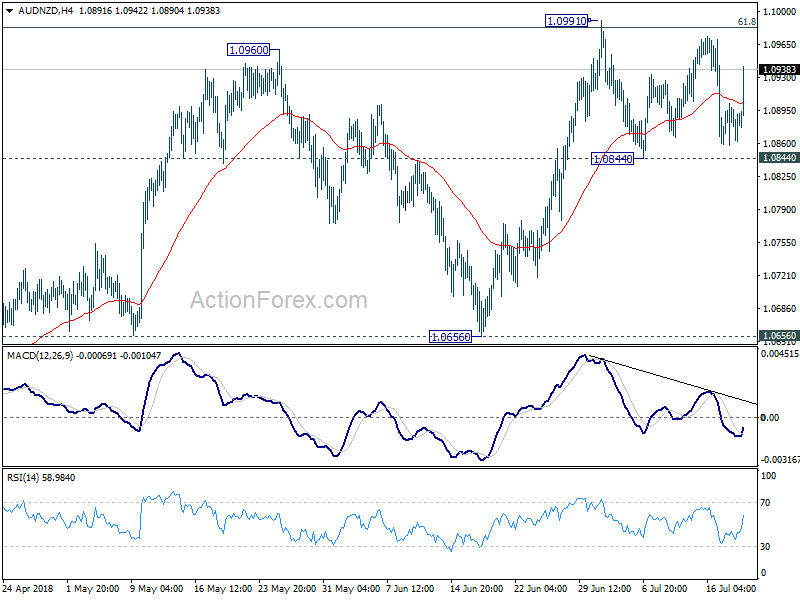

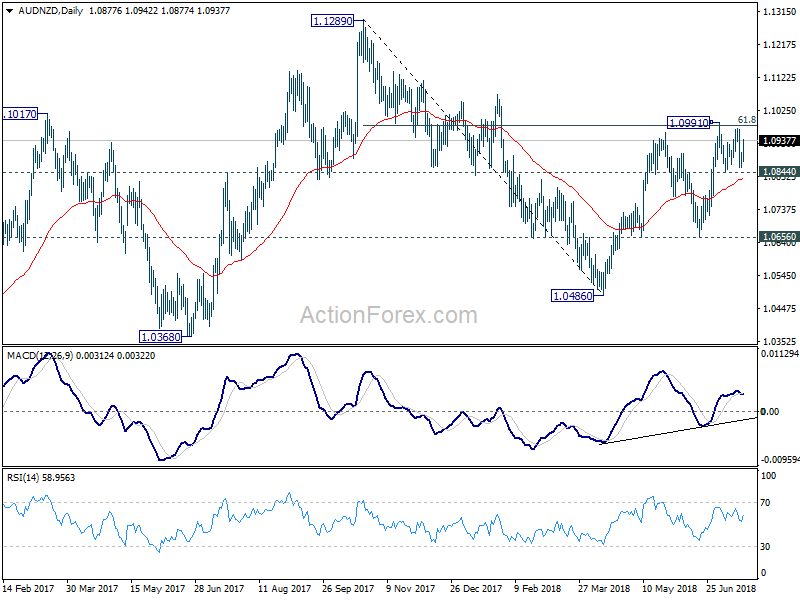

AUD/NZD rebounded ahead of 1.0844 support and retained near term bullishness in the cross. Price actions from 1.0991 short term top now look more like a consolidation pattern. Focus is back on 61.8% retracement of 1.1289 to 1.0486 at 1.0982. Firm break there will resume the whole rise from 1.0486.

Fed: Beige Book Shows Rising Wage and Price Pressures, and Increasing Tariff Worries

Today's Beige Book showed 10 of 12 districts reporting moderate or modest growth over the late May to early July period. As was the case in the last report, Dallas remained an outlier, with strong growth driven in part by the energy sector. Now, however, activity in the St Louis district is described as slight.

New in the July Beige Book were concrete impacts from import tariffs, described as follows: "Manufacturers in all Districts expressed concern about tariffs and in many Districts reported higher prices and supply disruptions that they attributed to the new trade policies".

Reports of higher input costs and shrinking margins were also featured. Trucking capacity was a specific issue in six districts and attributed it to a shortage of commercial drivers.

Price increases were characterized as modest to moderate on average, but upticks occurred in several districts. Key input prices rose further including fuel construction materials, freight, and metals. Tariffs contributed to the increases for metals and lumber. However, the extent of pass-through from input to consumer prices remained slight to moderate. Pricing pressures are expected to intensify further in some Districts, while in others the outlook is for stable price increases at a modest to moderate pace.

The assessment of wage increases was upgraded slightly from modest in the last Beige book, to "modest to moderate" in the July report, with a couple of districts cited a pickup in the pace of wages (likely Philadelphia and Minneapolis). Some districts cite that labor shortages are constraining growth.

Several Districts reported slow growth in existing home sales, but were not overly concerned about rising rates.

Key Implications

The assessment of overall economic activity in the July Beige Book remained broadly unchanged, but wage and price pressures appear to have increased. This suggests an economy at the mature stage of the economic cycle, with several pockets running up against capacity constraints. At the same time, concerns about import tariffs have become more widespread, and the impacts more concrete, with higher prices and supply disruptions reported.

Market reaction to this release will likely be limited, given markets had already heard from Fed Chair Powell in his two days of testimony before Congress. In an otherwise upbeat assessment of the U.S. economic outlook, he addressed the risks from protectionism, but noted that impacts are highly uncertain. Powell is also leaving the door open to the possibility that over time, the administration's tough-love strategy on tariffs could result in more open trade with the U.S.'s partners and therefore benefit economic activity.

Overall, today's report is consistent with continued rate hikes by the FOMC, with the next likely to come at the end of September. Rising trade protectionism is a clear downside risk that the Fed is no doubt watching closely, but for now, the risk is not strong enough to forestall further hikes.

EUR/JPY Likely Formed Short-Term Top

Key Highlights

- The Euro found a strong selling interest near 132.00 and declined against the Japanese Yen.

- There was a break below a major bullish trend line with support at 131.80 on the 4-hours chart of EUR/JPY.

- The Euro Zone CPI increased 0.1% in June 2018 (MoM), less than the last +0.5%.

- Today in the UK, the Retail Sales figure for June 2018 will be released, which is forecasted to rise 0.4% (MoM).

EURJPY Technical Analysis

The Euro was in a significant uptrend this past week with a break above 130.00 against the Japanese Yen. The EUR/JPY pair climbed towards 132.00, which acted as a strong resistance.

Looking at the 4-hours chart, the pair formed a short-term top at 131.98 and started a downward move. It broke the 23.6% Fib retracement level of the last wave from the 129.90 low to 131.98 high.

More importantly, there was a break below a major bullish trend line with support at 131.80 on the same chart. The current price action suggests that there could be more declines in EUR/JPY below the 131.00 level.

The next major support is near the 61.8% Fib retracement level of the last wave from the 129.90 low to 131.98 high at 1.3070. On the upside, the previous support at 131.50 and 131.80 are likely to act as hurdles. Above these, the pair has to move above 132.00 to start a fresh rally.

Recently in the Euro Zone, the CPI report for June 2018 was released by Eurostat. The market was looking for a rise of 0.1% in the CPI compared with the previous month.

The result was in line with the forecast, but it was much lower than the last increase of 0.5%. Moreover, the Core CPI remained flat in June 2018, whereas the market was looking for a rise of 0.1%.

The report added:

In June 2018, the highest contribution to the annual euro area inflation rate came from energy (+0.76 percentage points, pp), followed by services (+0.57 pp), food, alcohol & tobacco (+0.53 pp) and non-energy industrial goods (+0.10 pp).

Overall, the Euro may continue to face selling interest in the near term against the US Dollar and Japanese Yen.

Economic Releases to Watch Today

- US Initial Jobless Claims – Forecast 220K, versus 214K previous.

- UK Retail Sales for June 2018 (YoY) – Forecast +3.9%, versus +3.9% previous.

- UK Retail Sales for June 2018 (MoM) – Forecast +0.3%, versus +1.4% previous.

- UK Retail Sales ex-fuel for June 2018 (YoY) – Forecast +3.7% versus +4.4% previous.

- UK Retail Sales ex-fuel or June 2018 (MoM) – Forecast +0.3% versus +1.3% previous.

Eco Data 7/19/18

[php_everywhere instance="1"]

Upbeat Powell Sends Gold to 16-Month Low

Gold has steadied in the Wednesday session after posting sharp losses on Tuesday. In North American trade, the spot price for one ounce of gold is $1226.78, down 0.08% on the day. On the release front, U.S housing numbers were softer than expected. Building Permits dropped to 1.27 million, shy of the estimate of 1.33 million. Housing Starts fell sharply to 1.17 million, down from 1.35 million. This was well below the estimate of 1.32 million. Federal Reserve Chair Jerome Powell is testifying before the House Financial Services Committee. On Thursday, the U.S releases Philly Fed Manufacturing Index and unemployment claims.

With the U.S economy performing well, there was no surprise that Fed Chair Jerome Powell sounded bullish on the U.S economy during testimony before the Senate Banking Committee on Tuesday. Powell said that he expected the labor market to remain tight and inflation to stay close to the Fed’s target of 2 percent for the next several years. Powell added that the Fed would continue to gradually raise interest rates. Lawmakers appeared satisfied with current monetary policy, but Powell did face some pointed questions regarding the escalating trade war, which has raised concerns that economy could take a downturn if the tariff battles continue. Still, consumer spending remains strong, the labor market is close to full capacity and inflation continues to move close to the Fed target of 2.0 percent. The Fed is widely expected to raise interest rates twice in the second half of the year, starting with a hike in September.

British Pound Slips to 10-Month Low as CPI Misses Mark

The British pound continues to lose ground and has dropped perilously close to the symbolic 1.30 line. In Wednesday’s North American session, the pair is trading at 1.3044, down 0.53% on the day. On the release front, British CPI remained steady at 2.4%, missing the estimate of 2.6%. U.S housing numbers were softer than expected. Building Permits dropped to 1.27 million, shy of the estimate of 1.33 million. Housing Starts fell sharply to 1.17 million, down from 1.35 million. This was well below the estimate of 1.32 million. Later in the day, Federal Reserve Chair Jerome Powell testifies before the House Financial Services Committee. On Thursday, there are key releases on both sides of the border. The UK releases Retail Sales, with the markets braced for a paltry gain of 0.1%. The U.S will publish the Philly Fed Manufacturing Index and unemployment claims.

It’s been a rough week for the pound, which has declined 1.4 percent. Employment data was weaker than expected on Tuesday, and this was followed by a soft CPI on Wednesday. The weak numbers have dampened expectations that the BoE will raise interest rates at its August meeting. With the May government continuing to squabble over Brexit and negotiations with the EU at a standstill, the pound could face further headwinds.

Things are looking rosy for the U.S economy. Consumer spending is strong, the labor market is close to full capacity and inflation continues to move close to the Fed target of 2.0 percent. With this kind of performance, there was no surprise that Fed Chair Jerome Powell sounded bullish on the U.S economy during testimony before the Senate Banking Committee. Powell said that he expected the labor market to remain tight and inflation to stay close to the Fed’s target of 2 percent for the next several years. Powell added that the Fed would continue to gradually raise interest rates. Lawmakers appeared satisfied with current monetary policy, but Powell did face some pointed questions regarding the escalating trade war, which has raised concerns that economy could take a downturn if the tariff battles continue.

US Ross said it will conduct section 232 national security probe on uranium imports

US Commerce Secretary Wilbur Ross indicates today that the country is heading towards more trade protectionism. Another Section 232 national security probe was triggered, as prompted by two U.S. uranium mining companies, Ur-Energy Inc and Energy Fuels Inc. Both companies complained that subsidized foreign competitors have caused them to cut capacity and lay off workers.

Ross said that "the Department of Commerce's Bureau of Industry and Security will conduct a thorough, fair, and transparent review to determine whether uranium imports threaten to impair national security."

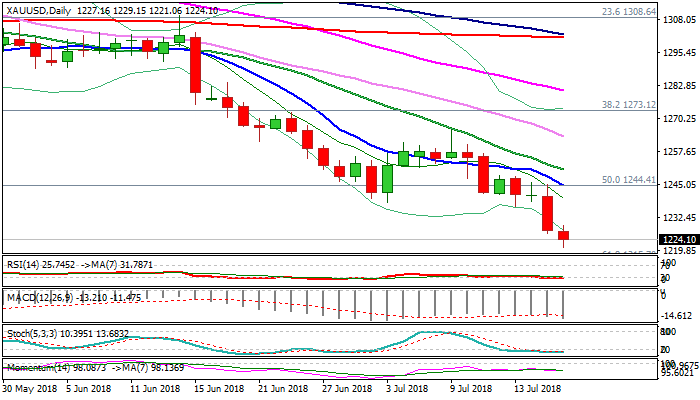

SPOT GOLD – Consolidation May Precede Bearish Continuation Towards $1215/00 Targets

Spot Gold fell to new one-year low at $1221 on Wednesday, in extension of previous day’s strong bearish acceleration after hawkish Fed boosted dollar.

Bears generated fresh signals on break below $1236 (Former trough of 12 Dec) and $1234 (weekly 200SMA) for test of next pivotal support at $1215 (Fibo 61.8% of $1122/$1366 uptrend).

Oversold daily studies warn of corrective action in coming sessions, but so far without firmer signal.

Falling 10SMA ($1244) should limit upticks to keep broader bears intact.

Res: 1229; 1237; 1244; 1252

Sup: 1221; 1215; 1204; 1200